Financial Decision Making: Analysis of Skanska Plc's Finances Report

VerifiedAdded on 2022/11/29

|26

|3938

|116

Report

AI Summary

This report provides a comprehensive financial analysis of Skanska Plc, a UK-based construction company. It explores the importance of accounting and finance functions within an organization, including financial and management accounting, the roles of audit and tax functions, and the finance department's responsibilities. The report delves into Skanska Plc's financial statements, calculating and analyzing key ratios such as ROCE, net profit margin, current ratio, and debtor/creditor payment periods to assess the company's financial position. It also examines the company's strengths, weaknesses, opportunities, and threats. Based on the analysis, the report offers recommendations regarding the suitability of providing debt to the company, offering a clear understanding of Skanska's financial health and performance.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report gives an insight into importance of accounting and finance function within an

organisation and does a ratio analysis to judge financial position of the company and

recommends whether it is suitable to be given debt by another company.

The report gives an insight into importance of accounting and finance function within an

organisation and does a ratio analysis to judge financial position of the company and

recommends whether it is suitable to be given debt by another company.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

Importance of accounting............................................................................................................4

Management accounting..............................................................................................................5

Role of the Audit function...........................................................................................................6

Tax function.................................................................................................................................6

Finance department......................................................................................................................7

Importance of finance within organisation..................................................................................8

Ratio Analysis.............................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

Importance of accounting............................................................................................................4

Management accounting..............................................................................................................5

Role of the Audit function...........................................................................................................6

Tax function.................................................................................................................................6

Finance department......................................................................................................................7

Importance of finance within organisation..................................................................................8

Ratio Analysis.............................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The report is based on the company Skanska Plc. It is a construction company based in UK

started in 1984. Importance of accounting and finance functions, duties and responsibility are

elaborated in the study. The financial statements are provided with calculation of ratios and

analysis. Skanska Plc operates in around 10 countries like Sweden, Norway, Finland, Denmark,

Poland, UK to name a few (Ballard and Elfving, 2020). As of May 2020, Skanska had 33,585

employees working and is considered a leading construction company in market with annual

turnover of SEK 172.846 billion. Talking about strengths of company, it is reputed for eco-

friendly construction measures and has employees ownership programme, its weaknesses are it

has not been able to establish itself in developing nations, opportunities are that it has favourable

demographics in increasing urban hood and threats being uncertainty caused by Brexit and

increasing competition.

Importance of accounting

Financial Accounting : Accounts, as the name implies, keeps track of how much money comes

in and goes out of the business. It creates financial statements including general ledgers, balance

sheets, profit and loss statements, and so on to record financial transactions that occur over a set

period of time, such as annually or quarterly (Hall and O'Dwyer, 2017). These financial

statements will be used by management and shareholders who wish to invest in the business for

internal review. Some important statements are listed as below:

A) Income statement: This statement details all profits on cost of goods sold, as well as variable

and fixed costs, as well as overheads. The net profit or loss shows the sustainability over time,

whether it's quarterly or annually. Skanska Plc gives due importance to income statement

preparation (Nyathi and et.al., 2018).

B) Balance Sheet: It shows the assets and liabilities of the firm. It also delves into current assets

and liabilities, allowing investors to assess the company's current liquidity and solvency in the

market. It can also be used to measure net working capital, which is needed for a company's

The report is based on the company Skanska Plc. It is a construction company based in UK

started in 1984. Importance of accounting and finance functions, duties and responsibility are

elaborated in the study. The financial statements are provided with calculation of ratios and

analysis. Skanska Plc operates in around 10 countries like Sweden, Norway, Finland, Denmark,

Poland, UK to name a few (Ballard and Elfving, 2020). As of May 2020, Skanska had 33,585

employees working and is considered a leading construction company in market with annual

turnover of SEK 172.846 billion. Talking about strengths of company, it is reputed for eco-

friendly construction measures and has employees ownership programme, its weaknesses are it

has not been able to establish itself in developing nations, opportunities are that it has favourable

demographics in increasing urban hood and threats being uncertainty caused by Brexit and

increasing competition.

