Managing Financial Resources Report

VerifiedAdded on 2019/12/03

|19

|4535

|150

Report

AI Summary

This report comprehensively explores managing financial resources and decisions within a business context. It covers various sources of finance (retained earnings, issuing shares, bank loans), their implications, and associated costs. The report emphasizes the importance of financial planning and its role in decision-making. It delves into the financial information requirements for different stakeholders and how costs are reflected in financial statements (income statement, cash flow statement, balance sheet). Investment appraisal methods (payback period, ARR, NPV, IRR) are applied to evaluate investment proposals. The report also includes calculations of contribution, break-even point, and profitability, analyzing the impact of varying costs and sales discounts. Finally, it examines the purpose and use of different accounting records and analyzes financial statements using profitability, liquidity, and efficiency ratios to assess the overall financial health of a business.

MANAGING FINANCIAL RESOURCES

AND DECISIONS

AND DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction................................................................................................................................................1

Task 1.........................................................................................................................................................1

1.1 Sources of Finance...........................................................................................................................1

1.2 Implications of sources....................................................................................................................2

1.3 Source of finance for three different cases.......................................................................................2

Task 2.........................................................................................................................................................3

2.1 Costs associated with different sources...........................................................................................3

2.2 Importance of financial planning.....................................................................................................4

AC 2.3 Financial information requirement for decision making purposes............................................4

AC 2.4 Cost of financial statements showing in financial statements...................................................4

TASK 3......................................................................................................................................................5

AC 3.1 Evaluation of sales budget and cash flow statement.................................................................5

AC 3.3 Application of investment appraisal methods...........................................................................6

AC 3.2 Calculation of Contribution, breakeven point and profitability................................................8

Task 4.......................................................................................................................................................13

AC 4.1 Purpose and use of different accounting records.....................................................................13

AC 4.2 Purpose of the financial statements.........................................................................................13

AC 4.3 Analysis of the financial statements........................................................................................14

Conclusion...............................................................................................................................................15

References................................................................................................................................................16

Introduction................................................................................................................................................1

Task 1.........................................................................................................................................................1

1.1 Sources of Finance...........................................................................................................................1

1.2 Implications of sources....................................................................................................................2

1.3 Source of finance for three different cases.......................................................................................2

Task 2.........................................................................................................................................................3

2.1 Costs associated with different sources...........................................................................................3

2.2 Importance of financial planning.....................................................................................................4

AC 2.3 Financial information requirement for decision making purposes............................................4

AC 2.4 Cost of financial statements showing in financial statements...................................................4

TASK 3......................................................................................................................................................5

AC 3.1 Evaluation of sales budget and cash flow statement.................................................................5

AC 3.3 Application of investment appraisal methods...........................................................................6

AC 3.2 Calculation of Contribution, breakeven point and profitability................................................8

Task 4.......................................................................................................................................................13

AC 4.1 Purpose and use of different accounting records.....................................................................13

AC 4.2 Purpose of the financial statements.........................................................................................13

AC 4.3 Analysis of the financial statements........................................................................................14

Conclusion...............................................................................................................................................15

References................................................................................................................................................16

INTRODUCTION

Looking at the present condition of corporate market and economic conditions of UK, it is

essential for the companies operating in it to manage and control their financial resources in effective

and efficient manner so that they can attain long term growth and sustainability (Drake and Fabozzi,

2012). In the present study, researcher focuses on evaluating varied sources of finance and their

implications so that smart decision can be made regarding selection of appropriate source. Furthermore,

various financial tools and techniques have been used to evaluate actual position of the company and

accordingly recommending the suitable strategies and tactics for the future growth and success.

TASK 1

1.1 Sources of Finance

There are several sources of finance available to the businesses of different level which can be

used for the expansion of business operations. Furthermore, in order to buy up an organisation or

establishing business in new market it is important for the management to ensure adequate amount of

funding. Following are the sources of funds available to the business: Retained earnings: These are the funds that are kept reserved after distributing the profits to

investors, shareholders etc. The main purpose of using this source is that by the means of this

company does not raise any liabilities (Gibson, 2008). But contrary to this, management has to

make sure that company make optimum utilisation these funds otherwise it may be considered

as loss for the firm. Issue of share: Through the means of issuing shares company may generate large amount of

money. However, these are considered as the most common method of financing. There are two

methods through the help of firm can generate funds IPO and FPO (Mao, 2012). The main

advantage of this source is that company does not have to repay the principle amount. While

management has to make sure that dividend is given to each shareholder for the long term

relationship.

Bank loan: Bank borrowing is considered as the most common method of raising the funds

from external sources. However, the main aim of this source is that company can raise large

amount by completing few legal formalities. The major drawback of this source is that, firm has

to pay monthly instalment of interest which can affect the working capital of business.

1

Looking at the present condition of corporate market and economic conditions of UK, it is

essential for the companies operating in it to manage and control their financial resources in effective

and efficient manner so that they can attain long term growth and sustainability (Drake and Fabozzi,

2012). In the present study, researcher focuses on evaluating varied sources of finance and their

implications so that smart decision can be made regarding selection of appropriate source. Furthermore,

various financial tools and techniques have been used to evaluate actual position of the company and

accordingly recommending the suitable strategies and tactics for the future growth and success.

TASK 1

1.1 Sources of Finance

There are several sources of finance available to the businesses of different level which can be

used for the expansion of business operations. Furthermore, in order to buy up an organisation or

establishing business in new market it is important for the management to ensure adequate amount of

funding. Following are the sources of funds available to the business: Retained earnings: These are the funds that are kept reserved after distributing the profits to

investors, shareholders etc. The main purpose of using this source is that by the means of this

company does not raise any liabilities (Gibson, 2008). But contrary to this, management has to

make sure that company make optimum utilisation these funds otherwise it may be considered

as loss for the firm. Issue of share: Through the means of issuing shares company may generate large amount of

money. However, these are considered as the most common method of financing. There are two

methods through the help of firm can generate funds IPO and FPO (Mao, 2012). The main

advantage of this source is that company does not have to repay the principle amount. While

management has to make sure that dividend is given to each shareholder for the long term

relationship.

