Financial Accounting Report: Comparing Financial Accounting Concepts

VerifiedAdded on 2021/02/21

|17

|4332

|154

Report

AI Summary

This report delves into the core concepts of financial accounting, differentiating between sole traders and limited companies and their respective financial statement preparation. It examines the income statement and balance sheet, providing examples and working notes for both. The report explores the differences between the income statement and financial statements, outlining their distinct purposes, content, and users. It also includes a detailed explanation of bank reconciliation statements, highlighting their significance in identifying and resolving discrepancies between cash book and bank passbook entries. The report covers topics such as final accounts of sole properties and financial reports of a limited company and also includes evaluation of financial condition of the company, the process of statement of bank-reconciliation, detail discussion of control account and suspense account to reconcile the business records.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...............................................................................................................................3

Question - 01................................................................................................................................3

Question - 02...............................................................................................................................5

Question - 03................................................................................................................................7

Question - 04 ...............................................................................................................................9

Question - 05 .............................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...............................................................................................................................3

Question - 01................................................................................................................................3

Question - 02...............................................................................................................................5

Question - 03................................................................................................................................7

Question - 04 ...............................................................................................................................9

Question - 05 .............................................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial accounting is main field of accounting that is described as collecting, recording,

summering, evaluating the financial information in order to prepare the final statement of an

organisation (Nilsson and Stockenstrand, 2015). It is described as that keep the track record of a

business financial transaction in the company by using the guideline and accounting standard. It

involves the creation of the financial statement and reporting by using the business activities to

make available to internal as well as external stakeholder. Firm prepares the financial statements

to analysis the operational activities of the business that happened during the year. This report

includes the income statement and balance sheet with associated working notes by using the

following financial information provided by the company. It is also includes evaluation of

financial condition of the company, the process of statement of bank-reconciliation, detail

discussion of control account and suspense account to reconcile the business records. This

analytical report includes the statement of final account of sole properties and financial reports of

a limited company.

MAIN BODY

Question - 01

Sole traders- It is also called sole proprietors. The word sole business trader refers to

especially the individual who run the business without taking help of another person (Wang,

2014). The owner of the business prepares the final account by using the financial information

that happened during the year. The real owner of the business is called sole properties in the

business Properties of the particular business created the financial statement of a year by using

the activities related to business. Final account of a entity consist of profit and loss account and

final statement. Final statement can be made by helping the primary data such as journal entries,

ledger or posting and trial balances. The financial statement that are prepared by sole trader is

consist of:

Income statement

Balance sheet

Financial accounting is main field of accounting that is described as collecting, recording,

summering, evaluating the financial information in order to prepare the final statement of an

organisation (Nilsson and Stockenstrand, 2015). It is described as that keep the track record of a

business financial transaction in the company by using the guideline and accounting standard. It

involves the creation of the financial statement and reporting by using the business activities to

make available to internal as well as external stakeholder. Firm prepares the financial statements

to analysis the operational activities of the business that happened during the year. This report

includes the income statement and balance sheet with associated working notes by using the

following financial information provided by the company. It is also includes evaluation of

financial condition of the company, the process of statement of bank-reconciliation, detail

discussion of control account and suspense account to reconcile the business records. This

analytical report includes the statement of final account of sole properties and financial reports of

a limited company.

MAIN BODY

Question - 01

Sole traders- It is also called sole proprietors. The word sole business trader refers to

especially the individual who run the business without taking help of another person (Wang,

2014). The owner of the business prepares the final account by using the financial information

that happened during the year. The real owner of the business is called sole properties in the

business Properties of the particular business created the financial statement of a year by using

the activities related to business. Final account of a entity consist of profit and loss account and

final statement. Final statement can be made by helping the primary data such as journal entries,

ledger or posting and trial balances. The financial statement that are prepared by sole trader is

consist of:

Income statement

Balance sheet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial statement- Financial statement are the fundamental books of accounts that are prepared

by the business owner in order to evaluate the business operation and activities at any of the

entity. These are the financial reports that are presented by the management of a company to

owners to show the financial position in the market (Zeff, 2016). financial sheet of the business

represent the business position in the market. A general object behind the financial statement is

know the performance and actual status of the business. These financial statement are prepared

in once in a year after making basic accounting transaction.

Types of financial statements: Basically, These statement includes two types of account that are

mentioned below:

Balance sheet- It is a list of business items that includes the assets and obligation of a

particular company. It shows the fiscal condition of an entity. It is statement that includes

business's possession, liabilities, capital, short term liabilities and fix assets of a specific

business. Balance sheet of a business is based on the equation is as Assets is equals to

liabilities plus equity capital. Balance sheet is essential part of the consolidated final

statement that represent the business position to its internal stakeholders and management

Income statement- It is refers to statement of trading account and profit and loss account.

It is basically core financial statement of a particular business that presents the profit or

loss in the business firm (Pinnuck, 2012). It may defined as net revenue generated and

total expenditure made during the year. It stipulates how a sales volume is transformed

into net profit or net sales. Income statement includes the basic business transaction such

as recording, posting, balance of all data related to operational activities of the firm.

Final statement are prepared of Greg palmer as per information of trial balance.

