Financial Analysis and Management Report: Tesco and Sainsbury

VerifiedAdded on 2020/01/15

|15

|3924

|276

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco and Sainsbury, two major retail organizations. It utilizes ratio analysis to evaluate their performance across various financial aspects, including profitability, liquidity, solvency, and efficiency. The analysis covers a five-year period (2012-2016), comparing key financial ratios such as gross profit margin, net profit margin, current ratio, quick ratio, debt-equity ratio, and asset turnover ratio. The report highlights the financial strengths and weaknesses of each company, offering insights into their ability to manage expenses, maintain liquidity, and generate sales. The findings are presented with tables, graphs, and a comparative analysis to provide a clear understanding of the companies' financial health. Furthermore, the report discusses the level of disclosure in the published annual reports of both companies, emphasizing the adoption of IFRS principles and the use of graphs, charts, and tables. The report also addresses how both retail organizations have addressed the needs of their stakeholders.

Financial Analysis and Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

Assignment 2........................................................................................................................................3

TASK 1.................................................................................................................................................3

Presenting the report on the financial performance of Tesco and Sainsbury ..................................3

TASK 2.................................................................................................................................................4

Giving advise upon the level of disclosure which is used by both the companies in the published

annual reports...................................................................................................................................4

TASK 3.................................................................................................................................................5

Stating the extent to which both the retail organizations have addressed the need of the different

stakeholders by presenting the report .............................................................................................5

CONCLUSION ...................................................................................................................................7

REFERENCES.....................................................................................................................................8

2

INTRODUCTION................................................................................................................................3

Assignment 2........................................................................................................................................3

TASK 1.................................................................................................................................................3

Presenting the report on the financial performance of Tesco and Sainsbury ..................................3

TASK 2.................................................................................................................................................4

Giving advise upon the level of disclosure which is used by both the companies in the published

annual reports...................................................................................................................................4

TASK 3.................................................................................................................................................5

Stating the extent to which both the retail organizations have addressed the need of the different

stakeholders by presenting the report .............................................................................................5

CONCLUSION ...................................................................................................................................7

REFERENCES.....................................................................................................................................8

2

INTRODUCTION

Financial analysis is the tool which enables business entity to evaluate the level to which

firm is liquid, solvent, stable and profitable. In this way, financial analysis and its outcomes provide

high level of assistance to the firm in framing competent strategic policies which aid in increasing

productivity and profitability of business. Further, business organization can also take strategic

actions by conducting financial analysis of competitors. In this context, report will describe the

manner through which financial report can be drafted and presented in a structure way. Besides this,

it will also describe the aspects of annual report which satisfy the information need of decision

maker to a large extent.

ASSIGNMENT 2

TASK 1

Presenting the report on the financial performance of Tesco and Sainsbury

Ratio analysis of Tesco and Sainsbury for the five years from 2012-2016

Profitability ratios

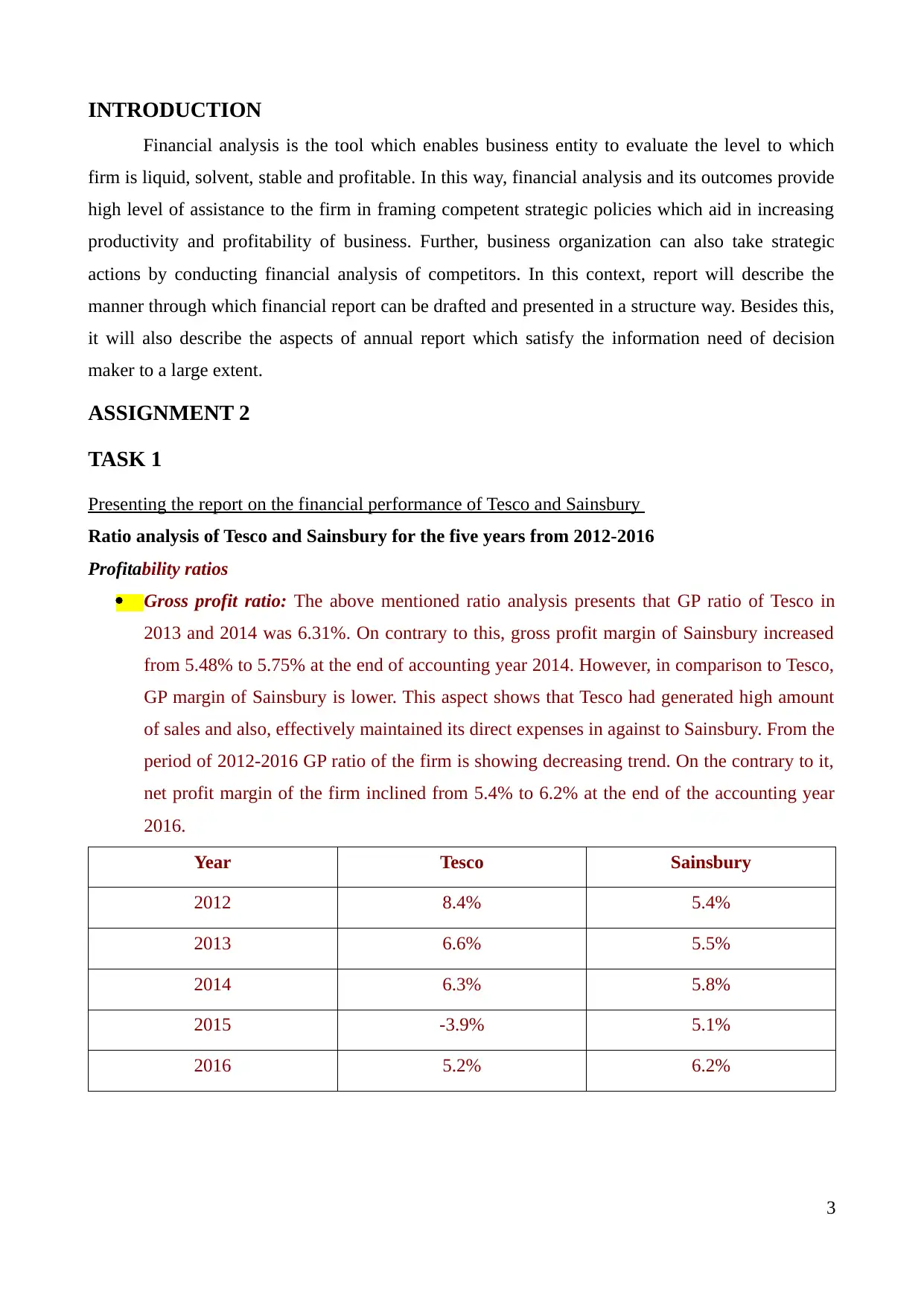

Gross profit ratio: The above mentioned ratio analysis presents that GP ratio of Tesco in

2013 and 2014 was 6.31%. On contrary to this, gross profit margin of Sainsbury increased

from 5.48% to 5.75% at the end of accounting year 2014. However, in comparison to Tesco,

GP margin of Sainsbury is lower. This aspect shows that Tesco had generated high amount

of sales and also, effectively maintained its direct expenses in against to Sainsbury. From the

period of 2012-2016 GP ratio of the firm is showing decreasing trend. On the contrary to it,

net profit margin of the firm inclined from 5.4% to 6.2% at the end of the accounting year

2016.

