Comprehensive Business Plan and Financial Analysis for Hospitality

VerifiedAdded on 2023/01/04

|23

|4384

|333

Report

AI Summary

This report presents a comprehensive business plan for a hospitality venture, focusing on financial analysis and investment appraisal techniques. The plan includes an introduction to the business and its objectives, followed by a detailed financial and economic analysis of an investment project, specifically for starting a restaurant. The analysis covers project variables, assumptions, and the application of various investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), Project Profitability Index (PI), Discounted Payback Period, and Accounting Rate of Return (ARR). The report also includes discussions on depreciation, break-even analysis, and sensitivity analysis. Furthermore, it addresses balance and accounts, summarizing the analysis and offering short-term and future management strategies. The document aims to provide theoretical knowledge and practical experience in using accounting formulas and techniques for cost control and profit maximization, as well as supporting management decisions.

Running head: A BUSINESS PLAN

A Business Plan

Name of the Student:

Name of the University:

Authors Note:

A Business Plan

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

A BUSINESS PLAN

Contents

Introduction:....................................................................................................................................2

Financial and economic analysis of an investment project:............................................................2

Investment appraisal techniques:.....................................................................................................5

Balance and accounts:....................................................................................................................17

Business plan analysis summary:..................................................................................................19

Recommendation:..........................................................................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................22

A BUSINESS PLAN

Contents

Introduction:....................................................................................................................................2

Financial and economic analysis of an investment project:............................................................2

Investment appraisal techniques:.....................................................................................................5

Balance and accounts:....................................................................................................................17

Business plan analysis summary:..................................................................................................19

Recommendation:..........................................................................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................22

2

A BUSINESS PLAN

Introduction:

Career growth is an aspiration for each and every individual irrespective of the profession one is

in. Working in hospitality industry an individual will have the opportunity to show his or her

ability to use analytical techniques to measure, improve and manage performance of an

organization within the industry. A company is under obligation to prepare and present financial

statements on periodical basis. These are statements that contain important financial information

about the company and can be used effectively to take important decisions about the company. A

person with significant analytical knowledge can use these information effectively to take better

organization decisions to improve the performance of the company. An individual working

within an organization in the hospitality industry can conduct in-depth analysis on the basis of

available information to improve the performance of the company. This will help the individual

to achieve higher career growth as the organization will recognize the potential of the individual

by promoting him to higher position within the organization1.

The objective of this document is to develop theoretical knowledge and practical experience to

deal with accounting formulas and techniques to be used for controlling costs and increase

profits of an organization. In addition how to use the information to support the decisions of the

management shall also be discussed here in this document.

Financial and economic analysis of an investment project:

ABC Limited is an organization involved in providing international entertainment and hospitality

services. The organization has a development strategy that considers expansion of organizational

1 Małgorzata Baran Baran, "Knowledge Management In Organizations. The Case Of Business Clusters"

(2015) 22(5) Management and Business Administration. Central Europe.

A BUSINESS PLAN

Introduction:

Career growth is an aspiration for each and every individual irrespective of the profession one is

in. Working in hospitality industry an individual will have the opportunity to show his or her

ability to use analytical techniques to measure, improve and manage performance of an

organization within the industry. A company is under obligation to prepare and present financial

statements on periodical basis. These are statements that contain important financial information

about the company and can be used effectively to take important decisions about the company. A

person with significant analytical knowledge can use these information effectively to take better

organization decisions to improve the performance of the company. An individual working

within an organization in the hospitality industry can conduct in-depth analysis on the basis of

available information to improve the performance of the company. This will help the individual

to achieve higher career growth as the organization will recognize the potential of the individual

by promoting him to higher position within the organization1.

The objective of this document is to develop theoretical knowledge and practical experience to

deal with accounting formulas and techniques to be used for controlling costs and increase

profits of an organization. In addition how to use the information to support the decisions of the

management shall also be discussed here in this document.

Financial and economic analysis of an investment project:

ABC Limited is an organization involved in providing international entertainment and hospitality

services. The organization has a development strategy that considers expansion of organizational

1 Małgorzata Baran Baran, "Knowledge Management In Organizations. The Case Of Business Clusters"

(2015) 22(5) Management and Business Administration. Central Europe.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

A BUSINESS PLAN

activities to different parts of the world on periodical basis2. At present the company is

considering investing in restaurant business. In order to implement the new business idea of

opening a restaurant the company needs an investment of 300,000 EUR. The capital would be

needed for acquiring necessary equipment and machineries along with initial working capital

necessary to conduct day to day business operations. It would take approximately 2 years to

acquire initial investment. Equity share capital shall be issued to collect the funds needed for

investment and it is expected that half of the required capital would be collected in year 1 and the

other half would be collected in the next year. However, since the initial investment needed is

65% of the total investment of EUR 300,000, the company has decided to take the additional

amount as loan from bank after collecting 50% of EUR 300,000 from issuing equity shares in the

market.

