Financial Analysis: EMA 18K Assignment on Financial Management

VerifiedAdded on 2021/10/14

|19

|4096

|31

Homework Assignment

AI Summary

This document presents a comprehensive solution to an EMA 18K financial management assignment, addressing key concepts such as net present value (NPV), foreign exchange risk, and credit risk assessment. The solution begins with calculating the NPV of cash flow gaps under different discount rates, demonstrating the impact of interest rate changes. It then delves into foreign exchange risk, specifically transaction exposure, and explores hedging strategies like forward rate agreements, future contracts, and options. Furthermore, the assignment assesses the creditworthiness of the American Red Cross, analyzing its market reputation, financial performance, and working capital to determine its ability to handle a large credit order. The document provides detailed calculations and explanations for each question, offering a thorough understanding of the financial management principles involved.

EMA 18K: Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

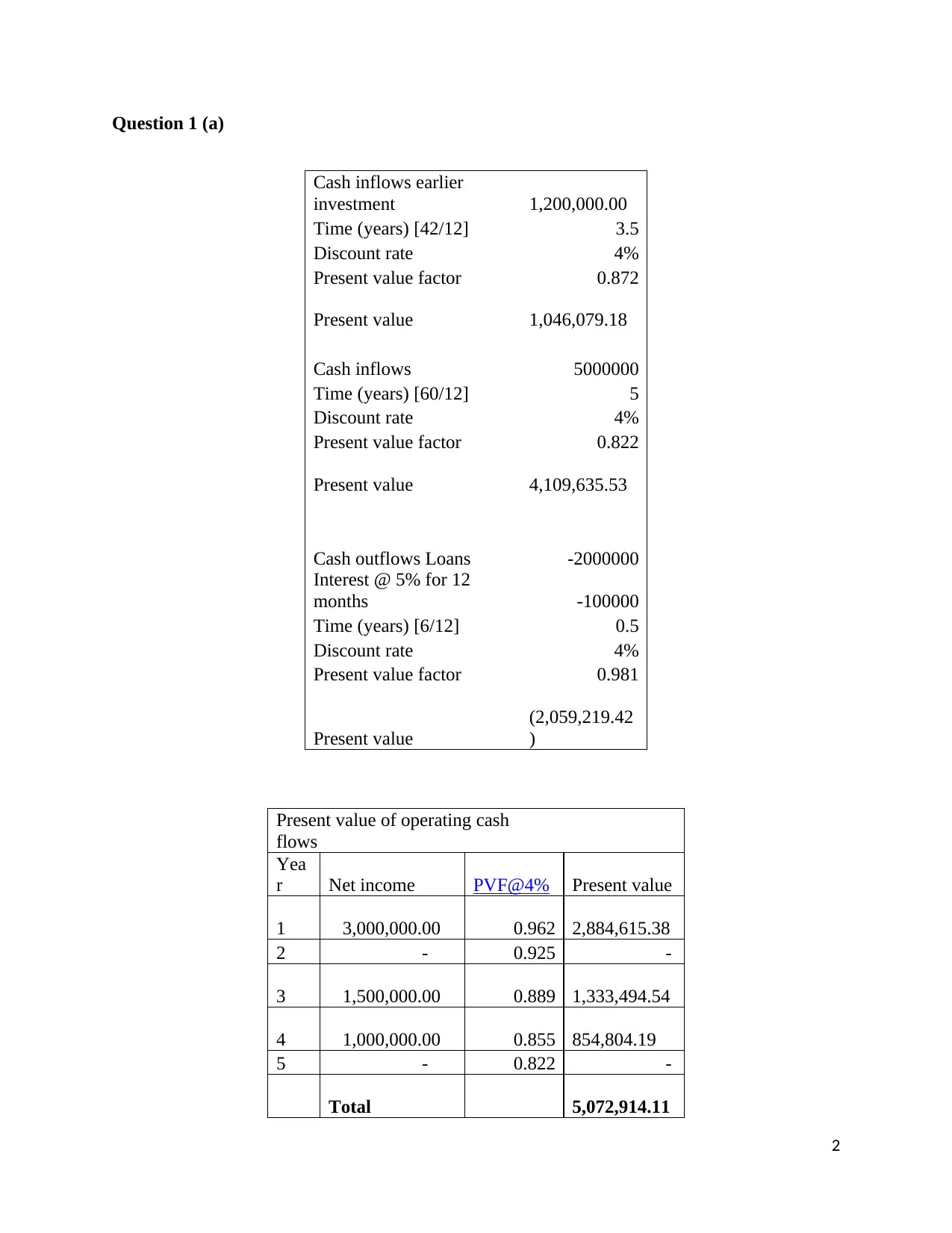

Question 1 (a)

Cash inflows earlier

investment 1,200,000.00

Time (years) [42/12] 3.5

Discount rate 4%

Present value factor 0.872

Present value 1,046,079.18

Cash inflows 5000000

Time (years) [60/12] 5

Discount rate 4%

Present value factor 0.822

Present value 4,109,635.53

Cash outflows Loans -2000000

Interest @ 5% for 12

months -100000

Time (years) [6/12] 0.5

Discount rate 4%

Present value factor 0.981

Present value

(2,059,219.42

)

Present value of operating cash

flows

Yea

r Net income PVF@4% Present value

1 3,000,000.00 0.962 2,884,615.38

2 - 0.925 -

3 1,500,000.00 0.889 1,333,494.54

4 1,000,000.00 0.855 854,804.19

5 - 0.822 -

Total 5,072,914.11

2

Cash inflows earlier

investment 1,200,000.00

Time (years) [42/12] 3.5

Discount rate 4%

Present value factor 0.872

Present value 1,046,079.18

Cash inflows 5000000

Time (years) [60/12] 5

Discount rate 4%

Present value factor 0.822

Present value 4,109,635.53

Cash outflows Loans -2000000

Interest @ 5% for 12

months -100000

Time (years) [6/12] 0.5

Discount rate 4%

Present value factor 0.981

Present value

(2,059,219.42

)