Year Tesco Sainsbury

2012 8.4% 5.4%

2013 6.6% 5.5%

2014 6.3% 5.8%

2015 -3.9% 5.1%

2016 5.2% 6.2%

3

Financial analysis is the tool which enables business entity to evaluate the level to which

firm is liquid, solvent, stable and profitable. In this way, financial analysis and its outcomes provide

high level of assistance to the firm in framing competent strategic policies which aid in increasing

productivity and profitability of business. Further, business organization can also take strategic

actions by conducting financial analysis of competitors. In this context, report will describe the

manner through which financial report can be drafted and presented in a structure way. Besides this,

it will also describe the aspects of annual report which satisfy the information need of decision

maker to a large extent.

ASSIGNMENT 2

TASK 1

Presenting the report on the financial performance of Tesco and Sainsbury

Ratio analysis of Tesco and Sainsbury for the five years from 2012-2016

Profitability ratios

Gross profit ratio: The above mentioned ratio analysis presents that GP ratio of Tesco in

2013 and 2014 was 6.31%. On contrary to this, gross profit margin of Sainsbury increased

from 5.48% to 5.75% at the end of accounting year 2014. However, in comparison to Tesco,

GP margin of Sainsbury is lower. This aspect shows that Tesco had generated high amount

of sales and also, effectively maintained its direct expenses in against to Sainsbury. From the

period of 2012-2016 GP ratio of the firm is showing decreasing trend. On the contrary to it,

net profit margin of the firm inclined from 5.4% to 6.2% at the end of the accounting year

2016.

Year Tesco Sainsbury

2012 8.4% 5.4%

2013 6.6% 5.5%

2014 6.3% 5.8%

2015 -3.9% 5.1%

2016 5.2% 6.2%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

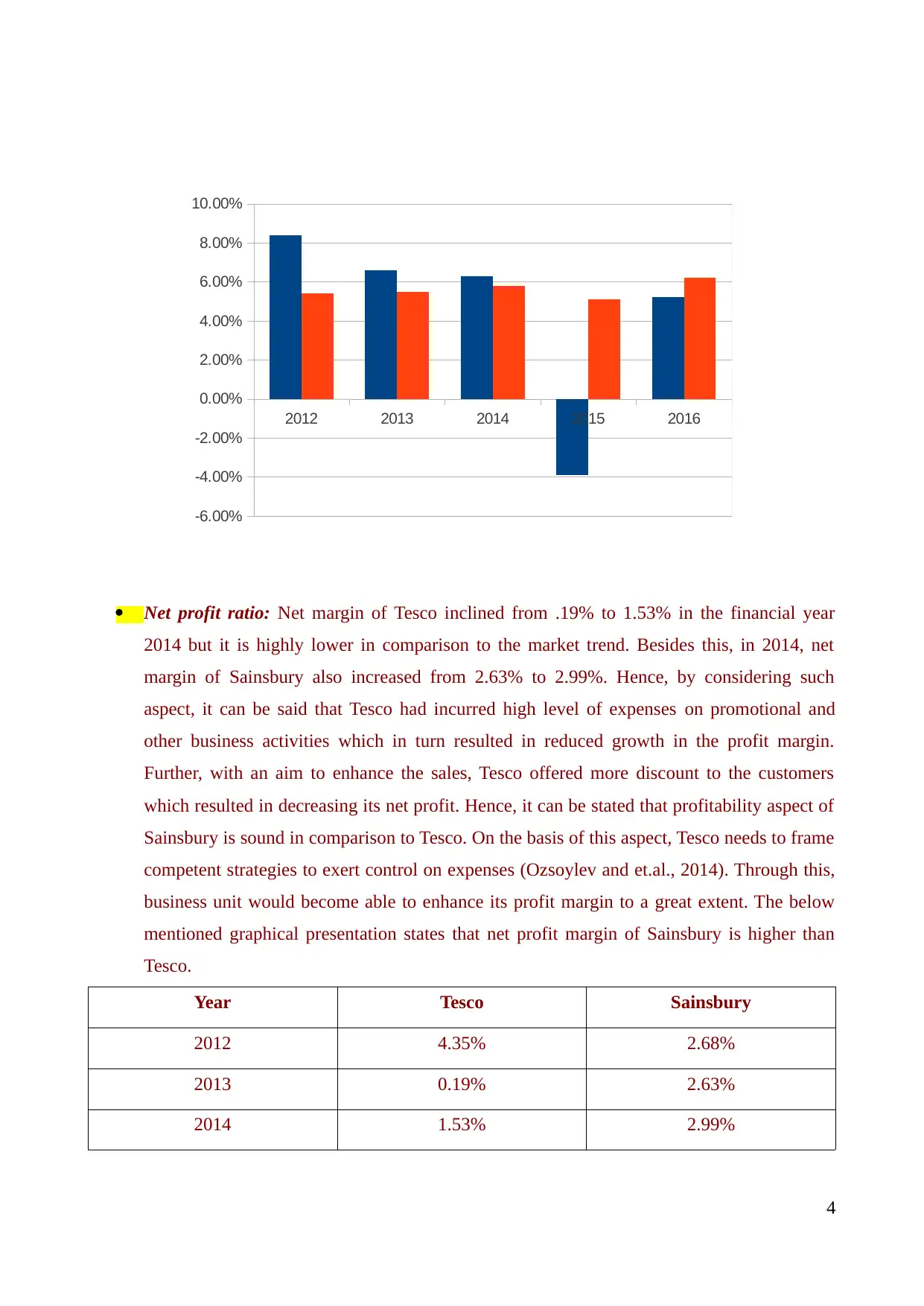

Net profit ratio: Net margin of Tesco inclined from .19% to 1.53% in the financial year

2014 but it is highly lower in comparison to the market trend. Besides this, in 2014, net

margin of Sainsbury also increased from 2.63% to 2.99%. Hence, by considering such

aspect, it can be said that Tesco had incurred high level of expenses on promotional and

other business activities which in turn resulted in reduced growth in the profit margin.

