Comprehensive Financial Analysis Report: Medical Australia Limited

VerifiedAdded on 2020/03/16

|13

|3090

|30

Report

AI Summary

This report provides a comprehensive financial analysis of Medical Australia Limited, focusing on debt valuation, share valuation, cost of capital, and market analysis. The analysis includes an examination of short-term and long-term debts, the company's debt structure, and the proportion of short-term to long-term debts. Share valuation is assessed using the Earnings Price Ratio approach, considering revenue, earnings, and EPS trends. The report calculates the Weighted Average Cost of Capital (WACC) and explores the optimal capital structure for the company. A market analysis is also conducted, evaluating the company's financial performance and market risk, including its beta value. The report concludes that the company has a low beta, making it a good bet during downturns.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Medical Australia Limited

Executive summary

An analysis of the company can be done with the aid of various factors such as ratio analysis,

debt valuation, share valuation, cost of capital, market analysis, etc. In this report, the major

emphasis is on the financial strategy of the company. The selected company for the report is

Medical Australia Limited. The report sheds light on the various components of debt, ratio,

market evaluation and the financial management of the company is revealed in an appropriate

manner. The overall analysis indicates that the company has low beta and hence, is a good bet

when it comes to downturn.

2

Executive summary

An analysis of the company can be done with the aid of various factors such as ratio analysis,

debt valuation, share valuation, cost of capital, market analysis, etc. In this report, the major

emphasis is on the financial strategy of the company. The selected company for the report is

Medical Australia Limited. The report sheds light on the various components of debt, ratio,

market evaluation and the financial management of the company is revealed in an appropriate

manner. The overall analysis indicates that the company has low beta and hence, is a good bet

when it comes to downturn.

2

Medical Australia Limited

Contents

I. Debt Valuation.....................................................................................................................................4

i. Short-term and long-term debts..........................................................................................................4

ii. Debt structure.....................................................................................................................................4

iii. Proportion of short-term to long-term debts......................................................................................4

II. Share Valuation...................................................................................................................................5

i. Calculation of Cost of Equity:.............................................................................................................5

ii. Revenue, earning, EPS........................................................................................................................5

iii. P/E Approach...................................................................................................................................6

iv. Most reasonable...............................................................................................................................7

v. Valuation of the company stocks.........................................................................................................7

III. Cost of Capital.................................................................................................................................8

i. Calculation of WACC.........................................................................................................................8

ii. Company’s tax rate..............................................................................................................................8

iii. Difference in the cost of debt and the cost of equity........................................................................8

iv. Pros and cons of including current liabilities in the cost of capital calculation................................8

v. Major value of the WACC calculation................................................................................................9

vii. Capital structure...............................................................................................................................9

viii. Optimal capital structure..................................................................................................................9

IV. Market Analysis.............................................................................................................................10

i. Financial performance.......................................................................................................................10

ii. Overview of the company..................................................................................................................11

iii. Other discussion............................................................................................................................11

Reference:.................................................................................................................................................12

Appendix...................................................................................................................................................13

3

Contents

I. Debt Valuation.....................................................................................................................................4

i. Short-term and long-term debts..........................................................................................................4

ii. Debt structure.....................................................................................................................................4

iii. Proportion of short-term to long-term debts......................................................................................4

II. Share Valuation...................................................................................................................................5

i. Calculation of Cost of Equity:.............................................................................................................5

ii. Revenue, earning, EPS........................................................................................................................5

iii. P/E Approach...................................................................................................................................6

iv. Most reasonable...............................................................................................................................7

v. Valuation of the company stocks.........................................................................................................7

III. Cost of Capital.................................................................................................................................8

i. Calculation of WACC.........................................................................................................................8

ii. Company’s tax rate..............................................................................................................................8

iii. Difference in the cost of debt and the cost of equity........................................................................8

iv. Pros and cons of including current liabilities in the cost of capital calculation................................8

v. Major value of the WACC calculation................................................................................................9

vii. Capital structure...............................................................................................................................9

viii. Optimal capital structure..................................................................................................................9

