Management Accounting Report: Financial Analysis for Imda Ltd

VerifiedAdded on 2020/02/03

|16

|3776

|280

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within Imda Ltd. It begins by defining management accounting, differentiating it from financial accounting, and highlighting its importance in decision-making. The report explores various types of management accounting, including cost accounting, inventory management, job costing, and price optimization systems. It details the benefits of a management accounting system, such as improved business decisions, cost reduction, increased financial returns, and effective planning and performance evaluation. The report also examines the integration of management accounting and management reporting systems within an organizational context. Furthermore, the report includes an income statement prepared using both absorption and marginal costing methods. It discusses the techniques of management accounting, such as financial planning, decision-making accounting, performance management, planning, budgeting, and ratio analysis. The report also analyzes different types of budgets, their advantages, and disadvantages, along with the process of preparing a budget and pricing strategies. Finally, it covers the balance scorecard and its implementation as a planning tool, concluding with the role of planning tools in solving financial problems.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

(a)Management accounting.........................................................................................................4

(b)Different types of management accounting............................................................................5

M1 Benefits of management accounting system.........................................................................5

D1 Integration of management accounting system and management reporting system in

organizational process.................................................................................................................6

TASK 2............................................................................................................................................6

Income statement of Imda tech....................................................................................................6

M2 Techniques of management accounting................................................................................2

D2 Interpret the data for the business activities...........................................................................2

TASK 3............................................................................................................................................3

(a)Types of budgets their advantages and disadvantages............................................................3

(b) Process of preparing the budget.............................................................................................4

(c)Pricing Strategies.....................................................................................................................4

M3 Use of different planning tools..............................................................................................4

D3 Role of planning tools in solving financial problems............................................................4

TASK 4............................................................................................................................................5

Balance scorecard and its implementation..................................................................................5

M4&D3 Planning tools................................................................................................................5

Conclusion.......................................................................................................................................5

References........................................................................................................................................6

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

(a)Management accounting.........................................................................................................4

(b)Different types of management accounting............................................................................5

M1 Benefits of management accounting system.........................................................................5

D1 Integration of management accounting system and management reporting system in

organizational process.................................................................................................................6

TASK 2............................................................................................................................................6

Income statement of Imda tech....................................................................................................6

M2 Techniques of management accounting................................................................................2

D2 Interpret the data for the business activities...........................................................................2

TASK 3............................................................................................................................................3

(a)Types of budgets their advantages and disadvantages............................................................3

(b) Process of preparing the budget.............................................................................................4

(c)Pricing Strategies.....................................................................................................................4

M3 Use of different planning tools..............................................................................................4

D3 Role of planning tools in solving financial problems............................................................4

TASK 4............................................................................................................................................5

Balance scorecard and its implementation..................................................................................5

M4&D3 Planning tools................................................................................................................5

Conclusion.......................................................................................................................................5

References........................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

This report contain all the relevant information relating to the management operations of

Imda ltd. Present report shows the relevant information like what is management accounting and

what is financial accounting and how management accounting provide relevant information to

the managers in taking important decision for the enterprise. What is cost accounting system,

inventory management system, job costing system and pricing optimizing system is detailed

under this report. How many types of budgets are there and how the enterprise can be benefited

by making the budgets. How these budgets can help the Imda ltd in achieving its objectives. This

report tells how Imda ltd can use the concept of balance scorecard and how this can help them in

achieving their operation efficiency. Absorption and marginal costing are described under this.

What pricing strategy should a firm use to fix the price of its products and services is described

under this.

TASK 1

(a)Management accounting

Management accounting is a technique of using all the relevant information collected

with the help of accounts department of the enterprise in order to achieve the efficiency in the

business operations. The concept of management accounting is based on the information of

financial and non financial data of the enterprise.

Difference between Management accounting and financial accounting

Management accounting is a technique to provide that information to the managers which

will help them in taking useful decisions for the enterprise. By using or apply this managers can

better take the decision in maximizing the profits of the business.

Financial accounting is a process dealing with the monetary terms it mainly deals with

the financial statements of the enterprise and evaluate them in order to improve the performance

of the financial system of the enterprise.

