FINANCE 6: Financial Analysis of Comprehensive Income Statement

VerifiedAdded on 2022/08/17

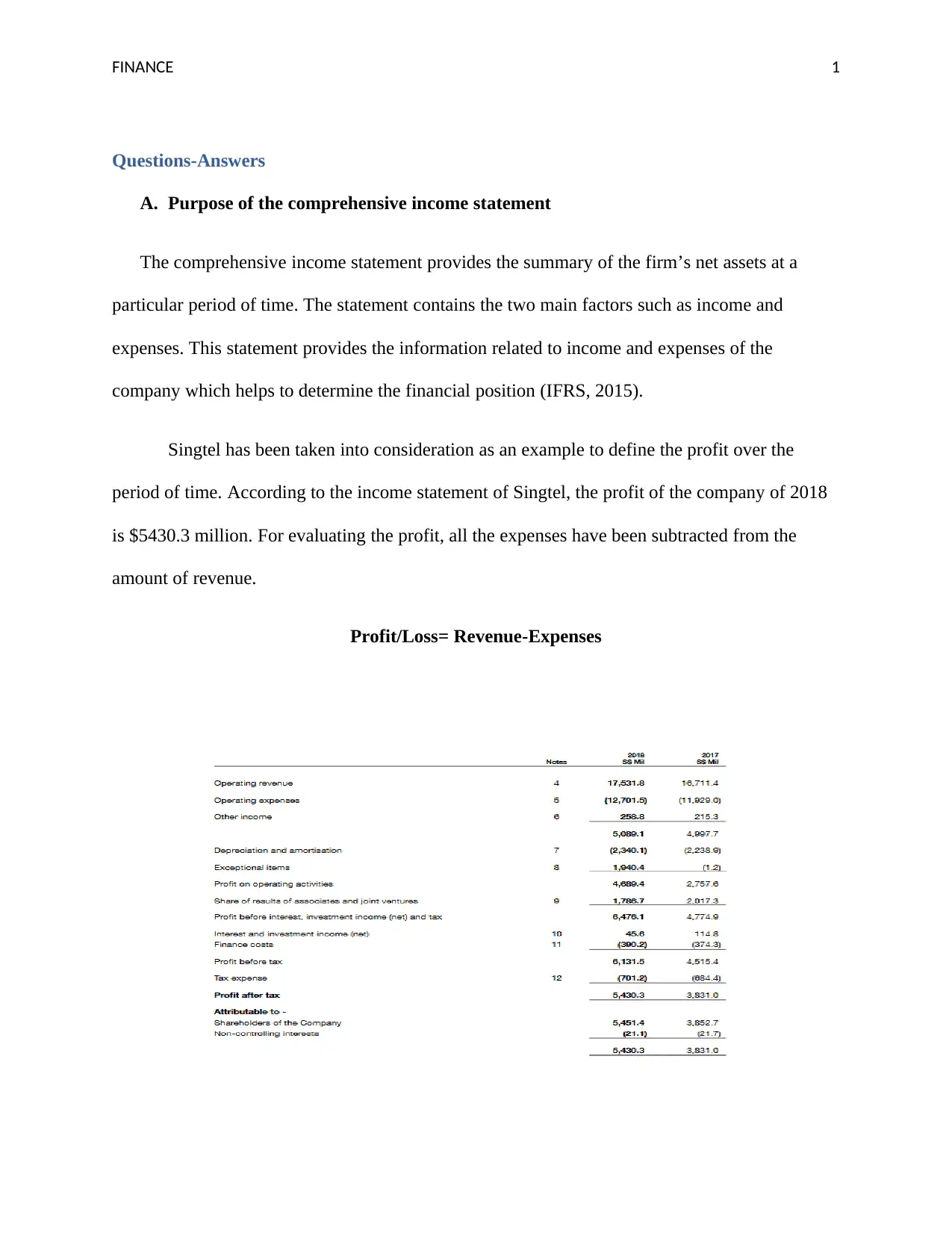

|10

|1688

|11

Report

AI Summary

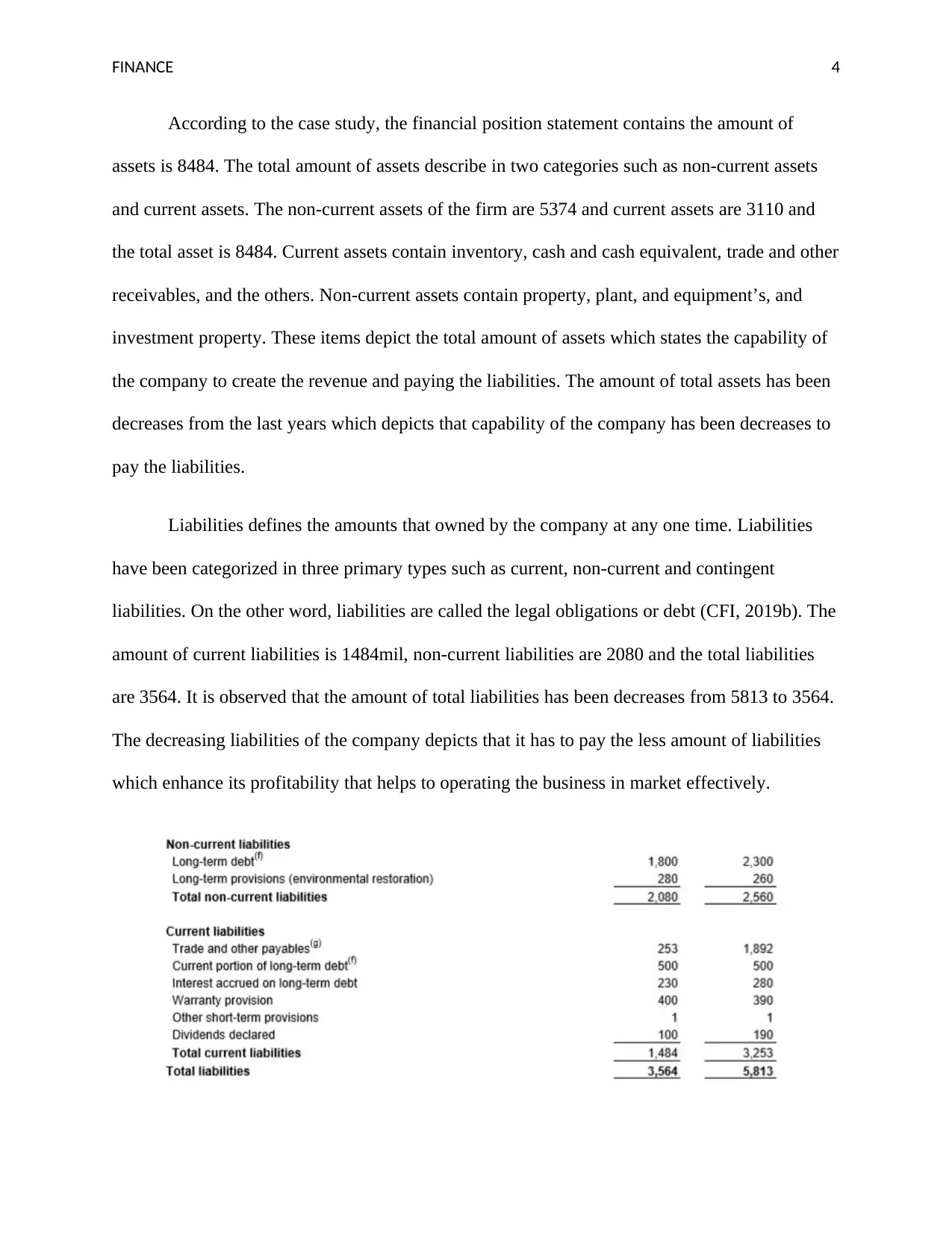

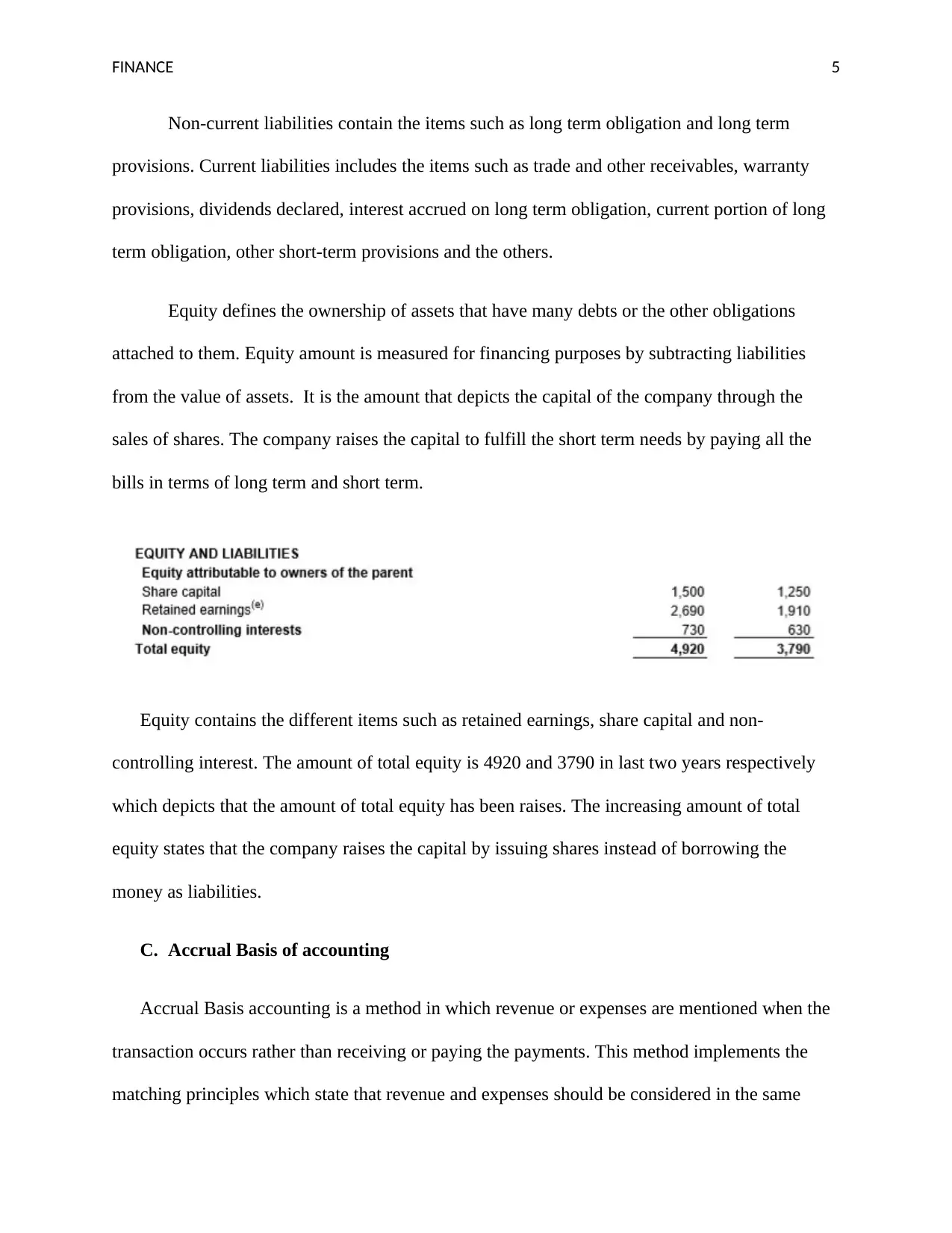

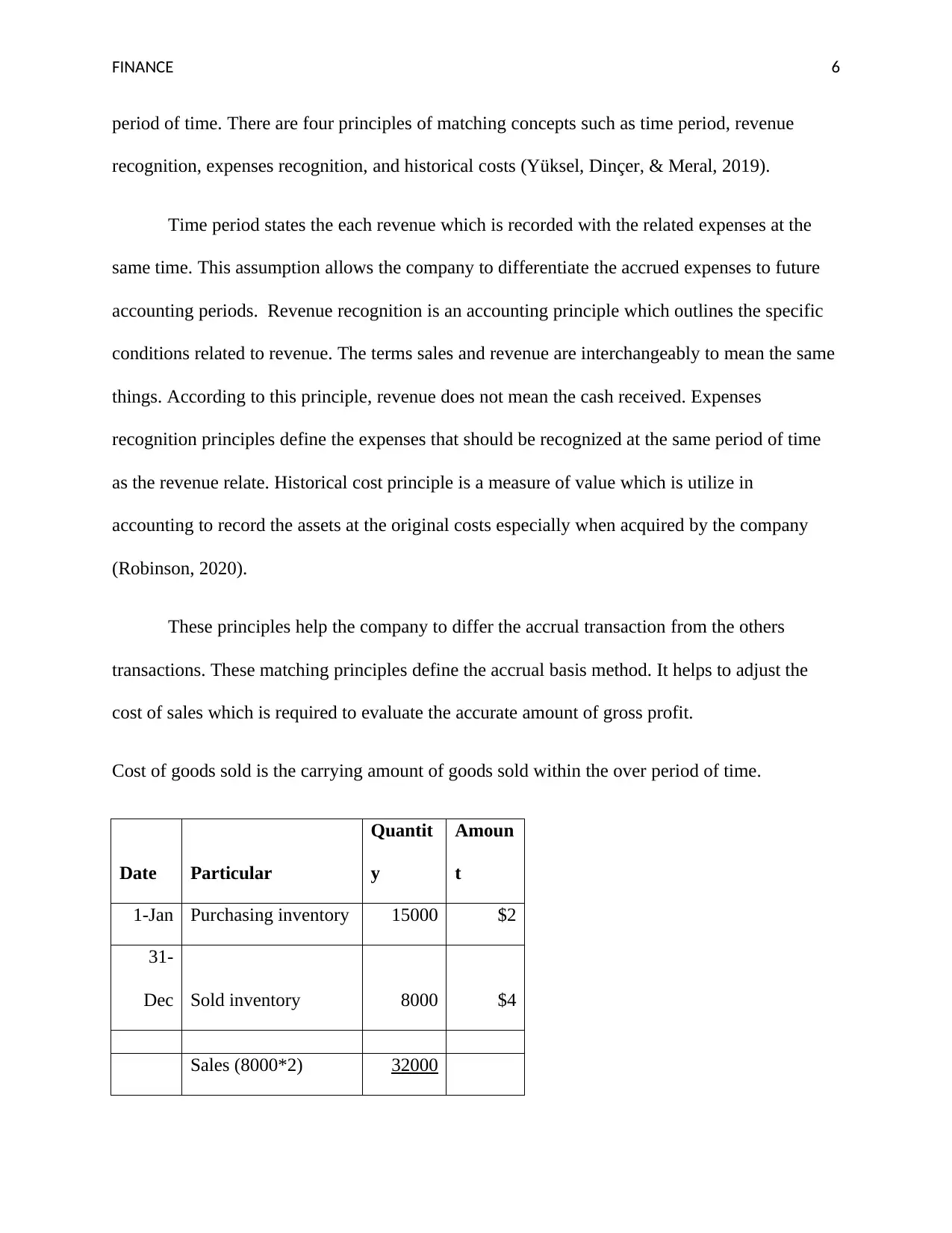

