Comprehensive Analysis: Cash Flow, OCI, and Tax Expense of Woolworths

VerifiedAdded on 2021/05/31

|11

|2906

|62

Report

AI Summary

This report provides a detailed analysis of Woolworths Limited's financial performance, focusing on its cash flow statement, other comprehensive income (OCI), and tax expenses for the year ending 2017. The report examines the company's cash flow activities, categorizing them into operating, investing, and financing activities. It highlights key items like cash received from customers, payments to creditors, income tax, and dividends, and includes a comparative evaluation of cash flow trends over three years. The analysis of OCI explains the nature of hedging and foreign currency translation, differentiating it from the profit and loss account. Furthermore, the report delves into the company's income tax expense, comparing accounting income with the tax rate and discussing deferred tax assets and liabilities. The report concludes with a comprehensive assessment of the company's financial reporting practices, offering recommendations based on the findings. References from where the data for the report has been obtained are also provided.

ANALYSIS OF CASH FLOWS, OCI AND TAX EXPENSE

Student Name: Student

ID:

5/18/2018

Student Name: Student

ID:

5/18/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................3

DETAILS OF SELECTED COMPANY................................................................................................................4

ACTIVITIES OF CASH FLOWS – STATEMENT ANALYSIS.................................................................................4

Item Reported.........................................................................................................................................4

Comparative Evaluation..........................................................................................................................6

ANALYSIS OF OCI.........................................................................................................................................6

Reported Details......................................................................................................................................6

Description of Each head.........................................................................................................................7

Different from Profit and Loss Account...................................................................................................7

COMPANY’S INCOME TAX...........................................................................................................................7

Tax Expense for Current Period...............................................................................................................7

Accounting Income and Tax Rate............................................................................................................8

Reporting of Deferred Tax Assets/Liabilities............................................................................................8

Tax expense and Tax Payable..................................................................................................................9

Tax Expense and Actual Tax Paid.............................................................................................................9

Tax- Accounting Treatment Rating..........................................................................................................9

CONCLUSION AND RECOMMENDATION.....................................................................................................9

REFERENCES..............................................................................................................................................10

EXECUTIVE SUMMARY

Companies are mandatorily required to prepare the accounting books and present the results

thereon to the public including the stakeholders so that their needs can be satisfied and

accordingly the company can run in the future. In this report, the results have been detailed with

respect to the two statements – one is the statement of cash flows and other is the other

comprehensive income statement. The report it satisfy the three main purposes and each of it

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................3

DETAILS OF SELECTED COMPANY................................................................................................................4

ACTIVITIES OF CASH FLOWS – STATEMENT ANALYSIS.................................................................................4

Item Reported.........................................................................................................................................4

Comparative Evaluation..........................................................................................................................6

ANALYSIS OF OCI.........................................................................................................................................6

Reported Details......................................................................................................................................6

Description of Each head.........................................................................................................................7

Different from Profit and Loss Account...................................................................................................7

COMPANY’S INCOME TAX...........................................................................................................................7

Tax Expense for Current Period...............................................................................................................7

Accounting Income and Tax Rate............................................................................................................8

Reporting of Deferred Tax Assets/Liabilities............................................................................................8

Tax expense and Tax Payable..................................................................................................................9

Tax Expense and Actual Tax Paid.............................................................................................................9

Tax- Accounting Treatment Rating..........................................................................................................9

CONCLUSION AND RECOMMENDATION.....................................................................................................9

REFERENCES..............................................................................................................................................10

EXECUTIVE SUMMARY

Companies are mandatorily required to prepare the accounting books and present the results

thereon to the public including the stakeholders so that their needs can be satisfied and

accordingly the company can run in the future. In this report, the results have been detailed with

respect to the two statements – one is the statement of cash flows and other is the other

comprehensive income statement. The report it satisfy the three main purposes and each of it

have been followed throughout the report. The first purpose of the report is to discuss about the

results of the company through the cash flows generated and paid by the company. The second

purpose of the report is to identify as to why the other comprehensive income are separately

shown after the profit and loss account and why other classification have also been made in the

annual report of the company. The third and the last main purpose of the report is to know the

expense which has been accounted for by the company for Income Tax and how the same have

been dealt in the presentation of the financial statements. With these three purposes and to know

more about the results of the company, the report is being prepared and provided with adequate

headings and sub headings.