Importance of management accounting system as a decision making tool

Every business enterprise has to take lot of important decisions and management

accounting helps them in taking appropriate and more effective decision by provide them useful

information(Kaplan and Atkinson, 2015). The importance of management accounting can be

understood by the following points:

Relevant cost analysis: Management accounting system helps the mangers in taking

relevant cost decisions. Management accounting helps the enterprise in deciding what

method should be adopted by them in achieving the objectives with minimum cost.

This report contain all the relevant information relating to the management operations of

Imda ltd. Present report shows the relevant information like what is management accounting and

what is financial accounting and how management accounting provide relevant information to

the managers in taking important decision for the enterprise. What is cost accounting system,

inventory management system, job costing system and pricing optimizing system is detailed

under this report. How many types of budgets are there and how the enterprise can be benefited

by making the budgets. How these budgets can help the Imda ltd in achieving its objectives. This

report tells how Imda ltd can use the concept of balance scorecard and how this can help them in

achieving their operation efficiency. Absorption and marginal costing are described under this.

What pricing strategy should a firm use to fix the price of its products and services is described

under this.

TASK 1

(a)Management accounting

Management accounting is a technique of using all the relevant information collected

with the help of accounts department of the enterprise in order to achieve the efficiency in the

business operations. The concept of management accounting is based on the information of

financial and non financial data of the enterprise.

Difference between Management accounting and financial accounting

Management accounting is a technique to provide that information to the managers which

will help them in taking useful decisions for the enterprise. By using or apply this managers can

better take the decision in maximizing the profits of the business.

Financial accounting is a process dealing with the monetary terms it mainly deals with

the financial statements of the enterprise and evaluate them in order to improve the performance

of the financial system of the enterprise.

Importance of management accounting system as a decision making tool

Every business enterprise has to take lot of important decisions and management

accounting helps them in taking appropriate and more effective decision by provide them useful

information(Kaplan and Atkinson, 2015). The importance of management accounting can be

understood by the following points:

Relevant cost analysis: Management accounting system helps the mangers in taking

relevant cost decisions. Management accounting helps the enterprise in deciding what

method should be adopted by them in achieving the objectives with minimum cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Make or buy decisions: Management accounting system helps the enterprise in taking the

decision relating to whether make or buy the equipments or product.

(b)Different types of management accounting

Cost accounting system: Cost accounting system is a system or framework used by the enterprise

to estimate the cost of their products(Macintosh and Quattrone, 2010)

It helps the enterprise in knowing which products are more profitable and which are less

profitable.

Inventory management system: It helps the enterprise in maintaining a optimum level of

inventory which will help the enterprise in achieving the objectives and demands of the

customers. Lack of inventory does not make the enterprise able to meet the specific

demands of the customers on the other hand over level of inventory will, give the rise to

storage cost.

Job costing system: This system helps the enterprise in knowing the cost relating to the

each job and helps in evaluating the profitability related with each job. This is a useful

technique because this helps the managers in focusing on the more profitable jobs of the

enterprise.

Price optimizing system: It is a technique helps the enterprise in deciding a price by

which the company can best achieve the objective of maximum profit and at the same

time the price satisfy the needs of the customers.

M1 Benefits of management accounting system

By applying or using the concept of management accounting system an enterprise can be

benefited by the following benefits:

Business decision: The most useful benefit of management accounting to the enterprise is that it

helps the enterprise in taking better decisions(Ward, 2012)

Management accounting evaluate all the activities of the business and provide useful information

to the managers and managers can better utilize the information in taking decisions.

Reduce expenses: Business enterprises use the management accounting system in

reducing the cost of the operations. Firms use the management accounting in analyzing

how the quality can be increased and how the cost can be reduced of the business

operations.

Increase financial returns: Managers apply the concept of management accounting in increase the

financial returns and to enhance the profitability of the business(Baldvinsdottir, Mitchell and

Nørreklit, 2010)

By collecting all the relevant information the managers can better take the decisions like

what to produce in better achieving or satisfying the customers demand and to achieve

the profitability.

decision relating to whether make or buy the equipments or product.

(b)Different types of management accounting

Cost accounting system: Cost accounting system is a system or framework used by the enterprise

to estimate the cost of their products(Macintosh and Quattrone, 2010)

It helps the enterprise in knowing which products are more profitable and which are less

profitable.

