Analysis of Financial Resources for Sweet Menu Restaurant Expansion

VerifiedAdded on 2020/01/15

|17

|5300

|159

Report

AI Summary

This report provides a comprehensive financial analysis of Sweet Menu Restaurant, focusing on its expansion plans. It explores various sources of finance, including bank loans, venture capital, and retained earnings, while examining the implications and costs associated with each. The report emphasizes the importance of financial planning for the restaurant's growth and identifies the information needs of different decision-makers. Investment appraisal techniques are applied to evaluate the feasibility of expansion projects, and ratio analysis is used to compare the restaurant's performance with competitors. The analysis covers budgeting, unit cost calculations, and the role of key financial statements in decision-making. Overall, the report offers insights into strategic financial management for the restaurant's sustainable growth and success in a competitive market.

Managing Financial Resources and

Decision

Decision

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Different sources of finance for Sweet Menu Restaurant......................................................1

1.2 Implications of Sources.........................................................................................................2

1.3 Appropriate source of finance...............................................................................................2

Task 2...............................................................................................................................................3

2.1 Costs associated with different means of funding.................................................................3

2.2 Importance of Financial Planning..........................................................................................3

2.3 Information needs of different decision makers that are associated with Sweet Menu

Restaurant....................................................................................................................................4

2.4 Impact of finance on the statements......................................................................................5

Task 3...............................................................................................................................................5

3.1 Analyse budget......................................................................................................................5

3.2 Unit costs calculation.............................................................................................................6

3.3 Investment Appraisal Techniques..........................................................................................7

Task 4...............................................................................................................................................9

4.1 Discuss the main financial statements...................................................................................9

4.2 Different between major financial statements.....................................................................10

4.3 Ratio Analysis......................................................................................................................11

Conclusion.....................................................................................................................................12

References........................................................................................................................................1

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Different sources of finance for Sweet Menu Restaurant......................................................1

1.2 Implications of Sources.........................................................................................................2

1.3 Appropriate source of finance...............................................................................................2

Task 2...............................................................................................................................................3

2.1 Costs associated with different means of funding.................................................................3

2.2 Importance of Financial Planning..........................................................................................3

2.3 Information needs of different decision makers that are associated with Sweet Menu

Restaurant....................................................................................................................................4

2.4 Impact of finance on the statements......................................................................................5

Task 3...............................................................................................................................................5

3.1 Analyse budget......................................................................................................................5

3.2 Unit costs calculation.............................................................................................................6

3.3 Investment Appraisal Techniques..........................................................................................7

Task 4...............................................................................................................................................9

4.1 Discuss the main financial statements...................................................................................9

4.2 Different between major financial statements.....................................................................10

4.3 Ratio Analysis......................................................................................................................11

Conclusion.....................................................................................................................................12

References........................................................................................................................................1

INTRODUCTION

In the current corporate scenario, every business requires adequate amount of funds or

money to carry out operations appropriately. However, increasing competition has also enforced

the companies to enhance their level of operations to attain future sustainability. Thus, financial

resources are the integral part of business enterprise and it is the duty of senior authority to

ensure that they make optimum utilisation of available resources and generate desired results and

outcomes (Cunningham, 2006). In this context, current report focuses on economic analysis of

Sweet Menu Restaurant Ltd which is one the its own kind of restaurant in Gants Hills in East

London. With recent success top level management of restaurant are planning to open two new

branches in popular places of London with the aim of attracting large number of customers

through hygiene and delicious intercontinental offerings. In this regard, various sources of funds

has been analysed to raise the amount between £300000 and £500000. Further, implications

associated with the different sources has been focused on and importance of financial planning

for the betterment of business operations. Thereafter, different stakeholder of cited restaurant has

been identified and their importance in decision making. Along with this, investment appraisal

techniques have been used to evaluate the feasibility and reliability of the proposals for the future

expansion and lastly, with the help of ratio analysis performance of cited firm is compared with

its competitor (Blue Island Restaurant).

TASK 1

1.1 Different sources of finance for Sweet Menu Restaurant

As per the present provided case, Sweet Menu Restaurant is planning to enhance its

business functioning by opening two new branches in popular places of London. In order to do

so, huge amount between £300000 to £500000 is required by the management and for which

they can make use of following sources of finance:

Bank Loan: At present in UK there are several financial institutions which provide

corporate loan to the firms so that they can enhance their business operations and attain

long term sustainability (Narayananand Nanda, 2004). Considering the debt financing it

is one of the most feasible options available to the management of Sweet Menu

Restaurant. The main benefit of this source is that it is available on the basis of mere

formalities as well as repayment of loan is based on monthly instalment which is feasible

for the SME like Sweet Menu Restaurant to repay.

1

In the current corporate scenario, every business requires adequate amount of funds or

money to carry out operations appropriately. However, increasing competition has also enforced

the companies to enhance their level of operations to attain future sustainability. Thus, financial

resources are the integral part of business enterprise and it is the duty of senior authority to

ensure that they make optimum utilisation of available resources and generate desired results and

outcomes (Cunningham, 2006). In this context, current report focuses on economic analysis of

Sweet Menu Restaurant Ltd which is one the its own kind of restaurant in Gants Hills in East

London. With recent success top level management of restaurant are planning to open two new

branches in popular places of London with the aim of attracting large number of customers

through hygiene and delicious intercontinental offerings. In this regard, various sources of funds

has been analysed to raise the amount between £300000 and £500000. Further, implications

associated with the different sources has been focused on and importance of financial planning

for the betterment of business operations. Thereafter, different stakeholder of cited restaurant has

been identified and their importance in decision making. Along with this, investment appraisal

techniques have been used to evaluate the feasibility and reliability of the proposals for the future

expansion and lastly, with the help of ratio analysis performance of cited firm is compared with

its competitor (Blue Island Restaurant).