INTRODUCTION

The mandatory preparation of the books of accounts and the financial statements thereon has not

been casted by the statute only rather it is the basic need of every investor of the company to

have the full details of the results of the company and the same shall be monitored by the

company on the regular intervals. The statement which provides the results of the company to the

users of its financial statements shall present the true and fair view otherwise the decision of the

users of the financial statements shall become meaningless.

As the title of the report suggests the analysis of the cash flow statement, the statement showing

the other comprehensive income and the tax expense incurred by the company have been

detailed. The company that has been selected for the purpose of the report is Woolworths limited

and the annual report for the year ending 2017 has been considered. At first the statement of the

cash flows has been discussed and how the same have represented the operations of the company

and details whether the company is generating the cash inflows or incurring the cash outflows.

Each major as well as minor had been discussed in detail. Secondly the statement of the other

comprehensive income had been analysed as to how the statement is different from the normal

income and expenditure statement and the reason as to why it is being prepared and why the

some items of it has the effect of reversing in the future for and gets transferred to the statement

of the profit and loss account. Thirdly the major head has been considered for the company

results of the company through the cash flows generated and paid by the company. The second

purpose of the report is to identify as to why the other comprehensive income are separately

shown after the profit and loss account and why other classification have also been made in the

annual report of the company. The third and the last main purpose of the report is to know the

expense which has been accounted for by the company for Income Tax and how the same have

been dealt in the presentation of the financial statements. With these three purposes and to know

more about the results of the company, the report is being prepared and provided with adequate

headings and sub headings.

INTRODUCTION

The mandatory preparation of the books of accounts and the financial statements thereon has not

been casted by the statute only rather it is the basic need of every investor of the company to

have the full details of the results of the company and the same shall be monitored by the

company on the regular intervals. The statement which provides the results of the company to the

users of its financial statements shall present the true and fair view otherwise the decision of the

users of the financial statements shall become meaningless.

As the title of the report suggests the analysis of the cash flow statement, the statement showing

the other comprehensive income and the tax expense incurred by the company have been

detailed. The company that has been selected for the purpose of the report is Woolworths limited

and the annual report for the year ending 2017 has been considered. At first the statement of the

cash flows has been discussed and how the same have represented the operations of the company

and details whether the company is generating the cash inflows or incurring the cash outflows.

Each major as well as minor had been discussed in detail. Secondly the statement of the other

comprehensive income had been analysed as to how the statement is different from the normal

income and expenditure statement and the reason as to why it is being prepared and why the

some items of it has the effect of reversing in the future for and gets transferred to the statement

of the profit and loss account. Thirdly the major head has been considered for the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which is the tax expense which is mostly remains understood by the shareholders and the

stakeholders of the company.

With these views the report has then included the concluding paragraph and the set of the

reference from where the data for report has been obtained.

DETAILS OF SELECTED COMPANY

The company that has been selected for the purpose of the report is the Woolworths Limited. The

company that has been selected is from Australia and is registered in the stock exchange of

Australia. The company is into the retail industry since its inception which is hundred plus years

ago. The company has been into the activities of having the departmental store and the market

chains and provides all the home products and other related products and services at one place

and has provided the customers with the facility of getting all the things at once place. It has

been operating across Australia and New Zealand and most importantly it is the number two

company in the retail sector. Its major competitor is Wesfarmers Limited. Its main focus is to

increase the customer base by providing the best services to the customers. With the retail sector,

the report has been started and accordingly the annual report of the company as obtained from

website has been considered for this report.

ACTIVITIES OF CASH FLOWS – STATEMENT ANALYSIS

The incoming and outgoing of cash has been detailed in the statement which is known as the

statement showing the cash flows. The incoming and outgoing has been identified and detailed

under the three major heads namely the activities relating to operating function, activities relating

to investment function and the activities relating to the financing function. The minor heads

under each of the above major head has been discussed below.

stakeholders of the company.

With these views the report has then included the concluding paragraph and the set of the

reference from where the data for report has been obtained.

