Case Study: Financial Audit Failure - Deloitte & Touche v. Livent Inc.

VerifiedAdded on 2023/01/04

|9

|565

|47

Case Study

AI Summary

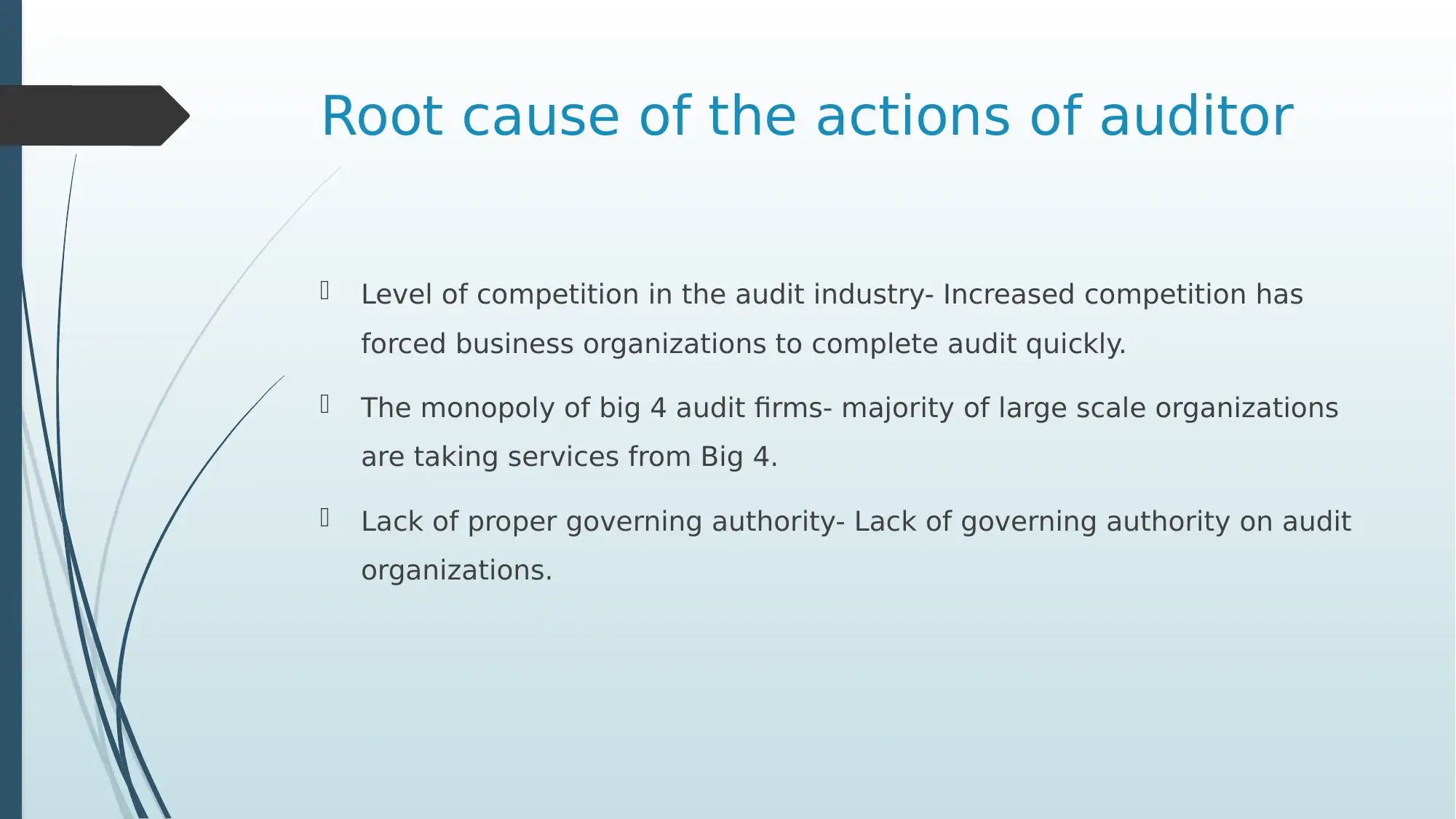

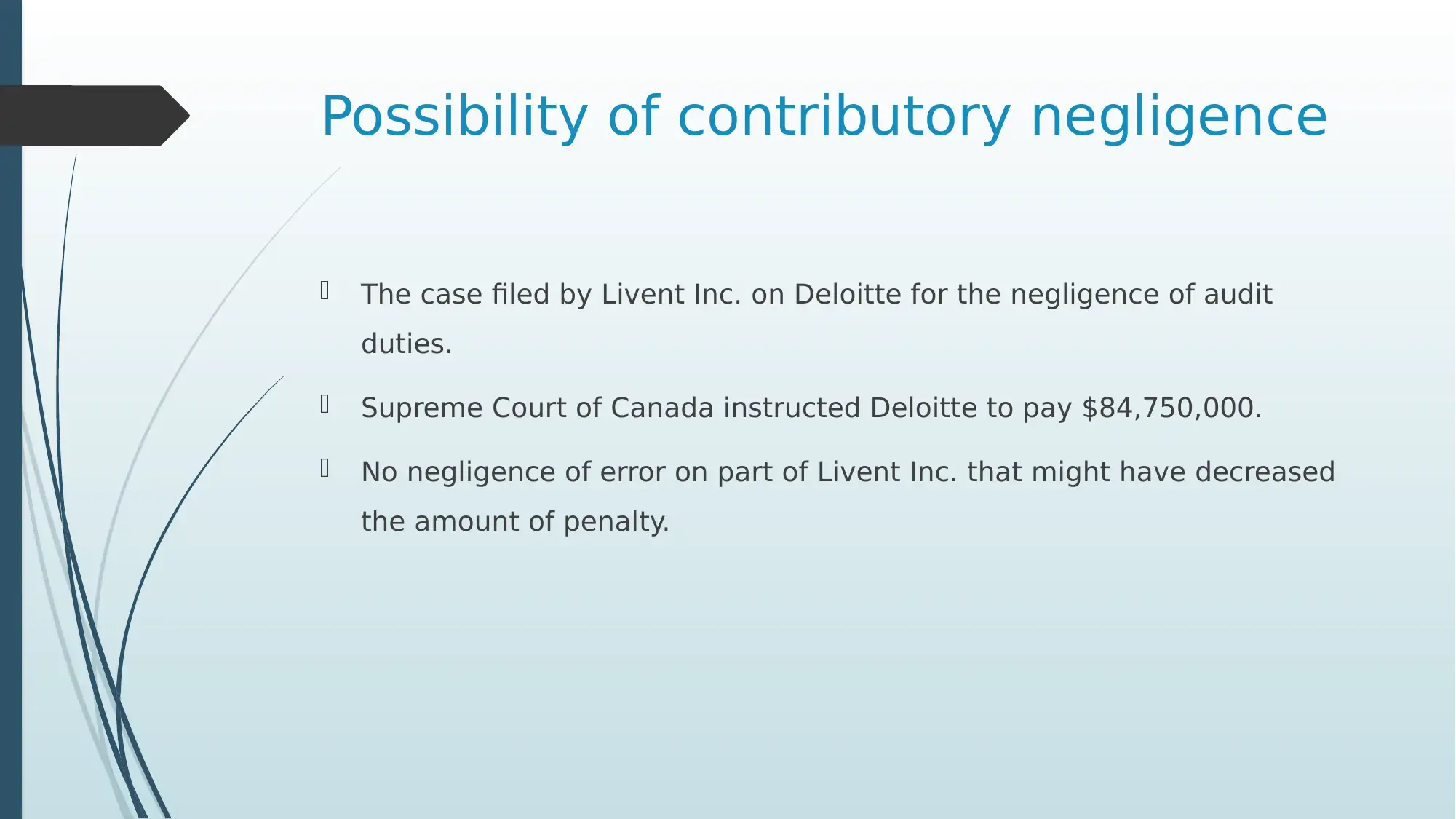

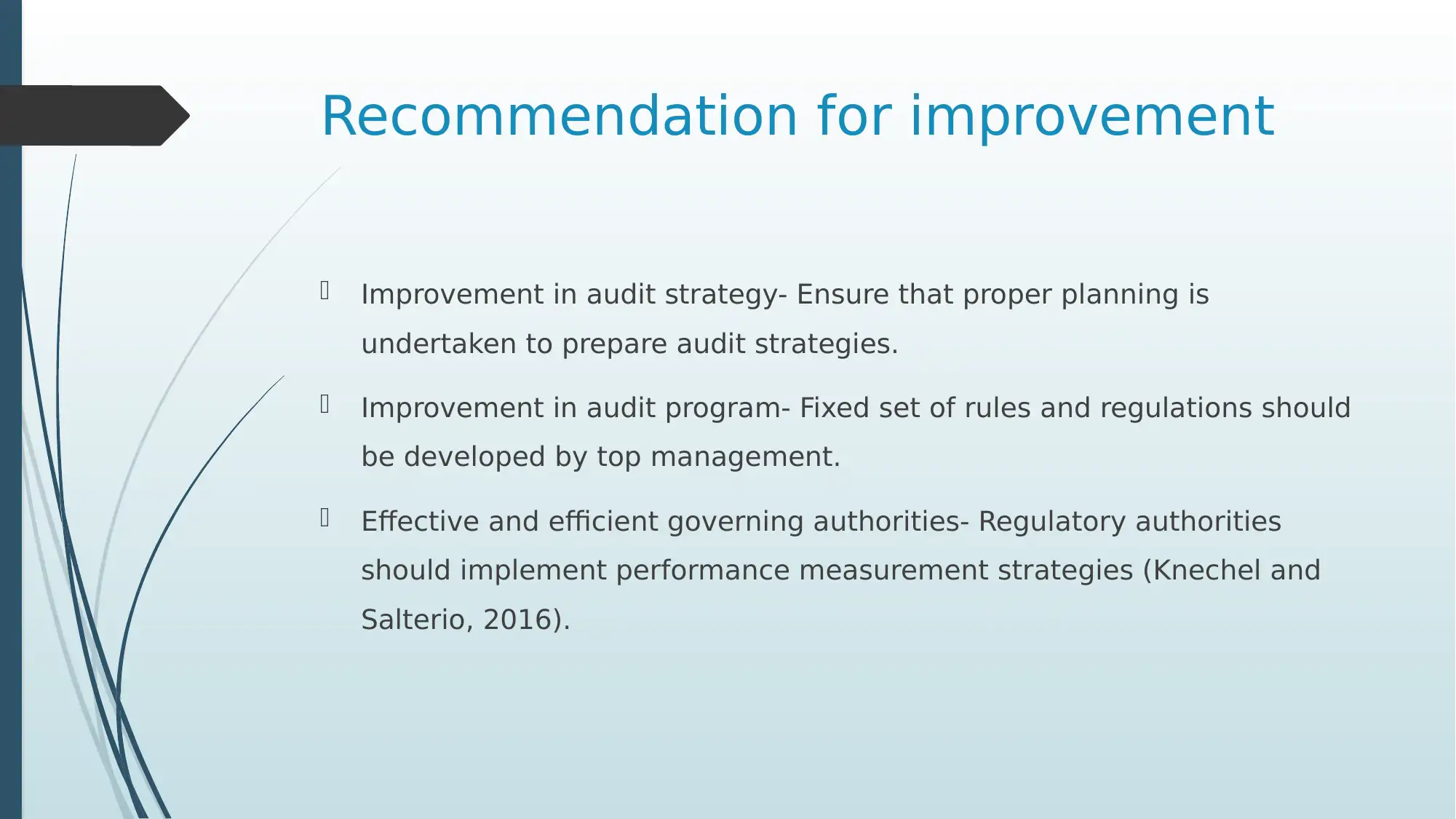

This case study analyzes the financial audit failure in the case of Deloitte & Touche v. Livent Inc. The assignment examines the responsibilities of auditors, the failure to identify misstatements in financial statements, and the subsequent legal and financial repercussions. The case highlights the negligence of Deloitte in its audit duties, the role of management and internal audit, and the impact on investors due to inaccurate financial reporting. The study explores the root causes of the audit failure, including competitive pressures and the structure of the audit industry, and recommends improvements in audit strategies, programs, and regulatory oversight. The Supreme Court of Canada's decision and the awarded penalties are also discussed, emphasizing the importance of adherence to accounting standards and the consequences of audit failures. This case study provides a comprehensive overview of the issues surrounding audit quality and the importance of effective governance in financial reporting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.