Financial Resource Management and Decision Making Report - Bakery

VerifiedAdded on 2019/12/28

|17

|5345

|117

Report

AI Summary

This report analyzes financial resource management and decision-making for a small bakery business. It covers various finance sources like personal savings, hire purchase, and bank loans, evaluating their implications and appropriateness. The report emphasizes the importance of financial planning, including cost analysis of different funding sources and the information needs of various stakeholders. It presents projected cash, sales, and purchase budgets, along with unit cost calculations and product pricing strategies. Additionally, the report explores project evaluation techniques such as NPV, IRR, and ARR. It concludes with an examination of financial statements, including their content, purpose, and the differences between sole trader, partnership, and company structures, supported by a financial performance analysis of Sainsbury's.

MANAGING

FINANCIAL

RESOURCES AND

DECISIONS

1AA

FINANCIAL

RESOURCES AND

DECISIONS

1AA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

AC 1.1 Types of finance sources available to the business ............................................................4

AC 1.2 Implication of above identified finance sources.................................................................5

AC 1.3 Most appropriate finance source.........................................................................................6

TASK 2.................................................................................................................................................7

AC 2.1 Importance of financial planning........................................................................................7

AC 2.2 Cost of financial sources.....................................................................................................7

AC 2.3 Information needs of users..................................................................................................7

AC 2.4 Impact of finance on financial statements...........................................................................8

TASK 3.................................................................................................................................................9

AC 3.1 Projected cash, sales and purchase budget and analyse it for the decision-making............9

AC 3.2 Calculation of unit cost and set selling price.....................................................................11

AC 3.3 Project evaluation techniques NPV, IRR, ARR and IRR..................................................12

TASK 4...............................................................................................................................................13

AC 4.1 Financial statement, content, purpose and users...............................................................13

AC 4.2 Describing and comparing financial statement of sole trader, partnership and company.13

AC 4.3 Sainsbury's financial performance analysis.......................................................................14

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................17

2AA

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

AC 1.1 Types of finance sources available to the business ............................................................4

AC 1.2 Implication of above identified finance sources.................................................................5

AC 1.3 Most appropriate finance source.........................................................................................6

TASK 2.................................................................................................................................................7

AC 2.1 Importance of financial planning........................................................................................7

AC 2.2 Cost of financial sources.....................................................................................................7

AC 2.3 Information needs of users..................................................................................................7

AC 2.4 Impact of finance on financial statements...........................................................................8

TASK 3.................................................................................................................................................9

AC 3.1 Projected cash, sales and purchase budget and analyse it for the decision-making............9

AC 3.2 Calculation of unit cost and set selling price.....................................................................11

AC 3.3 Project evaluation techniques NPV, IRR, ARR and IRR..................................................12

TASK 4...............................................................................................................................................13

AC 4.1 Financial statement, content, purpose and users...............................................................13

AC 4.2 Describing and comparing financial statement of sole trader, partnership and company.13

AC 4.3 Sainsbury's financial performance analysis.......................................................................14

CONCLUSION..................................................................................................................................15

REFERENCES...................................................................................................................................17

2AA

INTRODUCTION

In the present age of globalization, large number of companies are operating at global level.

It lead to arise fierce competition between different organization who are operating in same

industry. For the success of the business, it becomes necessary for the managers to take quicker and

efficient decisions. Financial decisions are one of the most important decisions which makes an

significant contribution to business success or failure as well. Present project report is designed to

determine ways that how small and medium sized businesses can collect funds from variety of

internal as well as external sources. The report is based on financial management through better

financial planning so that companies will not face any financial difficulties in future. Moreover, the

report will describe methods available to determine products selling prices to generate sales

revenues. It will be helpful to eliminate short-term financial requirement in a great extent. Along

with this, variety of budgets such as purchase, sales and cash budget will be prepared to assure

effective administration of funds. At the end, report will explain the content, structure and purpose

of different financial statement of various type of businesses.

TASK 1

Brief description

A medium sized bakery shop has been selected for this assignment. It will be a counter

service bakery business who will have a small commercial space to establish their counter and sell

bakery products such as pastry, breads, cakes and other baked foods over the counter.

AC 1.1 Types of finance sources available to the business

Bakery entrepreneur can collect funds from following sources;

3AA

In the present age of globalization, large number of companies are operating at global level.

It lead to arise fierce competition between different organization who are operating in same

industry. For the success of the business, it becomes necessary for the managers to take quicker and

efficient decisions. Financial decisions are one of the most important decisions which makes an

significant contribution to business success or failure as well. Present project report is designed to

determine ways that how small and medium sized businesses can collect funds from variety of

internal as well as external sources. The report is based on financial management through better

financial planning so that companies will not face any financial difficulties in future. Moreover, the

report will describe methods available to determine products selling prices to generate sales

revenues. It will be helpful to eliminate short-term financial requirement in a great extent. Along

with this, variety of budgets such as purchase, sales and cash budget will be prepared to assure

effective administration of funds. At the end, report will explain the content, structure and purpose

of different financial statement of various type of businesses.

TASK 1

Brief description

A medium sized bakery shop has been selected for this assignment. It will be a counter

service bakery business who will have a small commercial space to establish their counter and sell

bakery products such as pastry, breads, cakes and other baked foods over the counter.

AC 1.1 Types of finance sources available to the business

Bakery entrepreneur can collect funds from following sources;

3AA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Personal savings: it is one of the most finest and easily available source to meet short and

medium term financial need because no legal and regulatory requirement need to be

satisfied (Tatuev and Bahturazova, 2014). Bakery entrepreneur can invest his or her personal

savings in the business and satisfy financial need as large as possible. Hire purchase: This is a better way to purchase equipments without buying it immediately.

By making payment of only the initial charges and balance in equal instalment, bakery

owner can use assets in the operations and get benefited through it. Financial support from relatives: Another source is financial help from the family members,

friends and other relatives (Deindl and Brandt, 2011). Its benefit is they provide funds

without demanding any security and available comparatively at cheaper rate from the bank

loan. Bakery owner can satisfy their medium-term requirement from financial help.

Debt source: Bakery owner can generate funds from the bank loan. It will helps to satisfy

long term funds requirement at fixed or fluctuating interest rate.

AC 1.2 Implication of above identified finance sources

Source Financial Legal Dilution of

control

Bankruptc

y

Owner's

savings

No financial

implication.

No legal

implication.

Higher the owner

contribution will

transfer higher

the control rights

to the entity.

No

bankruptcy.

4AA

medium term financial need because no legal and regulatory requirement need to be

satisfied (Tatuev and Bahturazova, 2014). Bakery entrepreneur can invest his or her personal

savings in the business and satisfy financial need as large as possible. Hire purchase: This is a better way to purchase equipments without buying it immediately.

