Accounting 12: Financial Analysis of a Pizza Franchise Project

VerifiedAdded on 2021/05/30

|11

|2109

|142

Homework Assignment

AI Summary

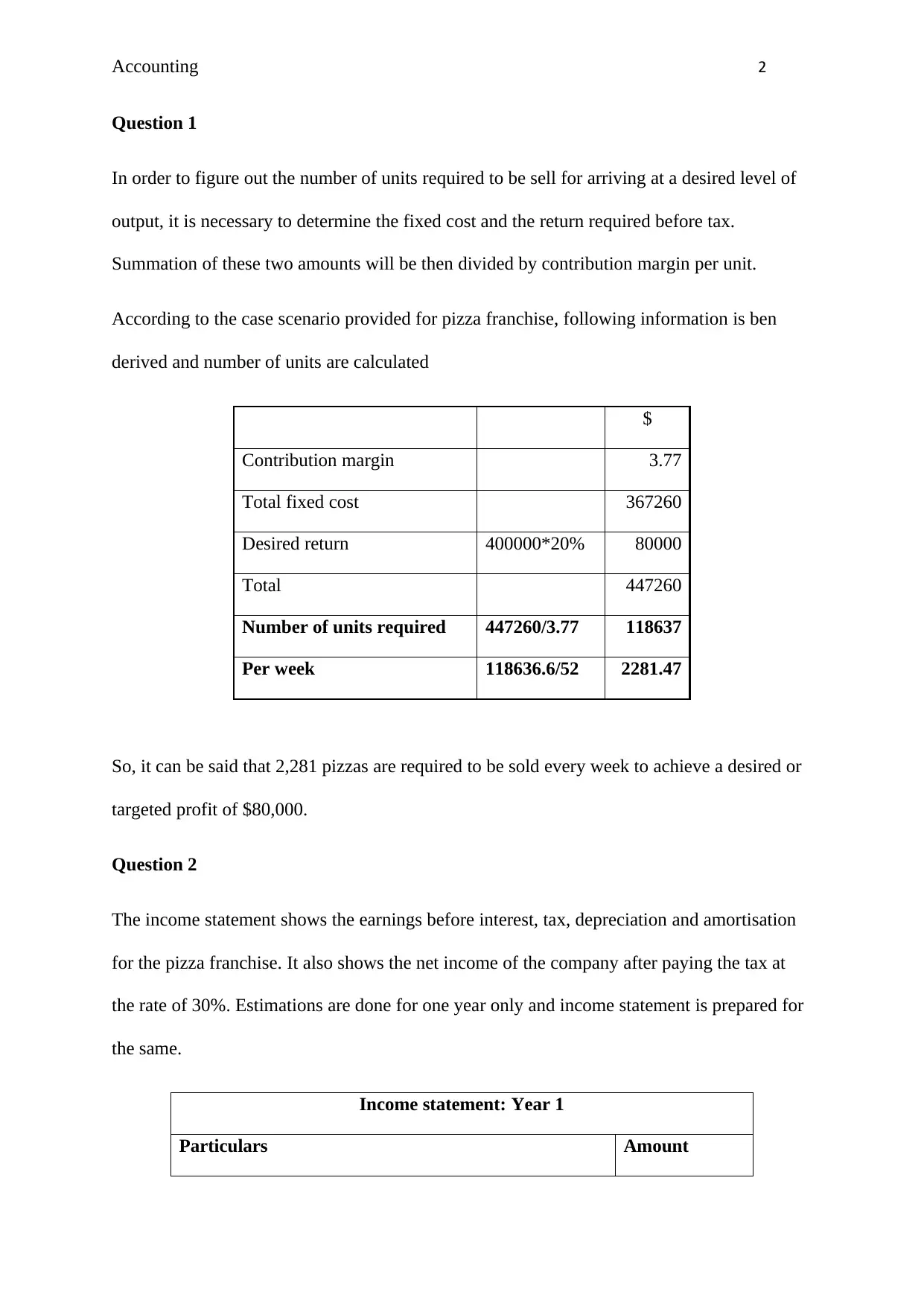