Importance of accounting

Financial Accounting : Accounts, as the name implies, keeps track of how much money comes

in and goes out of the business. It creates financial statements including general ledgers, balance

sheets, profit and loss statements, and so on to record financial transactions that occur over a set

period of time, such as annually or quarterly (Hall and O'Dwyer, 2017). These financial

statements will be used by management and shareholders who wish to invest in the business for

internal review. Some important statements are listed as below:

A) Income statement: This statement details all profits on cost of goods sold, as well as variable

and fixed costs, as well as overheads. The net profit or loss shows the sustainability over time,

whether it's quarterly or annually. Skanska Plc gives due importance to income statement

preparation (Nyathi and et.al., 2018).

B) Balance Sheet: It shows the assets and liabilities of the firm. It also delves into current assets

and liabilities, allowing investors to assess the company's current liquidity and solvency in the

market. It can also be used to measure net working capital, which is needed for a company's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operations. Annual report of the company Skanska signifies the Balance sheet describing its

assets, capital and liabilities.

C) Ledgers: Also known as general ledgers, ledgers document debit and credit transactions for

the company. For the firm, debit records all inbound transactions and credit records all outbound

transactions.

Management accounting

It is the internal accounting reports prepared from managers point of view to identify, measure

and interpret various parameters which can help fulfil the short term as well as the long-term

obligations. They are helpful for the internal stakeholders of the company. One of the important

management accounting function is of variance analysis and budgeting.

i) Variance analysis: It helps in finding the variance or deviation which has happened in

performance of departments from achieving the targets and the deviation which has

been caused (Hall and O'Dwyer, 2017). It helps realise the factors which caused the

variance and also identifies achievements of departments who were able to achieve

targets within budgetary constraints.

ii) Budgeting: An important tool of reporting in management accounting, it reflects on

planning of finances by a company and allotment of money for various departmental

operations. It can be done in ways like incremental budgeting and zero-based

budgeting method. Skanska Plc has used these methods for cost estimations in

various projects.

iii) Cost analysis: Through this method, companies are able to calculate per unit

production cost by dividing total production cost by number of units. This helps to set

prices of products too.

iv) Investment analysis: Through measures like NPV and IRR, Skanska is able to find the

profitability of projects before investing. Cost estimations using discount factor and

internal rate of return help in zeroing on the right return giving project.

assets, capital and liabilities.

C) Ledgers: Also known as general ledgers, ledgers document debit and credit transactions for

the company. For the firm, debit records all inbound transactions and credit records all outbound

transactions.

Management accounting

It is the internal accounting reports prepared from managers point of view to identify, measure

and interpret various parameters which can help fulfil the short term as well as the long-term

obligations. They are helpful for the internal stakeholders of the company. One of the important

management accounting function is of variance analysis and budgeting.

i) Variance analysis: It helps in finding the variance or deviation which has happened in

performance of departments from achieving the targets and the deviation which has

been caused (Hall and O'Dwyer, 2017). It helps realise the factors which caused the

variance and also identifies achievements of departments who were able to achieve

targets within budgetary constraints.

ii) Budgeting: An important tool of reporting in management accounting, it reflects on

planning of finances by a company and allotment of money for various departmental

operations. It can be done in ways like incremental budgeting and zero-based

budgeting method. Skanska Plc has used these methods for cost estimations in

various projects.

iii) Cost analysis: Through this method, companies are able to calculate per unit

production cost by dividing total production cost by number of units. This helps to set

prices of products too.

iv) Investment analysis: Through measures like NPV and IRR, Skanska is able to find the

profitability of projects before investing. Cost estimations using discount factor and

internal rate of return help in zeroing on the right return giving project.

Role of the Audit function

When doing business, a corporation must follow certain rules and regulations. Skanska's audit

department ensures that statutory rules are followed in order to prevent fines. Internal auditors

are employed by businesses to assess operational records and identify any mistakes that may

have crept in. Before the external audit, the executives are given instructions to correct the errors.

They also review financial statements for consistency and look at the company's targets to see if

any policy changes are needed to help the company meet its goals.

Tax function

Construction firms, such as Skanska, use different tax reporting methods. Profits and

expenditures for finished contracts are reported until the job is completed, allowing for tax

deferral before the project is completed. Percentage of Completion, on the other hand, is a great

way to tackle tax volatility because it tracks revenue and expenditures as per year earned. With

the approval of the Internal Revenue Service, businesses may also defer taxes (Nyathi and et.al.,

2018). Here is a discussion of ways which help save taxes:

i)Job costing

Skanska, as a construction firm, has contracts that cover a wide range of projects or jobs.