By making payment of only the initial charges and balance in equal instalment, bakery

owner can use assets in the operations and get benefited through it. Financial support from relatives: Another source is financial help from the family members,

friends and other relatives (Deindl and Brandt, 2011). Its benefit is they provide funds

without demanding any security and available comparatively at cheaper rate from the bank

loan. Bakery owner can satisfy their medium-term requirement from financial help.

Debt source: Bakery owner can generate funds from the bank loan. It will helps to satisfy

long term funds requirement at fixed or fluctuating interest rate.

AC 1.2 Implication of above identified finance sources

Source Financial Legal Dilution of

control

Bankruptc

y

Owner's

savings

No financial

implication.

No legal

implication.

Higher the owner

contribution will

transfer higher

the control rights

to the entity.

No

bankruptcy.

4AA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

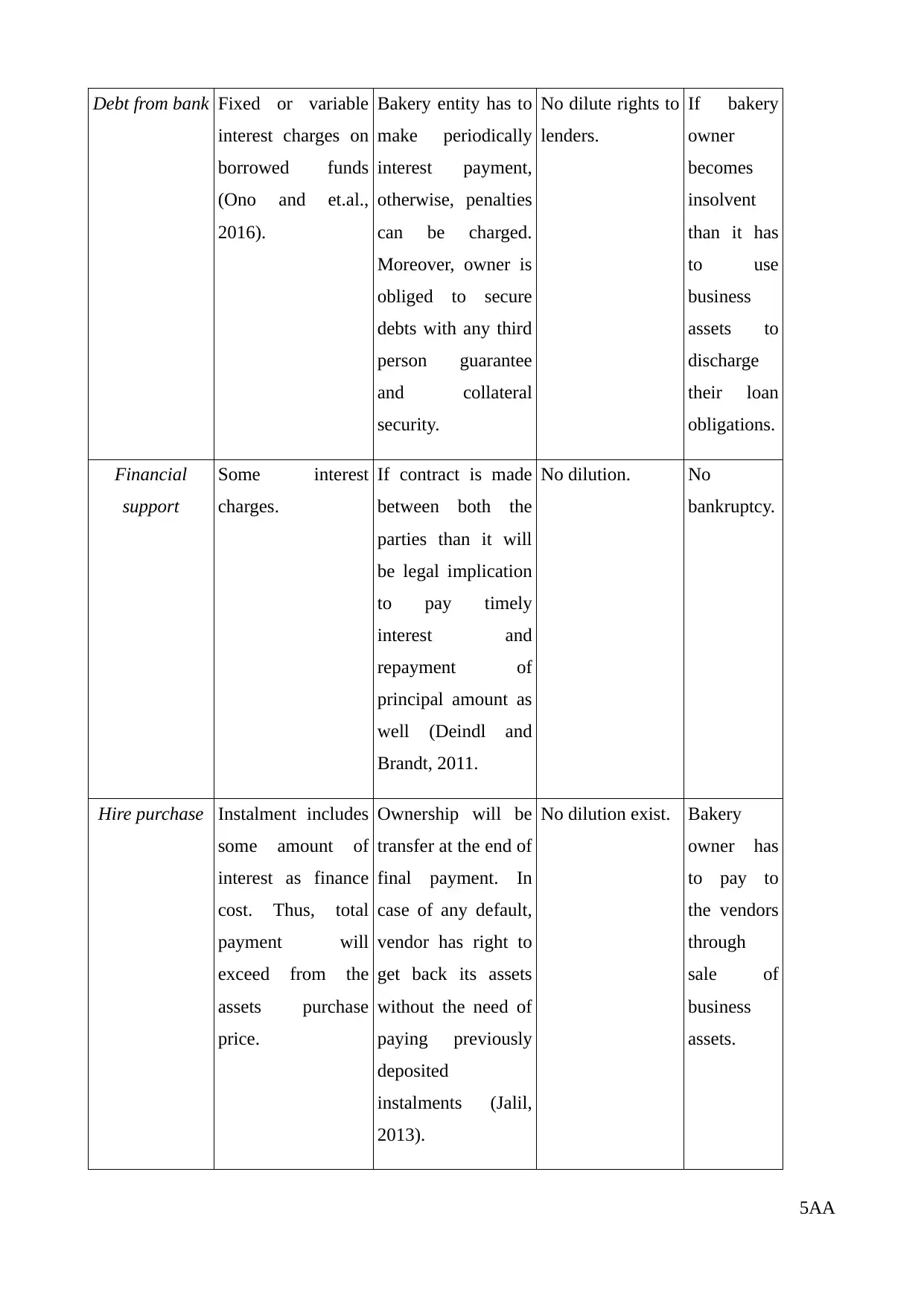

Debt from bank Fixed or variable

interest charges on

borrowed funds

(Ono and et.al.,

2016).

Bakery entity has to

make periodically

interest payment,

otherwise, penalties

can be charged.

Moreover, owner is

obliged to secure

debts with any third

person guarantee

and collateral

security.

No dilute rights to

lenders.

If bakery

owner

becomes

insolvent

than it has

to use

business

assets to

discharge

their loan

obligations.

Financial

support

Some interest

charges.

If contract is made

between both the

parties than it will

be legal implication

to pay timely

interest and

repayment of

principal amount as

well (Deindl and

Brandt, 2011.

No dilution. No

bankruptcy.

Hire purchase Instalment includes

some amount of

interest as finance

cost. Thus, total

payment will

exceed from the

assets purchase

price.

Ownership will be

transfer at the end of

final payment. In

case of any default,

vendor has right to

get back its assets

without the need of

paying previously

deposited

instalments (Jalil,

2013).

No dilution exist. Bakery

owner has

to pay to

the vendors

through

sale of

business

assets.

5AA

interest charges on

borrowed funds

(Ono and et.al.,

2016).

Bakery entity has to

make periodically

interest payment,

otherwise, penalties

can be charged.

Moreover, owner is

obliged to secure

debts with any third

person guarantee

and collateral

security.

No dilute rights to

lenders.

If bakery

owner

becomes

insolvent

than it has

to use

business

assets to

discharge

their loan

obligations.

Financial

support

Some interest

charges.

If contract is made

between both the

parties than it will

be legal implication

to pay timely

interest and

repayment of

principal amount as

well (Deindl and

Brandt, 2011.

No dilution. No

bankruptcy.

Hire purchase Instalment includes

some amount of

interest as finance

cost. Thus, total

payment will

exceed from the

assets purchase

price.