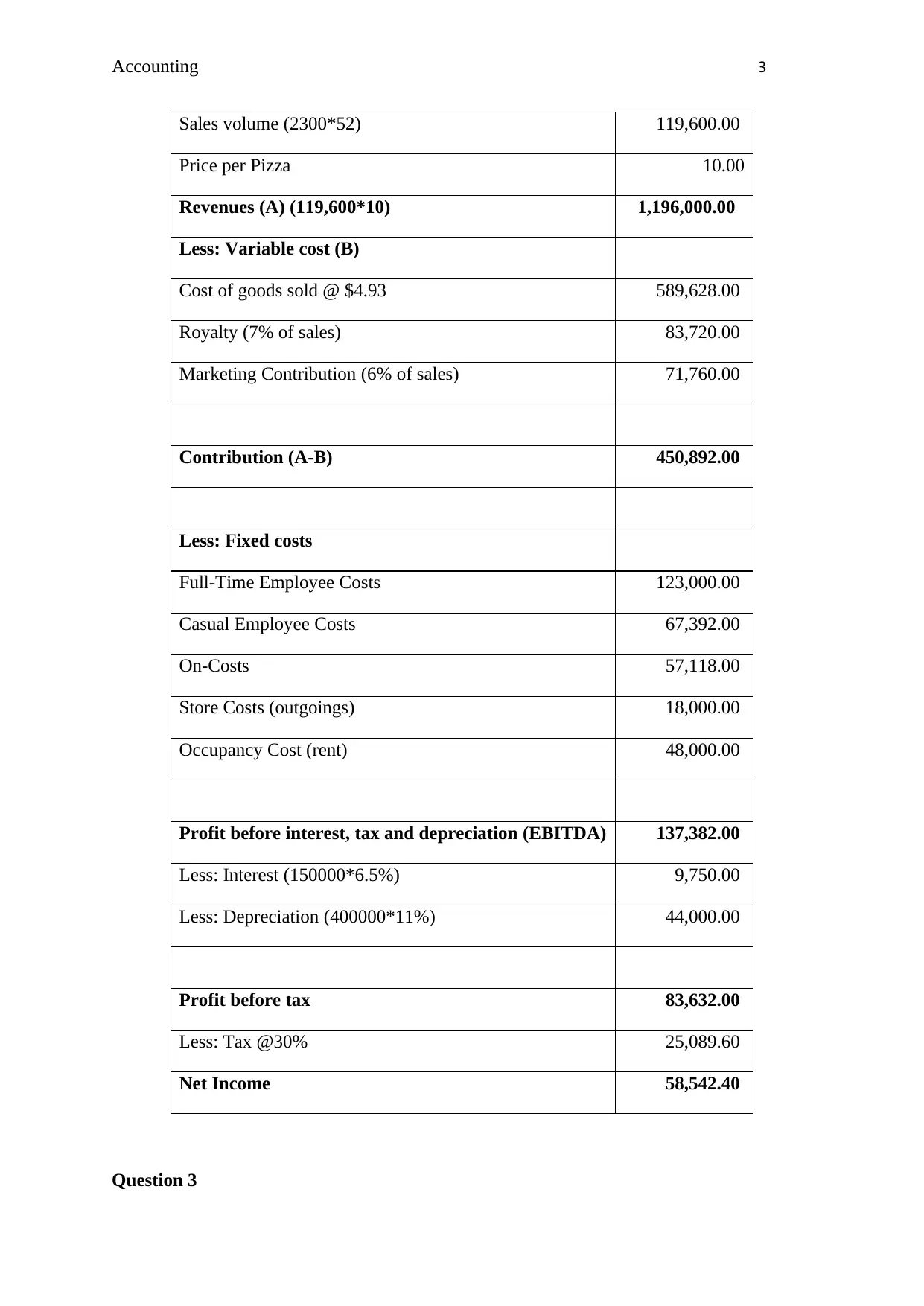

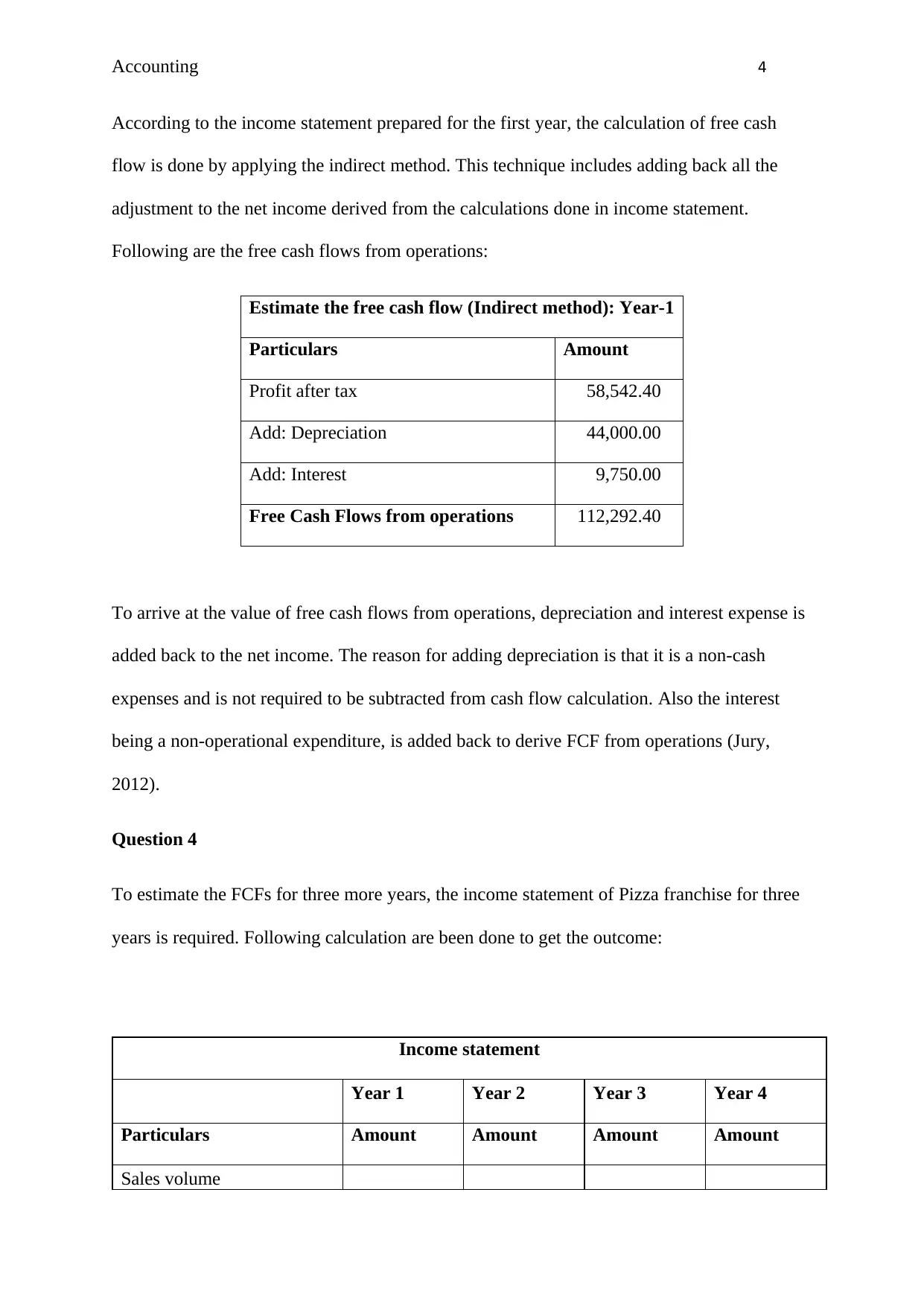

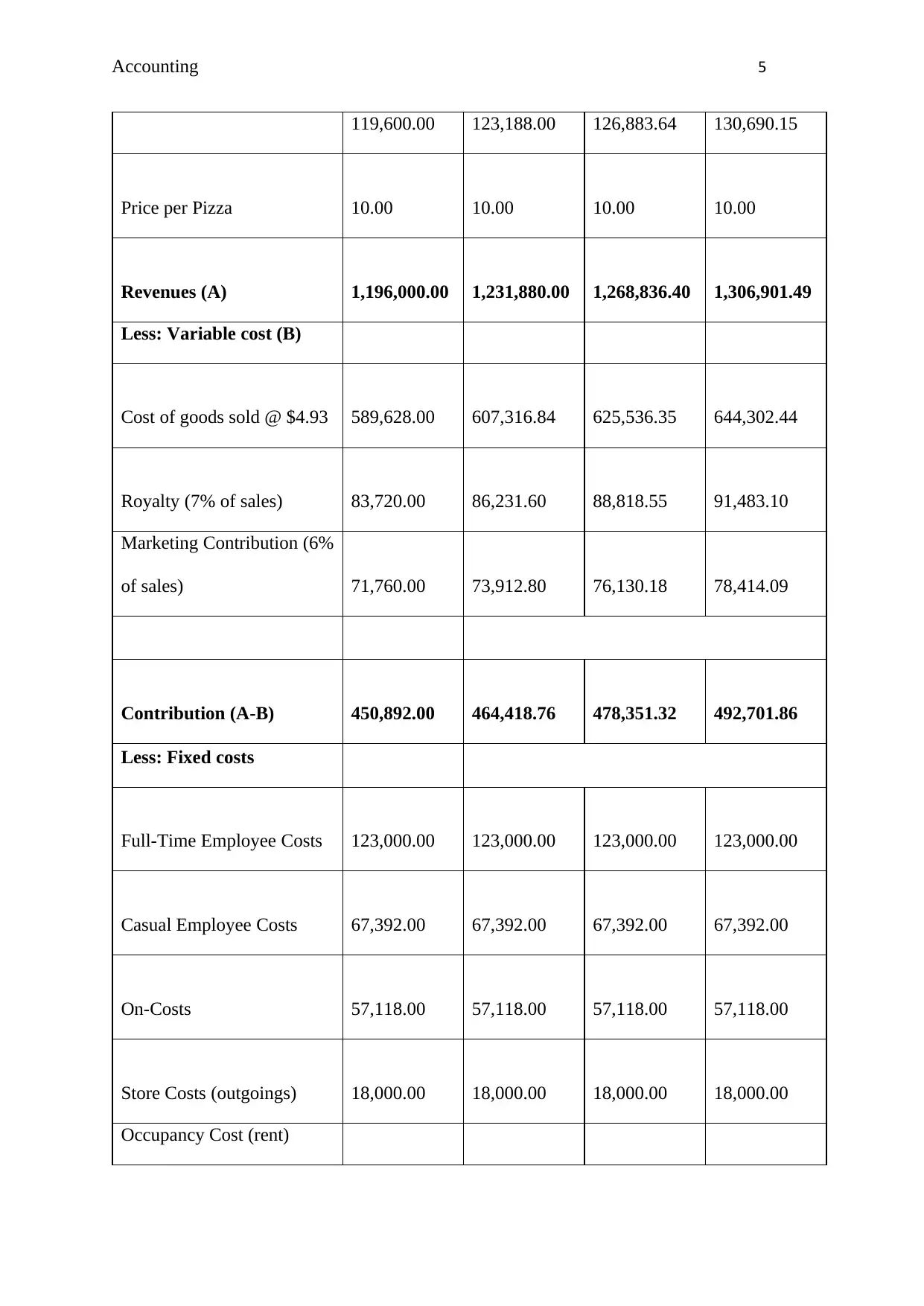

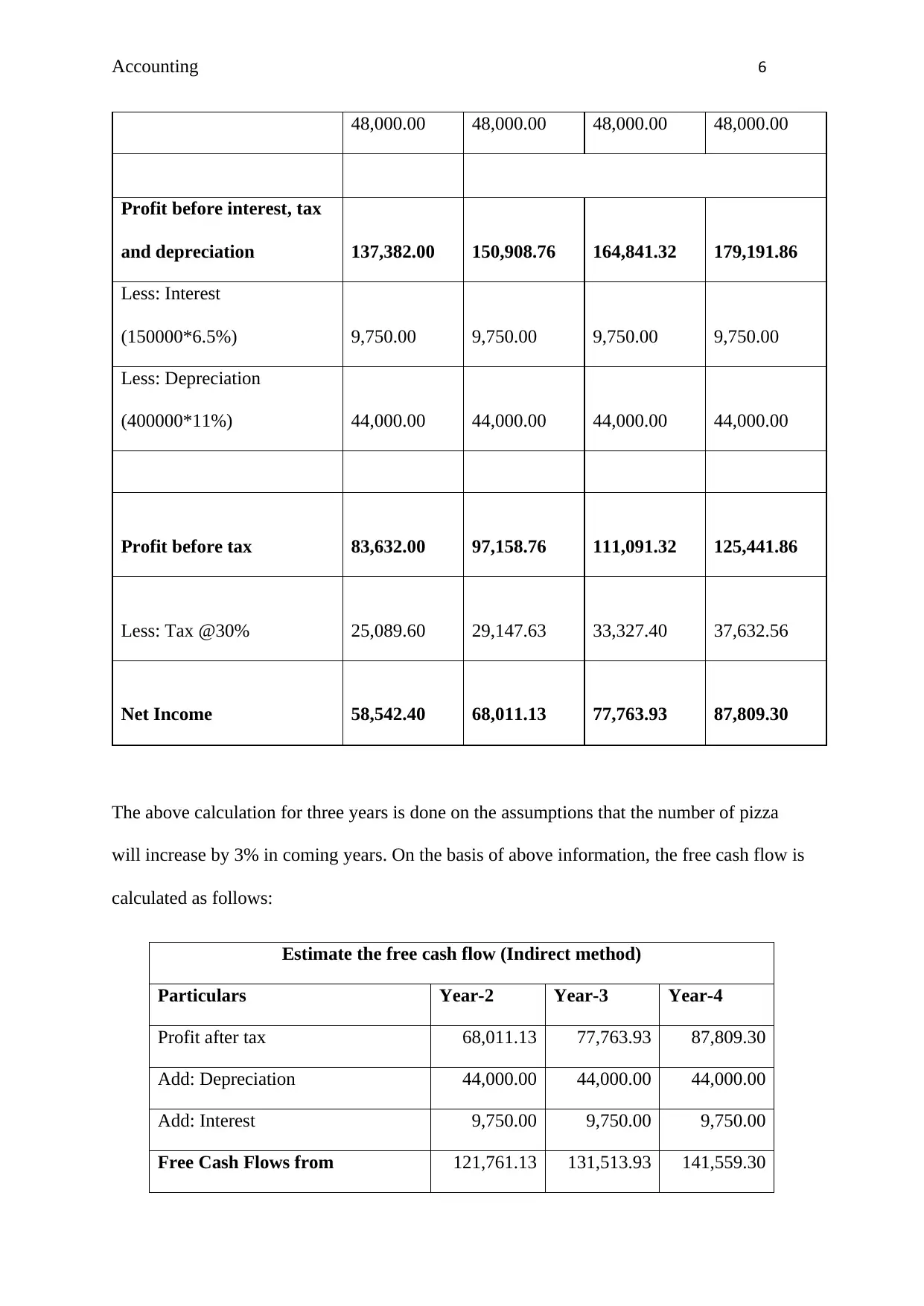

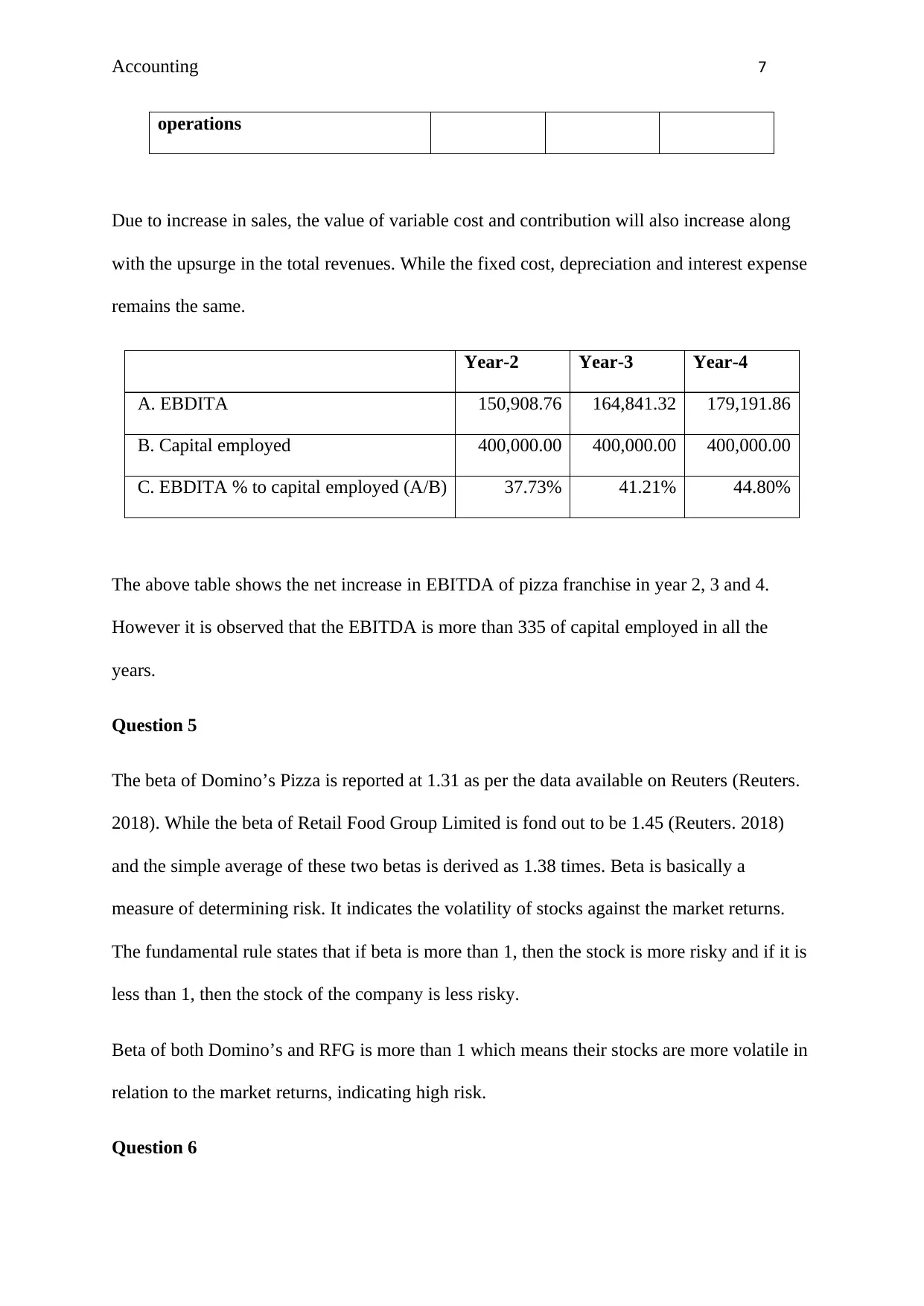