Further, with an aim to enhance the sales, Tesco offered more discount to the customers

which resulted in decreasing its net profit. Hence, it can be stated that profitability aspect of

Sainsbury is sound in comparison to Tesco. On the basis of this aspect, Tesco needs to frame

competent strategies to exert control on expenses (Ozsoylev and et.al., 2014). Through this,

business unit would become able to enhance its profit margin to a great extent. The below

mentioned graphical presentation states that net profit margin of Sainsbury is higher than

Tesco.

Year Tesco Sainsbury

2012 4.35% 2.68%

2013 0.19% 2.63%

2014 1.53% 2.99%

4

2012 2013 2014 2015 2016

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

2014 but it is highly lower in comparison to the market trend. Besides this, in 2014, net

margin of Sainsbury also increased from 2.63% to 2.99%. Hence, by considering such

aspect, it can be said that Tesco had incurred high level of expenses on promotional and

other business activities which in turn resulted in reduced growth in the profit margin.

Further, with an aim to enhance the sales, Tesco offered more discount to the customers

which resulted in decreasing its net profit. Hence, it can be stated that profitability aspect of

Sainsbury is sound in comparison to Tesco. On the basis of this aspect, Tesco needs to frame

competent strategies to exert control on expenses (Ozsoylev and et.al., 2014). Through this,

business unit would become able to enhance its profit margin to a great extent. The below

mentioned graphical presentation states that net profit margin of Sainsbury is higher than

Tesco.

Year Tesco Sainsbury

2012 4.35% 2.68%

2013 0.19% 2.63%

2014 1.53% 2.99%

4

2012 2013 2014 2015 2016

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

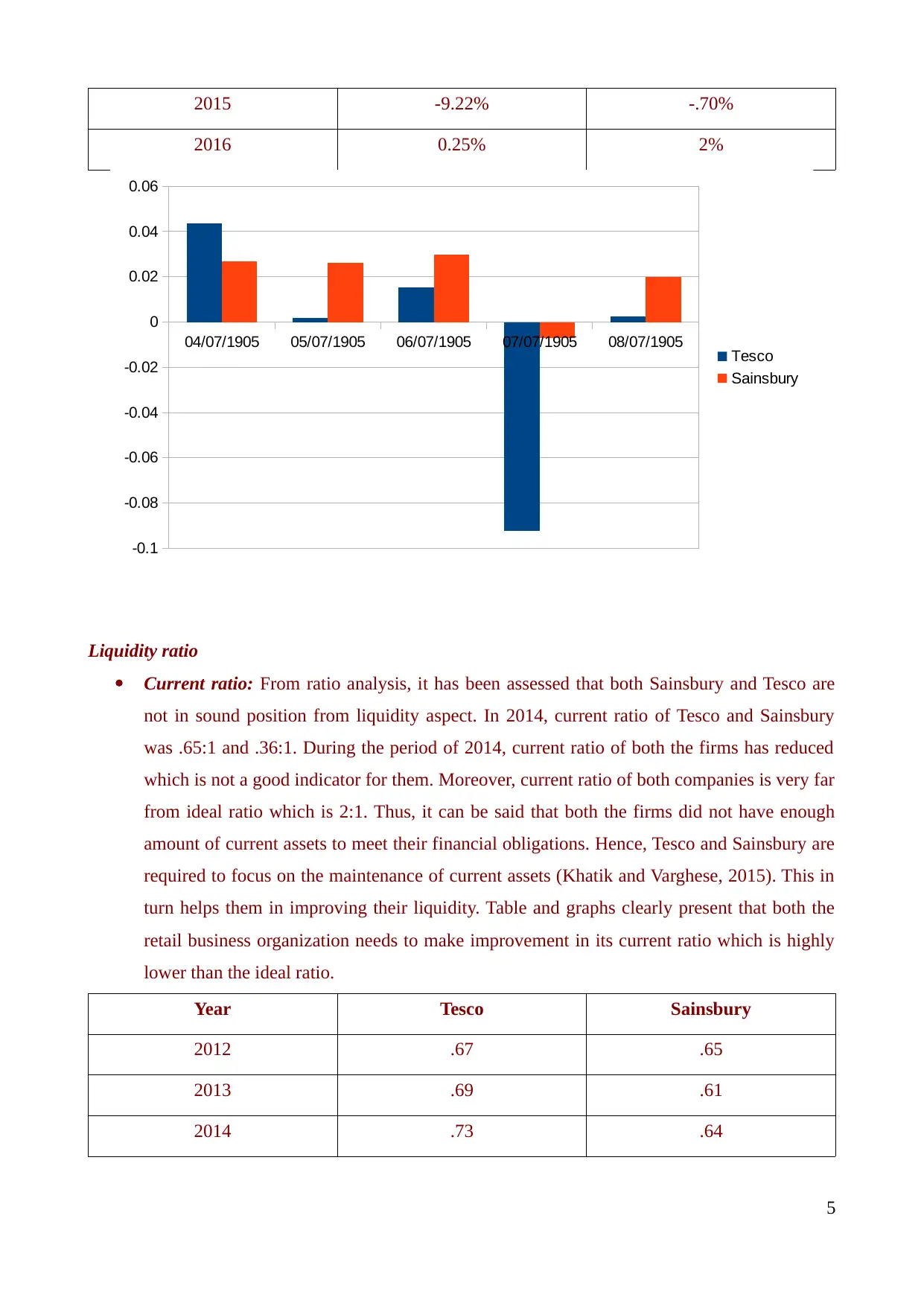

2015 -9.22% -.70%

2016 0.25% 2%

Liquidity ratio

Current ratio: From ratio analysis, it has been assessed that both Sainsbury and Tesco are

not in sound position from liquidity aspect. In 2014, current ratio of Tesco and Sainsbury

was .65:1 and .36:1. During the period of 2014, current ratio of both the firms has reduced

which is not a good indicator for them. Moreover, current ratio of both companies is very far

from ideal ratio which is 2:1. Thus, it can be said that both the firms did not have enough

amount of current assets to meet their financial obligations. Hence, Tesco and Sainsbury are

required to focus on the maintenance of current assets (Khatik and Varghese, 2015). This in

turn helps them in improving their liquidity. Table and graphs clearly present that both the

retail business organization needs to make improvement in its current ratio which is highly

lower than the ideal ratio.

Year Tesco Sainsbury

2012 .67 .65

2013 .69 .61

2014 .73 .64

5

04/07/1905 05/07/1905 06/07/1905 07/07/1905 08/07/1905

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Tesco

Sainsbury

2016 0.25% 2%

Liquidity ratio

Current ratio: From ratio analysis, it has been assessed that both Sainsbury and Tesco are

not in sound position from liquidity aspect. In 2014, current ratio of Tesco and Sainsbury

was .65:1 and .36:1. During the period of 2014, current ratio of both the firms has reduced

which is not a good indicator for them. Moreover, current ratio of both companies is very far

from ideal ratio which is 2:1. Thus, it can be said that both the firms did not have enough

amount of current assets to meet their financial obligations. Hence, Tesco and Sainsbury are

required to focus on the maintenance of current assets (Khatik and Varghese, 2015). This in

turn helps them in improving their liquidity. Table and graphs clearly present that both the

retail business organization needs to make improvement in its current ratio which is highly

lower than the ideal ratio.