TASK 1

1.1 Different sources of finance for Sweet Menu Restaurant

As per the present provided case, Sweet Menu Restaurant is planning to enhance its

business functioning by opening two new branches in popular places of London. In order to do

so, huge amount between £300000 to £500000 is required by the management and for which

they can make use of following sources of finance:

Bank Loan: At present in UK there are several financial institutions which provide

corporate loan to the firms so that they can enhance their business operations and attain

long term sustainability (Narayananand Nanda, 2004). Considering the debt financing it

is one of the most feasible options available to the management of Sweet Menu

Restaurant. The main benefit of this source is that it is available on the basis of mere

formalities as well as repayment of loan is based on monthly instalment which is feasible

for the SME like Sweet Menu Restaurant to repay.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hire purchase and leasing: These are the sources categorized under short and medium

term financing. With the use of this, restaurant can easily acquire machinery of their

choice and enhance the technological aspect so that customers of restaurant get new

experience (Thomas, 2008). However, the main advantage of these sources is that they

are available at feasible monthly instalments.

Venture Capitalist: Owners of the cited restaurant has the duty to influence venture

capitalist so that investment can be raised. One of the major benefits of this source is that,

capitalist have lesser interest in the functioning of business as compared to shareholders

(Curry, 2013). But it is essential to provide accurate and reliable information to these

people so that they can make smart decision regarding future investments.

Retained earnings: It is another major internal source that top level management of Sweet

Menu can use in order to raise funds for the future expansion. However, advantage of this

source is that it is already kept reserved for the future contingency and does not raise any

debt. Along with this, firm does not raise any liability of repaying it.

Sale of fixed assets: Considering the short term financial needs, sales of fixed assets is

appropriate source of finance. It is the duty of senior authority of Sweet Menu Restaurant

to focus on those assets which are of no use or less use in the functioning of business

should be sold to raise the money for buying new technology or machinery for the new

restaurants. But contradicting to this, once the asset is being sold management cannot

make use of it again.

Third party investment: In order to raise funds from the market it is important for the

senior authority of Sweet Menu Restaurant to influence investors for investing the

money. The advantage of this source is that third party investors have very little interest

in the functioning of firm but despite of this, management has to provide them accurate

and reliable information about the functioning so that they can assess risks and

uncertainties and accordingly make smart and effective decisions.

Government grants: It is considered as the legal system in which government of UK

provide monetary rewards to those entrepreneurs who are starting a business or

expanding the operations. But in order raise the funds from grants wide range of past and

current information of Sweet Menu Restaurant has to be provided to the government

authority so that they can analyse and accordingly make the decisions.

2

term financing. With the use of this, restaurant can easily acquire machinery of their

choice and enhance the technological aspect so that customers of restaurant get new

experience (Thomas, 2008). However, the main advantage of these sources is that they

are available at feasible monthly instalments.

Venture Capitalist: Owners of the cited restaurant has the duty to influence venture

capitalist so that investment can be raised. One of the major benefits of this source is that,

capitalist have lesser interest in the functioning of business as compared to shareholders

(Curry, 2013). But it is essential to provide accurate and reliable information to these

people so that they can make smart decision regarding future investments.

Retained earnings: It is another major internal source that top level management of Sweet

Menu can use in order to raise funds for the future expansion. However, advantage of this

source is that it is already kept reserved for the future contingency and does not raise any

debt. Along with this, firm does not raise any liability of repaying it.

Sale of fixed assets: Considering the short term financial needs, sales of fixed assets is

appropriate source of finance. It is the duty of senior authority of Sweet Menu Restaurant

to focus on those assets which are of no use or less use in the functioning of business

should be sold to raise the money for buying new technology or machinery for the new

restaurants. But contradicting to this, once the asset is being sold management cannot

make use of it again.

Third party investment: In order to raise funds from the market it is important for the

senior authority of Sweet Menu Restaurant to influence investors for investing the

money. The advantage of this source is that third party investors have very little interest

in the functioning of firm but despite of this, management has to provide them accurate

and reliable information about the functioning so that they can assess risks and

uncertainties and accordingly make smart and effective decisions.

Government grants: It is considered as the legal system in which government of UK

provide monetary rewards to those entrepreneurs who are starting a business or

expanding the operations. But in order raise the funds from grants wide range of past and

current information of Sweet Menu Restaurant has to be provided to the government

authority so that they can analyse and accordingly make the decisions.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Issue of shares: Operating at small and medium sized business, top level management can

issue the shares of the firm within the market. In this Sweet Menu Restaurant needs to

register as the IPO (Initial Public Offerings). Through the help of this firm can attract

numerous amount of shareholders to buy shares and raise funds for the firm. The main

pros of this source is that large amount of funds is raise without raising major liabilities.