Accounting for them all at once can be a difficult task because they all have different costs and

expenditures. Employment costing allows you to account for both direct and indirect costs as

well as income for each job individually, removing any doubt. This has aided the corporation in

covering all operating costs and calculating project profitability. Internal accountants can quickly

review financial statements and file tax returns thanks to this well-organized system.

ii)Cash basis

Skanska has benefited from cash basis accounting because it allows them to report sales and

expenditures as they occur in a contract, simplifying the process of maintaining records. But, if

the contract is multi-year, the expenses must be spread equally over the years (Dumay and et.al.,

2018).

When doing business, a corporation must follow certain rules and regulations. Skanska's audit

department ensures that statutory rules are followed in order to prevent fines. Internal auditors

are employed by businesses to assess operational records and identify any mistakes that may

have crept in. Before the external audit, the executives are given instructions to correct the errors.

They also review financial statements for consistency and look at the company's targets to see if

any policy changes are needed to help the company meet its goals.

Tax function

Construction firms, such as Skanska, use different tax reporting methods. Profits and

expenditures for finished contracts are reported until the job is completed, allowing for tax

deferral before the project is completed. Percentage of Completion, on the other hand, is a great

way to tackle tax volatility because it tracks revenue and expenditures as per year earned. With

the approval of the Internal Revenue Service, businesses may also defer taxes (Nyathi and et.al.,

2018). Here is a discussion of ways which help save taxes:

i)Job costing

Skanska, as a construction firm, has contracts that cover a wide range of projects or jobs.

Accounting for them all at once can be a difficult task because they all have different costs and

expenditures. Employment costing allows you to account for both direct and indirect costs as

well as income for each job individually, removing any doubt. This has aided the corporation in

covering all operating costs and calculating project profitability. Internal accountants can quickly

review financial statements and file tax returns thanks to this well-organized system.

ii)Cash basis

Skanska has benefited from cash basis accounting because it allows them to report sales and

expenditures as they occur in a contract, simplifying the process of maintaining records. But, if

the contract is multi-year, the expenses must be spread equally over the years (Dumay and et.al.,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

iii)Percentage of completion

Since contracts vary in duration, matching final revenues and expenditures may be challenging.

Here comes Skanska's Percentage of Completion method, which aids the company in

overcoming this obstacle. There is an estimate of expenses made on a specific job in the project,

and then the real expenses incurred in completing the job are taken and split by the former to

determine the benefit or loss. This aids in determining whether or not a project is on track. If

there is a benefit, it is compounded by the percentage of the project that has yet to be completed

to calculate the total gross profit. This has shown consistent results with little variation.

Finance department

Investment function

Managers at Skanska determine how to collect money for the company's activities. To raise

money for the company's activities, the company will issue IPOs, shares, and debentures in the

market. Managers at Skanska ensure that there is a balance of equity and debt, as relying too

heavily on debt could lead to potential solvency issues. Debt may take the form of a bank loan

from the company's bank, a credit card issued by a group, and so on (Loscher. and Kaiser,

2020).

Function of financing

As a company generates revenue on a daily basis, it is important to properly allocate funds to

areas such as outstanding payments, bills, equipment and raw material financing, machinery

financing, paying labour, and suppliers, as well as delegating funds to different parts within the

organisation. Skanska can assign funds to the appropriate sections and keep regular records with

the help of good operating finance software. The funds delegated in increase or decrease mode

are also matched using previous financials.

Dividends function

Skanska is required to pay a portion of its earnings to its investors on an annual basis. The sum to

be given is determined by the managers using estimates based on the shareholder's stake. This is

Since contracts vary in duration, matching final revenues and expenditures may be challenging.

Here comes Skanska's Percentage of Completion method, which aids the company in

overcoming this obstacle. There is an estimate of expenses made on a specific job in the project,

and then the real expenses incurred in completing the job are taken and split by the former to

determine the benefit or loss. This aids in determining whether or not a project is on track. If

there is a benefit, it is compounded by the percentage of the project that has yet to be completed

to calculate the total gross profit. This has shown consistent results with little variation.