DETAILS OF SELECTED COMPANY

The company that has been selected for the purpose of the report is the Woolworths Limited. The

company that has been selected is from Australia and is registered in the stock exchange of

Australia. The company is into the retail industry since its inception which is hundred plus years

ago. The company has been into the activities of having the departmental store and the market

chains and provides all the home products and other related products and services at one place

and has provided the customers with the facility of getting all the things at once place. It has

been operating across Australia and New Zealand and most importantly it is the number two

company in the retail sector. Its major competitor is Wesfarmers Limited. Its main focus is to

increase the customer base by providing the best services to the customers. With the retail sector,

the report has been started and accordingly the annual report of the company as obtained from

website has been considered for this report.

ACTIVITIES OF CASH FLOWS – STATEMENT ANALYSIS

The incoming and outgoing of cash has been detailed in the statement which is known as the

statement showing the cash flows. The incoming and outgoing has been identified and detailed

under the three major heads namely the activities relating to operating function, activities relating

to investment function and the activities relating to the financing function. The minor heads

under each of the above major head has been discussed below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Item Reported

Although many items are reported in the statement of cash flows, but for the purpose of the

report the main items under the heads have been considered and detailed below:

The item that comes first under the operating activity is the cash that has been received

from the persons to whom the payment has been made. Over the past two years the

increasing trend has been observed in case of the cash which is received from the

customers of the company. Increase has been observed to the tune of $169 millions.

The item that comes after the debtors is the creditors to whom the company makes the

payment for the purchase of the goods and services. It is clear that it is outflow of the

cash and decreasing trend has been observed to the tune of $360 millions.

The item which is of utmost importance is the income tax. Income tax is considered as

the part of the operating activities and accordingly it is the outflow for the company.

Income tax is the amount calculated on the taxable income of the company and not the

accounting income of the company.

Whenever the company sells its goods and that too only capital goods then the cash

inflows will be there and accordingly cash inflows will be considered in the statement.

In case the company purchases its goods and that too only capital goods then the cash

outflows will be there and accordingly the cash outflows will be considered in the

statement.

The other major part in the cash flow statement is the case when the company purchases

the other businesses and accordingly the cash outflows will be there. It is the one time

activity and not the running activity.

The other major item is the dividend. It is that item which is considered as the cash

inflows as well as the cash outflows. Cash inflow occurs when the company receives the

dividend on the investment if any made by the company and cash inflow occurs when the

company pays the dividend.

Whenever the company issues the share to the public the amount comes and that amount

is regarded as the cash inflow for the company.

Whenever the company borrows the amount from the banks and the financial institutions

then the amount received is considered as the inflows of cash. The company will repay

the same and accordingly the amount which repaid by the company to the banks will be

Although many items are reported in the statement of cash flows, but for the purpose of the

report the main items under the heads have been considered and detailed below:

The item that comes first under the operating activity is the cash that has been received

from the persons to whom the payment has been made. Over the past two years the

increasing trend has been observed in case of the cash which is received from the

customers of the company. Increase has been observed to the tune of $169 millions.

The item that comes after the debtors is the creditors to whom the company makes the

payment for the purchase of the goods and services. It is clear that it is outflow of the

cash and decreasing trend has been observed to the tune of $360 millions.

The item which is of utmost importance is the income tax. Income tax is considered as

the part of the operating activities and accordingly it is the outflow for the company.

Income tax is the amount calculated on the taxable income of the company and not the

accounting income of the company.

Whenever the company sells its goods and that too only capital goods then the cash

inflows will be there and accordingly cash inflows will be considered in the statement.

In case the company purchases its goods and that too only capital goods then the cash

outflows will be there and accordingly the cash outflows will be considered in the

statement.

The other major part in the cash flow statement is the case when the company purchases

the other businesses and accordingly the cash outflows will be there. It is the one time

activity and not the running activity.

The other major item is the dividend. It is that item which is considered as the cash

inflows as well as the cash outflows. Cash inflow occurs when the company receives the

dividend on the investment if any made by the company and cash inflow occurs when the

company pays the dividend.

Whenever the company issues the share to the public the amount comes and that amount

is regarded as the cash inflow for the company.

