HI5020 Corporate Accounting: Woolworths Limited Cash Flow Statement

VerifiedAdded on 2023/06/13

|10

|2714

|103

Report

AI Summary

This report provides a detailed financial statement analysis of Woolworths Limited, focusing on the cash flow statement, other comprehensive income, and corporate income tax disclosures. The analysis of the cash flow statement includes a breakdown of cash inflows and outflows from operating, investing, and financing activities, with a comparative analysis across three years (2015-2017) highlighting trends and potential areas of concern. The report also examines the components of other comprehensive income, such as hedging reserves and foreign currency translation, explaining their significance. Finally, the report analyzes the company's income tax expense, considering both the expense reported and the actual tax paid, with reference to the notes in the financial statements. The report concludes with a summary of key findings and recommendations based on the analysis. Desklib provides access to this and many other solved assignments for students.

CORPORATE ACCOUNTING –FINANCIAL STATEMENT ANALYSIS

Student Name:

Student ID:

2018

Woolworths Limited

Student Name:

Student ID:

2018

Woolworths Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

DETAILS OF COMPANY SELECTED................................................................................................................2

ANALYSIS OF THE CASH FLOW STATEMENT................................................................................................2

ANALYSIS OF OTHER COMPREHENSIVE INCOME.........................................................................................2

ANALYSIS OF CORPORATE INCOME TAX......................................................................................................2

CONCLUSION AND RECOMMENDATION.....................................................................................................2

REFERENCES................................................................................................................................................2

EXECUTIVE SUMMARY

The health of every company is judged with the help of the annual report of the company and

therefore it becomes very necessary for the company to have the data in the annual report as true

and correct and shall not in any manner provide the inaccurate results. The annual report of every

company includes the set of the statements for the purpose of providing the useful information.

This report has come up with objectives. One of the main aims of this report is to understand the

different heads of the statement of the cash flows and analysis of the same has been done. The

second main aim is to understand the need of preparing the statement showing the other

comprehensive income and how the same is represented. The third and the last aim are to know

how the company discloses the tax expenditure in its books of accounts and the financial

statements thereon. Keeping in consideration the effect and the impact of aforesaid aims, the

report is being prepared and has been appropriately presented with the headings and sub

headings wherever required.

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

DETAILS OF COMPANY SELECTED................................................................................................................2

ANALYSIS OF THE CASH FLOW STATEMENT................................................................................................2

ANALYSIS OF OTHER COMPREHENSIVE INCOME.........................................................................................2

ANALYSIS OF CORPORATE INCOME TAX......................................................................................................2

CONCLUSION AND RECOMMENDATION.....................................................................................................2

REFERENCES................................................................................................................................................2

EXECUTIVE SUMMARY

The health of every company is judged with the help of the annual report of the company and

therefore it becomes very necessary for the company to have the data in the annual report as true

and correct and shall not in any manner provide the inaccurate results. The annual report of every

company includes the set of the statements for the purpose of providing the useful information.

This report has come up with objectives. One of the main aims of this report is to understand the

different heads of the statement of the cash flows and analysis of the same has been done. The

second main aim is to understand the need of preparing the statement showing the other

comprehensive income and how the same is represented. The third and the last aim are to know

how the company discloses the tax expenditure in its books of accounts and the financial

statements thereon. Keeping in consideration the effect and the impact of aforesaid aims, the

report is being prepared and has been appropriately presented with the headings and sub

headings wherever required.

INTRODUCTION

Financial report is prepared by the company in an accurate manner. The reason is that through

the financial report only the stakeholders of the company can take the better and the informed

decision. If the financial report does not provide the full disclosure of the affairs of the company

then the stakeholders of the company will not be able to take the informed and the useful

decision. The title of the report is financial statement analysis. It is evident from the title that the

analysis is required to be done and majorly for the purpose of this report only three statements

have been considered and analysed in detail. These are the statement which depicts what are the

cash inflows and outflows of the company, the statement which considers the items which are

not the part of the profit and loss account and thus forms the part of the statement of the other

comprehensive income and lastly the disclosure about the tax expense of the company. For the

first head of the statement, all the items contained therein along whether minor or major has been

detailed. Major heads are the operating, financing and investing activities and the minor heads

are the items contained therein. In the second statement the heads have been considered and

explained in detail and it is discussed as to why the items contained therein does not forms part

of the statement of the profit and loss account and lastly the notes of the financial statements

have been analysed with respect to the income tax expense as reported. Tax expense has been

discussed with reference to the expense reported and paid. Then at the end the concluding

paragraph has been given in order to bring an end to the report by summarizing all the relevant

facts.

