The Australian Banking System: Regulations, History, and Future

VerifiedAdded on 2020/04/01

|10

|3851

|53

Essay

AI Summary

This essay provides a comprehensive overview of the Australian banking system. It begins with a historical perspective, tracing the establishment and evolution of banks in Australia, including the major players and their growth. The essay then delves into the regulatory framework, outlining the roles and responsibilities of key bodies like APRA, ASIC, the Australian Treasury, and the Reserve Bank of Australia (RBA). It examines the RBA's monetary policy tools and presents a table of exchange rates. The essay also analyzes current trends, technological advancements, and potential challenges facing the banking system, such as customer satisfaction and home ownership. The analysis covers the four pillars policy and the impact of deregulation. In conclusion, the essay provides a detailed understanding of the Australian banking sector's past, present, and potential future developments.

Financial Institutions 1

Financial Institutions

Financial Institutions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Institutions 2

Introduction

This essay is based on the banking system of Australia. This essay contains past, present and

future regulation of Australian banks. This essay describes the establishment of first bank in

Australia and the years when the first bank of Australia opened its branches across Australia,

the major four banks of Australia and the sum total of domestic assets with them, the four

regulatory bodies and their roles and responsibilities in the development of banking system

and the economy of Australia, central bank of Australia and the monetary policy tools with

the central bank, a table of exchange rates of Reserve bank of Australia (Adapa and Roy,

2017). This essay contains history of almost all the banks of Australia and some factors are

also discussed which can affect the growth of banking system in future.

Research

Before 1817, there were no banks in Australia. According to Bryan Fitz-Gibbon and Marianne

Gizycki, the first bank of Australia was the Bank of New South Wales. In 1817, this bank was

established in Sydney. The bank opened its branches during nineteenth and early twentieth

century across Australia and Oceania. The first branch of this bank was opened in 1850 at

Morton Bay. Second branch was established in 1851 in Victoria then third branch was opened

in 1861 in New Zealand, fourth branch was established in 1877 in South Australia, fifth

branch was established in 1883 in Western Australia, the sixth branch was established in Fizi

in 1901 and the seventh branch was established in Tasmania in 1910 (Ahmed and Ndayisaba,

2016). After this, the Commercial banking company of Sydney was established. The next

bank after the Commercial banking company of Sydney was the National bank of Australasia.

This bank was established in 1858 and later opened its branches in Tasmania in 1859,

Western Australia in 1866, New South Wales in 1885, Queensland in 1920 and London bank

in 1864. In the opinion of G.D. Carnegie in 2016, the National Commercial banking

corporation of Australia was formed with the merger of the Commercial banking company

and the National bank of Australasia. This bank was later renamed as the National Australian

bank (Hudson, et al., 2017). During 1960s, Australian banks have adopted new technologies

in order to reduce operating costs. In Australia, automated teller machine (ATM’s)

commenced in 1969. The largest five banks which are using a number of automated teller

machine were: the NAB-redi ATM with over 3400 machines, ANZ with over 2600 machines,

the Commonwealth bank-Bank west network with over 4000 machines, Suncorp with over

2000 machines and Westpac-St.george-Bank SA and Bank of Melbourne with over 3000

machines (The Conversation, 2016).

Introduction

This essay is based on the banking system of Australia. This essay contains past, present and

future regulation of Australian banks. This essay describes the establishment of first bank in

Australia and the years when the first bank of Australia opened its branches across Australia,

the major four banks of Australia and the sum total of domestic assets with them, the four

regulatory bodies and their roles and responsibilities in the development of banking system

and the economy of Australia, central bank of Australia and the monetary policy tools with

the central bank, a table of exchange rates of Reserve bank of Australia (Adapa and Roy,

2017). This essay contains history of almost all the banks of Australia and some factors are

also discussed which can affect the growth of banking system in future.

Research

Before 1817, there were no banks in Australia. According to Bryan Fitz-Gibbon and Marianne

Gizycki, the first bank of Australia was the Bank of New South Wales. In 1817, this bank was

established in Sydney. The bank opened its branches during nineteenth and early twentieth

century across Australia and Oceania. The first branch of this bank was opened in 1850 at

Morton Bay. Second branch was established in 1851 in Victoria then third branch was opened

in 1861 in New Zealand, fourth branch was established in 1877 in South Australia, fifth

branch was established in 1883 in Western Australia, the sixth branch was established in Fizi

in 1901 and the seventh branch was established in Tasmania in 1910 (Ahmed and Ndayisaba,

2016). After this, the Commercial banking company of Sydney was established. The next

bank after the Commercial banking company of Sydney was the National bank of Australasia.

This bank was established in 1858 and later opened its branches in Tasmania in 1859,

Western Australia in 1866, New South Wales in 1885, Queensland in 1920 and London bank

in 1864. In the opinion of G.D. Carnegie in 2016, the National Commercial banking

corporation of Australia was formed with the merger of the Commercial banking company

and the National bank of Australasia. This bank was later renamed as the National Australian

bank (Hudson, et al., 2017). During 1960s, Australian banks have adopted new technologies

in order to reduce operating costs. In Australia, automated teller machine (ATM’s)

commenced in 1969. The largest five banks which are using a number of automated teller

machine were: the NAB-redi ATM with over 3400 machines, ANZ with over 2600 machines,

the Commonwealth bank-Bank west network with over 4000 machines, Suncorp with over

2000 machines and Westpac-St.george-Bank SA and Bank of Melbourne with over 3000

machines (The Conversation, 2016).

Financial Institutions 3

According to T.P. Truong, and N.N. Nguyen, N.N. (2017), there is a difference of

effectiveness, quality and accessibility between the current and previous banking. The use of

technology in the current banking system is also increased. As per the opinion of L.Goss, the

customers were not satisfied with the services of banking system and said that lack of face-to-

face communication due to the excessive use of technology is the root cause for this

unsatisfaction. At the same time, the educated customers find it feasible because they are able

to do most of their banking formalities by the help of their mobile phones. Another

shortcoming was described by Tracey Dagger and Jillian Sweeney in the year 2007 that in the

initial stages, consumers rely on search based attributes. As per the view of Greg Jericho, the

retirement system is in trouble if the home ownership continues to shrink. As per the last

year’s census, only 34.5% of homes are owned with a mortgage. So, Australians are less

interested in buying homes than they were in past. As per the opinion of A. Lui, (2016), there

is integration between prudential regulation and financial stability.