Bank loan: Bank borrowing is considered as the most common method of raising the funds

from external sources. However, the main aim of this source is that company can raise large

amount by completing few legal formalities. The major drawback of this source is that, firm has

to pay monthly instalment of interest which can affect the working capital of business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

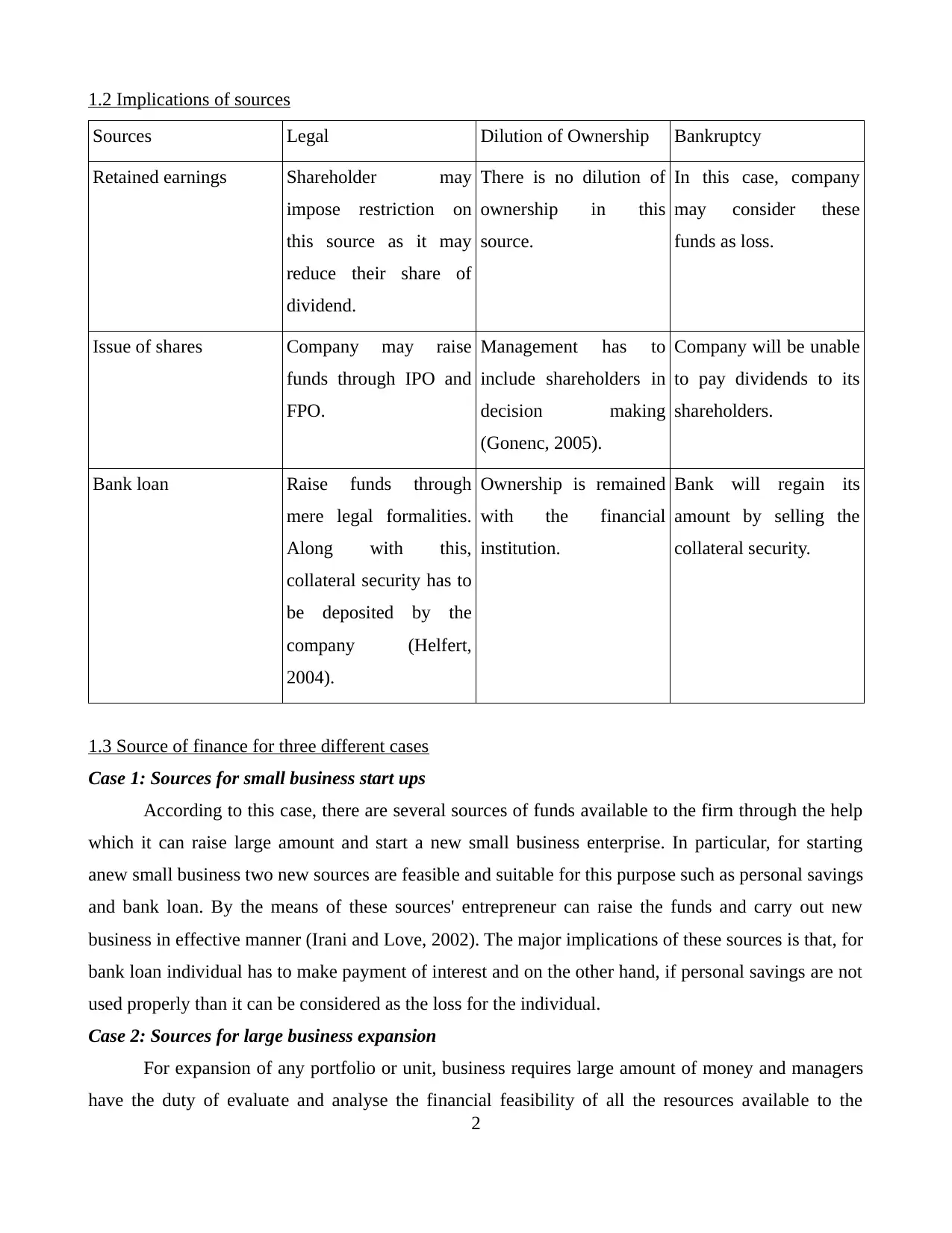

1.2 Implications of sources

Sources Legal Dilution of Ownership Bankruptcy

Retained earnings Shareholder may

impose restriction on

this source as it may

reduce their share of

dividend.

There is no dilution of

ownership in this

source.

In this case, company

may consider these

funds as loss.

Issue of shares Company may raise

funds through IPO and

FPO.

Management has to

include shareholders in

decision making

(Gonenc, 2005).

Company will be unable

to pay dividends to its

shareholders.

Bank loan Raise funds through

mere legal formalities.

Along with this,

collateral security has to

be deposited by the

company (Helfert,

2004).

Ownership is remained

with the financial

institution.

Bank will regain its

amount by selling the

collateral security.

1.3 Source of finance for three different cases

Case 1: Sources for small business start ups

According to this case, there are several sources of funds available to the firm through the help

which it can raise large amount and start a new small business enterprise. In particular, for starting

anew small business two new sources are feasible and suitable for this purpose such as personal savings

and bank loan. By the means of these sources' entrepreneur can raise the funds and carry out new

business in effective manner (Irani and Love, 2002). The major implications of these sources is that, for

bank loan individual has to make payment of interest and on the other hand, if personal savings are not

used properly than it can be considered as the loss for the individual.

Case 2: Sources for large business expansion

For expansion of any portfolio or unit, business requires large amount of money and managers

have the duty of evaluate and analyse the financial feasibility of all the resources available to the

2

Sources Legal Dilution of Ownership Bankruptcy

Retained earnings Shareholder may

impose restriction on

this source as it may

reduce their share of

dividend.

There is no dilution of

ownership in this

source.

In this case, company

may consider these

funds as loss.

Issue of shares Company may raise

funds through IPO and

FPO.