IV. Market Analysis.............................................................................................................................10

i. Financial performance.......................................................................................................................10

ii. Overview of the company..................................................................................................................11

iii. Other discussion............................................................................................................................11

Reference:.................................................................................................................................................12

Appendix...................................................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Medical Australia Limited

I. Debt Valuation

i. Short-term and long-term debts

The long-term debts are those that are due for a period exceeding 12 months. In the case

of Medical Australia Limited, the long-term debt comprises of trade creditors and

payables. The non-current liabilities are the obligations and for the company, it is the

long-term debt as they are not due in the present course of time.

a. On the other hand, the short-term debt comprises of the debts that are due in a

short course of time that is within a span of 12 months. The current liabilities of

the company such as trade creditors, income in advance, payroll liabilities,

accruals, etc are the short-term debts.

ii. Debt structure

The debt structure of the company can be commented with the help of debt-equity ratio.

As per standard industrial norms, the debt-equity ratio should not exceed 1. This means

that a higher reliance on the debt will affect the performance of the company as more

interest payment will be required.

b. As per the computation of the ratio, it can be seen that the debt-equity of the

company stands below 0.50 that means it is in synchronization with the industrial

standards as the company does not contain a major reliance on debt.

iii. Proportion of short-term to long-term debts

When it comes to the short-term debts it can be said that the company has utilized more

of short-term debts. This implies the company operates with a motto of better operation

in the short-term. Such debts are due for payment in a span of 12 months and hence, the

company does not have the obligation of the longer term. On the contrary, the long-term

debt comprises of the trade payable and provisions that decreased in comparison to the

4

I. Debt Valuation

i. Short-term and long-term debts

The long-term debts are those that are due for a period exceeding 12 months. In the case

of Medical Australia Limited, the long-term debt comprises of trade creditors and

payables. The non-current liabilities are the obligations and for the company, it is the

long-term debt as they are not due in the present course of time.

a. On the other hand, the short-term debt comprises of the debts that are due in a

short course of time that is within a span of 12 months. The current liabilities of

the company such as trade creditors, income in advance, payroll liabilities,

accruals, etc are the short-term debts.

ii. Debt structure

The debt structure of the company can be commented with the help of debt-equity ratio.

As per standard industrial norms, the debt-equity ratio should not exceed 1. This means

that a higher reliance on the debt will affect the performance of the company as more

interest payment will be required.

b. As per the computation of the ratio, it can be seen that the debt-equity of the

company stands below 0.50 that means it is in synchronization with the industrial

standards as the company does not contain a major reliance on debt.

iii. Proportion of short-term to long-term debts

When it comes to the short-term debts it can be said that the company has utilized more

of short-term debts. This implies the company operates with a motto of better operation

in the short-term. Such debts are due for payment in a span of 12 months and hence, the

company does not have the obligation of the longer term. On the contrary, the long-term

debt comprises of the trade payable and provisions that decreased in comparison to the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Medical Australia Limited

year 2015. This reflects that the company has more involvement in terms of current

liabilities in contrast to the long-term liabilities (Medical Australia Limited, 2016).

iv. No long-term debt

II. Share Valuation

i. Calculation of Cost of Equity:

As other details are not available, we shall calculate Cost of Equity using Earnings Price Ratio

Approach an under:

Cost of Equity = Current EPS * (1+ growth rate)/ Current Market Price per share

= 0.30 cents (1+ 0%) / 0.50 cents

= 60 %

Growth rate of EPS is negative, hence taken at zero.

