ACC510 Financial Reporting Task 2 - Major Assignment, ATMC, 2017

VerifiedAdded on 2020/04/07

|11

|2501

|322

Homework Assignment

AI Summary

This document presents a detailed solution to ACC510 Financial Reporting Task 2, a major assignment completed at ATMC in Semester 2, 2017. The assignment addresses four key questions, each exploring crucial aspects of financial reporting. Question 1 examines fair value measurement, its accounting justifications, and its application in an aged care home scenario. Question 2 focuses on impairment testing, including calculations and journal entries for both 2016 and 2017. Question 3 delves into the accounting treatment of research and development costs, differentiating between the two phases. Finally, Question 4 analyzes employee benefit plans, specifically defined benefit plans, including calculations for deficit, net defined benefit liability, net interest, reconciliation, and summary journal entries. The solution provides accounting justifications, relevant issues, and detailed calculations for each question, referencing relevant accounting standards and providing insights into complex financial reporting topics.

ACC510 (ATMC) - Financial Reporting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Impairment Test 31/12/16....................................................................................................5

a. Calculations:.......................................................................................................................5

b. General Journal Entries 31/12/16:.....................................................................................6

2. Impairment Test 31/12/17....................................................................................................6

a. Calculations........................................................................................................................6

b. General Journal Entries 31/12/17:.....................................................................................7

Question 3. Case Study 6.1....................................................................................................................8

Accounting Justification:................................................................................................................8

Relevant Issues:.............................................................................................................................8

1. Difference between two phases:...........................................................................................8

2. Accounting for Research & Development:.............................................................................8

3. Decision / Conclusion / Reasons and Justification:................................................................8

Question 4. Ex 9.19................................................................................................................................9

Accounting Justification:................................................................................................................9

Relevant Issues:.............................................................................................................................9

1. Deficit of Fund...........................................................................................................................9

2. Net Defined Benefit Liability......................................................................................................9

3. Net Interest................................................................................................................................9

4. Reconciliation..........................................................................................................................10

5. Summary Journal.....................................................................................................................10

Page 2 of 11

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Impairment Test 31/12/16....................................................................................................5

a. Calculations:.......................................................................................................................5

b. General Journal Entries 31/12/16:.....................................................................................6

2. Impairment Test 31/12/17....................................................................................................6

a. Calculations........................................................................................................................6

b. General Journal Entries 31/12/17:.....................................................................................7

Question 3. Case Study 6.1....................................................................................................................8

Accounting Justification:................................................................................................................8

Relevant Issues:.............................................................................................................................8

1. Difference between two phases:...........................................................................................8

2. Accounting for Research & Development:.............................................................................8

3. Decision / Conclusion / Reasons and Justification:................................................................8

Question 4. Ex 9.19................................................................................................................................9

Accounting Justification:................................................................................................................9

Relevant Issues:.............................................................................................................................9

1. Deficit of Fund...........................................................................................................................9

2. Net Defined Benefit Liability......................................................................................................9

3. Net Interest................................................................................................................................9

4. Reconciliation..........................................................................................................................10

5. Summary Journal.....................................................................................................................10