Inventory management system: It helps the enterprise in maintaining a optimum level of

inventory which will help the enterprise in achieving the objectives and demands of the

customers. Lack of inventory does not make the enterprise able to meet the specific

demands of the customers on the other hand over level of inventory will, give the rise to

storage cost.

Job costing system: This system helps the enterprise in knowing the cost relating to the

each job and helps in evaluating the profitability related with each job. This is a useful

technique because this helps the managers in focusing on the more profitable jobs of the

enterprise.

Price optimizing system: It is a technique helps the enterprise in deciding a price by

which the company can best achieve the objective of maximum profit and at the same

time the price satisfy the needs of the customers.

M1 Benefits of management accounting system

By applying or using the concept of management accounting system an enterprise can be

benefited by the following benefits:

Business decision: The most useful benefit of management accounting to the enterprise is that it

helps the enterprise in taking better decisions(Ward, 2012)

Management accounting evaluate all the activities of the business and provide useful information

to the managers and managers can better utilize the information in taking decisions.

Reduce expenses: Business enterprises use the management accounting system in

reducing the cost of the operations. Firms use the management accounting in analyzing

how the quality can be increased and how the cost can be reduced of the business

operations.

Increase financial returns: Managers apply the concept of management accounting in increase the

financial returns and to enhance the profitability of the business(Baldvinsdottir, Mitchell and

Nørreklit, 2010)

By collecting all the relevant information the managers can better take the decisions like

what to produce in better achieving or satisfying the customers demand and to achieve

the profitability.

Planning: Management accounting system helps the manager in plan all the activities of

the enterprise by providing all the relevant information related to the all business

operations.

Performance evaluation: Management accounting does not only evaluate the other

activities of the enterprise but also helps in evaluating the performance of the employees.

D1 Integration of management accounting system and management reporting

system in organizational process.

Management accounting system helps the managers in taking various important decisions

related to the business activities. Management accounting evaluates all the activities of the

business and shows that if any corrective action is needed in the enterprise to increase the output.

Imda ltd can use these two techniques to increase the efficiency in their business operations.

Management reporting system is a technique which record daily activities of the business and

tells the manager about the true picture of the business. On the basis of that a manger can take

better decisions and can increase the efficiency of the business operations. Management

reporting tells any corrective action needed in the business activities and improve the activities of

the business. This also evaluates the performance of the employees of the enterprise and helps

the managers in planning the development and training programme for the employees. Both

management accounting and reporting system helps the enterprise in working efficiently and

achieve its goals effectively(Lukka and Modell, 2010). Imda ltd can use both the techniques to

improve the efficiency in their activities.

TASK 2

Income statement of Imda tech

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

the enterprise by providing all the relevant information related to the all business

operations.

Performance evaluation: Management accounting does not only evaluate the other

activities of the enterprise but also helps in evaluating the performance of the employees.

D1 Integration of management accounting system and management reporting

system in organizational process.

Management accounting system helps the managers in taking various important decisions

related to the business activities. Management accounting evaluates all the activities of the

business and shows that if any corrective action is needed in the enterprise to increase the output.

Imda ltd can use these two techniques to increase the efficiency in their business operations.

Management reporting system is a technique which record daily activities of the business and

tells the manager about the true picture of the business. On the basis of that a manger can take

better decisions and can increase the efficiency of the business operations. Management

reporting tells any corrective action needed in the business activities and improve the activities of

the business. This also evaluates the performance of the employees of the enterprise and helps

the managers in planning the development and training programme for the employees. Both

management accounting and reporting system helps the enterprise in working efficiently and

achieve its goals effectively(Lukka and Modell, 2010). Imda ltd can use both the techniques to

improve the efficiency in their activities.