Ownership will be

transfer at the end of

final payment. In

case of any default,

vendor has right to

get back its assets

without the need of

paying previously

deposited

instalments (Jalil,

2013).

No dilution exist. Bakery

owner has

to pay to

the vendors

through

sale of

business

assets.

5AA

AC 1.3 Most appropriate finance source

Bank loan is the most appropriate source due to the following reasons:

Helpful to eliminate short, medium and long run financial need. Thus, bakery owner can use

this source to buy capital assets such as commercial space for the establishing counter in

UK.

Does not diversify controlling rights to the banks (Plumlee and et.al., 2015).

Fixed as well as fluctuate interest payment are deductible expenses which results in

declining tax obligations.

Instalment can be paid by generating revenues from the sales operations hence, it will be

more suitable and feasible.

Hire purchase will be good source to buy appliances such as ovens and fridges because

entity has to pay some charges as down payment and balance in instalment which will be paid at

fixed interval of time.

TASK 2

AC 2.1 Importance of financial planning

Advance or prior business plan to ensure adequate fund availability at every point of time is

called financial planning. Its main objective is to mitigate potential financial threats or problems

that can be arise due to competitive and changing environment.

It helps bakery owner to determine their start-up costs and satisfy it by most appropriate

sources at least cost.

It helps to ensure effective utilization of all the monetary sources so that business will not

face any difficulties due to lack of funds (Lewis, 2012).

It helps to determine shortfall or surplus availability of funds. Thus, in case of deficit,

bakery management can design policies and take decisions to overcome from such shortfall.

Bakery owner will need to purchase equipments and appliances such as ovens and

refrigerators. Effective financial plan will helps to acquire required funds timely so that

business can run without any hazards.

It will helps to take financial decisions by optimum utilization of funds according to set

priorities. So that, owner can manage their costs and earn high profitability as well.

Thus, it can be said that financial planning is the insurance of bakery business's financial security

results in hazard free functioning.

6AA

Bank loan is the most appropriate source due to the following reasons:

Helpful to eliminate short, medium and long run financial need. Thus, bakery owner can use

this source to buy capital assets such as commercial space for the establishing counter in

UK.

Does not diversify controlling rights to the banks (Plumlee and et.al., 2015).

Fixed as well as fluctuate interest payment are deductible expenses which results in

declining tax obligations.

Instalment can be paid by generating revenues from the sales operations hence, it will be

more suitable and feasible.

Hire purchase will be good source to buy appliances such as ovens and fridges because

entity has to pay some charges as down payment and balance in instalment which will be paid at

fixed interval of time.

TASK 2

AC 2.1 Importance of financial planning

Advance or prior business plan to ensure adequate fund availability at every point of time is

called financial planning. Its main objective is to mitigate potential financial threats or problems

that can be arise due to competitive and changing environment.

It helps bakery owner to determine their start-up costs and satisfy it by most appropriate

sources at least cost.

It helps to ensure effective utilization of all the monetary sources so that business will not

face any difficulties due to lack of funds (Lewis, 2012).

It helps to determine shortfall or surplus availability of funds. Thus, in case of deficit,

bakery management can design policies and take decisions to overcome from such shortfall.

Bakery owner will need to purchase equipments and appliances such as ovens and

refrigerators. Effective financial plan will helps to acquire required funds timely so that

business can run without any hazards.

It will helps to take financial decisions by optimum utilization of funds according to set

priorities. So that, owner can manage their costs and earn high profitability as well.

Thus, it can be said that financial planning is the insurance of bakery business's financial security

results in hazard free functioning.

6AA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC 2.2 Cost of financial sources

Finance source Costs

Savings Opportunity costs exists in personal savings. It refers to the loss of return

which owner can earn by investing his or her savings in alternative

opportunity (Tam and Dholakia, 2011).

Debt through bank As already said, fixed or variable interest payment is the costs of borrowed

funds through banks (Yen and et.al., 2015).

Hire purchase Periodical instalment involve some amount of interest as the cost of hire

purchase system.

Financial support Relatives, friends and family members provide funds at less interest charges

compare to the market rate which is known as its costs.

AC 2.3 Information needs of users

There are varied range of users who have any kind of direct and indirect relationship in the

business performance. Lenders require information about business capital risk, profit margin and

cash flow capacity so that they can secure their funds. Shareholders need information about profit

performance, dividend growth and potential earnings so that they can fulfil their investment

objective of high return. Creditors desires to know liquidity status so that they can analysis that firm

has enough resources or not to pay off them timely (Meltzer and et.al., 2011). While, employees are

interested to earn high salary and other benefits such as appraisal awards, So that, they require

information about profitability performance because only high profit earnings organizations can pay

more to their employees.

Another, managers are responsible to manage core business functioning therefore, they need

information about each and every aspects which assist in performance analysis. They will need to

know profit, liquidity, solvency, efficiency and cash generating ability. So that, they can make

effective and strategic decisions and frame policies which will aid to future performance. Further,

government desires to know profit and determine tax liabilities (Needs of users of financial

information, 2009). Moreover, they examine that all the business functioning are conducting

ethically and legally or not. They make policies to business as well a industrial growth which makes

an significant contribution to the economic development in form of GDP. Public are more interested

that business will fulfilling their environmental responsibility and give respect to all the culture.

Customer desires to purchase different type of products at different prices and quality as well.

7AA

Finance source Costs

Savings Opportunity costs exists in personal savings. It refers to the loss of return

which owner can earn by investing his or her savings in alternative

opportunity (Tam and Dholakia, 2011).

Debt through bank As already said, fixed or variable interest payment is the costs of borrowed

funds through banks (Yen and et.al., 2015).

Hire purchase Periodical instalment involve some amount of interest as the cost of hire

purchase system.

Financial support Relatives, friends and family members provide funds at less interest charges

compare to the market rate which is known as its costs.

AC 2.3 Information needs of users

There are varied range of users who have any kind of direct and indirect relationship in the

business performance. Lenders require information about business capital risk, profit margin and

cash flow capacity so that they can secure their funds. Shareholders need information about profit

performance, dividend growth and potential earnings so that they can fulfil their investment

objective of high return. Creditors desires to know liquidity status so that they can analysis that firm

has enough resources or not to pay off them timely (Meltzer and et.al., 2011). While, employees are

interested to earn high salary and other benefits such as appraisal awards, So that, they require

information about profitability performance because only high profit earnings organizations can pay

more to their employees.