After Federation

In 1910, parliament passed Australian notes. Before this, treasury notes and private bank

notes were circulated in Australia. 10% per annum tax was imposed under the Bank notes tax

act, 1910 on the banks notes issued or re-issued by any bank in the common-wealth and not

redeemed. This act leads to the end of notes issued by Queensland treasury and trading banks.

The Commonwealth bank was established by the Federal government during 1911 and it

opened its branches in six states by 1913 (International Monetary Fund, 2015). During 1980,

Australia had only a few banks as compared to other countries like Hong Kong and United

States. In Australia, the banks were classified into two categories i.e. trading banks and

savings banks. The trading banks did not provide any facilities to the general public. Savings

banks were the banks in which compulsory mortgage were needed for lending and they

charge no interest from the depositors.

Deregulation

In the mid 1960s, all the banks were allowed to operate in money market by removing the

separation of trading and savings bank. The banks were free to set their own interest rates.

During 1990, the Australian government adopted four pillars policy (MacDonald and van

Oordt, 2017). As per this policy, mergers were not allowed between the big four banks. These

four banks were not allowed to acquire any small bank. But this policy was breached when

the Commonwealth bank acquired the State bank of Victoria and West bank. Similarly,

Westpac acquired the Challenge bank, St. George bank and Bank of Melbourne.

According to T.P. Truong, and N.N. Nguyen, N.N. (2017), there is a difference of

effectiveness, quality and accessibility between the current and previous banking. The use of

technology in the current banking system is also increased. As per the opinion of L.Goss, the

customers were not satisfied with the services of banking system and said that lack of face-to-

face communication due to the excessive use of technology is the root cause for this

unsatisfaction. At the same time, the educated customers find it feasible because they are able

to do most of their banking formalities by the help of their mobile phones. Another

shortcoming was described by Tracey Dagger and Jillian Sweeney in the year 2007 that in the

initial stages, consumers rely on search based attributes. As per the view of Greg Jericho, the

retirement system is in trouble if the home ownership continues to shrink. As per the last

year’s census, only 34.5% of homes are owned with a mortgage. So, Australians are less

interested in buying homes than they were in past. As per the opinion of A. Lui, (2016), there

is integration between prudential regulation and financial stability.

After Federation

In 1910, parliament passed Australian notes. Before this, treasury notes and private bank

notes were circulated in Australia. 10% per annum tax was imposed under the Bank notes tax

act, 1910 on the banks notes issued or re-issued by any bank in the common-wealth and not

redeemed. This act leads to the end of notes issued by Queensland treasury and trading banks.

The Commonwealth bank was established by the Federal government during 1911 and it

opened its branches in six states by 1913 (International Monetary Fund, 2015). During 1980,

Australia had only a few banks as compared to other countries like Hong Kong and United

States. In Australia, the banks were classified into two categories i.e. trading banks and

savings banks. The trading banks did not provide any facilities to the general public. Savings

banks were the banks in which compulsory mortgage were needed for lending and they

charge no interest from the depositors.

Deregulation

In the mid 1960s, all the banks were allowed to operate in money market by removing the

separation of trading and savings bank. The banks were free to set their own interest rates.

During 1990, the Australian government adopted four pillars policy (MacDonald and van

Oordt, 2017). As per this policy, mergers were not allowed between the big four banks. These

four banks were not allowed to acquire any small bank. But this policy was breached when

the Commonwealth bank acquired the State bank of Victoria and West bank. Similarly,

Westpac acquired the Challenge bank, St. George bank and Bank of Melbourne.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Institutions 4

Analysis

It is analysed that there are 53 banks which are operating in Australia. The four major banks

of Australia include National Australia bank, ANZ banking group, Westpac banking group

and Commonwealth bank of Australia. The sum of assets with these four banks is around

$960 billion (Salter, et al., 2017). The Australian financial system is regulated by four

agencies i.e. the Australian Prudential Regulation Authority (APRA), the Australian Treasury,

the Australian securities and Investments Commission (ASIC) and the Reserve Bank of

Australia (RBA). The regulators are mainly ASIC and APRA. The main aim of Australian

securities and Investments commission is to prevent consumers from the manipulative market.

ASIC also takes of the licences of the participants of the financial system. The responsibilities

of Australian securities and investment commission include consumer protection, integrity of

market and the regulation of finance companies and investment banks (Truong and Nguyen,

2017). Australian securities and investment commission is having two types of EDRs

(External Dispute resolution Schemes) which are operating in Australia. One is Credit and

Investment Ombudsman (CIO) and second is Financial Ombudsman Service (FOS). The role

of both EDRs is to receive complaints and to work on these complaints in order to solve them.

These both are non-governmental and non-profit organizations. Financial service providers,

banks and financial advisors provide funds for these EDRs (Goss, 2017). APRA is the

regulator of the financial services of Australia. The vision of APRA is excellence in

supervision so that it will become the prudential regulator. Its mission is to make an efficient,

effective and competitive financial system. The financial transactions of Australia are

protected by APRA. The major values of APRA include excellence, integrity, honesty,

accountability and collaboration. The Australian Prudential Regulation authority is

responsible for the general insurance and reinsurance companies, credit unions, private health

insurance, building societies and members of the superannuation industry. The industries

which are supervised by APRA, provides funds for the regulation of it. The approach of

APRA is forward-looking so the main responsibility related to it is the estimation of risk that

is related with the future. The Australian treasury is the department of Australian government

(Sheedy, et al., 2017). Their main roles of Australian treasury are related to the budget, fiscal

policy, economic stability and regulation of the market.

The department of treasury was developed in January, 1901. The Australian treasury

department has four parts i.e. markets, fiscal, revenue and macroeconomics. The Australian

treasury’s main responsibility is related to these four departments. First is maintaining a sound

macroeconomic environment. The treasury analysis the opportunities and threats in overseas

Analysis

It is analysed that there are 53 banks which are operating in Australia. The four major banks

of Australia include National Australia bank, ANZ banking group, Westpac banking group

and Commonwealth bank of Australia. The sum of assets with these four banks is around

$960 billion (Salter, et al., 2017). The Australian financial system is regulated by four

agencies i.e. the Australian Prudential Regulation Authority (APRA), the Australian Treasury,

the Australian securities and Investments Commission (ASIC) and the Reserve Bank of

Australia (RBA). The regulators are mainly ASIC and APRA. The main aim of Australian

securities and Investments commission is to prevent consumers from the manipulative market.