However, there is liability of paying dividends but that in case when Sweet Menu

Restaurant generates profits.

1.2 Implications of Sources

Different sources have different implications but it is the duty of senior authority to make

sure that they evaluate each and every sources and then make smart decision. Following are the

implications of above stated sources:

Bank loan: In terms of legal, with the help of legal formalities cited restaurant can raise

funds but have to deposit collateral security. While after the completion of legal

documents, money can be used by owners in any form. But for raising it management has

to deposited collateral security.

Venture capitalist: There is no legal implications but on the basis of terms and conditions

ownership will vary (Ismail and et.al, 2005). Whereas, liabilities of third party are not

fully settled company is considered as insolvent.

Hire purchase and leasing: There are no major legal implications associated with it as

management has to complete legal paperwork. Whereas, after the last instalment is settled

ownership is transferred to the owner. Along with this, if Sweet Menu is unable to pay

the leasing amount it may lead to the loss for hire purchasing institution.

Retained earnings: The major legal implication associated with this source is that,

restriction from shareholders may cause hindrance for the management to make use of

reserved amount. However, it is because it will reduce the return on investment

(Dividend) for the shareholders. Along with this, if accompany is unable to make

optimum utilisation of this source that it can be considered as the loss for firm.

Sale of Fixed assets: There are not legal implications imposed on this source as it is the

decision of management whether to sell the asset or not. But after selling the asset

company will lose its ownership and will not be able to make use of it again.

3

issue the shares of the firm within the market. In this Sweet Menu Restaurant needs to

register as the IPO (Initial Public Offerings). Through the help of this firm can attract

numerous amount of shareholders to buy shares and raise funds for the firm. The main

pros of this source is that large amount of funds is raise without raising major liabilities.

However, there is liability of paying dividends but that in case when Sweet Menu

Restaurant generates profits.

1.2 Implications of Sources

Different sources have different implications but it is the duty of senior authority to make

sure that they evaluate each and every sources and then make smart decision. Following are the

implications of above stated sources:

Bank loan: In terms of legal, with the help of legal formalities cited restaurant can raise

funds but have to deposit collateral security. While after the completion of legal

documents, money can be used by owners in any form. But for raising it management has

to deposited collateral security.

Venture capitalist: There is no legal implications but on the basis of terms and conditions

ownership will vary (Ismail and et.al, 2005). Whereas, liabilities of third party are not

fully settled company is considered as insolvent.

Hire purchase and leasing: There are no major legal implications associated with it as

management has to complete legal paperwork. Whereas, after the last instalment is settled

ownership is transferred to the owner. Along with this, if Sweet Menu is unable to pay

the leasing amount it may lead to the loss for hire purchasing institution.

Retained earnings: The major legal implication associated with this source is that,

restriction from shareholders may cause hindrance for the management to make use of

reserved amount. However, it is because it will reduce the return on investment

(Dividend) for the shareholders. Along with this, if accompany is unable to make

optimum utilisation of this source that it can be considered as the loss for firm.

Sale of Fixed assets: There are not legal implications imposed on this source as it is the

decision of management whether to sell the asset or not. But after selling the asset

company will lose its ownership and will not be able to make use of it again.

3

Government grants: Top level management has to prepare appropriate and reliable

proposal and should be presented to the associated authority so that they can allow to

raise the funds. But once the proposal is rejected it is very difficult for the firm to raise

the funds again through this source.

Issue of shares: Company has to register in IPO to issue the shares as well as at the initial

stage attracting shareholders is quite tough as people invest in those shares which have

the reputation of generating higher returns. Along with this, restaurant is liable to pay the

dividends to its shareholder for satisfying their needs and wants.

1.3 Appropriate source of finance

In the present case, owners of cited restaurant are focusing on expanding business by

opening two new branches in popular places of London. For this variety of sources has been

analysed out of which the best suitable sources are bank loan and venture capitalist. Rationale

behind electing bank loan is that, in order to raise expected amount of capital this source can be

helpful. Furthermore, monthly instalment of repayment is feasible for SMEs to carry out

business operations and generate desired results and outcomes (Andersonand Coleman, 2000).On

the other hand, venture capitalist will be feasible because operating in such an attractive industry

as well as demand of inter-continental food in London is increasing day by day. Therefore,

influencing investor will be easy for the owners. Moreover, the interest of capitalist in business

operations is lesser then the shareholder therefore, Sweet Menu Restaurant can make use of

funds in suitable and reliable manner. Henceforth, these are the sources of funds recommended

to top level management of cited restaurant with the help of which they can easily carry out

expansion process.

TASK 2

2.1 Costs associated with different means of funding

While acquiring the funds through different means of sources there are several costs that

company has to bear. However, it is the duty of senior authority to make sure that they analyse

each and every aspect of sources as well as carry out cost benefit analysis of the sources to make

the best possible selection. Herein, bank loan and venture capitalist has been recommended as

the sources (Brighamand Houston, 2009). Therefore, managers of Sweet Menu Restaurant have

to bear certain costs associated with both of these sources. Bank loan assist in generate large

amount which is the need of restaurant but management have to bear the costs of monthly

4

proposal and should be presented to the associated authority so that they can allow to

raise the funds. But once the proposal is rejected it is very difficult for the firm to raise

the funds again through this source.