Page 2 of 11

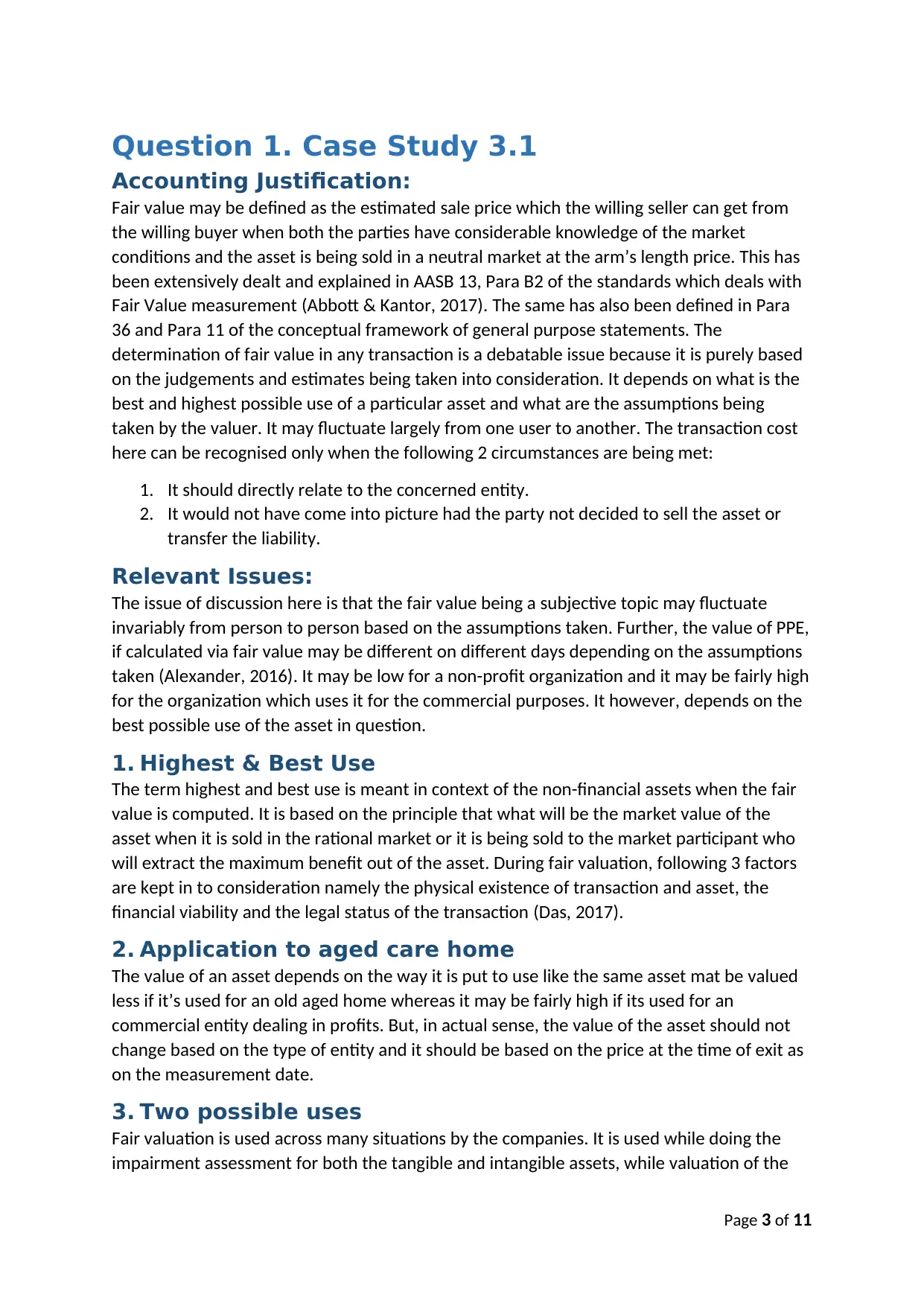

Question 1. Case Study 3.1

Accounting Justification:

Fair value may be defined as the estimated sale price which the willing seller can get from

the willing buyer when both the parties have considerable knowledge of the market

conditions and the asset is being sold in a neutral market at the arm’s length price. This has

been extensively dealt and explained in AASB 13, Para B2 of the standards which deals with

Fair Value measurement (Abbott & Kantor, 2017). The same has also been defined in Para

36 and Para 11 of the conceptual framework of general purpose statements. The

determination of fair value in any transaction is a debatable issue because it is purely based

on the judgements and estimates being taken into consideration. It depends on what is the

best and highest possible use of a particular asset and what are the assumptions being

taken by the valuer. It may fluctuate largely from one user to another. The transaction cost

here can be recognised only when the following 2 circumstances are being met:

1. It should directly relate to the concerned entity.

2. It would not have come into picture had the party not decided to sell the asset or

transfer the liability.

Relevant Issues:

The issue of discussion here is that the fair value being a subjective topic may fluctuate

invariably from person to person based on the assumptions taken. Further, the value of PPE,

if calculated via fair value may be different on different days depending on the assumptions

taken (Alexander, 2016). It may be low for a non-profit organization and it may be fairly high

for the organization which uses it for the commercial purposes. It however, depends on the

best possible use of the asset in question.

1. Highest & Best Use

The term highest and best use is meant in context of the non-financial assets when the fair

value is computed. It is based on the principle that what will be the market value of the

asset when it is sold in the rational market or it is being sold to the market participant who

will extract the maximum benefit out of the asset. During fair valuation, following 3 factors

are kept in to consideration namely the physical existence of transaction and asset, the

financial viability and the legal status of the transaction (Das, 2017).

2. Application to aged care home

The value of an asset depends on the way it is put to use like the same asset mat be valued

less if it’s used for an old aged home whereas it may be fairly high if its used for an

commercial entity dealing in profits. But, in actual sense, the value of the asset should not

change based on the type of entity and it should be based on the price at the time of exit as

on the measurement date.

3. Two possible uses

Fair valuation is used across many situations by the companies. It is used while doing the

impairment assessment for both the tangible and intangible assets, while valuation of the

Page 3 of 11

Accounting Justification:

Fair value may be defined as the estimated sale price which the willing seller can get from

the willing buyer when both the parties have considerable knowledge of the market

conditions and the asset is being sold in a neutral market at the arm’s length price. This has

been extensively dealt and explained in AASB 13, Para B2 of the standards which deals with

Fair Value measurement (Abbott & Kantor, 2017). The same has also been defined in Para

36 and Para 11 of the conceptual framework of general purpose statements. The

determination of fair value in any transaction is a debatable issue because it is purely based

on the judgements and estimates being taken into consideration. It depends on what is the

best and highest possible use of a particular asset and what are the assumptions being

taken by the valuer. It may fluctuate largely from one user to another. The transaction cost

here can be recognised only when the following 2 circumstances are being met:

1. It should directly relate to the concerned entity.

2. It would not have come into picture had the party not decided to sell the asset or

transfer the liability.

Relevant Issues:

The issue of discussion here is that the fair value being a subjective topic may fluctuate

invariably from person to person based on the assumptions taken. Further, the value of PPE,

if calculated via fair value may be different on different days depending on the assumptions

taken (Alexander, 2016). It may be low for a non-profit organization and it may be fairly high

for the organization which uses it for the commercial purposes. It however, depends on the

best possible use of the asset in question.

1. Highest & Best Use

The term highest and best use is meant in context of the non-financial assets when the fair

value is computed. It is based on the principle that what will be the market value of the

asset when it is sold in the rational market or it is being sold to the market participant who

will extract the maximum benefit out of the asset. During fair valuation, following 3 factors

are kept in to consideration namely the physical existence of transaction and asset, the

financial viability and the legal status of the transaction (Das, 2017).

2. Application to aged care home

The value of an asset depends on the way it is put to use like the same asset mat be valued

less if it’s used for an old aged home whereas it may be fairly high if its used for an

commercial entity dealing in profits. But, in actual sense, the value of the asset should not

change based on the type of entity and it should be based on the price at the time of exit as

on the measurement date.

