Auditing Report: Case Studies, Analysis, and Recommendations

VerifiedAdded on 2020/06/03

|10

|2251

|114

Report

AI Summary

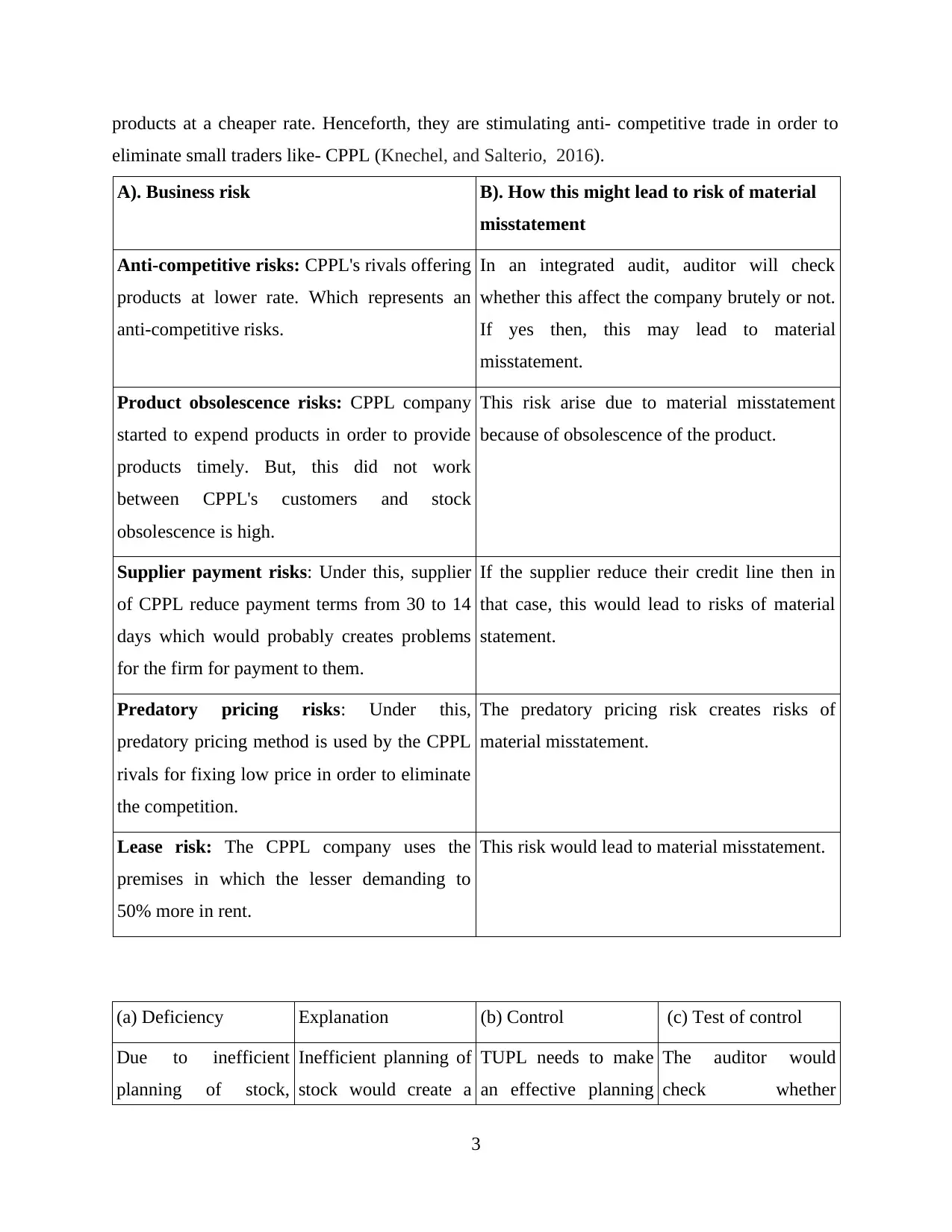

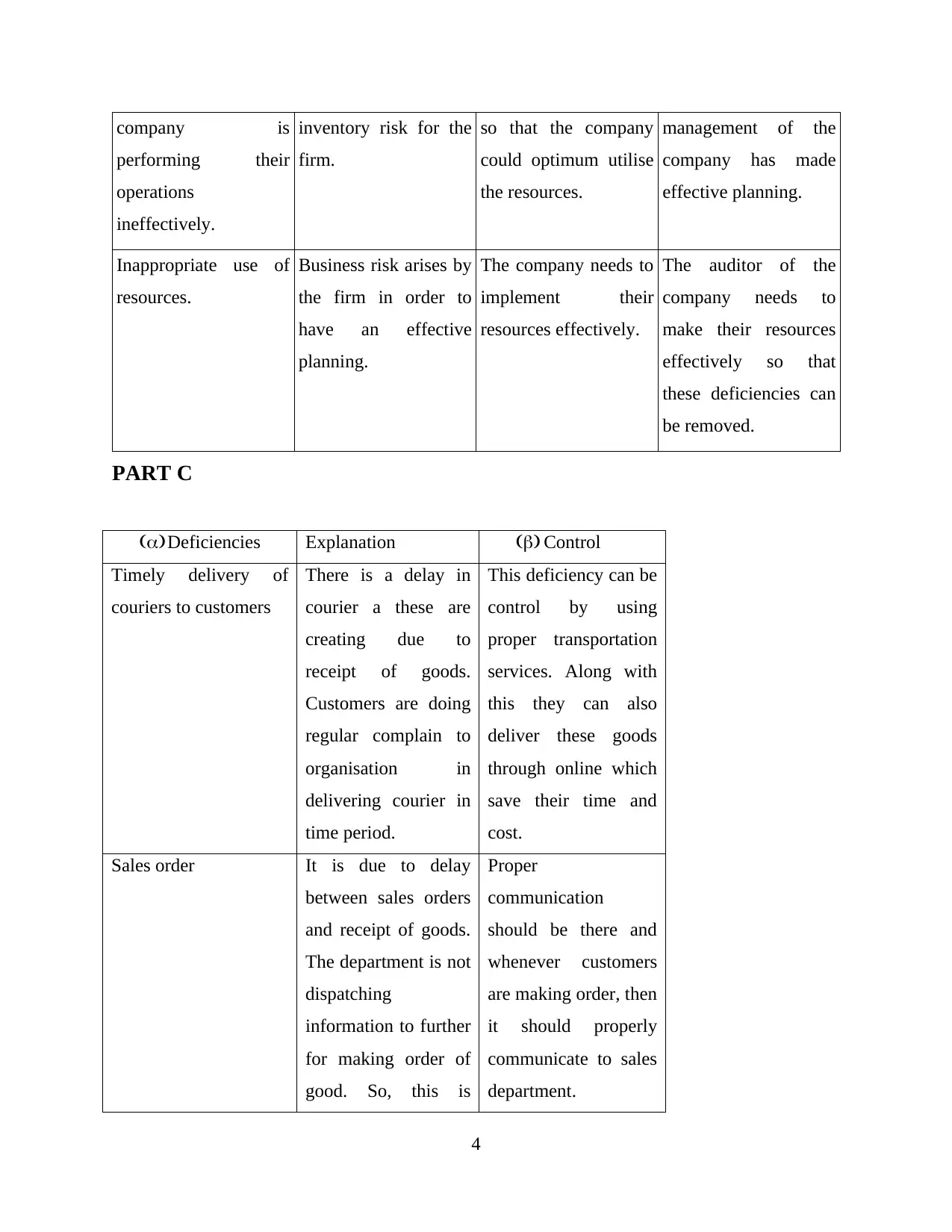

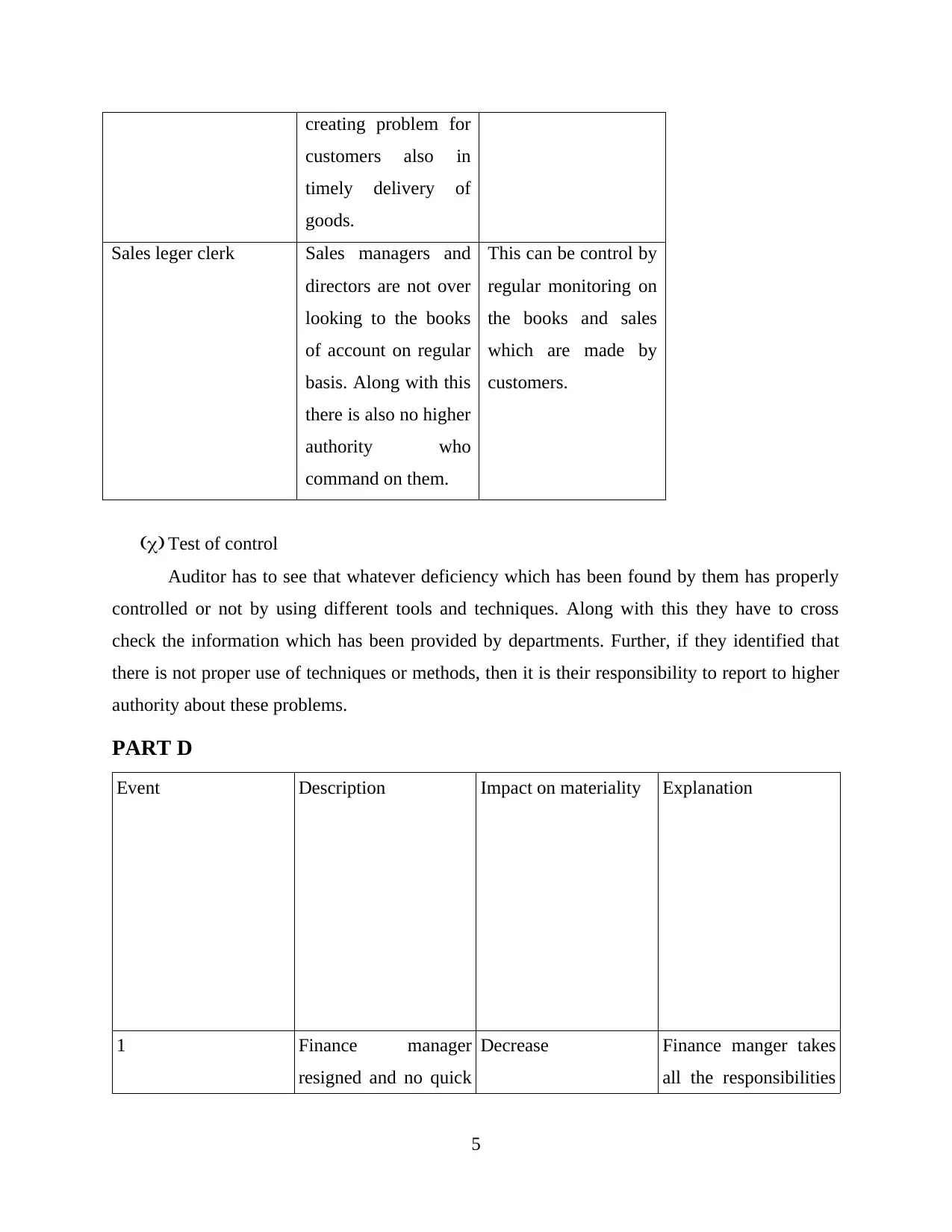

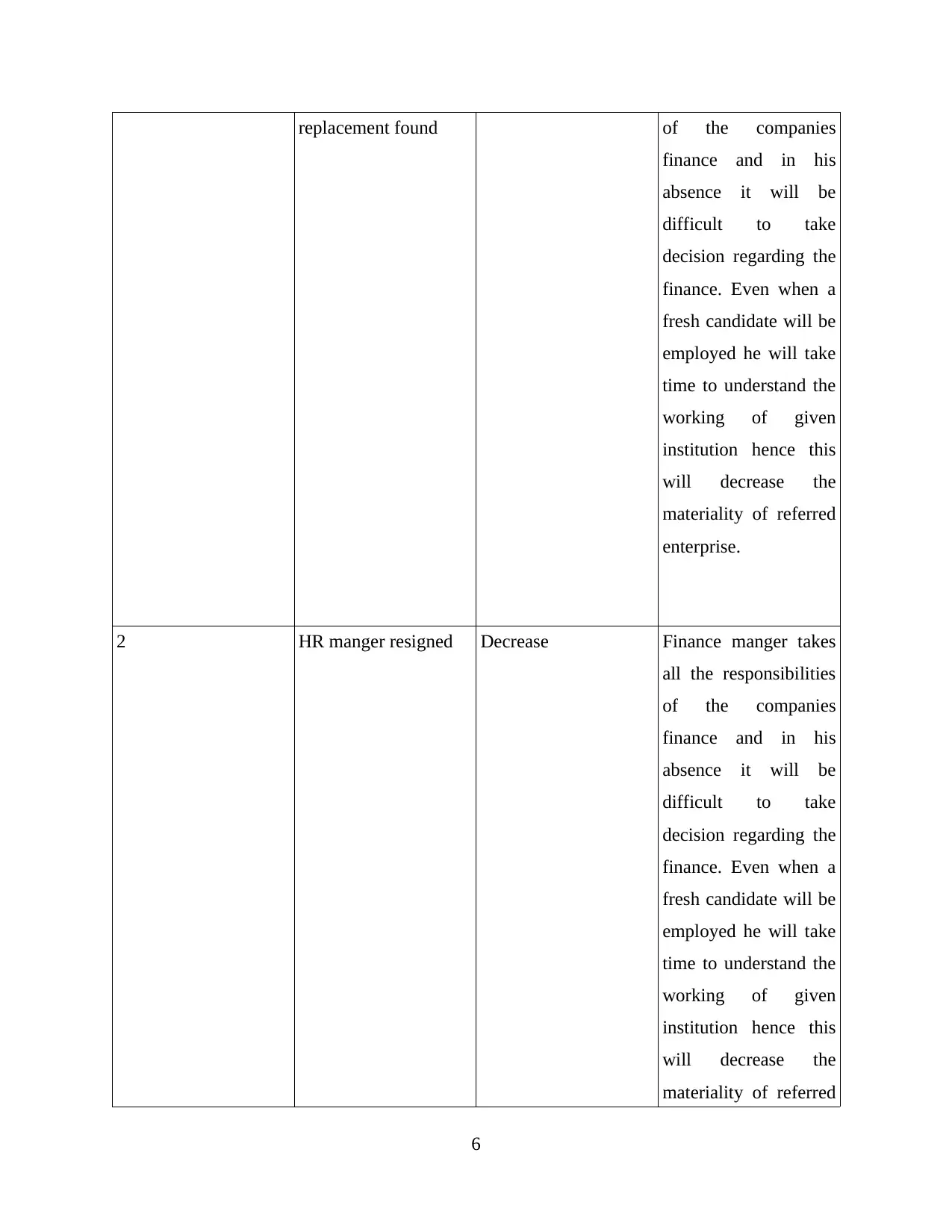

This report provides a comprehensive analysis of auditing practices, encompassing various case studies and their corresponding solutions. The report begins with an introduction to auditing, emphasizing its role in verifying financial results and meeting societal expectations. Part A delves into ethical considerations in the pharmaceutical industry, auditor responsibilities in managing hedge transactions, and the importance of sufficient audit evidence. Part B explores business risks, potential material misstatements, and the importance of internal controls, using a case study of a convenience store chain. Part C focuses on deficiencies in courier services, sales order processes, and sales ledger management, proposing control measures to address these issues. Finally, Part D examines the impact of events, such as changes in management, and errors on materiality. The report concludes by summarizing the key findings and reinforcing the importance of adhering to proper auditing standards and evaluating financial performance.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.