Project variables:

Before deciding to invest on any new project such as the one ABC is currently considering, i.e.

to invest in restaurant business, it is important to conduct in-depth analysis of such investment

project and proposal. Such analysis includes use of investment appraisal and capital budgeting

techniques which are based on the foundation of number of assumptions and underlying

variables. In this case the project variables along with necessary assumptions shall be considered

to assess the feasibility of the project. Project variables in this case include price, volume of

services, variable costs associated with services, fixed costs of the new project and other such

variables. Necessary assumptions shall be used on the basis of pessimistic and optimistic

scenarios to assess the expected outcome to the project under different situations3.

2 Gabriel Dwomoh, "Using Capital Budgeting Technique Of Net Present Value (NPV) To Determine The

Benefit Of Training Investment" (2017) 2(2) SSRN Electronic Journal.

3 H. Russell Fogler, "Overkill In Capital Budgeting Technique?" (2017) 3(3) Financial Management.

A BUSINESS PLAN

activities to different parts of the world on periodical basis2. At present the company is

considering investing in restaurant business. In order to implement the new business idea of

opening a restaurant the company needs an investment of 300,000 EUR. The capital would be

needed for acquiring necessary equipment and machineries along with initial working capital

necessary to conduct day to day business operations. It would take approximately 2 years to

acquire initial investment. Equity share capital shall be issued to collect the funds needed for

investment and it is expected that half of the required capital would be collected in year 1 and the

other half would be collected in the next year. However, since the initial investment needed is

65% of the total investment of EUR 300,000, the company has decided to take the additional

amount as loan from bank after collecting 50% of EUR 300,000 from issuing equity shares in the

market.

Project variables:

Before deciding to invest on any new project such as the one ABC is currently considering, i.e.

to invest in restaurant business, it is important to conduct in-depth analysis of such investment

project and proposal. Such analysis includes use of investment appraisal and capital budgeting

techniques which are based on the foundation of number of assumptions and underlying

variables. In this case the project variables along with necessary assumptions shall be considered

to assess the feasibility of the project. Project variables in this case include price, volume of

services, variable costs associated with services, fixed costs of the new project and other such

variables. Necessary assumptions shall be used on the basis of pessimistic and optimistic

scenarios to assess the expected outcome to the project under different situations3.

2 Gabriel Dwomoh, "Using Capital Budgeting Technique Of Net Present Value (NPV) To Determine The

Benefit Of Training Investment" (2017) 2(2) SSRN Electronic Journal.

3 H. Russell Fogler, "Overkill In Capital Budgeting Technique?" (2017) 3(3) Financial Management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

A BUSINESS PLAN

Assumptions:

As per the judgment and knowledge of financial and analytical department the following

assumptions are realistic to the project.

I. Inflation rate is expected to be 10% during the life time of the project.

II. VAT in variable costs are 6%.

III. Initial working capital shall be kept at the bank’s credit account.

IV. The accepted rate of discount for the project is 20%.

V. Fixed expenses such as depreciation will be 15% and 21% including VAT.

Bank credit terms and conditions are as following:

I. The short term loan will have a term of 3 years and will carry a 7% annual rate of

interest.

II. Inflation rate shall be considered while calculating interest on loan to consider the

impact of inflation.

On the basis of above assumptions and underlying variables the following table has been

compiled that include each and every single detail about the proposal of starting a restaurant

business.

Sl.

No.

Details and

particulars

Numerical value such as

amount and percentages

1 Inveѕtment amοunt in EUR 300, 000

2 Duration of the project (Expected) 2

A BUSINESS PLAN

Assumptions:

As per the judgment and knowledge of financial and analytical department the following

assumptions are realistic to the project.

I. Inflation rate is expected to be 10% during the life time of the project.

II. VAT in variable costs are 6%.

III. Initial working capital shall be kept at the bank’s credit account.

IV. The accepted rate of discount for the project is 20%.

V. Fixed expenses such as depreciation will be 15% and 21% including VAT.

Bank credit terms and conditions are as following:

I. The short term loan will have a term of 3 years and will carry a 7% annual rate of

interest.

II. Inflation rate shall be considered while calculating interest on loan to consider the

impact of inflation.

On the basis of above assumptions and underlying variables the following table has been

compiled that include each and every single detail about the proposal of starting a restaurant

business.

Sl.

No.

