University Assignment: GlaxoSmithKline Financial Ratio Analysis

VerifiedAdded on 2021/04/24

|10

|1612

|33

Report

AI Summary

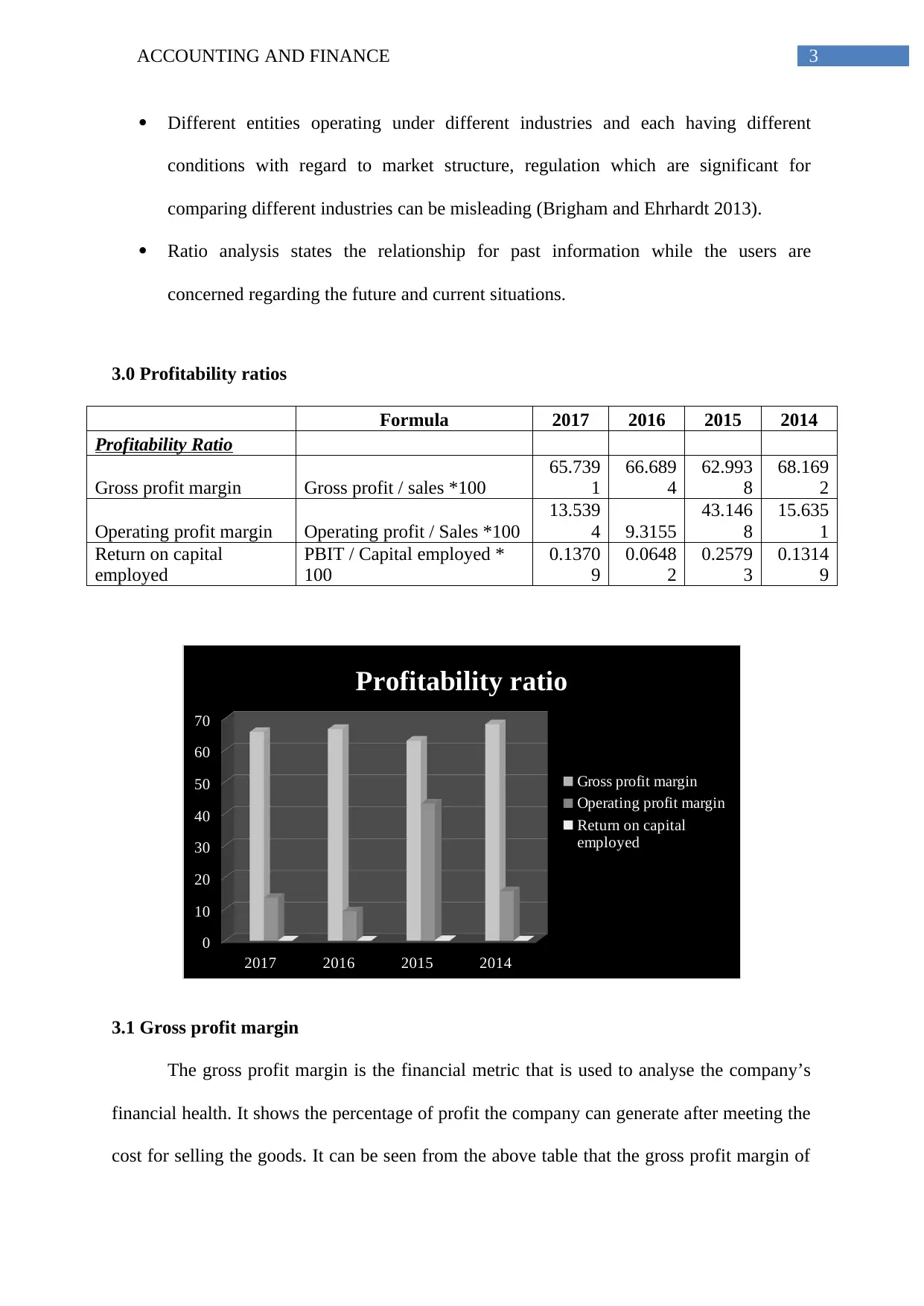

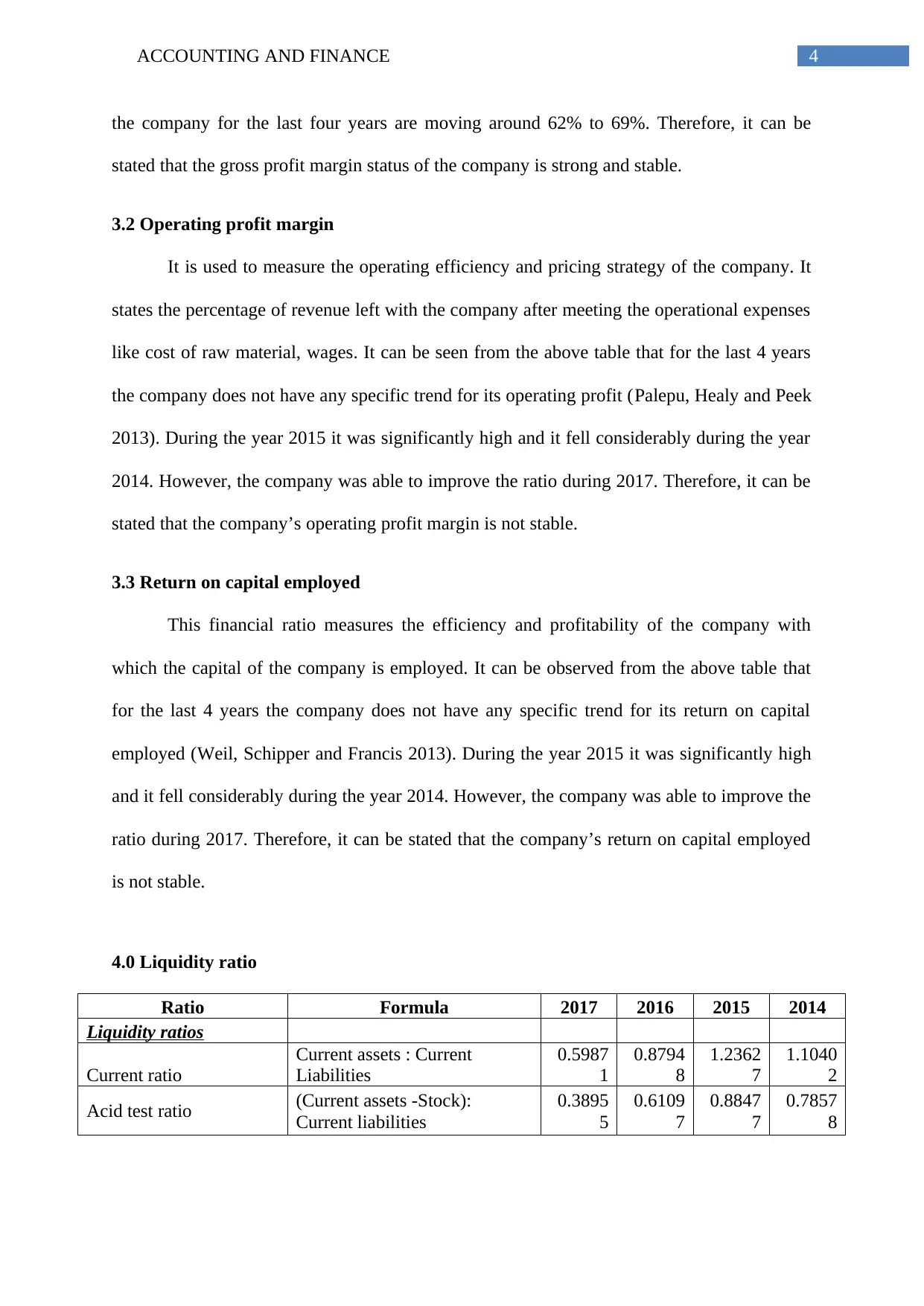

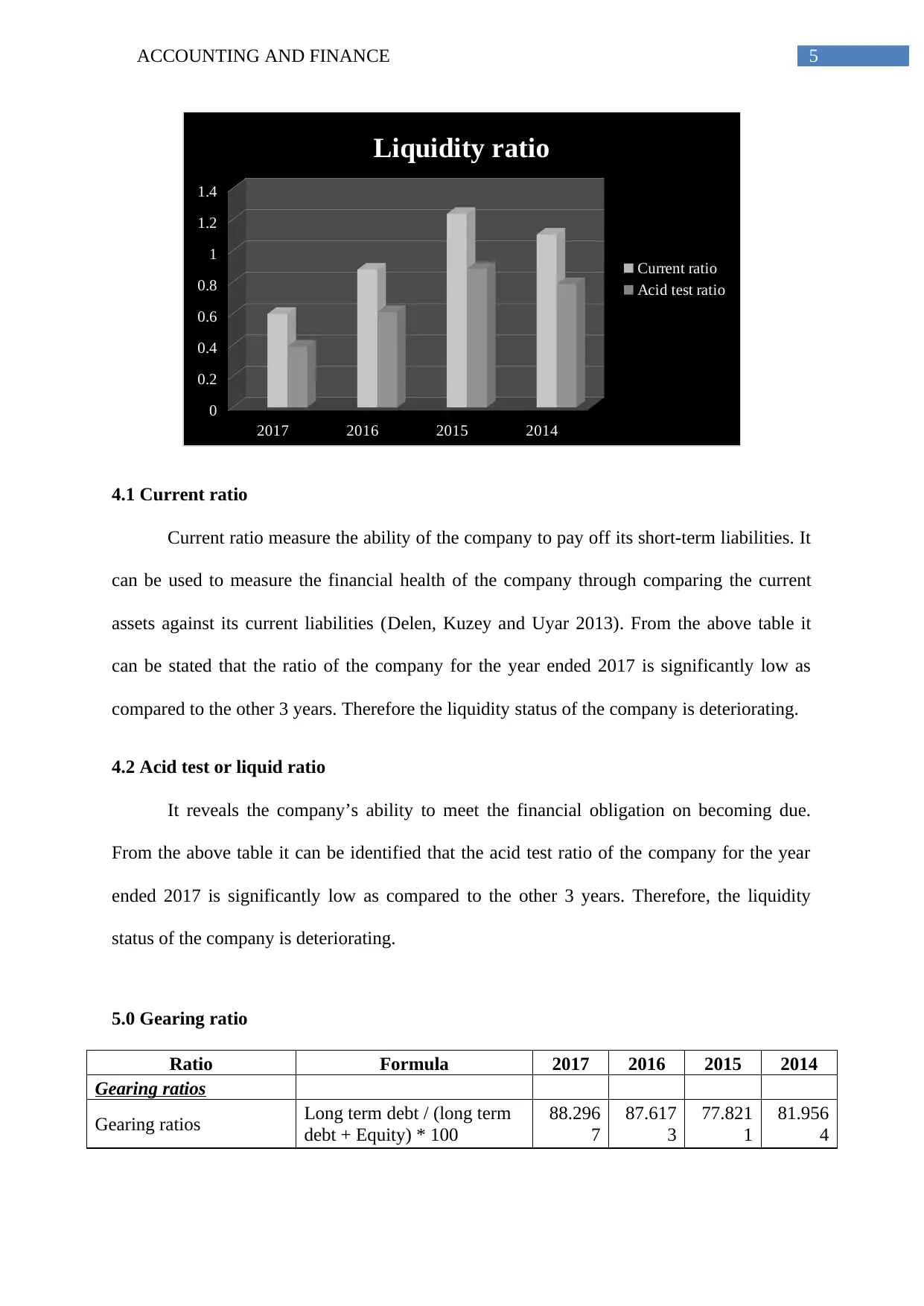

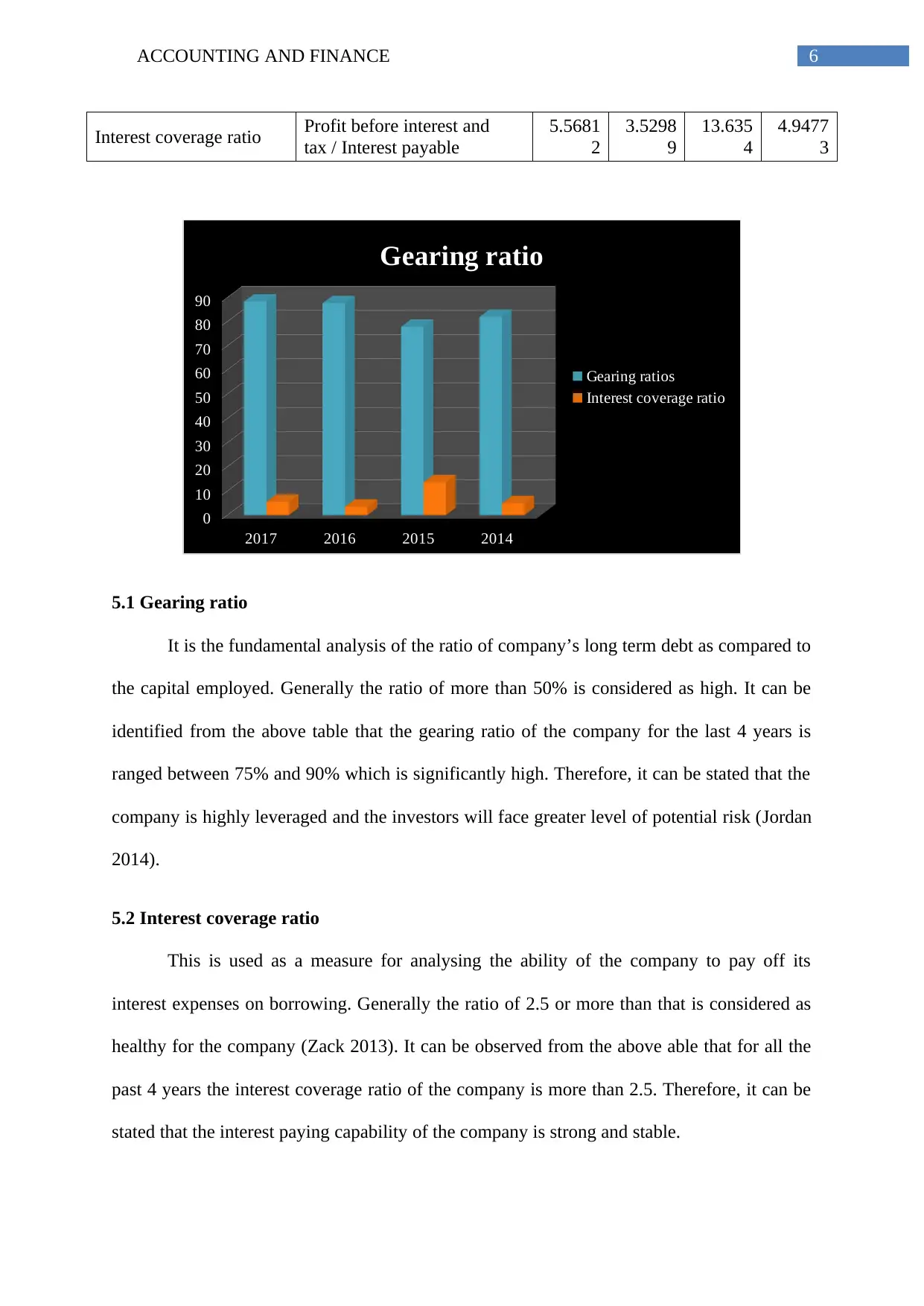