Another, managers are responsible to manage core business functioning therefore, they need

information about each and every aspects which assist in performance analysis. They will need to

know profit, liquidity, solvency, efficiency and cash generating ability. So that, they can make

effective and strategic decisions and frame policies which will aid to future performance. Further,

government desires to know profit and determine tax liabilities (Needs of users of financial

information, 2009). Moreover, they examine that all the business functioning are conducting

ethically and legally or not. They make policies to business as well a industrial growth which makes

an significant contribution to the economic development in form of GDP. Public are more interested

that business will fulfilling their environmental responsibility and give respect to all the culture.

Customer desires to purchase different type of products at different prices and quality as well.

7AA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC 2.4 Impact of finance on financial statements

Owner's capital employed: It will be disclose in the liability side of balance sheet and

enhance cash availability in the assets side (Tatuev and Bahturazova, 2014).

Borrowed funds: It will be disclose in the liabilities side of B/S under the head non-current

liabilities and will be added in cash balance of current assets.

Hire purchase: Initial payment will be subtracted from the cash balance and shows as

revenue expenditures in the profitability statement. On contrary, assets will be shows as fixed assets

in the B/S.

Instalment payment: Instalment of hire purchase and bank loan will be reported as

expenditures in the profitability statement. However, in B/S, it will be deducted from the closing

cash balance. Moreover, loan instalment will be subtracted from the borrowed funds under the non-

current liabilities head.

Principal payment: It will be deducted from the respective debt funds and necessarily

deducted from the cash position in B/S.

In addition to this, Bakery's operating functions will drive funds in the business and helps to

mitigate short-term financing. For instance, sales will contribute to increase revenue and will be

reported as income in profit and loss a/c while, collection of money will be included in cash balance

of the business. On contrary to this, expenditures will results in decline cash funds hence, will be

recognised as spendings in profit and loss a/c and deducted from the cash balance as well.

TASK 3

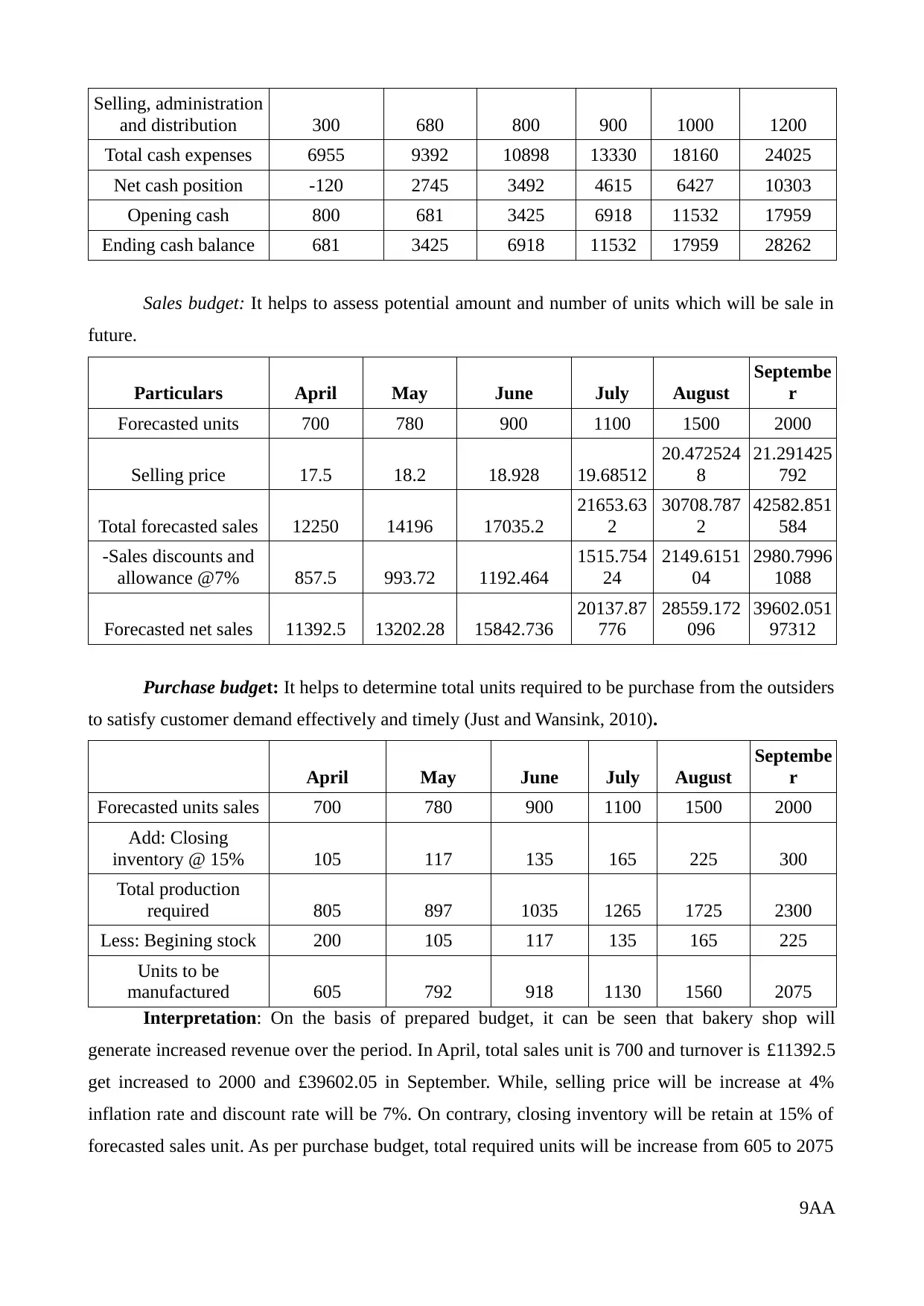

AC 3.1 Projected cash, sales and purchase budget and analyse it for the decision-making

Cash budget: It is the projection of all the cash incomes and expenditures helps to determine

net cash flow and closing cash balance (Just and Wansink, 2010).

Particulars April May June July August September

Cash income

Cash sales 6836 7921 9506 12083 17136 23761

Accounts for sale 4215 4885 5862 7451 10567

Total cash income 6836 12137 14390 17945 24587 34328

Cash application

Direct material

purchase 3630 4752 5508 6780 9360 12450

Direct labour 1815 2376 2754 3390 4680 6225

Manufacturing

overhead 1210 1584 1836 2260 3120 4150

8AA

Owner's capital employed: It will be disclose in the liability side of balance sheet and

enhance cash availability in the assets side (Tatuev and Bahturazova, 2014).

Borrowed funds: It will be disclose in the liabilities side of B/S under the head non-current

liabilities and will be added in cash balance of current assets.

Hire purchase: Initial payment will be subtracted from the cash balance and shows as

revenue expenditures in the profitability statement. On contrary, assets will be shows as fixed assets

in the B/S.