Management has to

include shareholders in

decision making

(Gonenc, 2005).

Company will be unable

to pay dividends to its

shareholders.

Bank loan Raise funds through

mere legal formalities.

Along with this,

collateral security has to

be deposited by the

company (Helfert,

2004).

Ownership is remained

with the financial

institution.

Bank will regain its

amount by selling the

collateral security.

1.3 Source of finance for three different cases

Case 1: Sources for small business start ups

According to this case, there are several sources of funds available to the firm through the help

which it can raise large amount and start a new small business enterprise. In particular, for starting

anew small business two new sources are feasible and suitable for this purpose such as personal savings

and bank loan. By the means of these sources' entrepreneur can raise the funds and carry out new

business in effective manner (Irani and Love, 2002). The major implications of these sources is that, for

bank loan individual has to make payment of interest and on the other hand, if personal savings are not

used properly than it can be considered as the loss for the individual.

Case 2: Sources for large business expansion

For expansion of any portfolio or unit, business requires large amount of money and managers

have the duty of evaluate and analyse the financial feasibility of all the resources available to the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company. In this context, large corporation is recommended to use issue of share for raising the funds

as it is the most feasible method for generating money for a large business enterprise. The main benefit

of this source is that, company is liable to pay principle amount to its shareholders. But in return of

invested amount, company has to pay dividends to its shareholders so that they can continue with the

business in the future. Along with this, retained earnings can be used because they are kept reserved for

expansion and other related purpose only as well as retained earnings will not raise liability of business.

Case 3: Sources for small group of people for buying up existing venture

According to this case, small group of people in order to enhance their existing business

operations are planning to buy existing venture thus requires large amount of money. Therefore, it has

been recommended to these people is that they should use government grants and venture capitalist as

the major source of finance (Leung, 2011). However, the rationale behind government grants is that

they are easy to acquire and government of UK promotes such investment so that small business can

grow effectively. On the other hand, venture capitalists are the investors who can invest in the potential

proposal of business and carry out the operations effectively.

TASK 2

2.1 Costs associated with different sources

In order to raise funds there are several costs that company has to incur. However, each source

has its own cost associated that manager has to evaluate and avoid the risks and uncertainties associated

with it. Retained earnings: These are the funds that are kept reserved after paying all the interest,

dividends, and share of profits to the different stakeholders (Pavlatos and Paggios, 2009).

Retained earnings consist of opportunity costs that company have in investing for future

potential business. Issue of shares: In this source, company is going to bear the costs of dividend as well as the cost

of issuing the shares within the market. It is important for the firm to pay dividends to its

shareholders so that their needs and wants can be satisfied in effective and efficient manner.

Bank loan: This source consists of interest cost and it is essential for the management of

business enterprise to pay interest instalment every month despite having adverse financial

position (Lewellen, 2004).

These are some of the costs associated with different sources of finance available to the business

enterprise.

3

as it is the most feasible method for generating money for a large business enterprise. The main benefit

of this source is that, company is liable to pay principle amount to its shareholders. But in return of

invested amount, company has to pay dividends to its shareholders so that they can continue with the

business in the future. Along with this, retained earnings can be used because they are kept reserved for

expansion and other related purpose only as well as retained earnings will not raise liability of business.

Case 3: Sources for small group of people for buying up existing venture

According to this case, small group of people in order to enhance their existing business

operations are planning to buy existing venture thus requires large amount of money. Therefore, it has

been recommended to these people is that they should use government grants and venture capitalist as

the major source of finance (Leung, 2011). However, the rationale behind government grants is that

they are easy to acquire and government of UK promotes such investment so that small business can

grow effectively. On the other hand, venture capitalists are the investors who can invest in the potential

proposal of business and carry out the operations effectively.

TASK 2

2.1 Costs associated with different sources

In order to raise funds there are several costs that company has to incur. However, each source

has its own cost associated that manager has to evaluate and avoid the risks and uncertainties associated

with it. Retained earnings: These are the funds that are kept reserved after paying all the interest,

dividends, and share of profits to the different stakeholders (Pavlatos and Paggios, 2009).

Retained earnings consist of opportunity costs that company have in investing for future

potential business. Issue of shares: In this source, company is going to bear the costs of dividend as well as the cost

of issuing the shares within the market. It is important for the firm to pay dividends to its

shareholders so that their needs and wants can be satisfied in effective and efficient manner.

Bank loan: This source consists of interest cost and it is essential for the management of

business enterprise to pay interest instalment every month despite having adverse financial

position (Lewellen, 2004).

These are some of the costs associated with different sources of finance available to the business

enterprise.

3

2.2 Importance of financial planning

Financial planning or forecasting can be defined as the process of managing and making

optimum utilisation of available resources. However, the main purpose behind having financial

planning is that it assists in avoiding risks and uncertainties associated with the financial position of

business enterprise. Further, it also plays important role in the success of business enterprise. By the

means of proper financial forecasting, manager can easily identify future income and expenditure that

company's functioning may possess during the course of accounting period (Prorokowski, 2011). In

addition to this, through the help economic management senior authority can make effective and

profitable investment decisions. Lastly, it helps in maintaining balance between company's cash

outflow and inflow.

AC 2.3 Financial information requirement for decision making purposes

There are several stakeholders associated with the firm which requires wide range of information

so that they can make smart and effective decisions regarding future contingency. However, these users

gather information from varied sources such as budgets, financial statements, and annual report of the

desired company. Further, budgets help internal stakeholders such as managers, management and other

crucial managerial people in identifying and understanding variance by comparing the actual outcome

and budgeted value (Lapsley, Miller and Panozzo, 2010). By the means of this, managers can make

suitable and reliable strategies and tactics so that negative variances can be converted into fruitful

results for the company. Along with this, suppliers uses the financial statements to evaluate the

capability of firm in paying the debt amount so that they can make decisions regarding future supply of

goods and services as well as determine the credit period given to the corporation. In case of

employees, they are the stakeholders who are interested in evaluating the actual financial position of

the business so that they can analyse their future within the company and other benefits such as bonus,

incentives etc. Lastly, shareholders investigate the net profit of the company in order to make decision

related to their dividend as well as the policy framed by the company regarding dividends. By the

means of this they can easily make decision on future investments.