Present value of operating cash

flows

Yea

r Net income PVF@4% Present value

1 3,000,000.00 0.962 2,884,615.38

2 - 0.925 -

3 1,500,000.00 0.889 1,333,494.54

4 1,000,000.00 0.855 854,804.19

5 - 0.822 -

Total 5,072,914.11

2

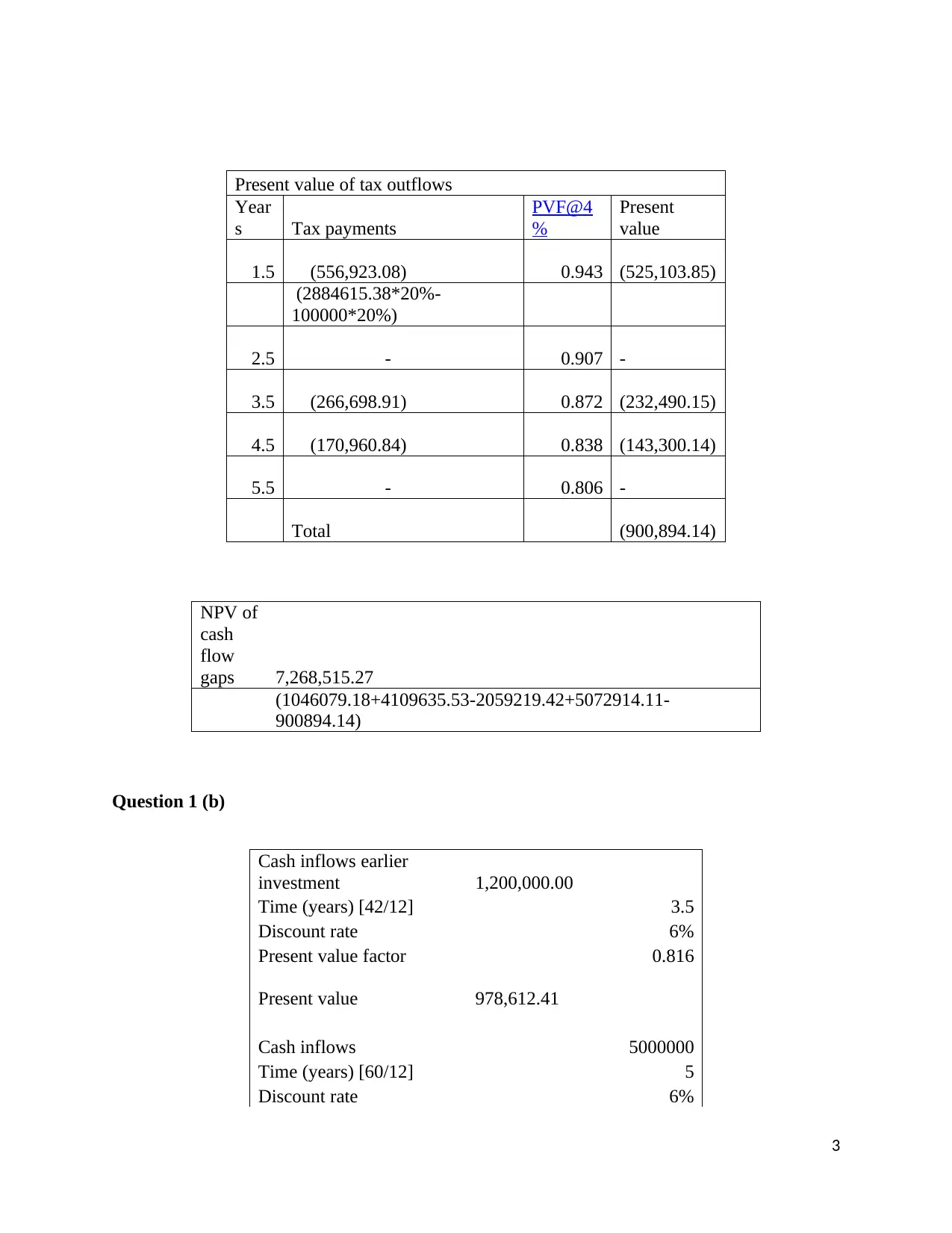

Present value of tax outflows

Year

s Tax payments

PVF@4

%

Present

value

1.5 (556,923.08) 0.943 (525,103.85)

(2884615.38*20%-

100000*20%)

2.5 - 0.907 -

3.5 (266,698.91) 0.872 (232,490.15)

4.5 (170,960.84) 0.838 (143,300.14)

5.5 - 0.806 -

Total (900,894.14)

NPV of

cash

flow

gaps 7,268,515.27

(1046079.18+4109635.53-2059219.42+5072914.11-

900894.14)

Question 1 (b)

