Finance in Hospitality: Performance Analysis and Recommendations

VerifiedAdded on 2020/01/28

|20

|4629

|100

Report

AI Summary

This report provides a comprehensive analysis of finance within the hospitality industry, focusing on key financial concepts and their practical application. The report begins by exploring various sources of funding, both internal and external, and methods for revenue generation. It then delves into cost components, gross profit, and selling price determination, followed by an examination of inventory and cash management techniques. Budgetary control, including its procedures and objectives, is discussed, along with variance analysis to assess business performance. The report also covers financial ratio analysis to evaluate business performance and offers recommendations for improvement. Furthermore, it classifies costs associated with the firm, computes contribution per customer, and defines the cost-volume-profit (CVP) relationship. The report also includes calculations for recipe costing, cost per portion, and selling price, along with an assessment of costs for package deals and break-even analysis. The report concludes with a summary of findings and recommendations for financial management in the hospitality sector.

Finance in Hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

Assessment Tasks............................................................................................................................4

LO1..................................................................................................................................................4

1.1 Sources of funding to raise capital.........................................................................................4

1.2 Methods through which income generates within business...................................................5

LO2..................................................................................................................................................5

2.1 Components of cost, gross profit and selling price of goods and services............................5

2.2 Evaluating ways for managing stock and cash in firm..........................................................6

LO3..................................................................................................................................................6

3.1 Source as well as format of trial balance...............................................................................6

3.2 Evaluating business accounts, adjustments as well as notes.................................................7

3.3 Procedures and objectives of budgetary control....................................................................8

3.4 Variance analysis and suggestion for further management action........................................8

LO4..................................................................................................................................................9

4.1 Computing as well as analysing financial ratios to assess business performance.................9

4.2 Recommendations for improving business performance.....................................................11

LO5................................................................................................................................................11

5.1 Classified costs associated with the firm.............................................................................11

5.2 Computing contribution per customer and defining CVP relationship...............................12

5.3 Justification of management decisions for short-term.........................................................12

PART 2..........................................................................................................................................12

1. Calculating the recipe cost ....................................................................................................13

2. Calculating the cost per portion ............................................................................................13

3. Calculating the quantity required to produce 70 portions .....................................................14

INTRODUCTION...........................................................................................................................4

Assessment Tasks............................................................................................................................4

LO1..................................................................................................................................................4

1.1 Sources of funding to raise capital.........................................................................................4

1.2 Methods through which income generates within business...................................................5

LO2..................................................................................................................................................5

2.1 Components of cost, gross profit and selling price of goods and services............................5

2.2 Evaluating ways for managing stock and cash in firm..........................................................6

LO3..................................................................................................................................................6

3.1 Source as well as format of trial balance...............................................................................6

3.2 Evaluating business accounts, adjustments as well as notes.................................................7

3.3 Procedures and objectives of budgetary control....................................................................8

3.4 Variance analysis and suggestion for further management action........................................8

LO4..................................................................................................................................................9

4.1 Computing as well as analysing financial ratios to assess business performance.................9

4.2 Recommendations for improving business performance.....................................................11

LO5................................................................................................................................................11

5.1 Classified costs associated with the firm.............................................................................11

5.2 Computing contribution per customer and defining CVP relationship...............................12

5.3 Justification of management decisions for short-term.........................................................12

PART 2..........................................................................................................................................12

1. Calculating the recipe cost ....................................................................................................13

2. Calculating the cost per portion ............................................................................................13

3. Calculating the quantity required to produce 70 portions .....................................................14

4. Claculating selling price to earn 85% margin .......................................................................14

Section B....................................................................................................................................15

1. Assessing the total cost for package deal ..............................................................................15

2. identifying the cost per person on the basis of selling all the seats ......................................16

3. Calculating selling price when mark up is 35%....................................................................16

4. Assessing fixed expenses and cost per unit when BEP is 36 seats .......................................16

5. Assessment of profit when break-even point is 36 seats ......................................................17

CONCLUSION .............................................................................................................................18

REFERENCES .............................................................................................................................19

Section B....................................................................................................................................15

1. Assessing the total cost for package deal ..............................................................................15

2. identifying the cost per person on the basis of selling all the seats ......................................16

3. Calculating selling price when mark up is 35%....................................................................16

4. Assessing fixed expenses and cost per unit when BEP is 36 seats .......................................16

5. Assessment of profit when break-even point is 36 seats ......................................................17

CONCLUSION .............................................................................................................................18

REFERENCES .............................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the hospitality sector, effective management of funds is highly required to attain the

goals and objectives. Moreover, without making optimum use of finance firm would not become

able to place emphasis on innovative business practices. Thus, by employing the financial tools

and techniques companies which are operated in the hospitality and travel & tourism sector

would become able to take suitable decisions that aid in the growth and success of firm. In this,

report will provide deeper insight about the concept of unit cost, gross margin and selling price.

Besides this, report will also develop understanding about the aspects of BEP which in turn aids

in the managerial decision making.

Assessment Tasks

LO1

1.1 Sources of funding to raise capital

In order to enhance fund in the business for expansion or any other objective various

sources are used which are stated below:

Internal sources of finance:

When the company raise capital from the internal environment rather than considering

market then that sources are known as internal. Cost of finance with this kind of sources is not

there. Moreover, sources include sale of assets, retained earnings, personal savings etc.