4

Financial planning or forecasting can be defined as the process of managing and making

optimum utilisation of available resources. However, the main purpose behind having financial

planning is that it assists in avoiding risks and uncertainties associated with the financial position of

business enterprise. Further, it also plays important role in the success of business enterprise. By the

means of proper financial forecasting, manager can easily identify future income and expenditure that

company's functioning may possess during the course of accounting period (Prorokowski, 2011). In

addition to this, through the help economic management senior authority can make effective and

profitable investment decisions. Lastly, it helps in maintaining balance between company's cash

outflow and inflow.

AC 2.3 Financial information requirement for decision making purposes

There are several stakeholders associated with the firm which requires wide range of information

so that they can make smart and effective decisions regarding future contingency. However, these users

gather information from varied sources such as budgets, financial statements, and annual report of the

desired company. Further, budgets help internal stakeholders such as managers, management and other

crucial managerial people in identifying and understanding variance by comparing the actual outcome

and budgeted value (Lapsley, Miller and Panozzo, 2010). By the means of this, managers can make

suitable and reliable strategies and tactics so that negative variances can be converted into fruitful

results for the company. Along with this, suppliers uses the financial statements to evaluate the

capability of firm in paying the debt amount so that they can make decisions regarding future supply of

goods and services as well as determine the credit period given to the corporation. In case of

employees, they are the stakeholders who are interested in evaluating the actual financial position of

the business so that they can analyse their future within the company and other benefits such as bonus,

incentives etc. Lastly, shareholders investigate the net profit of the company in order to make decision

related to their dividend as well as the policy framed by the company regarding dividends. By the

means of this they can easily make decision on future investments.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC 2.4 Cost of financial statements showing in financial statements

Every organisation operating in the corporate market has to prepare different types of statements so

that they can record their transaction taken place during the course of accounting period. There are

three major financial statements of the company that are: income statement, cash flow statement and

balance sheet. Following are the effects of selected sources on the financial statements:

Issue of shares: Under this source cost of dividend is shown under the debit side of the profit and

loss account (Income statement). While on the other hand, the amount raised through issuing

shares is headed under the liability side of share capital in the balance sheet (Dayananda, 2002).

Bank loan: The amount generated through loan will be considered as the long term liability of the

company. Thus, it is headed to the liability side of balance sheet. As well as the amount changed

by financial institution on monthly basis in terms of interest will be shown in debit side of profit

and loss account.

Retained earnings: These are the funds that are kept reserved by the management for the future

contingency. Thus, the amount raised through this source will reduce the retained profit in the

income statement of the company (Neale and McElroy, 2004).

TASK 3

AC 3.1 Evaluation of sales budget and cash flow statement

According to the present given case there are two statements of the company that has been

analysed to evaluate the variances and loopholes within the financial position of the firm.

Sales budget: In the given sales budget it has been evaluated that, negative variance within the

sales performance of the company is constantly increasing from month of July to December. However,

it clearly states that actual sales of company are less than the anticipated sales value. In addition to this,

this can be due to the reason of lower quality of product leads to lower demand of the products (Shim,

Siegel and Shim, 2011). Thus, it is important for the management to focus on maintaining the quality

aspect at each level so that products reliability and suitability can be increased as per the expectations

of the customers and hence, leads to higher demand in the market.

Cash flow statement: The total cash is showing fluctuating results and it because of the sales

volatile during the months of July to December. Further, expenditure like wages, rent and rates,

insurance and directors salaries are volatile in nature. In addition to it, the available balance of cash has

shown decreasing figures till the month of April. While better sales strategy helps in generating higher

cash balance in the next month of 43000 but again due to lack of management showed decreasing

5

Every organisation operating in the corporate market has to prepare different types of statements so

that they can record their transaction taken place during the course of accounting period. There are

three major financial statements of the company that are: income statement, cash flow statement and

balance sheet. Following are the effects of selected sources on the financial statements:

Issue of shares: Under this source cost of dividend is shown under the debit side of the profit and

loss account (Income statement). While on the other hand, the amount raised through issuing

shares is headed under the liability side of share capital in the balance sheet (Dayananda, 2002).

Bank loan: The amount generated through loan will be considered as the long term liability of the

company. Thus, it is headed to the liability side of balance sheet. As well as the amount changed

by financial institution on monthly basis in terms of interest will be shown in debit side of profit

and loss account.

Retained earnings: These are the funds that are kept reserved by the management for the future

contingency. Thus, the amount raised through this source will reduce the retained profit in the

income statement of the company (Neale and McElroy, 2004).

TASK 3

AC 3.1 Evaluation of sales budget and cash flow statement

According to the present given case there are two statements of the company that has been

analysed to evaluate the variances and loopholes within the financial position of the firm.

Sales budget: In the given sales budget it has been evaluated that, negative variance within the

sales performance of the company is constantly increasing from month of July to December. However,

it clearly states that actual sales of company are less than the anticipated sales value. In addition to this,

this can be due to the reason of lower quality of product leads to lower demand of the products (Shim,

Siegel and Shim, 2011). Thus, it is important for the management to focus on maintaining the quality

aspect at each level so that products reliability and suitability can be increased as per the expectations

of the customers and hence, leads to higher demand in the market.

Cash flow statement: The total cash is showing fluctuating results and it because of the sales

volatile during the months of July to December. Further, expenditure like wages, rent and rates,

insurance and directors salaries are volatile in nature. In addition to it, the available balance of cash has

shown decreasing figures till the month of April. While better sales strategy helps in generating higher

cash balance in the next month of 43000 but again due to lack of management showed decreasing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

results in the month of November. Thus, it can be recommended that, senior authority should focus on

increasing company’s sales so that it can generate higher profitability.

