Comprehensive Finance Report: Houzit Pty Ltd Budget Analysis 2011-2012

VerifiedAdded on 2020/07/22

|11

|3072

|255

Report

AI Summary

This report provides a comprehensive financial analysis of Houzit Pty Ltd, examining its financial performance for the period of 2011-2012. It includes detailed analyses of the sales and profit budget, GST cash flow budget, and aged debtors budget, providing insights into the company's revenue, cost of goods sold, gross profit, and expenditures. The report also interprets the financial data, highlighting key trends and performance indicators, such as total sales, GST payable, and debtor sales percentages. Furthermore, the report discusses the organizational policies and procedures related to budgeting, reasons behind the previous year's profit and losses, effective financial management approaches, and the use of assumptions in budget preparation. It also covers tax liabilities, including income tax, fringe benefit tax, and GST, and discusses the relevant accounting standards and corporate legislation used in preparing the budgets, such as the Corporate Tax Act 2001. The report offers a detailed overview of Houzit Pty Ltd's financial position and provides recommendations for monitoring budget costs and improving financial performance.

MANAGE FINANCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.A .........................................................................................................................................1

1. Budgets are based on the organisational policies and procedures.................................3

1.B .........................................................................................................................................4

PART 2............................................................................................................................................4

1. ............................................................................................................................................4

2. ............................................................................................................................................6

3. ............................................................................................................................................6

4. ............................................................................................................................................6

5. ............................................................................................................................................7

6. ............................................................................................................................................7

7. ............................................................................................................................................7

8. ............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1.A .........................................................................................................................................1

1. Budgets are based on the organisational policies and procedures.................................3

1.B .........................................................................................................................................4

PART 2............................................................................................................................................4

1. ............................................................................................................................................4

2. ............................................................................................................................................6

3. ............................................................................................................................................6

4. ............................................................................................................................................6

5. ............................................................................................................................................7

6. ............................................................................................................................................7

7. ............................................................................................................................................7

8. ............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

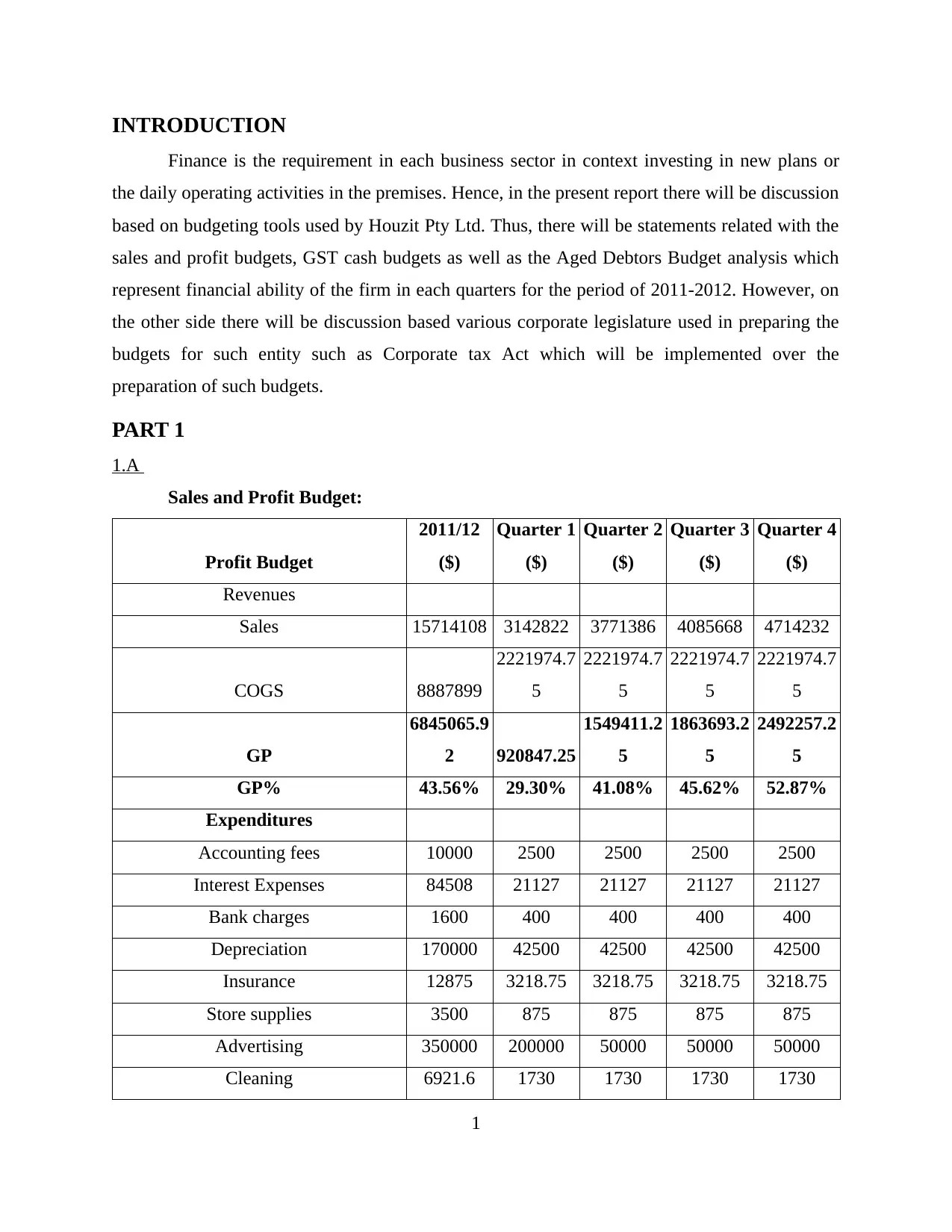

INTRODUCTION

Finance is the requirement in each business sector in context investing in new plans or

the daily operating activities in the premises. Hence, in the present report there will be discussion

based on budgeting tools used by Houzit Pty Ltd. Thus, there will be statements related with the

sales and profit budgets, GST cash budgets as well as the Aged Debtors Budget analysis which

represent financial ability of the firm in each quarters for the period of 2011-2012. However, on

the other side there will be discussion based various corporate legislature used in preparing the

budgets for such entity such as Corporate tax Act which will be implemented over the

preparation of such budgets.