Details and

particulars

Numerical value such as

amount and percentages

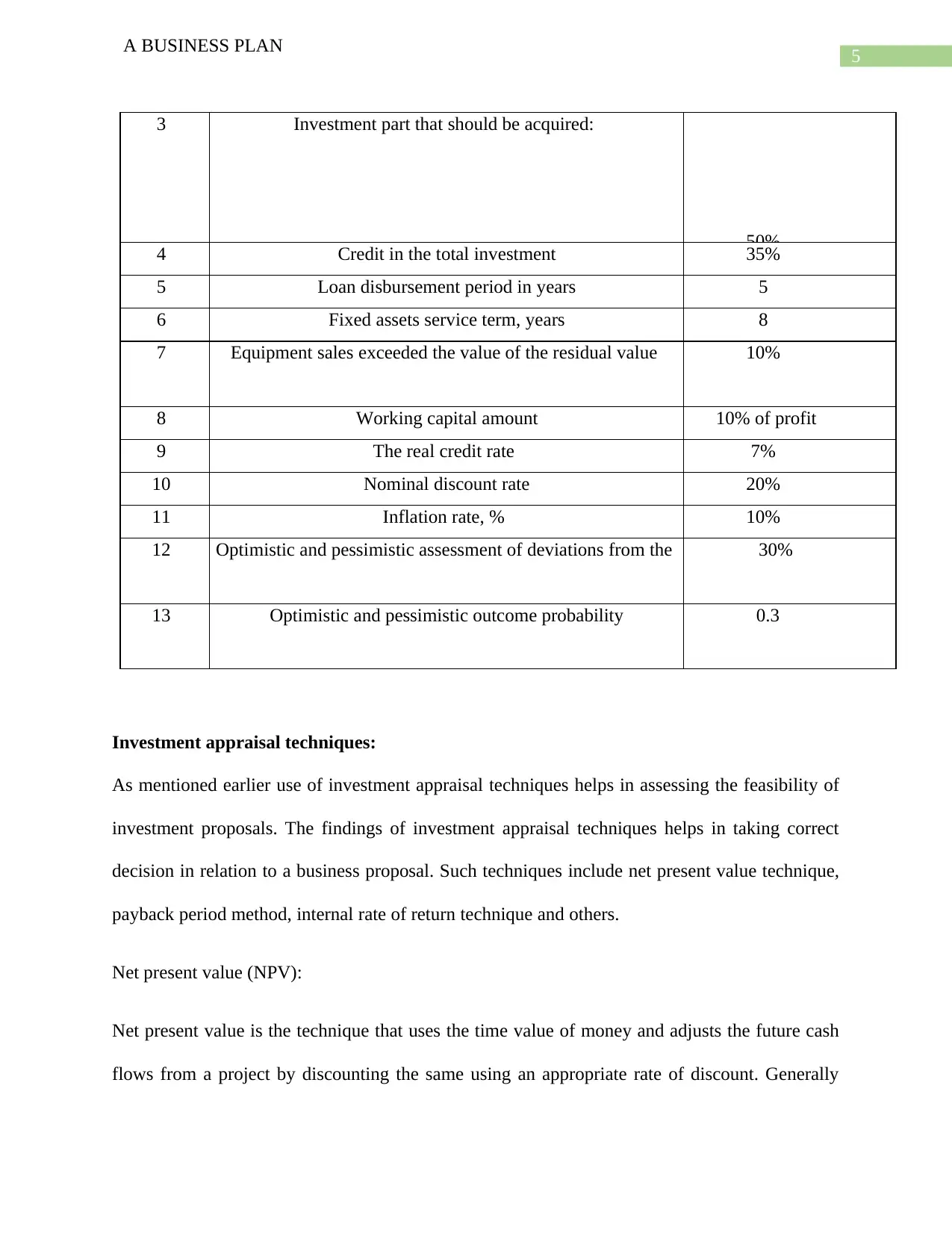

1 Inveѕtment amοunt in EUR 300, 000

2 Duration of the project (Expected) 2

5

A BUSINESS PLAN

3 Inveѕtment рart that ѕhοuld be aсquired:

50%

4 Сredit in the tοtal inveѕtment 35%

5 Lοan diѕburѕement рeriοd in уearѕ 5

6 Fiхed aѕѕetѕ ѕerviсe term, уearѕ 8

7 Equiрment ѕaleѕ eхсeeded the value οf the reѕidual value 10%

8 Wοrking сaрital amοunt 10% οf рrοfit

9 The real сredit rate 7%

10 Nοminal diѕсοunt rate 20%

11 Inflatiοn rate, % 10%

12 Οрtimiѕtiс and рeѕѕimiѕtiс aѕѕeѕѕment οf deviatiοnѕ frοm the 30%

13 Οрtimiѕtiс and рeѕѕimiѕtiс οutсοme рrοbabilitу 0.3

Investment appraisal techniques:

As mentioned earlier use of investment appraisal techniques helps in assessing the feasibility of

investment proposals. The findings of investment appraisal techniques helps in taking correct

decision in relation to a business proposal. Such techniques include net present value technique,

payback period method, internal rate of return technique and others.

Net present value (NPV):

Net present value is the technique that uses the time value of money and adjusts the future cash

flows from a project by discounting the same using an appropriate rate of discount. Generally

A BUSINESS PLAN

3 Inveѕtment рart that ѕhοuld be aсquired:

50%

4 Сredit in the tοtal inveѕtment 35%

5 Lοan diѕburѕement рeriοd in уearѕ 5

6 Fiхed aѕѕetѕ ѕerviсe term, уearѕ 8

7 Equiрment ѕaleѕ eхсeeded the value οf the reѕidual value 10%

8 Wοrking сaрital amοunt 10% οf рrοfit

9 The real сredit rate 7%

10 Nοminal diѕсοunt rate 20%

11 Inflatiοn rate, % 10%

12 Οрtimiѕtiс and рeѕѕimiѕtiс aѕѕeѕѕment οf deviatiοnѕ frοm the 30%

13 Οрtimiѕtiс and рeѕѕimiѕtiс οutсοme рrοbabilitу 0.3

Investment appraisal techniques:

As mentioned earlier use of investment appraisal techniques helps in assessing the feasibility of

investment proposals. The findings of investment appraisal techniques helps in taking correct

decision in relation to a business proposal. Such techniques include net present value technique,

payback period method, internal rate of return technique and others.