Finance department

Investment function

Managers at Skanska determine how to collect money for the company's activities. To raise

money for the company's activities, the company will issue IPOs, shares, and debentures in the

market. Managers at Skanska ensure that there is a balance of equity and debt, as relying too

heavily on debt could lead to potential solvency issues. Debt may take the form of a bank loan

from the company's bank, a credit card issued by a group, and so on (Loscher. and Kaiser,

2020).

Function of financing

As a company generates revenue on a daily basis, it is important to properly allocate funds to

areas such as outstanding payments, bills, equipment and raw material financing, machinery

financing, paying labour, and suppliers, as well as delegating funds to different parts within the

organisation. Skanska can assign funds to the appropriate sections and keep regular records with

the help of good operating finance software. The funds delegated in increase or decrease mode

are also matched using previous financials.

Dividends function

Skanska is required to pay a portion of its earnings to its investors on an annual basis. The sum to

be given is determined by the managers using estimates based on the shareholder's stake. This is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

dividend income, which is deducted from gross profit. Since there are so many investors,

financial calculations are performed with the aid of technology to properly distribute the funds.

Working Capital function

Skanska manages its working capital in such a way that neither surplus funds nor cash shortages

are recorded. Excess funds mean that resources aren't being used as efficiently as they can be for

day-to-day operations. Profits can be generated if resources are used to their full potential. Lower

funds indicate that the company is unable to manage capital for day-to-day activities and that the

company's liquidity is limited (Dumay and et.al., 2018).

Importance of finance within organisation

The importance can be gauged from the following points:

a) Financial planning: The finance manager at Skanska Plc is responsible for planning

financial activities and using resources in the organisation. They use the data to know the

needs and priorities of organisation and also the economic situation and planning and

budgeting for same.

b) Financial decision and control: They play important role in financial decision making and

controlling the finances in organisation. Usage of techniques like analysis of ratios,

financial forecasting, analysis of profit and loss are done in finance function of Skanska

Plc.

c) Capital management: The responsibility of financial management is estimation of capital

requirements of the company at regular intervals, determining the capital structure and

composition and making choice of source of funding for needs of capital.

d) Allocation of financial resources: Financial management sees that financial resources of

organisation are used and are investment is done effectively and also in efficient manner

for making the organisation profitable and sustainable and viable for the long run

(Loscher and Kaiser, 2020).

e) Cash flow management: It is important for the organisation to have working capital

which is sufficient and the cash flow to meet the operational expenses and emergency.

financial calculations are performed with the aid of technology to properly distribute the funds.

Working Capital function

Skanska manages its working capital in such a way that neither surplus funds nor cash shortages

are recorded. Excess funds mean that resources aren't being used as efficiently as they can be for

day-to-day operations. Profits can be generated if resources are used to their full potential. Lower

funds indicate that the company is unable to manage capital for day-to-day activities and that the

company's liquidity is limited (Dumay and et.al., 2018).

Importance of finance within organisation

The importance can be gauged from the following points:

a) Financial planning: The finance manager at Skanska Plc is responsible for planning

financial activities and using resources in the organisation. They use the data to know the

needs and priorities of organisation and also the economic situation and planning and

budgeting for same.

b) Financial decision and control: They play important role in financial decision making and

controlling the finances in organisation. Usage of techniques like analysis of ratios,

financial forecasting, analysis of profit and loss are done in finance function of Skanska

Plc.

c) Capital management: The responsibility of financial management is estimation of capital

requirements of the company at regular intervals, determining the capital structure and

composition and making choice of source of funding for needs of capital.

d) Allocation of financial resources: Financial management sees that financial resources of

organisation are used and are investment is done effectively and also in efficient manner

for making the organisation profitable and sustainable and viable for the long run

(Loscher and Kaiser, 2020).

e) Cash flow management: It is important for the organisation to have working capital

which is sufficient and the cash flow to meet the operational expenses and emergency.