PART 1

1.A

Sales and Profit Budget:

Profit Budget

2011/12

($)

Quarter 1

($)

Quarter 2

($)

Quarter 3

($)

Quarter 4

($)

Revenues

Sales 15714108 3142822 3771386 4085668 4714232

COGS 8887899

2221974.7

5

2221974.7

5

2221974.7

5

2221974.7

5

GP

6845065.9

2 920847.25

1549411.2

5

1863693.2

5

2492257.2

5

GP% 43.56% 29.30% 41.08% 45.62% 52.87%

Expenditures

Accounting fees 10000 2500 2500 2500 2500

Interest Expenses 84508 21127 21127 21127 21127

Bank charges 1600 400 400 400 400

Depreciation 170000 42500 42500 42500 42500

Insurance 12875 3218.75 3218.75 3218.75 3218.75

Store supplies 3500 875 875 875 875

Advertising 350000 200000 50000 50000 50000

Cleaning 6921.6 1730 1730 1730 1730

1

Finance is the requirement in each business sector in context investing in new plans or

the daily operating activities in the premises. Hence, in the present report there will be discussion

based on budgeting tools used by Houzit Pty Ltd. Thus, there will be statements related with the

sales and profit budgets, GST cash budgets as well as the Aged Debtors Budget analysis which

represent financial ability of the firm in each quarters for the period of 2011-2012. However, on

the other side there will be discussion based various corporate legislature used in preparing the

budgets for such entity such as Corporate tax Act which will be implemented over the

preparation of such budgets.

PART 1

1.A

Sales and Profit Budget:

Profit Budget

2011/12

($)

Quarter 1

($)

Quarter 2

($)

Quarter 3

($)

Quarter 4

($)

Revenues

Sales 15714108 3142822 3771386 4085668 4714232

COGS 8887899

2221974.7

5

2221974.7

5

2221974.7

5

2221974.7

5

GP

6845065.9

2 920847.25

1549411.2

5

1863693.2

5

2492257.2

5

GP% 43.56% 29.30% 41.08% 45.62% 52.87%

Expenditures

Accounting fees 10000 2500 2500 2500 2500

Interest Expenses 84508 21127 21127 21127 21127

Bank charges 1600 400 400 400 400

Depreciation 170000 42500 42500 42500 42500

Insurance 12875 3218.75 3218.75 3218.75 3218.75

Store supplies 3500 875 875 875 875

Advertising 350000 200000 50000 50000 50000

Cleaning 6921.6 1730 1730 1730 1730

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Repairs and Maintenance 118656 29664 29664 29664 29664

Rent 2538950 634737.5 634737.5 634737.5 634737.5

Telephone 27686.4 6922 6922 6922 6922

Electricity Expenses 49440 12360 12360 12360 12360

Luxury car Tax 40166.4 10041.6 10041.6 10041.6 10041.6

Fringe Benefit Tax 28000 7000 7000 7000 7000

Superannuation 359078 89770 89770 89770 89770

Wages and Salaries 3989760 997440 997440 997440 997440

Payroll Tax 189514 47378 47378 47378 47378

Worker's Compensation 79795 19949 19949 19949 19949

Total Expenses 8060451 2127613 1977613 1977613 1977613

Net profit before tax

-

1215384.6

8

-

1206765.4 -428201.4 -113919.4 514644.6

Income tax 839585.5 83419.13 202600.9 239691.8 313873.6

Net Profit

-

2054970.1

8

-

1290184.5

3 -630802.3 -353611.2 200771

Interpretation: By considering the above listed table based on Sale and purchase budget

for 2011-12 which provides informations related to each quarters in the year. Hence, the total

sales for thee year by considering all the quarters are amounted at $15714108. COGS can be

measured as per the adjustments of the business plan provide by Houzit Pty Ltd which states

that, it will be inverse of the changes incurred in GP. Hence, GP is reducing 1% for such period

then it can be said that the cogs of the product will be increasing 1%. There will be income taxes

levied over the income generated by the organisation in each quarter at 30% of the corporate tax.

Hence, after reducing the taxes form the income generated by the organisation in each quarter the

net profit has been obtained by the 4th quarter is for $200771.

GST CASH FLOW BUDGET

COGS 2011/12 Q1 Q2 Q3 Q4

2

Rent 2538950 634737.5 634737.5 634737.5 634737.5

Telephone 27686.4 6922 6922 6922 6922

Electricity Expenses 49440 12360 12360 12360 12360

Luxury car Tax 40166.4 10041.6 10041.6 10041.6 10041.6

Fringe Benefit Tax 28000 7000 7000 7000 7000

Superannuation 359078 89770 89770 89770 89770

Wages and Salaries 3989760 997440 997440 997440 997440

Payroll Tax 189514 47378 47378 47378 47378

Worker's Compensation 79795 19949 19949 19949 19949

Total Expenses 8060451 2127613 1977613 1977613 1977613

Net profit before tax

-

1215384.6

8

-

1206765.4 -428201.4 -113919.4 514644.6

Income tax 839585.5 83419.13 202600.9 239691.8 313873.6

Net Profit

-

2054970.1

8

-

1290184.5

3 -630802.3 -353611.2 200771

Interpretation: By considering the above listed table based on Sale and purchase budget

for 2011-12 which provides informations related to each quarters in the year. Hence, the total

sales for thee year by considering all the quarters are amounted at $15714108. COGS can be

measured as per the adjustments of the business plan provide by Houzit Pty Ltd which states

that, it will be inverse of the changes incurred in GP. Hence, GP is reducing 1% for such period

then it can be said that the cogs of the product will be increasing 1%. There will be income taxes

levied over the income generated by the organisation in each quarter at 30% of the corporate tax.

