Finance for Managers: Morrison and Sainsbury Performance Analysis

VerifiedAdded on 2020/02/05

|27

|7719

|47

Report

AI Summary

This report provides a comprehensive financial and non-financial performance evaluation of two British retailers, Morrison and Sainsbury. It begins with an introduction to finance and its impact on business success, emphasizing the importance of financial analysis for investors. The report outlines key parameters for financial and non-financial analysis, including strategic financial analysis, profitability ratios, return on capital employed, and non-financial factors like SWOT analysis and CSR initiatives. It then delves into the specific financial performance of Morrison, analyzing turnover, cost of sales, and profitability narratives. A comparative analysis with Sainsbury is implied, although not fully developed in the provided text. The report aims to advise investors by assessing the companies' financial health, business models, and strategic approaches, ultimately offering insights into their investment potential. It incorporates ratio analysis, strategic analysis, CSR initiatives, SWOT analysis, and business models to provide a holistic view.

Finance for managers

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

1. Parameters for the financial as well as non-financial analysis....................................................3

2. Different financial and non-financial areas need to be consider by investor:..............................5

3. Evaluation of financial and non-financial performance of Morrison with its competitor

Sainsbury.........................................................................................................................................6

4. Reflection...................................................................................................................................12

RECOMMENDATION......................................................................................................................12

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................14

APPENDIX........................................................................................................................................16

2

INTRODUCTION................................................................................................................................3

1. Parameters for the financial as well as non-financial analysis....................................................3

2. Different financial and non-financial areas need to be consider by investor:..............................5

3. Evaluation of financial and non-financial performance of Morrison with its competitor

Sainsbury.........................................................................................................................................6

4. Reflection...................................................................................................................................12

RECOMMENDATION......................................................................................................................12

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................14

APPENDIX........................................................................................................................................16

2

INTRODUCTION

Finance is the most crucial element which has high level of impact on the growth and

success of the firm. It is mainly because, in order to carry out regular business operations and

functions, companies are require to gather appropriate amount of fund for meeting out its daily

expenditures and CAPEX such as investment in plant and property, meet out debt obligations,

administration and selling payments and so on. Looking at the present corporate world, companies

gather large amount of money from the investors either domestic or international. Before making

investment in any firm, investors ones assess their risk and return relationship associated with their

potential investment and invest money in that organization where risk is minimum and possibility of

return is maximum. In order to make such analysis, investors need to evaluate business operational

outcome and financial strength by calculating number of ratios like profitability, long-term solvency

and liquidity and so on. This assignment lay emphasizes on financial as well as non-financial

performance evaluation of two British retailers, Morrison and its competitor Sainsbury. It will be

done by ratio analysis strategic analysis, CSR initiatives, SWOT analysis, business model and

others so as to advice investors to make solid decisions.

Brief overview of business

UK retail sector shows a rapid growth as numbers of retailers are delivering excellent

services to the customers. WM Morrison Supermarket is a public limited company listed on LSE,

founded in 1899 and operates in retail sector. It provides retailing services to the people through via

both the established retail stores and online medium. The main aim of the company is to deliver top-

quality food and grocery products to the customers so as to gain competitive advantage.

Another retail organization that has been chosen for comparative analysis is Sainsbury

founded in the year 1869, listed on LSE. It delivers retailing services to the people through its

convenience stores, forecourt stores, hypermarket, supermarkets and superstores. Company also

deliver services to the target audiences using online channel i.e. website development and web

marketing etc.

1. Parameters for the financial as well as non-financial analysis

In the current era of tough competition, all the commercial establishments require to

examine and interpret their actual performance including both financial as well as non-financial

results. There are many parameters available to business analysts to compare and evaluate their

actual outcome either quantitative or qualitative for a given duration. The most often use parameters

for monetary as well as non-monetary analyses are enumerated hereunder:

Strategic Financial Analysis: SFA regarded as the process of examining and evaluating

3

Finance is the most crucial element which has high level of impact on the growth and

success of the firm. It is mainly because, in order to carry out regular business operations and

functions, companies are require to gather appropriate amount of fund for meeting out its daily

expenditures and CAPEX such as investment in plant and property, meet out debt obligations,

administration and selling payments and so on. Looking at the present corporate world, companies

gather large amount of money from the investors either domestic or international. Before making

investment in any firm, investors ones assess their risk and return relationship associated with their

potential investment and invest money in that organization where risk is minimum and possibility of

return is maximum. In order to make such analysis, investors need to evaluate business operational

outcome and financial strength by calculating number of ratios like profitability, long-term solvency

and liquidity and so on. This assignment lay emphasizes on financial as well as non-financial

performance evaluation of two British retailers, Morrison and its competitor Sainsbury. It will be

done by ratio analysis strategic analysis, CSR initiatives, SWOT analysis, business model and

others so as to advice investors to make solid decisions.

Brief overview of business

UK retail sector shows a rapid growth as numbers of retailers are delivering excellent

services to the customers. WM Morrison Supermarket is a public limited company listed on LSE,

founded in 1899 and operates in retail sector. It provides retailing services to the people through via

both the established retail stores and online medium. The main aim of the company is to deliver top-

quality food and grocery products to the customers so as to gain competitive advantage.

Another retail organization that has been chosen for comparative analysis is Sainsbury

founded in the year 1869, listed on LSE. It delivers retailing services to the people through its

convenience stores, forecourt stores, hypermarket, supermarkets and superstores. Company also

deliver services to the target audiences using online channel i.e. website development and web

marketing etc.

1. Parameters for the financial as well as non-financial analysis

In the current era of tough competition, all the commercial establishments require to

examine and interpret their actual performance including both financial as well as non-financial

results. There are many parameters available to business analysts to compare and evaluate their

actual outcome either quantitative or qualitative for a given duration. The most often use parameters

for monetary as well as non-monetary analyses are enumerated hereunder:

Strategic Financial Analysis: SFA regarded as the process of examining and evaluating

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial performance of an organization so as to diagnose business problems, operational

difficulties and reason for poor performance. There are various techniques available to the Morrison

for performance analysis such as common-size/vertical analysis, trend analysis and ratio analysis

(Shiller, 2013). Out of these, ratio analysis is considered as the best methodology that assesses

relationship between each and every variable of the reported annual accounts.

Profitability analysis: WM Morisson’s profitability can be examined by utilizing ratios like

gross profit and net profit (Brealey & et.al., 2012). In this, gross profits indicate the percentage that

company earned through adding a mark-up on their total turnover. However, net margin helps to

identify surplus percentage that company earned by generating excess revenue over total business

expenses.

Return on capital employed: This parameter can be used to determine percentage that firm

earned on their total capital invested. In other words, it measure that how efficiently Morrison is

generating yield on their total capital employed (total assets-current liabilities) in the business.