Issue of shares: Company has to register in IPO to issue the shares as well as at the initial

stage attracting shareholders is quite tough as people invest in those shares which have

the reputation of generating higher returns. Along with this, restaurant is liable to pay the

dividends to its shareholder for satisfying their needs and wants.

1.3 Appropriate source of finance

In the present case, owners of cited restaurant are focusing on expanding business by

opening two new branches in popular places of London. For this variety of sources has been

analysed out of which the best suitable sources are bank loan and venture capitalist. Rationale

behind electing bank loan is that, in order to raise expected amount of capital this source can be

helpful. Furthermore, monthly instalment of repayment is feasible for SMEs to carry out

business operations and generate desired results and outcomes (Andersonand Coleman, 2000).On

the other hand, venture capitalist will be feasible because operating in such an attractive industry

as well as demand of inter-continental food in London is increasing day by day. Therefore,

influencing investor will be easy for the owners. Moreover, the interest of capitalist in business

operations is lesser then the shareholder therefore, Sweet Menu Restaurant can make use of

funds in suitable and reliable manner. Henceforth, these are the sources of funds recommended

to top level management of cited restaurant with the help of which they can easily carry out

expansion process.

TASK 2

2.1 Costs associated with different means of funding

While acquiring the funds through different means of sources there are several costs that

company has to bear. However, it is the duty of senior authority to make sure that they analyse

each and every aspect of sources as well as carry out cost benefit analysis of the sources to make

the best possible selection. Herein, bank loan and venture capitalist has been recommended as

the sources (Brighamand Houston, 2009). Therefore, managers of Sweet Menu Restaurant have

to bear certain costs associated with both of these sources. Bank loan assist in generate large

amount which is the need of restaurant but management have to bear the costs of monthly

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

instalments of interest. Payment of principle amount is based on yearly basis which can affect the

entire financial position of the restaurant. Furthermore, it will raise the debt position of cited firm

as compared to the equity financing which is not suitable for the longer period of functioning.

On the other hand, venture capitalist will not raise major concerns but management have

to provide adequate and accurate information to the capitalist so that he/she can make decisions

regarding future contingency. Furthermore, capitalist requires equity of business so that in any

adverse situation he/she may regain mount through equity. As well as the control because

venture capitalist wants to mitigate risk that is associated with the future expansion of Sweet

Menu Restaurant.

2.2 Importance of Financial Planning

In general it can be defined as the process of meeting goals of business enterprise by

making proper management of funds or money. It is the process of defining objectives, policies,

procedures and budgets regarding different activities of business concern. Herein, top level

management of Sweet Menu Restaurant is planning to expand business thus; financial planning

is of great use (Jury, 2012). Operating in such a competitive environment it is important to

manage and make optimum utilisation of funds for which financial planning is necessary.

Through the means of financial forecasting finance managers of Sweet Menu Restaurant can

easily identify the suitable reliable sources of funds available and accordingly make decisions

regarding selecting the appropriate sources for raising funds and carrying out expansion process

effectively. In addition to this, it will also assist in analysing the risks and uncertainties

associated with two locations so that potential measures can be employed accordingly. The

significance of financial planning is that it helps in managing the income generated by Sweet

Menu Restaurant more efficiently. Along with this, it leads to increase the cash inflow and

monitor the spending habits of managers so that expenses can be controlled (Kwok, 2002). In

context to capital of Sweet Menu Restaurant it will assist in building long term capital and

shaping the financial future. Furthermore, it assists in identifying different investment

opportunities so that expansion of business can be made and long term sustainability can be

achieved.

5

entire financial position of the restaurant. Furthermore, it will raise the debt position of cited firm

as compared to the equity financing which is not suitable for the longer period of functioning.

On the other hand, venture capitalist will not raise major concerns but management have

to provide adequate and accurate information to the capitalist so that he/she can make decisions

regarding future contingency. Furthermore, capitalist requires equity of business so that in any

adverse situation he/she may regain mount through equity. As well as the control because

venture capitalist wants to mitigate risk that is associated with the future expansion of Sweet

Menu Restaurant.

2.2 Importance of Financial Planning

In general it can be defined as the process of meeting goals of business enterprise by

making proper management of funds or money. It is the process of defining objectives, policies,

procedures and budgets regarding different activities of business concern. Herein, top level

management of Sweet Menu Restaurant is planning to expand business thus; financial planning

is of great use (Jury, 2012). Operating in such a competitive environment it is important to

manage and make optimum utilisation of funds for which financial planning is necessary.

Through the means of financial forecasting finance managers of Sweet Menu Restaurant can

easily identify the suitable reliable sources of funds available and accordingly make decisions

regarding selecting the appropriate sources for raising funds and carrying out expansion process

effectively. In addition to this, it will also assist in analysing the risks and uncertainties

associated with two locations so that potential measures can be employed accordingly. The

significance of financial planning is that it helps in managing the income generated by Sweet

Menu Restaurant more efficiently. Along with this, it leads to increase the cash inflow and

monitor the spending habits of managers so that expenses can be controlled (Kwok, 2002). In

context to capital of Sweet Menu Restaurant it will assist in building long term capital and

shaping the financial future. Furthermore, it assists in identifying different investment

opportunities so that expansion of business can be made and long term sustainability can be

achieved.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Information needs of different decision makers that are associated with Sweet Menu

Restaurant

In order to carry out the operations of business there are several stakeholders associated

with the firm. However, the main purpose of these stakeholders is to carry out their part in

effective manner so that overall aim and objectives of the business can be achieved. But for that

they require adequate amount of information on the basis of which they can be carry out their

part (Jakhotiya, 2002). Following are the stakeholders associated with Sweet Menu Restaurant

and the information required by them for making suitable decisions:

Employees: These are the integral stakeholder of business and require accurate and

appropriate financial information of business so that decision regarding future growth

opportunities can be made. Through the means of financial statements, employee

understands about the retention, salaries and other monetary information (Kawai,

Mayesand Morgan, 2012).