Hence, after reducing the taxes form the income generated by the organisation in each quarter the

net profit has been obtained by the 4th quarter is for $200771.

GST CASH FLOW BUDGET

COGS 2011/12 Q1 Q2 Q3 Q4

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

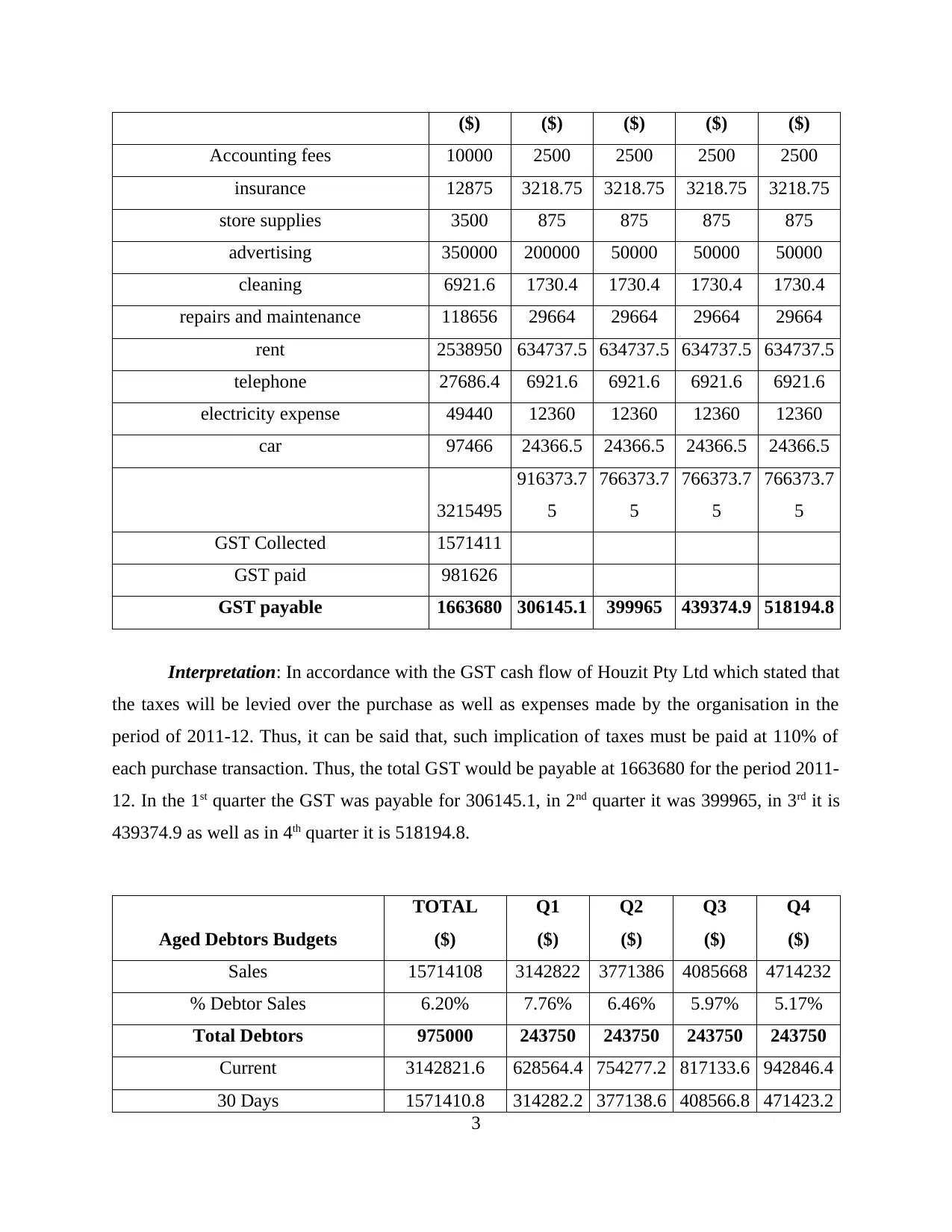

($) ($) ($) ($) ($)

Accounting fees 10000 2500 2500 2500 2500

insurance 12875 3218.75 3218.75 3218.75 3218.75

store supplies 3500 875 875 875 875

advertising 350000 200000 50000 50000 50000

cleaning 6921.6 1730.4 1730.4 1730.4 1730.4

repairs and maintenance 118656 29664 29664 29664 29664

rent 2538950 634737.5 634737.5 634737.5 634737.5

telephone 27686.4 6921.6 6921.6 6921.6 6921.6

electricity expense 49440 12360 12360 12360 12360

car 97466 24366.5 24366.5 24366.5 24366.5

3215495

916373.7

5

766373.7

5

766373.7

5

766373.7

5

GST Collected 1571411

GST paid 981626

GST payable 1663680 306145.1 399965 439374.9 518194.8

Interpretation: In accordance with the GST cash flow of Houzit Pty Ltd which stated that

the taxes will be levied over the purchase as well as expenses made by the organisation in the

period of 2011-12. Thus, it can be said that, such implication of taxes must be paid at 110% of

each purchase transaction. Thus, the total GST would be payable at 1663680 for the period 2011-

12. In the 1st quarter the GST was payable for 306145.1, in 2nd quarter it was 399965, in 3rd it is

439374.9 as well as in 4th quarter it is 518194.8.