ii. Revenue, earning, EPS

The revenue of the company has been showing increasing trends since past years. This can be

seen from the revenue figures in the financial statements of the company. With regard to the

changes in revenue earnings, EPS, dividends and growth expectations, following facts can be

considered:

i. Revenue - the revenue for the year ending 30th June 2016 have shown an impressive

growth as compared to the revenue earnings for the year ending 30th June 2015. The

revenue for the year ending 30th June 2016 was $ 12,419,938 as compared to $

11,510,774 for the year ending 30th June 2015. The growth in revenue earnings has

been approximately 8% (Medical Australia Limited, 2016).

ii. Earning- There was no foreign exchange gain in the year ending June 2016. Also, the

expenses for the year 2016 have increased as compared to the year 2015 which has

reduced the net profits by more than 70 %. The major reason behind the decrease in

profits is due to increase in employee benefits and increase in the cost of goods sold.

5

year 2015. This reflects that the company has more involvement in terms of current

liabilities in contrast to the long-term liabilities (Medical Australia Limited, 2016).

iv. No long-term debt

II. Share Valuation

i. Calculation of Cost of Equity:

As other details are not available, we shall calculate Cost of Equity using Earnings Price Ratio

Approach an under:

Cost of Equity = Current EPS * (1+ growth rate)/ Current Market Price per share

= 0.30 cents (1+ 0%) / 0.50 cents

= 60 %

Growth rate of EPS is negative, hence taken at zero.

ii. Revenue, earning, EPS

The revenue of the company has been showing increasing trends since past years. This can be

seen from the revenue figures in the financial statements of the company. With regard to the

changes in revenue earnings, EPS, dividends and growth expectations, following facts can be

considered:

i. Revenue - the revenue for the year ending 30th June 2016 have shown an impressive

growth as compared to the revenue earnings for the year ending 30th June 2015. The

revenue for the year ending 30th June 2016 was $ 12,419,938 as compared to $

11,510,774 for the year ending 30th June 2015. The growth in revenue earnings has

been approximately 8% (Medical Australia Limited, 2016).

ii. Earning- There was no foreign exchange gain in the year ending June 2016. Also, the

expenses for the year 2016 have increased as compared to the year 2015 which has

reduced the net profits by more than 70 %. The major reason behind the decrease in

profits is due to increase in employee benefits and increase in the cost of goods sold.

5

Medical Australia Limited

Despite the fact, the sale has increased by 8%, but the cost of goods sold has

increased by more than 20%. So all of this has reduced the profits or PBIT to $

3,85,251 (Medical Australia Limited, 2016).

iii. EPS has gone down drastically in the year 2016 as compared to the year 2015

because EPS in the year 2016 was (3.24)cents which shows that there has been an

overall loss in the business. One of the positive signs are EPS calculated as per the

continuing business which stands at 0.30 cents. Although this has also reduced around

70% from the year 2015 where the EPS was 1.04 cents per share.

iv. Dividends- Dividend have not been declared during the year, hence no comments can

be added for the same.

v. Growth expectations- the business is expected to grow at a minimum of 8% as per the

growth trends of the business. However, there has to be a check on two things

mainly- the cost of goods sold and employee benefits (Parrino et. al, 2012).

iii. P/E Approach

P/E ratio depicts the price which an investor can pay to invest in a company for earning the

P/E Ratio = Market Price per Share/ Earnings per Share

Market Value per share as on 30th June 2016 was 0.05 AUD

Earnings per share as on 30th June 2016 was 0.03 AUD or 0.30 cents (Medical Australia Limited,

2016)

Hence, P/E Ratio = 0.05/ 0.03 = 1.667 times

Constant dividend Growth rate model cannot be calculated here as the company has not declared

any dividend during the year (Parrino et. al, 2012).