3. Two possible uses

Fair valuation is used across many situations by the companies. It is used while doing the

impairment assessment for both the tangible and intangible assets, while valuation of the

Page 3 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inventory as per the IFRS standards, while taking over entity in the course of amalgamation

or merger, etc. Further, it is a basic requirement in some of the IFRS standards as well.

Page 4 of 11

or merger, etc. Further, it is a basic requirement in some of the IFRS standards as well.

Page 4 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

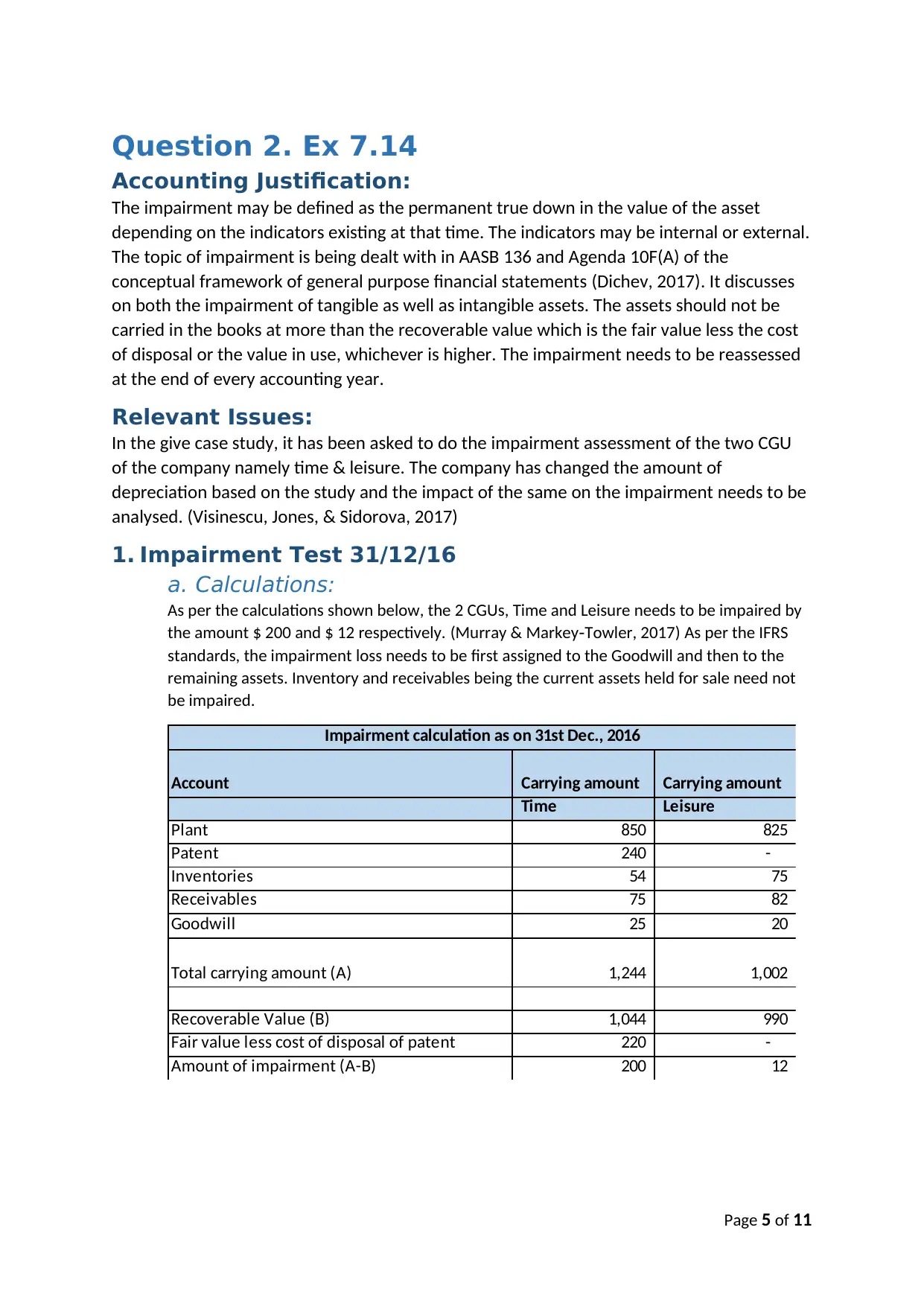

Question 2. Ex 7.14

Accounting Justification:

The impairment may be defined as the permanent true down in the value of the asset

depending on the indicators existing at that time. The indicators may be internal or external.

The topic of impairment is being dealt with in AASB 136 and Agenda 10F(A) of the

conceptual framework of general purpose financial statements (Dichev, 2017). It discusses

on both the impairment of tangible as well as intangible assets. The assets should not be

carried in the books at more than the recoverable value which is the fair value less the cost

of disposal or the value in use, whichever is higher. The impairment needs to be reassessed

at the end of every accounting year.

Relevant Issues:

In the give case study, it has been asked to do the impairment assessment of the two CGU

of the company namely time & leisure. The company has changed the amount of

depreciation based on the study and the impact of the same on the impairment needs to be

analysed. (Visinescu, Jones, & Sidorova, 2017)

1. Impairment Test 31/12/16

a. Calculations:

As per the calculations shown below, the 2 CGUs, Time and Leisure needs to be impaired by

the amount $ 200 and $ 12 respectively. (Murray & Markey Towler, 2017)‐ As per the IFRS

standards, the impairment loss needs to be first assigned to the Goodwill and then to the

remaining assets. Inventory and receivables being the current assets held for sale need not

be impaired.