Income statement of Greg Palmer are as follows:

Income Statement for the year ended 31st April 2019

Particulars Amount Particulars Amount

To Opening stock 160000 By Sales revenue 1400000

To Purchase 840000 By Closing stock 100000

To Wages 440000

Add:Outstanding wages 20000 460000

To Gross Profit 40000

1500000 1500000

by the business owner in order to evaluate the business operation and activities at any of the

entity. These are the financial reports that are presented by the management of a company to

owners to show the financial position in the market (Zeff, 2016). financial sheet of the business

represent the business position in the market. A general object behind the financial statement is

know the performance and actual status of the business. These financial statement are prepared

in once in a year after making basic accounting transaction.

Types of financial statements: Basically, These statement includes two types of account that are

mentioned below:

Balance sheet- It is a list of business items that includes the assets and obligation of a

particular company. It shows the fiscal condition of an entity. It is statement that includes

business's possession, liabilities, capital, short term liabilities and fix assets of a specific

business. Balance sheet of a business is based on the equation is as Assets is equals to

liabilities plus equity capital. Balance sheet is essential part of the consolidated final

statement that represent the business position to its internal stakeholders and management

Income statement- It is refers to statement of trading account and profit and loss account.

It is basically core financial statement of a particular business that presents the profit or

loss in the business firm (Pinnuck, 2012). It may defined as net revenue generated and

total expenditure made during the year. It stipulates how a sales volume is transformed

into net profit or net sales. Income statement includes the basic business transaction such

as recording, posting, balance of all data related to operational activities of the firm.

Final statement are prepared of Greg palmer as per information of trial balance.

Income statement of Greg Palmer are as follows:

Income Statement for the year ended 31st April 2019

Particulars Amount Particulars Amount

To Opening stock 160000 By Sales revenue 1400000

To Purchase 840000 By Closing stock 100000

To Wages 440000

Add:Outstanding wages 20000 460000

To Gross Profit 40000

1500000 1500000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

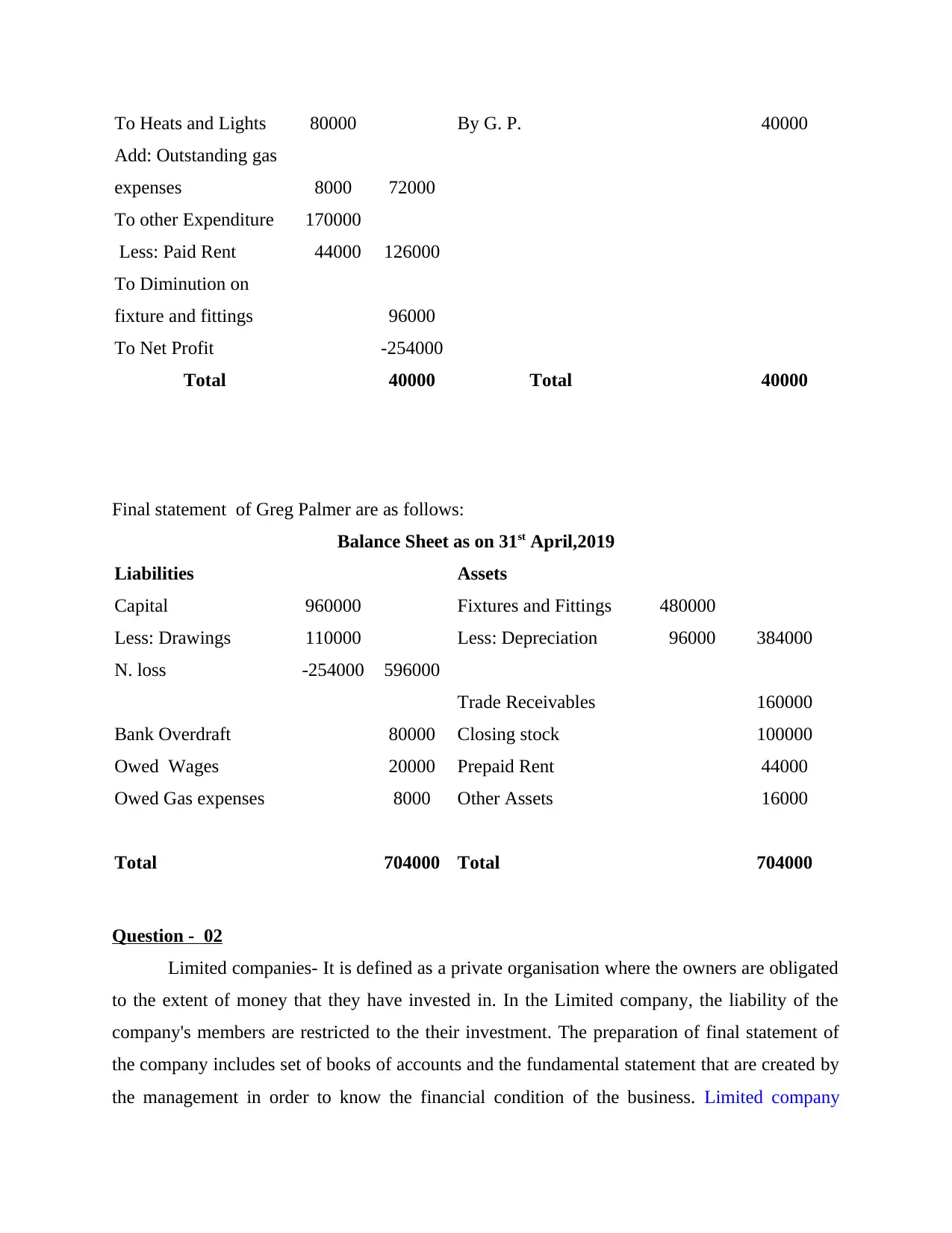

To Heats and Lights 80000 By G. P. 40000

Add: Outstanding gas

expenses 8000 72000

To other Expenditure 170000

Less: Paid Rent 44000 126000

To Diminution on

fixture and fittings 96000

To Net Profit -254000

Total 40000 Total 40000

Final statement of Greg Palmer are as follows:

Balance Sheet as on 31st April,2019

Liabilities Assets

Capital 960000 Fixtures and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

N. loss -254000 596000

Trade Receivables 160000

Bank Overdraft 80000 Closing stock 100000

Owed Wages 20000 Prepaid Rent 44000

Owed Gas expenses 8000 Other Assets 16000

Total 704000 Total 704000

Question - 02

Limited companies- It is defined as a private organisation where the owners are obligated

to the extent of money that they have invested in. In the Limited company, the liability of the

company's members are restricted to the their investment. The preparation of final statement of

the company includes set of books of accounts and the fundamental statement that are created by

the management in order to know the financial condition of the business. Limited company

Add: Outstanding gas

expenses 8000 72000

To other Expenditure 170000

Less: Paid Rent 44000 126000

To Diminution on

fixture and fittings 96000

To Net Profit -254000

Total 40000 Total 40000

Final statement of Greg Palmer are as follows:

Balance Sheet as on 31st April,2019

Liabilities Assets

Capital 960000 Fixtures and Fittings 480000

Less: Drawings 110000 Less: Depreciation 96000 384000

N. loss -254000 596000

Trade Receivables 160000

Bank Overdraft 80000 Closing stock 100000

Owed Wages 20000 Prepaid Rent 44000

Owed Gas expenses 8000 Other Assets 16000

Total 704000 Total 704000

Question - 02

Limited companies- It is defined as a private organisation where the owners are obligated

to the extent of money that they have invested in. In the Limited company, the liability of the

company's members are restricted to the their investment. The preparation of final statement of

the company includes set of books of accounts and the fundamental statement that are created by

the management in order to know the financial condition of the business. Limited company

provides the dividend to its shareholders as per their investment. Company follow the rules and

regulation of company act and standard to maintain the books of accounts. The financial account

of the limited company includes trading and profit and loss account with balance sheet. With the

help of the vouchers, business transaction records related to business records it is easy to prepare

the financial statement of the business (Gheorghe, 2012). All the financial statement and

accounts are prepared by the accountant of the business. Here, the limited companies maintain

the following accounts in the firm:

Trading account

profit and loss account

Balance sheet

Cash flow statement

P&L appropriation account

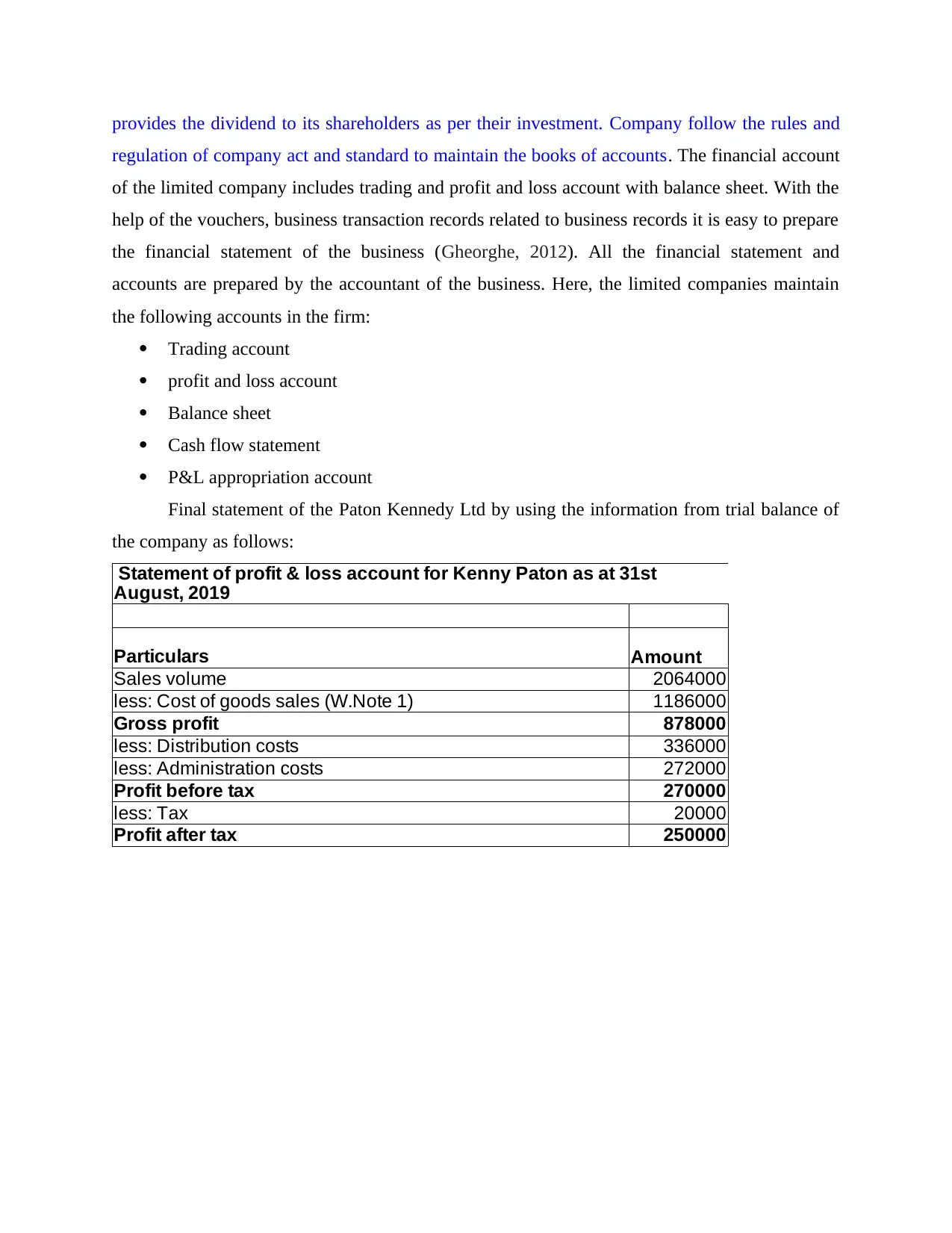

Final statement of the Paton Kennedy Ltd by using the information from trial balance of

the company as follows:

Particulars

Sales volume 2064000

less: Cost of goods sales (W.Note 1) 1186000

Gross profit 878000

less: Distribution costs 336000

less: Administration costs 272000

Profit before tax 270000

less: Tax 20000

Profit after tax 250000

Statement of profit & loss account for Kenny Paton as at 31st

August, 2019

Amount

regulation of company act and standard to maintain the books of accounts. The financial account

of the limited company includes trading and profit and loss account with balance sheet. With the

help of the vouchers, business transaction records related to business records it is easy to prepare

the financial statement of the business (Gheorghe, 2012). All the financial statement and

accounts are prepared by the accountant of the business. Here, the limited companies maintain

the following accounts in the firm:

Trading account

profit and loss account

Balance sheet

Cash flow statement

P&L appropriation account

Final statement of the Paton Kennedy Ltd by using the information from trial balance of

the company as follows:

Particulars

Sales volume 2064000

less: Cost of goods sales (W.Note 1) 1186000

Gross profit 878000

less: Distribution costs 336000

less: Administration costs 272000

Profit before tax 270000

less: Tax 20000

Profit after tax 250000

Statement of profit & loss account for Kenny Paton as at 31st

August, 2019

Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

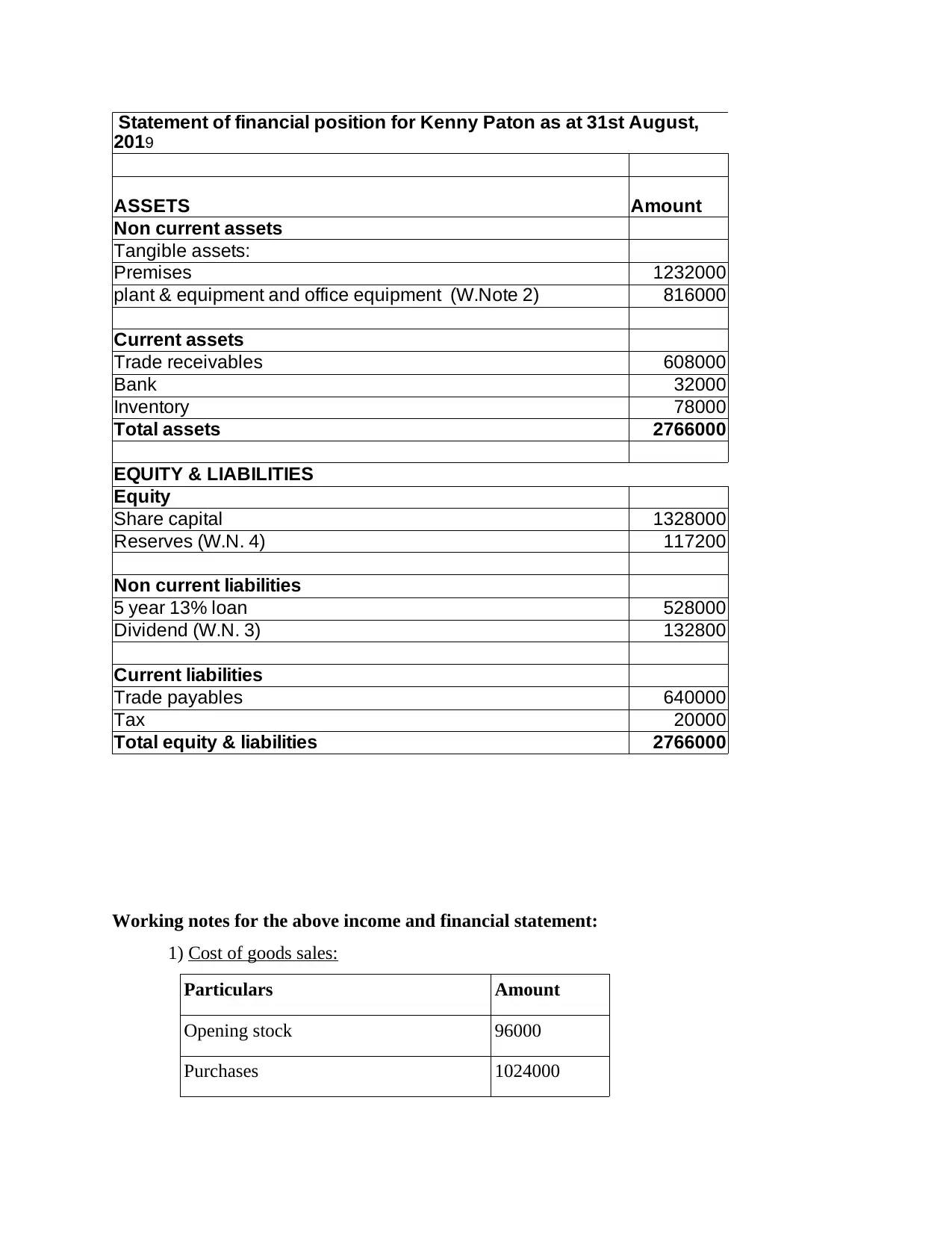

ASSETS

Non current assets

Tangible assets:

Premises 1232000

plant & equipment and office equipment (W.Note 2) 816000

Current assets

Trade receivables 608000

Bank 32000

Inventory 78000

Total assets 2766000

EQUITY & LIABILITIES

Equity

Share capital 1328000

Reserves (W.N. 4) 117200

Non current liabilities

5 year 13% loan 528000

Dividend (W.N. 3) 132800

Current liabilities

Trade payables 640000

Tax 20000

Total equity & liabilities 2766000

Statement of financial position for Kenny Paton as at 31st August,

2019

Amount

Working notes for the above income and financial statement:

1) Cost of goods sales:

Particulars Amount

Opening stock 96000

Purchases 1024000

Non current assets

Tangible assets:

Premises 1232000

plant & equipment and office equipment (W.Note 2) 816000

Current assets

Trade receivables 608000

Bank 32000

Inventory 78000

Total assets 2766000

EQUITY & LIABILITIES

Equity

Share capital 1328000

Reserves (W.N. 4) 117200

Non current liabilities

5 year 13% loan 528000

Dividend (W.N. 3) 132800

Current liabilities

Trade payables 640000

Tax 20000

Total equity & liabilities 2766000

Statement of financial position for Kenny Paton as at 31st August,

2019

Amount

Working notes for the above income and financial statement:

1) Cost of goods sales:

Particulars Amount

Opening stock 96000

Purchases 1024000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: closing stock 78000

Depreciation: plant & equipment 115200

Office equipment 28800

Sum 1186000

2) plant & equipment and office equipment:

Items Plant &

equipment

Office

equipment

Cost 768000 192000

Less: dep. 115200 28800

Sum 652800 163200

3) Dividend:

10% of Share capital = 1328000 x 10%

= 132800

4) Reserves:

Profit less dividend = 250000 - 132800

= 117200

Question - 03

Differences between income statement and financial statement:

Income statement is defined as core financial statement that indicates the profit and loss

of the company. It is financial reporting process that provides the detail regarding the business

operating activities. It shows the sales volume generated by the firm, direct and indirect

expenditure, gain and loss during the financial year. It indicates how the sales revenue are

transformed into net profit or loss. The primary purpose of this statement to represent the

business situation to investor whether it have profit or loss in a financial year. Whereas financial

statement are the accounts and reports that are prepared to present the financial condition in

front of management and user so management can make the final decision regarding the

formulation and implementation of the business strategies and investors can make decision

Depreciation: plant & equipment 115200

Office equipment 28800

Sum 1186000

2) plant & equipment and office equipment:

Items Plant &

equipment

Office

equipment

Cost 768000 192000

Less: dep. 115200 28800

Sum 652800 163200

3) Dividend:

10% of Share capital = 1328000 x 10%

= 132800

4) Reserves:

Profit less dividend = 250000 - 132800

= 117200

Question - 03

Differences between income statement and financial statement:

Income statement is defined as core financial statement that indicates the profit and loss

of the company. It is financial reporting process that provides the detail regarding the business

operating activities. It shows the sales volume generated by the firm, direct and indirect

expenditure, gain and loss during the financial year. It indicates how the sales revenue are

transformed into net profit or loss. The primary purpose of this statement to represent the

business situation to investor whether it have profit or loss in a financial year. Whereas financial

statement are the accounts and reports that are prepared to present the financial condition in

front of management and user so management can make the final decision regarding the

formulation and implementation of the business strategies and investors can make decision

whether they wants to invest money in it or not (Gray, Coenenberg and Gordon, 2013). It

represent the financial performance of the particular firm over the certain time of period.