To,

The Director of ABC Ltd

Date _____

Subject: Current financial position of the business enterprise

Looking at the present condition of firm’s expenditure and revenues it has been evaluated

that; management should indulge better and effective strategies so that desired results can be

obtained. Along with this, negative sales volume affecting the cash balance and less

profitability. Henceforth, it is recommended to top level management that they should

undertake new strategies so that sales of the offerings can be increased as well as manager

should use effective marketing planning to market and promote the products so that desired

audience can be reached in the best possible manner.

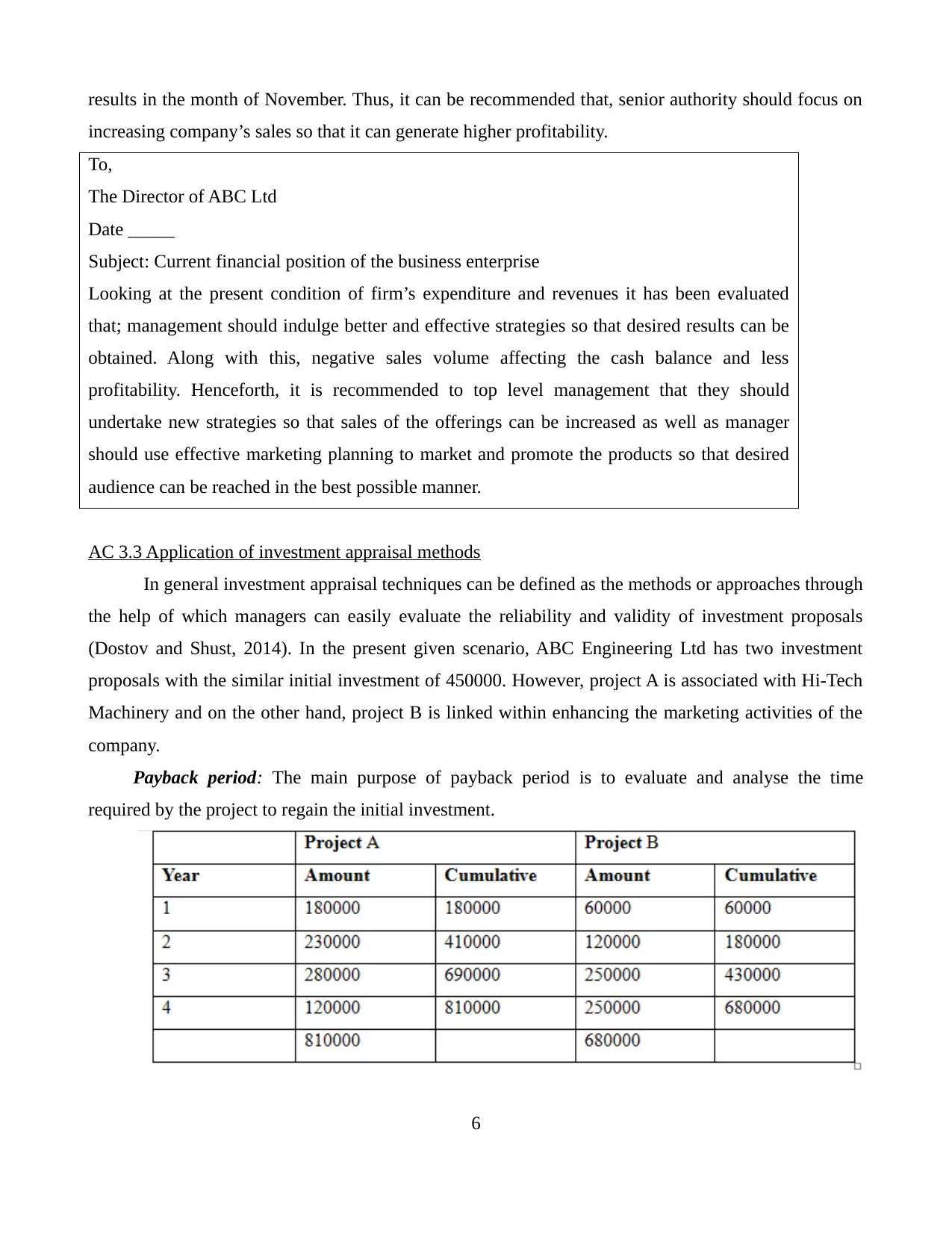

AC 3.3 Application of investment appraisal methods

In general investment appraisal techniques can be defined as the methods or approaches through

the help of which managers can easily evaluate the reliability and validity of investment proposals

(Dostov and Shust, 2014). In the present given scenario, ABC Engineering Ltd has two investment

proposals with the similar initial investment of 450000. However, project A is associated with Hi-Tech

Machinery and on the other hand, project B is linked within enhancing the marketing activities of the

company.

Payback period: The main purpose of payback period is to evaluate and analyse the time

required by the project to regain the initial investment.

6

increasing company’s sales so that it can generate higher profitability.

To,

The Director of ABC Ltd

Date _____

Subject: Current financial position of the business enterprise

Looking at the present condition of firm’s expenditure and revenues it has been evaluated

that; management should indulge better and effective strategies so that desired results can be

obtained. Along with this, negative sales volume affecting the cash balance and less

profitability. Henceforth, it is recommended to top level management that they should

undertake new strategies so that sales of the offerings can be increased as well as manager

should use effective marketing planning to market and promote the products so that desired

audience can be reached in the best possible manner.

AC 3.3 Application of investment appraisal methods

In general investment appraisal techniques can be defined as the methods or approaches through

the help of which managers can easily evaluate the reliability and validity of investment proposals

(Dostov and Shust, 2014). In the present given scenario, ABC Engineering Ltd has two investment

proposals with the similar initial investment of 450000. However, project A is associated with Hi-Tech

Machinery and on the other hand, project B is linked within enhancing the marketing activities of the

company.

Payback period: The main purpose of payback period is to evaluate and analyse the time

required by the project to regain the initial investment.