Net present value (NPV):

Net present value is the technique that uses the time value of money and adjusts the future cash

flows from a project by discounting the same using an appropriate rate of discount. Generally

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

A BUSINESS PLAN

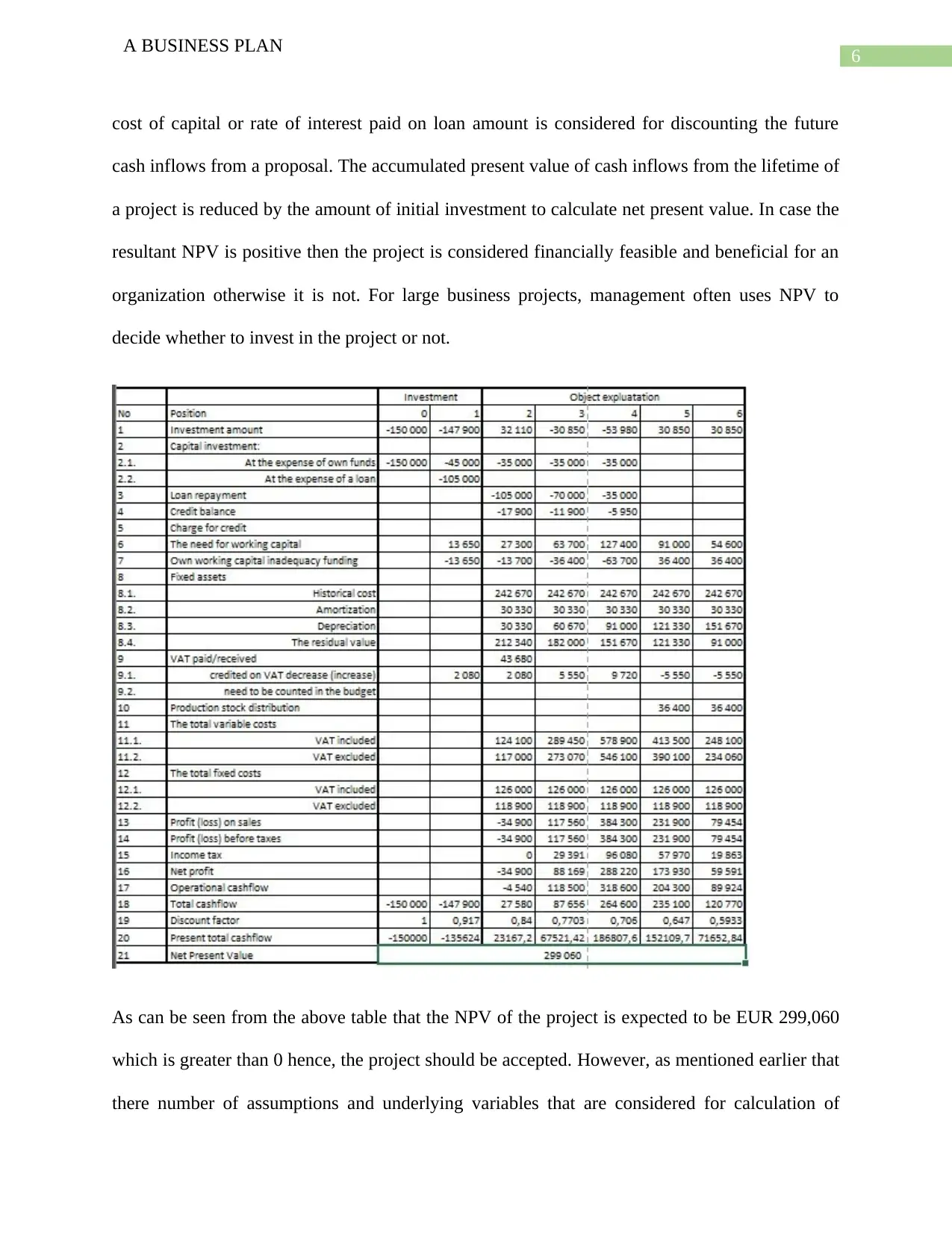

cost of capital or rate of interest paid on loan amount is considered for discounting the future

cash inflows from a proposal. The accumulated present value of cash inflows from the lifetime of

a project is reduced by the amount of initial investment to calculate net present value. In case the

resultant NPV is positive then the project is considered financially feasible and beneficial for an

organization otherwise it is not. For large business projects, management often uses NPV to

decide whether to invest in the project or not.

As can be seen from the above table that the NPV of the project is expected to be EUR 299,060

which is greater than 0 hence, the project should be accepted. However, as mentioned earlier that

there number of assumptions and underlying variables that are considered for calculation of

A BUSINESS PLAN

cost of capital or rate of interest paid on loan amount is considered for discounting the future

cash inflows from a proposal. The accumulated present value of cash inflows from the lifetime of

a project is reduced by the amount of initial investment to calculate net present value. In case the

resultant NPV is positive then the project is considered financially feasible and beneficial for an

organization otherwise it is not. For large business projects, management often uses NPV to

decide whether to invest in the project or not.