There are various factors that influence a company’s stock price such as:

Mergers & acquisitions

6

Despite the fact, the sale has increased by 8%, but the cost of goods sold has

increased by more than 20%. So all of this has reduced the profits or PBIT to $

3,85,251 (Medical Australia Limited, 2016).

iii. EPS has gone down drastically in the year 2016 as compared to the year 2015

because EPS in the year 2016 was (3.24)cents which shows that there has been an

overall loss in the business. One of the positive signs are EPS calculated as per the

continuing business which stands at 0.30 cents. Although this has also reduced around

70% from the year 2015 where the EPS was 1.04 cents per share.

iv. Dividends- Dividend have not been declared during the year, hence no comments can

be added for the same.

v. Growth expectations- the business is expected to grow at a minimum of 8% as per the

growth trends of the business. However, there has to be a check on two things

mainly- the cost of goods sold and employee benefits (Parrino et. al, 2012).

iii. P/E Approach

P/E ratio depicts the price which an investor can pay to invest in a company for earning the

P/E Ratio = Market Price per Share/ Earnings per Share

Market Value per share as on 30th June 2016 was 0.05 AUD

Earnings per share as on 30th June 2016 was 0.03 AUD or 0.30 cents (Medical Australia Limited,

2016)

Hence, P/E Ratio = 0.05/ 0.03 = 1.667 times

Constant dividend Growth rate model cannot be calculated here as the company has not declared

any dividend during the year (Parrino et. al, 2012).

There are various factors that influence a company’s stock price such as:

Mergers & acquisitions

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Medical Australia Limited

Change in demand for the products

Reviews and rumors about the company

Political changes

There are varied reasons for changes in share price. In the P/E Approach model, the reason for

the change in share price may be due to the decrease in profits and earnings per share of the

company due to which the market prices of the shares may go down. If we talk about the

dividend growth model, the share price can be affected in future due to no declaration or low

declaration of dividends to the shareholders (Scapens, 2012).

iv. Most reasonable

The earnings per share as shown in P/E Ratio Approach is the most reasonable value as

compared to the market price per share. EPS is 0.30 cents and MPS is 0.50 cents which are quite

comparable with each other (Medical Australia Limited, 2016).

v. Valuation of the company stocks

Other information that can be used to value the company’s stocks may be –

Dividends(if declared)- dividends are used in the valuation of shares by using models like

dividend growth mode, etc hence it is an important information to know if the market prices are

to be calculated (Subramanyam & Wild, 2014).

Financial ratios- such as N.P Ratio, Earning per share, etc. can be compared with other similar

company to find out the market valuation.

Other factors such as discounted cash flows, P/E Ratio, etc. also help in finding out the market

valuation and hence are important information to be preferred.

7

Change in demand for the products

Reviews and rumors about the company

Political changes

There are varied reasons for changes in share price. In the P/E Approach model, the reason for

the change in share price may be due to the decrease in profits and earnings per share of the

company due to which the market prices of the shares may go down. If we talk about the

dividend growth model, the share price can be affected in future due to no declaration or low

declaration of dividends to the shareholders (Scapens, 2012).

iv. Most reasonable

The earnings per share as shown in P/E Ratio Approach is the most reasonable value as

compared to the market price per share. EPS is 0.30 cents and MPS is 0.50 cents which are quite

comparable with each other (Medical Australia Limited, 2016).

v. Valuation of the company stocks

Other information that can be used to value the company’s stocks may be –

Dividends(if declared)- dividends are used in the valuation of shares by using models like

dividend growth mode, etc hence it is an important information to know if the market prices are

to be calculated (Subramanyam & Wild, 2014).

Financial ratios- such as N.P Ratio, Earning per share, etc. can be compared with other similar

company to find out the market valuation.

Other factors such as discounted cash flows, P/E Ratio, etc. also help in finding out the market

valuation and hence are important information to be preferred.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Medical Australia Limited

III. Cost of Capital

i. Calculation of WACC

As there are no preference shares, debentures or retained earnings in the company, hence Cost of

Capital is equal to the cost of equity only.

Hence WACC = 60%

Cost of Equity Capital has been calculated using Earnings Price Ratio, where it comes to 60%.

ii. Company’s tax rate

In the calculation of WACC, the tax rate has to be used where there are debentures and

preference shares in the company for calculating the cost of debt and cost of preference shares.