Year Tesco Sainsbury

2012 .67 .65

2013 .69 .61

2014 .73 .64

5

04/07/1905 05/07/1905 06/07/1905 07/07/1905 08/07/1905

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

Tesco

Sainsbury

2015 .60 .65

2016 .75 .66

\

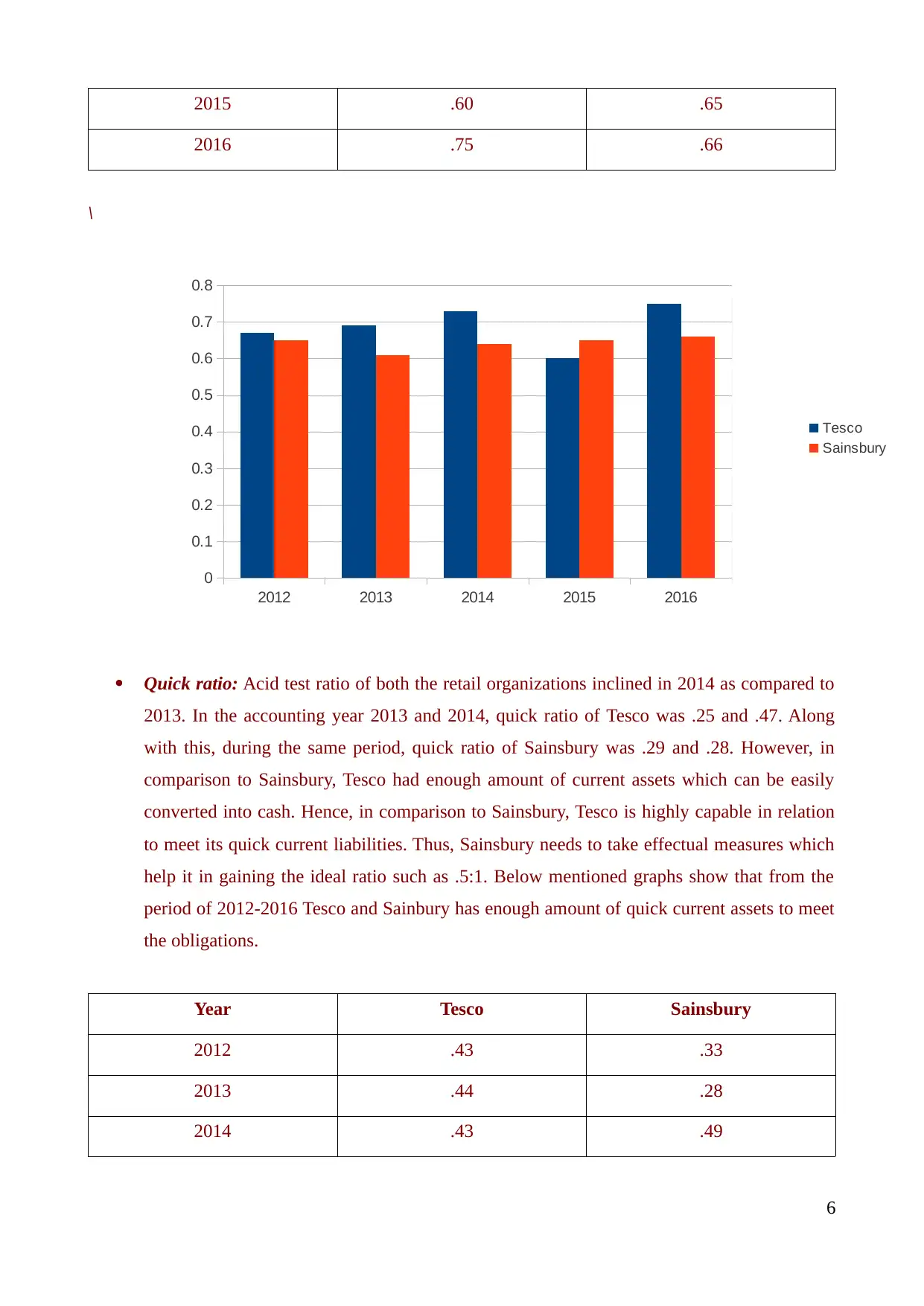

Quick ratio: Acid test ratio of both the retail organizations inclined in 2014 as compared to

2013. In the accounting year 2013 and 2014, quick ratio of Tesco was .25 and .47. Along

with this, during the same period, quick ratio of Sainsbury was .29 and .28. However, in

comparison to Sainsbury, Tesco had enough amount of current assets which can be easily

converted into cash. Hence, in comparison to Sainsbury, Tesco is highly capable in relation

to meet its quick current liabilities. Thus, Sainsbury needs to take effectual measures which

help it in gaining the ideal ratio such as .5:1. Below mentioned graphs show that from the

period of 2012-2016 Tesco and Sainbury has enough amount of quick current assets to meet

the obligations.

Year Tesco Sainsbury

2012 .43 .33

2013 .44 .28

2014 .43 .49

6

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Sainsbury

2016 .75 .66

\

Quick ratio: Acid test ratio of both the retail organizations inclined in 2014 as compared to

2013. In the accounting year 2013 and 2014, quick ratio of Tesco was .25 and .47. Along

with this, during the same period, quick ratio of Sainsbury was .29 and .28. However, in

comparison to Sainsbury, Tesco had enough amount of current assets which can be easily

converted into cash. Hence, in comparison to Sainsbury, Tesco is highly capable in relation

to meet its quick current liabilities. Thus, Sainsbury needs to take effectual measures which

help it in gaining the ideal ratio such as .5:1. Below mentioned graphs show that from the

period of 2012-2016 Tesco and Sainbury has enough amount of quick current assets to meet

the obligations.