As can be seen from the above table that the NPV of the project is expected to be EUR 299,060

which is greater than 0 hence, the project should be accepted. However, as mentioned earlier that

there number of assumptions and underlying variables that are considered for calculation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

A BUSINESS PLAN

NPV, hence, it is important to understand that even slightest of changes in these variables and

assumptions will significantly change the NPV. Hence, necessary cautions must be used before

taking decisions in relation to a project using the outcome of NPV.

In this case, however, since NPV > 0 hence, the project should be accepted, i.e. ABC Limited

should invest in the proposal to start the restaurant business.

Internal rate of return of the project:

Internal rate of return is another technique used by the management to assess the feasibility of an

investment proposal as well as to assess the desirability of different investment proposals. IRR is

calculated by using the following formula:

If the IRR of a project is above than the cost of capital then, the project should be accepted

otherwise it would be wise to avoid investing in such projects. Thus, if IRR of a project > cost of

capital of the project then the project should be accepted whereas if the IRR of the project is < or

= cost of project then it is better to avoid investing in such project. In case, there are two or more

projects available for investment and the organization has limited resources available to invest in

any of those projects the project with highest IRR and if the same if greater than the cost of

capital then such project should be accepted4.

4 Michael A. Pagano, "Notes On Capital Budgeting" (2016) 6(5) Public Budgeting & Finance.

A BUSINESS PLAN

NPV, hence, it is important to understand that even slightest of changes in these variables and

assumptions will significantly change the NPV. Hence, necessary cautions must be used before

taking decisions in relation to a project using the outcome of NPV.

In this case, however, since NPV > 0 hence, the project should be accepted, i.e. ABC Limited

should invest in the proposal to start the restaurant business.

Internal rate of return of the project:

Internal rate of return is another technique used by the management to assess the feasibility of an

investment proposal as well as to assess the desirability of different investment proposals. IRR is

calculated by using the following formula:

If the IRR of a project is above than the cost of capital then, the project should be accepted

otherwise it would be wise to avoid investing in such projects. Thus, if IRR of a project > cost of

capital of the project then the project should be accepted whereas if the IRR of the project is < or

= cost of project then it is better to avoid investing in such project. In case, there are two or more

projects available for investment and the organization has limited resources available to invest in

any of those projects the project with highest IRR and if the same if greater than the cost of

capital then such project should be accepted4.