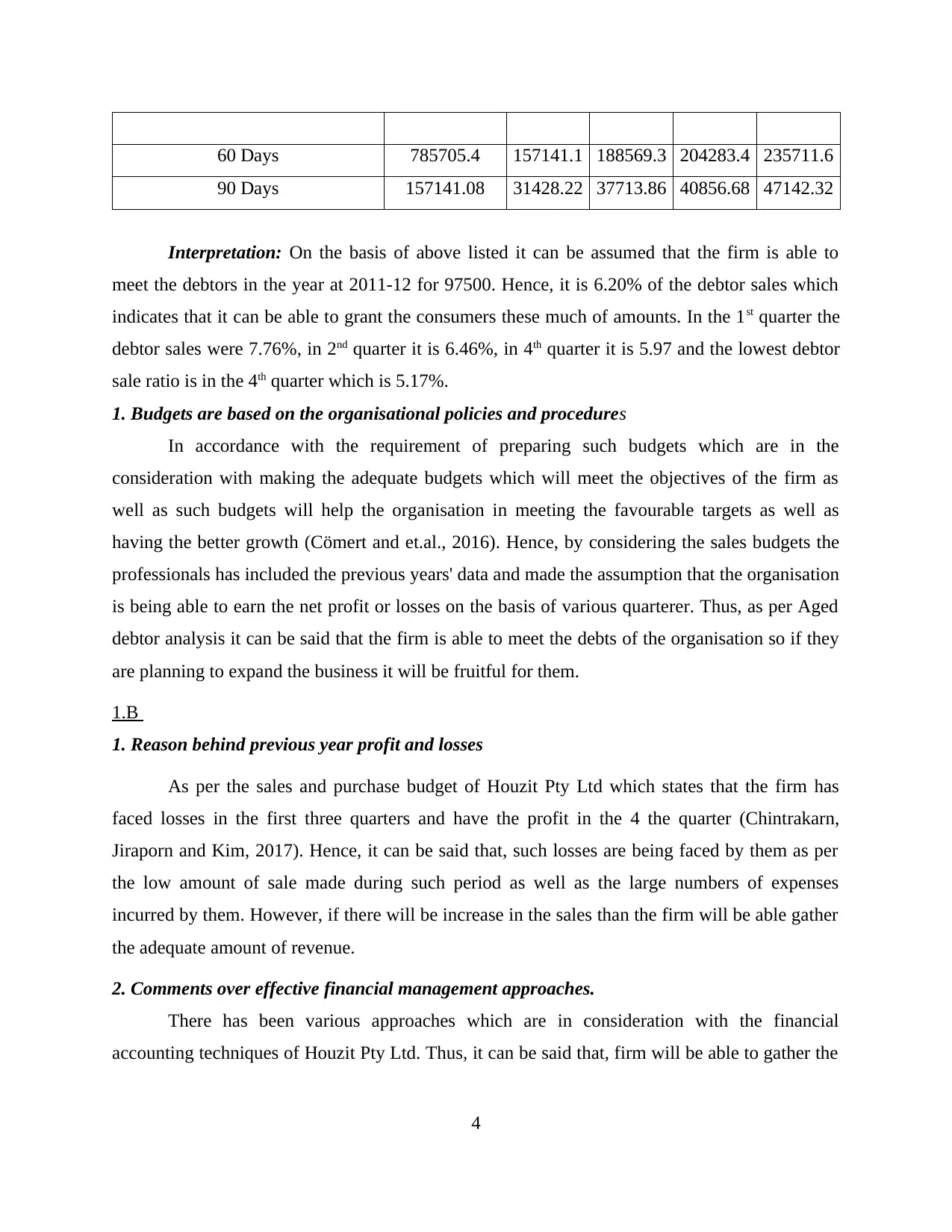

Aged Debtors Budgets

TOTAL

($)

Q1

($)

Q2

($)

Q3

($)

Q4

($)

Sales 15714108 3142822 3771386 4085668 4714232

% Debtor Sales 6.20% 7.76% 6.46% 5.97% 5.17%

Total Debtors 975000 243750 243750 243750 243750

Current 3142821.6 628564.4 754277.2 817133.6 942846.4

30 Days 1571410.8 314282.2 377138.6 408566.8 471423.2

3

Accounting fees 10000 2500 2500 2500 2500

insurance 12875 3218.75 3218.75 3218.75 3218.75

store supplies 3500 875 875 875 875

advertising 350000 200000 50000 50000 50000

cleaning 6921.6 1730.4 1730.4 1730.4 1730.4

repairs and maintenance 118656 29664 29664 29664 29664

rent 2538950 634737.5 634737.5 634737.5 634737.5

telephone 27686.4 6921.6 6921.6 6921.6 6921.6

electricity expense 49440 12360 12360 12360 12360

car 97466 24366.5 24366.5 24366.5 24366.5

3215495

916373.7

5

766373.7

5

766373.7

5

766373.7

5

GST Collected 1571411

GST paid 981626

GST payable 1663680 306145.1 399965 439374.9 518194.8

Interpretation: In accordance with the GST cash flow of Houzit Pty Ltd which stated that

the taxes will be levied over the purchase as well as expenses made by the organisation in the

period of 2011-12. Thus, it can be said that, such implication of taxes must be paid at 110% of

each purchase transaction. Thus, the total GST would be payable at 1663680 for the period 2011-

12. In the 1st quarter the GST was payable for 306145.1, in 2nd quarter it was 399965, in 3rd it is

439374.9 as well as in 4th quarter it is 518194.8.