External financing sources:

At the time of raising fund when entity considers market and external environment then

used sources called as external (Mullinova, 2016). Each and every external source impose high

cost of finance and create cost burden on the Hilton hotel. Such sources are like bank loan,

equity, debentures, crowdfunding, hire purchase, venture capital, leasing etc.

In the hospitality sector, effective management of funds is highly required to attain the

goals and objectives. Moreover, without making optimum use of finance firm would not become

able to place emphasis on innovative business practices. Thus, by employing the financial tools

and techniques companies which are operated in the hospitality and travel & tourism sector

would become able to take suitable decisions that aid in the growth and success of firm. In this,

report will provide deeper insight about the concept of unit cost, gross margin and selling price.

Besides this, report will also develop understanding about the aspects of BEP which in turn aids

in the managerial decision making.

Assessment Tasks

LO1

1.1 Sources of funding to raise capital

In order to enhance fund in the business for expansion or any other objective various

sources are used which are stated below:

Internal sources of finance:

When the company raise capital from the internal environment rather than considering

market then that sources are known as internal. Cost of finance with this kind of sources is not

there. Moreover, sources include sale of assets, retained earnings, personal savings etc.

External financing sources:

At the time of raising fund when entity considers market and external environment then

used sources called as external (Mullinova, 2016). Each and every external source impose high

cost of finance and create cost burden on the Hilton hotel. Such sources are like bank loan,

equity, debentures, crowdfunding, hire purchase, venture capital, leasing etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Methods through which income generates within business

In order to earn income and profit within hospitality businesses or any other wide range

of sources available. Moreover, those methods by which the company generate revenue within

working environment are stated below:

From selling goods and services the firm easily generate income from the customers.

By providing differentiate hospitality services and products it can attract more customers

and boost up total income.

Apart from this, after giving some outside part of the plant or property Hilton Hotel can

earn income which known as sub letting (Chan and et.al. 2016).

Further, return on investment generation is also a proportion of gain income.

LO2

2.1 Components of cost, gross profit and selling price of goods and services

Cost: There are several kinds of expenditures included within working environment of

hospitality business. Further, elements of the costs are such as follows:

Direct expenses

Indirect costs

Fixed costs

Variable expenditure

Semi-variable expenses

Production

Selling and expenditure expenses

Gross Profit: Level of yield in which only cost of product sold are deducted from the value of

sales earned by the firm is known as gross profit within Hilton hotel (Nigrini, 2016). Further,

elements taken into consideration in GP are stated below:

Cost of goods sold within an accounting period

Sales and revenue generated from selling products and services

Management of the whole hospitality firm

In order to earn income and profit within hospitality businesses or any other wide range

of sources available. Moreover, those methods by which the company generate revenue within

working environment are stated below:

From selling goods and services the firm easily generate income from the customers.

By providing differentiate hospitality services and products it can attract more customers

and boost up total income.

Apart from this, after giving some outside part of the plant or property Hilton Hotel can

earn income which known as sub letting (Chan and et.al. 2016).

Further, return on investment generation is also a proportion of gain income.

LO2

2.1 Components of cost, gross profit and selling price of goods and services

Cost: There are several kinds of expenditures included within working environment of

hospitality business. Further, elements of the costs are such as follows:

Direct expenses

Indirect costs

Fixed costs

Variable expenditure

Semi-variable expenses

Production

Selling and expenditure expenses

Gross Profit: Level of yield in which only cost of product sold are deducted from the value of

sales earned by the firm is known as gross profit within Hilton hotel (Nigrini, 2016). Further,

elements taken into consideration in GP are stated below:

Cost of goods sold within an accounting period

Sales and revenue generated from selling products and services

Management of the whole hospitality firm

Selling price: The value on which hospitality services of the Hilton Hotel are offered in the

market is known as selling price. Moreover, components involved in this aspect are such as

follows:

Demand and supply condition in market

Total cost of the production

Price level of competitors like Marriott etc.

Quality of the services

Brand image of the firm

2.2 Evaluating ways for managing stock and cash in firm

In order to manage as well as reduce level of total inventory within Hilton hotel some

methods are stated below:

Just-in-time

Fixed re-order stock

Fixed re-order time-frame

(EOQ) Economic Order Quantity

For control as well as boost up the level of cash within workplace some ways are

available which are listed below:

Auditing of the financial statements (Oulasvirta and Bailey, 2016)