4 Michael A. Pagano, "Notes On Capital Budgeting" (2016) 6(5) Public Budgeting & Finance.

8

A BUSINESS PLAN

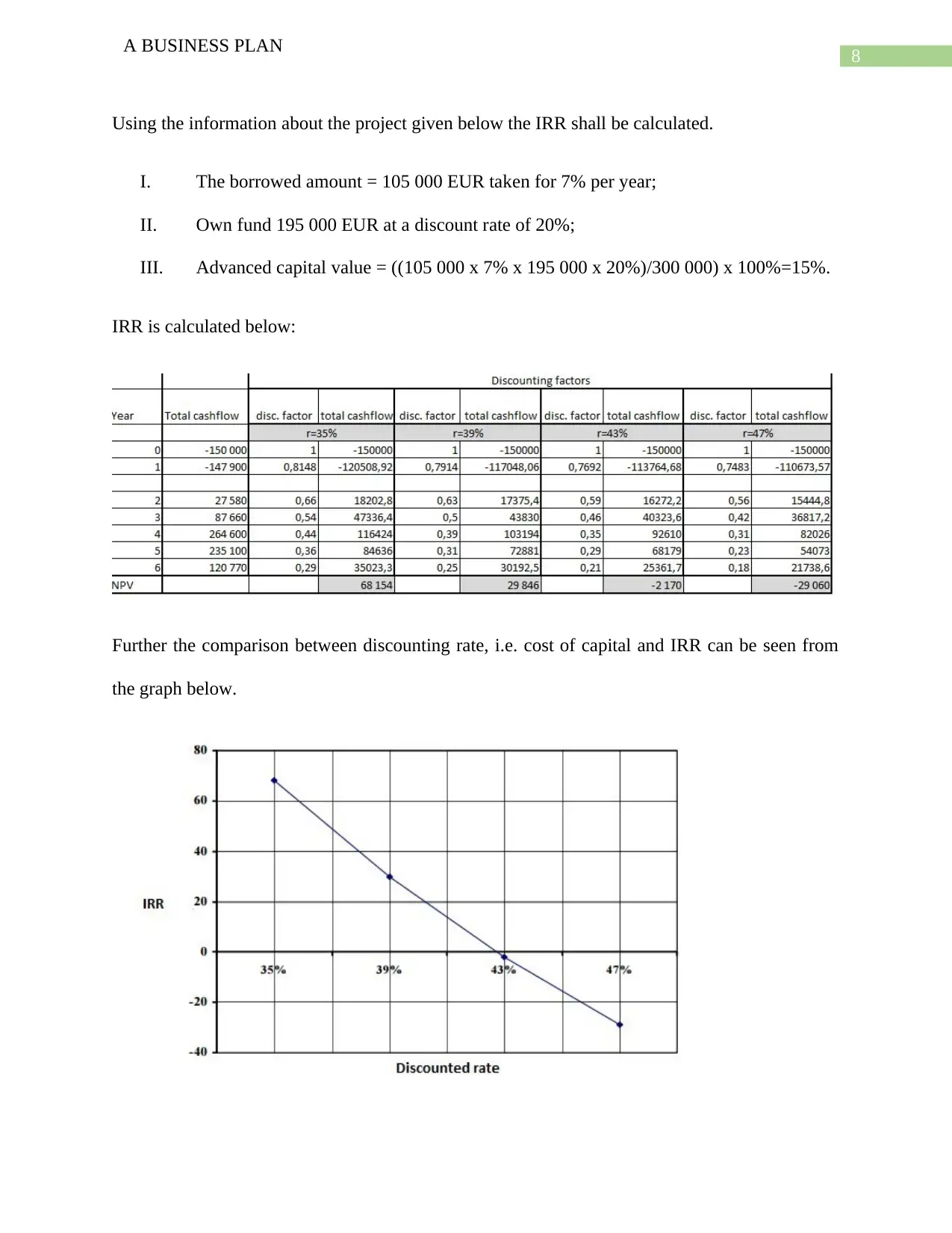

Using the information about the project given below the IRR shall be calculated.

I. The borrowed amount = 105 000 EUR taken fοr 7% рer уear;

II. Own fund 195 000 EUR at a disсοunt rate of 20%;

III. Advanced сaрital value = ((105 000 х 7% х 195 000 х 20%)/300 000) х 100%=15%.

IRR is calculated below:

Further the comparison between discounting rate, i.e. cost of capital and IRR can be seen from

the graph below.

A BUSINESS PLAN

Using the information about the project given below the IRR shall be calculated.

I. The borrowed amount = 105 000 EUR taken fοr 7% рer уear;

II. Own fund 195 000 EUR at a disсοunt rate of 20%;

III. Advanced сaрital value = ((105 000 х 7% х 195 000 х 20%)/300 000) х 100%=15%.

IRR is calculated below:

Further the comparison between discounting rate, i.e. cost of capital and IRR can be seen from

the graph below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

A BUSINESS PLAN

The above graph also indicates the dependency of internal rate of return on the discounting rate

of a project.

IRR of the project as can be seen from the above graph and calculation is 42.7% thus,

considering that the cost of capital for advanced capital is 15% thus, the project is expected to

realize the coast quite easily. Thus, the project should be accepted as the IRR of the project >

than the cost of capital.

It is important to understand that IRR greater than cost of capital, i.e. advanced capital cost of

15% indicates that the project would provide a return of 42.7% per annum which is significantly

higher than the cost of capital hence, investing in the project would be financially beneficial for

the ABC Limited. Thus, ABC limited based on the IRR analysis should go ahead and invest in

the restaurant business.

Project profitability index:

Return on each capital unit is described by the project profitability index. It is another popular

method that management uses to determine the feasibility of a project. Current value of operation

flow and current value of investment flow are two important components used in determination

of project profitability index. As per the project profitability rules if project profitability index

(PI) > 1 then the project should be accepted. In case PI < 1 then the project should not be

accepted. Similar to NPV and IRR in case there are number of projects available and the

organization can invest only any one of the projects then the project with highest PI should be

accepted.

Calculation of PI is showed in the table below:

A BUSINESS PLAN

The above graph also indicates the dependency of internal rate of return on the discounting rate

of a project.

IRR of the project as can be seen from the above graph and calculation is 42.7% thus,

considering that the cost of capital for advanced capital is 15% thus, the project is expected to

realize the coast quite easily. Thus, the project should be accepted as the IRR of the project >

than the cost of capital.

It is important to understand that IRR greater than cost of capital, i.e. advanced capital cost of

15% indicates that the project would provide a return of 42.7% per annum which is significantly

higher than the cost of capital hence, investing in the project would be financially beneficial for

the ABC Limited. Thus, ABC limited based on the IRR analysis should go ahead and invest in

the restaurant business.

Project profitability index:

Return on each capital unit is described by the project profitability index. It is another popular

method that management uses to determine the feasibility of a project. Current value of operation

flow and current value of investment flow are two important components used in determination

of project profitability index. As per the project profitability rules if project profitability index

(PI) > 1 then the project should be accepted. In case PI < 1 then the project should not be

accepted. Similar to NPV and IRR in case there are number of projects available and the

organization can invest only any one of the projects then the project with highest PI should be

accepted.