Year Tesco Sainsbury

2012 .43 .33

2013 .44 .28

2014 .43 .49

6

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Tesco

Sainsbury

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 .42 .48

2016 .59 .50

Solvency ratio

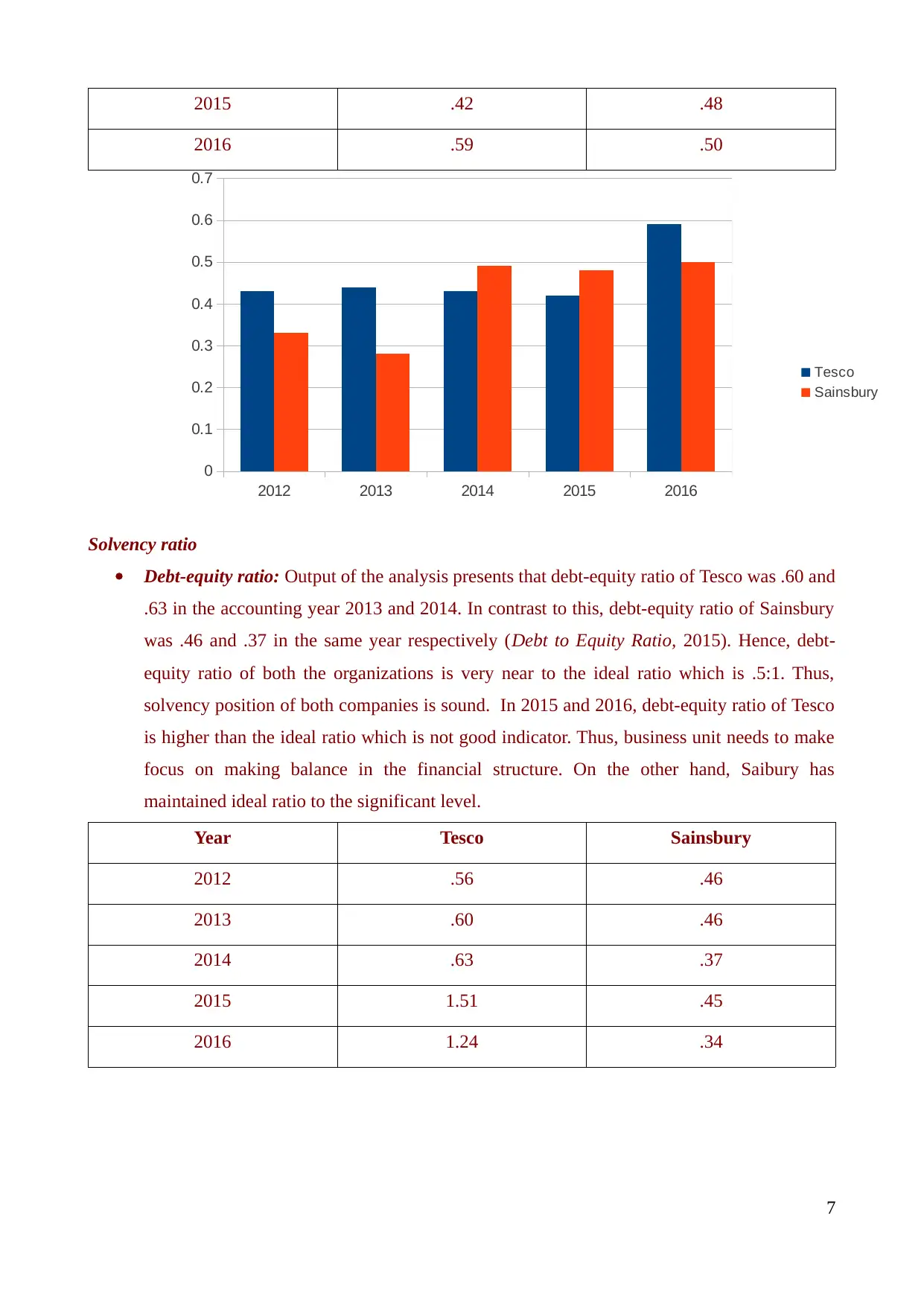

Debt-equity ratio: Output of the analysis presents that debt-equity ratio of Tesco was .60 and

.63 in the accounting year 2013 and 2014. In contrast to this, debt-equity ratio of Sainsbury

was .46 and .37 in the same year respectively (Debt to Equity Ratio, 2015). Hence, debt-

equity ratio of both the organizations is very near to the ideal ratio which is .5:1. Thus,

solvency position of both companies is sound. In 2015 and 2016, debt-equity ratio of Tesco

is higher than the ideal ratio which is not good indicator. Thus, business unit needs to make

focus on making balance in the financial structure. On the other hand, Saibury has

maintained ideal ratio to the significant level.

Year Tesco Sainsbury

2012 .56 .46

2013 .60 .46

2014 .63 .37

2015 1.51 .45

2016 1.24 .34

7

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Tesco

Sainsbury

2016 .59 .50

Solvency ratio

Debt-equity ratio: Output of the analysis presents that debt-equity ratio of Tesco was .60 and

.63 in the accounting year 2013 and 2014. In contrast to this, debt-equity ratio of Sainsbury

was .46 and .37 in the same year respectively (Debt to Equity Ratio, 2015). Hence, debt-

equity ratio of both the organizations is very near to the ideal ratio which is .5:1. Thus,

solvency position of both companies is sound. In 2015 and 2016, debt-equity ratio of Tesco

is higher than the ideal ratio which is not good indicator. Thus, business unit needs to make

focus on making balance in the financial structure. On the other hand, Saibury has

maintained ideal ratio to the significant level.

Year Tesco Sainsbury

2012 .56 .46

2013 .60 .46

2014 .63 .37

2015 1.51 .45

2016 1.24 .34

7

2012 2013 2014 2015 2016

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Tesco

Sainsbury

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Time-interest ratio: From this ratio, it has been identified that Sainsbury is highly capable

in relation to meet its interest expenses in comparison to Tesco. Moreover, in the accounting

year 2014, time interest ratio of Tesco and Sainsbury was 1.72 and 4.50. Thus, Tesco needs

to take actions which enhance its ability in relation to meet the interest expense. Moreover,

decision making of suppliers and other investors is highly influenced from such aspect

(Hoskin, Fizzell and Cherry, 2014).

Efficiency ratios

Total asset turnover ratio: This measure of both; Sainsbury and Tesco reduced in 2014 in

comparison to the past year. Moreover, in 2013 and 2014, total asset turnover ratio of Tesco

was 4.95 & 4.08. On contrary to this, such ratio of Sainsbury declined from 1.84 to 1.45. By

taking into consideration such ratio, it can be said that Tesco has made optimum use of total

assets for the generation of more sales in against to Sainsbury. Hence, Sainsbury needs to

make focus on the proper maintenance of assets like machinery, fixtures, etc. By this,

company would become able to get the desired level of outcomes or success.

Year Tesco Sainsbury

2012 1.32 1.88

2013 1.28 1.86

8

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Tesco

Sainsbury

in relation to meet its interest expenses in comparison to Tesco. Moreover, in the accounting

year 2014, time interest ratio of Tesco and Sainsbury was 1.72 and 4.50. Thus, Tesco needs

to take actions which enhance its ability in relation to meet the interest expense. Moreover,

decision making of suppliers and other investors is highly influenced from such aspect

(Hoskin, Fizzell and Cherry, 2014).