Hire and recruit skilled and talented workforce

Proper record of monetary transactions in books of final accounts

LO3

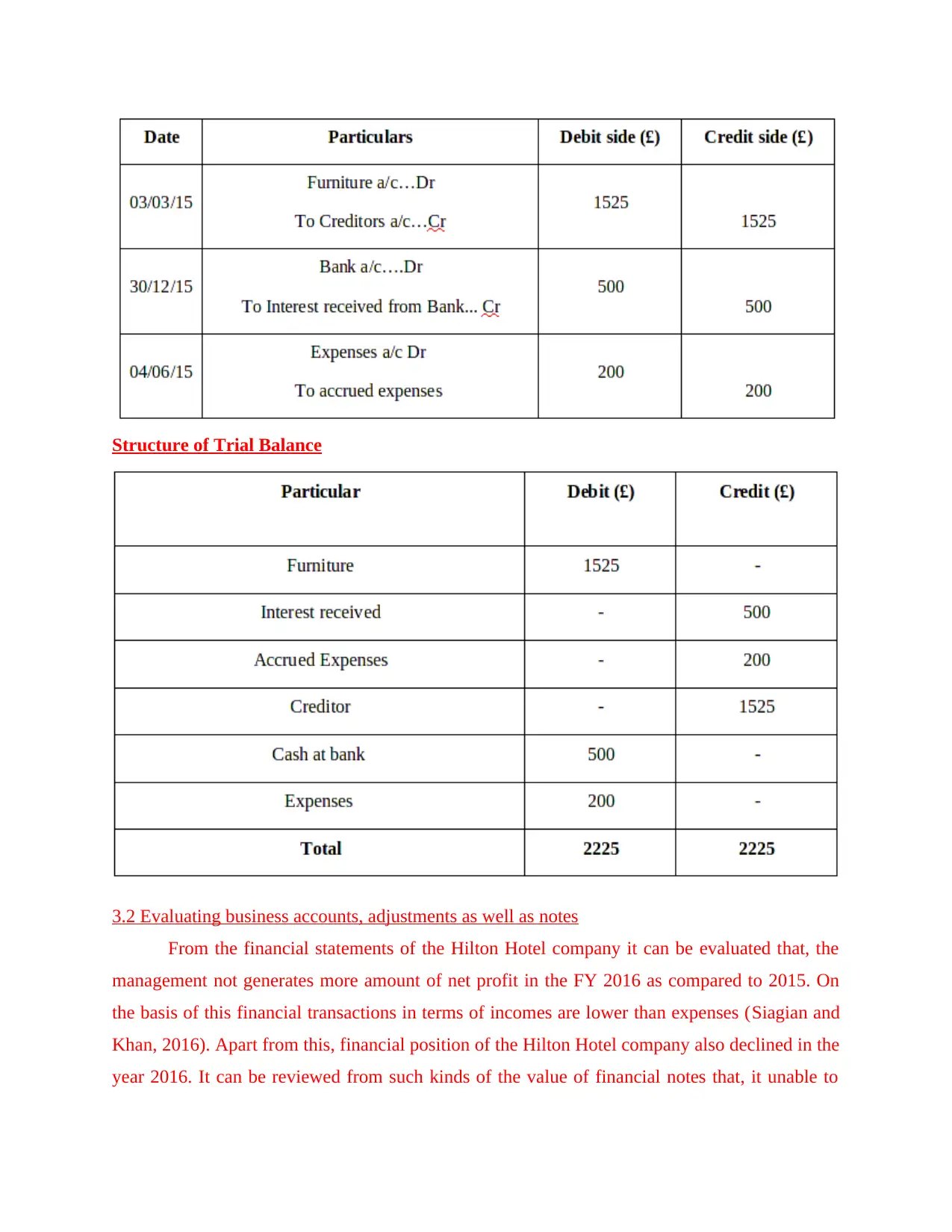

3.1 Source as well as format of trial balance

Within business of hospitality industry at the time of preparing income statement, trial

balance has the pivotal role. The reason is that, it is a base of preparing financial accounts of the

company. Moreover, sources through which trial balance is prepared are journal entries which

are shown below:

Journal Entries

market is known as selling price. Moreover, components involved in this aspect are such as

follows:

Demand and supply condition in market

Total cost of the production

Price level of competitors like Marriott etc.

Quality of the services

Brand image of the firm

2.2 Evaluating ways for managing stock and cash in firm

In order to manage as well as reduce level of total inventory within Hilton hotel some

methods are stated below:

Just-in-time

Fixed re-order stock

Fixed re-order time-frame

(EOQ) Economic Order Quantity

For control as well as boost up the level of cash within workplace some ways are

available which are listed below:

Auditing of the financial statements (Oulasvirta and Bailey, 2016)

Hire and recruit skilled and talented workforce

Proper record of monetary transactions in books of final accounts

LO3

3.1 Source as well as format of trial balance

Within business of hospitality industry at the time of preparing income statement, trial

balance has the pivotal role. The reason is that, it is a base of preparing financial accounts of the

company. Moreover, sources through which trial balance is prepared are journal entries which

are shown below:

Journal Entries

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Structure of Trial Balance

3.2 Evaluating business accounts, adjustments as well as notes

From the financial statements of the Hilton Hotel company it can be evaluated that, the

management not generates more amount of net profit in the FY 2016 as compared to 2015. On

the basis of this financial transactions in terms of incomes are lower than expenses (Siagian and

Khan, 2016). Apart from this, financial position of the Hilton Hotel company also declined in the

year 2016. It can be reviewed from such kinds of the value of financial notes that, it unable to

3.2 Evaluating business accounts, adjustments as well as notes

From the financial statements of the Hilton Hotel company it can be evaluated that, the

management not generates more amount of net profit in the FY 2016 as compared to 2015. On

the basis of this financial transactions in terms of incomes are lower than expenses (Siagian and

Khan, 2016). Apart from this, financial position of the Hilton Hotel company also declined in the

year 2016. It can be reviewed from such kinds of the value of financial notes that, it unable to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manage any kind of direct and indirect expenses. Along with this, not generated high level of the

sales and revenue in the financial year ending 2016.

