Detailed Management Accounting Report for Imda Tech (UK) Limited

VerifiedAdded on 2019/12/18

|16

|5379

|386

Report

AI Summary

This report provides a detailed analysis of the management accounting practices of Imda Tech (UK) Limited, focusing on the need for improved financial information for decision-making. It covers key functions of management accounting, differentiating it from financial accounting, and explores various management accounting systems like cost accounting and inventory management. The report includes calculations of product costs using both marginal and absorption costing methods, along with income statements prepared under each method. It highlights the importance of integrating management accounting systems with reporting for effective decision-making and emphasizes the role of budgeting and the balance scorecard. The report aims to help Imda Tech improve its financial returns, reduce expenses, and enhance its overall business decisions.

1

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 INTRODUCTION

Management accounting is used to inspect, record and report any financial information

for decision making. They do not follow any accounting standards of any country as they

themselves design management accounting according to the company and its operations or

management. We could say that management accounting is the process of investigation,

explanation and presentation of accounting information gathered with the help of financial

accounting and cost accounting. The information which is gathered is used for making

organisational decisions. All the report will be dealing with the management accounting of Imda

Tech (UK) limited who is producing special charger for mobile telephone and other carry

gadgets for a retail outlet in the UK (Asosheh, Nalchigar and Jamporazmey, 2010). The

department managers of the company in the last senior management meeting complained about

the lack of financial information to improve decision making. So as per the instructions of line

manager a report has been produced as a part learning which will include functions and

importance of management accounting, different types of management accounting system, cost

of the charges for mobile telephone, income statements, budgeting and its aspects,

implementation of balance score card and etc. This report will contain all the information related

to management accounting of the Imda Tech Limited which will help them in making proper and

effective decisions.

3 TASK 1

1 (a) Functions of Management Accounting.

Management accounting is related to the information that is needed by the management

of the company so we can say that it is technique or process which aims at providing managers

the information related to the accounting (Tseng, 2010). We know that in today's world the duty

of management accounting is not only restricted to report the score of the company but to use the

score or numbers in influencing the decisions of the company. These can be used to extracted

any new strategy or plan related to the management of the organisation. People who are assigned

with the task of preparation of information related to accounting should posses knowledge and

certain skills because through their report all the decisions, policies and plans will be made. A

manager takes decision on the basis of the accounting information which is provided to him, it is

basically the background of the company which defines what where the company stands or what

Management accounting is used to inspect, record and report any financial information

for decision making. They do not follow any accounting standards of any country as they

themselves design management accounting according to the company and its operations or

management. We could say that management accounting is the process of investigation,

explanation and presentation of accounting information gathered with the help of financial

accounting and cost accounting. The information which is gathered is used for making

organisational decisions. All the report will be dealing with the management accounting of Imda

Tech (UK) limited who is producing special charger for mobile telephone and other carry

gadgets for a retail outlet in the UK (Asosheh, Nalchigar and Jamporazmey, 2010). The

department managers of the company in the last senior management meeting complained about

the lack of financial information to improve decision making. So as per the instructions of line

manager a report has been produced as a part learning which will include functions and

importance of management accounting, different types of management accounting system, cost

of the charges for mobile telephone, income statements, budgeting and its aspects,

implementation of balance score card and etc. This report will contain all the information related

to management accounting of the Imda Tech Limited which will help them in making proper and

effective decisions.

3 TASK 1

1 (a) Functions of Management Accounting.

Management accounting is related to the information that is needed by the management

of the company so we can say that it is technique or process which aims at providing managers

the information related to the accounting (Tseng, 2010). We know that in today's world the duty

of management accounting is not only restricted to report the score of the company but to use the

score or numbers in influencing the decisions of the company. These can be used to extracted

any new strategy or plan related to the management of the organisation. People who are assigned

with the task of preparation of information related to accounting should posses knowledge and

certain skills because through their report all the decisions, policies and plans will be made. A

manager takes decision on the basis of the accounting information which is provided to him, it is

basically the background of the company which defines what where the company stands or what

is the performance of the firm in past financial years (Chen, Hsu, and Tzeng, 2011). Accounting

information will assist Imda Tech (UK) limited to control the working and take significant

decisions which would benefit company for a long run. It is seen that people take management

accounting same as the the financial accounting but they are different from each other. A table is

made below to differentiate between the financial accounting and management accounting.

Financial Accounting Management Accounting

Financial accounting is related to financial

information like balance sheet, income

statement, cash flow, income statement and

financial statements. These information is

provided outside the business to the financial

expert, shareholders and etc.

Management accounting deals with providing

information which is useful in maintaining the

efficiency of the management of the company.

We could say that in this the information is

provided to the internal body of the

organisation.

In this the information of all the company is

included or we could say that all the

departments of the company are analysed for

this report.

In this case only analyse or inspection of the

specific department or area is done, there may

be a particular product management accounting

is restricted by the company.

Time period is set for the financing accounting

report or a time period is considered for this.

For example, Imda Tech (UK) wants to prepare

its financial reports so they will take past

financial year and consider the growth and

development of the company (Giovannoni,

Maraghini, and Riccaboni, 2011).

Management accounting does not include or

specific any time period as they prepare reports

according to the demand and requirement of the

organisation.

It is a mandatory or compulsory for most of the

companies to extract or maintain financial

accounting.

It could be optional and but in modern era

companies also take note of it.

For the preparation of the financial accounting

information reports they accept general

accounting principles in the UK and other

policies.

Companies while making managing accounting

report develops and follows rules according top

the needs of the company (Macintosh and

Quattrone, 2010).

information will assist Imda Tech (UK) limited to control the working and take significant

decisions which would benefit company for a long run. It is seen that people take management

accounting same as the the financial accounting but they are different from each other. A table is

made below to differentiate between the financial accounting and management accounting.