Whenever the company borrows the amount from the banks and the financial institutions

then the amount received is considered as the inflows of cash. The company will repay

the same and accordingly the amount which repaid by the company to the banks will be

considered as the repayment of borrowings and hence is the cash outflow. The total of

approximately $1400 million has been the cash outflow for the company. (Fraser,

Ormiston and Fraser, 2010)

The last and the major item to with each of shareholders and the stakeholders of the

company is concerned is with the status of the cash flows of the company and

accordingly when there is excess of the cash then it will be said that there is increase in

the cash and cash equivalents and otherwise there will be decrease in the same

(Woolworths Limited, 2016).

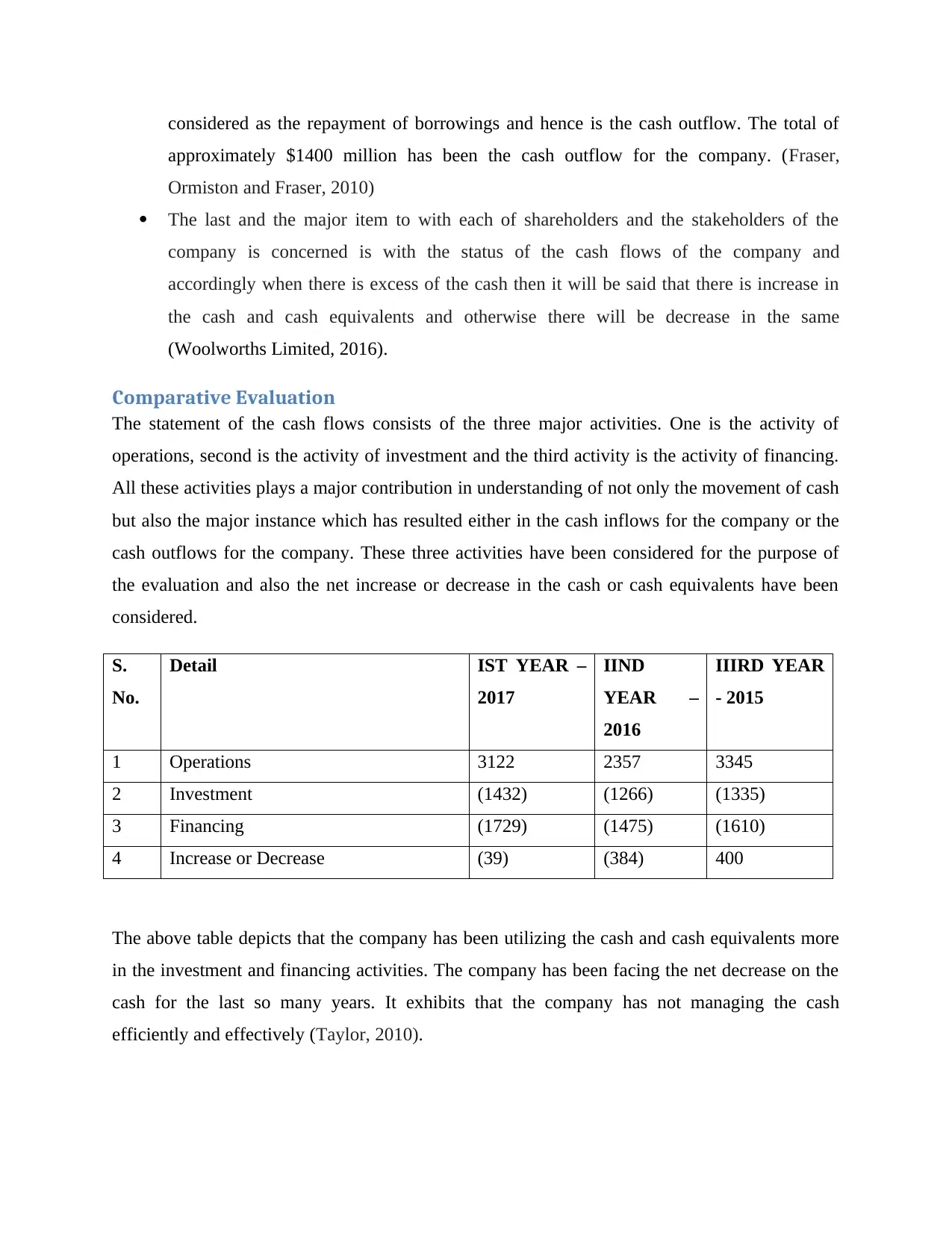

Comparative Evaluation

The statement of the cash flows consists of the three major activities. One is the activity of

operations, second is the activity of investment and the third activity is the activity of financing.