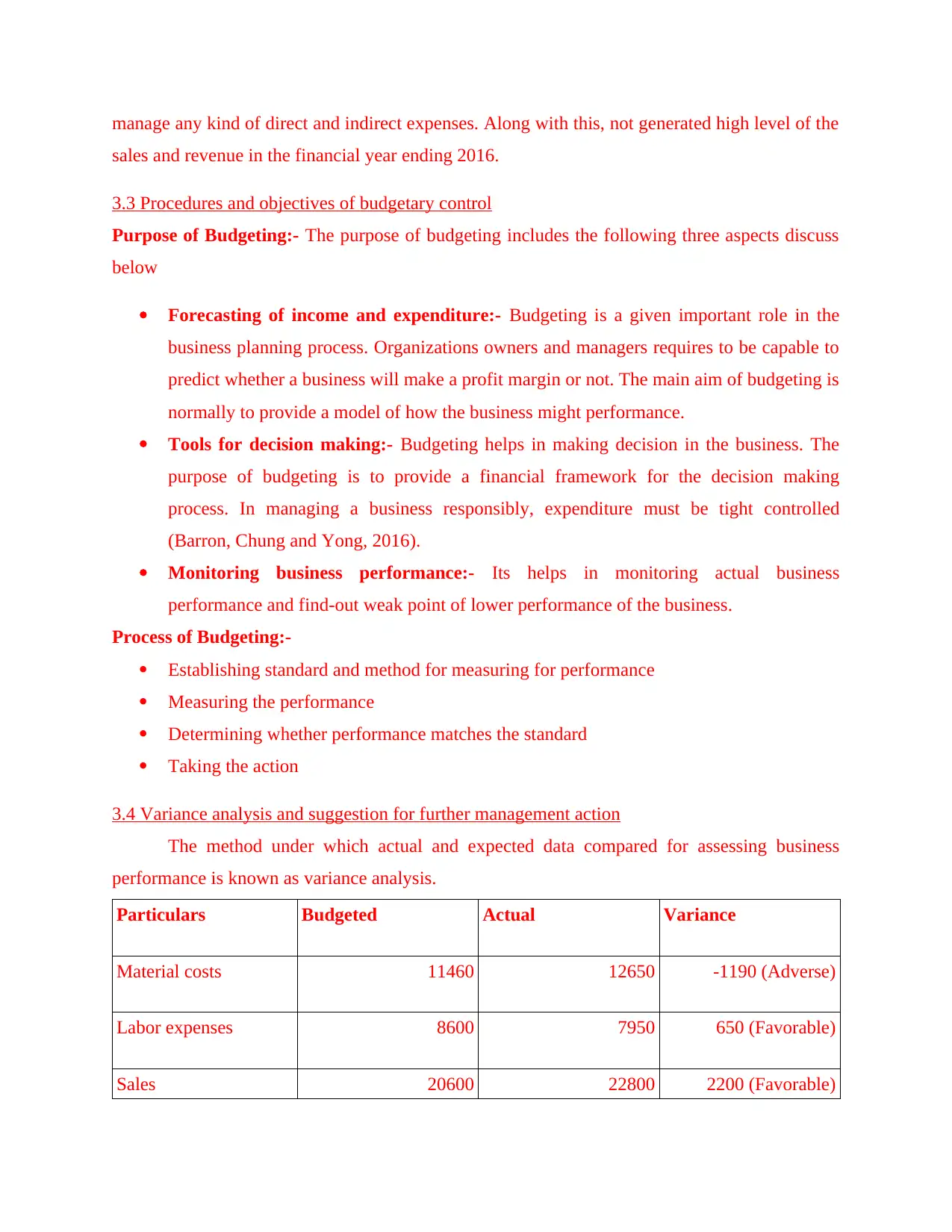

3.3 Procedures and objectives of budgetary control

Purpose of Budgeting:- The purpose of budgeting includes the following three aspects discuss

below

Forecasting of income and expenditure:- Budgeting is a given important role in the

business planning process. Organizations owners and managers requires to be capable to

predict whether a business will make a profit margin or not. The main aim of budgeting is

normally to provide a model of how the business might performance.

Tools for decision making:- Budgeting helps in making decision in the business. The

purpose of budgeting is to provide a financial framework for the decision making

process. In managing a business responsibly, expenditure must be tight controlled

(Barron, Chung and Yong, 2016).

Monitoring business performance:- Its helps in monitoring actual business

performance and find-out weak point of lower performance of the business.

Process of Budgeting:-

Establishing standard and method for measuring for performance

Measuring the performance

Determining whether performance matches the standard

Taking the action

3.4 Variance analysis and suggestion for further management action

The method under which actual and expected data compared for assessing business

performance is known as variance analysis.

