Company Accounting Project Report: Financial Statement Analysis

VerifiedAdded on 2023/06/07

|8

|958

|283

Report

AI Summary

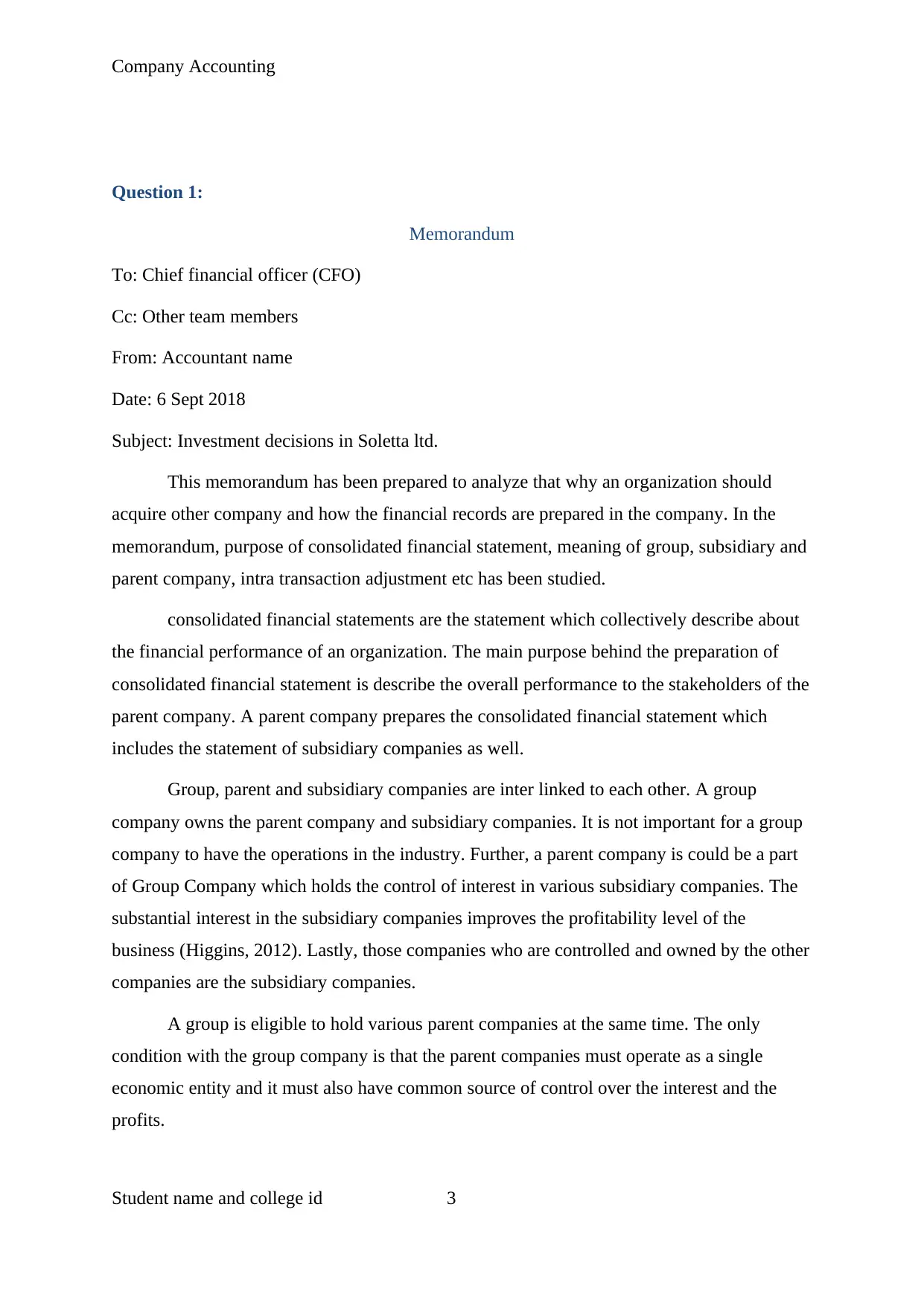

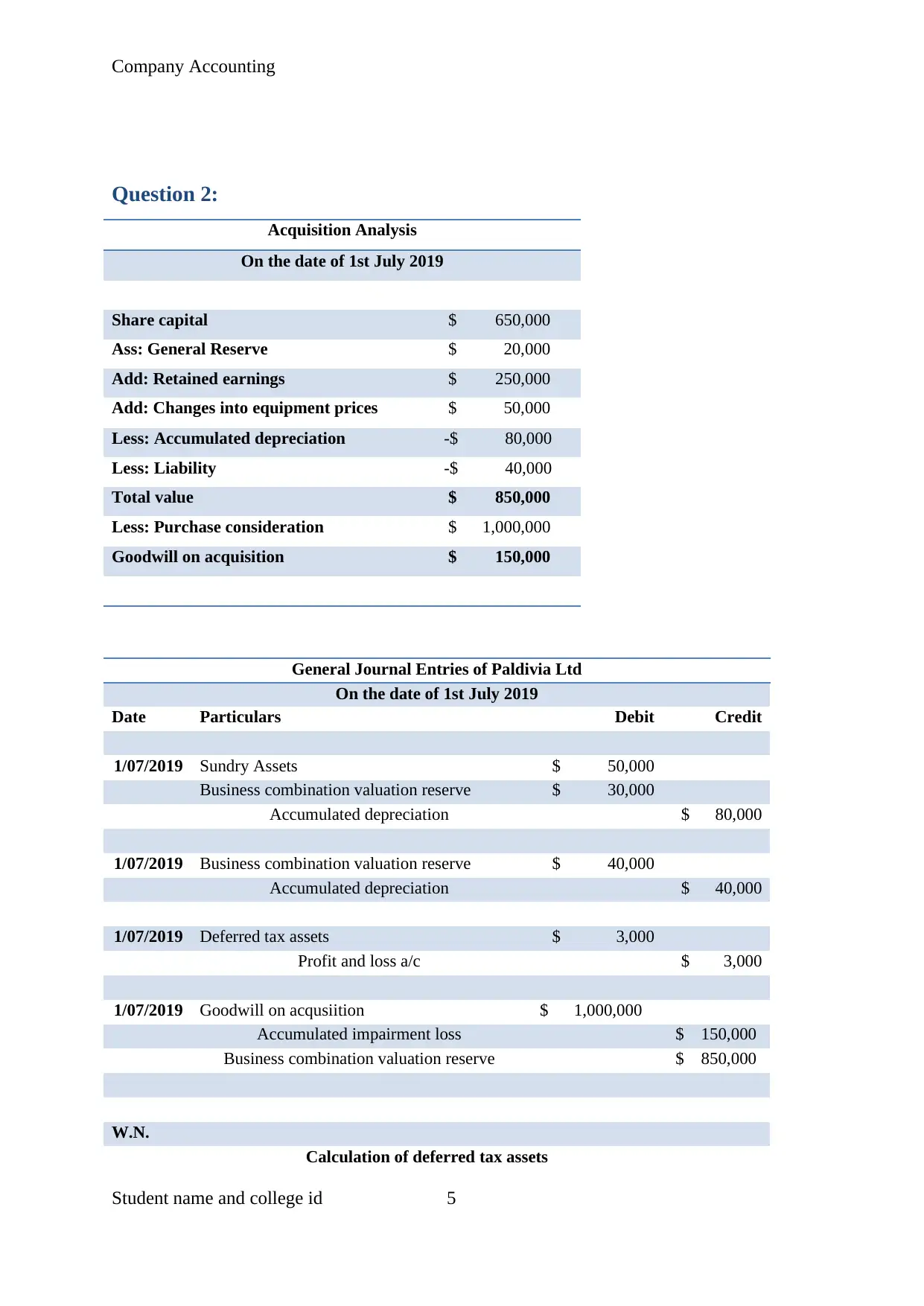

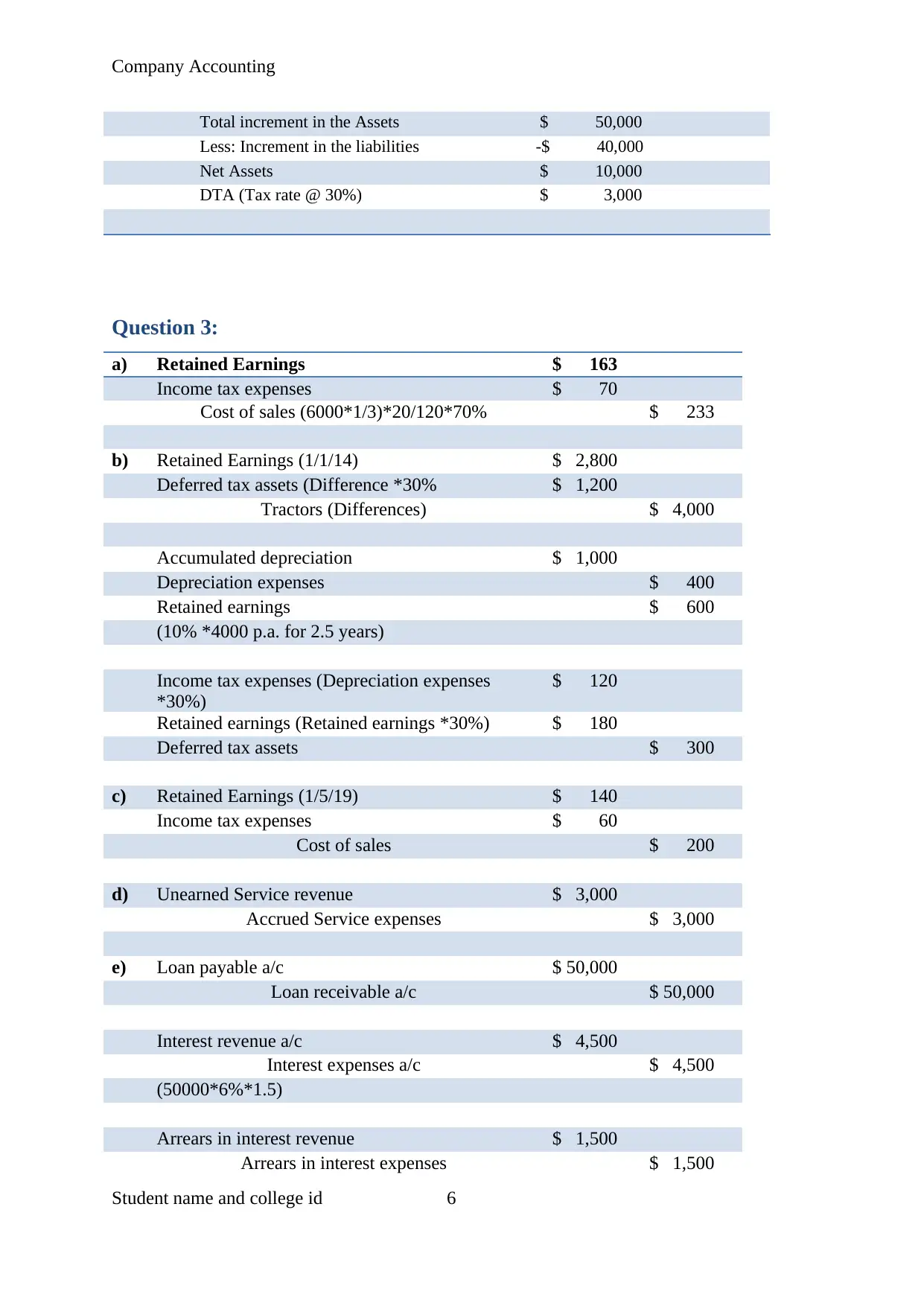

This company accounting project report analyzes investment decisions, the purpose of consolidated financial statements, and the roles of group, parent, and subsidiary companies. It includes an acquisition analysis of Paldivia Ltd, detailing goodwill calculation and journal entries. Furthermore, it covers various financial statement adjustments related to retained earnings, income tax, cost of sales, unearned service revenue, loan transactions, and dividend declarations. The report also addresses intra-group transactions and their impact on consolidated financial statements, emphasizing the importance of external transactions for revenue realization. Desklib provides this assignment solution and many more to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.