COMPANY’S DESCRIPTION

For the furtherance of this report to achieve the aim, the company – Woolworths Limited as been

defined and considered. The company is the registered company having its office in Australia,

Woolworth road. The company is also a registered entity in the stock exchange of Australia. The

company is into the sector of the retail and has been providing the various products to the

customers across the countries of Australia and New Zealand. It basically has the chains of the

supermarket which is working very effectively making the company as the second largest

company in the retail sector in Australia and has been delivering the valuable services to all the

customers of the company. For the purpose of making the analysis, the annual report for the year

Financial report is prepared by the company in an accurate manner. The reason is that through

the financial report only the stakeholders of the company can take the better and the informed

decision. If the financial report does not provide the full disclosure of the affairs of the company

then the stakeholders of the company will not be able to take the informed and the useful

decision. The title of the report is financial statement analysis. It is evident from the title that the

analysis is required to be done and majorly for the purpose of this report only three statements

have been considered and analysed in detail. These are the statement which depicts what are the

cash inflows and outflows of the company, the statement which considers the items which are

not the part of the profit and loss account and thus forms the part of the statement of the other

comprehensive income and lastly the disclosure about the tax expense of the company. For the

first head of the statement, all the items contained therein along whether minor or major has been

detailed. Major heads are the operating, financing and investing activities and the minor heads

are the items contained therein. In the second statement the heads have been considered and

explained in detail and it is discussed as to why the items contained therein does not forms part

of the statement of the profit and loss account and lastly the notes of the financial statements

have been analysed with respect to the income tax expense as reported. Tax expense has been

discussed with reference to the expense reported and paid. Then at the end the concluding

paragraph has been given in order to bring an end to the report by summarizing all the relevant

facts.

COMPANY’S DESCRIPTION

For the furtherance of this report to achieve the aim, the company – Woolworths Limited as been

defined and considered. The company is the registered company having its office in Australia,

Woolworth road. The company is also a registered entity in the stock exchange of Australia. The

company is into the sector of the retail and has been providing the various products to the

customers across the countries of Australia and New Zealand. It basically has the chains of the

supermarket which is working very effectively making the company as the second largest

company in the retail sector in Australia and has been delivering the valuable services to all the

customers of the company. For the purpose of making the analysis, the annual report for the year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ending two thousand and seventeen, two thousand and sixteen and two thousand and fifteen has

been considered.

STATEMENT OF CASH FLOWS – AN ANALYSIS

The inflows of the cash and the outflows of the cash are mentioned in the statement showing the

flows of cash during the year. The statement is prepared by considering the three main activities

around which the company works which includes the operating, investing and financing. There

are many items under each of the major head and these have been discussed in detail in the

following paragraphs.

Description of each head

In the statement of the cash flows there are many items present which have been detailed below

and analysed in regard to the meaning and treatment:

First item of the statement of the cash flow is the cash which is received from the

customers. It is the amount which the company receives from the customers of the

company to whom the products of the company has been sold. The cash received from

the customers have been increased slightly by one hundred and sixty nine dollars from

2016 to the year of 2017.

Second major item is the payment which the company pays to the person from whom the

company purchases the goods. Also the payment which is made to the employees in lieu

of the services made has been considered under this minor head. This head represents the

amount of the outflow that the company made in making the payments as required. It is

explicit that the amount of outflow has been decreased by three hundred sixty million

dollar.

Third major and the most considerable item is the amount of income tax. It is the amount

which is paid by the company on the taxable income of the company. This is counted as

the cash outflow of the company. The amount of outflow has been increased by $162

million over the year from the year of 2016 to 2017.

Fourth major item pertains to the inflows of the company. It is related to the amount that

the company receives from the sale of the items of the noncurrent assets and mainly

been considered.

STATEMENT OF CASH FLOWS – AN ANALYSIS

The inflows of the cash and the outflows of the cash are mentioned in the statement showing the

flows of cash during the year. The statement is prepared by considering the three main activities

around which the company works which includes the operating, investing and financing. There

are many items under each of the major head and these have been discussed in detail in the

following paragraphs.