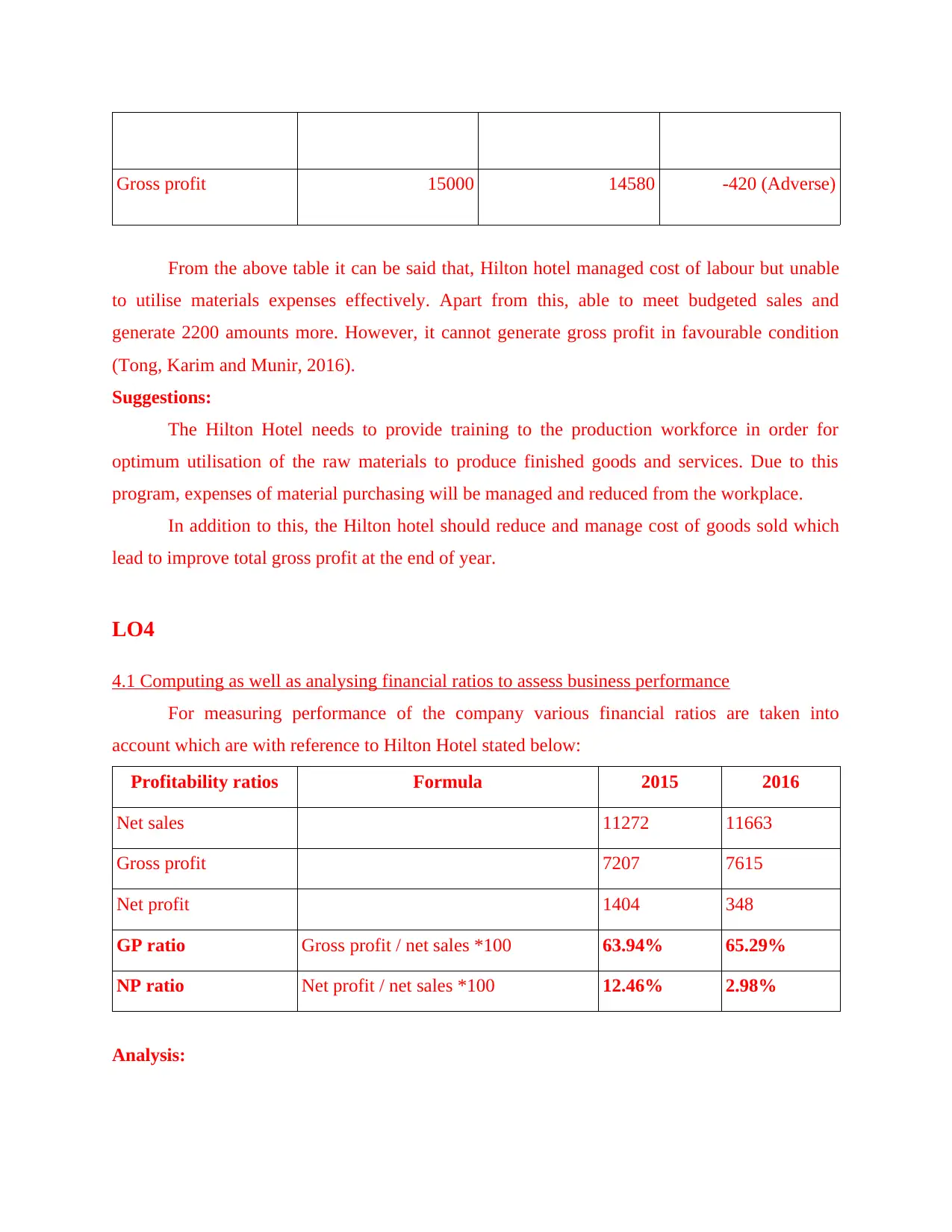

Particulars Budgeted Actual Variance

Material costs 11460 12650 -1190 (Adverse)

Labor expenses 8600 7950 650 (Favorable)

Sales 20600 22800 2200 (Favorable)

sales and revenue in the financial year ending 2016.

3.3 Procedures and objectives of budgetary control

Purpose of Budgeting:- The purpose of budgeting includes the following three aspects discuss

below

Forecasting of income and expenditure:- Budgeting is a given important role in the

business planning process. Organizations owners and managers requires to be capable to

predict whether a business will make a profit margin or not. The main aim of budgeting is

normally to provide a model of how the business might performance.

Tools for decision making:- Budgeting helps in making decision in the business. The

purpose of budgeting is to provide a financial framework for the decision making

process. In managing a business responsibly, expenditure must be tight controlled

(Barron, Chung and Yong, 2016).

Monitoring business performance:- Its helps in monitoring actual business

performance and find-out weak point of lower performance of the business.

Process of Budgeting:-

Establishing standard and method for measuring for performance

Measuring the performance

Determining whether performance matches the standard

Taking the action

3.4 Variance analysis and suggestion for further management action

The method under which actual and expected data compared for assessing business

performance is known as variance analysis.

Particulars Budgeted Actual Variance

Material costs 11460 12650 -1190 (Adverse)

Labor expenses 8600 7950 650 (Favorable)

Sales 20600 22800 2200 (Favorable)

Gross profit 15000 14580 -420 (Adverse)

From the above table it can be said that, Hilton hotel managed cost of labour but unable

to utilise materials expenses effectively. Apart from this, able to meet budgeted sales and

generate 2200 amounts more. However, it cannot generate gross profit in favourable condition

(Tong, Karim and Munir, 2016).

Suggestions:

The Hilton Hotel needs to provide training to the production workforce in order for

optimum utilisation of the raw materials to produce finished goods and services. Due to this

program, expenses of material purchasing will be managed and reduced from the workplace.

In addition to this, the Hilton hotel should reduce and manage cost of goods sold which

lead to improve total gross profit at the end of year.