In order to comparison both the statement, Income statement shows the profitability of a

business organisation where financial statement represent the overall performance of the

company or financial aspect related to assets and liabilities. It also shows the financial position

and stability of the company in the market. The main distinguish between them financial sheet

represent overall business activities and aspects to the management and internal stakeholders

while income sheet shows sales and purchase data with the profitability. The comparison and

contrasting between the income statement and financial statement are made as follows:

Time period: For evaluation of the business position of assess and liabilities that is made

after considering business transaction of the current year on the particular date. Statement of

financial position are prepared after reviewing the transaction of the income statement. Income

statement is laying on the monthly basis, half yearly and yearly basis but the statement of

financial position are constructed on the particular date. It provides a overlook on the assets and

liabilities and owners capital at the time of reporting the financial statement.

Use for management: Management of a business firm uses the data from the financial

statement in order to compare the business position with previous year. By considering all the

data and facts from the statement they formulate the business strategies and implement it to see

the advanced result in the future. While income statement of the companies shows the profit and

loss that occur from conducted the business operations. Management of the firm makes the

decision regarding the short run by measuring the income statement (Gupta, 2016).

Content: In the financial statement, the item that are reported to business prospective are

assets, liabilities, equity capital, investment, long term loan at the particular period of time. In the

asset side, it is concluded in the statement of financial position of a firm such as fix assets,

investment and current assets. In the liabilities side, it contents equity share capital, retained

earnings, non current liabilities and current liabilities. But income statement have different items

in comparison to the financial statement that are as sales revenue, purchase, direct and indirect

expenses, opening and closing stock, profit or loss made during the year.

Users of statement: Basically the user of the financial statement of the condition of the

business are internal as well as external stakeholder of the company. fiscal statement represent

the information regarding monetary fund pattern, liquidity position, financial leverage. All these

represent the financial performance of the particular firm over the certain time of period.

In order to comparison both the statement, Income statement shows the profitability of a

business organisation where financial statement represent the overall performance of the

company or financial aspect related to assets and liabilities. It also shows the financial position

and stability of the company in the market. The main distinguish between them financial sheet

represent overall business activities and aspects to the management and internal stakeholders

while income sheet shows sales and purchase data with the profitability. The comparison and

contrasting between the income statement and financial statement are made as follows:

Time period: For evaluation of the business position of assess and liabilities that is made

after considering business transaction of the current year on the particular date. Statement of

financial position are prepared after reviewing the transaction of the income statement. Income

statement is laying on the monthly basis, half yearly and yearly basis but the statement of

financial position are constructed on the particular date. It provides a overlook on the assets and

liabilities and owners capital at the time of reporting the financial statement.

Use for management: Management of a business firm uses the data from the financial

statement in order to compare the business position with previous year. By considering all the

data and facts from the statement they formulate the business strategies and implement it to see

the advanced result in the future. While income statement of the companies shows the profit and

loss that occur from conducted the business operations. Management of the firm makes the

decision regarding the short run by measuring the income statement (Gupta, 2016).

Content: In the financial statement, the item that are reported to business prospective are

assets, liabilities, equity capital, investment, long term loan at the particular period of time. In the

asset side, it is concluded in the statement of financial position of a firm such as fix assets,

investment and current assets. In the liabilities side, it contents equity share capital, retained

earnings, non current liabilities and current liabilities. But income statement have different items

in comparison to the financial statement that are as sales revenue, purchase, direct and indirect

expenses, opening and closing stock, profit or loss made during the year.

Users of statement: Basically the user of the financial statement of the condition of the

business are internal as well as external stakeholder of the company. fiscal statement represent

the information regarding monetary fund pattern, liquidity position, financial leverage. All these

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

detail are help to make the financial decision regarding the future. User of the financial statement

are supplier, investor, government, creditors etc. They all are external user of data related to

financial statement. They make detail analysis of the company's data and invest accordingly

(Ball, 2013). Data of Income statement are useful to management in order to prepare the

financial statement and make a comparative analysis of the sales revenue and profit of the

business.

Question - 04

Bank reconciliation statement

Bank reconciliation sheet is process that refers to variances between cash book bank's

column and bank pass book entries on a particular date. It shows the differences between balance

of the cash book and banks entries. All these variances hurdles are solved by preparing the bank-

reconciliation statement. The main purpose of the making the bank-reconciliation statement is to

ascertained difference that creates issue in determined the closing cash books and match the

balances of both cash and pass book entries (Bryer, 2013). It recognize the error in transactions

balance that are related to bank, error of omission, hidden charges related to bank. To

rectification of the bank transaction it is necessaries to prepare this sheet.

Process of bank reconciliation- To make a this statement, It is required to follow some step

which are as follows:

Determining the variances between cash account and bank account's statement- In the

process of the bank reconciliation, The first process is ascertain the differences between

cash transaction with bank details and differences amount entry should be made in this

statement.

Find out the cash entries records that are not present in the discloser of bank account- The

further process is to find out the cash transaction that are not available in the bank

statement. These transaction are really helpful in making the Bank reconciliation

statement.