Management: Top level management are responsible for carrying out the operations of

business in effective and efficient manner. In this context, managerial level people

requires adequate amount of accurate information of Sweet Menu Restaurant.

Information is related to position of working capital, debt to equity position and

availability of assets etc. so that strategies can be developed accordingly and fruitful

results can be achieved.

Suppliers and Trade Creditors: Dealing in such a competitive environment, Sweet Menu

Restaurant has to maintain its relationship with suppliers in order to acquire quality of

raw materials. With the aim of serving fresh and hygiene inter-continental food to

customers it is important for maintain relationship with suppliers (Weil, 2012). In against

to it, suppliers require the information to judge the capability of Sweet Menu Restaurant

in paying its debt as well as deciding the credit period terms.

Lenders: Bank and other investors critically analyse the position of Sweet Menu

Restaurant through its financial statements in regards to understand the ability of firm in

repaying the borrowing within the specific period or not. Investors evaluate the

statements to understand inflows and outflows of the firm so that they can make decision

regarding return on investments.

6

Restaurant

In order to carry out the operations of business there are several stakeholders associated

with the firm. However, the main purpose of these stakeholders is to carry out their part in

effective manner so that overall aim and objectives of the business can be achieved. But for that

they require adequate amount of information on the basis of which they can be carry out their

part (Jakhotiya, 2002). Following are the stakeholders associated with Sweet Menu Restaurant

and the information required by them for making suitable decisions:

Employees: These are the integral stakeholder of business and require accurate and

appropriate financial information of business so that decision regarding future growth

opportunities can be made. Through the means of financial statements, employee

understands about the retention, salaries and other monetary information (Kawai,

Mayesand Morgan, 2012).

Management: Top level management are responsible for carrying out the operations of

business in effective and efficient manner. In this context, managerial level people

requires adequate amount of accurate information of Sweet Menu Restaurant.

Information is related to position of working capital, debt to equity position and

availability of assets etc. so that strategies can be developed accordingly and fruitful

results can be achieved.

Suppliers and Trade Creditors: Dealing in such a competitive environment, Sweet Menu

Restaurant has to maintain its relationship with suppliers in order to acquire quality of

raw materials. With the aim of serving fresh and hygiene inter-continental food to

customers it is important for maintain relationship with suppliers (Weil, 2012). In against

to it, suppliers require the information to judge the capability of Sweet Menu Restaurant

in paying its debt as well as deciding the credit period terms.

Lenders: Bank and other investors critically analyse the position of Sweet Menu

Restaurant through its financial statements in regards to understand the ability of firm in

repaying the borrowing within the specific period or not. Investors evaluate the

statements to understand inflows and outflows of the firm so that they can make decision

regarding return on investments.

6

2.4 Impact of finance on the statements

In the present given scenario, top level management of Sweet Menu Restaurant is

planning to open two new branches within the London and for that they have been recommended

to bank loan and venture capital as the source of finance. Therefore, it is important to understand

the impact that these sources of funds will make on financial statements of the firm. In case of

bank loan, the amount raise will be recorded in the liability side of balance sheet which increases

the debt position of business (Brigham and Houston, 2009). Furthermore, the interest paid in

terms of monthly instalments will be shown in expenditure side of income statement. On the

other hand, venture capital source will increase the amount of share capital within balance sheet

as well as amount of cash will be increased the same. However, in against to its stakes of the

company are provided to capitalist which are written in the annual report for the future record.

Therefore, these are the impacts that these sources of finance will make on the financial

statement of Sweet Menu Restaurant if they adopted to raise funds for the future expansion.

TASK 3

3.1 Analyse budget

In general budget can be defined as the tool with the help of which managers can easily

analyse the inflow and outflow of the cash during the financial year. Further, it assists in

evaluating the risks and uncertainties associated with the functioning of firm in near future.

Herein, investigator concentrates on analysing the budget Blue Island Restaurant with the aim of

understanding the actual financial position (Broadbentand Cullen, 2012). On the basis of cash

budget it can be said that, the products offered by cited restaurant are generating reasonable

demand due to which fluctuating sales figures has been generated. In context to the outflow

during the month of September, Blue Island Restaurant was unable to meet the expenditure

through the cash sales because of increasing expenses like Van, furniture and fittings etc. But in

the October month restaurant was able to generate good sales which led in generating positive

closing balance of £3870. While in the month of November, increasing demand of food helps in

maintaining the positive closing balance which is feasible in maintaining position in such

competitive environment. Lastly, increasing expenditure again cost the Blue Island Restaurant to

attain negative closing balance. Therefore, it important for the senior authority of cites

Restaurant to indulge appropriate and feasible sales strategies so that revenue can be increased.