Earning per share: Companies like Morrison and others generate huge proportion of long-

term fund by shareholders. They invest money in the business so as to get optimum and maximum

return to meet their yield expectations (Masubuchi, 2013). EPS is an effective and often used

parameter to assess investment performance to interpret that in what extent, organization is able to

deliver favourable financial reward to their investors in return for undertaken risk.

Current ratio: This ratio helps to measure the proportion between current assets and

liabilities typically used to evaluate business ability to repay suppliers on right time. It is essential

for the managers to examine their liquidity position or creditworthiness to meet their short-term

obligations within extended credit period (Uechi & et.al., 2015).

Dividend payout ratio: In the real market, retailers kept some amount of their net earnings in

the business for the future growth, success and financial risk management (Wilson, 2016). DPS is

often used by the analysts to determine the proportion of net income that is distributed among

stockholders as dividend.

Gearing ratio: Investors often use this ratio as a parameter to determine the proportion or

mix of debt and equity fund so as to examine potential risk associated with their investment (Shiller,

2013).

Non-financial analysis/quantifiable performance

SWOT: It is a model used for identifying internal business strength and weaknesses as well

as market opportunity and threats due to volatile external market forces.

Strategic planning: Business strategies and planning can also be evaluate to measure that

how efficiently executives and managers plans proves successful for the corporate growth and

4

difficulties and reason for poor performance. There are various techniques available to the Morrison

for performance analysis such as common-size/vertical analysis, trend analysis and ratio analysis

(Shiller, 2013). Out of these, ratio analysis is considered as the best methodology that assesses

relationship between each and every variable of the reported annual accounts.

Profitability analysis: WM Morisson’s profitability can be examined by utilizing ratios like

gross profit and net profit (Brealey & et.al., 2012). In this, gross profits indicate the percentage that

company earned through adding a mark-up on their total turnover. However, net margin helps to

identify surplus percentage that company earned by generating excess revenue over total business

expenses.

Return on capital employed: This parameter can be used to determine percentage that firm

earned on their total capital invested. In other words, it measure that how efficiently Morrison is

generating yield on their total capital employed (total assets-current liabilities) in the business.

Earning per share: Companies like Morrison and others generate huge proportion of long-

term fund by shareholders. They invest money in the business so as to get optimum and maximum

return to meet their yield expectations (Masubuchi, 2013). EPS is an effective and often used

parameter to assess investment performance to interpret that in what extent, organization is able to

deliver favourable financial reward to their investors in return for undertaken risk.

Current ratio: This ratio helps to measure the proportion between current assets and

liabilities typically used to evaluate business ability to repay suppliers on right time. It is essential

for the managers to examine their liquidity position or creditworthiness to meet their short-term

obligations within extended credit period (Uechi & et.al., 2015).

Dividend payout ratio: In the real market, retailers kept some amount of their net earnings in

the business for the future growth, success and financial risk management (Wilson, 2016). DPS is

often used by the analysts to determine the proportion of net income that is distributed among

stockholders as dividend.

Gearing ratio: Investors often use this ratio as a parameter to determine the proportion or

mix of debt and equity fund so as to examine potential risk associated with their investment (Shiller,

2013).

Non-financial analysis/quantifiable performance

SWOT: It is a model used for identifying internal business strength and weaknesses as well

as market opportunity and threats due to volatile external market forces.

Strategic planning: Business strategies and planning can also be evaluate to measure that

how efficiently executives and managers plans proves successful for the corporate growth and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

success (Uechi & et.al., 2015).

Brand reputation: Market reputation and position also works as an indicator of business

strength. Customer loyalty, use of upgraded and advanced technology, globalized operations, strong

brand portfolio, expansion and growth projects helps to build a strong brand reputation.

CSR activities: In the present times, establishments like Morrison and other retailers have to

take several initiatives so as to meet their responsibilities towards all their stakeholders like

consumer, society, suppliers, employees and so on (Masubuchi, 2013).

2. Different financial and non-financial areas need to be consider by investor:

Every potential investor who is planning to invest fund in an organization desires to get

maximum return. Therefore, they require examining both the quantitative as well as qualitative

aspects so as to make solid investment decisions. According to Uechi and et.al., (2015), presented

ratio analysis as the best methodology for conducting quantitative and financial analysis. With the

help of this, investor can examine and evaluate business performance by computing variety of ratios

like profitability, solvency, liquidity and managerial efficiency. Gross margin, net margin, return on

shareholders fund, ROCE, debt to equity ratio, leverage and current ratio can be used for examining

the outcome of regular functions and financial health as well. Likewise, Shiller (2013), presented

that investors put their money in an organization to get maximum reward henceforth, they need to

examine current investors return. It can be done by computing investment ratios like earnings per

share and dividend payout ratio. EPS indicates return on each holding whereas dividend payout

ratio indicates that what proportion of net corporate yield is distributed among stockholders as

dividend.

However, it has been criticised by Wilson (2016), as the study outlined that ratio analysis

method has number of shortcomings. One of the most important limitations is that it gives

information about quantitative values and figures of historical years, however, investors are highly

motivated by the future performance. Moreover, the success of the decision based upon strategic

financial analysis of company’s annual accounts is highly dependent upon reliability, truthfulness

and validity of the information reported in financial statements. Incorrect and misleading

information can lead to take wrong decisions. Further, although comparative analysis is consider

useful for better decisions, but still, in the real corporate sector, companies use distinguish

accounting policies and rules which differentiate financial reporting structure and can lead to take

harmful decisions. In addition to this, changes in business performance may be the result of volatile

market conditions that are not considered by financial statement. Therefore, investors have to use a

combination of both the quantitative as well as qualitative methods for more accurate analysis.

5

Brand reputation: Market reputation and position also works as an indicator of business

strength. Customer loyalty, use of upgraded and advanced technology, globalized operations, strong

brand portfolio, expansion and growth projects helps to build a strong brand reputation.

CSR activities: In the present times, establishments like Morrison and other retailers have to

take several initiatives so as to meet their responsibilities towards all their stakeholders like

consumer, society, suppliers, employees and so on (Masubuchi, 2013).

2. Different financial and non-financial areas need to be consider by investor:

Every potential investor who is planning to invest fund in an organization desires to get

maximum return. Therefore, they require examining both the quantitative as well as qualitative

aspects so as to make solid investment decisions. According to Uechi and et.al., (2015), presented

ratio analysis as the best methodology for conducting quantitative and financial analysis. With the

help of this, investor can examine and evaluate business performance by computing variety of ratios

like profitability, solvency, liquidity and managerial efficiency. Gross margin, net margin, return on

shareholders fund, ROCE, debt to equity ratio, leverage and current ratio can be used for examining

the outcome of regular functions and financial health as well. Likewise, Shiller (2013), presented

that investors put their money in an organization to get maximum reward henceforth, they need to

examine current investors return. It can be done by computing investment ratios like earnings per

share and dividend payout ratio. EPS indicates return on each holding whereas dividend payout

ratio indicates that what proportion of net corporate yield is distributed among stockholders as

dividend.