Efficiency ratios

Total asset turnover ratio: This measure of both; Sainsbury and Tesco reduced in 2014 in

comparison to the past year. Moreover, in 2013 and 2014, total asset turnover ratio of Tesco

was 4.95 & 4.08. On contrary to this, such ratio of Sainsbury declined from 1.84 to 1.45. By

taking into consideration such ratio, it can be said that Tesco has made optimum use of total

assets for the generation of more sales in against to Sainsbury. Hence, Sainsbury needs to

make focus on the proper maintenance of assets like machinery, fixtures, etc. By this,

company would become able to get the desired level of outcomes or success.

Year Tesco Sainsbury

2012 1.32 1.88

2013 1.28 1.86

8

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Tesco

Sainsbury

2014 1.27 1.64

2015 1.32 1.44

2016 1.24 1.40

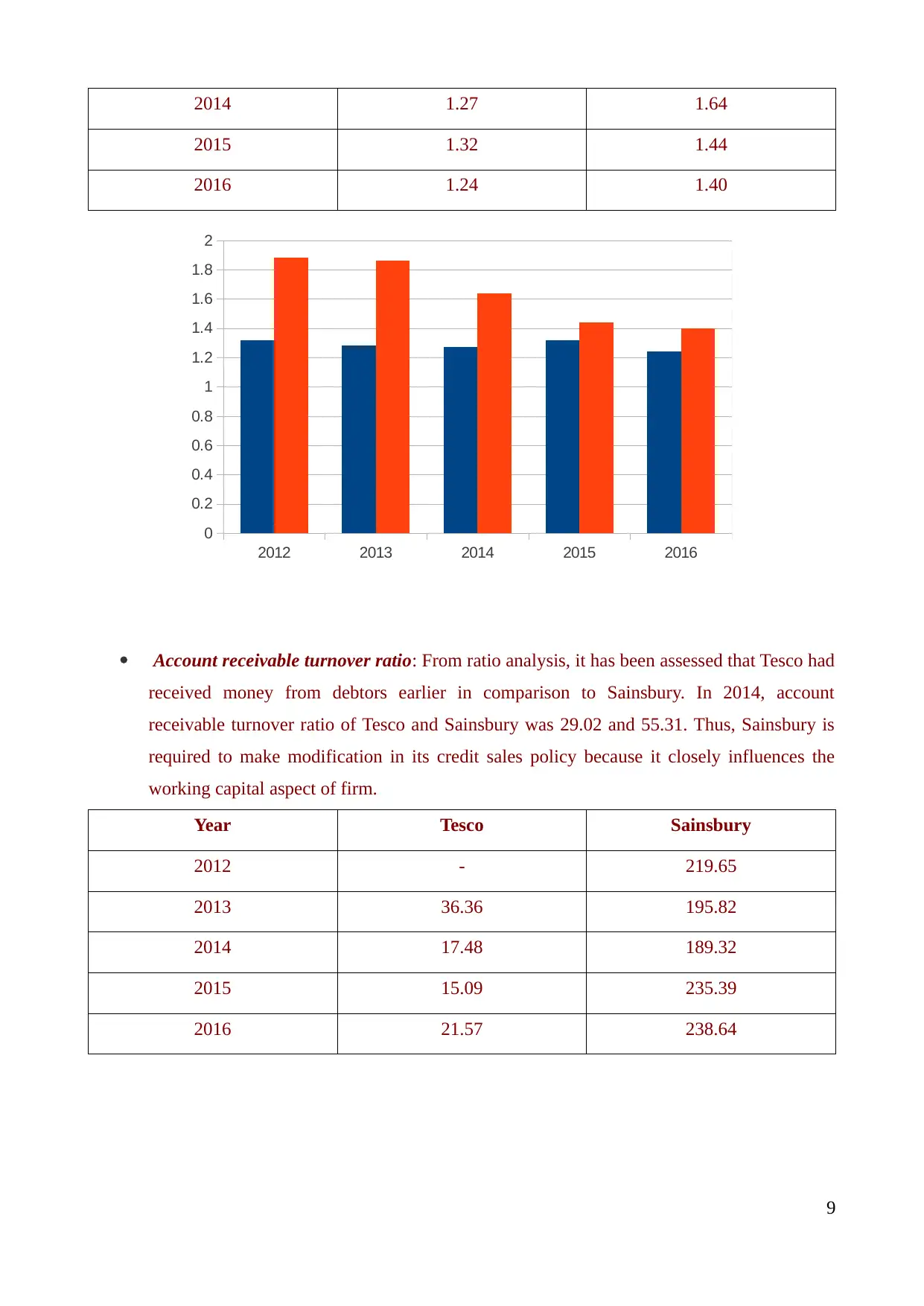

Account receivable turnover ratio: From ratio analysis, it has been assessed that Tesco had

received money from debtors earlier in comparison to Sainsbury. In 2014, account

receivable turnover ratio of Tesco and Sainsbury was 29.02 and 55.31. Thus, Sainsbury is

required to make modification in its credit sales policy because it closely influences the

working capital aspect of firm.

Year Tesco Sainsbury

2012 - 219.65

2013 36.36 195.82

2014 17.48 189.32

2015 15.09 235.39

2016 21.57 238.64

9

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2015 1.32 1.44

2016 1.24 1.40

Account receivable turnover ratio: From ratio analysis, it has been assessed that Tesco had

received money from debtors earlier in comparison to Sainsbury. In 2014, account

receivable turnover ratio of Tesco and Sainsbury was 29.02 and 55.31. Thus, Sainsbury is

required to make modification in its credit sales policy because it closely influences the

working capital aspect of firm.