Instalment payment: Instalment of hire purchase and bank loan will be reported as

expenditures in the profitability statement. However, in B/S, it will be deducted from the closing

cash balance. Moreover, loan instalment will be subtracted from the borrowed funds under the non-

current liabilities head.

Principal payment: It will be deducted from the respective debt funds and necessarily

deducted from the cash position in B/S.

In addition to this, Bakery's operating functions will drive funds in the business and helps to

mitigate short-term financing. For instance, sales will contribute to increase revenue and will be

reported as income in profit and loss a/c while, collection of money will be included in cash balance

of the business. On contrary to this, expenditures will results in decline cash funds hence, will be

recognised as spendings in profit and loss a/c and deducted from the cash balance as well.

TASK 3

AC 3.1 Projected cash, sales and purchase budget and analyse it for the decision-making

Cash budget: It is the projection of all the cash incomes and expenditures helps to determine

net cash flow and closing cash balance (Just and Wansink, 2010).

Particulars April May June July August September

Cash income

Cash sales 6836 7921 9506 12083 17136 23761

Accounts for sale 4215 4885 5862 7451 10567

Total cash income 6836 12137 14390 17945 24587 34328

Cash application

Direct material

purchase 3630 4752 5508 6780 9360 12450

Direct labour 1815 2376 2754 3390 4680 6225

Manufacturing

overhead 1210 1584 1836 2260 3120 4150

8AA

Selling, administration

and distribution 300 680 800 900 1000 1200

Total cash expenses 6955 9392 10898 13330 18160 24025

Net cash position -120 2745 3492 4615 6427 10303

Opening cash 800 681 3425 6918 11532 17959

Ending cash balance 681 3425 6918 11532 17959 28262

Sales budget: It helps to assess potential amount and number of units which will be sale in

future.

Particulars April May June July August

Septembe

r

Forecasted units 700 780 900 1100 1500 2000

Selling price 17.5 18.2 18.928 19.68512

20.472524

8

21.291425

792

Total forecasted sales 12250 14196 17035.2

21653.63

2

30708.787

2

42582.851

584

-Sales discounts and

allowance @7% 857.5 993.72 1192.464

1515.754

24

2149.6151

04

2980.7996

1088

Forecasted net sales 11392.5 13202.28 15842.736

20137.87

776

28559.172

096

39602.051

97312

Purchase budget: It helps to determine total units required to be purchase from the outsiders

to satisfy customer demand effectively and timely (Just and Wansink, 2010).

April May June July August

Septembe

r

Forecasted units sales 700 780 900 1100 1500 2000

Add: Closing

inventory @ 15% 105 117 135 165 225 300

Total production

required 805 897 1035 1265 1725 2300

Less: Begining stock 200 105 117 135 165 225

Units to be

manufactured 605 792 918 1130 1560 2075

Interpretation: On the basis of prepared budget, it can be seen that bakery shop will

generate increased revenue over the period. In April, total sales unit is 700 and turnover is £11392.5

get increased to 2000 and £39602.05 in September. While, selling price will be increase at 4%

inflation rate and discount rate will be 7%. On contrary, closing inventory will be retain at 15% of

forecasted sales unit. As per purchase budget, total required units will be increase from 605 to 2075

9AA

and distribution 300 680 800 900 1000 1200

Total cash expenses 6955 9392 10898 13330 18160 24025

Net cash position -120 2745 3492 4615 6427 10303

Opening cash 800 681 3425 6918 11532 17959

Ending cash balance 681 3425 6918 11532 17959 28262

Sales budget: It helps to assess potential amount and number of units which will be sale in

future.

Particulars April May June July August

Septembe

r

Forecasted units 700 780 900 1100 1500 2000

Selling price 17.5 18.2 18.928 19.68512

20.472524

8

21.291425

792

Total forecasted sales 12250 14196 17035.2

21653.63

2

30708.787

2

42582.851

584

-Sales discounts and

allowance @7% 857.5 993.72 1192.464

1515.754

24

2149.6151

04

2980.7996

1088

Forecasted net sales 11392.5 13202.28 15842.736

20137.87

776

28559.172

096

39602.051

97312

Purchase budget: It helps to determine total units required to be purchase from the outsiders

to satisfy customer demand effectively and timely (Just and Wansink, 2010).

April May June July August

Septembe

r

Forecasted units sales 700 780 900 1100 1500 2000

Add: Closing

inventory @ 15% 105 117 135 165 225 300

Total production

required 805 897 1035 1265 1725 2300

Less: Begining stock 200 105 117 135 165 225

Units to be

manufactured 605 792 918 1130 1560 2075

Interpretation: On the basis of prepared budget, it can be seen that bakery shop will

generate increased revenue over the period. In April, total sales unit is 700 and turnover is £11392.5

get increased to 2000 and £39602.05 in September. While, selling price will be increase at 4%

inflation rate and discount rate will be 7%. On contrary, closing inventory will be retain at 15% of

forecasted sales unit. As per purchase budget, total required units will be increase from 605 to 2075

9AA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

at the end of September.

Cash budget presents that Bakery shop will make 60% sales in cash and 40% on credit in

which 3% will be irrecoverable. Credit sales will be for one month hence, bakery shop will receive

it in next month. Whereas, material buying rate is £6, labour rate is £3 and manufacturing overhead

will incur at £2 per unit. On the other hand, selling, office and distribution expenses will be increase

from £300 to £1200. This in turn, total cash uses will be improve from £6955 to £24025. However,

ending cash balance will be increase from £681 to £28262 respectively.

Suggestion:

Bakery owner has to find out some supplier who will provide material at cheaper rate.

Food makers will be efficient in their work so that tasty and delicious baked food can be

prepared helps to enlarge turnover and profitability as well (Lawrence, 2008).

Control expenses through cut off unnecessary costs such as switching off lights and

recycling and reuse scrap such as oil.