Account Carrying amount Carrying amount

Time Leisure

Plant 850 825

Patent 240 -

Inventories 54 75

Receivables 75 82

Goodwill 25 20

Total carrying amount (A) 1,244 1,002

Recoverable Value (B) 1,044 990

Fair value less cost of disposal of patent 220 -

Amount of impairment (A-B) 200 12

Impairment calculation as on 31st Dec., 2016

Page 5 of 11

Accounting Justification:

The impairment may be defined as the permanent true down in the value of the asset

depending on the indicators existing at that time. The indicators may be internal or external.

The topic of impairment is being dealt with in AASB 136 and Agenda 10F(A) of the

conceptual framework of general purpose financial statements (Dichev, 2017). It discusses

on both the impairment of tangible as well as intangible assets. The assets should not be

carried in the books at more than the recoverable value which is the fair value less the cost

of disposal or the value in use, whichever is higher. The impairment needs to be reassessed

at the end of every accounting year.

Relevant Issues:

In the give case study, it has been asked to do the impairment assessment of the two CGU

of the company namely time & leisure. The company has changed the amount of

depreciation based on the study and the impact of the same on the impairment needs to be

analysed. (Visinescu, Jones, & Sidorova, 2017)

1. Impairment Test 31/12/16

a. Calculations:

As per the calculations shown below, the 2 CGUs, Time and Leisure needs to be impaired by

the amount $ 200 and $ 12 respectively. (Murray & Markey Towler, 2017)‐ As per the IFRS

standards, the impairment loss needs to be first assigned to the Goodwill and then to the

remaining assets. Inventory and receivables being the current assets held for sale need not

be impaired.

Account Carrying amount Carrying amount

Time Leisure

Plant 850 825

Patent 240 -

Inventories 54 75

Receivables 75 82

Goodwill 25 20

Total carrying amount (A) 1,244 1,002

Recoverable Value (B) 1,044 990

Fair value less cost of disposal of patent 220 -

Amount of impairment (A-B) 200 12

Impairment calculation as on 31st Dec., 2016

Page 5 of 11

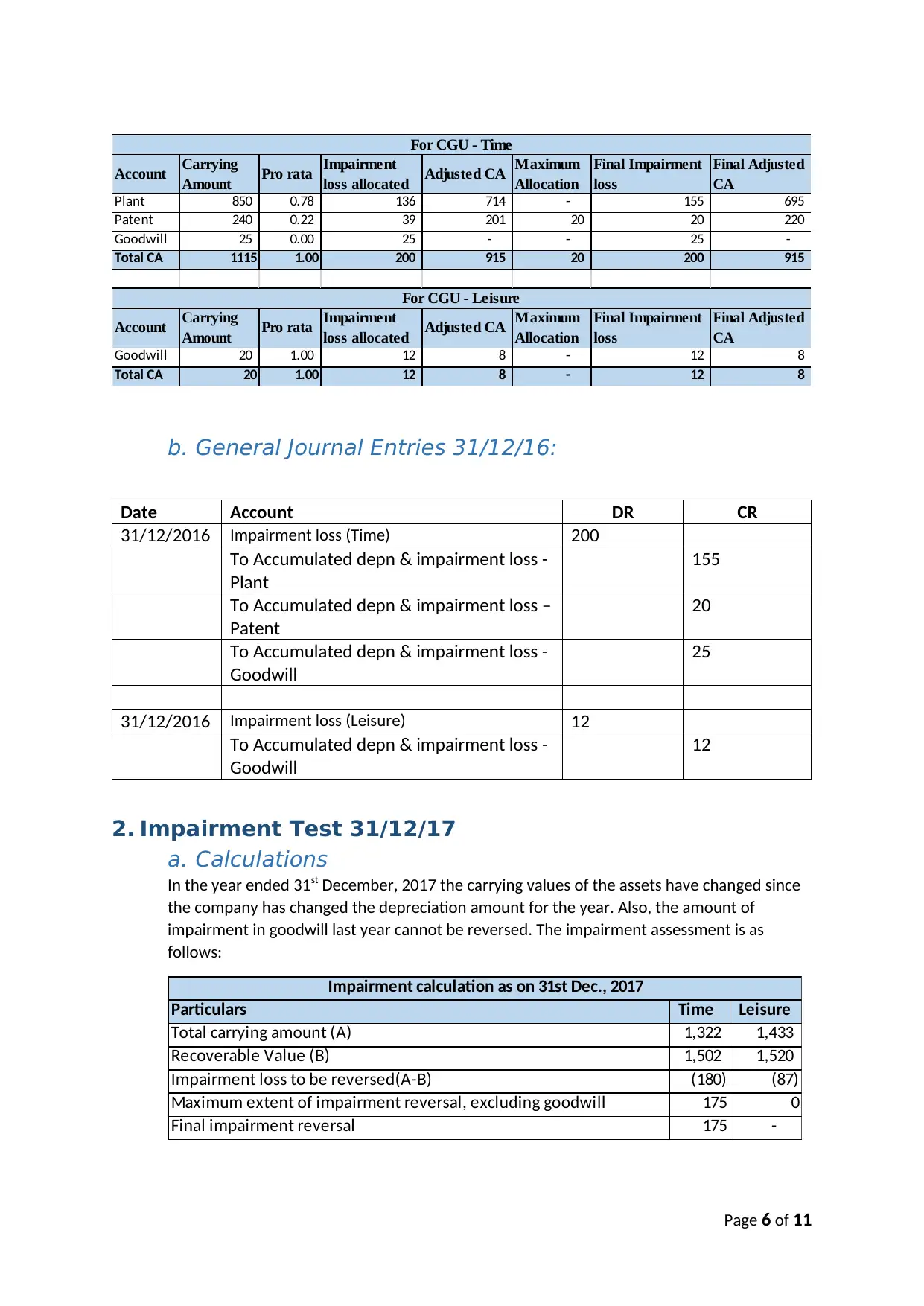

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Plant 850 0.78 136 714 - 155 695