ASIC also takes of the licences of the participants of the financial system. The responsibilities

of Australian securities and investment commission include consumer protection, integrity of

market and the regulation of finance companies and investment banks (Truong and Nguyen,

2017). Australian securities and investment commission is having two types of EDRs

(External Dispute resolution Schemes) which are operating in Australia. One is Credit and

Investment Ombudsman (CIO) and second is Financial Ombudsman Service (FOS). The role

of both EDRs is to receive complaints and to work on these complaints in order to solve them.

These both are non-governmental and non-profit organizations. Financial service providers,

banks and financial advisors provide funds for these EDRs (Goss, 2017). APRA is the

regulator of the financial services of Australia. The vision of APRA is excellence in

supervision so that it will become the prudential regulator. Its mission is to make an efficient,

effective and competitive financial system. The financial transactions of Australia are

protected by APRA. The major values of APRA include excellence, integrity, honesty,

accountability and collaboration. The Australian Prudential Regulation authority is

responsible for the general insurance and reinsurance companies, credit unions, private health

insurance, building societies and members of the superannuation industry. The industries

which are supervised by APRA, provides funds for the regulation of it. The approach of

APRA is forward-looking so the main responsibility related to it is the estimation of risk that

is related with the future. The Australian treasury is the department of Australian government

(Sheedy, et al., 2017). Their main roles of Australian treasury are related to the budget, fiscal

policy, economic stability and regulation of the market.

The department of treasury was developed in January, 1901. The Australian treasury

department has four parts i.e. markets, fiscal, revenue and macroeconomics. The Australian

treasury’s main responsibility is related to these four departments. First is maintaining a sound

macroeconomic environment. The treasury analysis the opportunities and threats in overseas

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Institutions 5

and Australia and then on the basis of this analysis it will help in the planning of

macroeconomic policies (Orsmond and Price, 2016). The treasury also takes care of the

foreign investments and make sure that it will not affect the interests of consumers of

Australia. One more responsibility of Treasury is to provide advice on the expenditure by the

government, revenue from taxes and the fiscal policy. Fiscal policy is the policy that is used

to control inflation and government expenditure. The main objective of fiscal policy is to

maintain equilibrium in balance of payments (BOP). Balance of payment is a record of

country’s transactions with rest of the world. Fiscal policy aims at controlling inflation by

attracting exports and reducing imports. Inflation increases in the prices of products year by

year and affects the financial system of the economy. Inflation can be measured in three ways:

1. Consumer Price Index (CPI): CPI compares the prices of commodities in the base year with

current year. It measures retail market prices. 2. Producer price index (PPI): It measures the

change in the selling price received by the producers for their outputs over a period of time. 3.

GDP deflator: GDP deflator is the most commonly used technique to measure inflation. But

RBA and Government do not prefer to use this because it evaluates data on quarterly basis for

the smooth arrangements related to retirement income and taxation, treasury department is

responsible. Reserve bank of Australia (RBA) is the central bank of Australia. The roles of

Reserve bank of Australia include management of the monetary policy, full employment and

making a balance between the incomes and expenses of the country. The Reserve bank act,

1959 gives powers to Reserve bank of Australia. It also manages foreign exchange reserves

and Australia’s gold. Reserve bank is responsible for the management of monetary policy of

Australia. The primary objective of monetary policy is to manage the money supply of an

economy (Lin and Cheng, 2016). Monetary policy tools with RBA are: First is Repo rate and

reverse repo rate: Repo rate is the rate at which clients borrow money from RBI. Reverse repo

rate is the rate at which RBI borrows money from commercial banks. Second is Cash Reserve

Ratio (CRR): CRR is a certain percentage of a bank’s total deposits that is compulsorily

required to be deposited with RBA. Third is Statutory Liquidity Ratio (SLR): SLR refers to

the percentage of bank’s deposits that they are compulsorily required to invest in government

securities. Fourth is Bank rate: Bank rate is the rate charged by RBA on loans and advances to

commercial banks. Fifth is Open market operations: An open market operation refers to the

buying and selling of government securities by RBA (Export.gov, 2017). Government is also

offering concession in excise duty on the goods produced within the country to attract foreign

investors to invest domestically.

Current exchange rates of RBA

and Australia and then on the basis of this analysis it will help in the planning of

macroeconomic policies (Orsmond and Price, 2016). The treasury also takes care of the

foreign investments and make sure that it will not affect the interests of consumers of

Australia. One more responsibility of Treasury is to provide advice on the expenditure by the

government, revenue from taxes and the fiscal policy. Fiscal policy is the policy that is used

to control inflation and government expenditure. The main objective of fiscal policy is to

maintain equilibrium in balance of payments (BOP). Balance of payment is a record of

country’s transactions with rest of the world. Fiscal policy aims at controlling inflation by

attracting exports and reducing imports. Inflation increases in the prices of products year by

year and affects the financial system of the economy. Inflation can be measured in three ways:

1. Consumer Price Index (CPI): CPI compares the prices of commodities in the base year with

current year. It measures retail market prices. 2. Producer price index (PPI): It measures the

change in the selling price received by the producers for their outputs over a period of time. 3.