LO4

4.1 Computing as well as analysing financial ratios to assess business performance

For measuring performance of the company various financial ratios are taken into

account which are with reference to Hilton Hotel stated below:

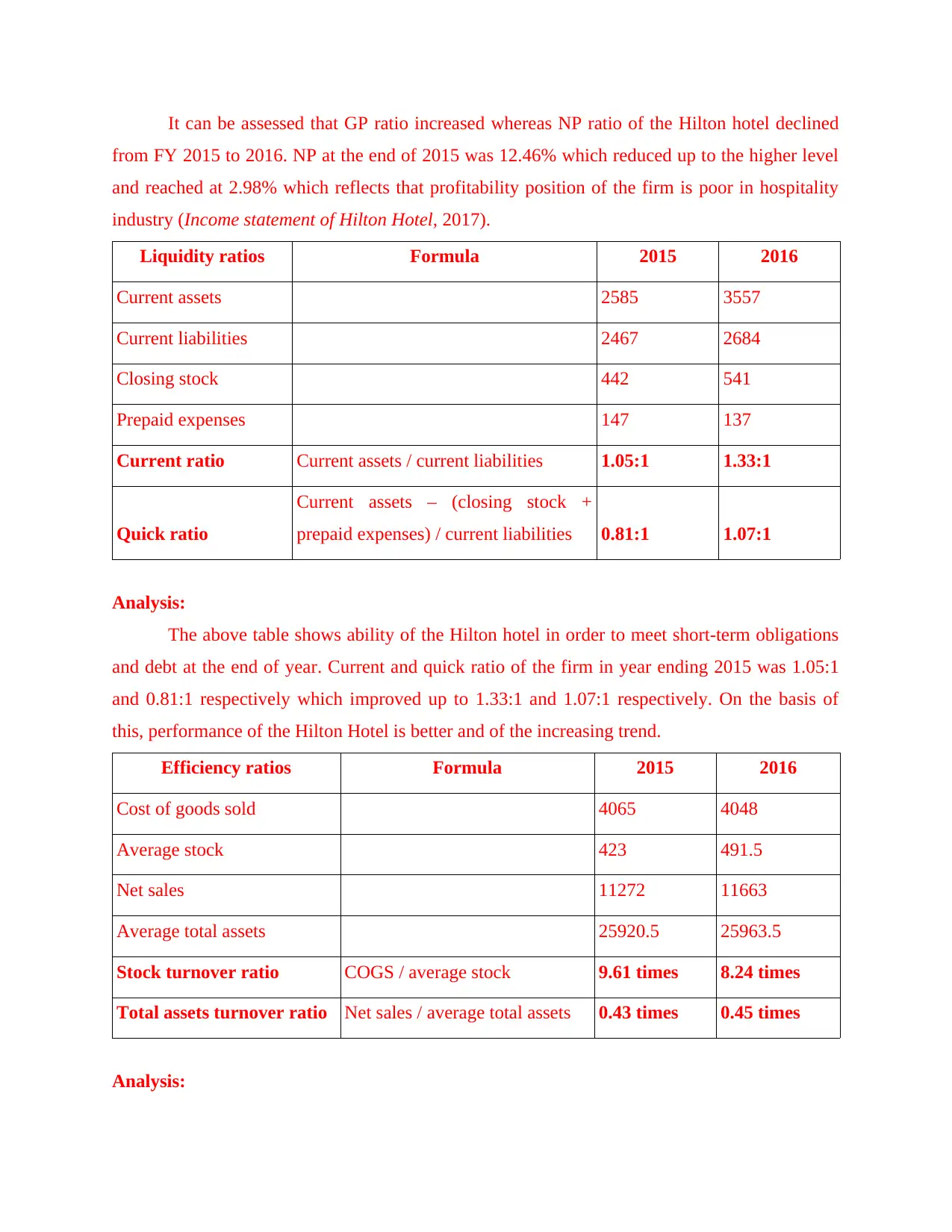

Profitability ratios Formula 2015 2016

Net sales 11272 11663

Gross profit 7207 7615

Net profit 1404 348

GP ratio Gross profit / net sales *100 63.94% 65.29%

NP ratio Net profit / net sales *100 12.46% 2.98%

Analysis:

From the above table it can be said that, Hilton hotel managed cost of labour but unable

to utilise materials expenses effectively. Apart from this, able to meet budgeted sales and

generate 2200 amounts more. However, it cannot generate gross profit in favourable condition

(Tong, Karim and Munir, 2016).

Suggestions:

The Hilton Hotel needs to provide training to the production workforce in order for

optimum utilisation of the raw materials to produce finished goods and services. Due to this

program, expenses of material purchasing will be managed and reduced from the workplace.

In addition to this, the Hilton hotel should reduce and manage cost of goods sold which

lead to improve total gross profit at the end of year.

LO4

4.1 Computing as well as analysing financial ratios to assess business performance

For measuring performance of the company various financial ratios are taken into

account which are with reference to Hilton Hotel stated below:

Profitability ratios Formula 2015 2016

Net sales 11272 11663

Gross profit 7207 7615

Net profit 1404 348

GP ratio Gross profit / net sales *100 63.94% 65.29%

NP ratio Net profit / net sales *100 12.46% 2.98%

Analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It can be assessed that GP ratio increased whereas NP ratio of the Hilton hotel declined

from FY 2015 to 2016. NP at the end of 2015 was 12.46% which reduced up to the higher level

and reached at 2.98% which reflects that profitability position of the firm is poor in hospitality

industry (Income statement of Hilton Hotel, 2017).