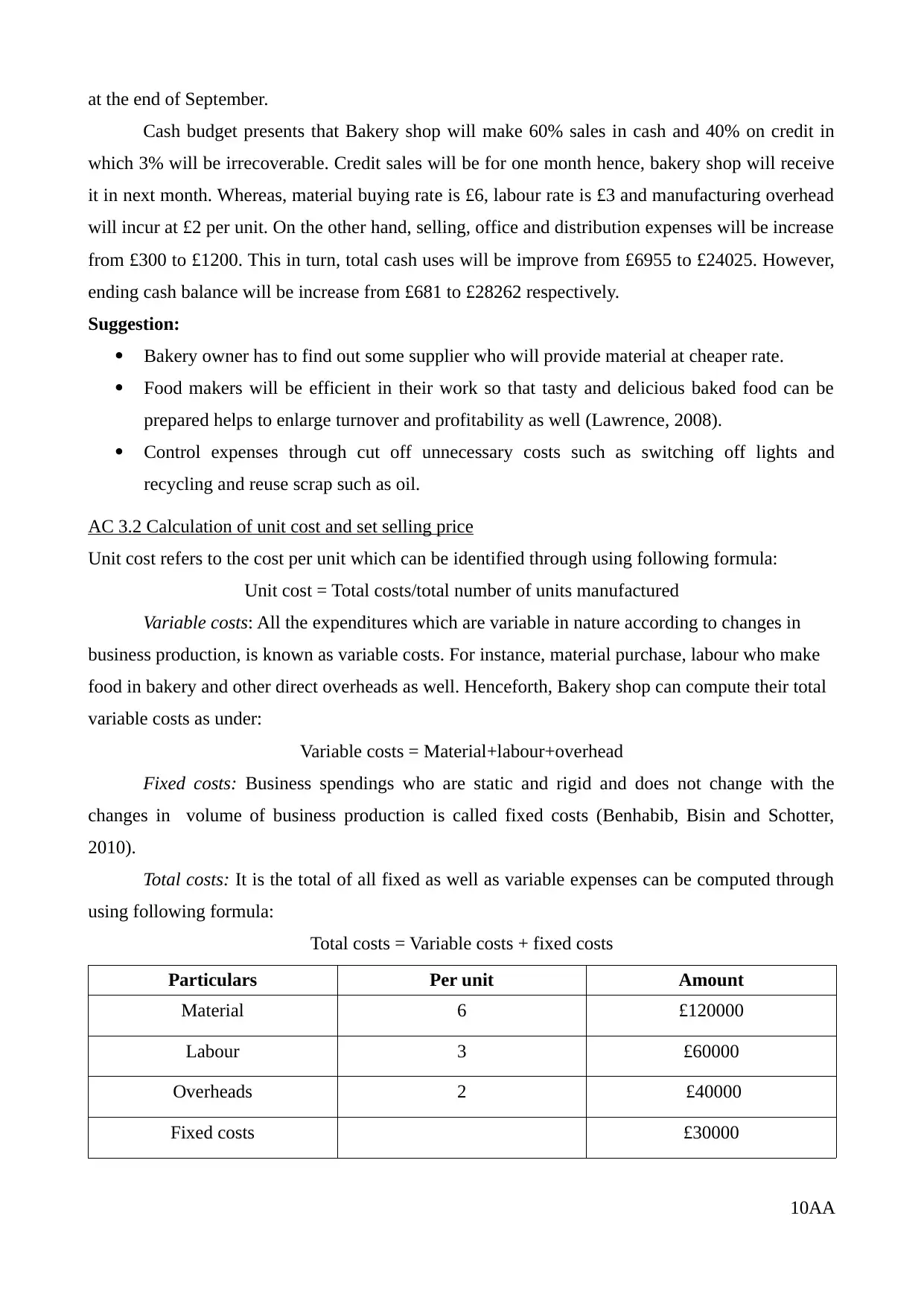

AC 3.2 Calculation of unit cost and set selling price

Unit cost refers to the cost per unit which can be identified through using following formula:

Unit cost = Total costs/total number of units manufactured

Variable costs: All the expenditures which are variable in nature according to changes in

business production, is known as variable costs. For instance, material purchase, labour who make

food in bakery and other direct overheads as well. Henceforth, Bakery shop can compute their total

variable costs as under:

Variable costs = Material+labour+overhead

Fixed costs: Business spendings who are static and rigid and does not change with the

changes in volume of business production is called fixed costs (Benhabib, Bisin and Schotter,

2010).

Total costs: It is the total of all fixed as well as variable expenses can be computed through

using following formula:

Total costs = Variable costs + fixed costs

Particulars Per unit Amount

Material 6 £120000

Labour 3 £60000

Overheads 2 £40000

Fixed costs £30000

10AA

Cash budget presents that Bakery shop will make 60% sales in cash and 40% on credit in

which 3% will be irrecoverable. Credit sales will be for one month hence, bakery shop will receive

it in next month. Whereas, material buying rate is £6, labour rate is £3 and manufacturing overhead

will incur at £2 per unit. On the other hand, selling, office and distribution expenses will be increase

from £300 to £1200. This in turn, total cash uses will be improve from £6955 to £24025. However,

ending cash balance will be increase from £681 to £28262 respectively.

Suggestion:

Bakery owner has to find out some supplier who will provide material at cheaper rate.

Food makers will be efficient in their work so that tasty and delicious baked food can be

prepared helps to enlarge turnover and profitability as well (Lawrence, 2008).

Control expenses through cut off unnecessary costs such as switching off lights and

recycling and reuse scrap such as oil.

AC 3.2 Calculation of unit cost and set selling price

Unit cost refers to the cost per unit which can be identified through using following formula:

Unit cost = Total costs/total number of units manufactured

Variable costs: All the expenditures which are variable in nature according to changes in

business production, is known as variable costs. For instance, material purchase, labour who make

food in bakery and other direct overheads as well. Henceforth, Bakery shop can compute their total

variable costs as under:

Variable costs = Material+labour+overhead

Fixed costs: Business spendings who are static and rigid and does not change with the

changes in volume of business production is called fixed costs (Benhabib, Bisin and Schotter,

2010).

Total costs: It is the total of all fixed as well as variable expenses can be computed through

using following formula:

Total costs = Variable costs + fixed costs

Particulars Per unit Amount

Material 6 £120000

Labour 3 £60000

Overheads 2 £40000

Fixed costs £30000

10AA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total costs £250000

Units produced £20000

Unit costs (£250000/20000 units) £12.5

Pricing decision: Target return pricing is an effective method to set prices for the bakery

items (Bonini and et.al., 2010). For instance, at the target return of 40%, bakery owner can set

prices as under:

Price = Unit costs + target return

= £12.5 + (40% of £12.5)

= £12.5+5 = £17.5

At this price, bakery shop can achieve its break even point at below mentioned level:

BEP (In units) = £30000/(£17.5-11)

£30000/£6.5

= 4615(Approx)