However, it has been criticised by Wilson (2016), as the study outlined that ratio analysis

method has number of shortcomings. One of the most important limitations is that it gives

information about quantitative values and figures of historical years, however, investors are highly

motivated by the future performance. Moreover, the success of the decision based upon strategic

financial analysis of company’s annual accounts is highly dependent upon reliability, truthfulness

and validity of the information reported in financial statements. Incorrect and misleading

information can lead to take wrong decisions. Further, although comparative analysis is consider

useful for better decisions, but still, in the real corporate sector, companies use distinguish

accounting policies and rules which differentiate financial reporting structure and can lead to take

harmful decisions. In addition to this, changes in business performance may be the result of volatile

market conditions that are not considered by financial statement. Therefore, investors have to use a

combination of both the quantitative as well as qualitative methods for more accurate analysis.

5

According to Chia-Hsing, Padmanabhan and Zhang (2013), initially, investor has to evaluate

several company/firm-specific factors, more importantly, business model. Before investigating

annual accounts, investors have to look at company’s business model at its website or financial

reports. It delivers information to the investors that how company work out its operations and

regular business activities. On the other hand, Masubuchi (2013), commented that it seems to be

difficult for the enterprises to understand business model clearly and precisely, therefore,

competitive advantage is considered as more essential element that an investor need to consider

before putting their money. It is an indicator of long-term business success, growth and

sustainability. In such respects, investor has to evaluate unique business preposition, strategic

planning and activities, technologies, operational effectiveness, strategic capabilities, market

presence and so on.

Despite this, in the study of Gelman, Carlin & Rubin (2014), it has been observed that

managers play a crucial role in the enterprise success, as they make policies, decisions and prepare

plans for the smooth functioning. Therefore, managerial efficiency is a key or vital element that an

investor needs to evaluate so as to invest money in that organization which managers are highly

skilled, talented and experienced and capable to reach business towards greatest heights.

However, on the critical note, Berk and et. al., (2013), said that every organization is a part

of society and have some responsibility towards all the stakeholders. Establishing excellent

managerial structure to meet interest and expectations of all the stakeholders is a sign of good

corporate governance. In other words, it refers to a set of transparent rules, policies, activities and

operational system which is developed to maintain reliability, integrity and meet out obligations

towards all the stakeholders. In contrast to this, Brealey & et.al. (2012), argued that

SWOT/PESTEL models can be used to conduct both the internal as well as external analysis. This

method gives assistance to the investor to examine the effectiveness of internal operations and the

impact of external market forces on regular business activities and functions. It enables investors to

make better and stronger decisions so as to make sure sufficient financial return for the money

invested.

3. Evaluation of financial and non-financial performance of Morrison with its competitor Sainsbury

Financial performance analysis of Morrison

Profitability narratives:

Gross margin: Morrison’s GM got declined from 6.89% to 3.83% in the year 2016 indicates

that company is generating less return on their total turnover due to following reasons:

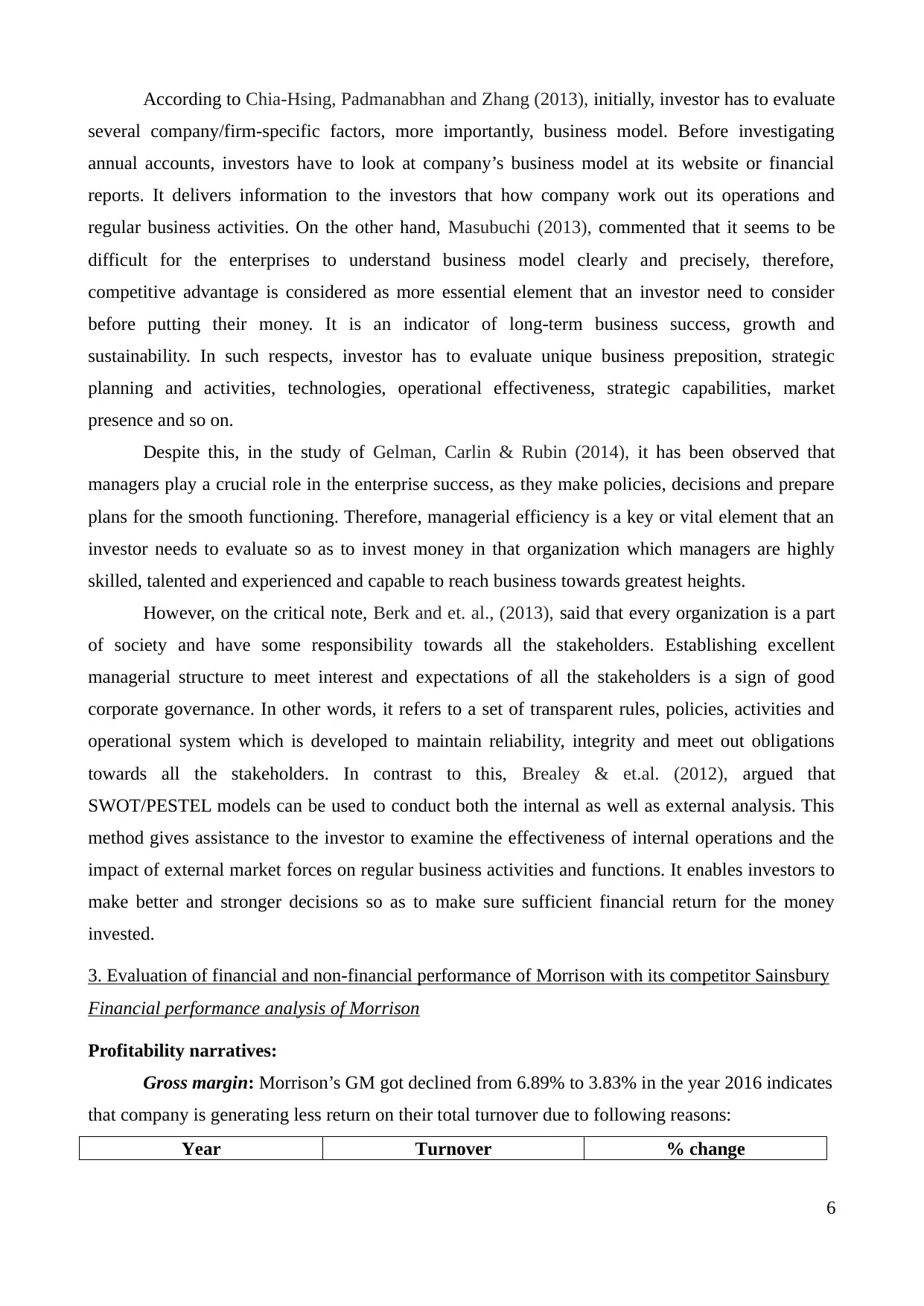

Year Turnover % change

6

several company/firm-specific factors, more importantly, business model. Before investigating

annual accounts, investors have to look at company’s business model at its website or financial

reports. It delivers information to the investors that how company work out its operations and

regular business activities. On the other hand, Masubuchi (2013), commented that it seems to be

difficult for the enterprises to understand business model clearly and precisely, therefore,

competitive advantage is considered as more essential element that an investor need to consider

before putting their money. It is an indicator of long-term business success, growth and

sustainability. In such respects, investor has to evaluate unique business preposition, strategic

planning and activities, technologies, operational effectiveness, strategic capabilities, market

presence and so on.