Liquidity ratios Formula 2015 2016

Current assets 2585 3557

Current liabilities 2467 2684

Closing stock 442 541

Prepaid expenses 147 137

Current ratio Current assets / current liabilities 1.05:1 1.33:1

Quick ratio

Current assets – (closing stock +

prepaid expenses) / current liabilities 0.81:1 1.07:1

Analysis:

The above table shows ability of the Hilton hotel in order to meet short-term obligations

and debt at the end of year. Current and quick ratio of the firm in year ending 2015 was 1.05:1

and 0.81:1 respectively which improved up to 1.33:1 and 1.07:1 respectively. On the basis of

this, performance of the Hilton Hotel is better and of the increasing trend.

Efficiency ratios Formula 2015 2016

Cost of goods sold 4065 4048

Average stock 423 491.5

Net sales 11272 11663

Average total assets 25920.5 25963.5

Stock turnover ratio COGS / average stock 9.61 times 8.24 times

Total assets turnover ratio Net sales / average total assets 0.43 times 0.45 times

Analysis:

from FY 2015 to 2016. NP at the end of 2015 was 12.46% which reduced up to the higher level

and reached at 2.98% which reflects that profitability position of the firm is poor in hospitality

industry (Income statement of Hilton Hotel, 2017).

Liquidity ratios Formula 2015 2016

Current assets 2585 3557

Current liabilities 2467 2684

Closing stock 442 541

Prepaid expenses 147 137

Current ratio Current assets / current liabilities 1.05:1 1.33:1

Quick ratio

Current assets – (closing stock +

prepaid expenses) / current liabilities 0.81:1 1.07:1

Analysis:

The above table shows ability of the Hilton hotel in order to meet short-term obligations

and debt at the end of year. Current and quick ratio of the firm in year ending 2015 was 1.05:1

and 0.81:1 respectively which improved up to 1.33:1 and 1.07:1 respectively. On the basis of

this, performance of the Hilton Hotel is better and of the increasing trend.

Efficiency ratios Formula 2015 2016

Cost of goods sold 4065 4048

Average stock 423 491.5

Net sales 11272 11663

Average total assets 25920.5 25963.5

Stock turnover ratio COGS / average stock 9.61 times 8.24 times

Total assets turnover ratio Net sales / average total assets 0.43 times 0.45 times

Analysis:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It can be ascertained from the above table that stock turnover ratio was 9.61 times which

declined up to 8.24 times in the FY 2016. On the other hand side, Hilton hotel capable to utilise

current and non-current assets within firm for generating net sales (Favilukis and et.al., 2017).

Due to this particular situation, total assets turnover ratio enhanced from 0.43 times to 0.45 times

in 2016 year ending.

Moreover, overall performance of Hilton Hotel in 2016 is at the moderate level where it

needs to work upon it.

4.2 Recommendations for improving business performance

It can be advised to the Hilton Hotel that it should manage total indirect expenses at the

end of year because it will be supportive for increasing net profit ratio. As total amount of

indirect costs will decline in then able to enhance net yield and business performance

both at the end of upcoming accounting year.

Apart from this, should consider highly effectual kind of marketing strategies which

helps to increase net revenue. Therefore, net income will also affect in positive direction.

In addition to this, it must give training to the employees for utilising total assets in

optimum way. The reason is that, it will help to enhance efficiency of the Hilton Hotel to

generate more sales with the help of available assets.

LO5

5.1 Classified costs associated with the firm

In the selected hotel of hospitality industry various number of the costs included which

are segregated in proper manner (Singleton, 2016). Further, fixed, semi-variable and non-fixed

expenses associated with the Hilton hotel are stated below:

Fixed expenses:

Selling and distribution costs

Rent of property

Premium of insurance

Interest charges on debt

Depreciation of equipments of fixed assets

Administration expenses etc.

declined up to 8.24 times in the FY 2016. On the other hand side, Hilton hotel capable to utilise

current and non-current assets within firm for generating net sales (Favilukis and et.al., 2017).

Due to this particular situation, total assets turnover ratio enhanced from 0.43 times to 0.45 times

in 2016 year ending.

Moreover, overall performance of Hilton Hotel in 2016 is at the moderate level where it

needs to work upon it.

4.2 Recommendations for improving business performance

It can be advised to the Hilton Hotel that it should manage total indirect expenses at the

end of year because it will be supportive for increasing net profit ratio. As total amount of

indirect costs will decline in then able to enhance net yield and business performance

both at the end of upcoming accounting year.

Apart from this, should consider highly effectual kind of marketing strategies which

helps to increase net revenue. Therefore, net income will also affect in positive direction.

In addition to this, it must give training to the employees for utilising total assets in

optimum way. The reason is that, it will help to enhance efficiency of the Hilton Hotel to

generate more sales with the help of available assets.

LO5

5.1 Classified costs associated with the firm

In the selected hotel of hospitality industry various number of the costs included which

are segregated in proper manner (Singleton, 2016). Further, fixed, semi-variable and non-fixed

expenses associated with the Hilton hotel are stated below:

Fixed expenses:

Selling and distribution costs

Rent of property

Premium of insurance

Interest charges on debt

Depreciation of equipments of fixed assets

Administration expenses etc.