Cash inflows earlier

investment 1,200,000.00

Time (years) [42/12] 3.5

Discount rate 6%

Present value factor 0.816

Present value 978,612.41

Cash inflows 5000000

Time (years) [60/12] 5

Discount rate 6%

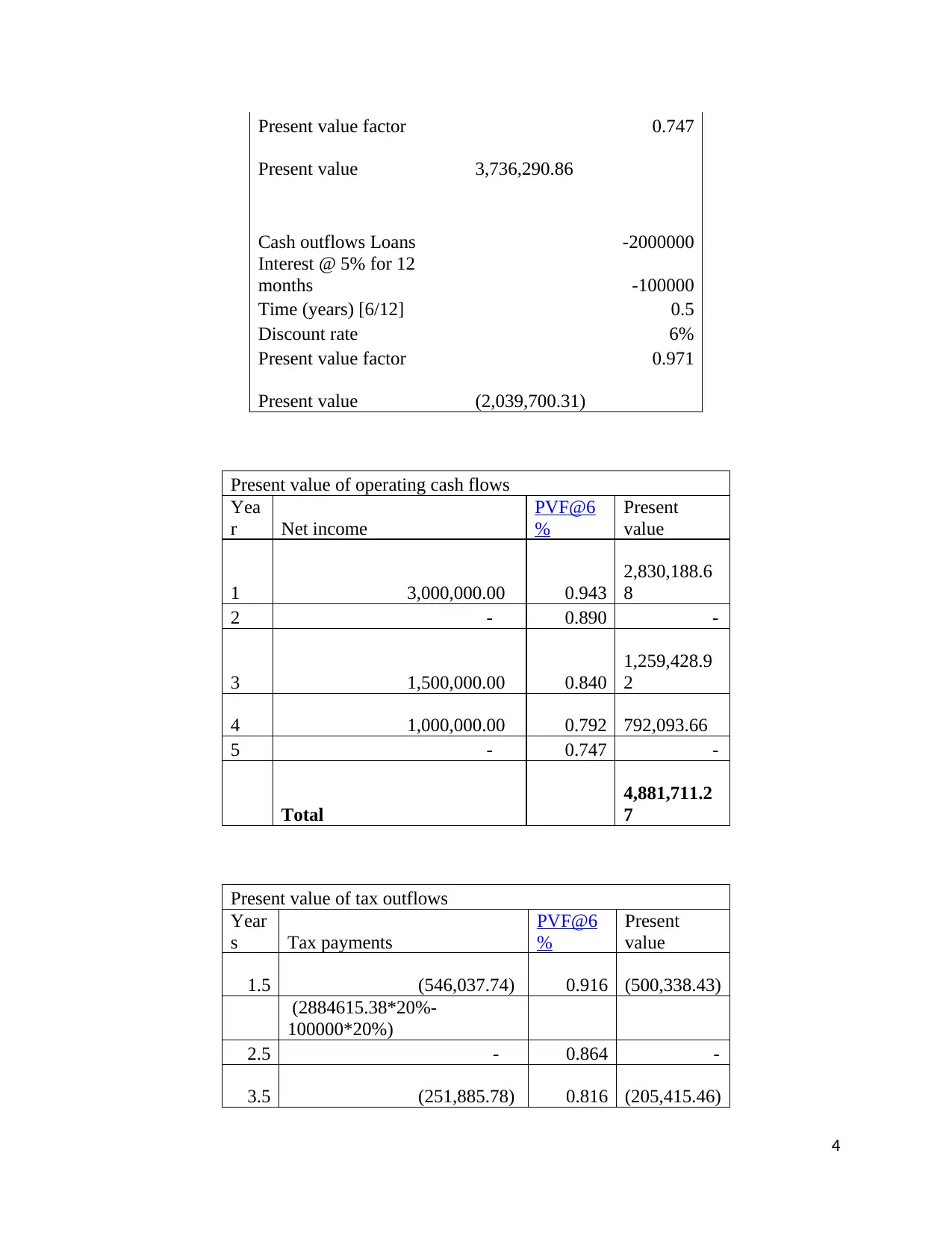

3

Year

s Tax payments

PVF@4

%

Present

value

1.5 (556,923.08) 0.943 (525,103.85)

(2884615.38*20%-

100000*20%)

2.5 - 0.907 -

3.5 (266,698.91) 0.872 (232,490.15)

4.5 (170,960.84) 0.838 (143,300.14)

5.5 - 0.806 -

Total (900,894.14)

NPV of

cash

flow

gaps 7,268,515.27

(1046079.18+4109635.53-2059219.42+5072914.11-

900894.14)

Question 1 (b)

Cash inflows earlier

investment 1,200,000.00

Time (years) [42/12] 3.5

Discount rate 6%

Present value factor 0.816

Present value 978,612.41

Cash inflows 5000000

Time (years) [60/12] 5

Discount rate 6%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Present value factor 0.747

Present value 3,736,290.86

Cash outflows Loans -2000000

Interest @ 5% for 12

months -100000

Time (years) [6/12] 0.5

Discount rate 6%

Present value factor 0.971

Present value (2,039,700.31)

Present value of operating cash flows

Yea

r Net income

PVF@6

%

Present

value

1 3,000,000.00 0.943

2,830,188.6

8

2 - 0.890 -

3 1,500,000.00 0.840

1,259,428.9

2

4 1,000,000.00 0.792 792,093.66

5 - 0.747 -

Total

4,881,711.2

7

Present value of tax outflows

Year

s Tax payments

PVF@6

%

Present

value

1.5 (546,037.74) 0.916 (500,338.43)

(2884615.38*20%-

100000*20%)

2.5 - 0.864 -

3.5 (251,885.78) 0.816 (205,415.46)

4

Present value 3,736,290.86

Cash outflows Loans -2000000

Interest @ 5% for 12

months -100000

Time (years) [6/12] 0.5

Discount rate 6%

Present value factor 0.971

Present value (2,039,700.31)

Present value of operating cash flows

Yea

r Net income

PVF@6

%

Present

value

1 3,000,000.00 0.943

2,830,188.6

8

2 - 0.890 -

3 1,500,000.00 0.840

1,259,428.9

2

4 1,000,000.00 0.792 792,093.66

5 - 0.747 -

Total

4,881,711.2

7

Present value of tax outflows

Year

s Tax payments

PVF@6

%

Present

value

1.5 (546,037.74) 0.916 (500,338.43)

(2884615.38*20%-

100000*20%)

2.5 - 0.864 -

3.5 (251,885.78) 0.816 (205,415.46)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.5 (158,418.73) 0.769 (121,879.35)

5.5 - 0.726 -

Total (827,633.24)

NPV of

cash

flow

gaps 6,729,280.98

978612.41+3736290.86-2039700.31+4881711.27-827633.24

Question 1 (c)

The net present value of the cash flow gaps is £7,268,515.27 at the discount rate of 4%.

When the interest rate rises by 2%, the discount rate also increases by 2%. The increase in the

discount rate implies decrease in the present value. Thus, the net present value of the cash flow

gaps declines to £6,729,280.98 when the interest rate rises to 6%. It can be seen that the net

present value reducing on an increase of 2% in the interest rate. However, the net present value is

still positive so the increase in the interest would be acceptable to the board of directors of the

company (Rossi, 2015).

Question 2 (a)

There are various types of foreign exchange risks such as transaction risk, translation

risk, economic risk, risk of netting and matching, and the risk of leading and lagging (Bessis,

2015). In the current case, Factor 14 Plc, which is a British manufacturer, is undertaking

transactions with the Euro zone counties. The company engages in various purchases and sales

transactions with the Euro zone counties. The truncations with the Euro zone countries are

5

5.5 - 0.726 -

Total (827,633.24)

NPV of

cash

flow

gaps 6,729,280.98

978612.41+3736290.86-2039700.31+4881711.27-827633.24

Question 1 (c)

The net present value of the cash flow gaps is £7,268,515.27 at the discount rate of 4%.

When the interest rate rises by 2%, the discount rate also increases by 2%. The increase in the

discount rate implies decrease in the present value. Thus, the net present value of the cash flow

gaps declines to £6,729,280.98 when the interest rate rises to 6%. It can be seen that the net

present value reducing on an increase of 2% in the interest rate. However, the net present value is

still positive so the increase in the interest would be acceptable to the board of directors of the

company (Rossi, 2015).