All these activities plays a major contribution in understanding of not only the movement of cash

but also the major instance which has resulted either in the cash inflows for the company or the

cash outflows for the company. These three activities have been considered for the purpose of

the evaluation and also the net increase or decrease in the cash or cash equivalents have been

considered.

S.

No.

Detail IST YEAR –

2017

IIND

YEAR –

2016

IIIRD YEAR

- 2015

1 Operations 3122 2357 3345

2 Investment (1432) (1266) (1335)

3 Financing (1729) (1475) (1610)

4 Increase or Decrease (39) (384) 400

The above table depicts that the company has been utilizing the cash and cash equivalents more

in the investment and financing activities. The company has been facing the net decrease on the

cash for the last so many years. It exhibits that the company has not managing the cash

efficiently and effectively (Taylor, 2010).

approximately $1400 million has been the cash outflow for the company. (Fraser,

Ormiston and Fraser, 2010)

The last and the major item to with each of shareholders and the stakeholders of the

company is concerned is with the status of the cash flows of the company and

accordingly when there is excess of the cash then it will be said that there is increase in

the cash and cash equivalents and otherwise there will be decrease in the same

(Woolworths Limited, 2016).

Comparative Evaluation

The statement of the cash flows consists of the three major activities. One is the activity of

operations, second is the activity of investment and the third activity is the activity of financing.

All these activities plays a major contribution in understanding of not only the movement of cash

but also the major instance which has resulted either in the cash inflows for the company or the

cash outflows for the company. These three activities have been considered for the purpose of

the evaluation and also the net increase or decrease in the cash or cash equivalents have been

considered.

S.

No.

Detail IST YEAR –

2017

IIND

YEAR –

2016

IIIRD YEAR

- 2015

1 Operations 3122 2357 3345

2 Investment (1432) (1266) (1335)

3 Financing (1729) (1475) (1610)

4 Increase or Decrease (39) (384) 400

The above table depicts that the company has been utilizing the cash and cash equivalents more

in the investment and financing activities. The company has been facing the net decrease on the

cash for the last so many years. It exhibits that the company has not managing the cash

efficiently and effectively (Taylor, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ANALYSIS OF OCI

Reported Details

Two items have been shown in the statement of the other comprehensive income which are:

- Hedging and

- Translation of Foreign Currency

Description of Each head

The hedging is mainly related to the hedge that is meant for the cash flows only. It is reclassified

as to be transferred to the profit and loss account and is transferred once it gets realized.

(Chambers, 2011).

Other item is the foreign currency translation which checks for the change in value of the foreign

currency and books the unrealized part in the statement and reclassifies the same into the

statement of the profit and loss (Bamber, Jiang, Petroni and Wang, 2010).

Different from Profit and Loss Account

The statement of the profit and loss is different from the statement of the comprehensive income

in the sense that the former considers the operating activities only and in case any non recurring

activity occurs then the same shall be disclosed in the statement of the other comprehensive

income.

The major part to consider is that the above items so reported in the statement of the other

comprehensive income is liable to be reclassified for transferring to the statement of the profit

and loss in the future when the same is realized.

Reported Details

Two items have been shown in the statement of the other comprehensive income which are:

- Hedging and

- Translation of Foreign Currency

Description of Each head

The hedging is mainly related to the hedge that is meant for the cash flows only. It is reclassified

as to be transferred to the profit and loss account and is transferred once it gets realized.

(Chambers, 2011).

Other item is the foreign currency translation which checks for the change in value of the foreign

currency and books the unrealized part in the statement and reclassifies the same into the

statement of the profit and loss (Bamber, Jiang, Petroni and Wang, 2010).

Different from Profit and Loss Account

The statement of the profit and loss is different from the statement of the comprehensive income

in the sense that the former considers the operating activities only and in case any non recurring

activity occurs then the same shall be disclosed in the statement of the other comprehensive

income.