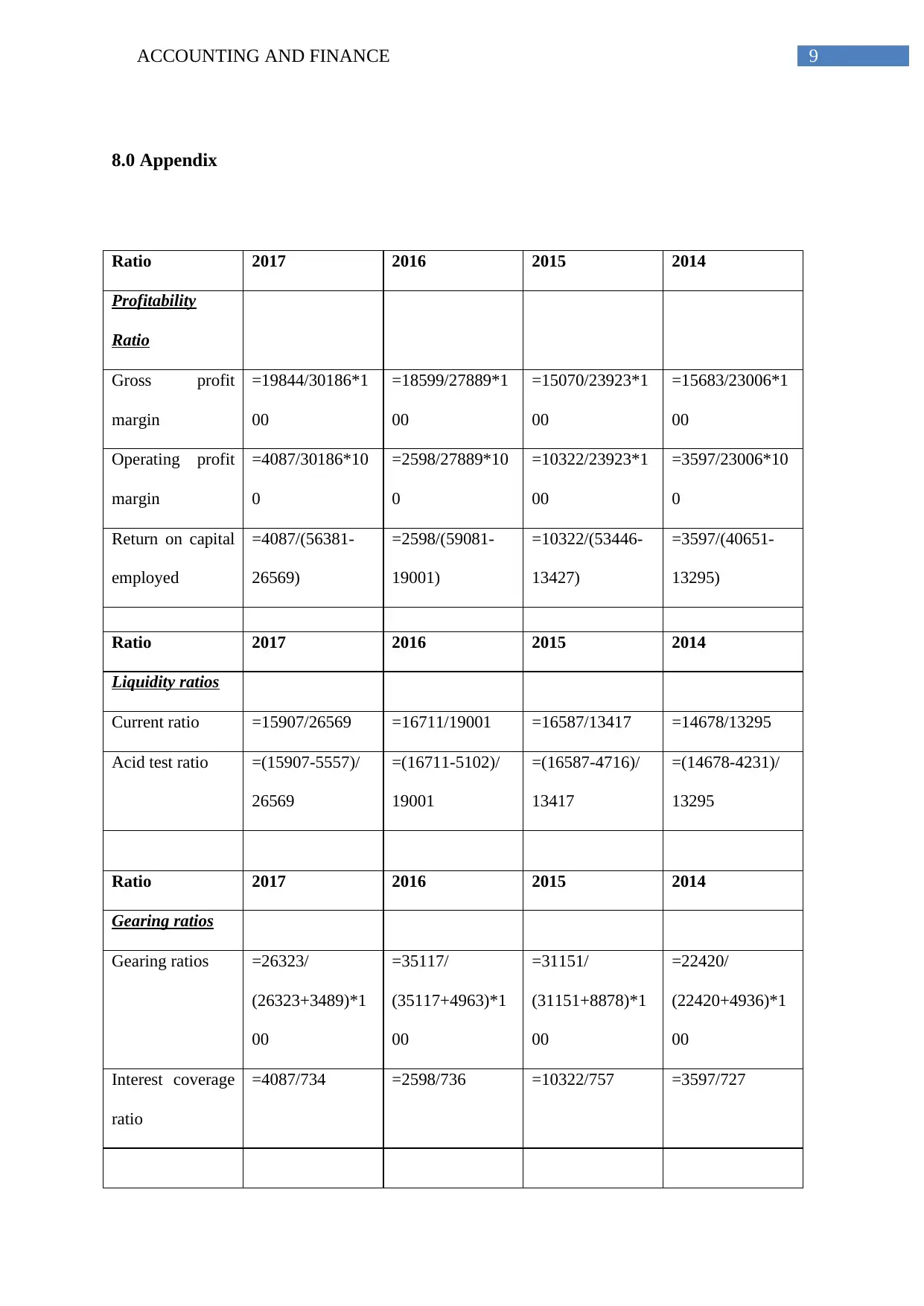

This report provides a comprehensive financial ratio analysis of GlaxoSmithKline (GSK), a major pharmaceutical company, from 2014 to 2017. The analysis covers various aspects of GSK's financial health, including profitability, liquidity, and gearing ratios. Profitability ratios such as gross profit margin, operating profit margin, and return on capital employed are examined to assess the company's efficiency in generating profits. Liquidity ratios, including the current ratio and acid-test ratio, are used to evaluate GSK's ability to meet short-term obligations. Gearing ratios, such as the gearing ratio and interest coverage ratio, are analyzed to assess the company's leverage and its ability to manage debt. The report concludes with a summary of GSK's financial strengths and weaknesses based on the ratio analysis, highlighting areas where the company excels and areas needing improvement. The report also includes detailed calculations and formulas for each ratio, providing a clear understanding of the analysis process.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.