Despite this, in the study of Gelman, Carlin & Rubin (2014), it has been observed that

managers play a crucial role in the enterprise success, as they make policies, decisions and prepare

plans for the smooth functioning. Therefore, managerial efficiency is a key or vital element that an

investor needs to evaluate so as to invest money in that organization which managers are highly

skilled, talented and experienced and capable to reach business towards greatest heights.

However, on the critical note, Berk and et. al., (2013), said that every organization is a part

of society and have some responsibility towards all the stakeholders. Establishing excellent

managerial structure to meet interest and expectations of all the stakeholders is a sign of good

corporate governance. In other words, it refers to a set of transparent rules, policies, activities and

operational system which is developed to maintain reliability, integrity and meet out obligations

towards all the stakeholders. In contrast to this, Brealey & et.al. (2012), argued that

SWOT/PESTEL models can be used to conduct both the internal as well as external analysis. This

method gives assistance to the investor to examine the effectiveness of internal operations and the

impact of external market forces on regular business activities and functions. It enables investors to

make better and stronger decisions so as to make sure sufficient financial return for the money

invested.

3. Evaluation of financial and non-financial performance of Morrison with its competitor Sainsbury

Financial performance analysis of Morrison

Profitability narratives:

Gross margin: Morrison’s GM got declined from 6.89% to 3.83% in the year 2016 indicates

that company is generating less return on their total turnover due to following reasons:

Year Turnover % change

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2012 17663

2013 18116 2.56%

2014 17680 -2.41%

2015 16816 -4.89%

2016 16122 -4.13%

1.J Sainsbury PLC 2.WM Morrison Supermarkets P L C

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

th GBP

Std dev. Av. 1 2

11 12 13

11 12 13

11

12 13

11 12 13

Turnover: In 2013, firm’s turnover got improved from £17,663m to £18,116m by 2.56% due

to increased demand. However, thereafter sales shows a continuous decrease by 2.41% and 4.89%

and 4.13% respectively may be due to decrease in consumer demand, worst quality products and

availability of substitute products at cheaper prices. Cutting product prices, improvement in quality

of service, online operations and rapid growth in offered discounts were the main reasons for the

grown turnover. Growing brand portfolio, premium quality service, price cut strategies proven as a

key pillars for high like for like sales and other revenues. In this year, company cut down its prices

on around 100 products, more importantly, fresh fruit and vegetables bring significant growth in

sales revenues (Morrison’s returns to profit as sales rise, 2016). In addition to this, opening new

convenience stores and grocery shops at different locations also assist entrepreneur to maximize

their total turnover and reach success. Besides this, increase in real wages increased availability of

disposable income, which in turn, rose customer demand and results in increased turnover.

Expansion of services at stores has explored total revenue of the firm.

7

2013 18116 2.56%

2014 17680 -2.41%

2015 16816 -4.89%

2016 16122 -4.13%

1.J Sainsbury PLC 2.WM Morrison Supermarkets P L C

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

th GBP

Std dev. Av. 1 2

11 12 13

11 12 13

11

12 13

11 12 13

Turnover: In 2013, firm’s turnover got improved from £17,663m to £18,116m by 2.56% due

to increased demand. However, thereafter sales shows a continuous decrease by 2.41% and 4.89%

and 4.13% respectively may be due to decrease in consumer demand, worst quality products and

availability of substitute products at cheaper prices. Cutting product prices, improvement in quality

of service, online operations and rapid growth in offered discounts were the main reasons for the

grown turnover. Growing brand portfolio, premium quality service, price cut strategies proven as a

key pillars for high like for like sales and other revenues. In this year, company cut down its prices

on around 100 products, more importantly, fresh fruit and vegetables bring significant growth in

sales revenues (Morrison’s returns to profit as sales rise, 2016). In addition to this, opening new

convenience stores and grocery shops at different locations also assist entrepreneur to maximize

their total turnover and reach success. Besides this, increase in real wages increased availability of

disposable income, which in turn, rose customer demand and results in increased turnover.

Expansion of services at stores has explored total revenue of the firm.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