Question 2 (a)

There are various types of foreign exchange risks such as transaction risk, translation

risk, economic risk, risk of netting and matching, and the risk of leading and lagging (Bessis,

2015). In the current case, Factor 14 Plc, which is a British manufacturer, is undertaking

transactions with the Euro zone counties. The company engages in various purchases and sales

transactions with the Euro zone counties. The truncations with the Euro zone countries are

5

settled in Euro while the home currency of the company is GBP. Thus, this gives rise to the

transaction exposure to the company. Here, the company has receivables of €200,000 due in next

six months, thus, the company incurring the risk of loss on account of unfavorable changes in the

foreign exchange rates between Euro and GBP. The company has receivables due, thus, if Euro

depreciates against GBP, the company will incur losses. The company can hedge against this risk

by opting to various strategies (Pilbeam, 2018).

There are various alternatives through which the company can hedge the risk of foreign

exchange. The prominent alternatives for such purpose are forward rate agreement, future

contract, option contract, and money market operations (Pilbeam, 2018). Under the forward rate

agreement, the company can enter into an agreement with the bank to receive foreign currency at

the specified rate on the specified date. Further, the future and option contracts of the currencies

are traded on the stock exchange. The future contract provides the company an alternative to fix

the foreign currency rate for the future transaction. For example, in the current case, Factor 14

Plc can enter into sale future contract on Euro for 6 months. Further, option contract also could

be used in the similar fashion to hedge the foreign exchange risk. However, option contract

provides little flexibility as compared to future contract. The option contract is not binding on the

buyer so the buyer gets that flexibility to exercise or get the option lapsed on the date of expiry

(Chance and Brooks, 2015).

Apart from the above, the company can also opt for money market operations. In the

money market operations, the company usages short term lending and borrowing instruments to

create hedge strategy. For instance, in the current case, Factor 14 Plc can lend money in Euro for

6 months. On the date of transaction after six months, the payables in Euro could be settled

against receivables (Chance and Brooks, 2015).

6

transaction exposure to the company. Here, the company has receivables of €200,000 due in next

six months, thus, the company incurring the risk of loss on account of unfavorable changes in the

foreign exchange rates between Euro and GBP. The company has receivables due, thus, if Euro

depreciates against GBP, the company will incur losses. The company can hedge against this risk

by opting to various strategies (Pilbeam, 2018).

There are various alternatives through which the company can hedge the risk of foreign

exchange. The prominent alternatives for such purpose are forward rate agreement, future

contract, option contract, and money market operations (Pilbeam, 2018). Under the forward rate

agreement, the company can enter into an agreement with the bank to receive foreign currency at

the specified rate on the specified date. Further, the future and option contracts of the currencies

are traded on the stock exchange. The future contract provides the company an alternative to fix

the foreign currency rate for the future transaction. For example, in the current case, Factor 14

Plc can enter into sale future contract on Euro for 6 months. Further, option contract also could

be used in the similar fashion to hedge the foreign exchange risk. However, option contract

provides little flexibility as compared to future contract. The option contract is not binding on the

buyer so the buyer gets that flexibility to exercise or get the option lapsed on the date of expiry

(Chance and Brooks, 2015).

Apart from the above, the company can also opt for money market operations. In the

money market operations, the company usages short term lending and borrowing instruments to

create hedge strategy. For instance, in the current case, Factor 14 Plc can lend money in Euro for

6 months. On the date of transaction after six months, the payables in Euro could be settled

against receivables (Chance and Brooks, 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2 (b)

Applying the concept of interest rate parity theory, forward rates between the foreign

currencies could be calculated. The interest rate parity theory states that the investment

opportunity in two countries must be same and if difference exists, it is due to difference in

foreign exchange rates (Du, Tepper, and Verdelhan, 2018). Thus, the forward rate between Euro

and GBP for 6 months is calculated as below:

Spot rate * (1+interest rate GBP)

(1+interest rate Euro)

0.88* (1+1%/2)/ (1+0.5%/2)

0.8823

Thus, the 6 months forward rate at which the company can take forward cover to hedge

the risk is 0.8823.

Question 2 (c)

In the current case, Factor 14 Plc has receivables of €200,000 thus; the company can

enter into put buy option on Euro. The put option on Euro would give the company the right to

sell Euro after 6 months at the exercise price i.e. 0.88 GBP/ Euro.