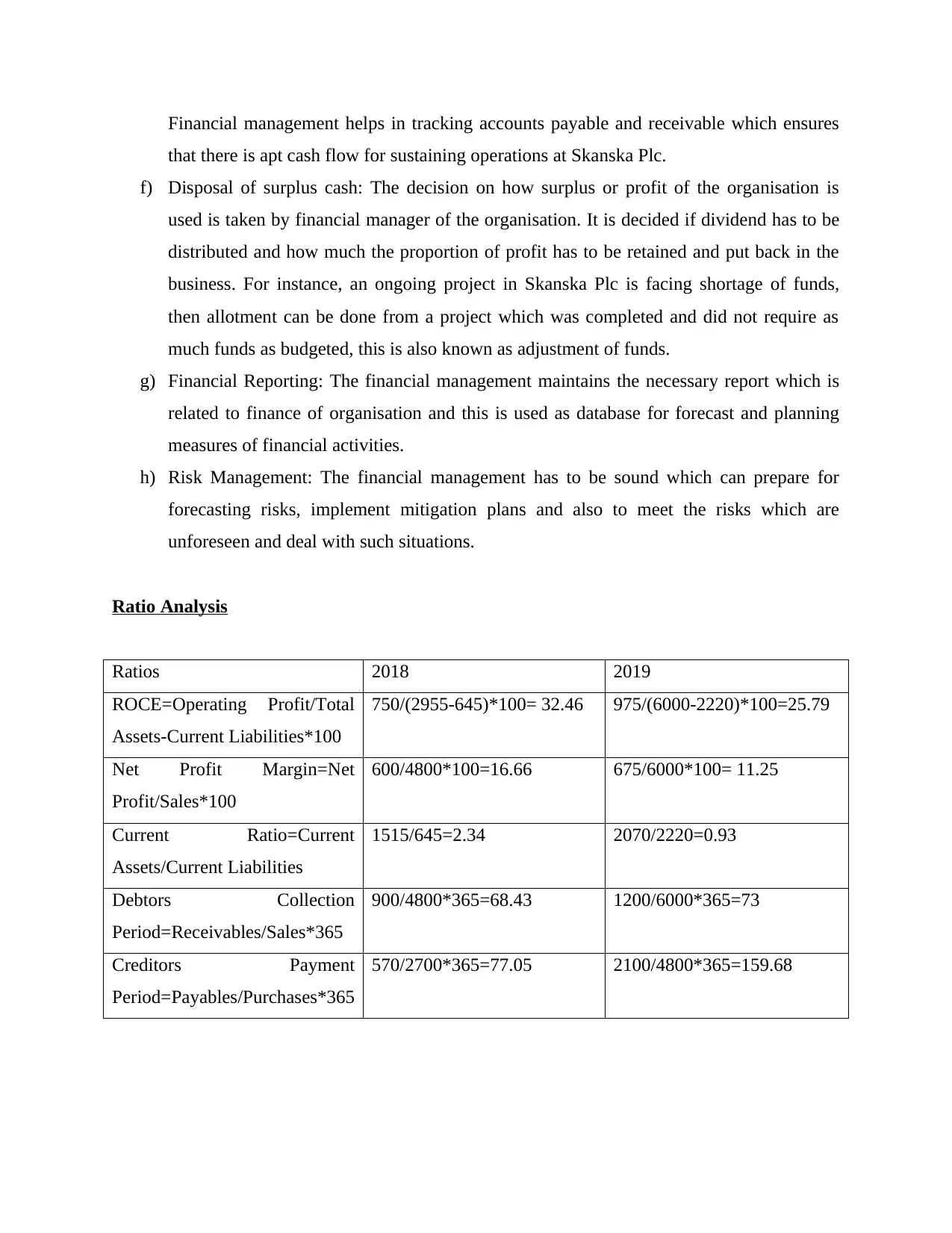

Financial management helps in tracking accounts payable and receivable which ensures

that there is apt cash flow for sustaining operations at Skanska Plc.

f) Disposal of surplus cash: The decision on how surplus or profit of the organisation is

used is taken by financial manager of the organisation. It is decided if dividend has to be

distributed and how much the proportion of profit has to be retained and put back in the

business. For instance, an ongoing project in Skanska Plc is facing shortage of funds,

then allotment can be done from a project which was completed and did not require as

much funds as budgeted, this is also known as adjustment of funds.

g) Financial Reporting: The financial management maintains the necessary report which is

related to finance of organisation and this is used as database for forecast and planning

measures of financial activities.

h) Risk Management: The financial management has to be sound which can prepare for

forecasting risks, implement mitigation plans and also to meet the risks which are

unforeseen and deal with such situations.