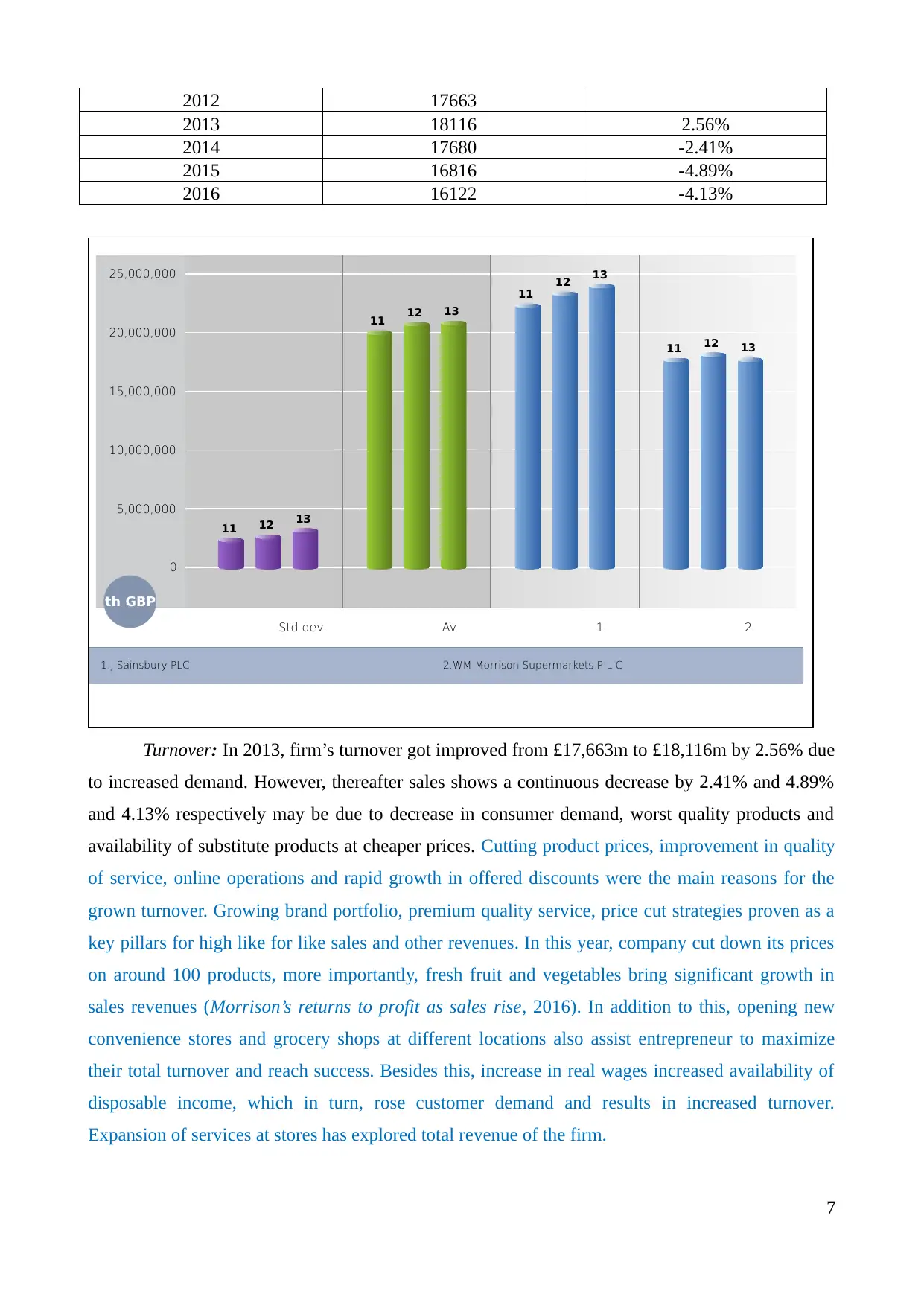

Year Cost of sale % change

2012 16446

2013 16910 2.82%

2014 16606 -1.80%

2015 16055 -3.32%

2016 15505 -3.43%

Cost of sales: Another reason for decrease in profitability is ineffective control over cost of

sale. The table reflects that in 2013, cost got improved by 2.82%, however, thereafter; it dropped

down by 1.80%, 3.32% and 3.43%. Although % decrease in cost is rising but still it is

comparatively less than % change in sales resulted in decreased gross margin (WM Morrison

Supermarket Plc, 2016).

J Sainsbury PLC

(62.77%)

WM Morrison Supermarkets P L

C

(37.23%)

Net margin: Till 2015, NM got declined from 5.36% to -4.71%, but in 2016, it got increased

to 1.35% which indicates that this year, Morrison generated favourable return on their total

revenues. Following are the reasons for volatility in net profit, enumerated underneath:

Sales, general and administration expense: In 2016, SG&A shows a sudden decline from

£1,670m to £472m by 71.74%, which in turn, resulted in high net margin. However, in this year,

company recruited 5000 new employees to serve their customers in the best manner during heavy

workload and busiest time.

Interest expense: Continuous increasing in interest expenses from £39m to £65m, £81m,

£95m and 98m increased total spending and declined net return (Marciukaityte & Szewczyk,

2011).

Other operational expense/income: In 2012, Morrison incurred expenses worth £340m

8

2012 16446

2013 16910 2.82%

2014 16606 -1.80%

2015 16055 -3.32%

2016 15505 -3.43%

Cost of sales: Another reason for decrease in profitability is ineffective control over cost of

sale. The table reflects that in 2013, cost got improved by 2.82%, however, thereafter; it dropped

down by 1.80%, 3.32% and 3.43%. Although % decrease in cost is rising but still it is

comparatively less than % change in sales resulted in decreased gross margin (WM Morrison

Supermarket Plc, 2016).

J Sainsbury PLC

(62.77%)

WM Morrison Supermarkets P L

C

(37.23%)

Net margin: Till 2015, NM got declined from 5.36% to -4.71%, but in 2016, it got increased

to 1.35% which indicates that this year, Morrison generated favourable return on their total

revenues. Following are the reasons for volatility in net profit, enumerated underneath:

Sales, general and administration expense: In 2016, SG&A shows a sudden decline from

£1,670m to £472m by 71.74%, which in turn, resulted in high net margin. However, in this year,

company recruited 5000 new employees to serve their customers in the best manner during heavy

workload and busiest time.

Interest expense: Continuous increasing in interest expenses from £39m to £65m, £81m,

£95m and 98m increased total spending and declined net return (Marciukaityte & Szewczyk,

2011).

Other operational expense/income: In 2012, Morrison incurred expenses worth £340m

8

however, which was wholly removed in 2014 and 2015. While, in 2016, firm generated revenue

worth £97m from their regular course of activities and functions helps to maximize their net

earnings.

Although, restructuring cost and cutting price strategy controlled total cost but still,

ineffective cost control upon indirect expenditures like selling and administration expenditures is

the reason for declined performance. Moreover, heavy expenditures on marketing and promotional

campaign to attract more and more customers, price-cut and larger discount declined Morrison’s

profitability margin (Cleme & Reilly, 2013). In addition to this, Morrison is highly committed

towards minimization of wastage and cost reduction by restructuring head office and

underperforming superstores so as to ensure a cost effective performance.