Description of each head

In the statement of the cash flows there are many items present which have been detailed below

and analysed in regard to the meaning and treatment:

First item of the statement of the cash flow is the cash which is received from the

customers. It is the amount which the company receives from the customers of the

company to whom the products of the company has been sold. The cash received from

the customers have been increased slightly by one hundred and sixty nine dollars from

2016 to the year of 2017.

Second major item is the payment which the company pays to the person from whom the

company purchases the goods. Also the payment which is made to the employees in lieu

of the services made has been considered under this minor head. This head represents the

amount of the outflow that the company made in making the payments as required. It is

explicit that the amount of outflow has been decreased by three hundred sixty million

dollar.

Third major and the most considerable item is the amount of income tax. It is the amount

which is paid by the company on the taxable income of the company. This is counted as

the cash outflow of the company. The amount of outflow has been increased by $162

million over the year from the year of 2016 to 2017.

Fourth major item pertains to the inflows of the company. It is related to the amount that

the company receives from the sale of the items of the noncurrent assets and mainly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

under the head of property plant and equipment and which further includes the tangible

assets of building, machinery and etc.

Fifth major item is the opposite of the fourth item. It is related to the outflow that the

company is required to make for the acquisition of the property plant and equipment.

Under this head the detail of intangibles are also included.

The sixth is the cash outflow which the company incurs on the acquisition of the business

of the other company. In this the company usually gives the purchase consideration

through the mode of cash or through the issue of equity shares. The payment in cash will

lead to cash outflow of the company. It is regarded as the non recurring activity which

happens once in a year if the specific arrangement is made so as to get this done. Thus,

the purchase consideration is the form of the cash outflow and is regarded as the major

event under the statement of the cash flow.

The seventh items in the statement of the cash flow are the amount which the company

receives as dividend. It is the amount of the investment that the company made in the

other company. It counts as the cash inflow for the company.

The eight items is the major item as it forms part of the equity of the company which is

considered by every bank so as to have the required ratio in order to sanction the loan or

the working capital limit for the company. This is regarded as the cash inflow of the

company as the amount is received on the issue of shares to the public or through the

private placement.

The ninth item is the amount which the company obtains from the lenders which

constitutes the banks, financial institutions and so on. It is termed as the amount received

from the borrowings. The company’s cash inflow has been decreasing from the year on

year basis as in the year of 2016, the company has received the amount of dollar six

hundred millions and in the year of 2017 only dollar two hundred approximately has been

obtained (Fraser, Ormiston and Fraser, 2010. )

The tenth item is the opposite of the ninth which deals with the outflows of the cash in

the sense that the borrowings which have been paid will be paid in future years and

accordingly the amount paid of borrowings will be repayment and is the cash outflow for

the company. The company has the outflows of the dollar fourteen hundred in year under

consideration and dollar thousand million in the year of 2016. Thus in this manner the

assets of building, machinery and etc.

Fifth major item is the opposite of the fourth item. It is related to the outflow that the

company is required to make for the acquisition of the property plant and equipment.

Under this head the detail of intangibles are also included.

The sixth is the cash outflow which the company incurs on the acquisition of the business

of the other company. In this the company usually gives the purchase consideration

through the mode of cash or through the issue of equity shares. The payment in cash will

lead to cash outflow of the company. It is regarded as the non recurring activity which

happens once in a year if the specific arrangement is made so as to get this done. Thus,

the purchase consideration is the form of the cash outflow and is regarded as the major

event under the statement of the cash flow.

The seventh items in the statement of the cash flow are the amount which the company

receives as dividend. It is the amount of the investment that the company made in the

other company. It counts as the cash inflow for the company.

The eight items is the major item as it forms part of the equity of the company which is

considered by every bank so as to have the required ratio in order to sanction the loan or

the working capital limit for the company. This is regarded as the cash inflow of the

company as the amount is received on the issue of shares to the public or through the

private placement.

The ninth item is the amount which the company obtains from the lenders which

constitutes the banks, financial institutions and so on. It is termed as the amount received

from the borrowings. The company’s cash inflow has been decreasing from the year on

year basis as in the year of 2016, the company has received the amount of dollar six

hundred millions and in the year of 2017 only dollar two hundred approximately has been

obtained (Fraser, Ormiston and Fraser, 2010. )

The tenth item is the opposite of the ninth which deals with the outflows of the cash in

the sense that the borrowings which have been paid will be paid in future years and

accordingly the amount paid of borrowings will be repayment and is the cash outflow for

the company. The company has the outflows of the dollar fourteen hundred in year under

consideration and dollar thousand million in the year of 2016. Thus in this manner the

cash outflow is higher and it is due to the higher inflows of borrowings in the previous

year.