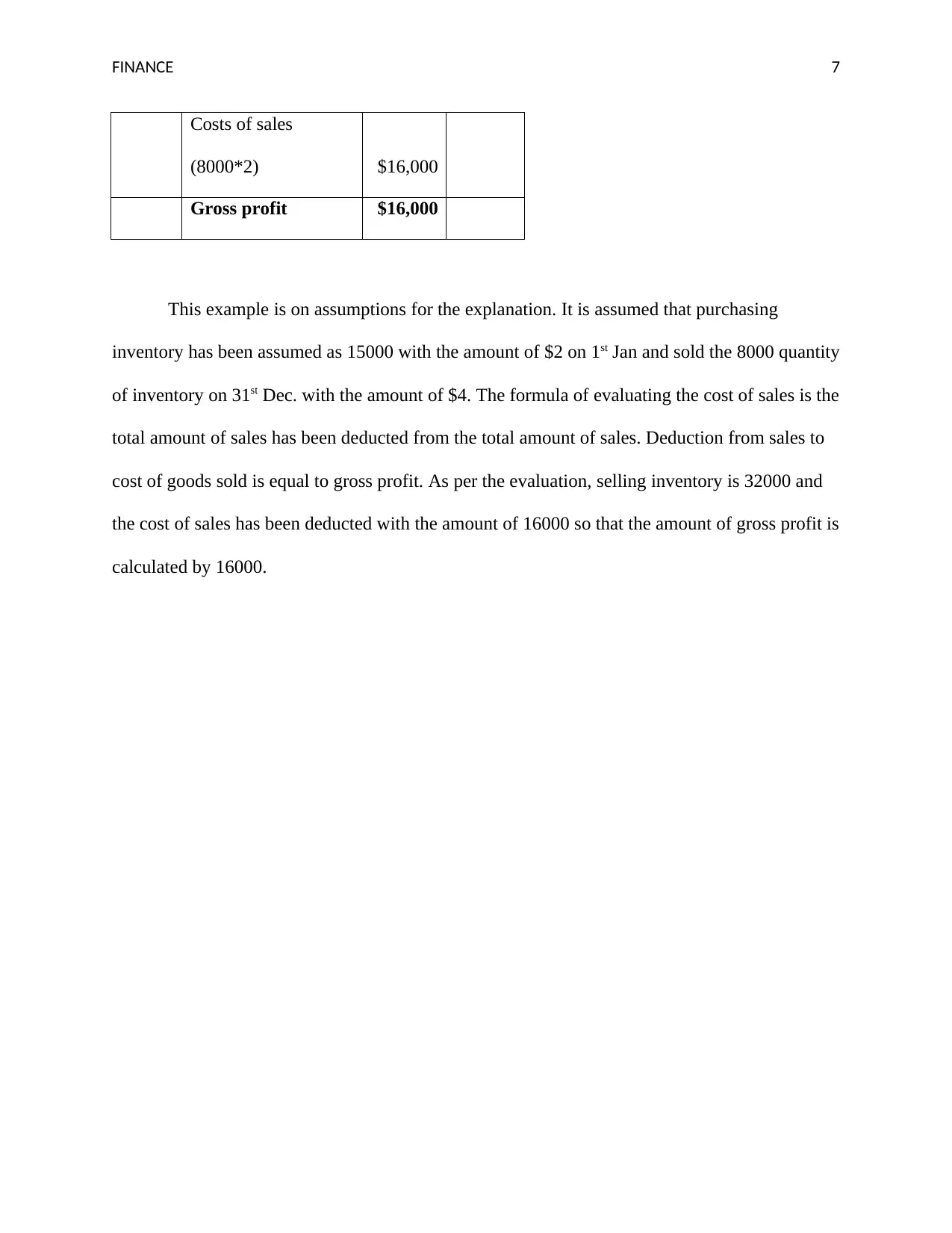

This report offers a comprehensive financial analysis, exploring the purpose of the comprehensive income statement, which summarizes a firm's net assets, including income and expenses. It uses Singtel as an example to illustrate profit calculation, emphasizing the deduction of expenses from revenue. The report differentiates between single and two-statement formats, highlighting the users of the information. It defines income and expenses, explains historical cost, and details the purpose of the financial position, which reveals a firm's assets, liabilities, and capital. The analysis covers the components of financial position, including assets, liabilities, and equity, along with the impact of changes in these components. It explains the accrual basis of accounting, its principles (time period, revenue recognition, expenses recognition, and historical costs), and provides an example to illustrate cost of goods sold calculation. The report references relevant sources for further understanding.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.