Patent 240 0.22 39 201 20 20 220

Goodwill 25 0.00 25 - - 25 -

Total CA 1115 1.00 200 915 20 200 915

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Goodwill 20 1.00 12 8 - 12 8

Total CA 20 1.00 12 8 - 12 8

For CGU - Time

For CGU - Leisure

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/2016 Impairment loss (Time) 200

To Accumulated depn & impairment loss -

Plant

155

To Accumulated depn & impairment loss –

Patent

20

To Accumulated depn & impairment loss -

Goodwill

25

31/12/2016 Impairment loss (Leisure) 12

To Accumulated depn & impairment loss -

Goodwill

12

2. Impairment Test 31/12/17

a. Calculations

In the year ended 31st December, 2017 the carrying values of the assets have changed since

the company has changed the depreciation amount for the year. Also, the amount of

impairment in goodwill last year cannot be reversed. The impairment assessment is as

follows:

Particulars Time Leisure

Total carrying amount (A) 1,322 1,433

Recoverable Value (B) 1,502 1,520

Impairment loss to be reversed(A-B) (180) (87)

Maximum extent of impairment reversal, excluding goodwill 175 0

Final impairment reversal 175 -

Impairment calculation as on 31st Dec., 2017

Page 6 of 11

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Plant 850 0.78 136 714 - 155 695

Patent 240 0.22 39 201 20 20 220

Goodwill 25 0.00 25 - - 25 -

Total CA 1115 1.00 200 915 20 200 915

Account Carrying

Amount Pro rata Impairment

loss allocated Adjusted CA Maximum

Allocation

Final Impairment

loss

Final Adjusted

CA

Goodwill 20 1.00 12 8 - 12 8

Total CA 20 1.00 12 8 - 12 8

For CGU - Time

For CGU - Leisure

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/2016 Impairment loss (Time) 200

To Accumulated depn & impairment loss -

Plant

155

To Accumulated depn & impairment loss –

Patent

20

To Accumulated depn & impairment loss -

Goodwill

25

31/12/2016 Impairment loss (Leisure) 12

To Accumulated depn & impairment loss -

Goodwill

12

2. Impairment Test 31/12/17

a. Calculations

In the year ended 31st December, 2017 the carrying values of the assets have changed since

the company has changed the depreciation amount for the year. Also, the amount of

impairment in goodwill last year cannot be reversed. The impairment assessment is as

follows:

Particulars Time Leisure

Total carrying amount (A) 1,322 1,433

Recoverable Value (B) 1,502 1,520

Impairment loss to be reversed(A-B) (180) (87)

Maximum extent of impairment reversal, excluding goodwill 175 0

Final impairment reversal 175 -

Impairment calculation as on 31st Dec., 2017

Page 6 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b. General Journal Entries 31/12/17:

Date Account DR CR

31/12/2017 Accumulated depn & impairment loss -

Plant

155

Accumulated depn & impairment loss

– Patent

20

To Impairment Loss (Time) 175

Page 7 of 11

Date Account DR CR

31/12/2017 Accumulated depn & impairment loss -

Plant

155

Accumulated depn & impairment loss

– Patent

20

To Impairment Loss (Time) 175

Page 7 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3. Case Study 6.1

Accounting Justification:

Paragraph 8 of AASB 138 deals with the classification, identification, measurement and

accounting of the research cost particularly in the case of the intangible assets. (Trieu, 2017)

Furthermore, SSAP 13 of the conceptual accounting framework also deals with the issues

research and development costs of intangible assets. Research cost is the initial cost being

incurred by the company when it is not sure of whether the project can be taken to

development or if it will be profitable and feasible to go ahead with it. It is the process

before the development of the asset starts. Development is a post facto activity which is

done once the research is over and the company has decided to pursue with the

development based on the technical feasibility and future economic benefits available. In

the development phase, the company develops the innovative products or the

technologically enhanced product based on the findings during the research phase

(Heminway, 2017). In case there is a classification issue between the research and the

development phase, the same needs to be considered as the research cost entirely in the

absence of the necessary information.

Relevant Issues:

The relevant issue here for discussion is the classification between the research and the

development cost and how the same is to be accounted in the financial books of accounts.

1. Difference between two phases:

Going by the definition, we can find a lot of differences between the research and the

development phase. However, the major difference here is the research phase may or

may not give rise to the intangible asset in the books but once the development is there,

it is certain to give rise to asset in the books. The stage of development always comes

after the research phase and when the technical and scientific feasibility of the same has

been seen. (Raiborn, Butler, & Martin, 2016)

2. Accounting for Research & Development:

The research cost is the cost which may or may not give financial feasibility to the

company and hence the company is not sure to account it as an asset and hence the

same should be charged as expense to P&L as and when it is incurred (Félix, 2017).

However, development of the asset occurs only when the company has checked on the

technical and scientific feasibility and that the development is going to give the future

economic benefits to the entity and should therefore be accounted as intangible assets

in the books. In case any incidental or related costs are incurred during development

phase, the same should also be capitalized.

3. Decision / Conclusion / Reasons and Justification:

The conclusion on the basis of the above study is that the research expenses needs to be

charged off as expenses in the P&L whereas the development expenses needs to be

capitalized to form the intangible asset. However, before accounting the same, few

situations needs to be checked like if it is saleable in the open market, if it is

Page 8 of 11

Accounting Justification:

Paragraph 8 of AASB 138 deals with the classification, identification, measurement and

accounting of the research cost particularly in the case of the intangible assets. (Trieu, 2017)

Furthermore, SSAP 13 of the conceptual accounting framework also deals with the issues

research and development costs of intangible assets. Research cost is the initial cost being

incurred by the company when it is not sure of whether the project can be taken to

development or if it will be profitable and feasible to go ahead with it. It is the process

before the development of the asset starts. Development is a post facto activity which is

done once the research is over and the company has decided to pursue with the

development based on the technical feasibility and future economic benefits available. In

the development phase, the company develops the innovative products or the

technologically enhanced product based on the findings during the research phase

(Heminway, 2017). In case there is a classification issue between the research and the

development phase, the same needs to be considered as the research cost entirely in the

absence of the necessary information.