7

In the present given scenario, top level management of Sweet Menu Restaurant is

planning to open two new branches within the London and for that they have been recommended

to bank loan and venture capital as the source of finance. Therefore, it is important to understand

the impact that these sources of funds will make on financial statements of the firm. In case of

bank loan, the amount raise will be recorded in the liability side of balance sheet which increases

the debt position of business (Brigham and Houston, 2009). Furthermore, the interest paid in

terms of monthly instalments will be shown in expenditure side of income statement. On the

other hand, venture capital source will increase the amount of share capital within balance sheet

as well as amount of cash will be increased the same. However, in against to its stakes of the

company are provided to capitalist which are written in the annual report for the future record.

Therefore, these are the impacts that these sources of finance will make on the financial

statement of Sweet Menu Restaurant if they adopted to raise funds for the future expansion.

TASK 3

3.1 Analyse budget

In general budget can be defined as the tool with the help of which managers can easily

analyse the inflow and outflow of the cash during the financial year. Further, it assists in

evaluating the risks and uncertainties associated with the functioning of firm in near future.

Herein, investigator concentrates on analysing the budget Blue Island Restaurant with the aim of

understanding the actual financial position (Broadbentand Cullen, 2012). On the basis of cash

budget it can be said that, the products offered by cited restaurant are generating reasonable

demand due to which fluctuating sales figures has been generated. In context to the outflow

during the month of September, Blue Island Restaurant was unable to meet the expenditure

through the cash sales because of increasing expenses like Van, furniture and fittings etc. But in

the October month restaurant was able to generate good sales which led in generating positive

closing balance of £3870. While in the month of November, increasing demand of food helps in

maintaining the positive closing balance which is feasible in maintaining position in such

competitive environment. Lastly, increasing expenditure again cost the Blue Island Restaurant to

attain negative closing balance. Therefore, it important for the senior authority of cites

Restaurant to indulge appropriate and feasible sales strategies so that revenue can be increased.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

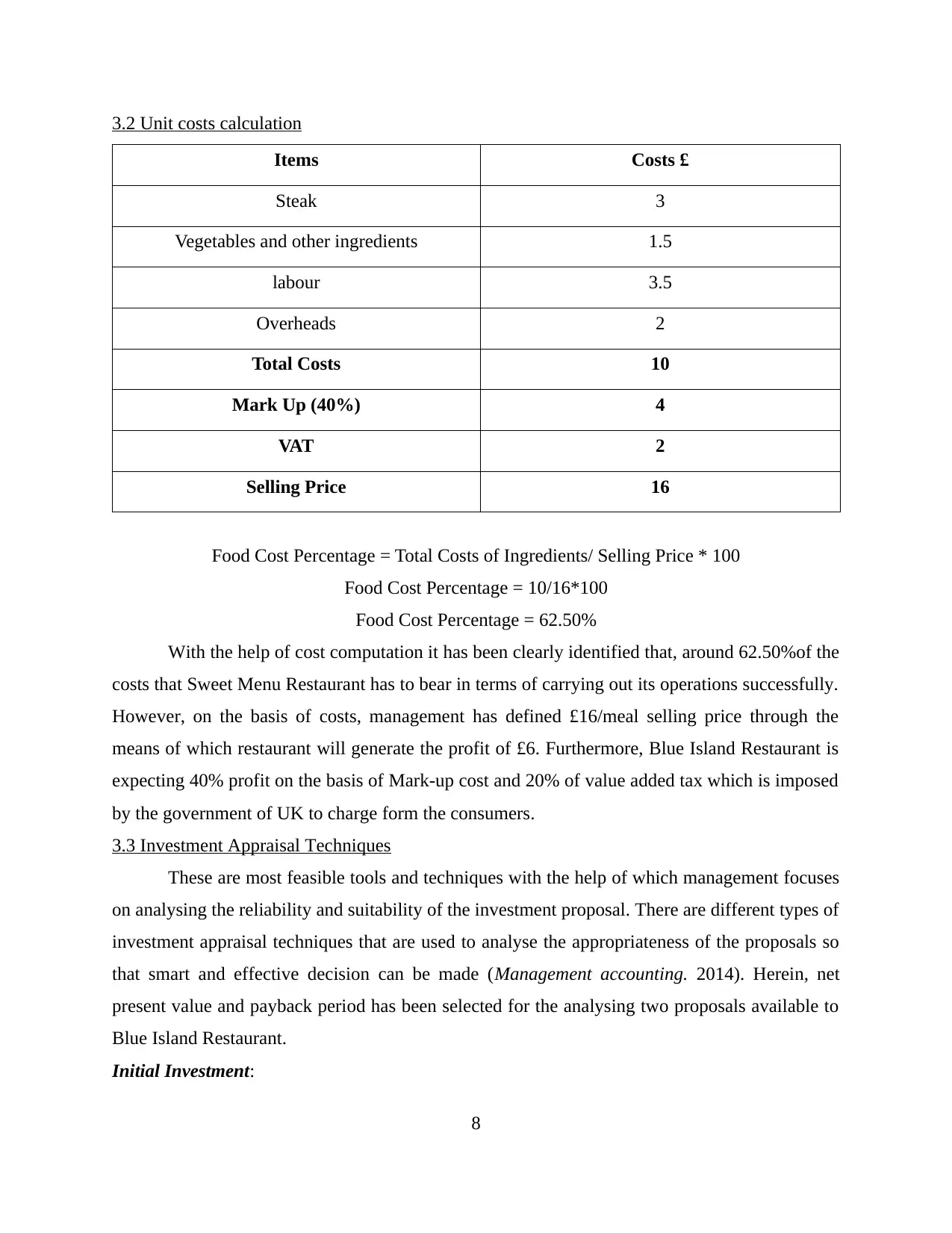

3.2 Unit costs calculation

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

Food Cost Percentage = Total Costs of Ingredients/ Selling Price * 100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