Ratio Analysis

Ratios 2018 2019

ROCE=Operating Profit/Total

Assets-Current Liabilities*100

750/(2955-645)*100= 32.46 975/(6000-2220)*100=25.79

Net Profit Margin=Net

Profit/Sales*100

600/4800*100=16.66 675/6000*100= 11.25

Current Ratio=Current

Assets/Current Liabilities

1515/645=2.34 2070/2220=0.93

Debtors Collection

Period=Receivables/Sales*365

900/4800*365=68.43 1200/6000*365=73

Creditors Payment

Period=Payables/Purchases*365

570/2700*365=77.05 2100/4800*365=159.68

that there is apt cash flow for sustaining operations at Skanska Plc.

f) Disposal of surplus cash: The decision on how surplus or profit of the organisation is

used is taken by financial manager of the organisation. It is decided if dividend has to be

distributed and how much the proportion of profit has to be retained and put back in the

business. For instance, an ongoing project in Skanska Plc is facing shortage of funds,

then allotment can be done from a project which was completed and did not require as

much funds as budgeted, this is also known as adjustment of funds.

g) Financial Reporting: The financial management maintains the necessary report which is

related to finance of organisation and this is used as database for forecast and planning

measures of financial activities.

h) Risk Management: The financial management has to be sound which can prepare for

forecasting risks, implement mitigation plans and also to meet the risks which are

unforeseen and deal with such situations.

Ratio Analysis

Ratios 2018 2019

ROCE=Operating Profit/Total

Assets-Current Liabilities*100

750/(2955-645)*100= 32.46 975/(6000-2220)*100=25.79

Net Profit Margin=Net

Profit/Sales*100

600/4800*100=16.66 675/6000*100= 11.25

Current Ratio=Current

Assets/Current Liabilities

1515/645=2.34 2070/2220=0.93

Debtors Collection

Period=Receivables/Sales*365

900/4800*365=68.43 1200/6000*365=73

Creditors Payment

Period=Payables/Purchases*365

570/2700*365=77.05 2100/4800*365=159.68

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on Capital Employed

This ratio shows how well a company's money has been used to produce profits. The numerator

is obtained by subtracting operating costs from gross profit. That's also known as Earnings

Before Interest and Taxes on the Stock, and it shows how much money the company makes from

its activities. Revenue is subtracted from cost of sales, and operating expenses are included.

Since current liabilities must be paid off and therefore cannot be considered as capital, capital

employed is calculated as current liabilities minus total assets (Karale, 2020).

Since ROCE considers shareholder equity as well as long-term debt as capital invested, it aids in

a more accurate financial analysis of businesses with significant debt.

Skanska's ROCE has decreased in 2019 compared to 2018, implying lower investor profitability.

Despite the fact that operating profit has increased as revenues have increased, total assets and

current liabilities have increased significantly. Present liabilities have risen as a result of higher

a/c payables. While a rise in assets is a positive sign, it can also indicate that the business is

carrying long-term debt. Second, to produce a substantial improvement in operating profits or

EBIT, the best possible asset utilisation is needed. The organisation would be able to produce a

higher ROCE as a result of this.

Net profit margin

The net profit or income earned from sales is displayed as a percentage and often as a decimal in

the ratio. Net profit is determined by subtracting operating costs from gross profit, then

subtracting interest and taxes again. This is often referred to as net earnings or income that has

been converted to profit. The numerator is sales or income, and it represents the dollar amount of

revenue that has been converted into profit for the company.

Investors look at the financials to see if the profit has been growing and if the business has been

able to raise sales and cover operating and overhead costs. The use of percentages to express net

profit allows companies of various sizes to be compared (Fombang and Adjasi, 2018).

In the case of Skanska, net profit decreased in 2019 compared to the previous year, which is a

bad indication since it indicates that the company's profits have decreased. The balance sheet

shows that overhead costs, such as purchases, have increased greatly, while operational expenses

have increased slightly.

This ratio shows how well a company's money has been used to produce profits. The numerator

is obtained by subtracting operating costs from gross profit. That's also known as Earnings

Before Interest and Taxes on the Stock, and it shows how much money the company makes from

its activities. Revenue is subtracted from cost of sales, and operating expenses are included.