Relevant Issues:

The relevant issue here for discussion is the classification between the research and the

development cost and how the same is to be accounted in the financial books of accounts.

1. Difference between two phases:

Going by the definition, we can find a lot of differences between the research and the

development phase. However, the major difference here is the research phase may or

may not give rise to the intangible asset in the books but once the development is there,

it is certain to give rise to asset in the books. The stage of development always comes

after the research phase and when the technical and scientific feasibility of the same has

been seen. (Raiborn, Butler, & Martin, 2016)

2. Accounting for Research & Development:

The research cost is the cost which may or may not give financial feasibility to the

company and hence the company is not sure to account it as an asset and hence the

same should be charged as expense to P&L as and when it is incurred (Félix, 2017).

However, development of the asset occurs only when the company has checked on the

technical and scientific feasibility and that the development is going to give the future

economic benefits to the entity and should therefore be accounted as intangible assets

in the books. In case any incidental or related costs are incurred during development

phase, the same should also be capitalized.

3. Decision / Conclusion / Reasons and Justification:

The conclusion on the basis of the above study is that the research expenses needs to be

charged off as expenses in the P&L whereas the development expenses needs to be

capitalized to form the intangible asset. However, before accounting the same, few

situations needs to be checked like if it is saleable in the open market, if it is

Page 8 of 11

commercially feasible, whether there was an intention to create the asset, whether

there will be any future economic benefits out of it and finally if it can be reliably

measured.

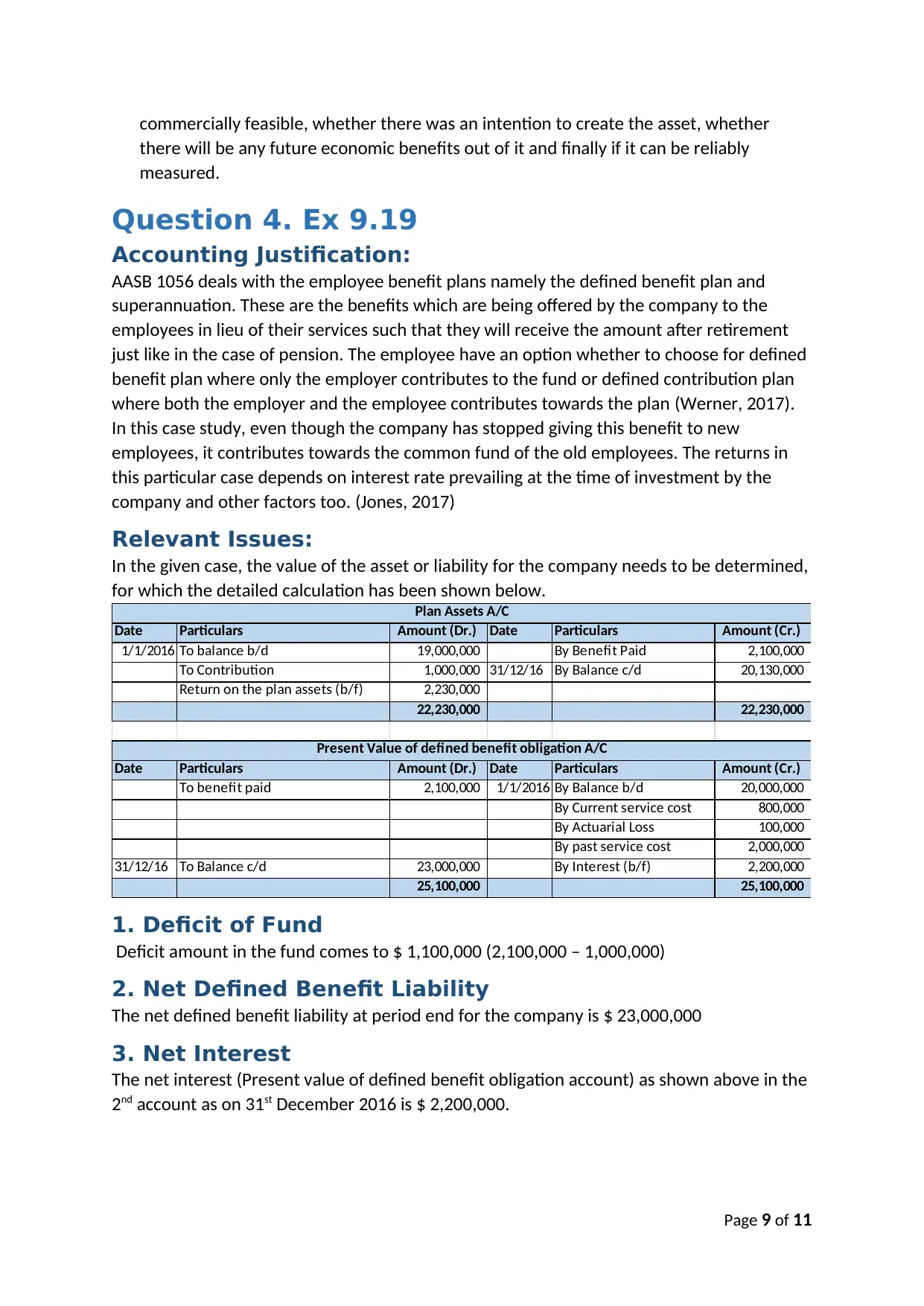

Question 4. Ex 9.19

Accounting Justification:

AASB 1056 deals with the employee benefit plans namely the defined benefit plan and

superannuation. These are the benefits which are being offered by the company to the

employees in lieu of their services such that they will receive the amount after retirement

just like in the case of pension. The employee have an option whether to choose for defined

benefit plan where only the employer contributes to the fund or defined contribution plan

where both the employer and the employee contributes towards the plan (Werner, 2017).