Year Tesco Sainsbury

2012 - 219.65

2013 36.36 195.82

2014 17.48 189.32

2015 15.09 235.39

2016 21.57 238.64

9

2012 2013 2014 2015 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

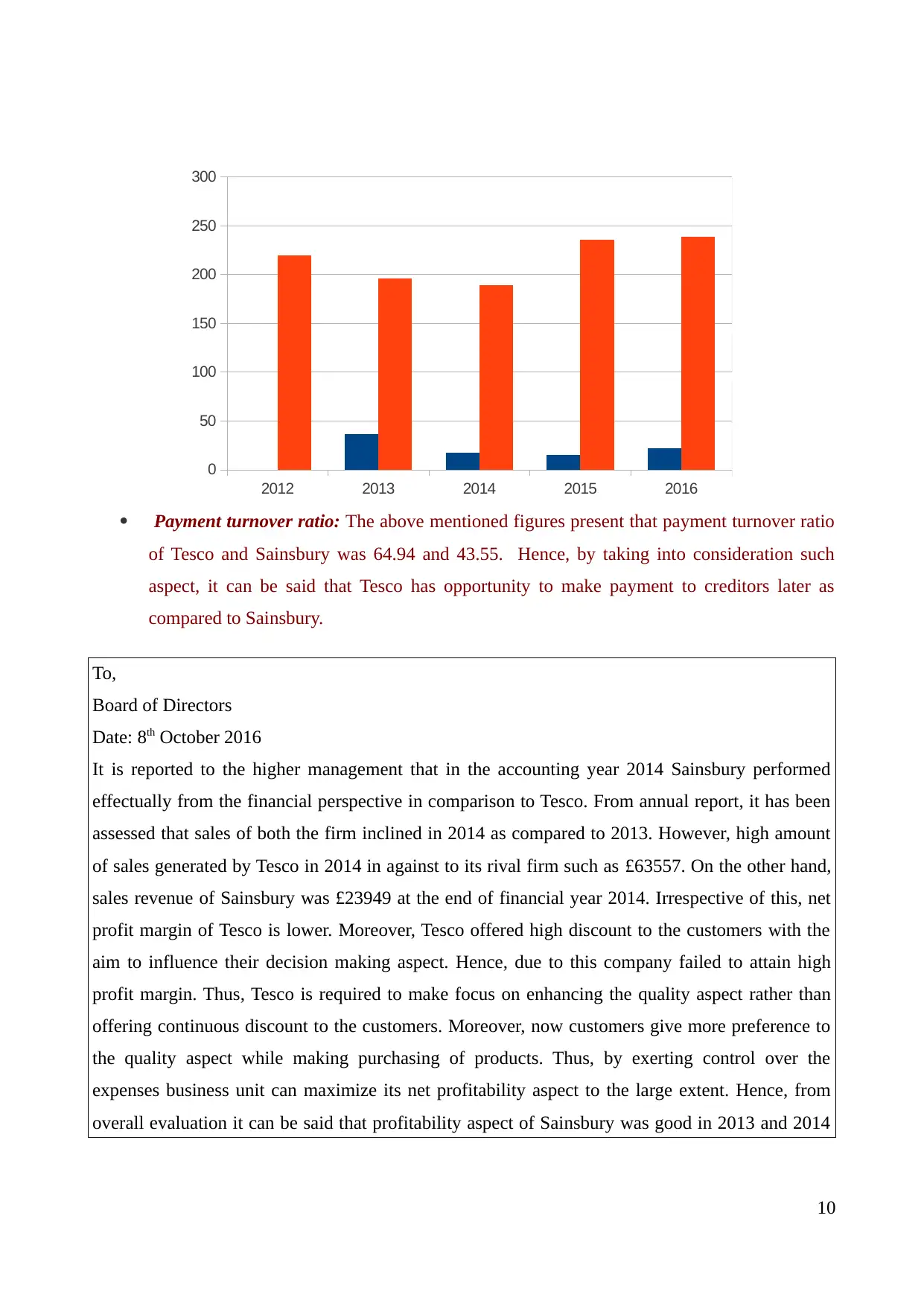

Payment turnover ratio: The above mentioned figures present that payment turnover ratio

of Tesco and Sainsbury was 64.94 and 43.55. Hence, by taking into consideration such

aspect, it can be said that Tesco has opportunity to make payment to creditors later as

compared to Sainsbury.

To,

Board of Directors

Date: 8th October 2016

It is reported to the higher management that in the accounting year 2014 Sainsbury performed

effectually from the financial perspective in comparison to Tesco. From annual report, it has been

assessed that sales of both the firm inclined in 2014 as compared to 2013. However, high amount

of sales generated by Tesco in 2014 in against to its rival firm such as £63557. On the other hand,

sales revenue of Sainsbury was £23949 at the end of financial year 2014. Irrespective of this, net

profit margin of Tesco is lower. Moreover, Tesco offered high discount to the customers with the

aim to influence their decision making aspect. Hence, due to this company failed to attain high

profit margin. Thus, Tesco is required to make focus on enhancing the quality aspect rather than

offering continuous discount to the customers. Moreover, now customers give more preference to

the quality aspect while making purchasing of products. Thus, by exerting control over the

expenses business unit can maximize its net profitability aspect to the large extent. Hence, from

overall evaluation it can be said that profitability aspect of Sainsbury was good in 2013 and 2014

10

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

of Tesco and Sainsbury was 64.94 and 43.55. Hence, by taking into consideration such

aspect, it can be said that Tesco has opportunity to make payment to creditors later as

compared to Sainsbury.

To,

Board of Directors

Date: 8th October 2016

It is reported to the higher management that in the accounting year 2014 Sainsbury performed

effectually from the financial perspective in comparison to Tesco. From annual report, it has been

assessed that sales of both the firm inclined in 2014 as compared to 2013. However, high amount

of sales generated by Tesco in 2014 in against to its rival firm such as £63557. On the other hand,

sales revenue of Sainsbury was £23949 at the end of financial year 2014. Irrespective of this, net

profit margin of Tesco is lower. Moreover, Tesco offered high discount to the customers with the

aim to influence their decision making aspect. Hence, due to this company failed to attain high

profit margin. Thus, Tesco is required to make focus on enhancing the quality aspect rather than

offering continuous discount to the customers. Moreover, now customers give more preference to

the quality aspect while making purchasing of products. Thus, by exerting control over the

expenses business unit can maximize its net profitability aspect to the large extent. Hence, from

overall evaluation it can be said that profitability aspect of Sainsbury was good in 2013 and 2014

10

2012 2013 2014 2015 2016

0

50

100

150

200

250

300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as compared to Tesco.

Further, by making analysis of the balance sheet it has been identified that both Tesco and

Sainsbury are not highly capable in relation to meeting the current financial obligations over

current assets. Moreover, outcome of ratio analysis presents that both the companies failed to

maintain the liquidity position according to the ideal ratio. Besides this, it also has been reported

that quick ratio of Tesco was in line with the ideal ratio. Further, in 2014, quick ratio of Sainsbury

was .28. Hence, Sainsbury was not highly capable to meet the quick obligations because it did not

have enough amount of current assets which can be converted into cash. Thus, it is advised to both

the organizations to make focus on maintaining the current assets which in turn helps in improving

the liquidity position.

It also has been reported to the higher management that in 2014 debentures of both the companies

were reduced to the significant level. During this period, debenture of Tesco and Sainsbury was

£9303 and £2250. Further, in 2014, equity share of Tesco decreased from £16661 to £14772. This

aspect shows that Tesco had made redemption of shares in 2014. On the contrary to it, more shares

were issued by Sainsbury in 2014. However, by taking strategic action business organization has

maintained the sound financial structure. Along with this, Sainsbury had made effectual use of

assets and thereby generated more sales.