6

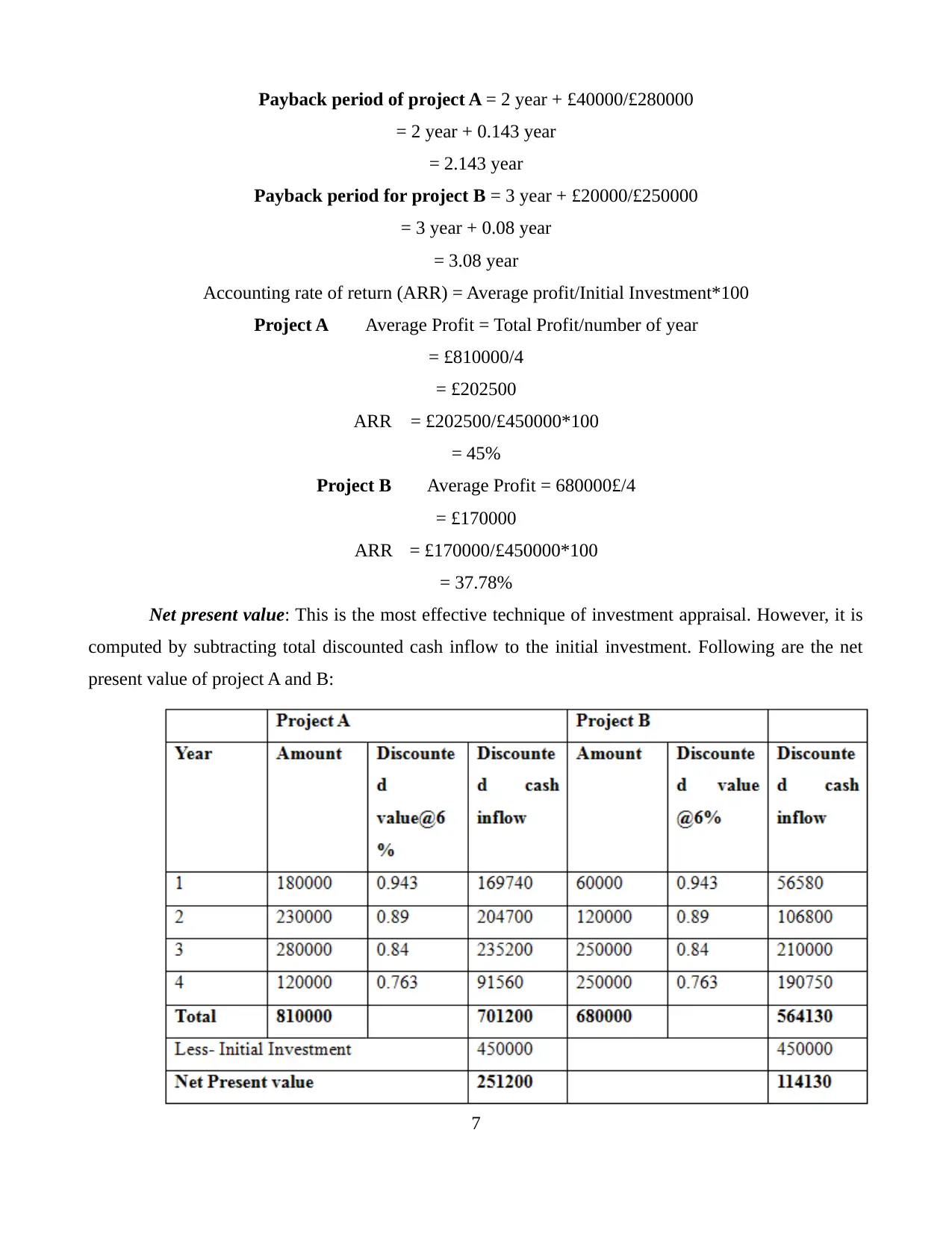

Payback period of project A = 2 year + £40000/£280000

= 2 year + 0.143 year

= 2.143 year

Payback period for project B = 3 year + £20000/£250000

= 3 year + 0.08 year

= 3.08 year

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= £810000/4

= £202500

ARR = £202500/£450000*100

= 45%

Project B Average Profit = 680000£/4

= £170000

ARR = £170000/£450000*100

= 37.78%

Net present value: This is the most effective technique of investment appraisal. However, it is

computed by subtracting total discounted cash inflow to the initial investment. Following are the net

present value of project A and B:

7

= 2 year + 0.143 year

= 2.143 year

Payback period for project B = 3 year + £20000/£250000

= 3 year + 0.08 year

= 3.08 year

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= £810000/4

= £202500

ARR = £202500/£450000*100

= 45%

Project B Average Profit = 680000£/4

= £170000

ARR = £170000/£450000*100

= 37.78%

Net present value: This is the most effective technique of investment appraisal. However, it is

computed by subtracting total discounted cash inflow to the initial investment. Following are the net

present value of project A and B:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Project A = net present value of project A is £251200