BEP ( In £) = 4615*£17.5 = £80762.5

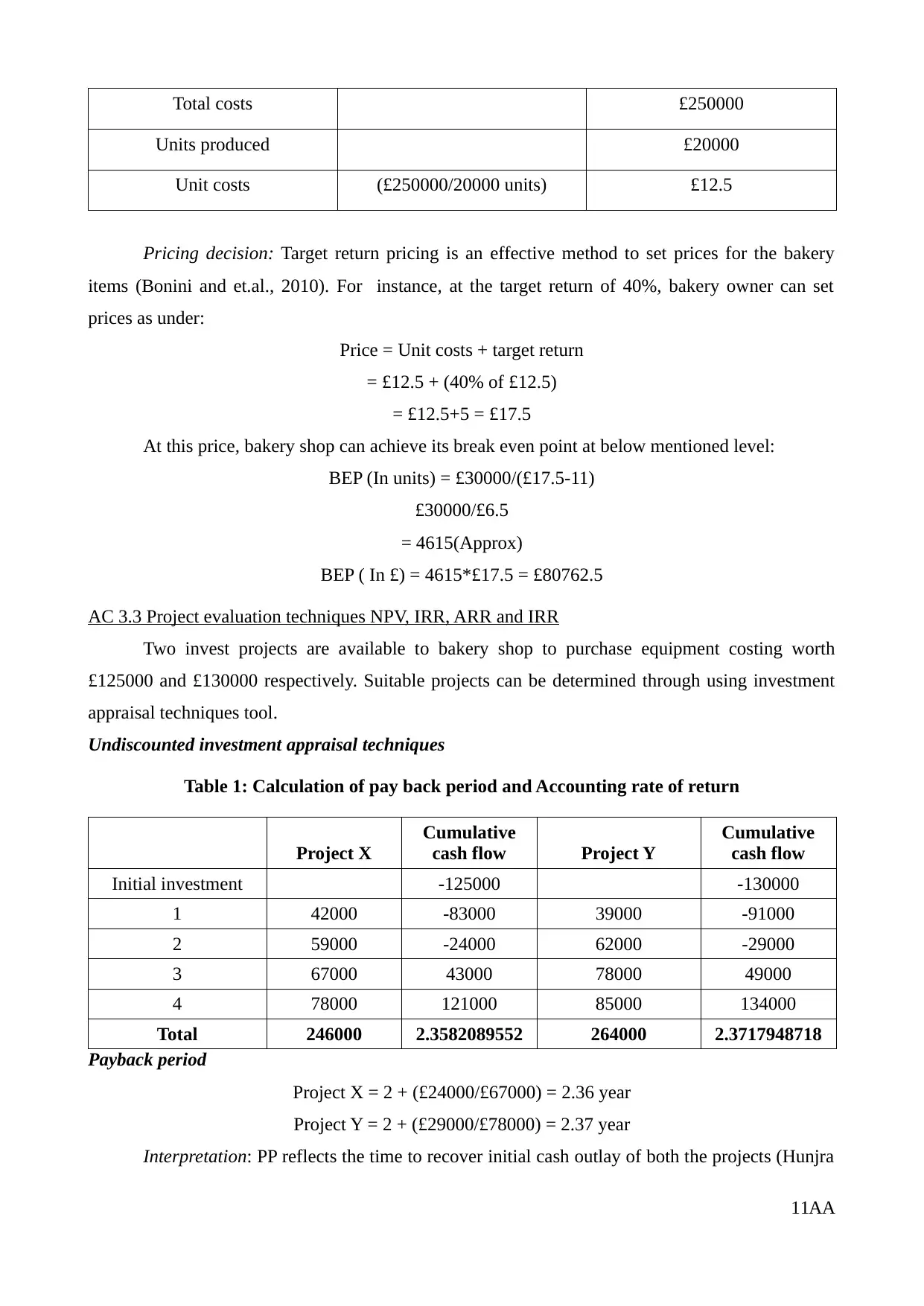

AC 3.3 Project evaluation techniques NPV, IRR, ARR and IRR

Two invest projects are available to bakery shop to purchase equipment costing worth

£125000 and £130000 respectively. Suitable projects can be determined through using investment

appraisal techniques tool.

Undiscounted investment appraisal techniques

Table 1: Calculation of pay back period and Accounting rate of return

Project X

Cumulative

cash flow Project Y

Cumulative

cash flow

Initial investment -125000 -130000

1 42000 -83000 39000 -91000

2 59000 -24000 62000 -29000

3 67000 43000 78000 49000

4 78000 121000 85000 134000

Total 246000 2.3582089552 264000 2.3717948718

Payback period

Project X = 2 + (£24000/£67000) = 2.36 year

Project Y = 2 + (£29000/£78000) = 2.37 year

Interpretation: PP reflects the time to recover initial cash outlay of both the projects (Hunjra

11AA

Units produced £20000

Unit costs (£250000/20000 units) £12.5

Pricing decision: Target return pricing is an effective method to set prices for the bakery

items (Bonini and et.al., 2010). For instance, at the target return of 40%, bakery owner can set

prices as under:

Price = Unit costs + target return

= £12.5 + (40% of £12.5)

= £12.5+5 = £17.5

At this price, bakery shop can achieve its break even point at below mentioned level:

BEP (In units) = £30000/(£17.5-11)

£30000/£6.5

= 4615(Approx)

BEP ( In £) = 4615*£17.5 = £80762.5

AC 3.3 Project evaluation techniques NPV, IRR, ARR and IRR

Two invest projects are available to bakery shop to purchase equipment costing worth

£125000 and £130000 respectively. Suitable projects can be determined through using investment

appraisal techniques tool.

Undiscounted investment appraisal techniques

Table 1: Calculation of pay back period and Accounting rate of return

Project X

Cumulative

cash flow Project Y

Cumulative

cash flow

Initial investment -125000 -130000

1 42000 -83000 39000 -91000

2 59000 -24000 62000 -29000

3 67000 43000 78000 49000

4 78000 121000 85000 134000

Total 246000 2.3582089552 264000 2.3717948718

Payback period

Project X = 2 + (£24000/£67000) = 2.36 year

Project Y = 2 + (£29000/£78000) = 2.37 year

Interpretation: PP reflects the time to recover initial cash outlay of both the projects (Hunjra

11AA

and et.al., 2012). In both the projects, PP indicates very little difference as it is 2.36 and 2.37

respectively. But still, less time by 0.01 year indicates that project X will reearn its project costs in

earlier period.

Accounting rate of return:

Project X = (£246000/4)/£125000*100 = £49.2%

Project Y = (£264000/4)/(£130000)*100 = £50.77%

Interpretation: ARR reflects the return or profit percentage from the investment projects. In

Project X, it is 49.2% while in project Y, it is 50.77%. High profit percentage by 1.57% entails that

bakery owner should invest in project Y.