Making the adjustment with those transaction that are not present in the cash ledger- In

order to making the bank transaction with the help of books of books of account. The

items are such as bank charges, interest on deposited money, interest on overhead.

Formation of bank-reconciliation statement by adjusting those transaction that makes the

difference – By considering all the above mention points, In the formulation of the this

are supplier, investor, government, creditors etc. They all are external user of data related to

financial statement. They make detail analysis of the company's data and invest accordingly

(Ball, 2013). Data of Income statement are useful to management in order to prepare the

financial statement and make a comparative analysis of the sales revenue and profit of the

business.

Question - 04

Bank reconciliation statement

Bank reconciliation sheet is process that refers to variances between cash book bank's

column and bank pass book entries on a particular date. It shows the differences between balance

of the cash book and banks entries. All these variances hurdles are solved by preparing the bank-

reconciliation statement. The main purpose of the making the bank-reconciliation statement is to

ascertained difference that creates issue in determined the closing cash books and match the

balances of both cash and pass book entries (Bryer, 2013). It recognize the error in transactions

balance that are related to bank, error of omission, hidden charges related to bank. To

rectification of the bank transaction it is necessaries to prepare this sheet.

Process of bank reconciliation- To make a this statement, It is required to follow some step

which are as follows:

Determining the variances between cash account and bank account's statement- In the

process of the bank reconciliation, The first process is ascertain the differences between

cash transaction with bank details and differences amount entry should be made in this

statement.

Find out the cash entries records that are not present in the discloser of bank account- The

further process is to find out the cash transaction that are not available in the bank

statement. These transaction are really helpful in making the Bank reconciliation

statement.

Making the adjustment with those transaction that are not present in the cash ledger- In

order to making the bank transaction with the help of books of books of account. The

items are such as bank charges, interest on deposited money, interest on overhead.

Formation of bank-reconciliation statement by adjusting those transaction that makes the

difference – By considering all the above mention points, In the formulation of the this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

detailed sheet the bank transaction must be included in the cash book which are presented

in the bank accounts (Chiang, Nouri and Samanta, 2014). To make the entries that are not

presented in the cash books or that makes the changes in bank and cash book, It is

required to make adjustment by differences amount.