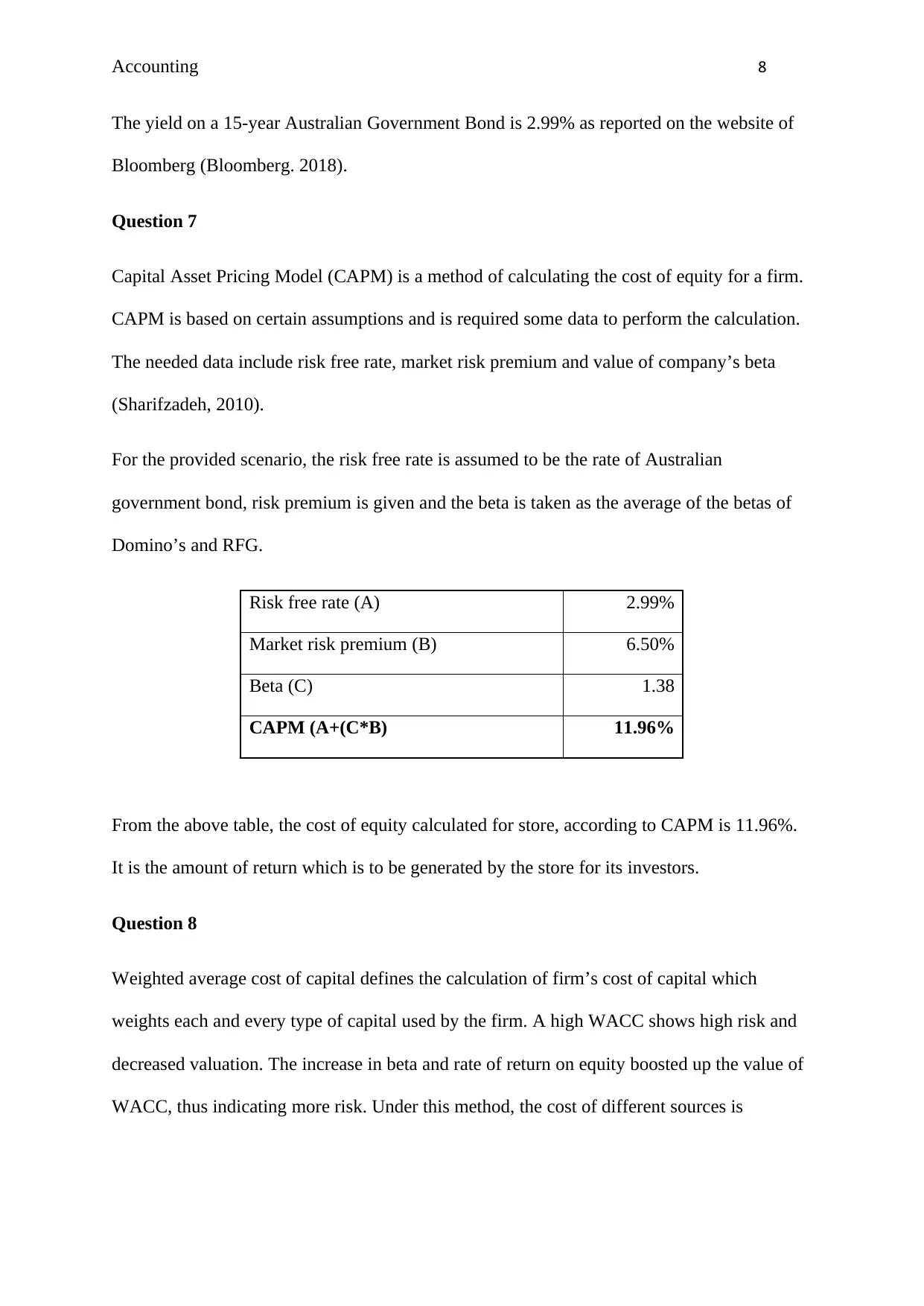

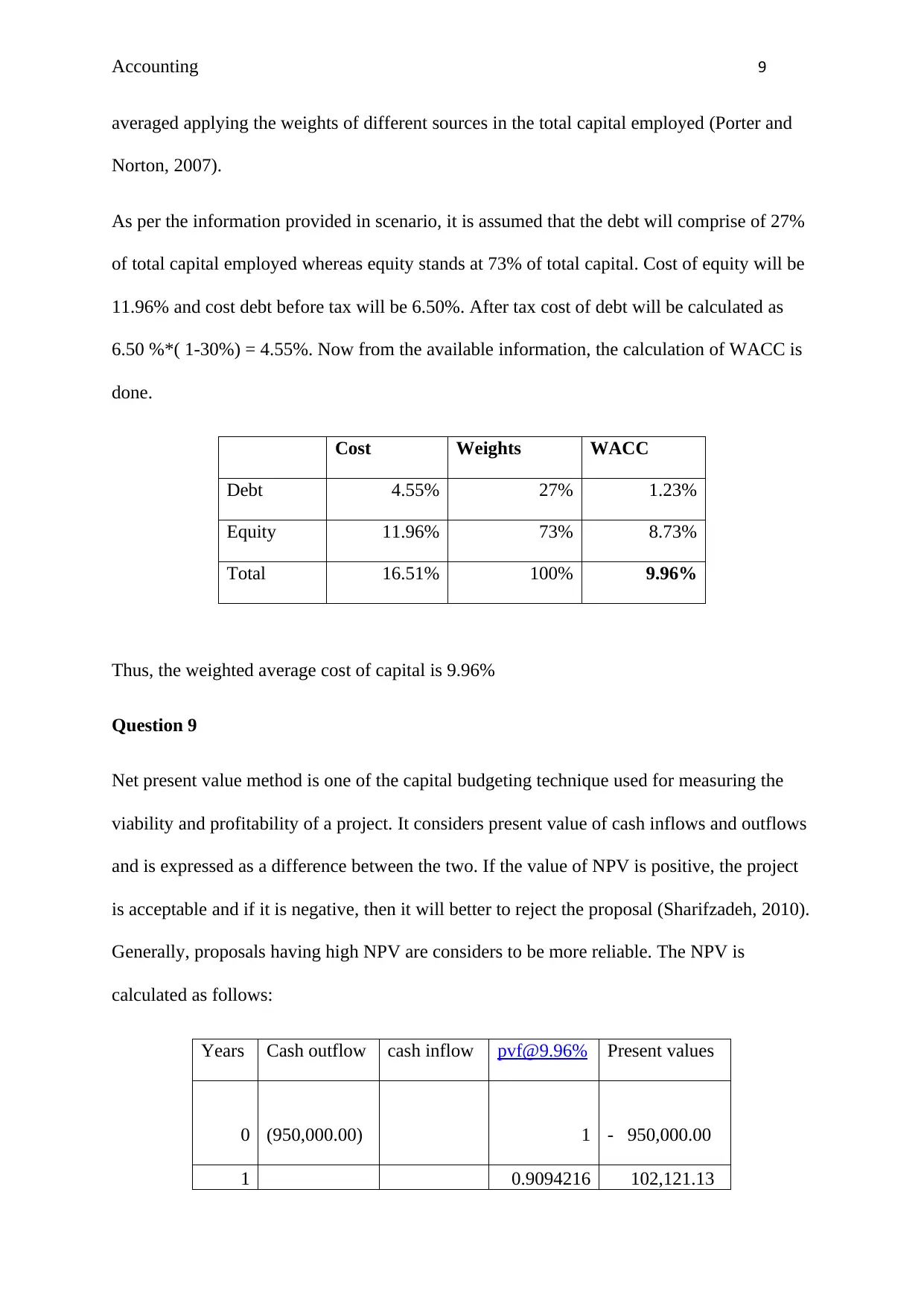

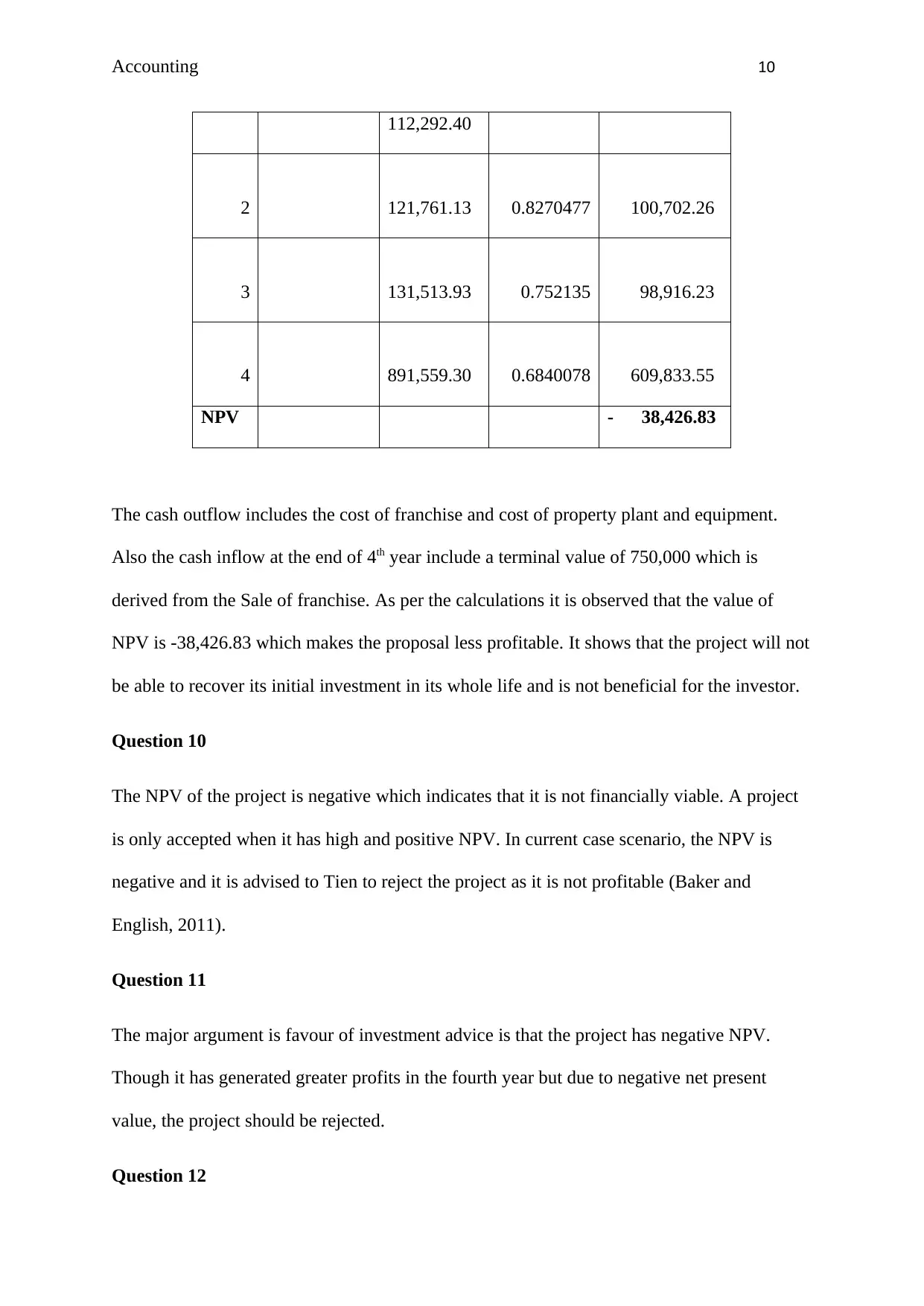

This assignment provides a comprehensive financial analysis of a pizza franchise, addressing several key financial concepts. It begins by calculating the number of pizza units needed to achieve a desired profit, followed by the preparation of an income statement and the calculation of free cash flow using the indirect method. The assignment then forecasts the income statement and free cash flows for the next three years, considering a 3% annual increase in pizza sales. It proceeds to determine the beta of the franchise and its competitors, calculate the cost of equity using the Capital Asset Pricing Model (CAPM), and estimate the weighted average cost of capital (WACC). Finally, the net present value (NPV) of the project is calculated, leading to an investment recommendation and a discussion of potential risks associated with the investment. The analysis utilizes various financial metrics and models to assess the project's viability and profitability.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.