The eleventh item is the amount which the company pays to its investors in lieu of the

amount invested by them in the company. It is termed as the payment of divided and it is

counted as the cash outflow for the company. The company has paid the amount o0f

dollar five hundred and forty million as the dividend during the year which has decreased

the amount of net cash at the end of the period.

The last item in the cash flow is the amount of the change in cash balance during the

year. It is achieved by adding the cash flows from all the activities and if the amount

comes with positive sign then it will be the net increase otherwise it will be the net

decrease. It has also been termed as the surplus or the deficit respectively (Woolworths

Limited, 2016).

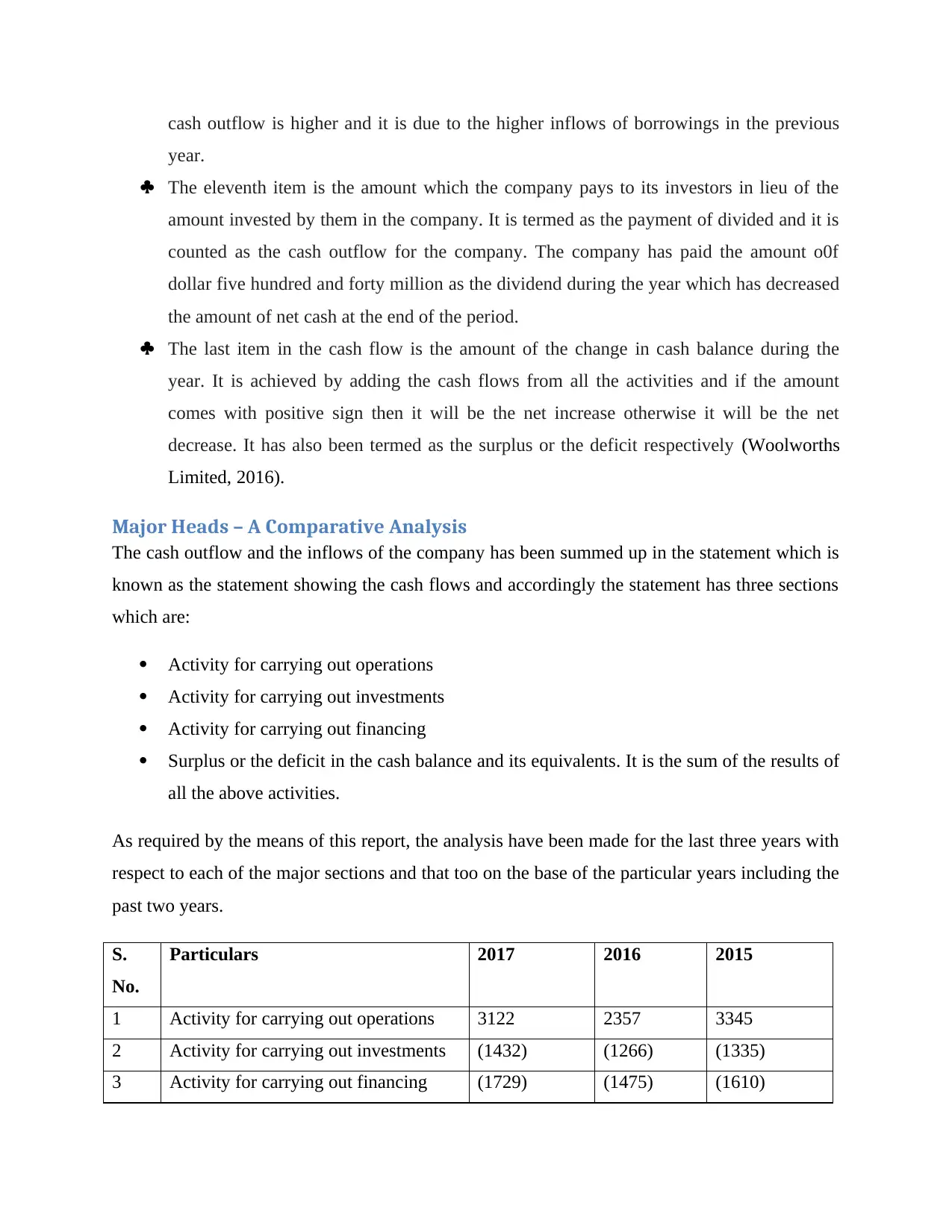

Major Heads – A Comparative Analysis

The cash outflow and the inflows of the company has been summed up in the statement which is

known as the statement showing the cash flows and accordingly the statement has three sections

which are:

Activity for carrying out operations

Activity for carrying out investments

Activity for carrying out financing

Surplus or the deficit in the cash balance and its equivalents. It is the sum of the results of

all the above activities.