In the given case, the whole capital structure consists of Equity shares only hence there is no use

of tax rate here (Porter & Norton, 2014).

iii. Difference in the cost of debt and the cost of equity

There is no debt in the company in its capital structure. Hence the cost of debt could not be

found out. In general, the difference is due to the difference in interest rate and taxes involved.

The cost of equity is generally calculated using dividend growth or CAPM or Earning Price

Ratio, etc whereas the cost of debt is calculated using interest rate and tax rate (Peirson et. al,

2015).

iv. Pros and cons of including current liabilities in the cost of capital calculation

No, the current liabilities should not be included in the cost of capital calculation. In the given

case there is only equity capital in the capital structure. These are short-term liabilities and not

long-term debts & occur due to trading activities of the business which may be repaid anytime by

8

III. Cost of Capital

i. Calculation of WACC

As there are no preference shares, debentures or retained earnings in the company, hence Cost of

Capital is equal to the cost of equity only.

Hence WACC = 60%

Cost of Equity Capital has been calculated using Earnings Price Ratio, where it comes to 60%.

ii. Company’s tax rate

In the calculation of WACC, the tax rate has to be used where there are debentures and

preference shares in the company for calculating the cost of debt and cost of preference shares.

In the given case, the whole capital structure consists of Equity shares only hence there is no use

of tax rate here (Porter & Norton, 2014).

iii. Difference in the cost of debt and the cost of equity

There is no debt in the company in its capital structure. Hence the cost of debt could not be

found out. In general, the difference is due to the difference in interest rate and taxes involved.

The cost of equity is generally calculated using dividend growth or CAPM or Earning Price

Ratio, etc whereas the cost of debt is calculated using interest rate and tax rate (Peirson et. al,

2015).

iv. Pros and cons of including current liabilities in the cost of capital calculation

No, the current liabilities should not be included in the cost of capital calculation. In the given

case there is only equity capital in the capital structure. These are short-term liabilities and not

long-term debts & occur due to trading activities of the business which may be repaid anytime by

8

Medical Australia Limited

selling off the stock or repayment received by the debtors (Porter & Norton, 2014). However,

payments to equity shareholders, debenture holders or preference shareholders can only be made

by selling off a substantial business or shares which may also bring the business to an end or end

of a business segment. So current liabilities are short-term which does not affect the cost of

equity (Shah, 2013).

v. Major value of the WACC calculation

The cost of equity is the major part in the calculation of WACC. As the cost of capital is quite

high, the company needs to invest its fund keeping in mind the high cost, so that the company is

able to recover its cost of capital and other expenses which should be ideally more than the cost

of equity.

vi. Information unavailable

vii. Capital structure

The capital structure of the company consists of only equity share capital. The cost of capital of

the company is very high. So, the company should choose other options also in line with the

industry and should include debentures and preference shares also in capital structure (Peirson et.

al, 2015). Also, the company should somehow restrict its expenses so that there can be some

retained earnings for the company.

viii. Optimal capital structure

An optimal capital structure is one which has the lowest cost of capital. It can be achieved by a

balance between the debts and equity. A structure with more debts generally has a lower cost of

capital due to tax deduction available. Hence the company should opt for some debt in its

structure as well. The circumstances that can cause a change in optimal capital structure can be

demerger of the company, the redemption of the heavy amount of debentures, the market in

fluctuation, etc (Medical Australia Limited, 2016).