TASK 2

Income statement of Imda tech

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

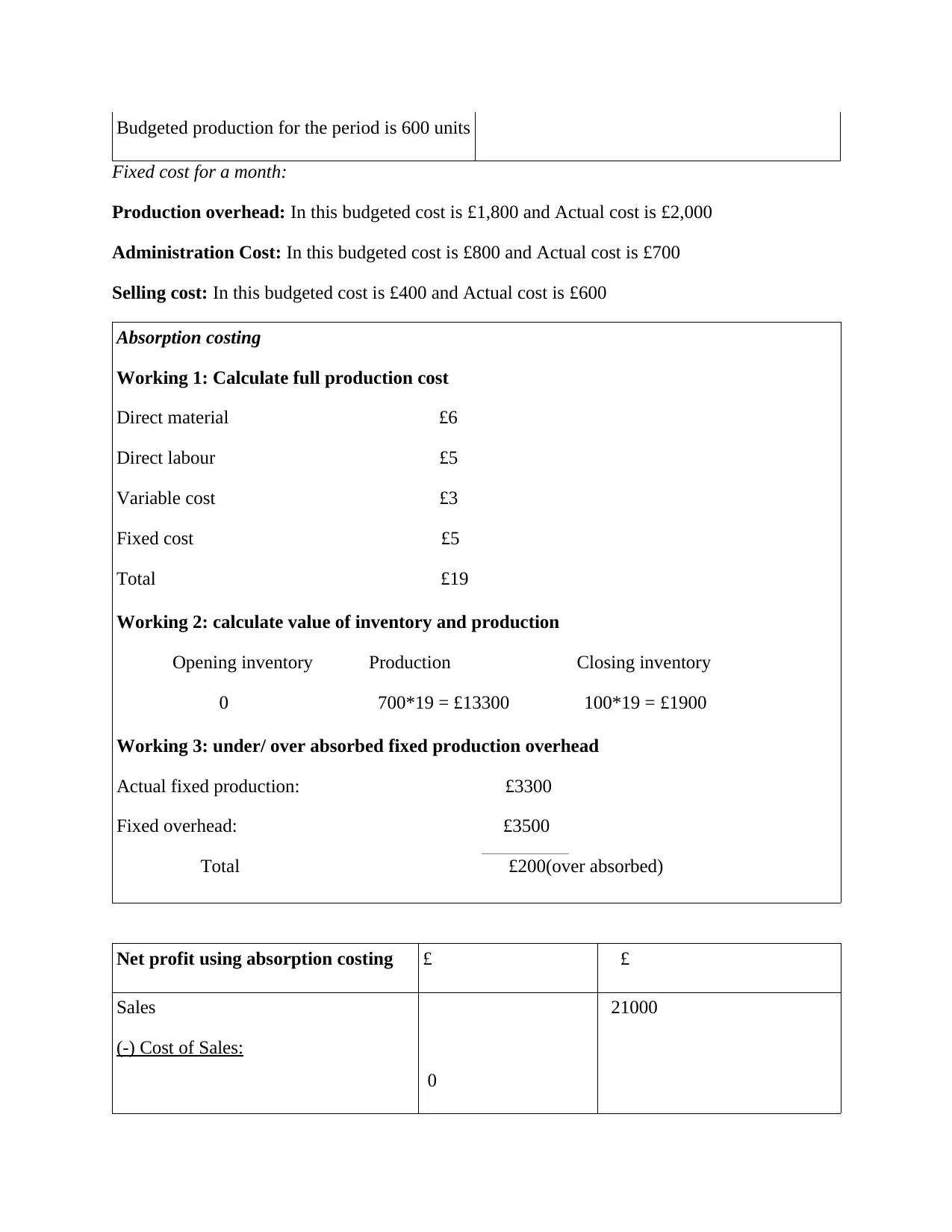

Budgeted production for the period is 600 units

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

0

21000

Fixed cost for a month:

Production overhead: In this budgeted cost is £1,800 and Actual cost is £2,000

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

0

21000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

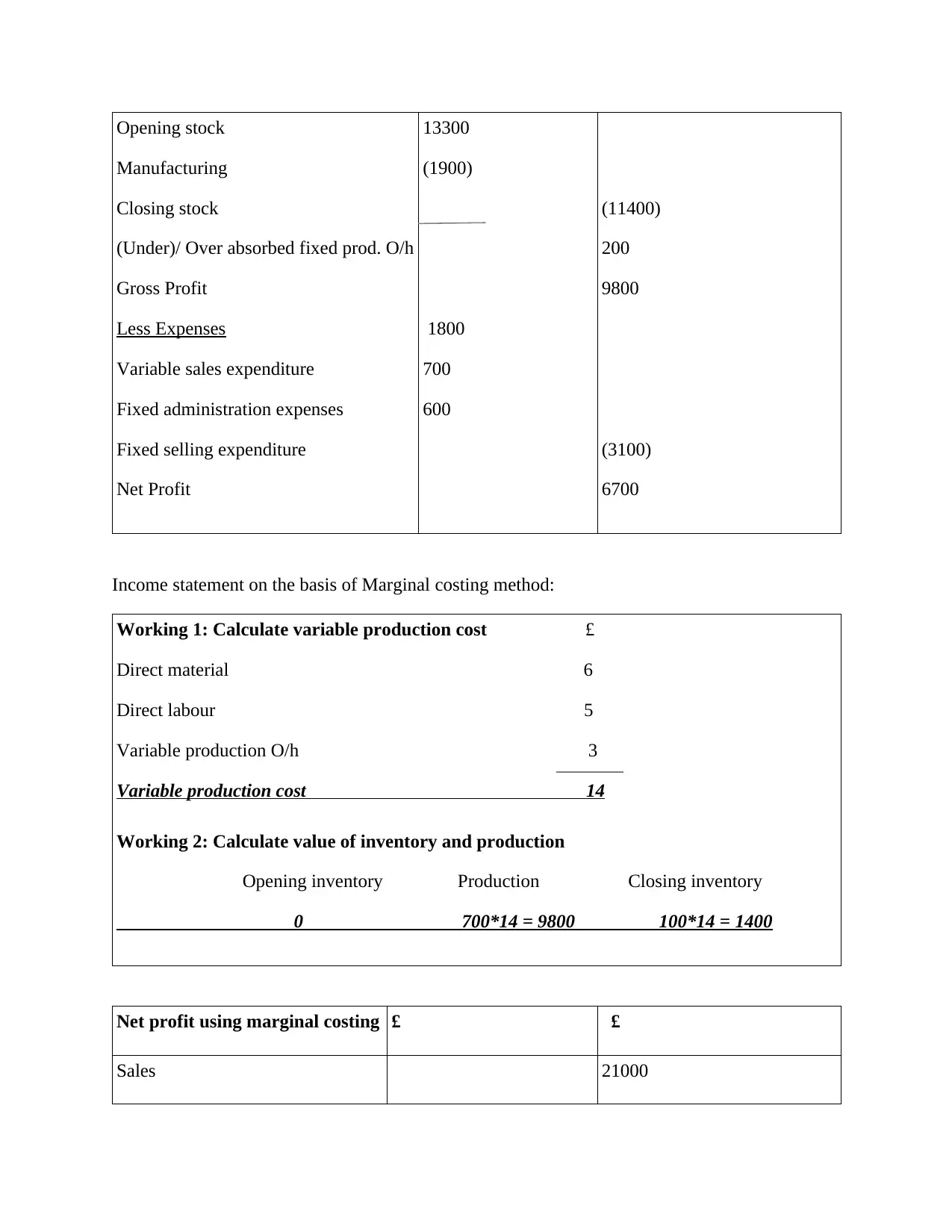

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Net Profit

13300

(1900)

1800

700

600

(11400)

200

9800

(3100)

6700

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Net Profit

13300

(1900)

1800

700

600

(11400)

200

9800

(3100)

6700

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales 21000

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9800

(1400)

2000

700

600

(8400)

(1800)

10800

3300

7500

Absorption and marginal costing

Absorption costing means all the costing which occurs in making or manufacturing a

product. It calculates all the variable cost which occur in making the product it ignores the fixed

cost because fixed cost is that cost which will occur while there is no production at all. It a

process of calculating all the cost occurred while making a product whether it is direct or indirect

expense. Absorption costing adds direct materials, variable manufacturing overhead and

manufacturing overhead in calculating the cost. Absorption costing is an important tool of

calculating the cost of a product includes direct and indirect cost.

