Analysis of HLW Club's Management Accounting and Finances Report

VerifiedAdded on 2020/05/16

|14

|2103

|81

Report

AI Summary

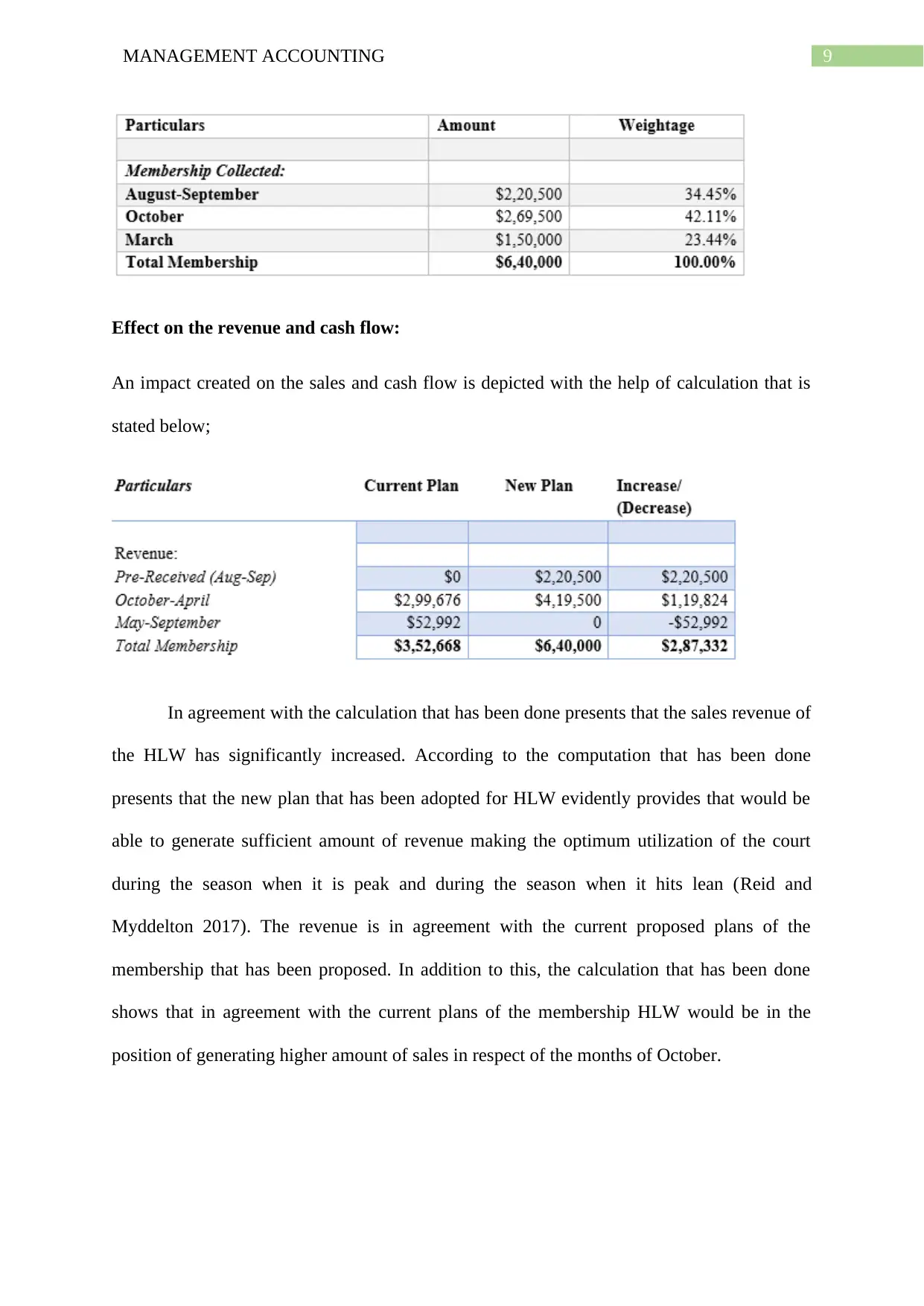

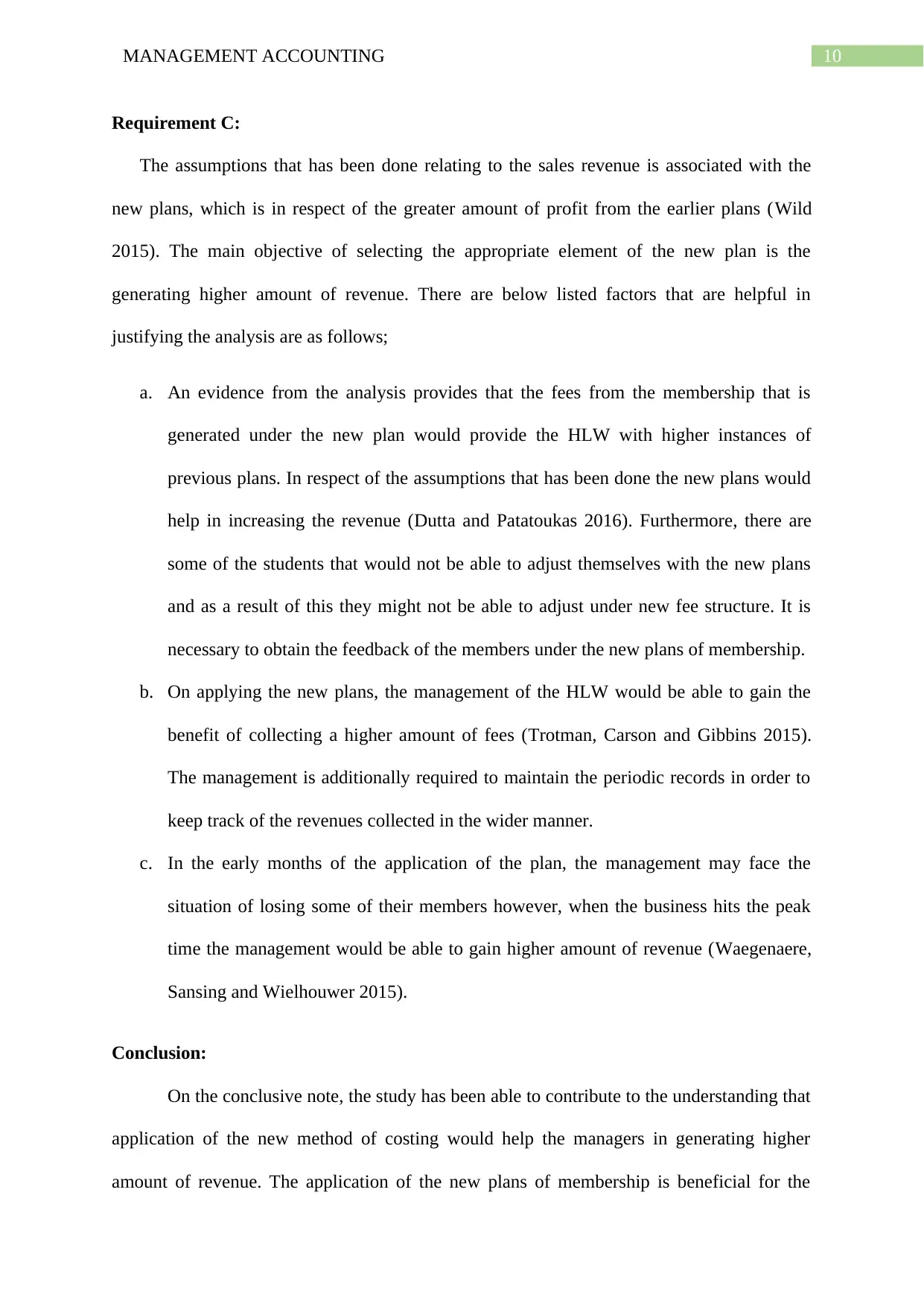

This report provides a comprehensive analysis of the financial aspects of the HLW Club, focusing on management accounting principles and the impact of new membership plans. The study examines activity-based costing, direct and indirect costs, and revenue generation strategies. It evaluates the benefits of the proposed membership plans, including their effect on cash flow and overall revenue. The report includes calculations and assumptions to assess the financial implications of different scenarios, such as varying court usage during peak and lean seasons. The analysis highlights the importance of considering direct costs in production and the potential advantages of the new membership structure in increasing revenue and optimizing court utilization. Furthermore, the report also discusses the importance of feedback from members and the maintenance of periodic records to track the revenues collected.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.