As required by the means of this report, the analysis have been made for the last three years with

respect to each of the major sections and that too on the base of the particular years including the

past two years.

S.

No.

Particulars 2017 2016 2015

1 Activity for carrying out operations 3122 2357 3345

2 Activity for carrying out investments (1432) (1266) (1335)

3 Activity for carrying out financing (1729) (1475) (1610)

year.

The eleventh item is the amount which the company pays to its investors in lieu of the

amount invested by them in the company. It is termed as the payment of divided and it is

counted as the cash outflow for the company. The company has paid the amount o0f

dollar five hundred and forty million as the dividend during the year which has decreased

the amount of net cash at the end of the period.

The last item in the cash flow is the amount of the change in cash balance during the

year. It is achieved by adding the cash flows from all the activities and if the amount

comes with positive sign then it will be the net increase otherwise it will be the net

decrease. It has also been termed as the surplus or the deficit respectively (Woolworths

Limited, 2016).

Major Heads – A Comparative Analysis

The cash outflow and the inflows of the company has been summed up in the statement which is

known as the statement showing the cash flows and accordingly the statement has three sections

which are:

Activity for carrying out operations

Activity for carrying out investments

Activity for carrying out financing

Surplus or the deficit in the cash balance and its equivalents. It is the sum of the results of

all the above activities.

As required by the means of this report, the analysis have been made for the last three years with

respect to each of the major sections and that too on the base of the particular years including the

past two years.

S.

No.

Particulars 2017 2016 2015

1 Activity for carrying out operations 3122 2357 3345

2 Activity for carrying out investments (1432) (1266) (1335)

3 Activity for carrying out financing (1729) (1475) (1610)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 Surplus or the deficit in the cash

balance and its equivalents

(39) (384) 400

The activities from the operations have been generating the cash flows but they are volatile in

nature. It is because the figures for the last three years is very fluctuating and if the graph is

prepared then in 2015 the graph will go up and then in 2016 it will go down and in 2017 again it

will go up. This trend shows the weakness of the internal control on operating activities with

regard to the collection from the customer and so on.

The activities from the investment have been negative only due to the fact of purchasing the

assets with the high value (Taylor, 2010).

On the similar terms, the activities from the financing have been negative only due to the fact of

repayment made for the set off of the borrowings amount of the company

Deficit has been there in the cash and its equivalents in the past year because of the high value of

negative investment and financing activities.

STATEMENT OF COMPREHENSIVE INCOME – AN ANALYSIS

Heads Disclosed

The statement has disclosed the reserve relating to Hedging and Foreign Currency Translation.

Description of Each head

First head deals with the change in the value of the cash flow hedges and will transferred to

profit and loss when it is realized (Chambers, 2011).

Second head deals with the change in the value of the foreign currency over the period of time.

The same is written to profit and loss account once it is realized (Bamber, Jiang, Petroni and

Wang, 2010).

balance and its equivalents

(39) (384) 400

The activities from the operations have been generating the cash flows but they are volatile in

nature. It is because the figures for the last three years is very fluctuating and if the graph is

prepared then in 2015 the graph will go up and then in 2016 it will go down and in 2017 again it

will go up. This trend shows the weakness of the internal control on operating activities with

regard to the collection from the customer and so on.

The activities from the investment have been negative only due to the fact of purchasing the

assets with the high value (Taylor, 2010).

On the similar terms, the activities from the financing have been negative only due to the fact of

repayment made for the set off of the borrowings amount of the company

Deficit has been there in the cash and its equivalents in the past year because of the high value of

negative investment and financing activities.

STATEMENT OF COMPREHENSIVE INCOME – AN ANALYSIS

Heads Disclosed

The statement has disclosed the reserve relating to Hedging and Foreign Currency Translation.

Description of Each head

First head deals with the change in the value of the cash flow hedges and will transferred to

profit and loss when it is realized (Chambers, 2011).

Second head deals with the change in the value of the foreign currency over the period of time.

