AC4410 Accounting & Finance: Financial Analysis Report on Shire Plc

VerifiedAdded on 2023/06/14

|11

|1953

|419

Report

AI Summary

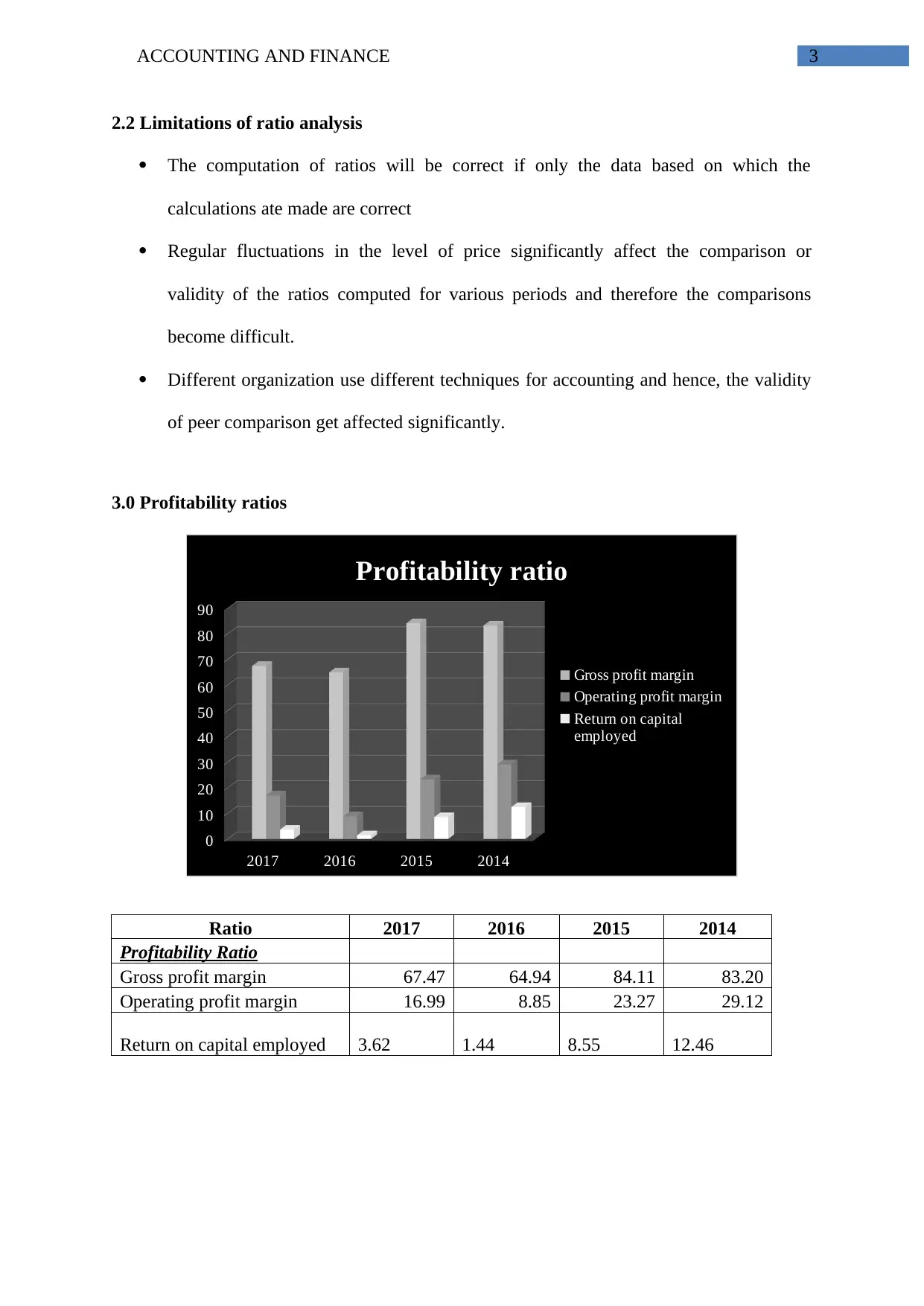

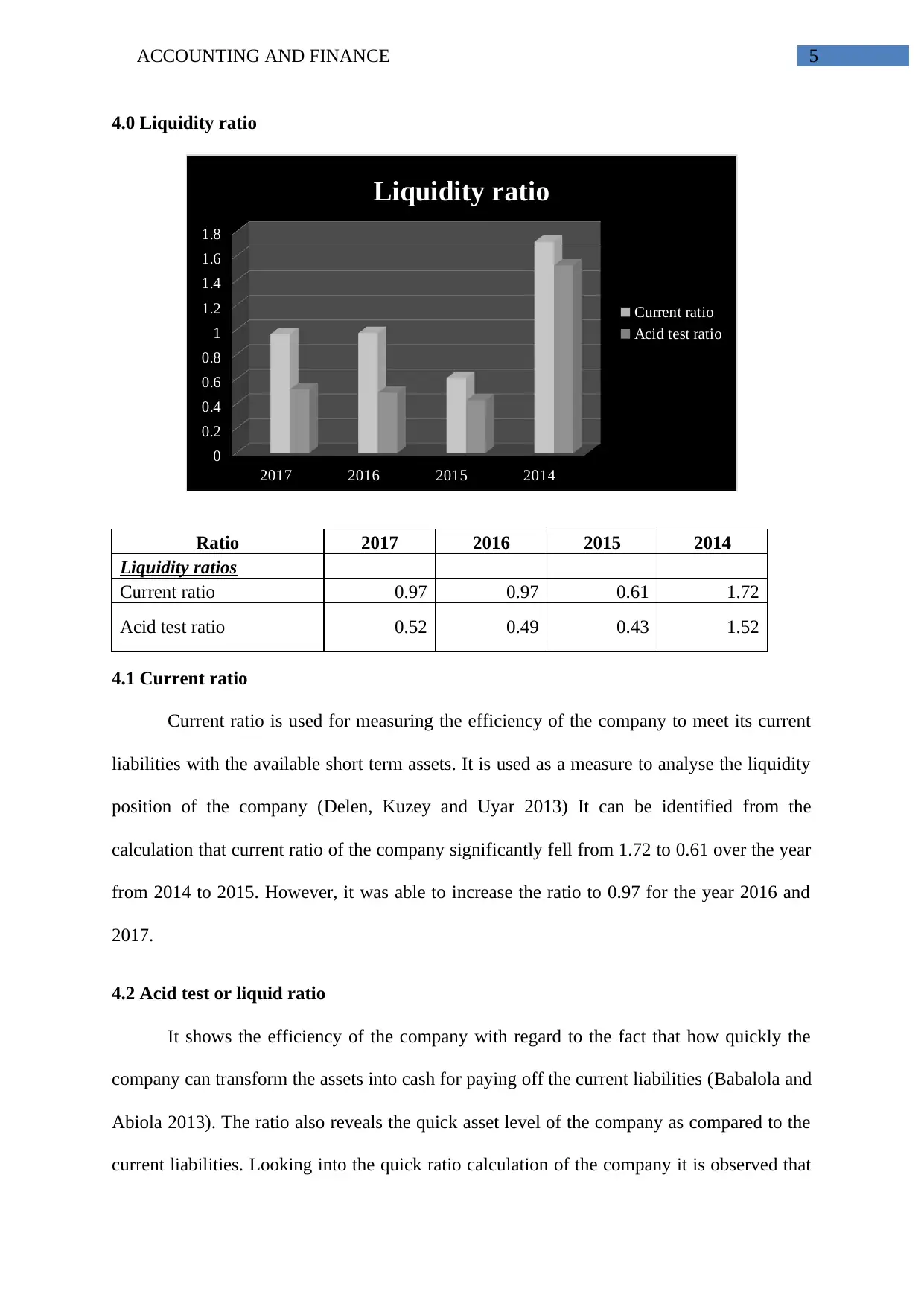

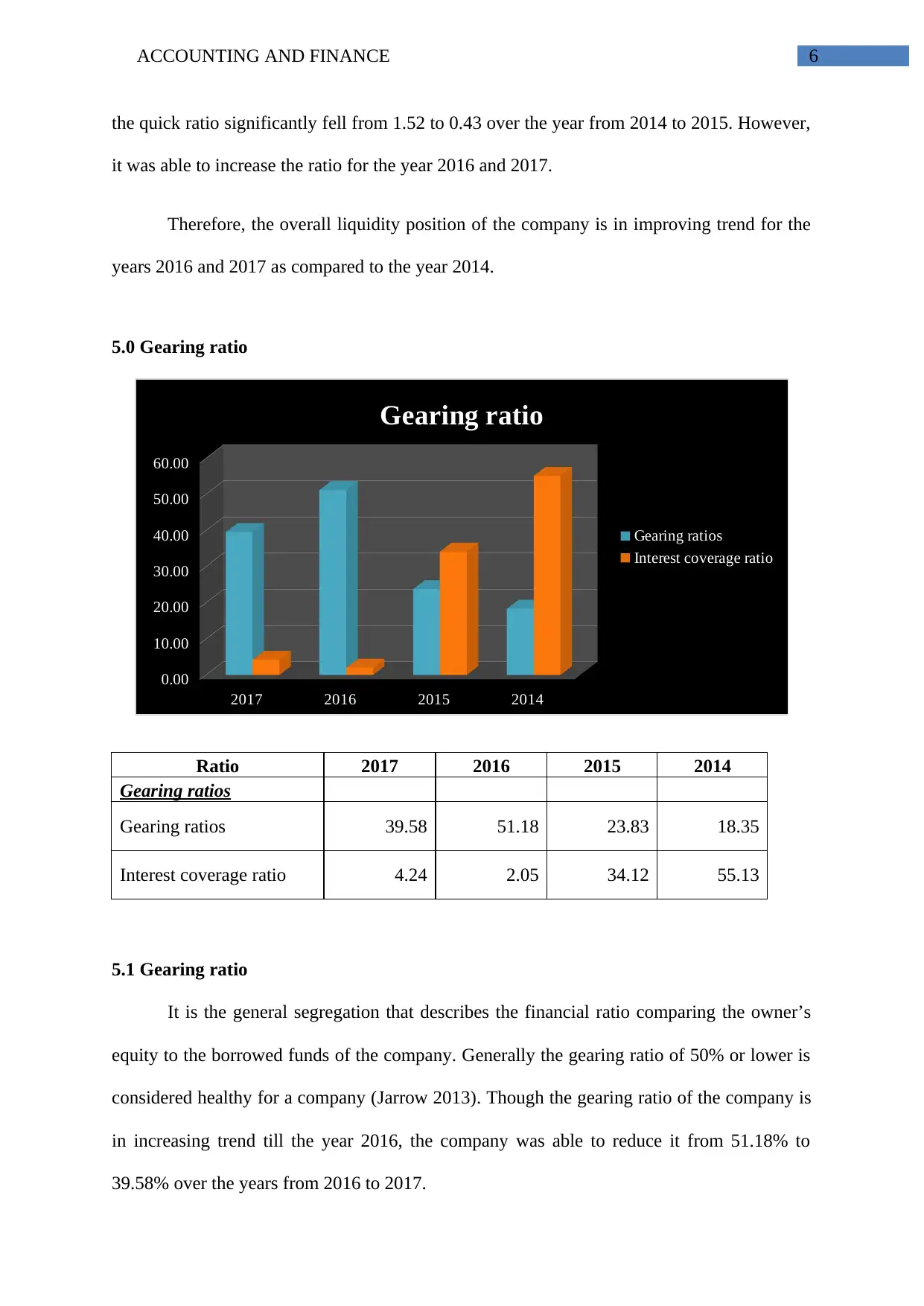

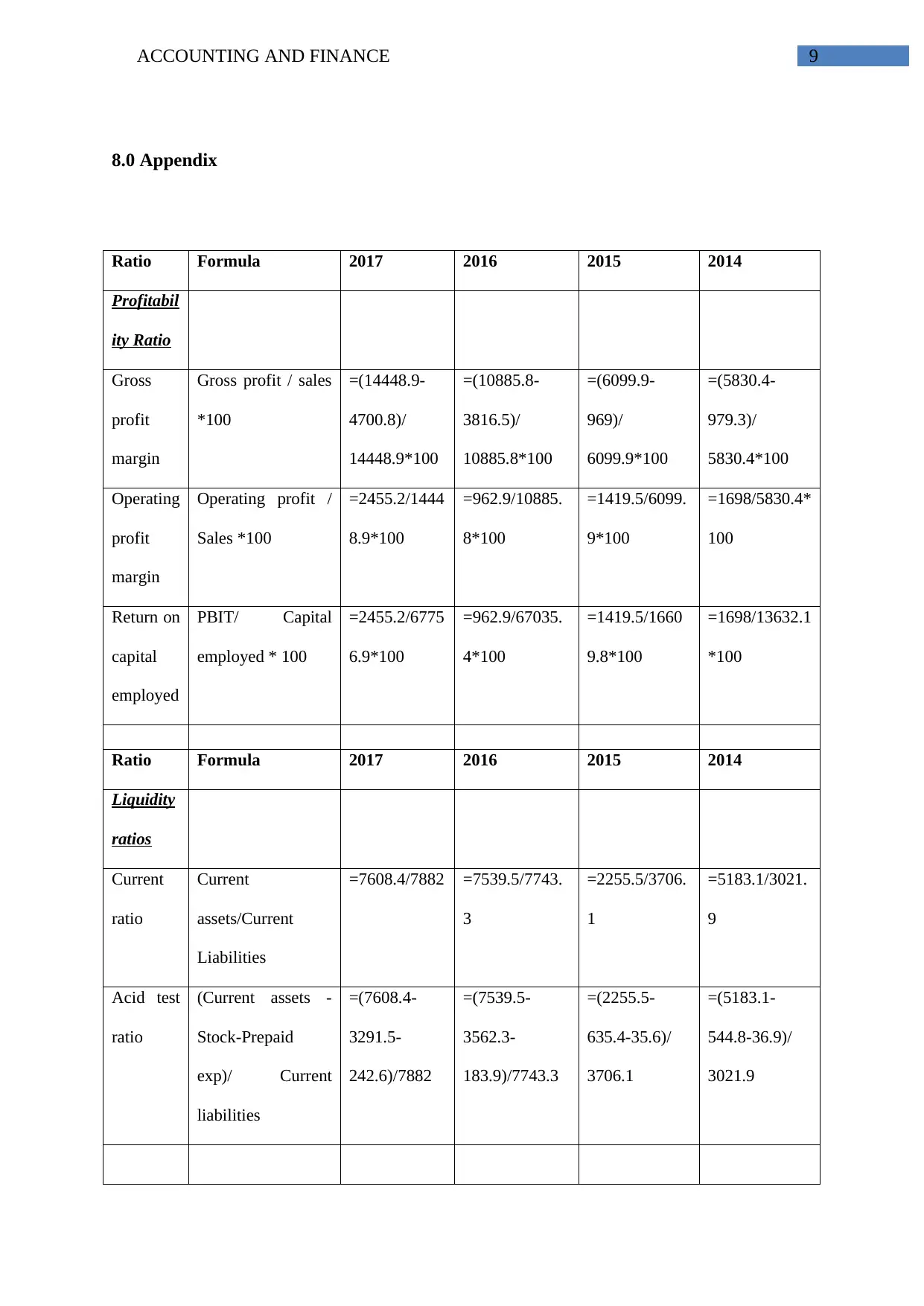

