Financial Accounting Analysis: Trial Balance, Statements, and Ratios

VerifiedAdded on 2023/01/11

|27

|4293

|40

Homework Assignment

AI Summary

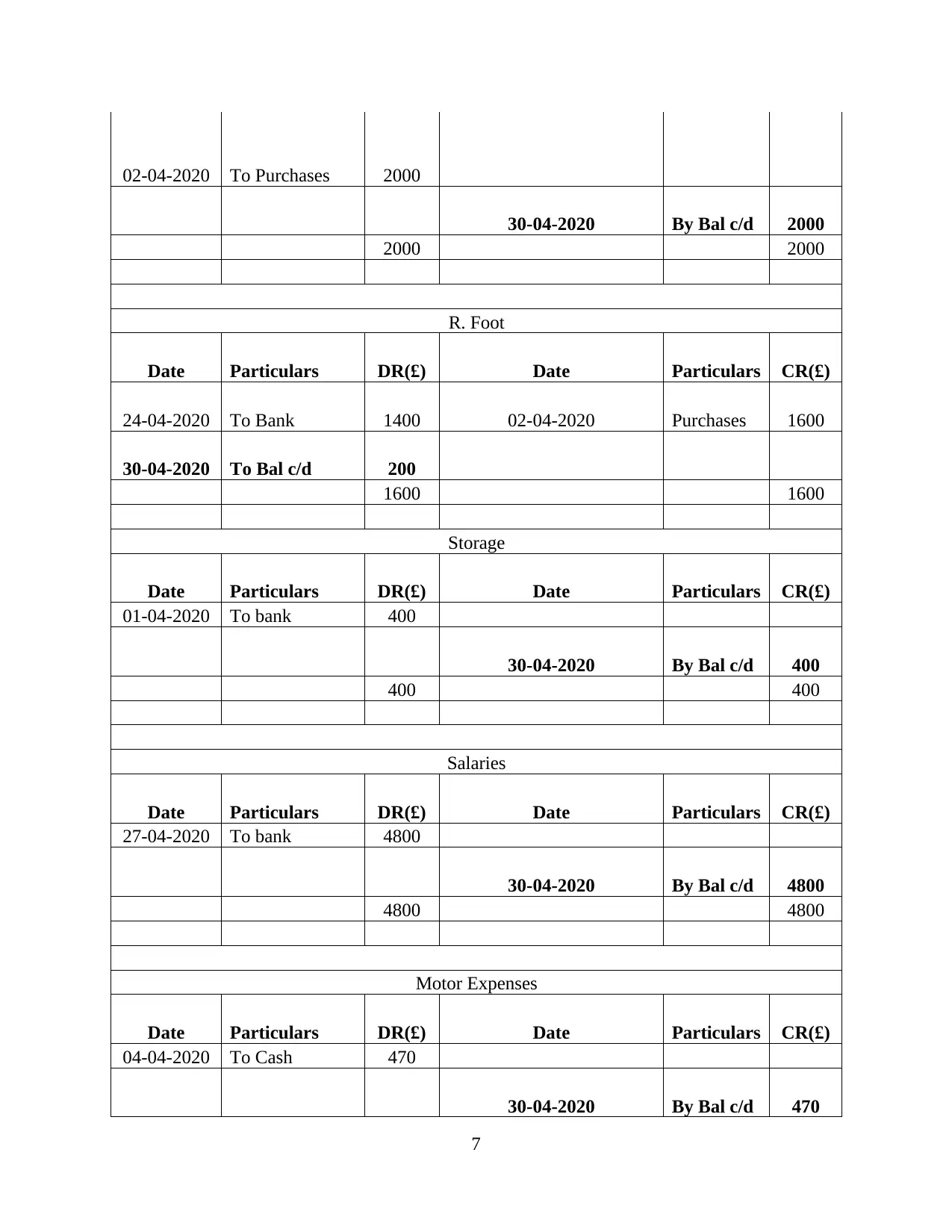

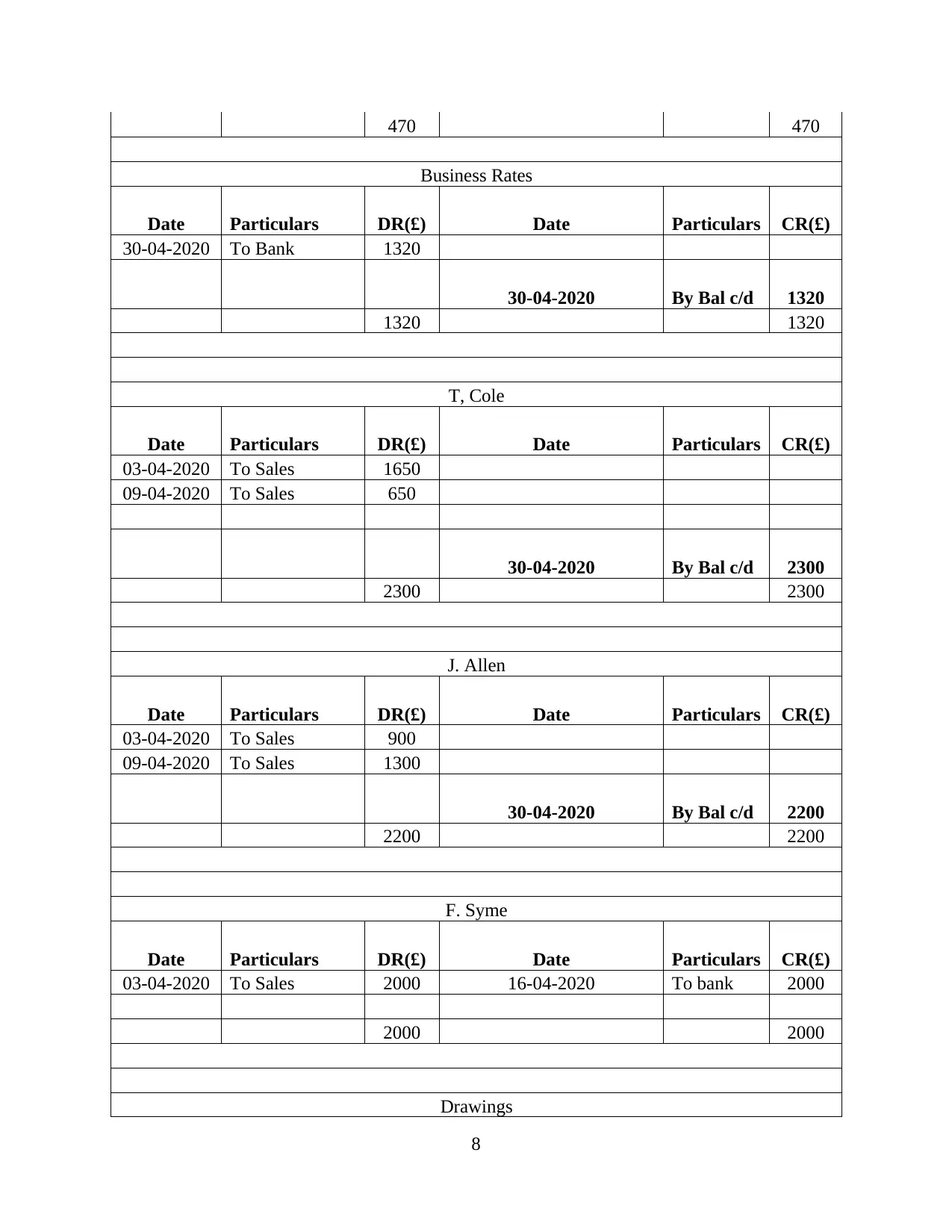

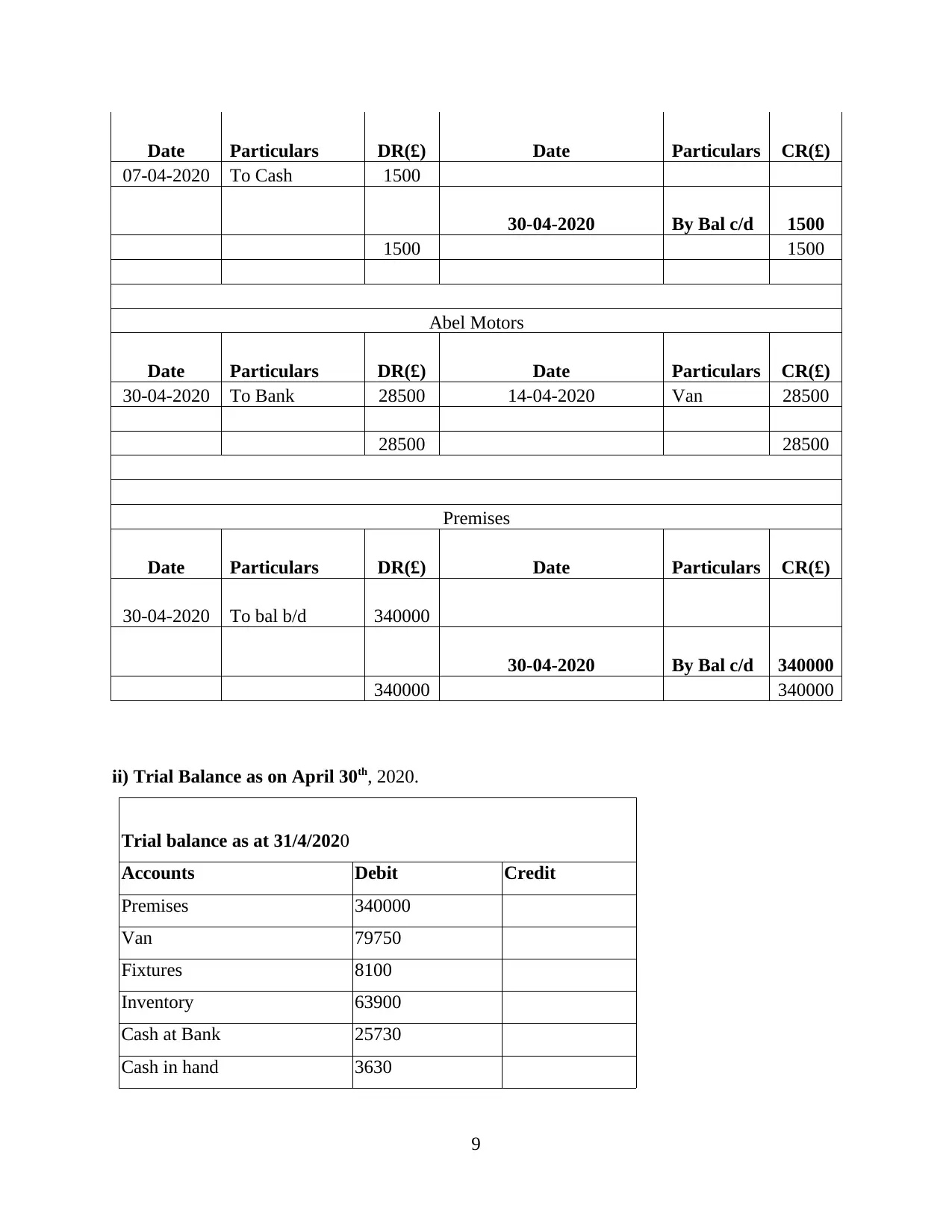

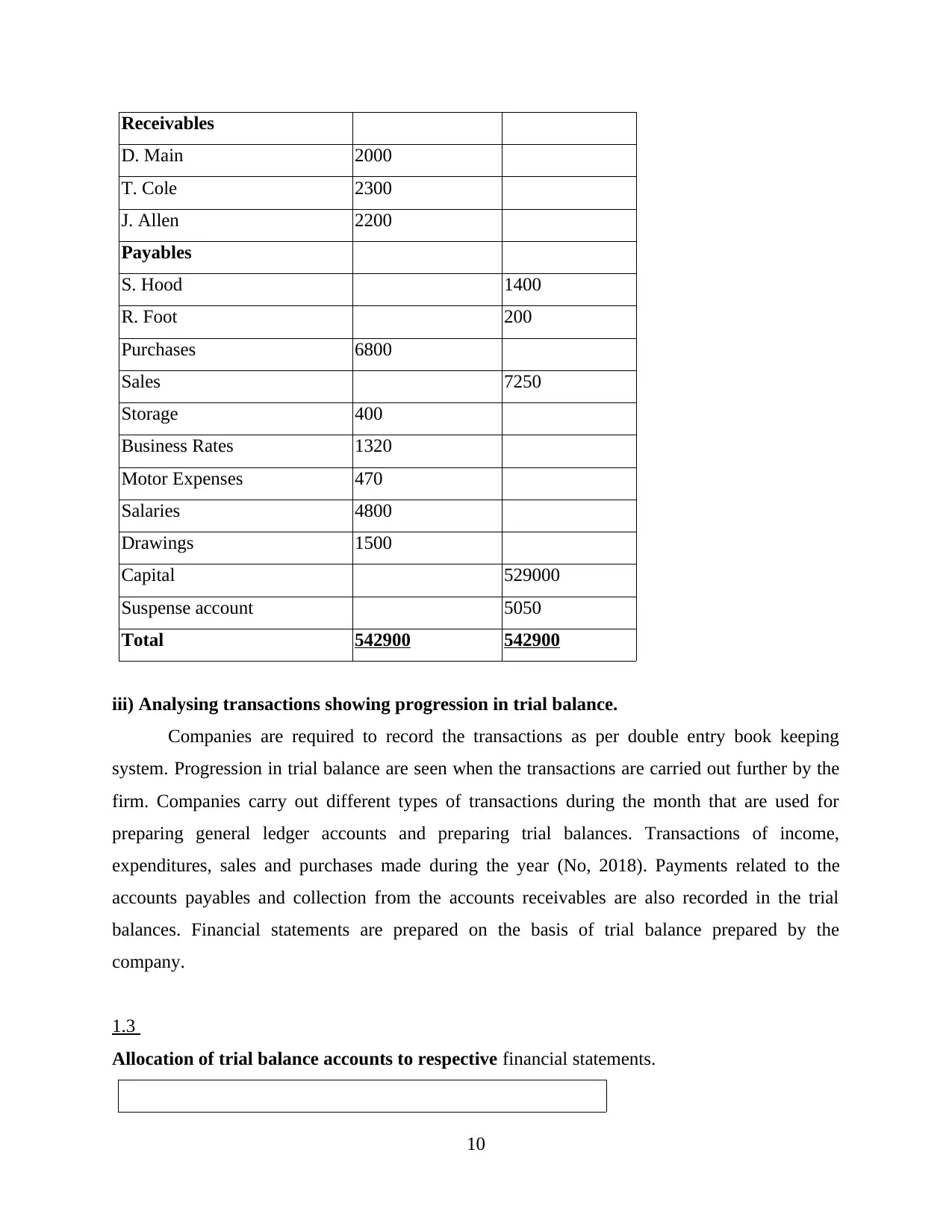

This financial accounting assignment provides a comprehensive analysis of key accounting principles and practices. It begins with a trial balance, demonstrating the application of the double-entry system to record business transactions. The assignment includes journal entries, ledger accounts, and a revised trial balance. It then delves into the different types of financial accounting statements, including income statements, balance sheets, and cash flow statements, with examples and explanations of their purpose and content. The report includes a detailed statement of financial position and concludes with a ratio analysis, evaluating the company's financial health and performance. The assignment covers topics such as financial accounting, trial balance, double entry system, financial statements, and ratio analysis.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.