In this case study, even though the company has stopped giving this benefit to new

employees, it contributes towards the common fund of the old employees. The returns in

this particular case depends on interest rate prevailing at the time of investment by the

company and other factors too. (Jones, 2017)

Relevant Issues:

In the given case, the value of the asset or liability for the company needs to be determined,

for which the detailed calculation has been shown below.

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

1/1/2016 To balance b/d 19,000,000 By Benefit Paid 2,100,000

To Contribution 1,000,000 31/12/16 By Balance c/d 20,130,000

Return on the plan assets (b/f) 2,230,000

22,230,000 22,230,000

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

To benefit paid 2,100,000 1/1/2016 By Balance b/d 20,000,000

By Current service cost 800,000

By Actuarial Loss 100,000

By past service cost 2,000,000

31/12/16 To Balance c/d 23,000,000 By Interest (b/f) 2,200,000

25,100,000 25,100,000

Plan Assets A/C

Present Value of defined benefit obligation A/C

1. Deficit of Fund

Deficit amount in the fund comes to $ 1,100,000 (2,100,000 – 1,000,000)

2. Net Defined Benefit Liability

The net defined benefit liability at period end for the company is $ 23,000,000

3. Net Interest

The net interest (Present value of defined benefit obligation account) as shown above in the

2nd account as on 31st December 2016 is $ 2,200,000.

Page 9 of 11

there will be any future economic benefits out of it and finally if it can be reliably

measured.

Question 4. Ex 9.19

Accounting Justification:

AASB 1056 deals with the employee benefit plans namely the defined benefit plan and

superannuation. These are the benefits which are being offered by the company to the

employees in lieu of their services such that they will receive the amount after retirement

just like in the case of pension. The employee have an option whether to choose for defined

benefit plan where only the employer contributes to the fund or defined contribution plan

where both the employer and the employee contributes towards the plan (Werner, 2017).

In this case study, even though the company has stopped giving this benefit to new

employees, it contributes towards the common fund of the old employees. The returns in

this particular case depends on interest rate prevailing at the time of investment by the

company and other factors too. (Jones, 2017)

Relevant Issues:

In the given case, the value of the asset or liability for the company needs to be determined,

for which the detailed calculation has been shown below.

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

1/1/2016 To balance b/d 19,000,000 By Benefit Paid 2,100,000

To Contribution 1,000,000 31/12/16 By Balance c/d 20,130,000

Return on the plan assets (b/f) 2,230,000

22,230,000 22,230,000

Date Particulars Amount (Dr.) Date Particulars Amount (Cr.)

To benefit paid 2,100,000 1/1/2016 By Balance b/d 20,000,000

By Current service cost 800,000

By Actuarial Loss 100,000

By past service cost 2,000,000

31/12/16 To Balance c/d 23,000,000 By Interest (b/f) 2,200,000

25,100,000 25,100,000

Plan Assets A/C

Present Value of defined benefit obligation A/C

1. Deficit of Fund

Deficit amount in the fund comes to $ 1,100,000 (2,100,000 – 1,000,000)

2. Net Defined Benefit Liability

The net defined benefit liability at period end for the company is $ 23,000,000

3. Net Interest

The net interest (Present value of defined benefit obligation account) as shown above in the

2nd account as on 31st December 2016 is $ 2,200,000.