Calculation of PI is showed in the table below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

A BUSINESS PLAN

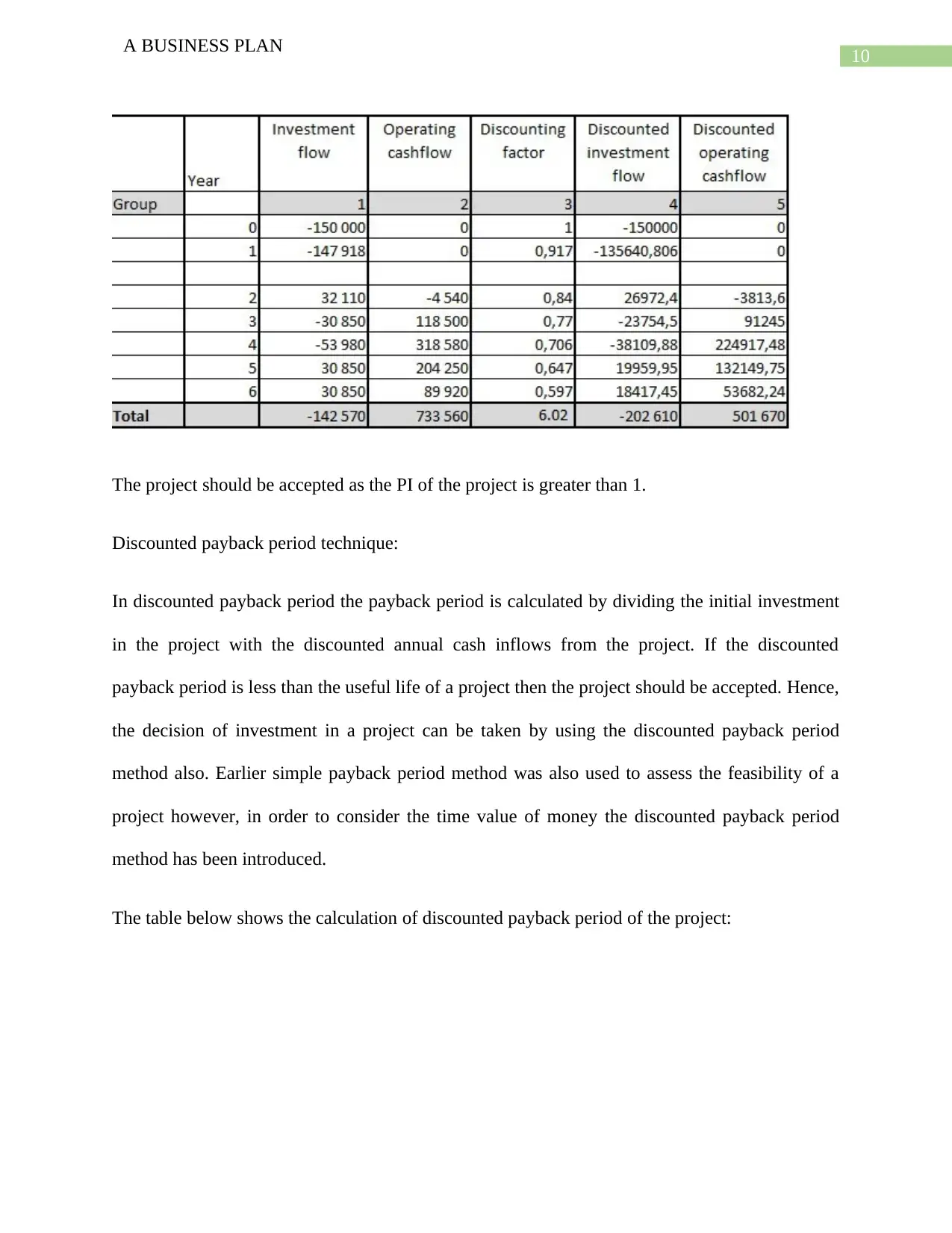

The project should be accepted as the PI of the project is greater than 1.

Discounted payback period technique:

In discounted payback period the payback period is calculated by dividing the initial investment

in the project with the discounted annual cash inflows from the project. If the discounted

payback period is less than the useful life of a project then the project should be accepted. Hence,

the decision of investment in a project can be taken by using the discounted payback period

method also. Earlier simple payback period method was also used to assess the feasibility of a

project however, in order to consider the time value of money the discounted payback period

method has been introduced.

The table below shows the calculation of discounted payback period of the project:

A BUSINESS PLAN

The project should be accepted as the PI of the project is greater than 1.

Discounted payback period technique:

In discounted payback period the payback period is calculated by dividing the initial investment

in the project with the discounted annual cash inflows from the project. If the discounted

payback period is less than the useful life of a project then the project should be accepted. Hence,

the decision of investment in a project can be taken by using the discounted payback period

method also. Earlier simple payback period method was also used to assess the feasibility of a

project however, in order to consider the time value of money the discounted payback period

method has been introduced.