GDP deflator: GDP deflator is the most commonly used technique to measure inflation. But

RBA and Government do not prefer to use this because it evaluates data on quarterly basis for

the smooth arrangements related to retirement income and taxation, treasury department is

responsible. Reserve bank of Australia (RBA) is the central bank of Australia. The roles of

Reserve bank of Australia include management of the monetary policy, full employment and

making a balance between the incomes and expenses of the country. The Reserve bank act,

1959 gives powers to Reserve bank of Australia. It also manages foreign exchange reserves

and Australia’s gold. Reserve bank is responsible for the management of monetary policy of

Australia. The primary objective of monetary policy is to manage the money supply of an

economy (Lin and Cheng, 2016). Monetary policy tools with RBA are: First is Repo rate and

reverse repo rate: Repo rate is the rate at which clients borrow money from RBI. Reverse repo

rate is the rate at which RBI borrows money from commercial banks. Second is Cash Reserve

Ratio (CRR): CRR is a certain percentage of a bank’s total deposits that is compulsorily

required to be deposited with RBA. Third is Statutory Liquidity Ratio (SLR): SLR refers to

the percentage of bank’s deposits that they are compulsorily required to invest in government

securities. Fourth is Bank rate: Bank rate is the rate charged by RBA on loans and advances to

commercial banks. Fifth is Open market operations: An open market operation refers to the

buying and selling of government securities by RBA (Export.gov, 2017). Government is also

offering concession in excise duty on the goods produced within the country to attract foreign

investors to invest domestically.

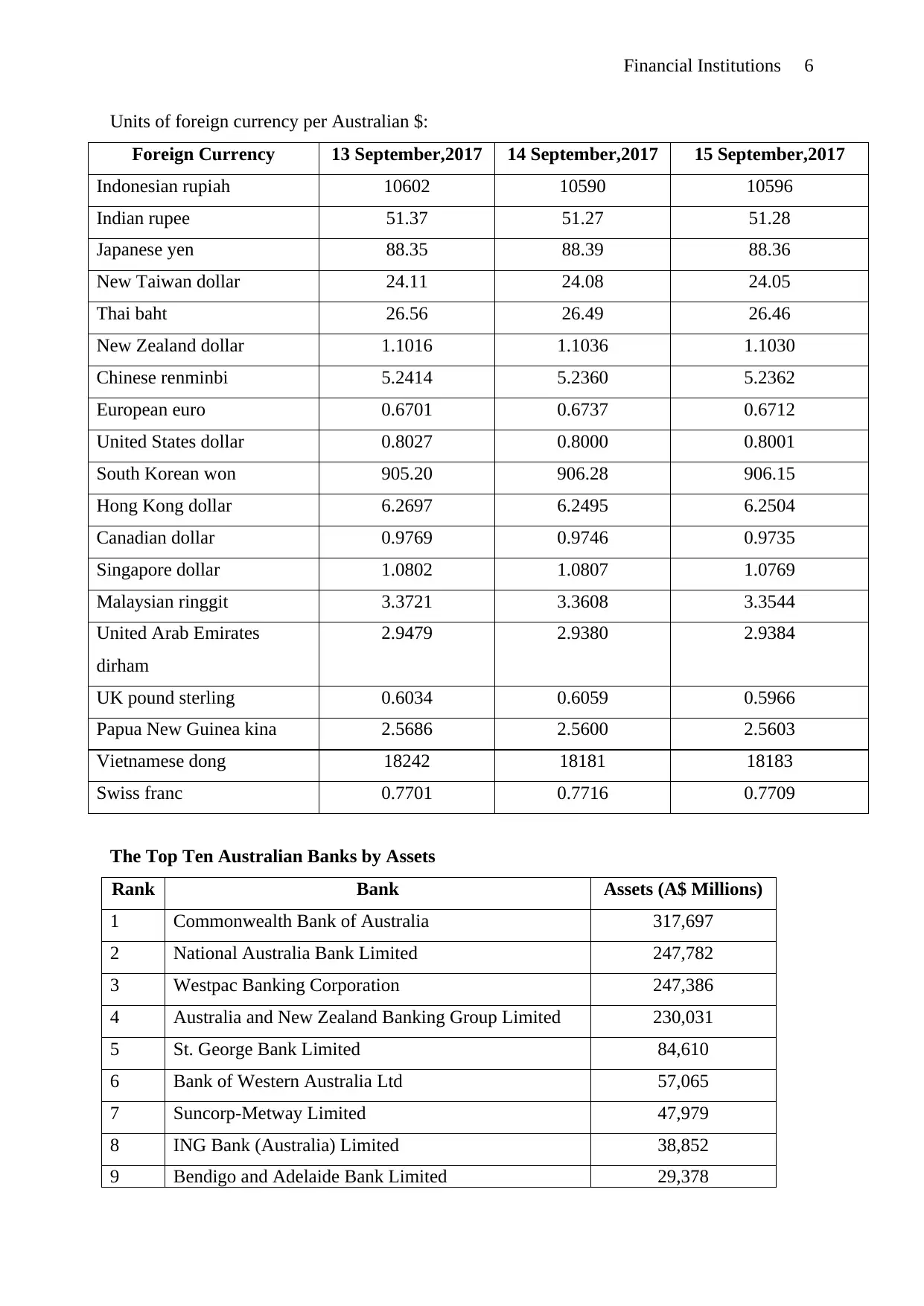

Current exchange rates of RBA

Financial Institutions 6

Units of foreign currency per Australian $:

Foreign Currency 13 September,2017 14 September,2017 15 September,2017

Indonesian rupiah 10602 10590 10596

Indian rupee 51.37 51.27 51.28

Japanese yen 88.35 88.39 88.36

New Taiwan dollar 24.11 24.08 24.05

Thai baht 26.56 26.49 26.46

New Zealand dollar 1.1016 1.1036 1.1030

Chinese renminbi 5.2414 5.2360 5.2362

European euro 0.6701 0.6737 0.6712

United States dollar 0.8027 0.8000 0.8001

South Korean won 905.20 906.28 906.15

Hong Kong dollar 6.2697 6.2495 6.2504

Canadian dollar 0.9769 0.9746 0.9735

Singapore dollar 1.0802 1.0807 1.0769

Malaysian ringgit 3.3721 3.3608 3.3544

United Arab Emirates

dirham

2.9479 2.9380 2.9384

UK pound sterling 0.6034 0.6059 0.5966

Papua New Guinea kina 2.5686 2.5600 2.5603

Vietnamese dong 18242 18181 18183

Swiss franc 0.7701 0.7716 0.7709

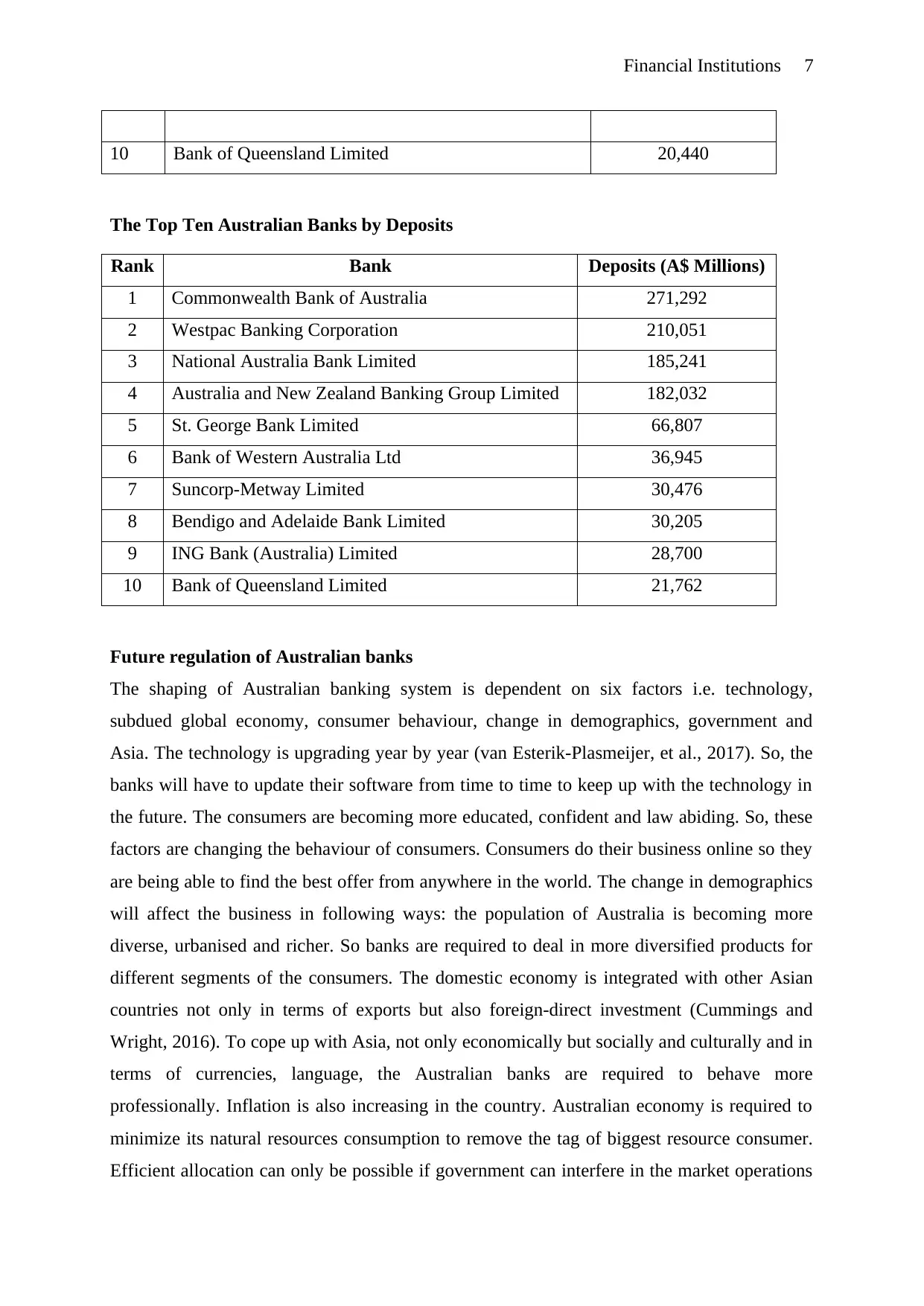

The Top Ten Australian Banks by Assets

Rank Bank Assets (A$ Millions)

1 Commonwealth Bank of Australia 317,697

2 National Australia Bank Limited 247,782

3 Westpac Banking Corporation 247,386

4 Australia and New Zealand Banking Group Limited 230,031

5 St. George Bank Limited 84,610

6 Bank of Western Australia Ltd 57,065

7 Suncorp-Metway Limited 47,979

8 ING Bank (Australia) Limited 38,852

9 Bendigo and Adelaide Bank Limited 29,378

Units of foreign currency per Australian $:

Foreign Currency 13 September,2017 14 September,2017 15 September,2017

Indonesian rupiah 10602 10590 10596

Indian rupee 51.37 51.27 51.28

Japanese yen 88.35 88.39 88.36

New Taiwan dollar 24.11 24.08 24.05

Thai baht 26.56 26.49 26.46

New Zealand dollar 1.1016 1.1036 1.1030

Chinese renminbi 5.2414 5.2360 5.2362

European euro 0.6701 0.6737 0.6712

United States dollar 0.8027 0.8000 0.8001

South Korean won 905.20 906.28 906.15

Hong Kong dollar 6.2697 6.2495 6.2504

Canadian dollar 0.9769 0.9746 0.9735

Singapore dollar 1.0802 1.0807 1.0769

Malaysian ringgit 3.3721 3.3608 3.3544

United Arab Emirates

dirham

2.9479 2.9380 2.9384

UK pound sterling 0.6034 0.6059 0.5966

Papua New Guinea kina 2.5686 2.5600 2.5603

Vietnamese dong 18242 18181 18183

Swiss franc 0.7701 0.7716 0.7709

The Top Ten Australian Banks by Assets

Rank Bank Assets (A$ Millions)