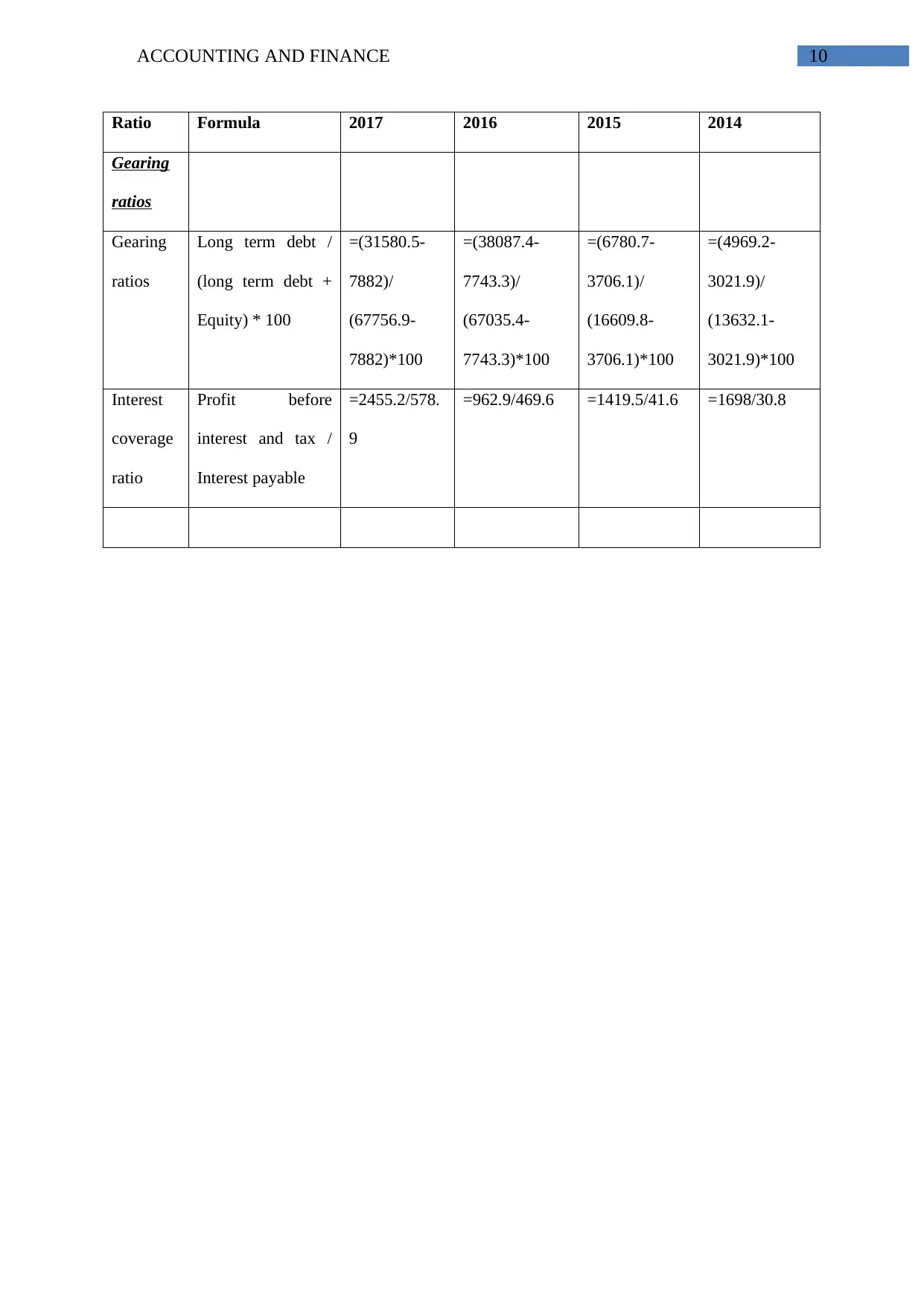

This report presents a financial analysis of Shire Plc, a biopharmaceutical company, using ratio analysis based on its financial statements from 2014 to 2017. The analysis covers profitability ratios (gross profit margin, operating profit margin, and return on capital employed), liquidity ratios (current ratio and acid test ratio), and gearing ratios (gearing ratio and interest coverage ratio). The report indicates that while the company experienced fluctuations in profitability and liquidity, it showed improvement in these areas in 2017. The gearing ratio also decreased in 2017, suggesting better financial health. The conclusion suggests that Shire Plc has a strong gross profit margin but needs to maintain focus on improving operating profit and return on capital employed. The company's liquidity and gearing positions improved in 2017, but further improvements can be achieved through strategic borrowing and short-term debt management. Desklib provides this document and many more solved assignments for students' reference.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.