Aged Debtors Budgets

TOTAL

($)

Q1

($)

Q2

($)

Q3

($)

Q4

($)

Sales 15714108 3142822 3771386 4085668 4714232

% Debtor Sales 6.20% 7.76% 6.46% 5.97% 5.17%

Total Debtors 975000 243750 243750 243750 243750

Current 3142821.6 628564.4 754277.2 817133.6 942846.4

30 Days 1571410.8 314282.2 377138.6 408566.8 471423.2

3

60 Days 785705.4 157141.1 188569.3 204283.4 235711.6

90 Days 157141.08 31428.22 37713.86 40856.68 47142.32

Interpretation: On the basis of above listed it can be assumed that the firm is able to

meet the debtors in the year at 2011-12 for 97500. Hence, it is 6.20% of the debtor sales which

indicates that it can be able to grant the consumers these much of amounts. In the 1st quarter the

debtor sales were 7.76%, in 2nd quarter it is 6.46%, in 4th quarter it is 5.97 and the lowest debtor

sale ratio is in the 4th quarter which is 5.17%.

1. Budgets are based on the organisational policies and procedures

In accordance with the requirement of preparing such budgets which are in the

consideration with making the adequate budgets which will meet the objectives of the firm as

well as such budgets will help the organisation in meeting the favourable targets as well as

having the better growth (Cömert and et.al., 2016). Hence, by considering the sales budgets the

professionals has included the previous years' data and made the assumption that the organisation

is being able to earn the net profit or losses on the basis of various quarterer. Thus, as per Aged

debtor analysis it can be said that the firm is able to meet the debts of the organisation so if they

are planning to expand the business it will be fruitful for them.

1.B

1. Reason behind previous year profit and losses

As per the sales and purchase budget of Houzit Pty Ltd which states that the firm has

faced losses in the first three quarters and have the profit in the 4 the quarter (Chintrakarn,

Jiraporn and Kim, 2017). Hence, it can be said that, such losses are being faced by them as per

the low amount of sale made during such period as well as the large numbers of expenses

incurred by them. However, if there will be increase in the sales than the firm will be able gather

the adequate amount of revenue.

2. Comments over effective financial management approaches.

There has been various approaches which are in consideration with the financial

accounting techniques of Houzit Pty Ltd. Thus, it can be said that, firm will be able to gather the

4

90 Days 157141.08 31428.22 37713.86 40856.68 47142.32

Interpretation: On the basis of above listed it can be assumed that the firm is able to

meet the debtors in the year at 2011-12 for 97500. Hence, it is 6.20% of the debtor sales which

indicates that it can be able to grant the consumers these much of amounts. In the 1st quarter the

debtor sales were 7.76%, in 2nd quarter it is 6.46%, in 4th quarter it is 5.97 and the lowest debtor

sale ratio is in the 4th quarter which is 5.17%.

1. Budgets are based on the organisational policies and procedures

In accordance with the requirement of preparing such budgets which are in the

consideration with making the adequate budgets which will meet the objectives of the firm as

well as such budgets will help the organisation in meeting the favourable targets as well as

having the better growth (Cömert and et.al., 2016). Hence, by considering the sales budgets the

professionals has included the previous years' data and made the assumption that the organisation

is being able to earn the net profit or losses on the basis of various quarterer. Thus, as per Aged

debtor analysis it can be said that the firm is able to meet the debts of the organisation so if they

are planning to expand the business it will be fruitful for them.

1.B

1. Reason behind previous year profit and losses

As per the sales and purchase budget of Houzit Pty Ltd which states that the firm has

faced losses in the first three quarters and have the profit in the 4 the quarter (Chintrakarn,

Jiraporn and Kim, 2017). Hence, it can be said that, such losses are being faced by them as per

the low amount of sale made during such period as well as the large numbers of expenses

incurred by them. However, if there will be increase in the sales than the firm will be able gather

the adequate amount of revenue.

2. Comments over effective financial management approaches.

There has been various approaches which are in consideration with the financial

accounting techniques of Houzit Pty Ltd. Thus, it can be said that, firm will be able to gather the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

large numbers of investors as well as have the increment in the capital gathering if they will

make innovative decisions which helps in enhancing the organisational efficiency.

3. Use of all assumption in preparing the budgets

On the basis of such budgets it can be assumed that the firm is not bale to earn the

adequate amount of net profit in the first 3 quarters. Hence, they need to make changes in the

selling techniques as well as need to lower down the expenses of the firm. However, it

accordance with Aged debtor budget it can be said that the firm will be able to make payments to

its debtors in the long run (John, 2017). Hence, it will create the favourable image of the

organisation in the future so it will be assumed that they will be able gain the better capital

revenue.

4. Relevant notes to monitor the budget costs

To monitor or execute the budgets of Houzit Pty Ltd it can be said that, the firm is need

to make fruitful changes in operational activities such as they would need to implemented

various techniques which will enhances the sales of the organisation (Shank and Vianna, 2016).