1 Commonwealth Bank of Australia 317,697

2 National Australia Bank Limited 247,782

3 Westpac Banking Corporation 247,386

4 Australia and New Zealand Banking Group Limited 230,031

5 St. George Bank Limited 84,610

6 Bank of Western Australia Ltd 57,065

7 Suncorp-Metway Limited 47,979

8 ING Bank (Australia) Limited 38,852

9 Bendigo and Adelaide Bank Limited 29,378

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Institutions 7

10 Bank of Queensland Limited 20,440

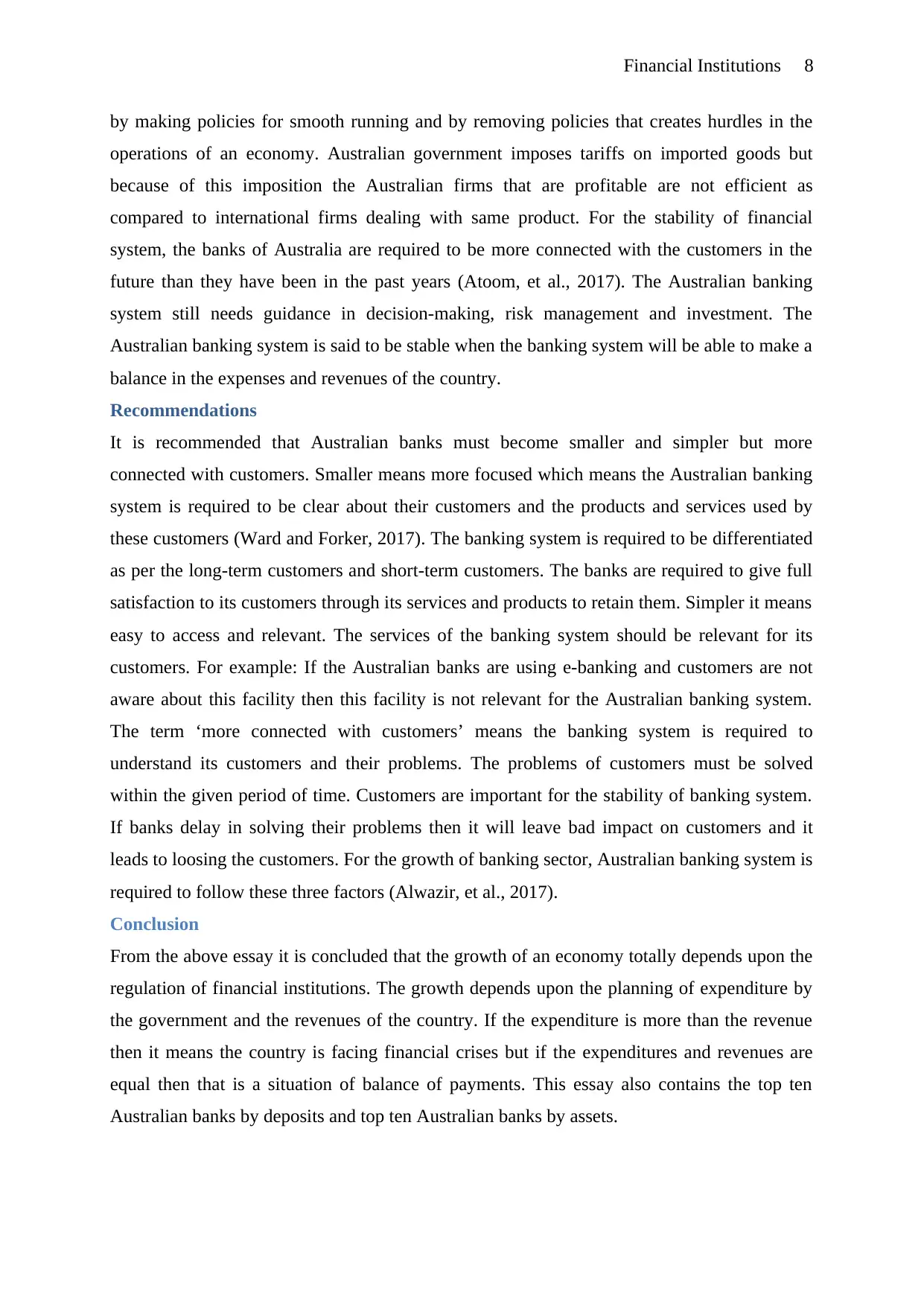

The Top Ten Australian Banks by Deposits

Rank Bank Deposits (A$ Millions)

1 Commonwealth Bank of Australia 271,292

2 Westpac Banking Corporation 210,051

3 National Australia Bank Limited 185,241

4 Australia and New Zealand Banking Group Limited 182,032

5 St. George Bank Limited 66,807

6 Bank of Western Australia Ltd 36,945

7 Suncorp-Metway Limited 30,476

8 Bendigo and Adelaide Bank Limited 30,205

9 ING Bank (Australia) Limited 28,700

10 Bank of Queensland Limited 21,762

Future regulation of Australian banks

The shaping of Australian banking system is dependent on six factors i.e. technology,

subdued global economy, consumer behaviour, change in demographics, government and

Asia. The technology is upgrading year by year (van Esterik-Plasmeijer, et al., 2017). So, the

banks will have to update their software from time to time to keep up with the technology in

the future. The consumers are becoming more educated, confident and law abiding. So, these

factors are changing the behaviour of consumers. Consumers do their business online so they

are being able to find the best offer from anywhere in the world. The change in demographics

will affect the business in following ways: the population of Australia is becoming more

diverse, urbanised and richer. So banks are required to deal in more diversified products for

different segments of the consumers. The domestic economy is integrated with other Asian

countries not only in terms of exports but also foreign-direct investment (Cummings and

Wright, 2016). To cope up with Asia, not only economically but socially and culturally and in

terms of currencies, language, the Australian banks are required to behave more

professionally. Inflation is also increasing in the country. Australian economy is required to

minimize its natural resources consumption to remove the tag of biggest resource consumer.

Efficient allocation can only be possible if government can interfere in the market operations

10 Bank of Queensland Limited 20,440

The Top Ten Australian Banks by Deposits

Rank Bank Deposits (A$ Millions)

1 Commonwealth Bank of Australia 271,292

2 Westpac Banking Corporation 210,051

3 National Australia Bank Limited 185,241

4 Australia and New Zealand Banking Group Limited 182,032

5 St. George Bank Limited 66,807

6 Bank of Western Australia Ltd 36,945

7 Suncorp-Metway Limited 30,476

8 Bendigo and Adelaide Bank Limited 30,205

9 ING Bank (Australia) Limited 28,700

10 Bank of Queensland Limited 21,762

Future regulation of Australian banks

The shaping of Australian banking system is dependent on six factors i.e. technology,

subdued global economy, consumer behaviour, change in demographics, government and

Asia. The technology is upgrading year by year (van Esterik-Plasmeijer, et al., 2017). So, the

banks will have to update their software from time to time to keep up with the technology in

the future. The consumers are becoming more educated, confident and law abiding. So, these

factors are changing the behaviour of consumers. Consumers do their business online so they

are being able to find the best offer from anywhere in the world. The change in demographics

will affect the business in following ways: the population of Australia is becoming more

diverse, urbanised and richer. So banks are required to deal in more diversified products for

different segments of the consumers. The domestic economy is integrated with other Asian

countries not only in terms of exports but also foreign-direct investment (Cummings and

Wright, 2016). To cope up with Asia, not only economically but socially and culturally and in

terms of currencies, language, the Australian banks are required to behave more

professionally. Inflation is also increasing in the country. Australian economy is required to

minimize its natural resources consumption to remove the tag of biggest resource consumer.