The major part to consider is that the above items so reported in the statement of the other

comprehensive income is liable to be reclassified for transferring to the statement of the profit

and loss in the future when the same is realized.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPANY’S INCOME TAX

Tax Expense for Current Period

Income tax expense of $ 837.70 million has been reported by the company for the year ended on

30th June 2017 in its annual report. The company has reported in statement of profit or loss and it

includes tax expense for current year, tax expense which has been deferred and adjustments for

tax expense related to past years (Woolworths Limited, 2017).

Accounting Income and Tax Rate

The reported income tax expense and the tax rate multiply by accounting income value are

different from each other. The both value reported or can be calculated value are not same for

Woolworths Limited for the period ended on June 2017. The reason for difference in two values

is because of timing differences which consists of tax effect on the below items:-

a. Off Shore tax rate differences reported in operations of the company

b. Amount of impairment not allowed as deduction

c. Not recognized tax loss

d. Non deductible expenses

Reporting of Deferred Tax Assets/Liabilities

As per AASB 112, every company has report deferred tax asset/liabilities created due to timing

difference in transactions having tax impact. In Woolworths Limited, $ 372.30 million has been

disclosed as deferred tax asset in the annual report for the period ending on 30th June, 2017. The

deferred tax asset has been created to report the timing difference which occurred due to

following transactions:-

a. Timing difference occurred due to difference in depreciation rates under different

laws which need to be followed while presenting financial statements

Tax Expense for Current Period

Income tax expense of $ 837.70 million has been reported by the company for the year ended on

30th June 2017 in its annual report. The company has reported in statement of profit or loss and it

includes tax expense for current year, tax expense which has been deferred and adjustments for

tax expense related to past years (Woolworths Limited, 2017).

Accounting Income and Tax Rate

The reported income tax expense and the tax rate multiply by accounting income value are

different from each other. The both value reported or can be calculated value are not same for

Woolworths Limited for the period ended on June 2017. The reason for difference in two values

is because of timing differences which consists of tax effect on the below items:-

a. Off Shore tax rate differences reported in operations of the company

b. Amount of impairment not allowed as deduction

c. Not recognized tax loss

d. Non deductible expenses

Reporting of Deferred Tax Assets/Liabilities

As per AASB 112, every company has report deferred tax asset/liabilities created due to timing

difference in transactions having tax impact. In Woolworths Limited, $ 372.30 million has been

disclosed as deferred tax asset in the annual report for the period ending on 30th June, 2017. The

deferred tax asset has been created to report the timing difference which occurred due to

following transactions:-

a. Timing difference occurred due to difference in depreciation rates under different

laws which need to be followed while presenting financial statements

b. Cash flow Hedges

c. Accrued expenses considered in books of accounts

d. Provisions recorded in financial statements

e. Unrealized differences in foreign exchange as the company is operating in more than

one country (Harrington, Smith and Trippeer, 2012)

Tax expense and Tax Payable

Woolworths Limited has reported the tax expense amount and tax payable amount. Both the

values are not same as the tax expense includes current tax expense and deferred tax expense and

on the other hand tax payable is actual amount which the company has to pay to tax authorities

of the country. In the annual report, the tax expense is $ 837.70 million where as tax payable is $

80.9 million for the year ended on 30th June 2017 (Laux, 2013).

Tax Expense and Actual Tax Paid

The amount of income tax expense is the combination of current tax and deferred tax. Tax paid is

the amount or outflow of cash and cash equivalents to discharge the liability which has been

arose on account of tax payable. The two values are different and can’t be same. Woolworths

Limited report $ 837.70 million has tax expense whereas the company has $ 668.1 million as tax

during the year ended on 30th June 2017 (Manzon, G.B. and Plesko, 2012).

Tax- Accounting Treatment Rating

Accounting treatment of tax adopted by the company in line with applicable rules and

regulations and is according to accounting principles governing the same. The policies adopted

c. Accrued expenses considered in books of accounts

d. Provisions recorded in financial statements

e. Unrealized differences in foreign exchange as the company is operating in more than

one country (Harrington, Smith and Trippeer, 2012)

Tax expense and Tax Payable

Woolworths Limited has reported the tax expense amount and tax payable amount. Both the

values are not same as the tax expense includes current tax expense and deferred tax expense and

on the other hand tax payable is actual amount which the company has to pay to tax authorities

of the country. In the annual report, the tax expense is $ 837.70 million where as tax payable is $

80.9 million for the year ended on 30th June 2017 (Laux, 2013).