9

selling off the stock or repayment received by the debtors (Porter & Norton, 2014). However,

payments to equity shareholders, debenture holders or preference shareholders can only be made

by selling off a substantial business or shares which may also bring the business to an end or end

of a business segment. So current liabilities are short-term which does not affect the cost of

equity (Shah, 2013).

v. Major value of the WACC calculation

The cost of equity is the major part in the calculation of WACC. As the cost of capital is quite

high, the company needs to invest its fund keeping in mind the high cost, so that the company is

able to recover its cost of capital and other expenses which should be ideally more than the cost

of equity.

vi. Information unavailable

vii. Capital structure

The capital structure of the company consists of only equity share capital. The cost of capital of

the company is very high. So, the company should choose other options also in line with the

industry and should include debentures and preference shares also in capital structure (Peirson et.

al, 2015). Also, the company should somehow restrict its expenses so that there can be some

retained earnings for the company.

viii. Optimal capital structure

An optimal capital structure is one which has the lowest cost of capital. It can be achieved by a

balance between the debts and equity. A structure with more debts generally has a lower cost of

capital due to tax deduction available. Hence the company should opt for some debt in its

structure as well. The circumstances that can cause a change in optimal capital structure can be

demerger of the company, the redemption of the heavy amount of debentures, the market in

fluctuation, etc (Medical Australia Limited, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Medical Australia Limited