With the help of cost computation it has been clearly identified that, around 62.50%of the

costs that Sweet Menu Restaurant has to bear in terms of carrying out its operations successfully.

However, on the basis of costs, management has defined £16/meal selling price through the

means of which restaurant will generate the profit of £6. Furthermore, Blue Island Restaurant is

expecting 40% profit on the basis of Mark-up cost and 20% of value added tax which is imposed

by the government of UK to charge form the consumers.

3.3 Investment Appraisal Techniques

These are most feasible tools and techniques with the help of which management focuses

on analysing the reliability and suitability of the investment proposal. There are different types of

investment appraisal techniques that are used to analyse the appropriateness of the proposals so

that smart and effective decision can be made (Management accounting. 2014). Herein, net

present value and payback period has been selected for the analysing two proposals available to

Blue Island Restaurant.

Initial Investment:

8

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

Food Cost Percentage = Total Costs of Ingredients/ Selling Price * 100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

With the help of cost computation it has been clearly identified that, around 62.50%of the

costs that Sweet Menu Restaurant has to bear in terms of carrying out its operations successfully.

However, on the basis of costs, management has defined £16/meal selling price through the

means of which restaurant will generate the profit of £6. Furthermore, Blue Island Restaurant is

expecting 40% profit on the basis of Mark-up cost and 20% of value added tax which is imposed

by the government of UK to charge form the consumers.

3.3 Investment Appraisal Techniques

These are most feasible tools and techniques with the help of which management focuses

on analysing the reliability and suitability of the investment proposal. There are different types of

investment appraisal techniques that are used to analyse the appropriateness of the proposals so

that smart and effective decision can be made (Management accounting. 2014). Herein, net

present value and payback period has been selected for the analysing two proposals available to

Blue Island Restaurant.