Since current liabilities must be paid off and therefore cannot be considered as capital, capital

employed is calculated as current liabilities minus total assets (Karale, 2020).

Since ROCE considers shareholder equity as well as long-term debt as capital invested, it aids in

a more accurate financial analysis of businesses with significant debt.

Skanska's ROCE has decreased in 2019 compared to 2018, implying lower investor profitability.

Despite the fact that operating profit has increased as revenues have increased, total assets and

current liabilities have increased significantly. Present liabilities have risen as a result of higher

a/c payables. While a rise in assets is a positive sign, it can also indicate that the business is

carrying long-term debt. Second, to produce a substantial improvement in operating profits or

EBIT, the best possible asset utilisation is needed. The organisation would be able to produce a

higher ROCE as a result of this.

Net profit margin

The net profit or income earned from sales is displayed as a percentage and often as a decimal in

the ratio. Net profit is determined by subtracting operating costs from gross profit, then

subtracting interest and taxes again. This is often referred to as net earnings or income that has

been converted to profit. The numerator is sales or income, and it represents the dollar amount of

revenue that has been converted into profit for the company.

Investors look at the financials to see if the profit has been growing and if the business has been

able to raise sales and cover operating and overhead costs. The use of percentages to express net

profit allows companies of various sizes to be compared (Fombang and Adjasi, 2018).

In the case of Skanska, net profit decreased in 2019 compared to the previous year, which is a

bad indication since it indicates that the company's profits have decreased. The balance sheet

shows that overhead costs, such as purchases, have increased greatly, while operational expenses

have increased slightly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company will need to increase revenue while still attempting to cut operating costs. It will

also need to ensure that purchases are kept under control by reducing non-essential goods.

While net profits are down in 2019, gross profits are up, indicating that if the company

takes the right steps, it will be able to cover its overhead costs in the coming year.

Current ratio

It is a type of liquidity ratio that shows the current assets and liabilities of a business. It

demonstrates whether a business can pay its short-term obligations within a year, as well as

maximising current assets to offset current liabilities and debts, thus the net working capital.

Current assets are those that must be used or sold within a year in order to keep operations

running smoothly (Karale, 2020).

In an ideal case, the current ratio will indicate that the company's current liabilities can be

entirely covered by current assets. A current ratio greater than one is sufficient for demonstrating

a company's current liquidity; however, a much higher ratio indicates that the company is unable

to efficiently control its asset utilisation.

Skanska's current ratio has fallen below one since 2018, which is a bad indicator for the

company's liquidity. This indicates that a company's existing assets are smaller than its current

liabilities. Previously, the ratio was less than 3, which was good for the company's liquidity and

asset utilisation.

Despite the fact that current assets have grown, cash on hand has decreased, and trade payables

have risen dramatically, resulting in a substantial rise in current liabilities. To help pay off the

payables, the company would need to find new ways to raise cash.

A current ratio greater than one is preferred by most investors. To increase current ratio and thus

draw investment, Skanska would need to focus on increasing current assets.

Debtors Collection Period

Debtors payment period refers to the length of time it takes to recover receivables from debtors.

The less time it takes to recover a loan, the more cash the company has to use for operations or

possibly to pay off debt. The sales denominator is used to measure the ratio since the recovery

rate of receivables is based on the sales produced. The resultant of numerator and sales is

also need to ensure that purchases are kept under control by reducing non-essential goods.

While net profits are down in 2019, gross profits are up, indicating that if the company

takes the right steps, it will be able to cover its overhead costs in the coming year.

Current ratio

It is a type of liquidity ratio that shows the current assets and liabilities of a business. It

demonstrates whether a business can pay its short-term obligations within a year, as well as

maximising current assets to offset current liabilities and debts, thus the net working capital.

Current assets are those that must be used or sold within a year in order to keep operations

running smoothly (Karale, 2020).

In an ideal case, the current ratio will indicate that the company's current liabilities can be

entirely covered by current assets. A current ratio greater than one is sufficient for demonstrating

a company's current liquidity; however, a much higher ratio indicates that the company is unable

to efficiently control its asset utilisation.

Skanska's current ratio has fallen below one since 2018, which is a bad indicator for the

company's liquidity. This indicates that a company's existing assets are smaller than its current

liabilities. Previously, the ratio was less than 3, which was good for the company's liquidity and

asset utilisation.