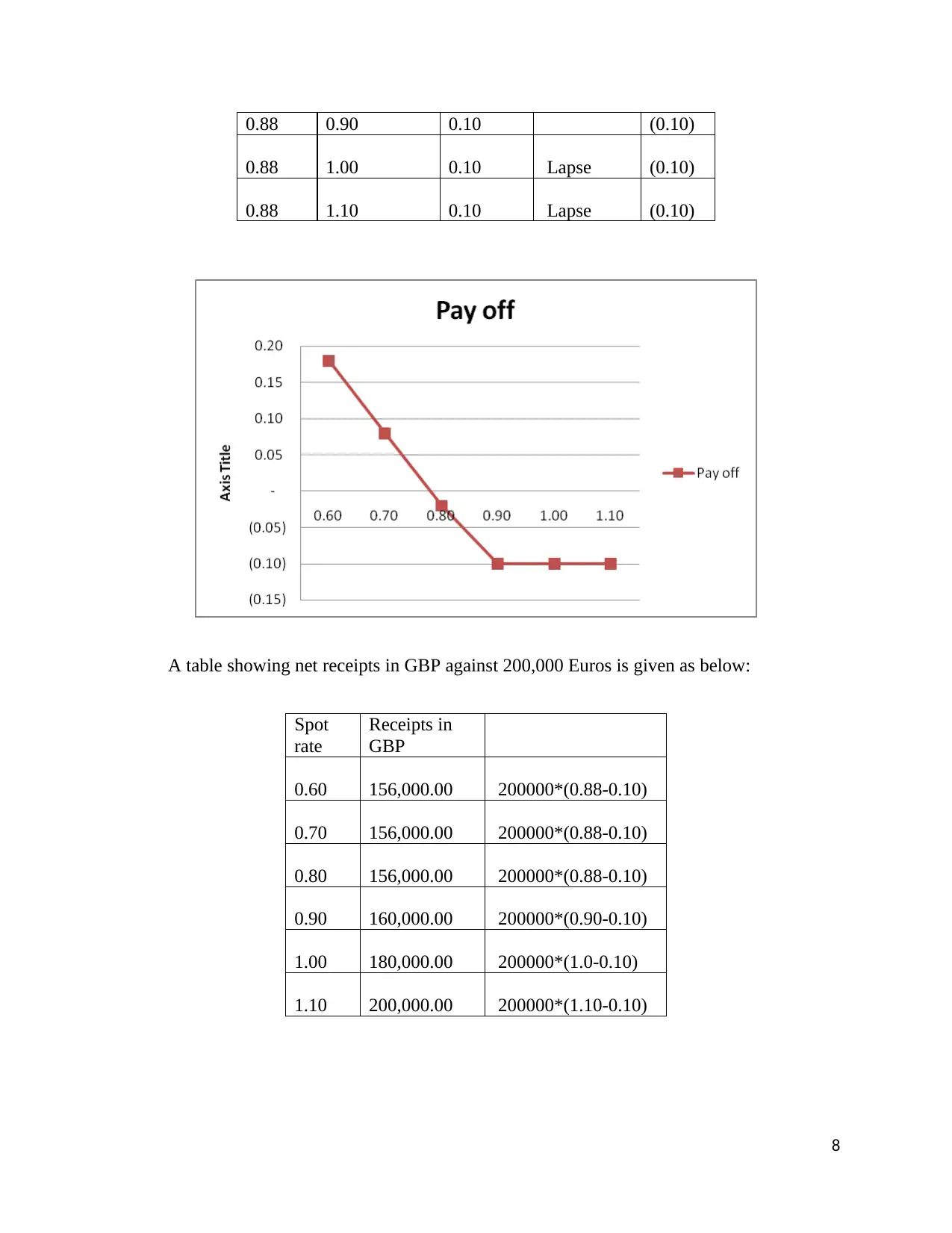

The table showing net pay off at different spot rates is given as below:

Exercis

e rate Spot rate Premium

Exercise/

Lapse Pay off

0.88 0.60 0.10 Exercise 0.18

0.88 0.70 0.10 Exercise 0.08

0.88 0.80 0.10 Exercise (0.02)

Lapse

7

Applying the concept of interest rate parity theory, forward rates between the foreign

currencies could be calculated. The interest rate parity theory states that the investment

opportunity in two countries must be same and if difference exists, it is due to difference in

foreign exchange rates (Du, Tepper, and Verdelhan, 2018). Thus, the forward rate between Euro

and GBP for 6 months is calculated as below:

Spot rate * (1+interest rate GBP)

(1+interest rate Euro)

0.88* (1+1%/2)/ (1+0.5%/2)

0.8823

Thus, the 6 months forward rate at which the company can take forward cover to hedge

the risk is 0.8823.

Question 2 (c)

In the current case, Factor 14 Plc has receivables of €200,000 thus; the company can

enter into put buy option on Euro. The put option on Euro would give the company the right to

sell Euro after 6 months at the exercise price i.e. 0.88 GBP/ Euro.

The table showing net pay off at different spot rates is given as below:

Exercis

e rate Spot rate Premium

Exercise/

Lapse Pay off

0.88 0.60 0.10 Exercise 0.18

0.88 0.70 0.10 Exercise 0.08

0.88 0.80 0.10 Exercise (0.02)

Lapse

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.88 0.90 0.10 (0.10)

0.88 1.00 0.10 Lapse (0.10)

0.88 1.10 0.10 Lapse (0.10)

A table showing net receipts in GBP against 200,000 Euros is given as below:

Spot

rate

Receipts in

GBP

0.60 156,000.00 200000*(0.88-0.10)

0.70 156,000.00 200000*(0.88-0.10)

0.80 156,000.00 200000*(0.88-0.10)

0.90 160,000.00 200000*(0.90-0.10)

1.00 180,000.00 200000*(1.0-0.10)

1.10 200,000.00 200000*(1.10-0.10)

8

0.88 1.00 0.10 Lapse (0.10)

0.88 1.10 0.10 Lapse (0.10)

A table showing net receipts in GBP against 200,000 Euros is given as below:

Spot

rate

Receipts in

GBP

0.60 156,000.00 200000*(0.88-0.10)

0.70 156,000.00 200000*(0.88-0.10)

0.80 156,000.00 200000*(0.88-0.10)

0.90 160,000.00 200000*(0.90-0.10)

1.00 180,000.00 200000*(1.0-0.10)

1.10 200,000.00 200000*(1.10-0.10)

8

It can be observed that the company would exercise the option contract till the spot rate

remains up to 0.88 (exercise rate). As soon as the spot rate surpasses the exercise rate, the

company would be better off in letting the option lapse. In that scenario, the company would get

money converted at the spot rate rather than exercising the option.

Further, it can be observed that by taking the put option, the company has fixed the

payment at GBP 156000, which means that the company will get at least GBP 156,000 against

Euro 200,000 even if the exchange rate goes down to 0.50. On the other hand, the company

would get opportunity to earn unlimited profits in case the exchange rate rises beyond 0.88

levels.

Question 2 (d)

The company’s decision to hedge the foreign exchange risk shows the apprehensions of

the company about depreciation in Euro against GBP in the coming months. This shows that the

economy of Euro zone is suffering from slow growth and high inflation which is causing the

money power of Euro to decline. However, the company should take hedging position after

analyzing the economic conditions of the foreign country and home country thoroughly.

Question 3 (a)

In the current case, the management is considering a large order of goods emanating from

American Red Cross. The order amount is $30 million and also the buyer (American Red Cross)

is seeking credit terms of more than 30 days, the usual credit period. In this connection, it is

imperative for the management to assess the creditworthiness of American Red Cross so that the

credit risk or the risk of default could be managed. The following methodology should be

adopted by the management for this purpose:

9

remains up to 0.88 (exercise rate). As soon as the spot rate surpasses the exercise rate, the

company would be better off in letting the option lapse. In that scenario, the company would get

money converted at the spot rate rather than exercising the option.

Further, it can be observed that by taking the put option, the company has fixed the

payment at GBP 156000, which means that the company will get at least GBP 156,000 against

Euro 200,000 even if the exchange rate goes down to 0.50. On the other hand, the company

would get opportunity to earn unlimited profits in case the exchange rate rises beyond 0.88

levels.

Question 2 (d)

The company’s decision to hedge the foreign exchange risk shows the apprehensions of

the company about depreciation in Euro against GBP in the coming months. This shows that the

economy of Euro zone is suffering from slow growth and high inflation which is causing the

money power of Euro to decline. However, the company should take hedging position after

analyzing the economic conditions of the foreign country and home country thoroughly.