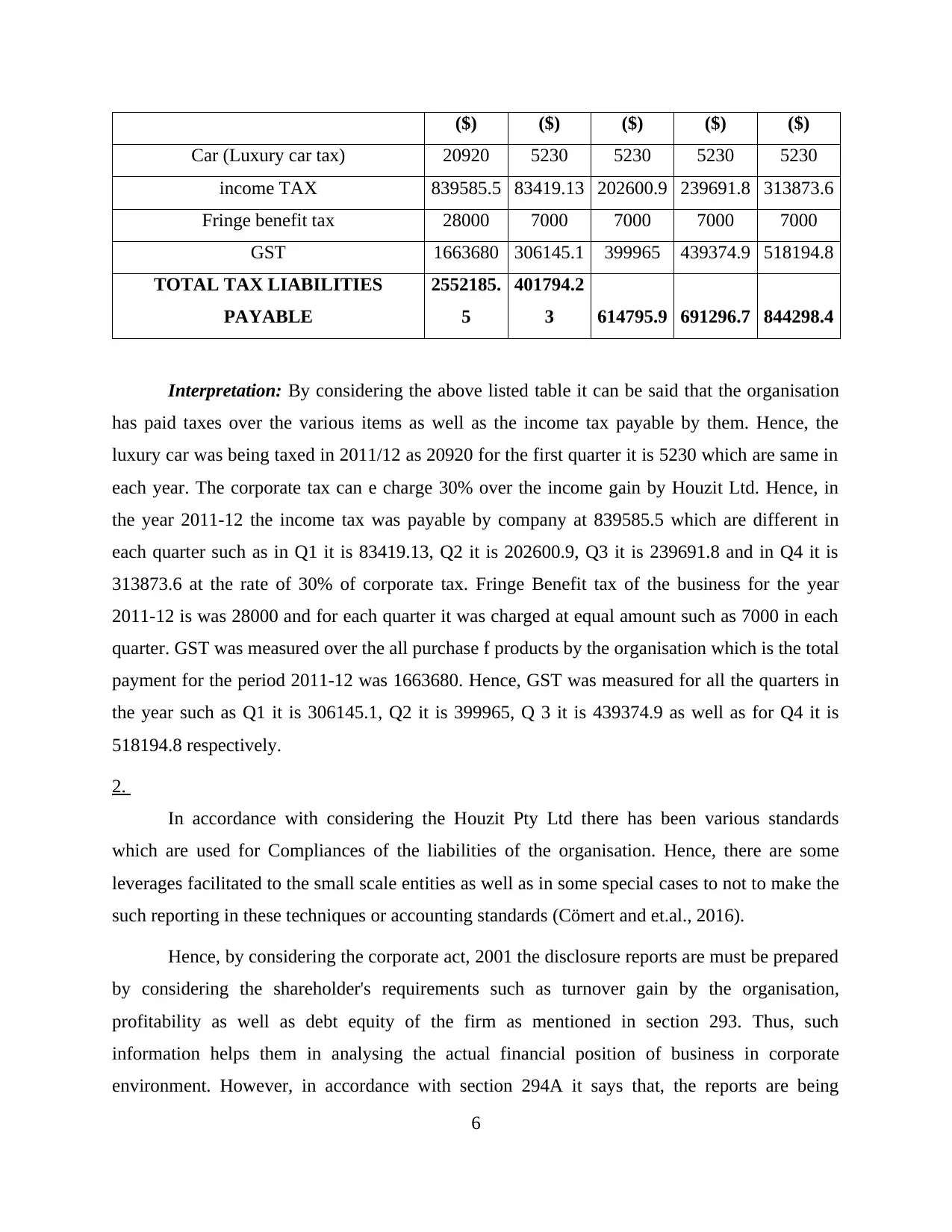

PART 2

1.

Taxes were been levied on the overall activities held in the organisation such as income

tax over the revenue gathered by firm after including all the income or expenses. Hence, GST

(General sale tax) were levied over all the goods of company. Thus, the accounting information

system includes that input tax credit must be included in GST for such period. However, the

taxes can be measure and collected over the purchase of assets and stock in context of the

business as well as the amount id being collected from such activities must be paid in accordance

with the assessment year. Hence, as per the federal legislation of ATO there has been various

rules and regulation In context with making the adequate payments of taxes for corporation and

individual. Thus, in Houzit Pty Ltd the taxes will be paid such as 30% of the corporate tax as

well as payroll tax for 4.75% over the wages and salaries paid by organisation. By considering

the tax liabilities of Houzit Pty Ltd which are facilitated for statutory requirements are mentioned

below such as:

Tax liabilities list 2011/12 Q1 Q2 Q3 Q4

5

make innovative decisions which helps in enhancing the organisational efficiency.

3. Use of all assumption in preparing the budgets

On the basis of such budgets it can be assumed that the firm is not bale to earn the

adequate amount of net profit in the first 3 quarters. Hence, they need to make changes in the

selling techniques as well as need to lower down the expenses of the firm. However, it

accordance with Aged debtor budget it can be said that the firm will be able to make payments to

its debtors in the long run (John, 2017). Hence, it will create the favourable image of the

organisation in the future so it will be assumed that they will be able gain the better capital

revenue.

4. Relevant notes to monitor the budget costs

To monitor or execute the budgets of Houzit Pty Ltd it can be said that, the firm is need

to make fruitful changes in operational activities such as they would need to implemented

various techniques which will enhances the sales of the organisation (Shank and Vianna, 2016).

PART 2

1.

Taxes were been levied on the overall activities held in the organisation such as income

tax over the revenue gathered by firm after including all the income or expenses. Hence, GST

(General sale tax) were levied over all the goods of company. Thus, the accounting information

system includes that input tax credit must be included in GST for such period. However, the

taxes can be measure and collected over the purchase of assets and stock in context of the

business as well as the amount id being collected from such activities must be paid in accordance

with the assessment year. Hence, as per the federal legislation of ATO there has been various

rules and regulation In context with making the adequate payments of taxes for corporation and

individual. Thus, in Houzit Pty Ltd the taxes will be paid such as 30% of the corporate tax as

well as payroll tax for 4.75% over the wages and salaries paid by organisation. By considering

the tax liabilities of Houzit Pty Ltd which are facilitated for statutory requirements are mentioned

below such as:

Tax liabilities list 2011/12 Q1 Q2 Q3 Q4

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

($) ($) ($) ($) ($)

Car (Luxury car tax) 20920 5230 5230 5230 5230

income TAX 839585.5 83419.13 202600.9 239691.8 313873.6

Fringe benefit tax 28000 7000 7000 7000 7000

GST 1663680 306145.1 399965 439374.9 518194.8

TOTAL TAX LIABILITIES

PAYABLE

2552185.

