Financial Analysis Report: Cash Budget, Breakeven, and NPV Analysis

VerifiedAdded on 2022/11/01

|9

|1234

|404

Report

AI Summary

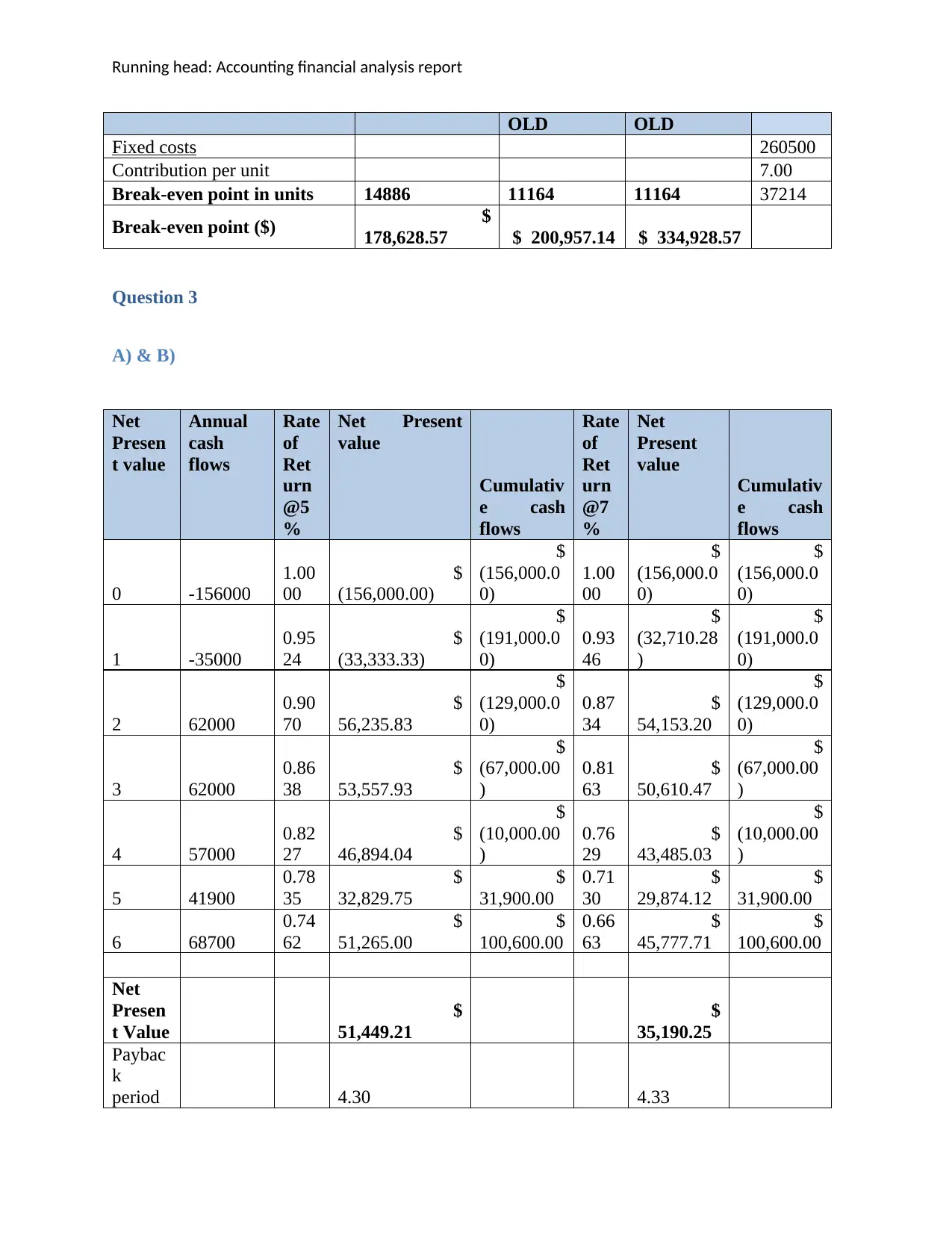

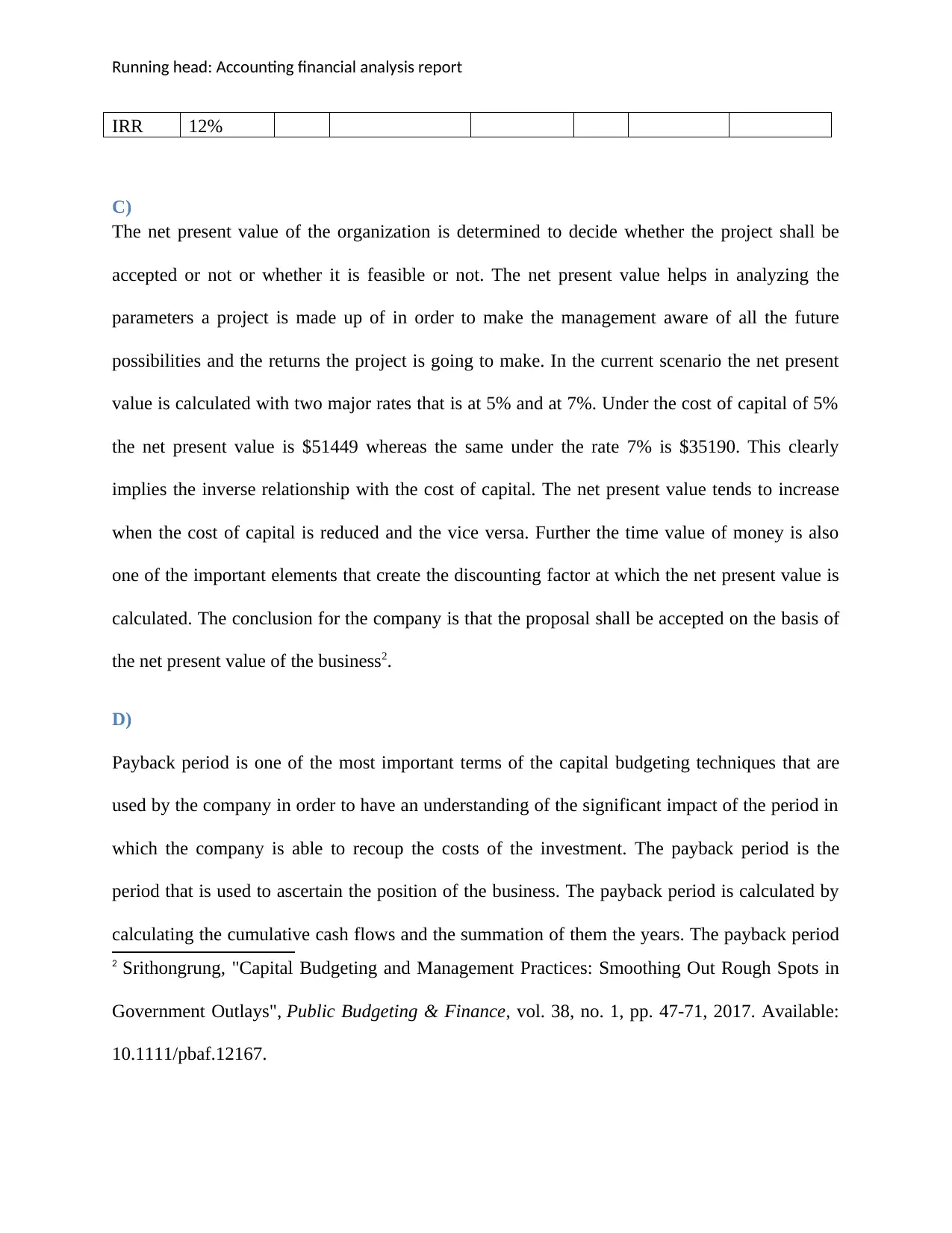

This financial analysis report presents a comprehensive examination of Garden Enterprises' financial performance. The report begins with a detailed cash budget analysis spanning three months, evaluating cash receipts and payments to determine the ending cash balance. Subsequently, a breakeven analysis is conducted, considering different product sales mixes and their impact on profitability. The report then delves into capital budgeting techniques, specifically net present value (NPV) calculations and payback period analysis, to assess the viability of a project under various discount rates. The NPV is calculated at 5% and 7%, and a payback period of 4.30 years is determined. The report concludes that the project should be accepted based on positive NPV and an acceptable payback period. The report includes references to relevant academic sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.