IV. Market Analysis

i. Financial performance

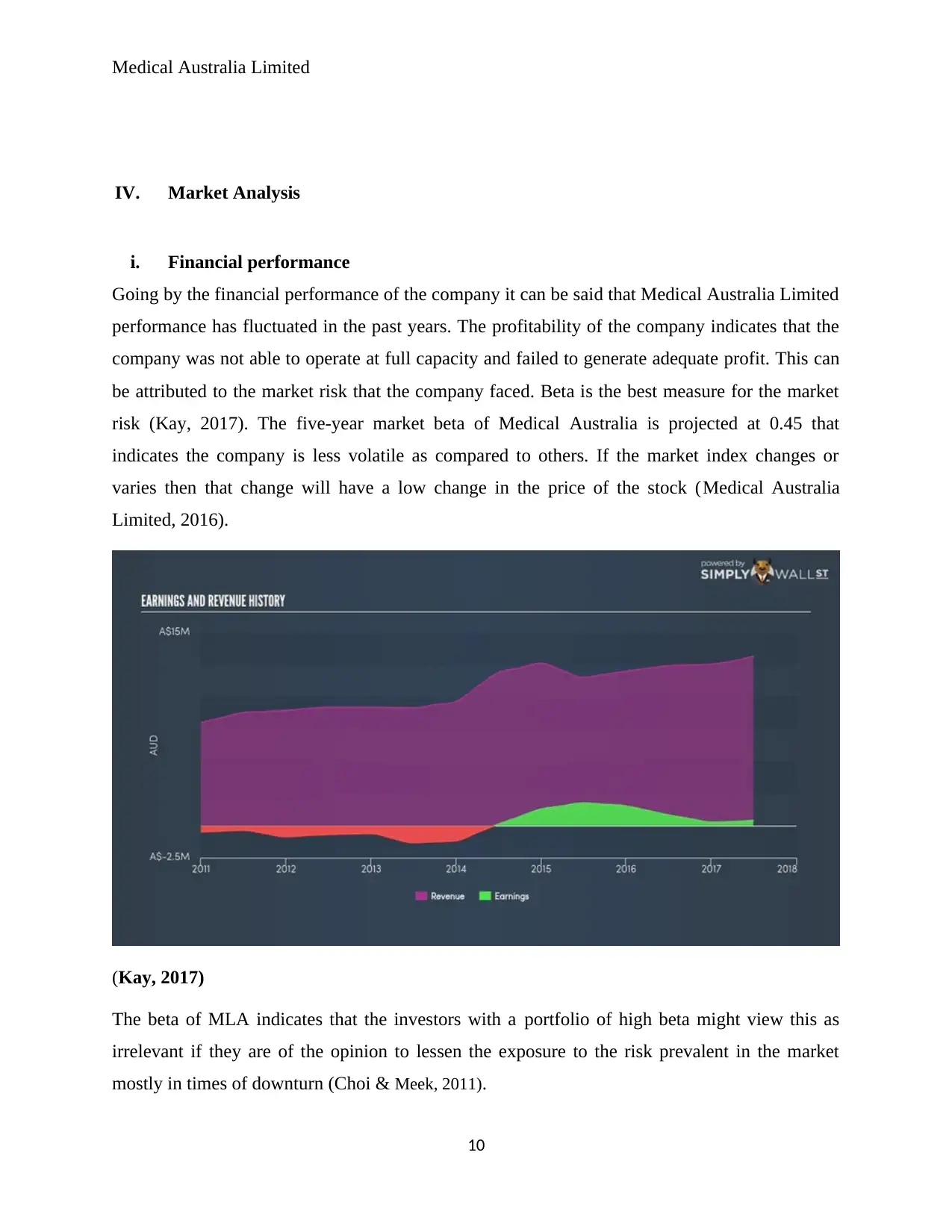

Going by the financial performance of the company it can be said that Medical Australia Limited

performance has fluctuated in the past years. The profitability of the company indicates that the

company was not able to operate at full capacity and failed to generate adequate profit. This can

be attributed to the market risk that the company faced. Beta is the best measure for the market

risk (Kay, 2017). The five-year market beta of Medical Australia is projected at 0.45 that

indicates the company is less volatile as compared to others. If the market index changes or

varies then that change will have a low change in the price of the stock (Medical Australia

Limited, 2016).

(Kay, 2017)

The beta of MLA indicates that the investors with a portfolio of high beta might view this as

irrelevant if they are of the opinion to lessen the exposure to the risk prevalent in the market

mostly in times of downturn (Choi & Meek, 2011).

10

IV. Market Analysis

i. Financial performance

Going by the financial performance of the company it can be said that Medical Australia Limited

performance has fluctuated in the past years. The profitability of the company indicates that the

company was not able to operate at full capacity and failed to generate adequate profit. This can

be attributed to the market risk that the company faced. Beta is the best measure for the market

risk (Kay, 2017). The five-year market beta of Medical Australia is projected at 0.45 that

indicates the company is less volatile as compared to others. If the market index changes or

varies then that change will have a low change in the price of the stock (Medical Australia

Limited, 2016).

(Kay, 2017)

The beta of MLA indicates that the investors with a portfolio of high beta might view this as

irrelevant if they are of the opinion to lessen the exposure to the risk prevalent in the market

mostly in times of downturn (Choi & Meek, 2011).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Medical Australia Limited

ii. Overview of the company

As per the market capitalization of the company that stands AUD $11.35M ranks MLA in the

small-cap category of stocks. Moreover, the company contains higher beta as compared to the

larger companies. The operation of the company is in the healthcare sector and tends to have low

sensitivity to the shocks of the market (Volcker, 2011). In tune to this, a high beta should be

expected for the company but overall a low beta should be present for the healthcare segment.

Therefore, it indicates that MLA should be more volatile (Brigham & Daves, 2012). During the

economic downturn, low demand will lead to re-assessment of the production. The fixed assets

of the company constitute only 22.23% of the total assets and the important fact that needs to be

noted is that the company does not have a heavy reliance on the costly assets (Medical Australia

Limited, 2016). Therefore, the volatility of the company is low and as per the experts, it is a safe

investment that is even projected by the beta of the company.

iii. Other discussion

The important fact that needs to be noted about MLA is that the company bears low fixed cost

meaning that when it comes to operating leverage, it is flexible when it is a downturn. Hence,

MLA can be tagged as a strong bet when it comes to the economic downturn as the beta is low

along with the fixed cost (Wagenhofer, 2014). Both the factors provide a strong cushion to the

company and hence, is an important element that can be taken into consideration.

11

ii. Overview of the company

As per the market capitalization of the company that stands AUD $11.35M ranks MLA in the

small-cap category of stocks. Moreover, the company contains higher beta as compared to the

larger companies. The operation of the company is in the healthcare sector and tends to have low

sensitivity to the shocks of the market (Volcker, 2011). In tune to this, a high beta should be

expected for the company but overall a low beta should be present for the healthcare segment.