The same is written to profit and loss account once it is realized (Bamber, Jiang, Petroni and

Wang, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different from Profit and Loss Account

The above activities are different from the normal activities and hence the same is not recorded

in the profit and loss account. It is mentioned when it is realized.

DETAIL OF INCOME TAX

Expense - Current

Tax expense includes the current tax and deferred tax amounting to $837 million (Woolworths

Limited, 2017).

Accounting Income - Tax

The tax expense will differ if the tax is calculated on the accounting income as the accounting

income does not take into consideration the tax effects on some items like expenses not

admissible, impairment and etc.

Interpreting Deferred Tax Assets and Liabilities

Deferred tax asset is reflecting in the statement of financial position and accordingly $372

million has been created. It has been created for timing differences which can be reversed in

future (Harrington, Smith and Trippeer, 2012).

Income Tax - Expense and Payable

Income tax payable has been reported and both are not same as the former include deferred tax

expense also (Laux, 2013).

Income Tax - Expense and Paid

Both are not same as the deferred tax is not paid in real terms. (Manzon, G.B. and Plesko, 2012).

The above activities are different from the normal activities and hence the same is not recorded

in the profit and loss account. It is mentioned when it is realized.

DETAIL OF INCOME TAX

Expense - Current

Tax expense includes the current tax and deferred tax amounting to $837 million (Woolworths

Limited, 2017).

Accounting Income - Tax

The tax expense will differ if the tax is calculated on the accounting income as the accounting

income does not take into consideration the tax effects on some items like expenses not

admissible, impairment and etc.

Interpreting Deferred Tax Assets and Liabilities

Deferred tax asset is reflecting in the statement of financial position and accordingly $372

million has been created. It has been created for timing differences which can be reversed in

future (Harrington, Smith and Trippeer, 2012).

Income Tax - Expense and Payable

Income tax payable has been reported and both are not same as the former include deferred tax

expense also (Laux, 2013).

Income Tax - Expense and Paid

Both are not same as the deferred tax is not paid in real terms. (Manzon, G.B. and Plesko, 2012).

Quality of Tax Treatment

The quality is best as everyone can understand the treatment. It has been interesting to

understand the treatment of tax. It has been gained that the correct treatment of tax is very

important part and it shall be disclosed in correct manner.

CONCLUSION AND RECOMMENDATION

The report has analysed the cash flow statement and statement of comprehensive income and

provides the detail of income tax expense. The report has been the exhaustive and detailed.

The recommendation is to prepare the annual report with full transparency.

REFERENCES

Bamber, L.S., Jiang, J., Petroni, K.R. and Wang, I.Y., 2010. Comprehensive income: Who's

afraid of performance reporting?. The Accounting Review, 85(1), pp.97-126

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements Pearson

Harrington, C., Smith, W. and Trippeer, D., 2012,Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, p.1

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments The Accounting Review, 88(4), pp.1357-1383

Manzon Jr, G.B. and Plesko, G.A., 2012. The relation between financial and tax reporting

measures of income Tax L. Rev., 55, p.175

Taylor, M., 2010, Financial statement analysis, pp 13-20

Woolworths Limited (2016), Annual Report -2016 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

The quality is best as everyone can understand the treatment. It has been interesting to

understand the treatment of tax. It has been gained that the correct treatment of tax is very

important part and it shall be disclosed in correct manner.

CONCLUSION AND RECOMMENDATION

The report has analysed the cash flow statement and statement of comprehensive income and

provides the detail of income tax expense. The report has been the exhaustive and detailed.

The recommendation is to prepare the annual report with full transparency.

REFERENCES

Bamber, L.S., Jiang, J., Petroni, K.R. and Wang, I.Y., 2010. Comprehensive income: Who's

afraid of performance reporting?. The Accounting Review, 85(1), pp.97-126

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements Pearson

Harrington, C., Smith, W. and Trippeer, D., 2012,Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, p.1

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments The Accounting Review, 88(4), pp.1357-1383

Manzon Jr, G.B. and Plesko, G.A., 2012. The relation between financial and tax reporting

measures of income Tax L. Rev., 55, p.175

Taylor, M., 2010, Financial statement analysis, pp 13-20

Woolworths Limited (2016), Annual Report -2016 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths Limited (2017), Annual Report -2017 online available

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

https://www.woolworthsgroup.com.au/page/investors/our-performance/reports/Reports at

accessed on 12-05-2018.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.