Finance for Decision Making Report: Greengrass Ltd. Analysis

VerifiedAdded on 2022/11/29

|7

|1187

|157

Report

AI Summary

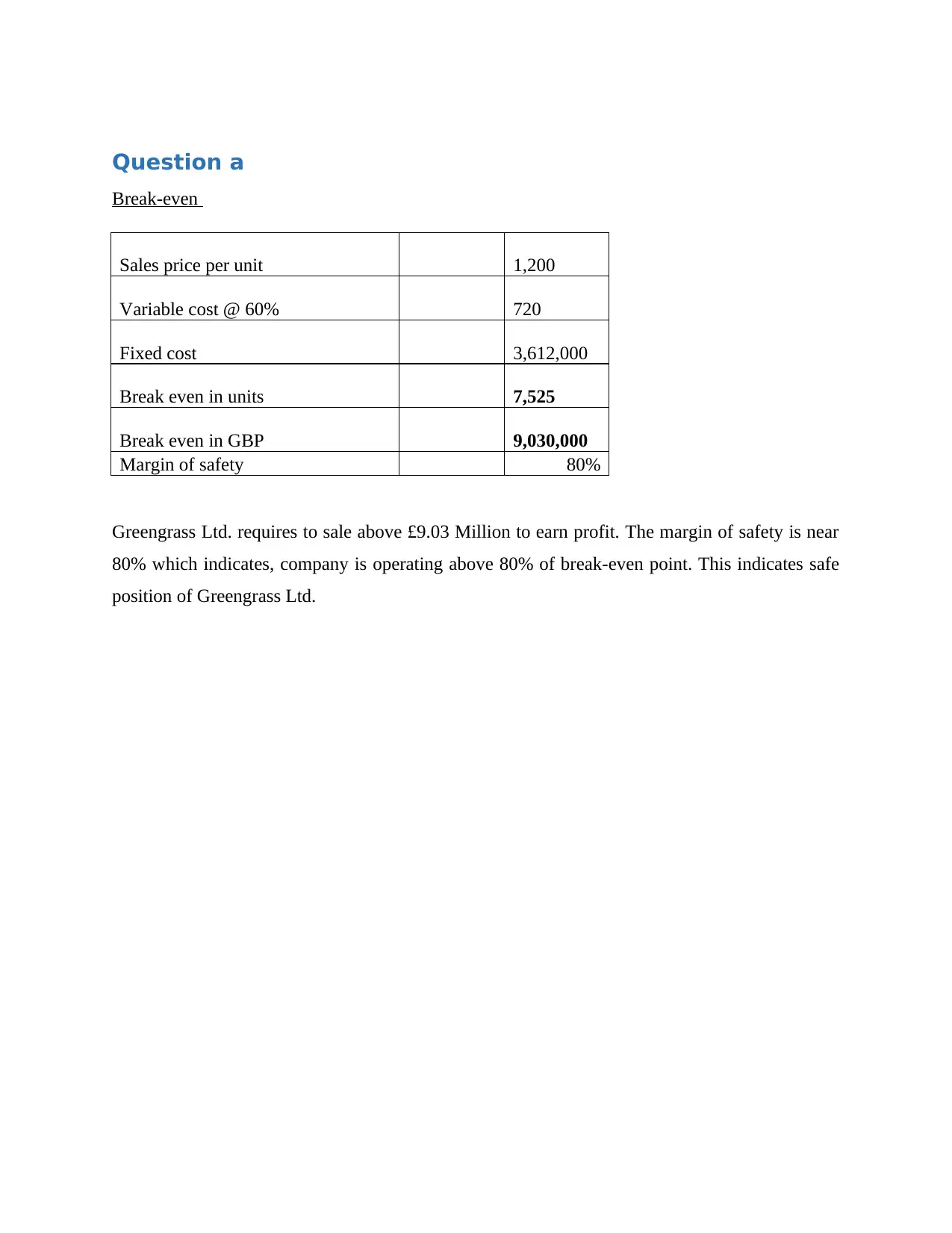

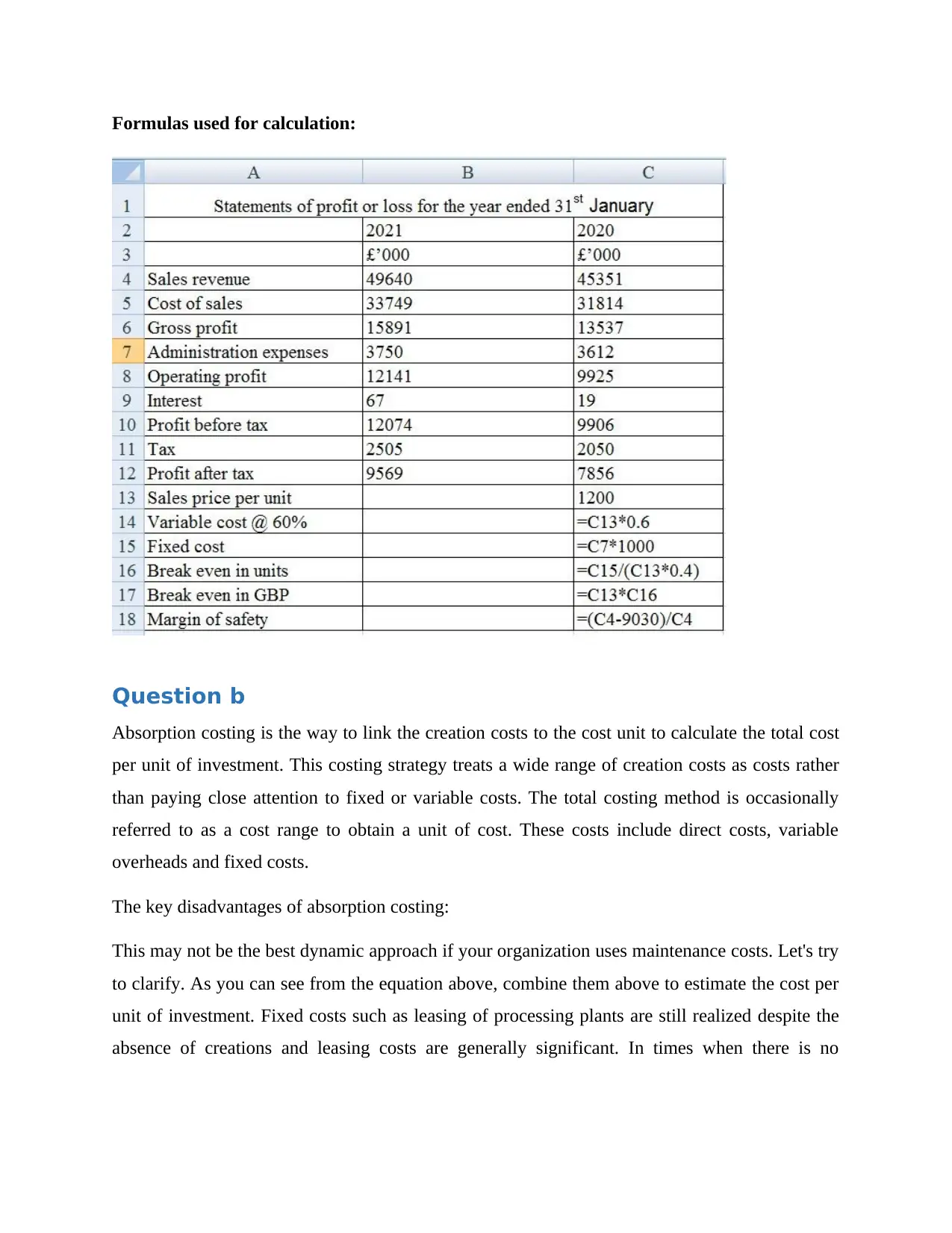

This finance report analyzes the financial performance of Greengrass Ltd., a company manufacturing robotic lawnmowers. The report includes a break-even analysis, calculating the break-even sales price per unit, break-even in units, and the margin of safety, revealing the company's safe operational position. It then delves into absorption costing, outlining its advantages and disadvantages, and compares it with activity-based costing (ABC), highlighting the benefits of ABC in terms of cost accuracy, cost behavior data, and cost management. The report also assesses the impact of current pricing strategies on sales revenue and discusses key financial performance indicators (KPIs) and selective performance measures (APMs), providing a comprehensive overview of the company's financial health and strategic insights for decision-making. The report is based on the provided assignment brief which includes details about the company and its products.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.