5

401794.2

3 614795.9 691296.7 844298.4

Interpretation: By considering the above listed table it can be said that the organisation

has paid taxes over the various items as well as the income tax payable by them. Hence, the

luxury car was being taxed in 2011/12 as 20920 for the first quarter it is 5230 which are same in

each year. The corporate tax can e charge 30% over the income gain by Houzit Ltd. Hence, in

the year 2011-12 the income tax was payable by company at 839585.5 which are different in

each quarter such as in Q1 it is 83419.13, Q2 it is 202600.9, Q3 it is 239691.8 and in Q4 it is

313873.6 at the rate of 30% of corporate tax. Fringe Benefit tax of the business for the year

2011-12 is was 28000 and for each quarter it was charged at equal amount such as 7000 in each

quarter. GST was measured over the all purchase f products by the organisation which is the total

payment for the period 2011-12 was 1663680. Hence, GST was measured for all the quarters in

the year such as Q1 it is 306145.1, Q2 it is 399965, Q 3 it is 439374.9 as well as for Q4 it is

518194.8 respectively.

2.

In accordance with considering the Houzit Pty Ltd there has been various standards

which are used for Compliances of the liabilities of the organisation. Hence, there are some

leverages facilitated to the small scale entities as well as in some special cases to not to make the

such reporting in these techniques or accounting standards (Cömert and et.al., 2016).

Hence, by considering the corporate act, 2001 the disclosure reports are must be prepared

by considering the shareholder's requirements such as turnover gain by the organisation,

profitability as well as debt equity of the firm as mentioned in section 293. Thus, such

information helps them in analysing the actual financial position of business in corporate

environment. However, in accordance with section 294A it says that, the reports are being

6

Car (Luxury car tax) 20920 5230 5230 5230 5230

income TAX 839585.5 83419.13 202600.9 239691.8 313873.6

Fringe benefit tax 28000 7000 7000 7000 7000

GST 1663680 306145.1 399965 439374.9 518194.8

TOTAL TAX LIABILITIES

PAYABLE

2552185.

5

401794.2

3 614795.9 691296.7 844298.4

Interpretation: By considering the above listed table it can be said that the organisation

has paid taxes over the various items as well as the income tax payable by them. Hence, the

luxury car was being taxed in 2011/12 as 20920 for the first quarter it is 5230 which are same in

each year. The corporate tax can e charge 30% over the income gain by Houzit Ltd. Hence, in

the year 2011-12 the income tax was payable by company at 839585.5 which are different in

each quarter such as in Q1 it is 83419.13, Q2 it is 202600.9, Q3 it is 239691.8 and in Q4 it is

313873.6 at the rate of 30% of corporate tax. Fringe Benefit tax of the business for the year

2011-12 is was 28000 and for each quarter it was charged at equal amount such as 7000 in each

quarter. GST was measured over the all purchase f products by the organisation which is the total

payment for the period 2011-12 was 1663680. Hence, GST was measured for all the quarters in

the year such as Q1 it is 306145.1, Q2 it is 399965, Q 3 it is 439374.9 as well as for Q4 it is

518194.8 respectively.

2.

In accordance with considering the Houzit Pty Ltd there has been various standards

which are used for Compliances of the liabilities of the organisation. Hence, there are some

leverages facilitated to the small scale entities as well as in some special cases to not to make the

such reporting in these techniques or accounting standards (Cömert and et.al., 2016).

Hence, by considering the corporate act, 2001 the disclosure reports are must be prepared

by considering the shareholder's requirements such as turnover gain by the organisation,

profitability as well as debt equity of the firm as mentioned in section 293. Thus, such

information helps them in analysing the actual financial position of business in corporate

environment. However, in accordance with section 294A it says that, the reports are being

6

prepared with the proper specification as well as there must be use of authenticate sources of

information which must have the transaction details then such informations will be acceptable

(Tax and Corporate Australia, 2017).

3.

In accordance with Australian legislation there has been use of various kinds of software

which will help Houzit Pty Ltd in preparing financial accounts in an adequate manner. Hence,

there will be implementation of the various rules and regulation which are facilitated as to make

the authenticated reporting of all the accounts of firm (Banerjee, 2017). For instance, if Houzit

made any business transaction with Europe or any other country than such laws and regulations

will help them in preparing the livestock of main exports that transit between Australia and

Europe.

4.

a. Matching principle:

In accordance with these techniques the professionals must measure the current

performance of the firm with the revenant previous operations (Shank and Vianna, 2016). Hence,

it can be said that, such techniques will help them in analysing the loopholes as well as

drawbacks of the firm.

b. Time periods:

There must be regular inspection of the financial accounts of Houzit by the accounting

professionals as well the budgets must be based on the time basis. Hence, it can be said that the

firm is need prepare and execute the budgets on required time period (Mullins and Schoar,

2016).

c. Account groups

There is need to prepare a team of the accounting group which will help the professionals

in making the better execution or audits of the accounts. Hence, they will be able to suggest the

required changes to be made in the operational activities of the firm.

5.

There is need to implement the various principle concepts and models which will help the

firm in enhancing better disclosure techniques. On the other side where compliance is not

7

information which must have the transaction details then such informations will be acceptable

(Tax and Corporate Australia, 2017).

3.