Tax Expense and Actual Tax Paid

The amount of income tax expense is the combination of current tax and deferred tax. Tax paid is

the amount or outflow of cash and cash equivalents to discharge the liability which has been

arose on account of tax payable. The two values are different and can’t be same. Woolworths

Limited report $ 837.70 million has tax expense whereas the company has $ 668.1 million as tax

during the year ended on 30th June 2017 (Manzon, G.B. and Plesko, 2012).

Tax- Accounting Treatment Rating

Accounting treatment of tax adopted by the company in line with applicable rules and

regulations and is according to accounting principles governing the same. The policies adopted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the company are very useful, easy and transparent so that effective and efficient decision

making can be done by different stakeholders of the company.

CONCLUSION AND RECOMMENDATION

Annual Reports of the company is the basis for providing information to different users of

accounting which serves the primary objectives of general purpose financial reporting. The

company which has been chosen for the study – Woolworths Limited has been analyzed in

details. The components of the financial statements have been describe in detail so that users can

understand the purpose for providing information in specific statement format by the company.

The cash flow statement has been analyzed which provide the information about the performance

of liquidity of the company. Also, statement of comprehensive income has explains what will be

the future prospective incomes of the company which are assesses in the current year. The

treatment and account of corporation tax has also been analyzed which shows that the company

is complying with all the relevant provisions of the accounting laws in relation to tax. In order to

conclude, it can be said Woolworths financial statements and their components so transparent

that can helps the users to provide effective information.

To recommend, the financial statements and all sub statements of financial statements should be

prepared by following the rules and regulations set by AASB and Corporation Act, 2001 so that

true and fair view of accounting information can be obtained and appropriate decision making

can happen.

REFERENCES

Bamber, L.S., Jiang, J., Petroni, K.R. and Wang, I.Y., 2010. Comprehensive income: Who's

afraid of performance reporting?. The Accounting Review, 85(1), pp.97-126

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements Pearson

Harrington, C., Smith, W. and Trippeer, D., 2012,Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, p.1

making can be done by different stakeholders of the company.

CONCLUSION AND RECOMMENDATION

Annual Reports of the company is the basis for providing information to different users of

accounting which serves the primary objectives of general purpose financial reporting. The

company which has been chosen for the study – Woolworths Limited has been analyzed in

details. The components of the financial statements have been describe in detail so that users can

understand the purpose for providing information in specific statement format by the company.

The cash flow statement has been analyzed which provide the information about the performance

of liquidity of the company. Also, statement of comprehensive income has explains what will be

the future prospective incomes of the company which are assesses in the current year. The

treatment and account of corporation tax has also been analyzed which shows that the company

is complying with all the relevant provisions of the accounting laws in relation to tax. In order to

conclude, it can be said Woolworths financial statements and their components so transparent

that can helps the users to provide effective information.

To recommend, the financial statements and all sub statements of financial statements should be

prepared by following the rules and regulations set by AASB and Corporation Act, 2001 so that

true and fair view of accounting information can be obtained and appropriate decision making

can happen.

REFERENCES

Bamber, L.S., Jiang, J., Petroni, K.R. and Wang, I.Y., 2010. Comprehensive income: Who's

afraid of performance reporting?. The Accounting Review, 85(1), pp.97-126

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements Pearson

Harrington, C., Smith, W. and Trippeer, D., 2012,Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, p.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments The Accounting Review, 88(4), pp.1357-1383

Manzon Jr, G.B. and Plesko, G.A., 2012. The relation between financial and tax reporting

measures of income Tax L. Rev., 55, p.175

Taylor, M., 2010, Financial statement analysis, pp 13-20

Woolworths Limited (2016), Annual Report -2016 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

Woolworths Limited (2017), Annual Report -2017 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

payments The Accounting Review, 88(4), pp.1357-1383

Manzon Jr, G.B. and Plesko, G.A., 2012. The relation between financial and tax reporting

measures of income Tax L. Rev., 55, p.175

Taylor, M., 2010, Financial statement analysis, pp 13-20

Woolworths Limited (2016), Annual Report -2016 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

Woolworths Limited (2017), Annual Report -2017 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.