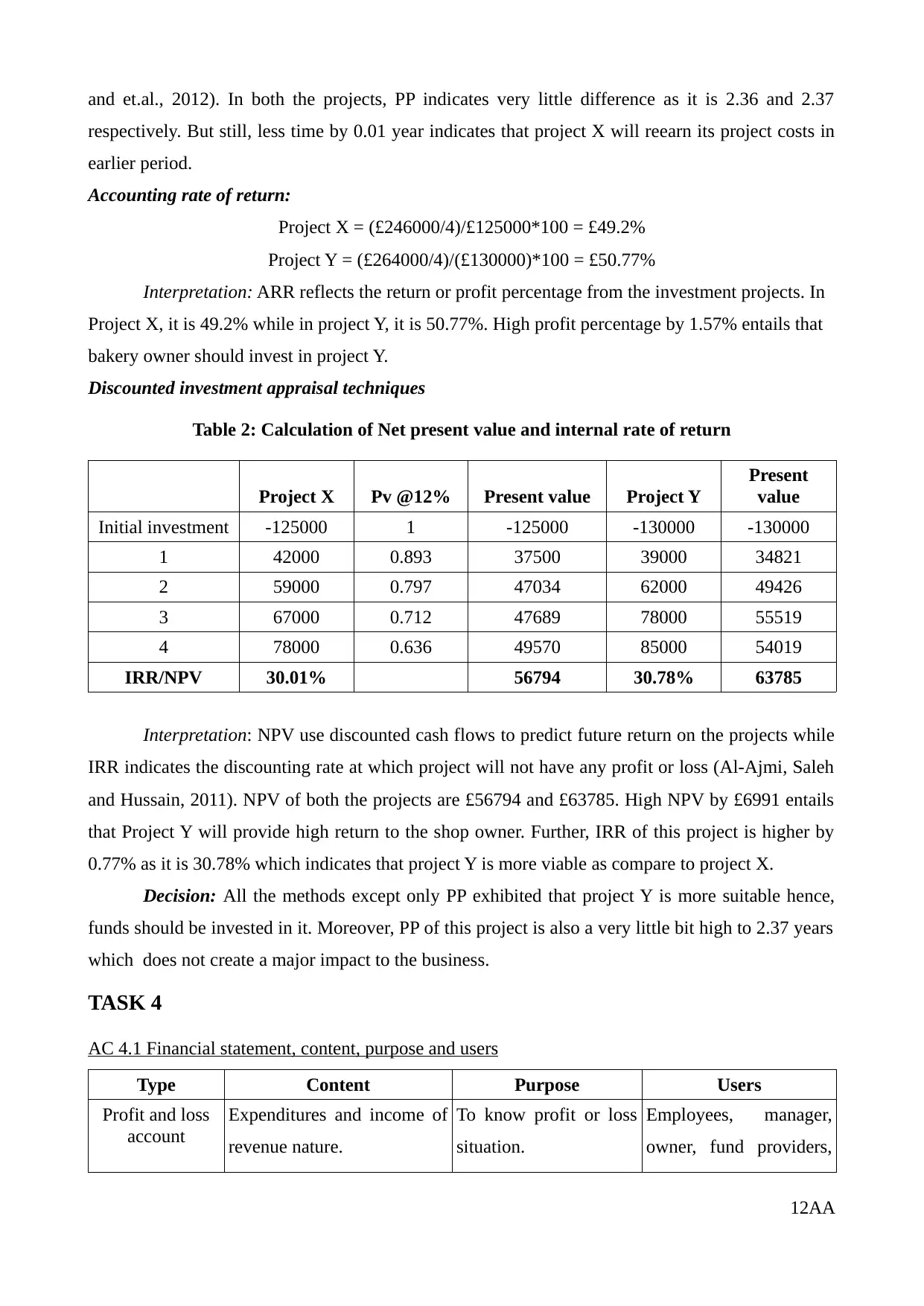

Discounted investment appraisal techniques

Table 2: Calculation of Net present value and internal rate of return

Project X Pv @12% Present value Project Y

Present

value

Initial investment -125000 1 -125000 -130000 -130000

1 42000 0.893 37500 39000 34821

2 59000 0.797 47034 62000 49426

3 67000 0.712 47689 78000 55519

4 78000 0.636 49570 85000 54019

IRR/NPV 30.01% 56794 30.78% 63785

Interpretation: NPV use discounted cash flows to predict future return on the projects while

IRR indicates the discounting rate at which project will not have any profit or loss (Al-Ajmi, Saleh

and Hussain, 2011). NPV of both the projects are £56794 and £63785. High NPV by £6991 entails

that Project Y will provide high return to the shop owner. Further, IRR of this project is higher by

0.77% as it is 30.78% which indicates that project Y is more viable as compare to project X.

Decision: All the methods except only PP exhibited that project Y is more suitable hence,

funds should be invested in it. Moreover, PP of this project is also a very little bit high to 2.37 years

which does not create a major impact to the business.

TASK 4

AC 4.1 Financial statement, content, purpose and users

Type Content Purpose Users

Profit and loss

account

Expenditures and income of

revenue nature.

To know profit or loss

situation.

Employees, manager,

owner, fund providers,

12AA

respectively. But still, less time by 0.01 year indicates that project X will reearn its project costs in

earlier period.

Accounting rate of return:

Project X = (£246000/4)/£125000*100 = £49.2%

Project Y = (£264000/4)/(£130000)*100 = £50.77%

Interpretation: ARR reflects the return or profit percentage from the investment projects. In

Project X, it is 49.2% while in project Y, it is 50.77%. High profit percentage by 1.57% entails that

bakery owner should invest in project Y.

Discounted investment appraisal techniques

Table 2: Calculation of Net present value and internal rate of return

Project X Pv @12% Present value Project Y

Present

value

Initial investment -125000 1 -125000 -130000 -130000

1 42000 0.893 37500 39000 34821

2 59000 0.797 47034 62000 49426

3 67000 0.712 47689 78000 55519

4 78000 0.636 49570 85000 54019

IRR/NPV 30.01% 56794 30.78% 63785

Interpretation: NPV use discounted cash flows to predict future return on the projects while

IRR indicates the discounting rate at which project will not have any profit or loss (Al-Ajmi, Saleh

and Hussain, 2011). NPV of both the projects are £56794 and £63785. High NPV by £6991 entails

that Project Y will provide high return to the shop owner. Further, IRR of this project is higher by

0.77% as it is 30.78% which indicates that project Y is more viable as compare to project X.

Decision: All the methods except only PP exhibited that project Y is more suitable hence,

funds should be invested in it. Moreover, PP of this project is also a very little bit high to 2.37 years

which does not create a major impact to the business.

TASK 4

AC 4.1 Financial statement, content, purpose and users

Type Content Purpose Users

Profit and loss

account

Expenditures and income of

revenue nature.

To know profit or loss

situation.

Employees, manager,

owner, fund providers,

12AA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.