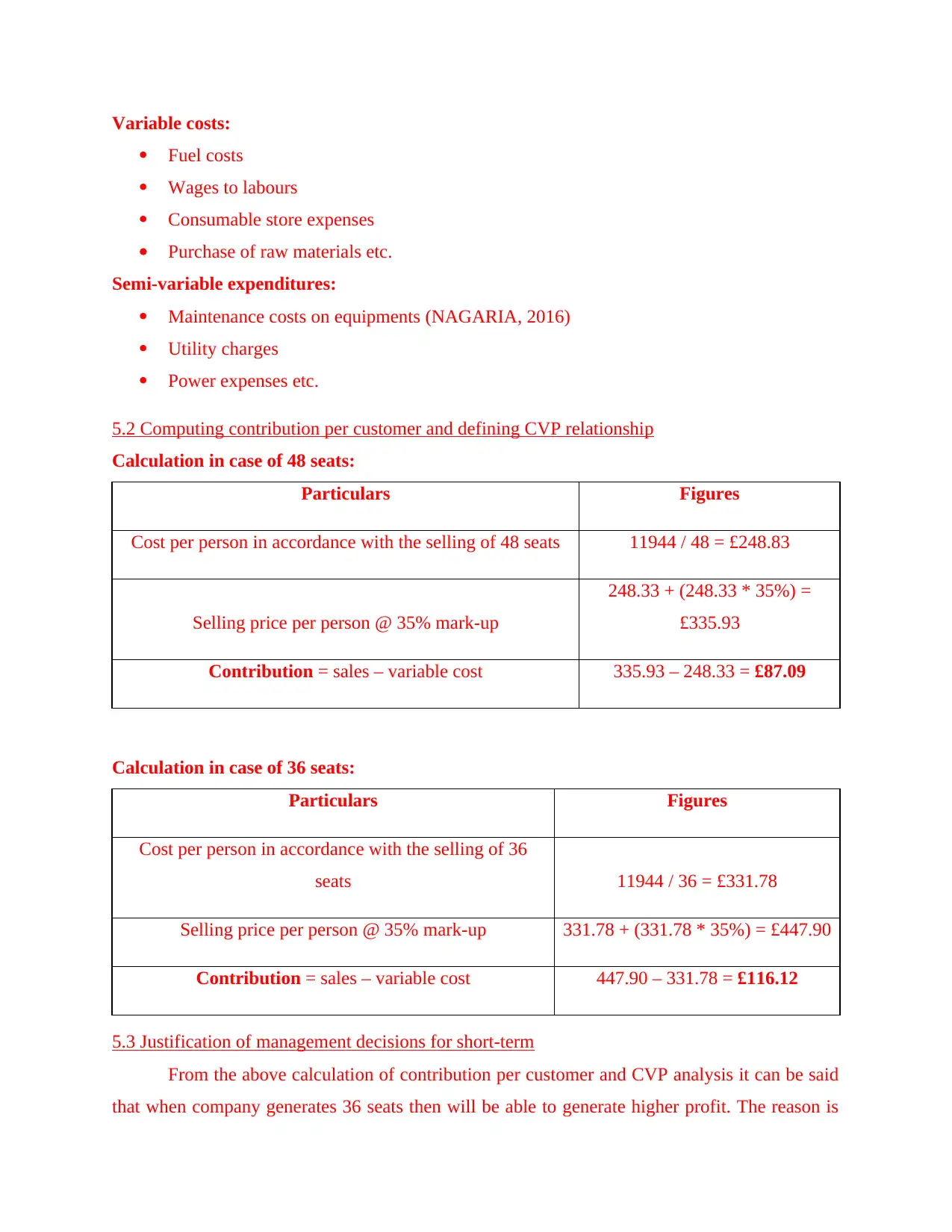

Variable costs:

Fuel costs

Wages to labours

Consumable store expenses

Purchase of raw materials etc.

Semi-variable expenditures:

Maintenance costs on equipments (NAGARIA, 2016)

Utility charges

Power expenses etc.

5.2 Computing contribution per customer and defining CVP relationship

Calculation in case of 48 seats:

Particulars Figures

Cost per person in accordance with the selling of 48 seats 11944 / 48 = £248.83

Selling price per person @ 35% mark-up

248.33 + (248.33 * 35%) =

£335.93

Contribution = sales – variable cost 335.93 – 248.33 = £87.09

Calculation in case of 36 seats:

Particulars Figures

Cost per person in accordance with the selling of 36

seats 11944 / 36 = £331.78

Selling price per person @ 35% mark-up 331.78 + (331.78 * 35%) = £447.90

Contribution = sales – variable cost 447.90 – 331.78 = £116.12

5.3 Justification of management decisions for short-term

From the above calculation of contribution per customer and CVP analysis it can be said

that when company generates 36 seats then will be able to generate higher profit. The reason is

Fuel costs

Wages to labours

Consumable store expenses

Purchase of raw materials etc.

Semi-variable expenditures:

Maintenance costs on equipments (NAGARIA, 2016)

Utility charges

Power expenses etc.

5.2 Computing contribution per customer and defining CVP relationship

Calculation in case of 48 seats:

Particulars Figures

Cost per person in accordance with the selling of 48 seats 11944 / 48 = £248.83

Selling price per person @ 35% mark-up

248.33 + (248.33 * 35%) =

£335.93

Contribution = sales – variable cost 335.93 – 248.33 = £87.09

Calculation in case of 36 seats:

Particulars Figures

Cost per person in accordance with the selling of 36

seats 11944 / 36 = £331.78

Selling price per person @ 35% mark-up 331.78 + (331.78 * 35%) = £447.90

Contribution = sales – variable cost 447.90 – 331.78 = £116.12

5.3 Justification of management decisions for short-term

From the above calculation of contribution per customer and CVP analysis it can be said

that when company generates 36 seats then will be able to generate higher profit. The reason is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.