Marginal costing is the opportunity cost which occurred while making an extra product. It is the

change in cost which happens when one product is produced by the enterprise. When an

enterprise make one product then it can rise two situations one is increasing in the total cost and

the other is decreasing in the total cost. By knowing this the managers of the enterprise can take

decision whether to make one more product or not(Renz, 2016.). If making one new product

increases the total cost of production than the enterprise should go for making the one more

product and if the production cost rises than the enterprise should continue with the old process

of making the product and should not add the one more product to the production process.

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9800

(1400)

2000

700

600

(8400)

(1800)

10800

3300

7500

Absorption and marginal costing

Absorption costing means all the costing which occurs in making or manufacturing a

product. It calculates all the variable cost which occur in making the product it ignores the fixed

cost because fixed cost is that cost which will occur while there is no production at all. It a

process of calculating all the cost occurred while making a product whether it is direct or indirect

expense. Absorption costing adds direct materials, variable manufacturing overhead and

manufacturing overhead in calculating the cost. Absorption costing is an important tool of

calculating the cost of a product includes direct and indirect cost.

Marginal costing is the opportunity cost which occurred while making an extra product. It is the

change in cost which happens when one product is produced by the enterprise. When an

enterprise make one product then it can rise two situations one is increasing in the total cost and

the other is decreasing in the total cost. By knowing this the managers of the enterprise can take

decision whether to make one more product or not(Renz, 2016.). If making one new product

increases the total cost of production than the enterprise should go for making the one more

product and if the production cost rises than the enterprise should continue with the old process

of making the product and should not add the one more product to the production process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Techniques of management accounting

Financial planning: The most important objective of every enterprise is to maximize the

profits with minimum cost and also achieving the customer satisfaction. This objective

can be achieved by the enterprise by doing financial planning

Decision making accounting: Every manager wants to take an decision which can give

fruitful results to the enterprise and management accounting helps the manager in

providing useful information which helps the manager in taking or making an appropriate

decision for the enterprise.

Performance management: Performance management tool is used to compare the

performance of the employees with their standard performance to take appropriate

decision.

Planning and budgeting: Records of sales is continue checked by the management to do

the further planning like how to increase the sales.

Ratio analysis: It is used by the management to do the followings functions like planning,

coordination and control. It is a method of effectively controlling all the business

activities.

D2 Interpret the data for the business activities

To run the all the business activity successful the manager of every enterprise has to

predict some data to make the future decisions(Otley and Emmanuel, 2013). A manager can

predict the data by the following information available through:

Past data: Past budgets help the manager in taking future decisions the mistakes which

occurred in the past can be removed in the present budget.

Sales records : Sales record used by the manager to forecast the sales of current year and

managers take the decisions or make policies to increase the sales of the enterprise.

Other than this the manager of the enterprise can predict the data for taking various important

decisions for the business.

TASK 3

(a)Types of budgets their advantages and disadvantages

Sales budget: Sales is the forecasting of total sales revenue generated by the firm by

selling the products and services to the target customers. It is one of the most important

Financial planning: The most important objective of every enterprise is to maximize the

profits with minimum cost and also achieving the customer satisfaction. This objective

can be achieved by the enterprise by doing financial planning

Decision making accounting: Every manager wants to take an decision which can give

fruitful results to the enterprise and management accounting helps the manager in

providing useful information which helps the manager in taking or making an appropriate

decision for the enterprise.

Performance management: Performance management tool is used to compare the

performance of the employees with their standard performance to take appropriate

decision.

Planning and budgeting: Records of sales is continue checked by the management to do

the further planning like how to increase the sales.

Ratio analysis: It is used by the management to do the followings functions like planning,

coordination and control. It is a method of effectively controlling all the business

activities.

D2 Interpret the data for the business activities

To run the all the business activity successful the manager of every enterprise has to

predict some data to make the future decisions(Otley and Emmanuel, 2013). A manager can

predict the data by the following information available through:

Past data: Past budgets help the manager in taking future decisions the mistakes which

occurred in the past can be removed in the present budget.

Sales records : Sales record used by the manager to forecast the sales of current year and

managers take the decisions or make policies to increase the sales of the enterprise.

Other than this the manager of the enterprise can predict the data for taking various important

decisions for the business.

TASK 3

(a)Types of budgets their advantages and disadvantages

Sales budget: Sales is the forecasting of total sales revenue generated by the firm by

selling the products and services to the target customers. It is one of the most important

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.