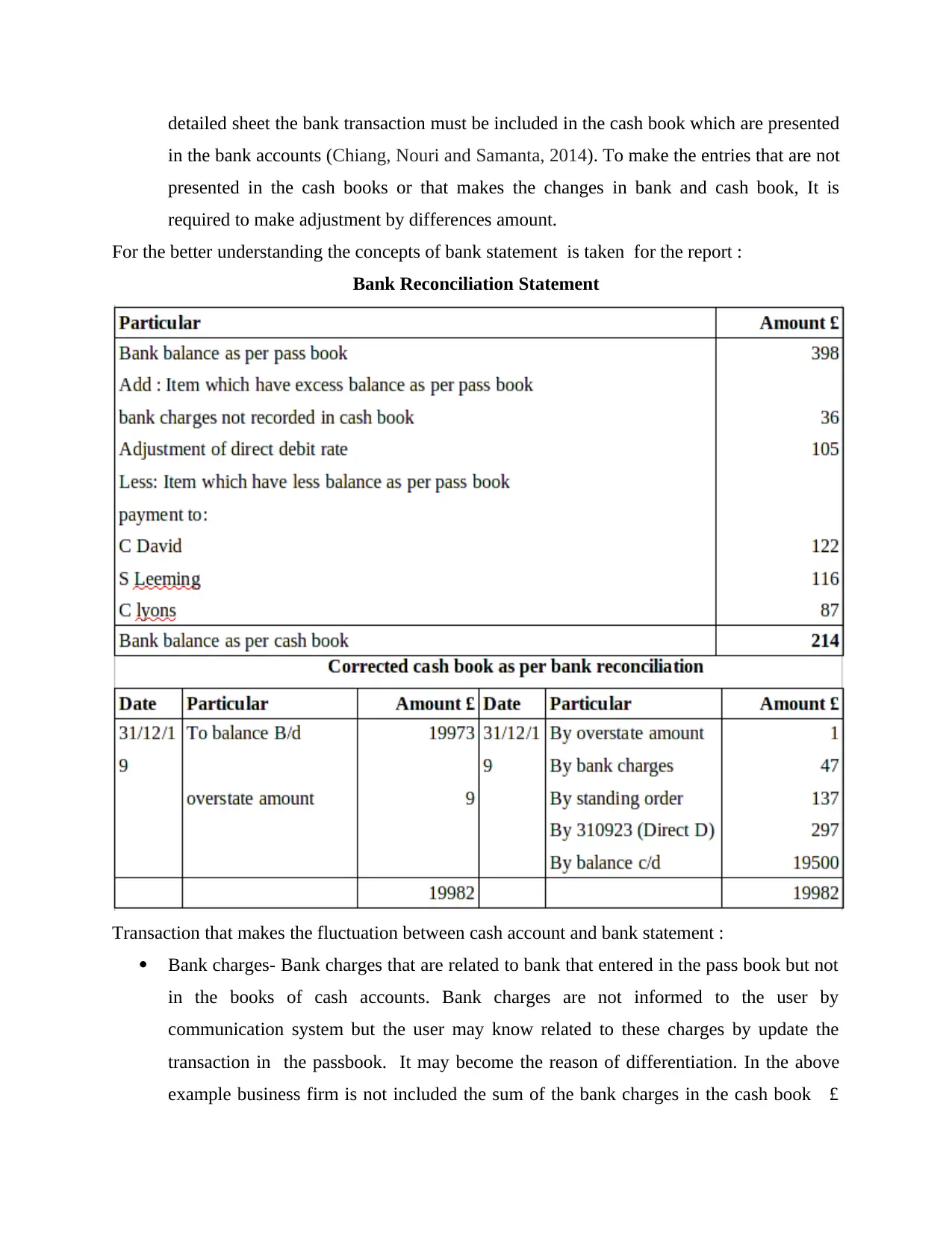

For the better understanding the concepts of bank statement is taken for the report :

Bank Reconciliation Statement

Transaction that makes the fluctuation between cash account and bank statement :

Bank charges- Bank charges that are related to bank that entered in the pass book but not

in the books of cash accounts. Bank charges are not informed to the user by

communication system but the user may know related to these charges by update the

transaction in the passbook. It may become the reason of differentiation. In the above

example business firm is not included the sum of the bank charges in the cash book £

in the bank accounts (Chiang, Nouri and Samanta, 2014). To make the entries that are not

presented in the cash books or that makes the changes in bank and cash book, It is

required to make adjustment by differences amount.

For the better understanding the concepts of bank statement is taken for the report :

Bank Reconciliation Statement

Transaction that makes the fluctuation between cash account and bank statement :

Bank charges- Bank charges that are related to bank that entered in the pass book but not

in the books of cash accounts. Bank charges are not informed to the user by

communication system but the user may know related to these charges by update the

transaction in the passbook. It may become the reason of differentiation. In the above

example business firm is not included the sum of the bank charges in the cash book £

36. so in preparing the bank-reconciliation statement it is included (Hope, Thomas and

Vyas, 2013).

Interest on deposited money - Bank provides the interest on the capital that is deposited

with bank. It may causes the difference between cash and pass book of accounts. It is

reflected in the records of the bank pass book but not in the books of accounts.

Interest on overhead – bank charges the interest on the withdrawal of the excess money

out of deposited in the bank. When business owner is required the urgent money they can

withdraw from bank and bank charges the specific interest on it. This interest makes the

difference between bank and cash book transaction.

Outstanding cheques that is in the process of banking system such as cheque truncation

system become the reason.

Uncleared cheques due to insufficient amount in the bank may be reason.

A situation where cheques issued by the debtors of the business firm but deposited in the

bank to clear it makes the reason of difference between cash sheet and bank statement:.

It verify the general business accounts and the balance sheet items. Bank reconciliation statement

is prepared to compare the bank account records and general business transaction that are based

on cash account. It match the general item and bank statement of a business to ascertain the true

cash balance in the business. These variation may happens due to outstanding cheques and

deposit that are in process in the bank. It is find out the error that is made by management to

record the transaction. Once all the transaction are reconcile in the cash book, general ledger and

balance sheet should match.

All the transaction that makes the difference in the bank sheet and cash transaction of a

firm can be reconcile by making the this statement and record the transaction by difference

amount by considering both statement. It will help in match the cash and bank transaction by

considering all the data related to bank pass book. For example amount of interest on overhead is

not included in the cash book of a firm but entered in the bank pass book, the bank reconcile

sheet allows the changes of account and match the balance of both account by making a entry

related to interest on overhead in the cash book. So it help in the match the balance to reconciled.

Vyas, 2013).

Interest on deposited money - Bank provides the interest on the capital that is deposited

with bank. It may causes the difference between cash and pass book of accounts. It is

reflected in the records of the bank pass book but not in the books of accounts.

Interest on overhead – bank charges the interest on the withdrawal of the excess money

out of deposited in the bank. When business owner is required the urgent money they can

withdraw from bank and bank charges the specific interest on it. This interest makes the

difference between bank and cash book transaction.

Outstanding cheques that is in the process of banking system such as cheque truncation

system become the reason.

Uncleared cheques due to insufficient amount in the bank may be reason.

A situation where cheques issued by the debtors of the business firm but deposited in the

bank to clear it makes the reason of difference between cash sheet and bank statement:.

It verify the general business accounts and the balance sheet items. Bank reconciliation statement

is prepared to compare the bank account records and general business transaction that are based

on cash account. It match the general item and bank statement of a business to ascertain the true

cash balance in the business. These variation may happens due to outstanding cheques and

deposit that are in process in the bank. It is find out the error that is made by management to

record the transaction. Once all the transaction are reconcile in the cash book, general ledger and

balance sheet should match.

All the transaction that makes the difference in the bank sheet and cash transaction of a

firm can be reconcile by making the this statement and record the transaction by difference

amount by considering both statement. It will help in match the cash and bank transaction by

considering all the data related to bank pass book. For example amount of interest on overhead is

not included in the cash book of a firm but entered in the bank pass book, the bank reconcile

sheet allows the changes of account and match the balance of both account by making a entry

related to interest on overhead in the cash book. So it help in the match the balance to reconciled.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.