Page 9 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

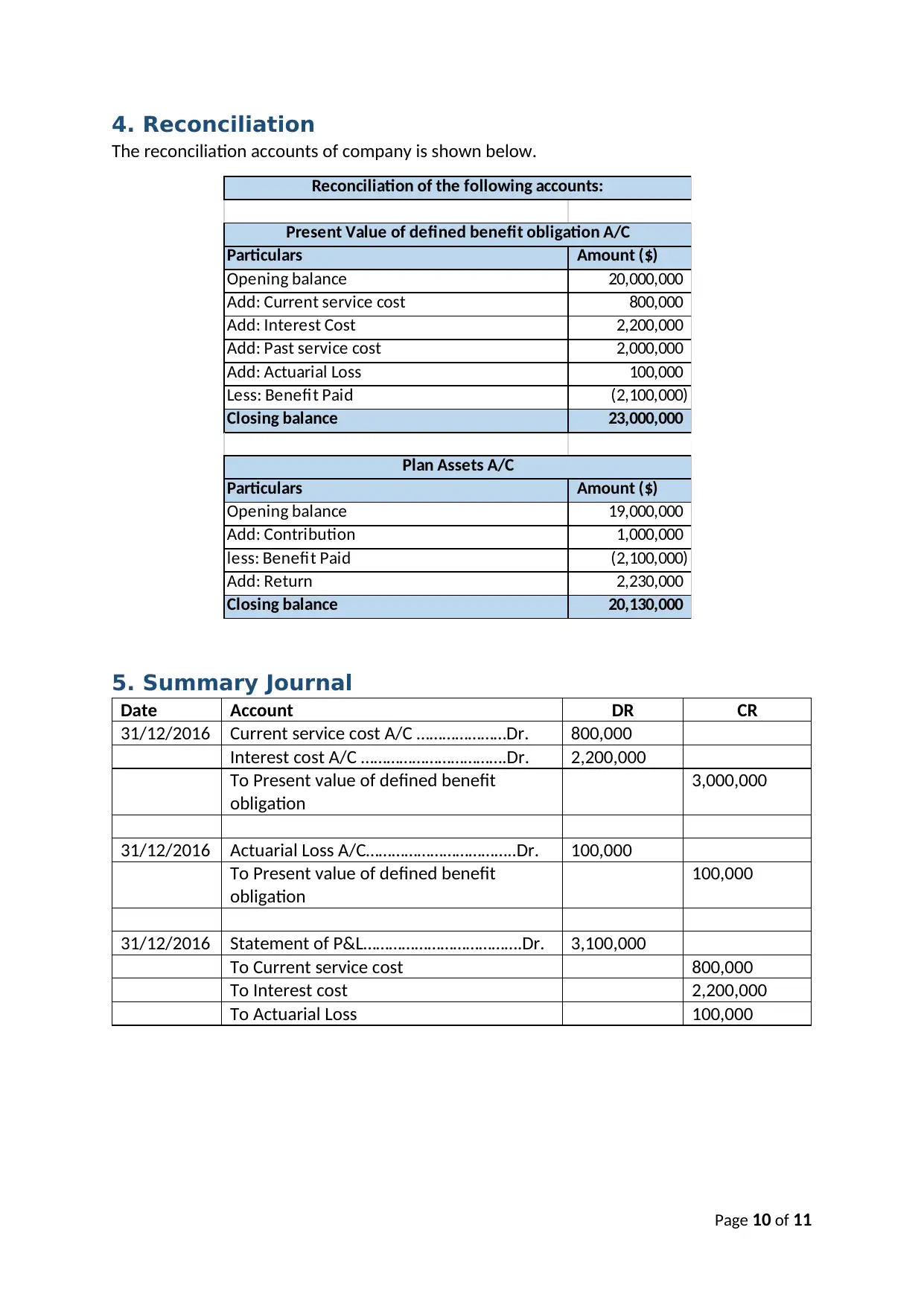

4. Reconciliation

The reconciliation accounts of company is shown below.

Particulars Amount ($)

Opening balance 20,000,000

Add: Current service cost 800,000

Add: Interest Cost 2,200,000

Add: Past service cost 2,000,000

Add: Actuarial Loss 100,000

Less: Benefit Paid (2,100,000)

Closing balance 23,000,000

Particulars Amount ($)

Opening balance 19,000,000

Add: Contribution 1,000,000

less: Benefit Paid (2,100,000)

Add: Return 2,230,000

Closing balance 20,130,000

Present Value of defined benefit obligation A/C

Plan Assets A/C

Reconciliation of the following accounts:

5. Summary Journal

Date Account DR CR

31/12/2016 Current service cost A/C …………………Dr. 800,000

Interest cost A/C …………………………….Dr. 2,200,000

To Present value of defined benefit

obligation

3,000,000

31/12/2016 Actuarial Loss A/C……………………………..Dr. 100,000

To Present value of defined benefit

obligation

100,000

31/12/2016 Statement of P&L……………………………….Dr. 3,100,000

To Current service cost 800,000

To Interest cost 2,200,000

To Actuarial Loss 100,000

Page 10 of 11

The reconciliation accounts of company is shown below.

Particulars Amount ($)

Opening balance 20,000,000

Add: Current service cost 800,000

Add: Interest Cost 2,200,000

Add: Past service cost 2,000,000

Add: Actuarial Loss 100,000

Less: Benefit Paid (2,100,000)

Closing balance 23,000,000

Particulars Amount ($)

Opening balance 19,000,000

Add: Contribution 1,000,000

less: Benefit Paid (2,100,000)

Add: Return 2,230,000

Closing balance 20,130,000

Present Value of defined benefit obligation A/C

Plan Assets A/C

Reconciliation of the following accounts:

5. Summary Journal

Date Account DR CR

31/12/2016 Current service cost A/C …………………Dr. 800,000

Interest cost A/C …………………………….Dr. 2,200,000

To Present value of defined benefit

obligation

3,000,000

31/12/2016 Actuarial Loss A/C……………………………..Dr. 100,000

To Present value of defined benefit

obligation

100,000

31/12/2016 Statement of P&L……………………………….Dr. 3,100,000

To Current service cost 800,000

To Interest cost 2,200,000

To Actuarial Loss 100,000

Page 10 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Abbott, M., & Kantor, A. (2017). Fair Value Measurement and Mandated Accounting Changes: The

Case of the Victorian Rail Track Corporation. Australian accounting Review.

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4),

411-431.

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social

Science Studies, 2(2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632.

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial

statements of insurance companies. MASTER THESIS, 1-69.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law,

and Organic Documents. SSRN, 1-35.

Jones, P. (2017). Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Murray, C., & Markey Towler, B. (2017). A Theory of Return-Seeking Firms.‐ SSRN, 1-14.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

Page 11 of 11

Abbott, M., & Kantor, A. (2017). Fair Value Measurement and Mandated Accounting Changes: The

Case of the Victorian Rail Track Corporation. Australian accounting Review.

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4),

411-431.

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social

Science Studies, 2(2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), 617-632.

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial

statements of insurance companies. MASTER THESIS, 1-69.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law,

and Organic Documents. SSRN, 1-35.

Jones, P. (2017). Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Murray, C., & Markey Towler, B. (2017). A Theory of Return-Seeking Firms.‐ SSRN, 1-14.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Werner, M. (2017). Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, 25, 57-80.

Page 11 of 11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.