Project B = net present value of project A is £114130

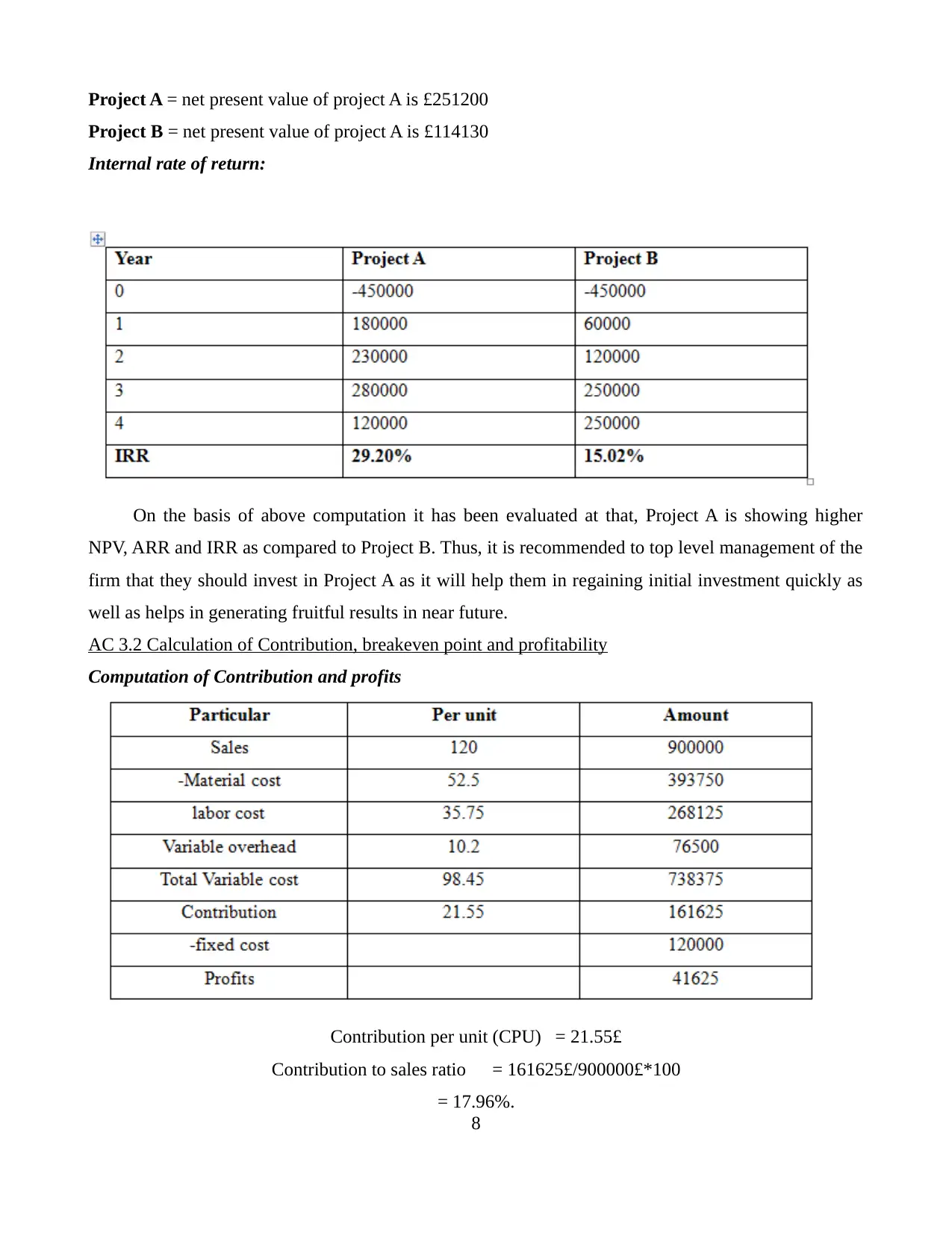

Internal rate of return:

On the basis of above computation it has been evaluated at that, Project A is showing higher

NPV, ARR and IRR as compared to Project B. Thus, it is recommended to top level management of the

firm that they should invest in Project A as it will help them in regaining initial investment quickly as

well as helps in generating fruitful results in near future.

AC 3.2 Calculation of Contribution, breakeven point and profitability

Computation of Contribution and profits

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio = 161625£/900000£*100

= 17.96%.

8

Project B = net present value of project A is £114130

Internal rate of return:

On the basis of above computation it has been evaluated at that, Project A is showing higher

NPV, ARR and IRR as compared to Project B. Thus, it is recommended to top level management of the

firm that they should invest in Project A as it will help them in regaining initial investment quickly as

well as helps in generating fruitful results in near future.