Despite the fact that current assets have grown, cash on hand has decreased, and trade payables

have risen dramatically, resulting in a substantial rise in current liabilities. To help pay off the

payables, the company would need to find new ways to raise cash.

A current ratio greater than one is preferred by most investors. To increase current ratio and thus

draw investment, Skanska would need to focus on increasing current assets.

Debtors Collection Period

Debtors payment period refers to the length of time it takes to recover receivables from debtors.

The less time it takes to recover a loan, the more cash the company has to use for operations or

possibly to pay off debt. The sales denominator is used to measure the ratio since the recovery

rate of receivables is based on the sales produced. The resultant of numerator and sales is

multiplied by 365 since sales is taken on an annual basis. Days are used to represent it (Andjelic

and Vesic, 2017).

When placing an advance order for supplies or issuing debt, a business is aware of the time

frame for debt recovery. The productivity of the organisation would be shown if the receivables

are obtained on time. In the case of Skanska, since 2018, there has been a small rise in the time it

takes for debtors to be collected. A longer collection time means the company would have less

cash on hand right now than it would if the terms were normal. Despite the fact that there isn't

much of a rise, investors will not be put off. Investors like to invest in companies that do not

have a large number of outstanding payments because this can delay dividend payments.

Creditors payment period

It's a ratio that shows how long it takes a company to settle trade credits, and it's often referred to

as account payables. The ratio's denominator is transactions made by the corporation on a yearly

basis, so the measurement is performed annually. To earn or retain its credibility with its

creditors, the company must use credit for its activities and pay its dues on time in an ethical

manner.

Skanska's payment cycle has more than doubled in 2019, owing to a rise in both account

payables and transactions. It also indicates that the business is taking longer to pay its bills.

Changes must be made so that payments do not take longer to complete and payments can be

completed in a regular manner (Andjelic and Vesic, 2017).

Investors may see it as a way for a business to use credit for a longer period of time, but it raises

concerns about whether or not the company is experiencing a liquidity crunch. Such doubts will

grow as the current ratio falls. To meet potential cash needs, a company's relationship with its

creditors must be strong.

CONCLUSION

It can be seen through the ratios, Skanska performance has declined in 2019 comparing with

ratios like ROCE, Current ratio and the net profit. Its receivables time period has also increased

slightly while the accounts payable has increased significantly around double the time which

may signify that company has less of paying power for credit taken. According to Balance sheet,

it can be seen that sales of company has increased with slight increase in net profit but increase

and Vesic, 2017).

When placing an advance order for supplies or issuing debt, a business is aware of the time

frame for debt recovery. The productivity of the organisation would be shown if the receivables

are obtained on time. In the case of Skanska, since 2018, there has been a small rise in the time it

takes for debtors to be collected. A longer collection time means the company would have less

cash on hand right now than it would if the terms were normal. Despite the fact that there isn't

much of a rise, investors will not be put off. Investors like to invest in companies that do not

have a large number of outstanding payments because this can delay dividend payments.

Creditors payment period

It's a ratio that shows how long it takes a company to settle trade credits, and it's often referred to

as account payables. The ratio's denominator is transactions made by the corporation on a yearly

basis, so the measurement is performed annually. To earn or retain its credibility with its

creditors, the company must use credit for its activities and pay its dues on time in an ethical

manner.

Skanska's payment cycle has more than doubled in 2019, owing to a rise in both account

payables and transactions. It also indicates that the business is taking longer to pay its bills.

Changes must be made so that payments do not take longer to complete and payments can be

completed in a regular manner (Andjelic and Vesic, 2017).

Investors may see it as a way for a business to use credit for a longer period of time, but it raises

concerns about whether or not the company is experiencing a liquidity crunch. Such doubts will

grow as the current ratio falls. To meet potential cash needs, a company's relationship with its

creditors must be strong.

CONCLUSION

It can be seen through the ratios, Skanska performance has declined in 2019 comparing with

ratios like ROCE, Current ratio and the net profit. Its receivables time period has also increased

slightly while the accounts payable has increased significantly around double the time which

may signify that company has less of paying power for credit taken. According to Balance sheet,

it can be seen that sales of company has increased with slight increase in net profit but increase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.