Question 3 (a)

In the current case, the management is considering a large order of goods emanating from

American Red Cross. The order amount is $30 million and also the buyer (American Red Cross)

is seeking credit terms of more than 30 days, the usual credit period. In this connection, it is

imperative for the management to assess the creditworthiness of American Red Cross so that the

credit risk or the risk of default could be managed. The following methodology should be

adopted by the management for this purpose:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

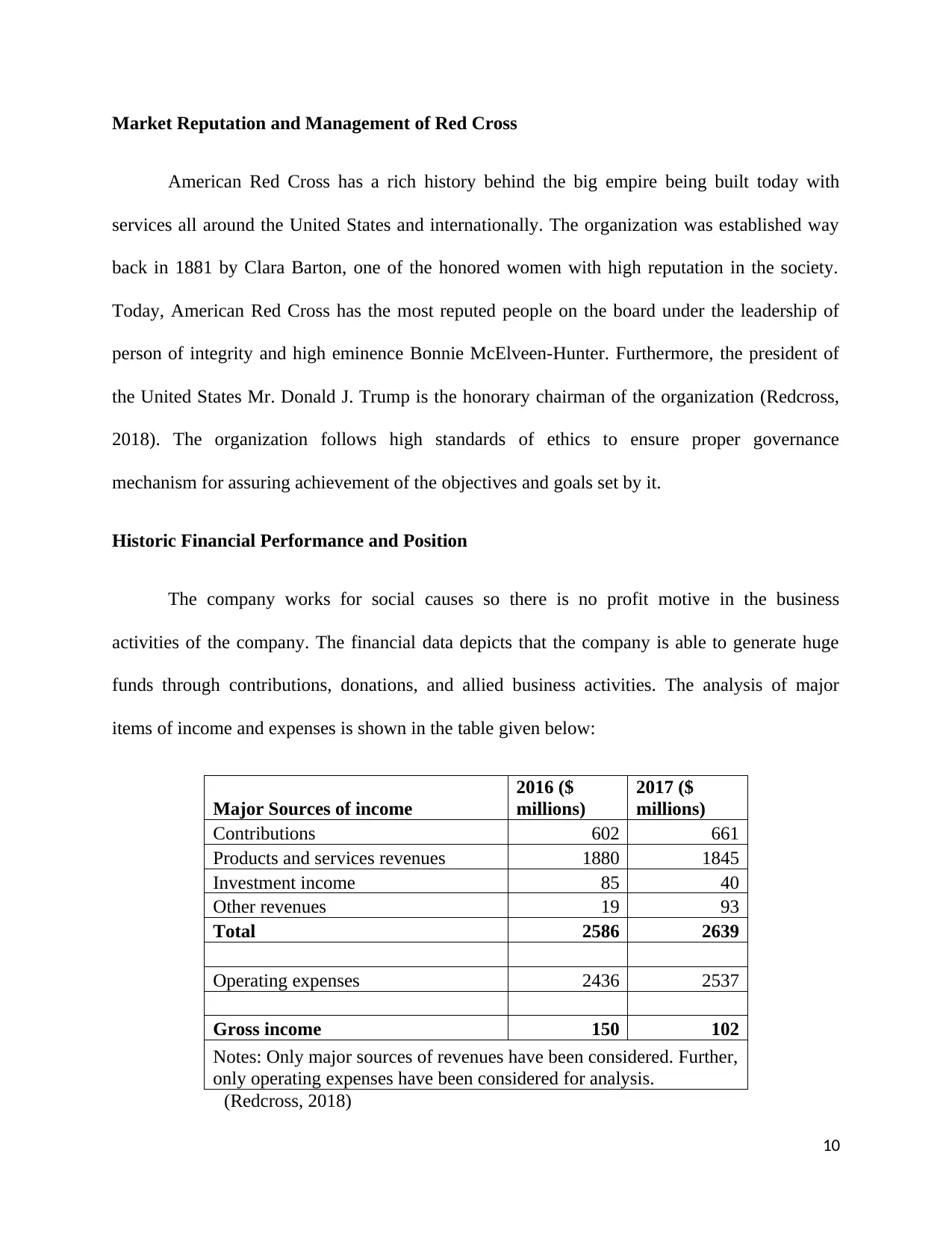

Market Reputation and Management of Red Cross

American Red Cross has a rich history behind the big empire being built today with

services all around the United States and internationally. The organization was established way

back in 1881 by Clara Barton, one of the honored women with high reputation in the society.

Today, American Red Cross has the most reputed people on the board under the leadership of

person of integrity and high eminence Bonnie McElveen-Hunter. Furthermore, the president of

the United States Mr. Donald J. Trump is the honorary chairman of the organization (Redcross,

2018). The organization follows high standards of ethics to ensure proper governance

mechanism for assuring achievement of the objectives and goals set by it.

Historic Financial Performance and Position

The company works for social causes so there is no profit motive in the business

activities of the company. The financial data depicts that the company is able to generate huge

funds through contributions, donations, and allied business activities. The analysis of major

items of income and expenses is shown in the table given below:

Major Sources of income

2016 ($

millions)

2017 ($

millions)

Contributions 602 661

Products and services revenues 1880 1845

Investment income 85 40

Other revenues 19 93

Total 2586 2639

Operating expenses 2436 2537

Gross income 150 102

Notes: Only major sources of revenues have been considered. Further,

only operating expenses have been considered for analysis.

(Redcross, 2018)

10

American Red Cross has a rich history behind the big empire being built today with

services all around the United States and internationally. The organization was established way

back in 1881 by Clara Barton, one of the honored women with high reputation in the society.

Today, American Red Cross has the most reputed people on the board under the leadership of

person of integrity and high eminence Bonnie McElveen-Hunter. Furthermore, the president of

the United States Mr. Donald J. Trump is the honorary chairman of the organization (Redcross,

2018). The organization follows high standards of ethics to ensure proper governance

mechanism for assuring achievement of the objectives and goals set by it.

Historic Financial Performance and Position

The company works for social causes so there is no profit motive in the business

activities of the company. The financial data depicts that the company is able to generate huge

funds through contributions, donations, and allied business activities. The analysis of major

items of income and expenses is shown in the table given below:

Major Sources of income

2016 ($

millions)

2017 ($

millions)

Contributions 602 661

Products and services revenues 1880 1845

Investment income 85 40

Other revenues 19 93

Total 2586 2639

Operating expenses 2436 2537

Gross income 150 102

Notes: Only major sources of revenues have been considered. Further,

only operating expenses have been considered for analysis.