In accordance with Australian legislation there has been use of various kinds of software

which will help Houzit Pty Ltd in preparing financial accounts in an adequate manner. Hence,

there will be implementation of the various rules and regulation which are facilitated as to make

the authenticated reporting of all the accounts of firm (Banerjee, 2017). For instance, if Houzit

made any business transaction with Europe or any other country than such laws and regulations

will help them in preparing the livestock of main exports that transit between Australia and

Europe.

4.

a. Matching principle:

In accordance with these techniques the professionals must measure the current

performance of the firm with the revenant previous operations (Shank and Vianna, 2016). Hence,

it can be said that, such techniques will help them in analysing the loopholes as well as

drawbacks of the firm.

b. Time periods:

There must be regular inspection of the financial accounts of Houzit by the accounting

professionals as well the budgets must be based on the time basis. Hence, it can be said that the

firm is need prepare and execute the budgets on required time period (Mullins and Schoar,

2016).

c. Account groups

There is need to prepare a team of the accounting group which will help the professionals

in making the better execution or audits of the accounts. Hence, they will be able to suggest the

required changes to be made in the operational activities of the firm.

5.

There is need to implement the various principle concepts and models which will help the

firm in enhancing better disclosure techniques. On the other side where compliance is not

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

necessary to be mentioned than it is previous accepted by the users that the reports of

organisation are nit prepared in consideration of such accounting standards (Chintrakarn,

Jiraporn and Kim, 2017).

6.

In accordance with the analysis of such financial data set which brings the ability of the

firm in not an adequate manner (Mullins and Schoar, 2016). Hence, there has been requirement

of various kinds of techniques which will help them in evaluate the efficiency of the

organisation.

7.

There must be increase in sales as well as organisation need to launch innovative

products as well as make scheme in attracting the large numbers of shareholders (Shank and

Vianna, 2016).

8.

It is important that there must be implementation all the norms and accounting standards

which helps in making the reports in the universally accepted format as well as which are easily

understood by all the persons (Banerjee, 2017).

CONCLUSION

On the basis of the report it can be said that, Hozit Pty Ltd need to adopt various changes

in the operational functioning of the business as well as generate ideas to make grasp the

preference or requirements of the employees. Further, while considering the budgets of the

organisation there is need to make reduction in the expenses of the activities that will help them

in gathering the adequate amount of funds.

8

organisation are nit prepared in consideration of such accounting standards (Chintrakarn,

Jiraporn and Kim, 2017).

6.

In accordance with the analysis of such financial data set which brings the ability of the

firm in not an adequate manner (Mullins and Schoar, 2016). Hence, there has been requirement

of various kinds of techniques which will help them in evaluate the efficiency of the

organisation.

7.

There must be increase in sales as well as organisation need to launch innovative

products as well as make scheme in attracting the large numbers of shareholders (Shank and

Vianna, 2016).

8.

It is important that there must be implementation all the norms and accounting standards

which helps in making the reports in the universally accepted format as well as which are easily

understood by all the persons (Banerjee, 2017).

CONCLUSION

On the basis of the report it can be said that, Hozit Pty Ltd need to adopt various changes

in the operational functioning of the business as well as generate ideas to make grasp the

preference or requirements of the employees. Further, while considering the budgets of the

organisation there is need to make reduction in the expenses of the activities that will help them

in gathering the adequate amount of funds.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Cömert, H. and et.al., 2016. Too big to manage: Innovation and instability from regulated

finance to the megabanking era.

Chintrakarn, P., Jiraporn, P. and Kim, Y. S., 2017. Did Firms Manage Earnings more

Aggressively during the Financial Crisis?. International Review of Finance.

John, S., 2017. Administration of the Public Finance Management Act 1999 in the North West

Provincial Administration in South Africa (Doctoral dissertation, University of Pretoria).

Shank, C. A. and Vianna, A. C., 2016. Are US-Dollar-Hedged-ETF investors aggressive on

exchange rates? A panel VAR approach. Research in International Business and Finance,

38, pp.430-438.

Mullins, W. and Schoar, A., 2016. How do CEOs see their roles? Management philosophies and

styles in family and non-family firms. Journal of Financial Economics. 119(1). pp.24-43.

Banerjee, R., 2017. Financial Analysis of an Urban Local Body in India Chosen under Smart

City Project: A Case Study of Kochi Municipal Corporation. Asian Journal of Research in

Business Economics and Management. 7(6). pp.237-250.

Online

Tax and Corporate Australia. 2017. [Online]. [Available through]

:<https://www.ato.gov.au/general/tax-and-corporate-australia/>. [Accessed on 27th October.

2017].

9

Books and Journals

Cömert, H. and et.al., 2016. Too big to manage: Innovation and instability from regulated

finance to the megabanking era.

Chintrakarn, P., Jiraporn, P. and Kim, Y. S., 2017. Did Firms Manage Earnings more

Aggressively during the Financial Crisis?. International Review of Finance.

John, S., 2017. Administration of the Public Finance Management Act 1999 in the North West

Provincial Administration in South Africa (Doctoral dissertation, University of Pretoria).

Shank, C. A. and Vianna, A. C., 2016. Are US-Dollar-Hedged-ETF investors aggressive on

exchange rates? A panel VAR approach. Research in International Business and Finance,

38, pp.430-438.

Mullins, W. and Schoar, A., 2016. How do CEOs see their roles? Management philosophies and

styles in family and non-family firms. Journal of Financial Economics. 119(1). pp.24-43.

Banerjee, R., 2017. Financial Analysis of an Urban Local Body in India Chosen under Smart

City Project: A Case Study of Kochi Municipal Corporation. Asian Journal of Research in

Business Economics and Management. 7(6). pp.237-250.

Online

Tax and Corporate Australia. 2017. [Online]. [Available through]

:<https://www.ato.gov.au/general/tax-and-corporate-australia/>. [Accessed on 27th October.

2017].

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.