Efficient allocation can only be possible if government can interfere in the market operations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Institutions 8

by making policies for smooth running and by removing policies that creates hurdles in the

operations of an economy. Australian government imposes tariffs on imported goods but

because of this imposition the Australian firms that are profitable are not efficient as

compared to international firms dealing with same product. For the stability of financial

system, the banks of Australia are required to be more connected with the customers in the

future than they have been in the past years (Atoom, et al., 2017). The Australian banking

system still needs guidance in decision-making, risk management and investment. The

Australian banking system is said to be stable when the banking system will be able to make a

balance in the expenses and revenues of the country.

Recommendations

It is recommended that Australian banks must become smaller and simpler but more

connected with customers. Smaller means more focused which means the Australian banking

system is required to be clear about their customers and the products and services used by

these customers (Ward and Forker, 2017). The banking system is required to be differentiated

as per the long-term customers and short-term customers. The banks are required to give full

satisfaction to its customers through its services and products to retain them. Simpler it means

easy to access and relevant. The services of the banking system should be relevant for its

customers. For example: If the Australian banks are using e-banking and customers are not

aware about this facility then this facility is not relevant for the Australian banking system.

The term ‘more connected with customers’ means the banking system is required to

understand its customers and their problems. The problems of customers must be solved

within the given period of time. Customers are important for the stability of banking system.

If banks delay in solving their problems then it will leave bad impact on customers and it

leads to loosing the customers. For the growth of banking sector, Australian banking system is

required to follow these three factors (Alwazir, et al., 2017).

Conclusion

From the above essay it is concluded that the growth of an economy totally depends upon the

regulation of financial institutions. The growth depends upon the planning of expenditure by

the government and the revenues of the country. If the expenditure is more than the revenue

then it means the country is facing financial crises but if the expenditures and revenues are

equal then that is a situation of balance of payments. This essay also contains the top ten

Australian banks by deposits and top ten Australian banks by assets.

by making policies for smooth running and by removing policies that creates hurdles in the

operations of an economy. Australian government imposes tariffs on imported goods but

because of this imposition the Australian firms that are profitable are not efficient as

compared to international firms dealing with same product. For the stability of financial

system, the banks of Australia are required to be more connected with the customers in the

future than they have been in the past years (Atoom, et al., 2017). The Australian banking

system still needs guidance in decision-making, risk management and investment. The

Australian banking system is said to be stable when the banking system will be able to make a

balance in the expenses and revenues of the country.

Recommendations

It is recommended that Australian banks must become smaller and simpler but more

connected with customers. Smaller means more focused which means the Australian banking

system is required to be clear about their customers and the products and services used by

these customers (Ward and Forker, 2017). The banking system is required to be differentiated

as per the long-term customers and short-term customers. The banks are required to give full

satisfaction to its customers through its services and products to retain them. Simpler it means

easy to access and relevant. The services of the banking system should be relevant for its

customers. For example: If the Australian banks are using e-banking and customers are not

aware about this facility then this facility is not relevant for the Australian banking system.

The term ‘more connected with customers’ means the banking system is required to

understand its customers and their problems. The problems of customers must be solved

within the given period of time. Customers are important for the stability of banking system.

If banks delay in solving their problems then it will leave bad impact on customers and it

leads to loosing the customers. For the growth of banking sector, Australian banking system is

required to follow these three factors (Alwazir, et al., 2017).

Conclusion

From the above essay it is concluded that the growth of an economy totally depends upon the

regulation of financial institutions. The growth depends upon the planning of expenditure by

the government and the revenues of the country. If the expenditure is more than the revenue

then it means the country is facing financial crises but if the expenditures and revenues are

equal then that is a situation of balance of payments. This essay also contains the top ten

Australian banks by deposits and top ten Australian banks by assets.

Financial Institutions 9

References

Adapa, S. and Roy, S.K. (2017) Consumers’ post-adoption behaviour towards Internet

banking: empirical evidence from Australia, Behaviour & Information Technology, pp.1-14.

Ahmed, A.D. and Ndayisaba, G.A. (2016) Effect of corporate governance on ceo pay-risk

taking association: empirical evidence from australian financial institutions, The Journal of

Developing Areas, 50(4), pp.309-344.

Alwazir, J., Jamaludin, F., Lee, D., Sheridan, N. and Tumbarello, P. (2017) Challenges in

Correspondent Banking in the Small States of the Pacific, Washington: International

Monetary Fund.

Atoom, R., Malkawi, E. and Al Share, B. (2017) Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks' Performance,

Journal of Applied Finance and Banking, 7(1), p.119.

Cummings, J.R. and Wright, S. (2016) Effect of higher capital requirements on the funding

costs of Australian banks, Australian Economic Review, 49(1), pp.44-53.

Export.gov (2017) Australia - Banking Systems. [Online]. Available at:

https://www.export.gov/article?id=Australia-banking-systems (Assessed: 15 September,

2017).

Goss, L. (2017) Current developments in litigation and arbitration insurance, Australian

Restructuring Insolvency & Turnaround Association Journal, 29(2), p.40.

Hudson, L.N., Newbold, T., Contu, S., Hill, S.L., Lysenko, I., De Palma, A., Phillips, H.R.,

Alhusseini, T.I., Bedford, F.E., Bennett, D.J. and Booth, H., (2017) The database of the

PREDICTS (Projecting Responses of Ecological Diversity In Changing Terrestrial Systems)

project, Ecology and evolution, 7(1), pp.145-188.

International Monetary Fund (2015) Australia: 2015 Article IV Consultation-Press Release;

Staff Report; and Statement by the Executive Director for Australia. Washington:

International Monetary Fund.