TASK 2

Giving advise upon the level of disclosure which is used by both the companies in the published

annual reports

In published annual reports of TESCO and Sainsbury, the two companies have adopted IFRS

principles. With the adoption of these principles the organizations are able to disclose the required

amount of information. It assists the firms to maintain transparency among its various stakeholders.

In addition to it, the annual reports of these firms consist graphs, charts and tables which assists the

users to create better understanding of the annual reports. However, disclosure is related with the

accounting policies, legal contingencies of the company which may be sometimes repetitive in the

discloser statements of the company (Parashar, 2014). As a result, it can affect the understanding of

the viewers which leaves negative impact. The cited companies applies appropriate accounting

policies in order to maintain quality disclosers.

In order to avoid repetition of policies, the two companies uses cross referencing. It assists

in avoiding duplication of policies and legal regulations of the firms. In addition to it, this aids the

11

Further, by making analysis of the balance sheet it has been identified that both Tesco and

Sainsbury are not highly capable in relation to meeting the current financial obligations over

current assets. Moreover, outcome of ratio analysis presents that both the companies failed to

maintain the liquidity position according to the ideal ratio. Besides this, it also has been reported

that quick ratio of Tesco was in line with the ideal ratio. Further, in 2014, quick ratio of Sainsbury

was .28. Hence, Sainsbury was not highly capable to meet the quick obligations because it did not

have enough amount of current assets which can be converted into cash. Thus, it is advised to both

the organizations to make focus on maintaining the current assets which in turn helps in improving

the liquidity position.

It also has been reported to the higher management that in 2014 debentures of both the companies

were reduced to the significant level. During this period, debenture of Tesco and Sainsbury was

£9303 and £2250. Further, in 2014, equity share of Tesco decreased from £16661 to £14772. This

aspect shows that Tesco had made redemption of shares in 2014. On the contrary to it, more shares

were issued by Sainsbury in 2014. However, by taking strategic action business organization has

maintained the sound financial structure. Along with this, Sainsbury had made effectual use of

assets and thereby generated more sales.

TASK 2

Giving advise upon the level of disclosure which is used by both the companies in the published

annual reports

In published annual reports of TESCO and Sainsbury, the two companies have adopted IFRS

principles. With the adoption of these principles the organizations are able to disclose the required

amount of information. It assists the firms to maintain transparency among its various stakeholders.

In addition to it, the annual reports of these firms consist graphs, charts and tables which assists the

users to create better understanding of the annual reports. However, disclosure is related with the

accounting policies, legal contingencies of the company which may be sometimes repetitive in the

discloser statements of the company (Parashar, 2014). As a result, it can affect the understanding of

the viewers which leaves negative impact. The cited companies applies appropriate accounting

policies in order to maintain quality disclosers.

In order to avoid repetition of policies, the two companies uses cross referencing. It assists

in avoiding duplication of policies and legal regulations of the firms. In addition to it, this aids the

11

reader to get knowledge over relevant and extra information about the companies. The two

companies adopt appropriate ways to disclose information which assist the management to maintain

transparency. In order to implement further improvements, the cited organizations can consider

additional ways to present the annual reports effectively. Footnotes can be added to the financial

statements of the firms where it includes detailed explanation of the information. It helps the reader

to get appropriate meaning of the stated information (Pyo and Chung, 2015). To improve the

process, two companies can also use the concept of quarterly disclosures. In addition to it, grouping

of disclosure by its nature can help the companies to improve their process. Executive summary can

also be added in the presentation so that it would reduce the problem of over burden.

The concept of materiality is required to considered while preparing financial statements of

the companies. The organizations can also includes presentation of certain disclosure which are not

included in financial statements. However, there are some areas that are necessarily been dis

closured by the two companies such as risk factors, legal proceedings and the key stakeholders of

the company. In order to improve the same the companies can eliminate repetitive information

which will help the user to get appropriate information.

However, firms can adopt significant accounting policies with consideration of UK GAAP.

It will help the firm to maintain appropriate methods and principles. It is also seen that there are

number of organizations that have started focusing on taking effective initiative on improving

disclosures. It will help the companies to make more meaningful for which the organizations needs

to take immediate actions. It will ultimately help both the company and its investors to get the crux

of the information (Ozsoylev and et.al., 2014). The profitability of the two companies is purely

based their services and required providence of the information. If it is done effectively, then the

goals and objectives of the organization can be attained effectively. In addition to it, having

appropriate knowledge of the company proceeding and its information can result into increasing

number of investors.

TASK 3

Stating the extent to which both the retail organizations have addressed the need of the different

stakeholders by presenting the report

Both Tesco and Sainsbury has accountability to prepare and publish audited financial

statements to satisfy the information need of varied stakeholders. Moreover, there are several

stakeholders who make use of the financial statements for the purpose of decision making. In this

regard, Tesco and Sainsbury has satisfied the information need of different stakeholders in the

following manner:

12

companies adopt appropriate ways to disclose information which assist the management to maintain

transparency. In order to implement further improvements, the cited organizations can consider

additional ways to present the annual reports effectively. Footnotes can be added to the financial

statements of the firms where it includes detailed explanation of the information. It helps the reader

to get appropriate meaning of the stated information (Pyo and Chung, 2015). To improve the

process, two companies can also use the concept of quarterly disclosures. In addition to it, grouping

of disclosure by its nature can help the companies to improve their process. Executive summary can

also be added in the presentation so that it would reduce the problem of over burden.

The concept of materiality is required to considered while preparing financial statements of

the companies. The organizations can also includes presentation of certain disclosure which are not

included in financial statements. However, there are some areas that are necessarily been dis

closured by the two companies such as risk factors, legal proceedings and the key stakeholders of

the company. In order to improve the same the companies can eliminate repetitive information

which will help the user to get appropriate information.

However, firms can adopt significant accounting policies with consideration of UK GAAP.

It will help the firm to maintain appropriate methods and principles. It is also seen that there are

number of organizations that have started focusing on taking effective initiative on improving

disclosures. It will help the companies to make more meaningful for which the organizations needs

to take immediate actions. It will ultimately help both the company and its investors to get the crux

of the information (Ozsoylev and et.al., 2014). The profitability of the two companies is purely

based their services and required providence of the information. If it is done effectively, then the

goals and objectives of the organization can be attained effectively. In addition to it, having

appropriate knowledge of the company proceeding and its information can result into increasing

number of investors.

TASK 3

Stating the extent to which both the retail organizations have addressed the need of the different

stakeholders by presenting the report

Both Tesco and Sainsbury has accountability to prepare and publish audited financial

statements to satisfy the information need of varied stakeholders. Moreover, there are several

stakeholders who make use of the financial statements for the purpose of decision making. In this

regard, Tesco and Sainsbury has satisfied the information need of different stakeholders in the

following manner:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.