Initial Investment:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

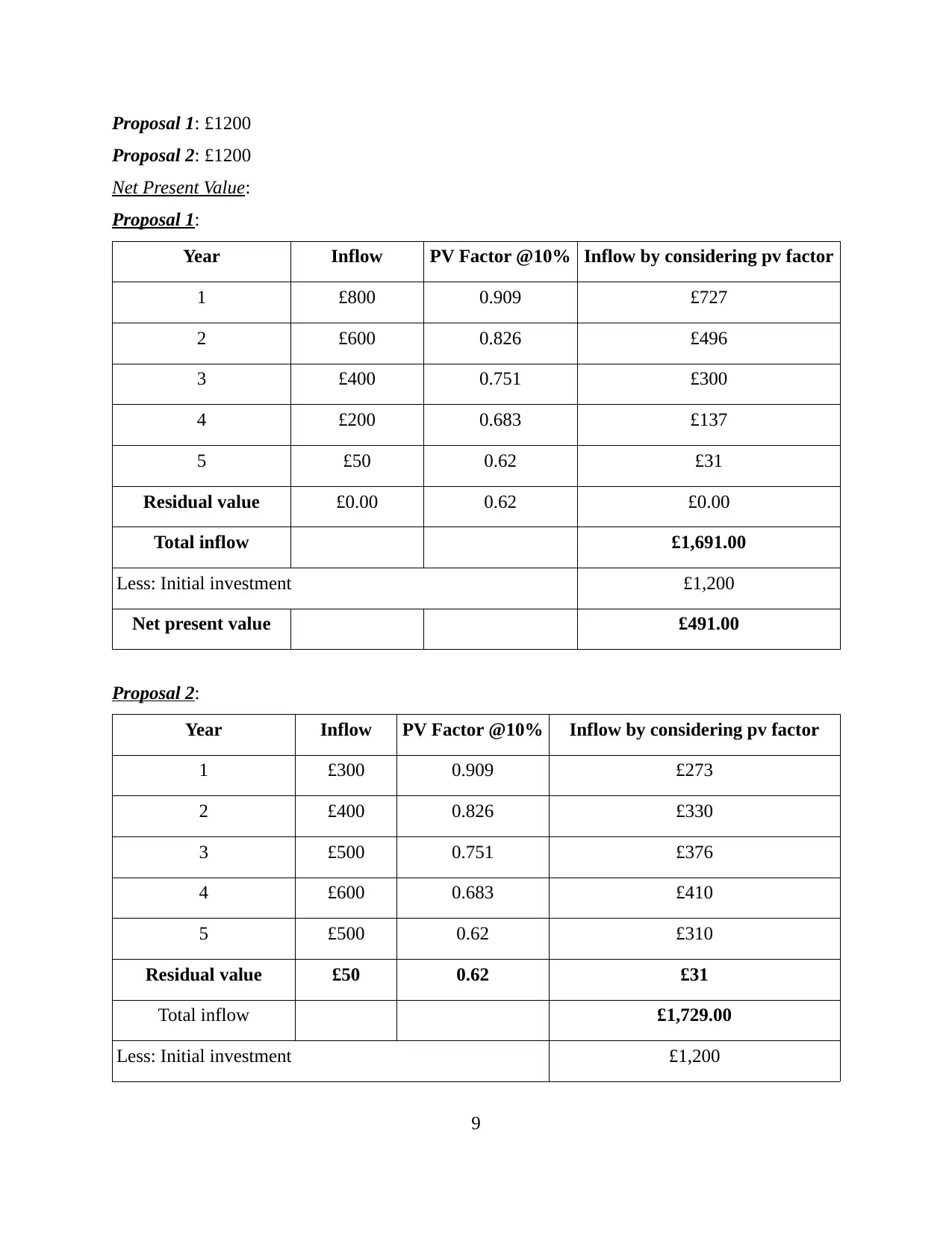

Proposal 1: £1200

Proposal 2: £1200

Net Present Value:

Proposal 1:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial investment £1,200

9

Proposal 2: £1200

Net Present Value:

Proposal 1:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial investment £1,200

9

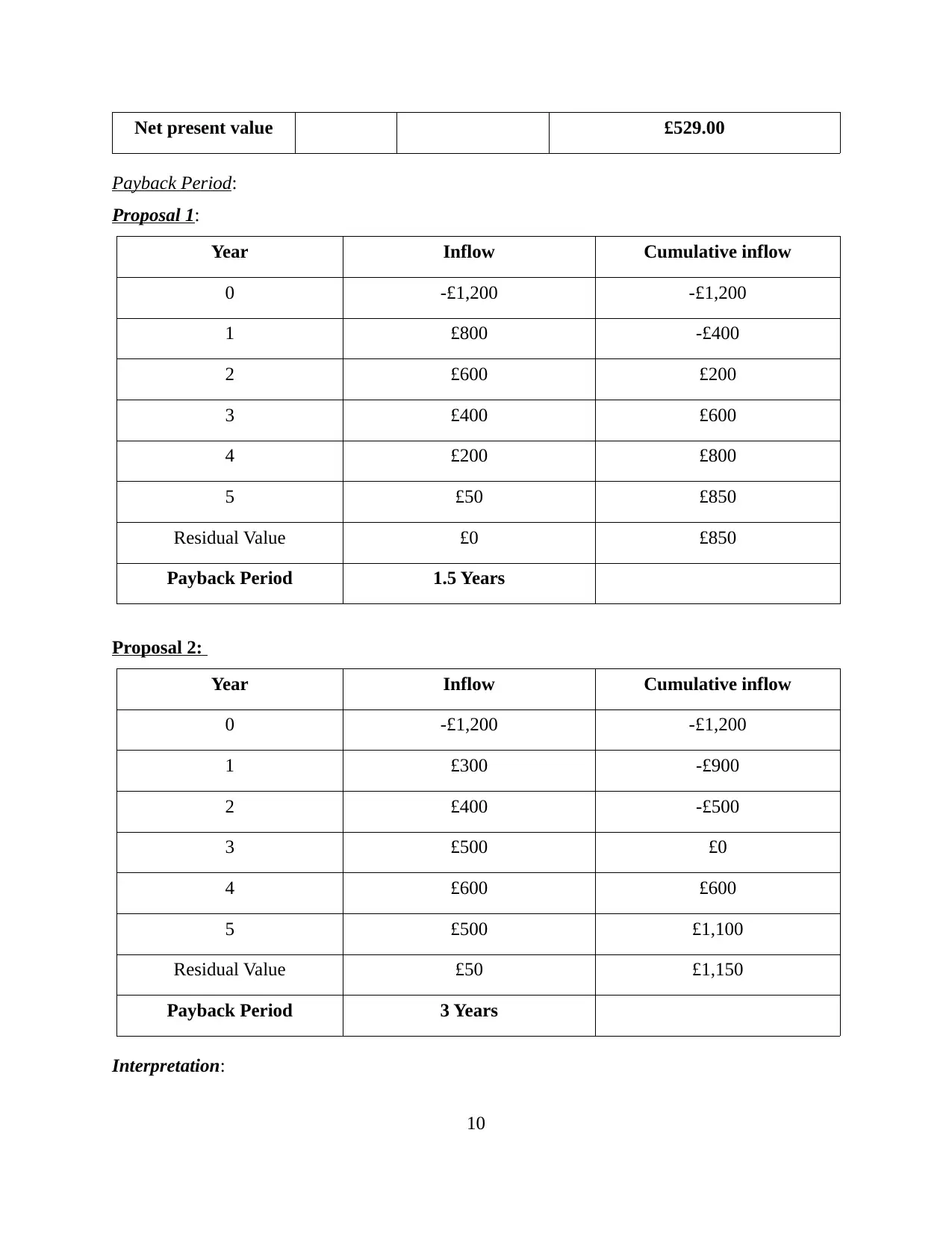

Net present value £529.00

Payback Period:

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

Interpretation:

10

Payback Period:

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

Interpretation:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.