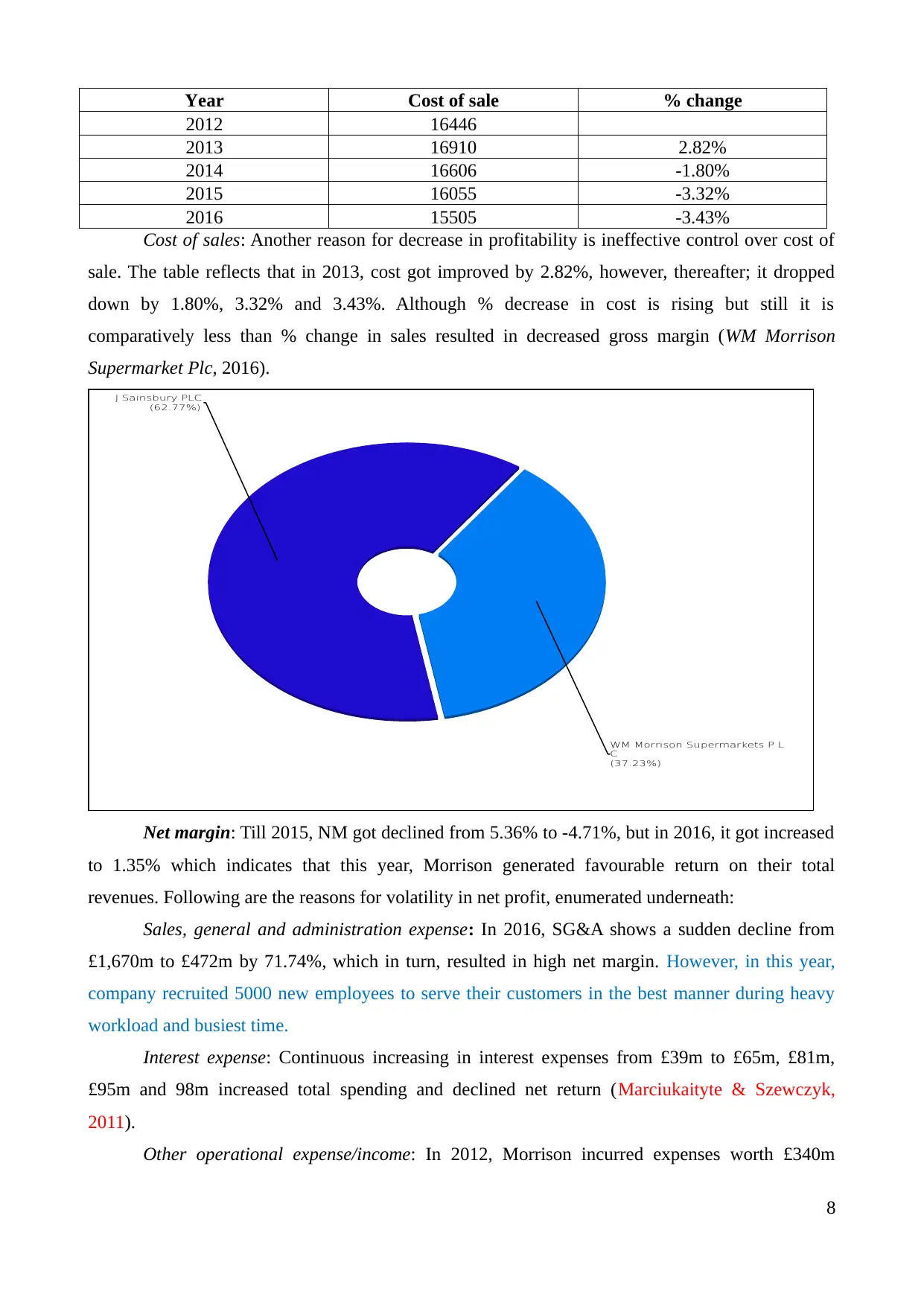

1.WM Morrison Supermarkets P L C 2.J Sainsbury PLC

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

%

Std dev. Av. 1 2

11 12

13 14

15

11

12

13

14

15

11

12

13 14

15

11 12 13

14

15

Return on capital employed: Morrison’s ROCE came down from 12.53% to -11.49% in

2015 demonstrates that firm generated loss on their total capital invested in the business (Kural &

et.al., 2016). However, in 2016, it got increased to 3.41% entails that firm generated positive return

on their capital employed due to transforming negative return into positive to £222m. It is a good

sign of business performance shows due to favourable return on total capital. Driven growth in sales

volume, control over cost and dealing effectively with underperforming assets were the reasons

towards grown ROCE (Marciukaityte & Szewczyk, 2011).

9

worth £97m from their regular course of activities and functions helps to maximize their net

earnings.

Although, restructuring cost and cutting price strategy controlled total cost but still,

ineffective cost control upon indirect expenditures like selling and administration expenditures is

the reason for declined performance. Moreover, heavy expenditures on marketing and promotional

campaign to attract more and more customers, price-cut and larger discount declined Morrison’s

profitability margin (Cleme & Reilly, 2013). In addition to this, Morrison is highly committed

towards minimization of wastage and cost reduction by restructuring head office and

underperforming superstores so as to ensure a cost effective performance.

1.WM Morrison Supermarkets P L C 2.J Sainsbury PLC

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

%

Std dev. Av. 1 2

11 12

13 14

15

11

12

13

14

15

11

12

13 14

15

11 12 13

14

15

Return on capital employed: Morrison’s ROCE came down from 12.53% to -11.49% in

2015 demonstrates that firm generated loss on their total capital invested in the business (Kural &

et.al., 2016). However, in 2016, it got increased to 3.41% entails that firm generated positive return

on their capital employed due to transforming negative return into positive to £222m. It is a good

sign of business performance shows due to favourable return on total capital. Driven growth in sales

volume, control over cost and dealing effectively with underperforming assets were the reasons

towards grown ROCE (Marciukaityte & Szewczyk, 2011).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EPS (earning per share): In 2012, EPS was 26.68p got improved to 27.26p in 2013,

Thereafter, it shows a continuous decrease to 23.08p, 10.93p and 7.77p. Changes in net earnings

available for the ordinary shareholders and stockholder’s equity are the reasons for volatility in

return on each holding. Regular decrease in EPS is a poor sign of business performance as investors

are getting less return on their equity capital and may give rise to dissatisfaction.

Price-earning ratio: In 2012, Morrison’s PE ratio was 10.23 shows an extreme level of

improvement in the year 2015 to 16.46. Increase in EPS is the main reasons for rising PE ratio

which is a good sign of business performance (Bull, 2007). Growth in PE ratio indicates that

investors are expecting more return from the company in return for the risk taken by putting their

own money.

Current ratio: In 2015, it remained constant to 0.57:1, while, after this, it shows a constant

decline to 0.57:1, 0.54:1 and 0.48:1. From the financial statement, it can be seen that till 2014, its

CA got improved to £1342m and £1430m but in 2014, it came down to £1228m. However, in 2016,

it rose to £1308m due to increased bank deposits from £241m to £488m. Contrary to this, from

2012 to 2016, Morrison’s current liabilities enhanced from £2303m to £2747m because of rise in

creditors, short-term loans and other nearby obligation (Rakićević & et.al., 2016). The ratio is also

far away from the idle ratio of 2:1 reflects that Morrison is unable to make their deferral payments

(short-term obligations) on right time because of having inadequate resources.

Dividend payout ratio: Morrison’s ratio rose up to 52.61% indicates that company delivered

more dividends to the investors out of profit generated to carry out regular business operations (WM

Morrison Supermarket Plc, 2016).