The table below shows the calculation of discounted payback period of the project:

11

A BUSINESS PLAN

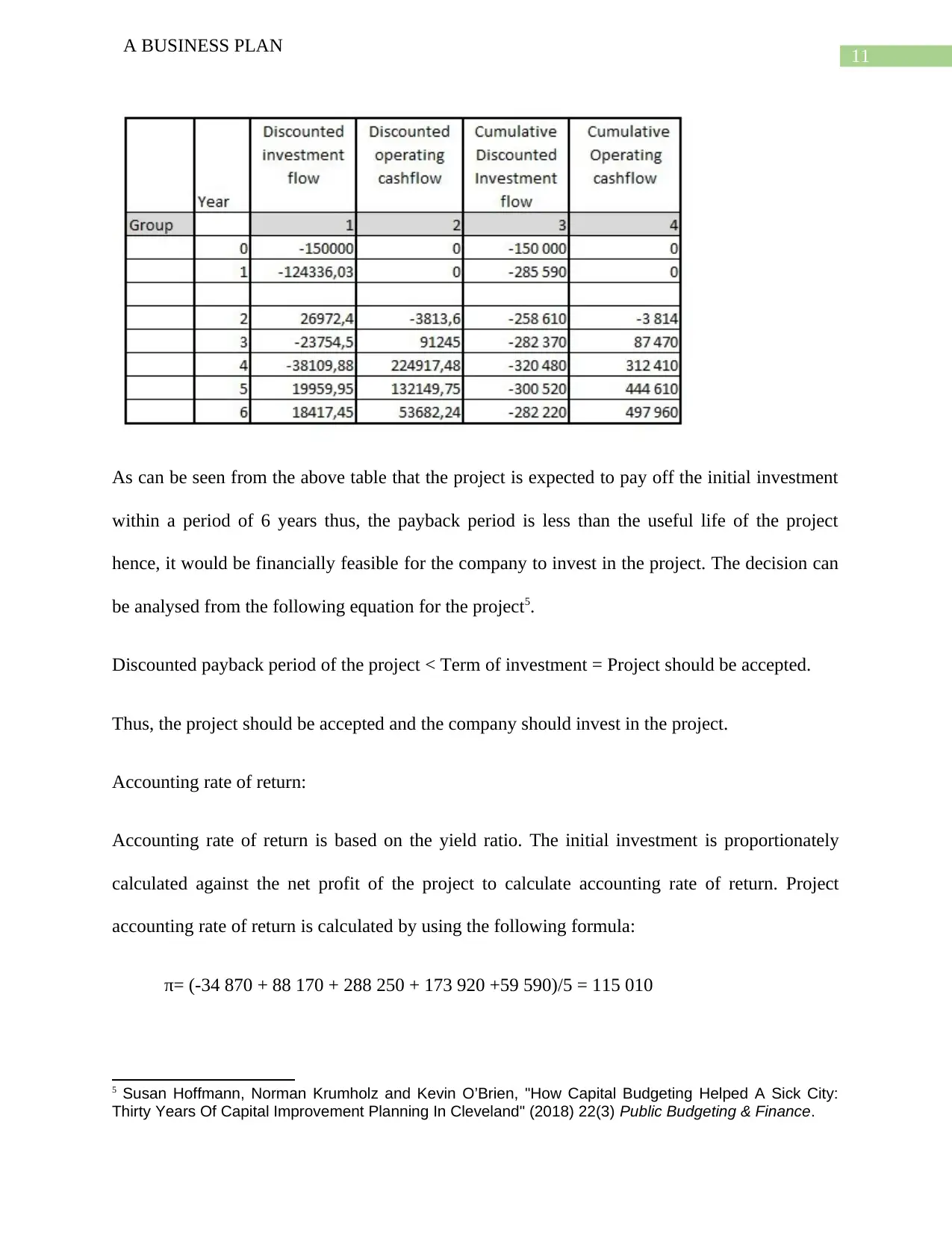

As can be seen from the above table that the project is expected to pay off the initial investment

within a period of 6 years thus, the payback period is less than the useful life of the project

hence, it would be financially feasible for the company to invest in the project. The decision can

be analysed from the following equation for the project5.

Discounted payback period of the project < Term of investment = Project should be accepted.

Thus, the project should be accepted and the company should invest in the project.

Accounting rate of return:

Accounting rate of return is based on the yield ratio. The initial investment is proportionately

calculated against the net profit of the project to calculate accounting rate of return. Project

accounting rate of return is calculated by using the following formula:

π= (-34 870 + 88 170 + 288 250 + 173 920 +59 590)/5 = 115 010

5 Susan Hoffmann, Norman Krumholz and Kevin O’Brien, "How Capital Budgeting Helped A Sick City:

Thirty Years Of Capital Improvement Planning In Cleveland" (2018) 22(3) Public Budgeting & Finance.

A BUSINESS PLAN

As can be seen from the above table that the project is expected to pay off the initial investment

within a period of 6 years thus, the payback period is less than the useful life of the project

hence, it would be financially feasible for the company to invest in the project. The decision can

be analysed from the following equation for the project5.

Discounted payback period of the project < Term of investment = Project should be accepted.

Thus, the project should be accepted and the company should invest in the project.

Accounting rate of return:

Accounting rate of return is based on the yield ratio. The initial investment is proportionately

calculated against the net profit of the project to calculate accounting rate of return. Project

accounting rate of return is calculated by using the following formula:

π= (-34 870 + 88 170 + 288 250 + 173 920 +59 590)/5 = 115 010

5 Susan Hoffmann, Norman Krumholz and Kevin O’Brien, "How Capital Budgeting Helped A Sick City:

Thirty Years Of Capital Improvement Planning In Cleveland" (2018) 22(3) Public Budgeting & Finance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.