Therefore, it indicates that MLA should be more volatile (Brigham & Daves, 2012). During the

economic downturn, low demand will lead to re-assessment of the production. The fixed assets

of the company constitute only 22.23% of the total assets and the important fact that needs to be

noted is that the company does not have a heavy reliance on the costly assets (Medical Australia

Limited, 2016). Therefore, the volatility of the company is low and as per the experts, it is a safe

investment that is even projected by the beta of the company.

iii. Other discussion

The important fact that needs to be noted about MLA is that the company bears low fixed cost

meaning that when it comes to operating leverage, it is flexible when it is a downturn. Hence,

MLA can be tagged as a strong bet when it comes to the economic downturn as the beta is low

along with the fixed cost (Wagenhofer, 2014). Both the factors provide a strong cushion to the

company and hence, is an important element that can be taken into consideration.

11

Medical Australia Limited

Reference:

Brigham, E. & Daves, P 2012, Intermediate Financial Management , USA: Cengage Learning.

Choi, R.D. & Meek, G.K 2011, International accounting, Pearson .

Kay, L 2017, Before You Buy Medical Australia Limited’s, viewed 13 October 2017

https://simplywall.st/news/2017/10/10/before-you-buy-medical-australia-limiteds-asxmla-you-

should-consider-this/

Medical Australia Limited 2016, Medical Australia Limited 2016 annual report and accounts,

viewed 13 October 2017 http://www.medaust.com/irm/company/showpage.aspx?

CategoryId=190&CPID=1565&InstanceVersionNumber=0

Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ: Wiley

Peirson, G, Brown, R., Easton, S, Howard, P & Pinder, S 2015, Business Finance, 12th ed,

North Ryde: McGraw-Hill Australia.

Porter, G & Norton, C 2014, Financial Accounting: The Impact on Decision Maker, Texas:

Cengage Learning

Scapens, R.W 2012, Commentary: How important is practice-relevant management accounting

research? Qualitative Research in Accounting & Management, vol. 9, no.3, pp. 293 – 295.

Shah, P 2013, Financial Accounting, London: Oxford University Press

Subramanyam, K & Wild, J 2014, Financial Statement Analysis, McGraw Hill

Volcker, P 2011, Financial Reform: Unfinished Business, New York Review of Books.

Wagenhofer, A 2014, The role of revenue recognition in performance reporting, Oxford

University Press

12

Reference:

Brigham, E. & Daves, P 2012, Intermediate Financial Management , USA: Cengage Learning.

Choi, R.D. & Meek, G.K 2011, International accounting, Pearson .

Kay, L 2017, Before You Buy Medical Australia Limited’s, viewed 13 October 2017

https://simplywall.st/news/2017/10/10/before-you-buy-medical-australia-limiteds-asxmla-you-

should-consider-this/

Medical Australia Limited 2016, Medical Australia Limited 2016 annual report and accounts,

viewed 13 October 2017 http://www.medaust.com/irm/company/showpage.aspx?

CategoryId=190&CPID=1565&InstanceVersionNumber=0

Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ: Wiley

Peirson, G, Brown, R., Easton, S, Howard, P & Pinder, S 2015, Business Finance, 12th ed,

North Ryde: McGraw-Hill Australia.

Porter, G & Norton, C 2014, Financial Accounting: The Impact on Decision Maker, Texas:

Cengage Learning

Scapens, R.W 2012, Commentary: How important is practice-relevant management accounting

research? Qualitative Research in Accounting & Management, vol. 9, no.3, pp. 293 – 295.

Shah, P 2013, Financial Accounting, London: Oxford University Press

Subramanyam, K & Wild, J 2014, Financial Statement Analysis, McGraw Hill

Volcker, P 2011, Financial Reform: Unfinished Business, New York Review of Books.

Wagenhofer, A 2014, The role of revenue recognition in performance reporting, Oxford

University Press

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.