(Redcross, 2018)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It could be observed that the total revenues of the company have increased from $2,586

million in the year 2016 to $2,639 million in the year 2017. The operating expenses have also

increased from $2436 million to 2537 million which shows enhancement in the scale of

operations of the company.

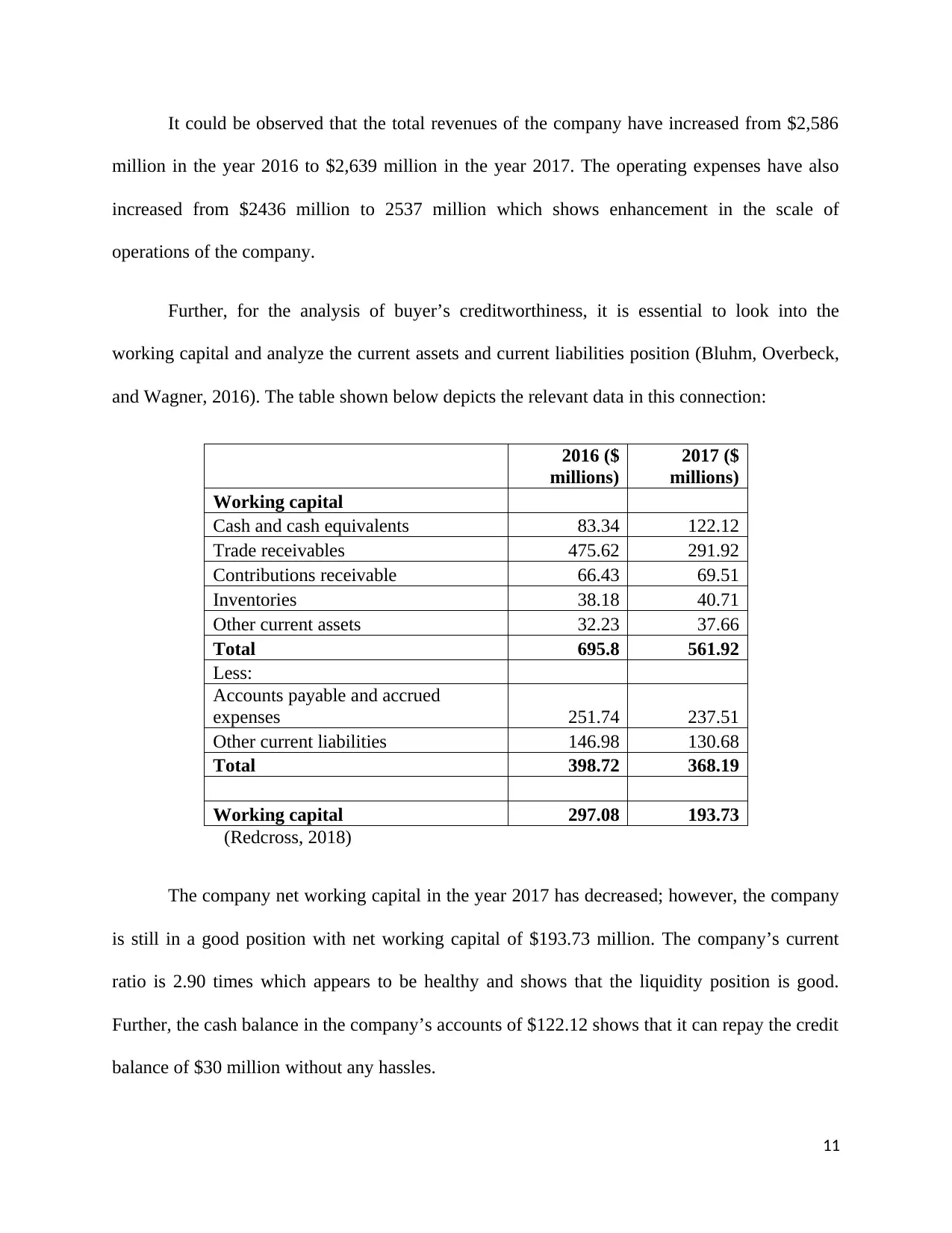

Further, for the analysis of buyer’s creditworthiness, it is essential to look into the

working capital and analyze the current assets and current liabilities position (Bluhm, Overbeck,

and Wagner, 2016). The table shown below depicts the relevant data in this connection:

2016 ($

millions)

2017 ($

millions)

Working capital

Cash and cash equivalents 83.34 122.12

Trade receivables 475.62 291.92

Contributions receivable 66.43 69.51

Inventories 38.18 40.71

Other current assets 32.23 37.66

Total 695.8 561.92

Less:

Accounts payable and accrued

expenses 251.74 237.51

Other current liabilities 146.98 130.68

Total 398.72 368.19

Working capital 297.08 193.73

(Redcross, 2018)

The company net working capital in the year 2017 has decreased; however, the company

is still in a good position with net working capital of $193.73 million. The company’s current

ratio is 2.90 times which appears to be healthy and shows that the liquidity position is good.

Further, the cash balance in the company’s accounts of $122.12 shows that it can repay the credit

balance of $30 million without any hassles.

11

million in the year 2016 to $2,639 million in the year 2017. The operating expenses have also

increased from $2436 million to 2537 million which shows enhancement in the scale of

operations of the company.

Further, for the analysis of buyer’s creditworthiness, it is essential to look into the

working capital and analyze the current assets and current liabilities position (Bluhm, Overbeck,

and Wagner, 2016). The table shown below depicts the relevant data in this connection:

2016 ($

millions)

2017 ($

millions)

Working capital

Cash and cash equivalents 83.34 122.12

Trade receivables 475.62 291.92

Contributions receivable 66.43 69.51

Inventories 38.18 40.71

Other current assets 32.23 37.66

Total 695.8 561.92

Less:

Accounts payable and accrued

expenses 251.74 237.51

Other current liabilities 146.98 130.68

Total 398.72 368.19

Working capital 297.08 193.73

(Redcross, 2018)

The company net working capital in the year 2017 has decreased; however, the company

is still in a good position with net working capital of $193.73 million. The company’s current

ratio is 2.90 times which appears to be healthy and shows that the liquidity position is good.

