Taxation Law: HI3042 Individual Assignment T2 2017 - Deductions & GST

VerifiedAdded on 2020/04/07

|7

|1388

|476

Homework Assignment

AI Summary

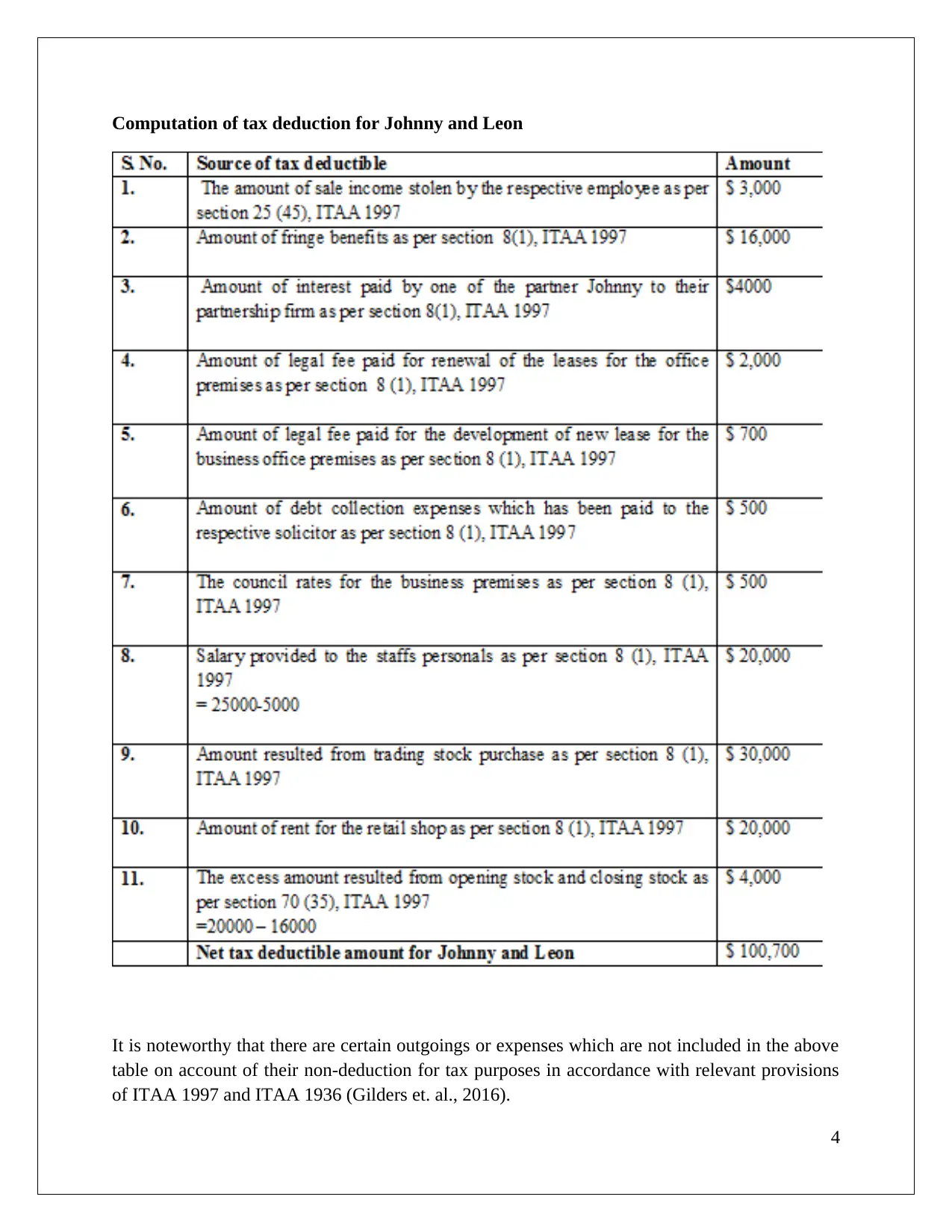

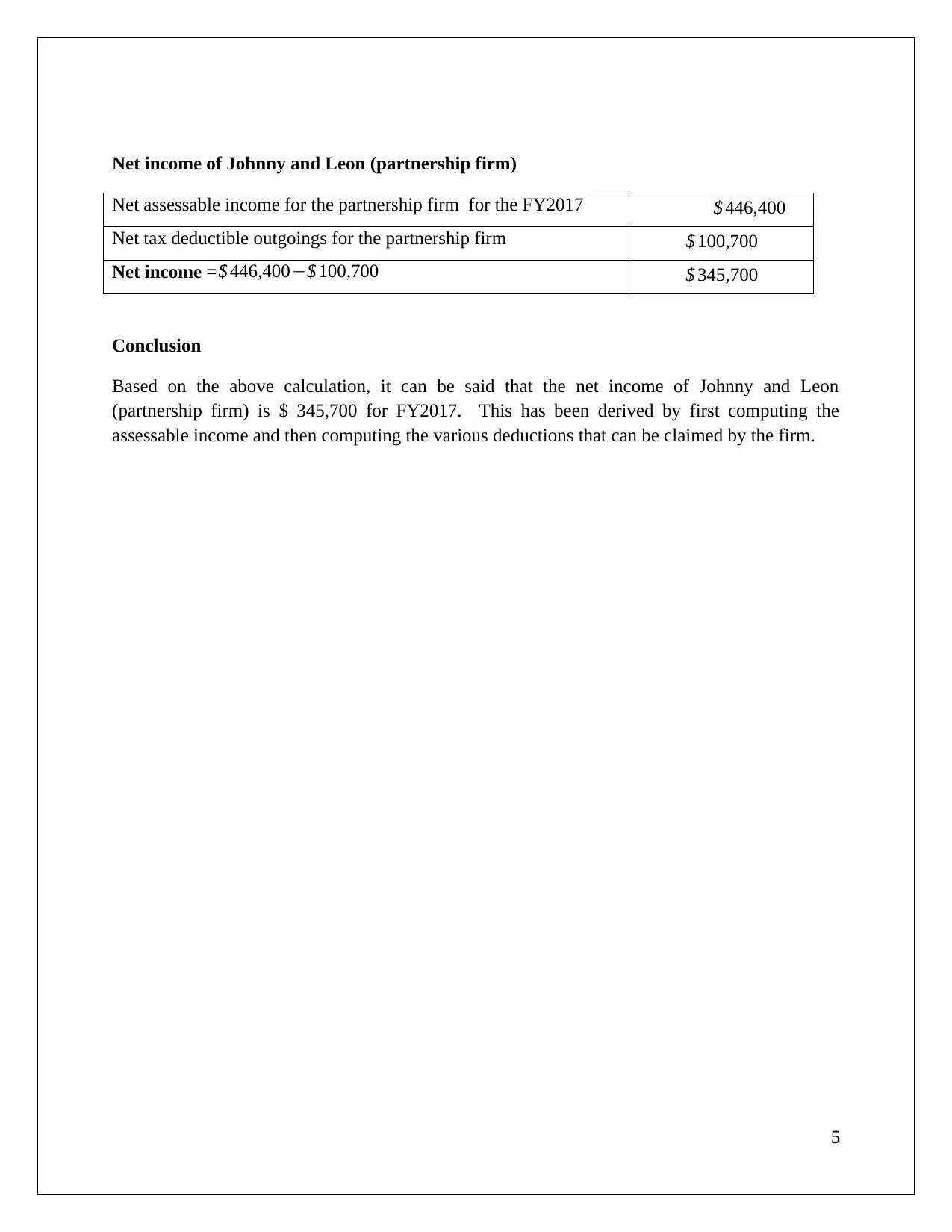

This taxation law assignment solution addresses key concepts including tax deductions under section 8-1 of the ITAA 1997, GST input tax credits, and the calculation of net income for a partnership firm. The assignment analyzes the deductibility of various expenses, such as machine relocation, asset revaluation, and legal fees, considering their nature (capital or revenue) and relevance to business operations. It also examines the application of GST principles, particularly the Financial Acquisition Threshold (FAT), to determine the availability of input tax credits on advertising expenses. Furthermore, the solution provides a detailed computation of the partnership's net income, incorporating assessable income and tax deductions to arrive at the final figure. References to relevant case law and tax legislation are included to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.