Gearing ratio: Till the end of 2015, Morrison’s gearing ratio got increased from 42.02 to

57.65, 79.22 and 92.13 indicates excessive risk because of rising mix of debt resources and

repayment of share capital to the investors. High ratio is a sign of improved risk because Morrison’s

debt obligation in relation to interest payment has been increased (Sharma & Mehra, 2016). But in

2016, it dropped down to 74.84 due to repayment of long-term debt worth £500m and more use of

shareholders equity as it got increased from £3594m to £3756m. It shows that management take

action to minimize financial risk and improve solvency position so as to meet long-term obligations

on right time as per repayment schedule (Weaver & Weston, 2007).

Financial performance analysis of Sainsbury

Gross margin: Sainsbury’s GM got enhanced from 5.43% to 6.19% which exhibits that

company generated greater return on their total sales due to following reasons:

Year Turnover % change Cost of sale % change

2012 22294 - 21091 -

10

Thereafter, it shows a continuous decrease to 23.08p, 10.93p and 7.77p. Changes in net earnings

available for the ordinary shareholders and stockholder’s equity are the reasons for volatility in

return on each holding. Regular decrease in EPS is a poor sign of business performance as investors

are getting less return on their equity capital and may give rise to dissatisfaction.

Price-earning ratio: In 2012, Morrison’s PE ratio was 10.23 shows an extreme level of

improvement in the year 2015 to 16.46. Increase in EPS is the main reasons for rising PE ratio

which is a good sign of business performance (Bull, 2007). Growth in PE ratio indicates that

investors are expecting more return from the company in return for the risk taken by putting their

own money.

Current ratio: In 2015, it remained constant to 0.57:1, while, after this, it shows a constant

decline to 0.57:1, 0.54:1 and 0.48:1. From the financial statement, it can be seen that till 2014, its

CA got improved to £1342m and £1430m but in 2014, it came down to £1228m. However, in 2016,

it rose to £1308m due to increased bank deposits from £241m to £488m. Contrary to this, from

2012 to 2016, Morrison’s current liabilities enhanced from £2303m to £2747m because of rise in

creditors, short-term loans and other nearby obligation (Rakićević & et.al., 2016). The ratio is also

far away from the idle ratio of 2:1 reflects that Morrison is unable to make their deferral payments

(short-term obligations) on right time because of having inadequate resources.

Dividend payout ratio: Morrison’s ratio rose up to 52.61% indicates that company delivered

more dividends to the investors out of profit generated to carry out regular business operations (WM

Morrison Supermarket Plc, 2016).

Gearing ratio: Till the end of 2015, Morrison’s gearing ratio got increased from 42.02 to

57.65, 79.22 and 92.13 indicates excessive risk because of rising mix of debt resources and

repayment of share capital to the investors. High ratio is a sign of improved risk because Morrison’s

debt obligation in relation to interest payment has been increased (Sharma & Mehra, 2016). But in

2016, it dropped down to 74.84 due to repayment of long-term debt worth £500m and more use of

shareholders equity as it got increased from £3594m to £3756m. It shows that management take

action to minimize financial risk and improve solvency position so as to meet long-term obligations

on right time as per repayment schedule (Weaver & Weston, 2007).

Financial performance analysis of Sainsbury

Gross margin: Sainsbury’s GM got enhanced from 5.43% to 6.19% which exhibits that

company generated greater return on their total sales due to following reasons:

Year Turnover % change Cost of sale % change

2012 22294 - 21091 -

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 23303 4.53% 22026 4.43%

2014 23949 2.77% 22562 2.43%

2015 23775 -0.73% 22567 0.02%

2016 23506 -1.13% 22050 -2.29%

Rise in turnover is the reasons for high gross margin till 2014, however, thereafter, although

sales moved downward, but still, effective cost control mechanism to curtail direct expenditures

helps to maximize gross margin and improved its performance.

Net margin: From 2012 to 2015, net margin dropped down from 3.58% to 0.30%, thereafter,

got increased to 2.33% more than Morrison’s NM demonstrates that Sainsbury is performing well.

Control over SG&A expenses by 24.91%, reduction in interest expense by 2.44% and high

operational income are the reason for better return in 2016. It shows that Sainsbury’s performance

has been improved as its net earnings have been converted from negative £166m to £471m

(Saisnbury’s annual report, 2016).

ROCE: In 2015, Sainsbury borne loss on their total capital as its ROCE is -1.30% whereas

in 2016, it shows a sudden increase to 8.61%. Positive return worth £471m is the reason behind

improved ROCE is a sign of greater performance on total capital invested in the firm to carry out

regular business activities and operations (Marciukaityte & Szewczyk, 2011). .

Earning per share: Sainsbury’s EPS came down from 0.32 to -0.08 in 2015, whereas, in

next year, it got increased to 0.23 depicts that company delivered more return to their investors by

generating more yield on their total revenues (Agarwal & et.al., 2015).

Dividend payout ratio: In 2016, Sainsbury’s dividend payout ratio rose to 60.3%

comparatively higher than Morrison’s ratio indicates that it is distributing more dividends to the

shareholders out of total generated net earnings (Sainsbury, 2016).

Current ratio: In 2013, it came down from 0.65:1 to 0.61:1 is a sign of poor liquidity

position. While, thereafter, it shows a constant increase as in 2016, it got inclined to 0.66:1 and also

higher than Morrison’s CR. Increase in short-term investment by 43.48%, prepaid expenses by

8.08% and other CA by 7.91% is the reason behind high availability of nearby resources (Cleme &

Reilly, 2013). However, CL came down by 2.87% due to repayment of some short-term debt,

decreased trade payables and other short-term liabilities. It indicates that liquidity position of the

Sainsbury is comparatively strong than that of Morrison (Patel, 2016).

Price earning ratio: Sainsbury’s PE ratio got decreased from 1.78 to 1.47 in 2014 while in

2015, it got improved to -0.50 which is not a good sign. Negative change in EPS by 19.51% in 2014

is the responsible reason behind declined PE ratio (Weaver & Weston, 2007).

. Decline in ratio may be due to exceptionally well performance as compare to the historical period

11

2014 23949 2.77% 22562 2.43%

2015 23775 -0.73% 22567 0.02%

2016 23506 -1.13% 22050 -2.29%

Rise in turnover is the reasons for high gross margin till 2014, however, thereafter, although

sales moved downward, but still, effective cost control mechanism to curtail direct expenditures

helps to maximize gross margin and improved its performance.

Net margin: From 2012 to 2015, net margin dropped down from 3.58% to 0.30%, thereafter,

got increased to 2.33% more than Morrison’s NM demonstrates that Sainsbury is performing well.

Control over SG&A expenses by 24.91%, reduction in interest expense by 2.44% and high

operational income are the reason for better return in 2016. It shows that Sainsbury’s performance

has been improved as its net earnings have been converted from negative £166m to £471m

(Saisnbury’s annual report, 2016).