Further, the cash balance in the company’s accounts of $122.12 shows that it can repay the credit

balance of $30 million without any hassles.

11

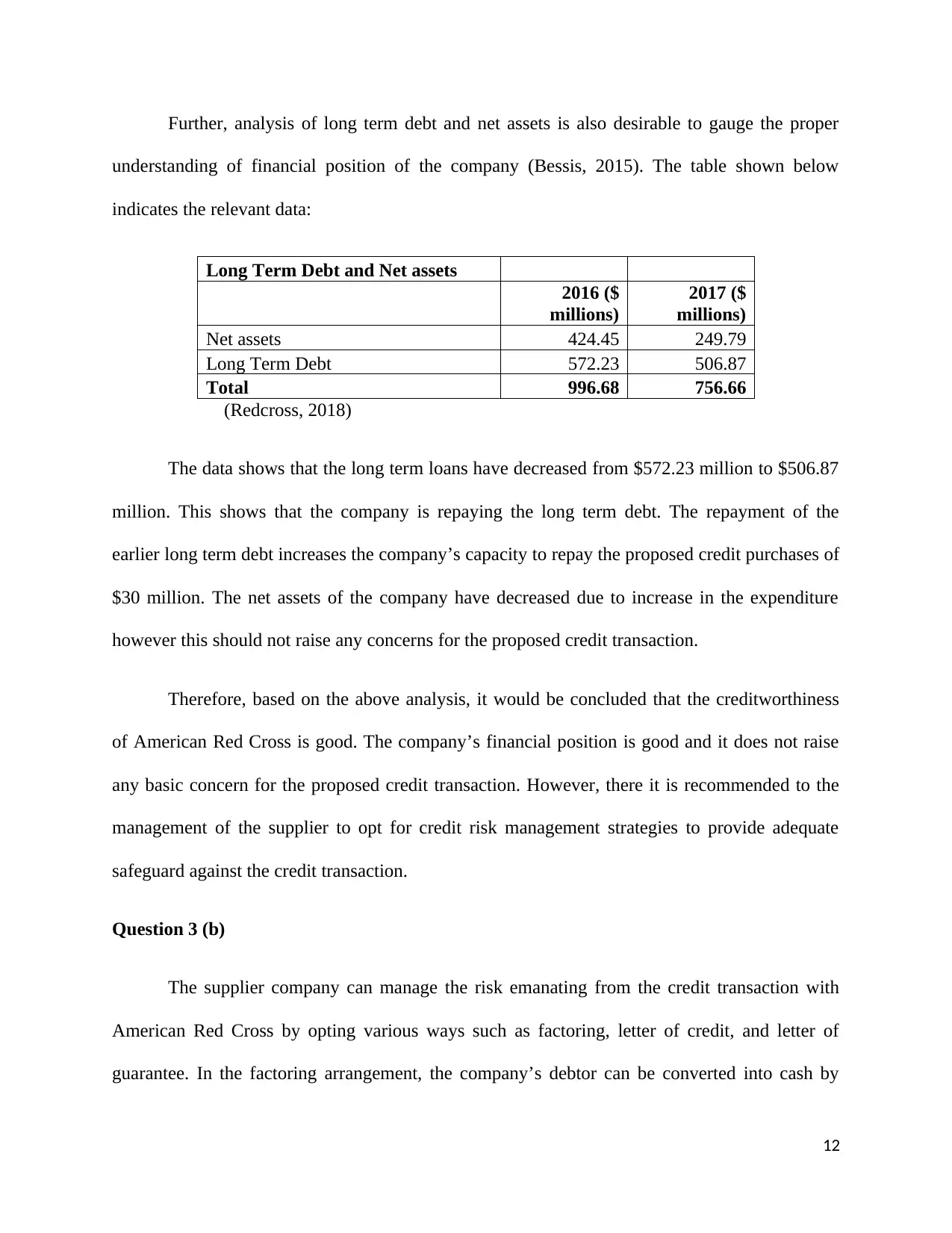

Further, analysis of long term debt and net assets is also desirable to gauge the proper

understanding of financial position of the company (Bessis, 2015). The table shown below

indicates the relevant data:

Long Term Debt and Net assets

2016 ($

millions)

2017 ($

millions)

Net assets 424.45 249.79

Long Term Debt 572.23 506.87

Total 996.68 756.66

(Redcross, 2018)

The data shows that the long term loans have decreased from $572.23 million to $506.87

million. This shows that the company is repaying the long term debt. The repayment of the

earlier long term debt increases the company’s capacity to repay the proposed credit purchases of

$30 million. The net assets of the company have decreased due to increase in the expenditure

however this should not raise any concerns for the proposed credit transaction.

Therefore, based on the above analysis, it would be concluded that the creditworthiness

of American Red Cross is good. The company’s financial position is good and it does not raise

any basic concern for the proposed credit transaction. However, there it is recommended to the

management of the supplier to opt for credit risk management strategies to provide adequate

safeguard against the credit transaction.

Question 3 (b)

The supplier company can manage the risk emanating from the credit transaction with

American Red Cross by opting various ways such as factoring, letter of credit, and letter of

guarantee. In the factoring arrangement, the company’s debtor can be converted into cash by

12

understanding of financial position of the company (Bessis, 2015). The table shown below

indicates the relevant data:

Long Term Debt and Net assets

2016 ($

millions)

2017 ($

millions)

Net assets 424.45 249.79

Long Term Debt 572.23 506.87

Total 996.68 756.66

(Redcross, 2018)

The data shows that the long term loans have decreased from $572.23 million to $506.87

million. This shows that the company is repaying the long term debt. The repayment of the

earlier long term debt increases the company’s capacity to repay the proposed credit purchases of

$30 million. The net assets of the company have decreased due to increase in the expenditure

however this should not raise any concerns for the proposed credit transaction.

Therefore, based on the above analysis, it would be concluded that the creditworthiness

of American Red Cross is good. The company’s financial position is good and it does not raise

any basic concern for the proposed credit transaction. However, there it is recommended to the

management of the supplier to opt for credit risk management strategies to provide adequate

safeguard against the credit transaction.

Question 3 (b)

The supplier company can manage the risk emanating from the credit transaction with

American Red Cross by opting various ways such as factoring, letter of credit, and letter of

guarantee. In the factoring arrangement, the company’s debtor can be converted into cash by

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.