AC 3.2 Calculation of Contribution, breakeven point and profitability

Computation of Contribution and profits

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio = 161625£/900000£*100

= 17.96%.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

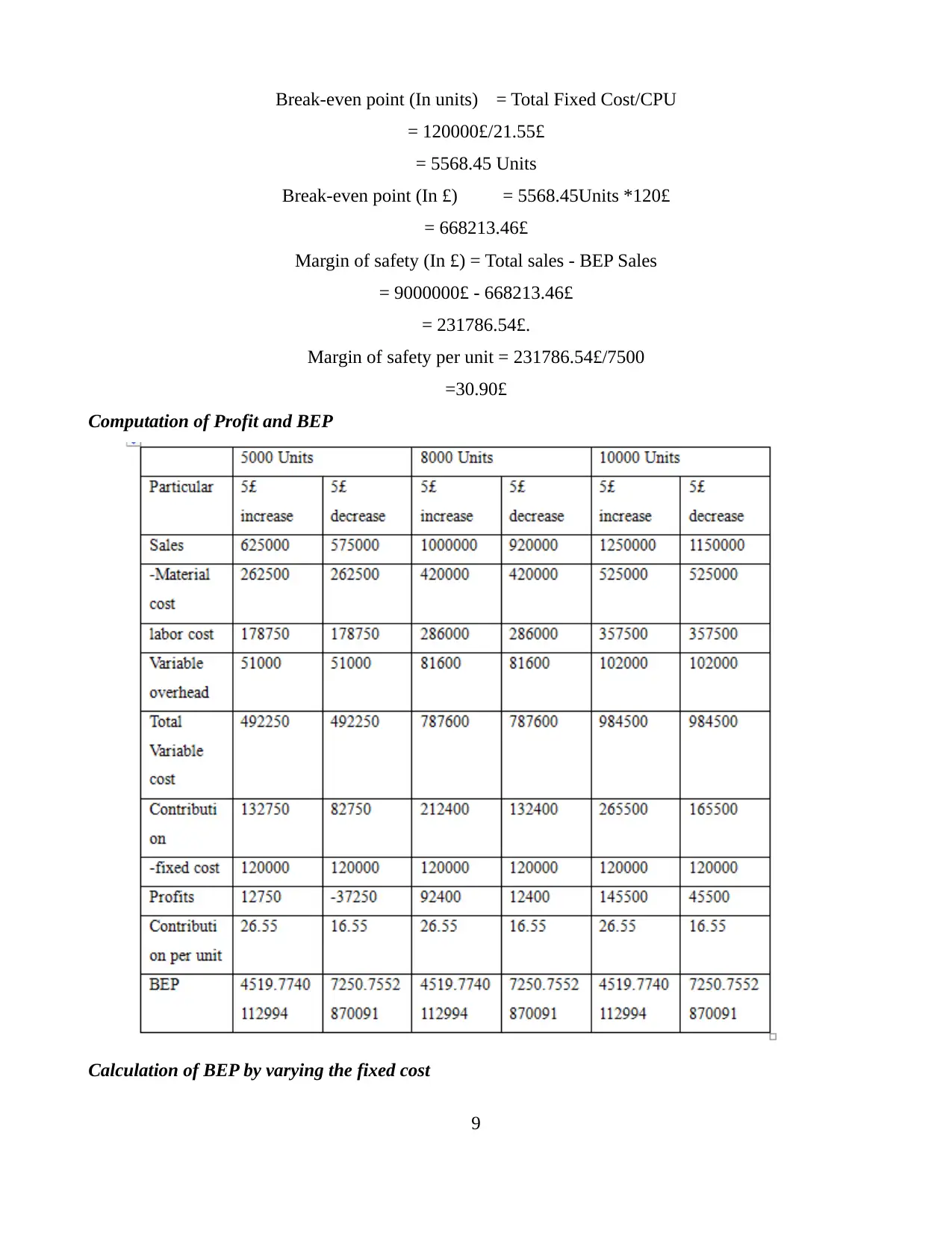

Break-even point (In units) = Total Fixed Cost/CPU

= 120000£/21.55£

= 5568.45 Units

Break-even point (In £) = 5568.45Units *120£

= 668213.46£

Margin of safety (In £) = Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

Computation of Profit and BEP

Calculation of BEP by varying the fixed cost

9

= 120000£/21.55£

= 5568.45 Units

Break-even point (In £) = 5568.45Units *120£

= 668213.46£

Margin of safety (In £) = Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

Computation of Profit and BEP

Calculation of BEP by varying the fixed cost

9

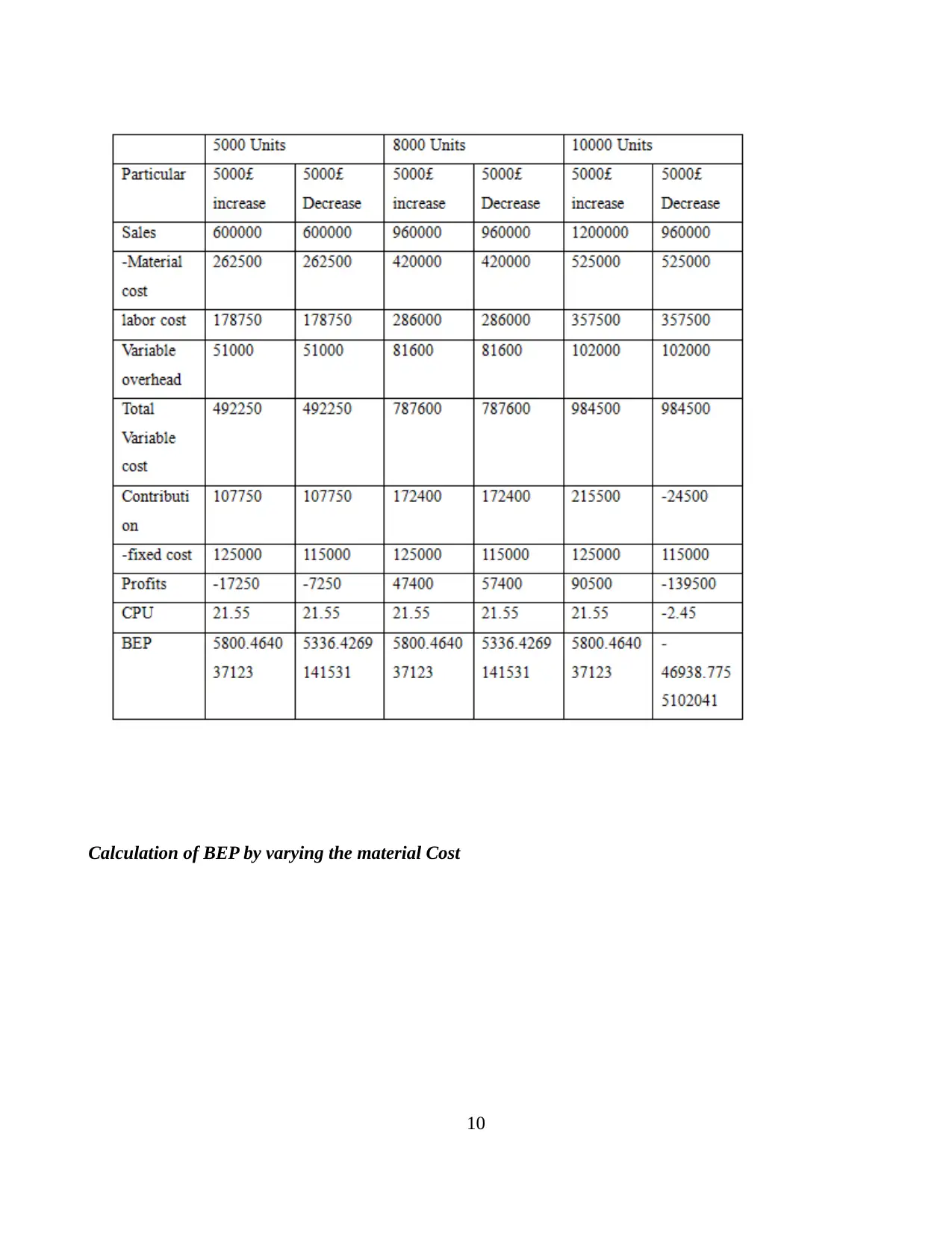

Calculation of BEP by varying the material Cost

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.