ROCE: In 2015, Sainsbury borne loss on their total capital as its ROCE is -1.30% whereas

in 2016, it shows a sudden increase to 8.61%. Positive return worth £471m is the reason behind

improved ROCE is a sign of greater performance on total capital invested in the firm to carry out

regular business activities and operations (Marciukaityte & Szewczyk, 2011). .

Earning per share: Sainsbury’s EPS came down from 0.32 to -0.08 in 2015, whereas, in

next year, it got increased to 0.23 depicts that company delivered more return to their investors by

generating more yield on their total revenues (Agarwal & et.al., 2015).

Dividend payout ratio: In 2016, Sainsbury’s dividend payout ratio rose to 60.3%

comparatively higher than Morrison’s ratio indicates that it is distributing more dividends to the

shareholders out of total generated net earnings (Sainsbury, 2016).

Current ratio: In 2013, it came down from 0.65:1 to 0.61:1 is a sign of poor liquidity

position. While, thereafter, it shows a constant increase as in 2016, it got inclined to 0.66:1 and also

higher than Morrison’s CR. Increase in short-term investment by 43.48%, prepaid expenses by

8.08% and other CA by 7.91% is the reason behind high availability of nearby resources (Cleme &

Reilly, 2013). However, CL came down by 2.87% due to repayment of some short-term debt,

decreased trade payables and other short-term liabilities. It indicates that liquidity position of the

Sainsbury is comparatively strong than that of Morrison (Patel, 2016).

Price earning ratio: Sainsbury’s PE ratio got decreased from 1.78 to 1.47 in 2014 while in

2015, it got improved to -0.50 which is not a good sign. Negative change in EPS by 19.51% in 2014

is the responsible reason behind declined PE ratio (Weaver & Weston, 2007).

. Decline in ratio may be due to exceptionally well performance as compare to the historical period

11

or firm also may be undervalued.

Gearing ratio: Till 2015, it shows a regular increase from 66.18% to 78.26%, whereas, in

2016, it dropped down to 64.52% and also less than Morrison’s GR of 74.84%. Excessive collection

of equity capital by 14.91% increase and repayment of debt worth 12.15% are the two responsible

reasons for declined gearing ratio. It indicates that managers are trying to minimize their investment

risk to strengthen their solvency position and repay long-term creditors like debt-holders on time

(Daka & Basu, 2016).

Non-financial analysis

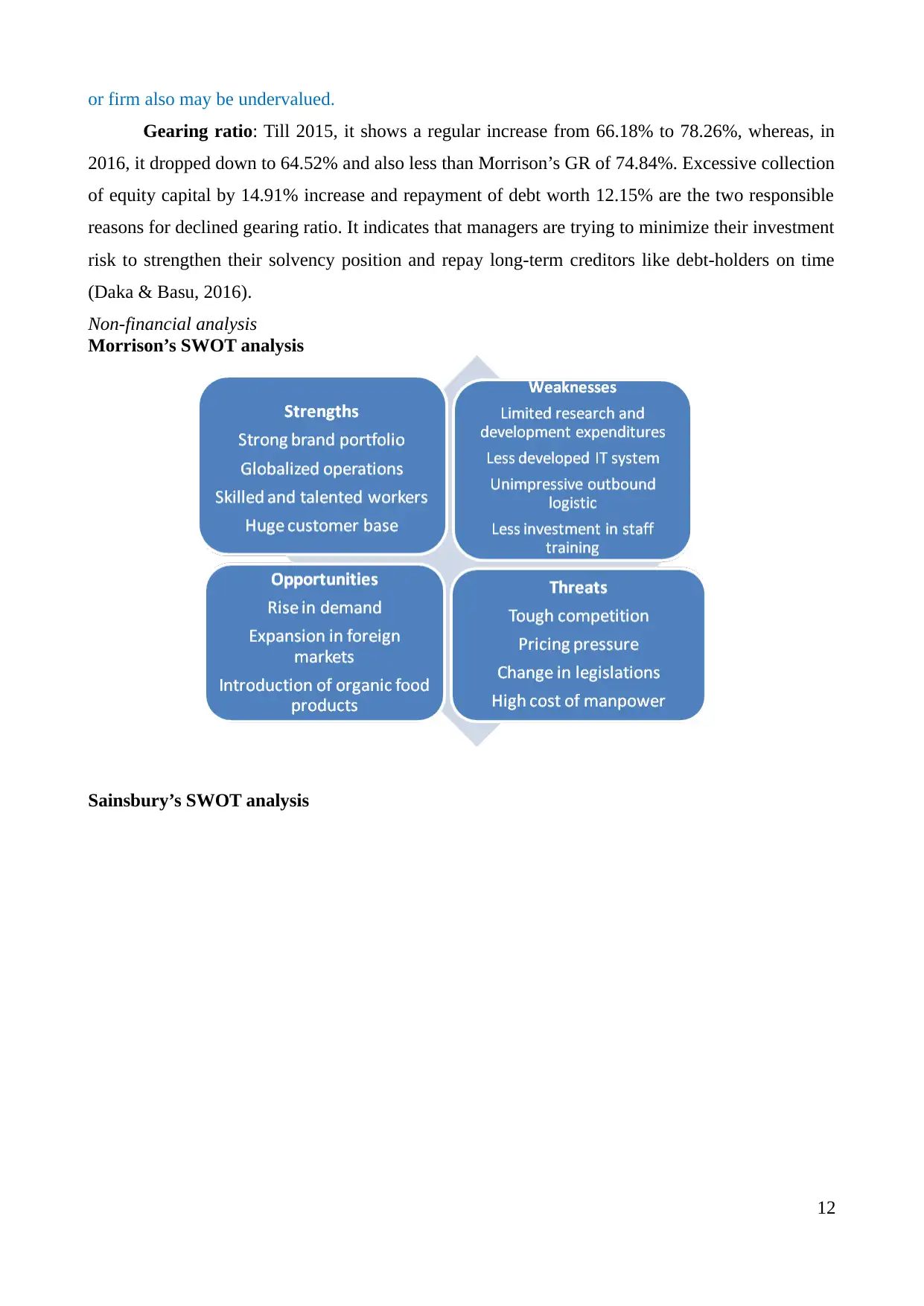

Morrison’s SWOT analysis

Sainsbury’s SWOT analysis

12

Gearing ratio: Till 2015, it shows a regular increase from 66.18% to 78.26%, whereas, in

2016, it dropped down to 64.52% and also less than Morrison’s GR of 74.84%. Excessive collection

of equity capital by 14.91% increase and repayment of debt worth 12.15% are the two responsible

reasons for declined gearing ratio. It indicates that managers are trying to minimize their investment

risk to strengthen their solvency position and repay long-term creditors like debt-holders on time

(Daka & Basu, 2016).

Non-financial analysis

Morrison’s SWOT analysis

Sainsbury’s SWOT analysis

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.