Lin, W. and Cheng, Y. (2016) The Bank Credit Transmission Channel of Monetary Policy in

Australia, International Journal of Financial Economics, 5(2), pp.61-65.

Lui, A. (2016) Financial Stability and Prudential Regulation: A Comparative Approach to the

UK, US, Canada, Australia and Germany. New York: Routledge.

MacDonald, C. and van Oordt, M.R. (2017) Using market-based indicators to Assess banking

System Resilience, Financial System, p.29.

Orsmond, D. and Price, F. (2016) Macroprudential Policy Frameworks and Tools, RBA

Bulletin, pp.75-86.

References

Adapa, S. and Roy, S.K. (2017) Consumers’ post-adoption behaviour towards Internet

banking: empirical evidence from Australia, Behaviour & Information Technology, pp.1-14.

Ahmed, A.D. and Ndayisaba, G.A. (2016) Effect of corporate governance on ceo pay-risk

taking association: empirical evidence from australian financial institutions, The Journal of

Developing Areas, 50(4), pp.309-344.

Alwazir, J., Jamaludin, F., Lee, D., Sheridan, N. and Tumbarello, P. (2017) Challenges in

Correspondent Banking in the Small States of the Pacific, Washington: International

Monetary Fund.

Atoom, R., Malkawi, E. and Al Share, B. (2017) Utilizing Australian Shareholders'

Association (ASA): Fifteen Top Financial Ratios to Evaluate Jordanian Banks' Performance,

Journal of Applied Finance and Banking, 7(1), p.119.

Cummings, J.R. and Wright, S. (2016) Effect of higher capital requirements on the funding

costs of Australian banks, Australian Economic Review, 49(1), pp.44-53.

Export.gov (2017) Australia - Banking Systems. [Online]. Available at:

https://www.export.gov/article?id=Australia-banking-systems (Assessed: 15 September,

2017).

Goss, L. (2017) Current developments in litigation and arbitration insurance, Australian

Restructuring Insolvency & Turnaround Association Journal, 29(2), p.40.

Hudson, L.N., Newbold, T., Contu, S., Hill, S.L., Lysenko, I., De Palma, A., Phillips, H.R.,

Alhusseini, T.I., Bedford, F.E., Bennett, D.J. and Booth, H., (2017) The database of the

PREDICTS (Projecting Responses of Ecological Diversity In Changing Terrestrial Systems)

project, Ecology and evolution, 7(1), pp.145-188.

International Monetary Fund (2015) Australia: 2015 Article IV Consultation-Press Release;

Staff Report; and Statement by the Executive Director for Australia. Washington:

International Monetary Fund.

Lin, W. and Cheng, Y. (2016) The Bank Credit Transmission Channel of Monetary Policy in

Australia, International Journal of Financial Economics, 5(2), pp.61-65.

Lui, A. (2016) Financial Stability and Prudential Regulation: A Comparative Approach to the

UK, US, Canada, Australia and Germany. New York: Routledge.

MacDonald, C. and van Oordt, M.R. (2017) Using market-based indicators to Assess banking

System Resilience, Financial System, p.29.

Orsmond, D. and Price, F. (2016) Macroprudential Policy Frameworks and Tools, RBA

Bulletin, pp.75-86.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Institutions 10

Salter, A.W., Veetil, V. and White, L.H. (2017) Extended shareholder liability as a means to

constrain moral hazard in insured banks, The Quarterly Review of Economics and Finance,

63, pp.153-160.

Sheedy, E.A., Griffin, B. and Barbour, J.P. (2017) A framework and measure for examining

risk climate in financial institutions, Journal of Business and Psychology, 32(1), pp.101-116.

The Conversation (2016) Banking outlook: threats from technology, burst of housing bubble,

end of mining boom. [Online]. Available at: http://theconversation.com/banking-outlook-

threats-from-technology-burst-of-housing-bubble-end-of-mining-boom-55627 (Assessed: 15

September, 2017).

Truong, T.P. and Nguyen, N.N. (2017) Regulatory Enforcement, Financial Reporting Quality

and Investment Efficiency: A Pitch, Accounting Research Journal, 30(1).

van Esterik-Plasmeijer, P.W., van Esterik-Plasmeijer, P.W., van Raaij, W.F. and van Raaij,

W.F. (2017) Banking system trust, bank trust, and bank loyalty, International Journal of Bank

Marketing, 35(1), pp.97-111.

Ward, A.M. and Forker, J. (2017) Financial management effectiveness and board gender

diversity in member-governed, community financial institutions, Journal of Business Ethics,

141(2), pp.351-366.

Carnegie, G.D. and Carnegie, G.D., (2016) The accounting professional project and bank

failures: The case of the early 1890s Australian banking crisis, Journal of Management

History, 22(4), pp.389-412.

Salter, A.W., Veetil, V. and White, L.H. (2017) Extended shareholder liability as a means to

constrain moral hazard in insured banks, The Quarterly Review of Economics and Finance,

63, pp.153-160.

Sheedy, E.A., Griffin, B. and Barbour, J.P. (2017) A framework and measure for examining

risk climate in financial institutions, Journal of Business and Psychology, 32(1), pp.101-116.

The Conversation (2016) Banking outlook: threats from technology, burst of housing bubble,

end of mining boom. [Online]. Available at: http://theconversation.com/banking-outlook-

threats-from-technology-burst-of-housing-bubble-end-of-mining-boom-55627 (Assessed: 15

September, 2017).

Truong, T.P. and Nguyen, N.N. (2017) Regulatory Enforcement, Financial Reporting Quality

and Investment Efficiency: A Pitch, Accounting Research Journal, 30(1).

van Esterik-Plasmeijer, P.W., van Esterik-Plasmeijer, P.W., van Raaij, W.F. and van Raaij,

W.F. (2017) Banking system trust, bank trust, and bank loyalty, International Journal of Bank

Marketing, 35(1), pp.97-111.

Ward, A.M. and Forker, J. (2017) Financial management effectiveness and board gender

diversity in member-governed, community financial institutions, Journal of Business Ethics,

141(2), pp.351-366.

Carnegie, G.D. and Carnegie, G.D., (2016) The accounting professional project and bank

failures: The case of the early 1890s Australian banking crisis, Journal of Management

History, 22(4), pp.389-412.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.