Financial Accounting Management Accounting

Financial accounting is related to financial

information like balance sheet, income

statement, cash flow, income statement and

financial statements. These information is

provided outside the business to the financial

expert, shareholders and etc.

Management accounting deals with providing

information which is useful in maintaining the

efficiency of the management of the company.

We could say that in this the information is

provided to the internal body of the

organisation.

In this the information of all the company is

included or we could say that all the

departments of the company are analysed for

this report.

In this case only analyse or inspection of the

specific department or area is done, there may

be a particular product management accounting

is restricted by the company.

Time period is set for the financing accounting

report or a time period is considered for this.

For example, Imda Tech (UK) wants to prepare

its financial reports so they will take past

financial year and consider the growth and

development of the company (Giovannoni,

Maraghini, and Riccaboni, 2011).

Management accounting does not include or

specific any time period as they prepare reports

according to the demand and requirement of the

organisation.

It is a mandatory or compulsory for most of the

companies to extract or maintain financial

accounting.

It could be optional and but in modern era

companies also take note of it.

For the preparation of the financial accounting

information reports they accept general

accounting principles in the UK and other

policies.

Companies while making managing accounting

report develops and follows rules according top

the needs of the company (Macintosh and

Quattrone, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the high-level summary of the business of

the company.

It emphasis on the certain required details of

the organisation.

Whatever the information extracted from management accounting process plays a significant

role in the decision-making process of a company (Van der Stede, 2011). This will provide them

the information in relation to the performance of the Imda Tech (UK) Limited which would be a

great help for them in recognizing the performance of the specific departments. This information

can be evaluated and can be compared with the expected results. What all plans and strategies

has gone wrong which has resulted in downfall of the performance and by this the cost of the

product can be managed.

2 (b) Different types of management accounting systems.

There are different management accounting systems which can be used by the Imda Tech

(UK) limited to inspect or record information related to its products and service. Following are

some management according systems: -

Cost Accounting System: - Production related activities can be traced through use of

inventory perpetual system (Scapens and Bromwich, 2010). This is one of the important system

used by the organisations and five parts of the system which are an input measurement basis, an

inventory valuation method in which valuation of inventory is done, third includes accumulation

of all the cost methods, fourth one is assumption of cost flow, and in the last one capability at

certain levels of recording inventory cost flows.

Inventory Management System: - Through this numbers of the products which is to be

sold can be managed because it helps in controlling the storage, orders and what are their use in

production of the items. Any decision concerned with the quantity and storage can be taken

through inventory management system.

Job costing system: - This is a process of accumulating information related to the costs

attached with a product. The information which is extracted through this are required in order to

give cost information to a buyer or customer and this can be also a useful method for

determining the accuracy of the company's estimating system. Imda Tech limited can earn profits

by quoting the price of the charges they are producing. Job costing system gives information of

the cost related to material, labours and other.

the company.

It emphasis on the certain required details of

the organisation.

Whatever the information extracted from management accounting process plays a significant

role in the decision-making process of a company (Van der Stede, 2011). This will provide them

the information in relation to the performance of the Imda Tech (UK) Limited which would be a

great help for them in recognizing the performance of the specific departments. This information

can be evaluated and can be compared with the expected results. What all plans and strategies

has gone wrong which has resulted in downfall of the performance and by this the cost of the

product can be managed.

2 (b) Different types of management accounting systems.

There are different management accounting systems which can be used by the Imda Tech

(UK) limited to inspect or record information related to its products and service. Following are

some management according systems: -

Cost Accounting System: - Production related activities can be traced through use of

inventory perpetual system (Scapens and Bromwich, 2010). This is one of the important system

used by the organisations and five parts of the system which are an input measurement basis, an

inventory valuation method in which valuation of inventory is done, third includes accumulation

of all the cost methods, fourth one is assumption of cost flow, and in the last one capability at

certain levels of recording inventory cost flows.

Inventory Management System: - Through this numbers of the products which is to be

sold can be managed because it helps in controlling the storage, orders and what are their use in

production of the items. Any decision concerned with the quantity and storage can be taken

through inventory management system.

Job costing system: - This is a process of accumulating information related to the costs

attached with a product. The information which is extracted through this are required in order to

give cost information to a buyer or customer and this can be also a useful method for

determining the accuracy of the company's estimating system. Imda Tech limited can earn profits

by quoting the price of the charges they are producing. Job costing system gives information of

the cost related to material, labours and other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimising systems: - This system shows how the price affects the demands of any

product and then combining all the data with the inventory levels and costs to fix the appropriate

prices which will help company in improving their profit margins. This can be used in checking

the response of the customers when the price of any specific product is increased (Soin and

Collier, 2013).

3 M1

Through management accounting Imda Tech limited can get lots of advantage and can

earn more profits. Through this Imda can reduce its expenses and in this the owners of the

business gets an idea that what cost it takes to run a business. Other than this they can improve

their cash flows, improve business decisions and can increase their financial returns.

4 D1

Management accounting system and management accounting reporting can be integrate

by Imda Tech Limited because before taking any decision or managing the decisions a report

will be required which will contain relevant information and on basis of that a reporting will be

done and that information is extracted or obtained from management accounting system

(Fullerton, Kennedy and Widener, 2014).

4 TASK 2

1 Calculation of the Cost

Marginal cost can be defined as variable cost of manufacturing a product and it is

calculated by adding the direct material cost, direct labour cost, direct expenses and all the

variable production overheads. Marginal cost are charged on the basis of per unit and the total

fixed are deducted from the full contribution. Fixed cost will remain same and does not have any

effect on the level of production. On the other hand absorption costing is the process in which all

the costs which are attached to the product are collected and than they are divided on distributed

on per unit basis. For the creation of the inventory valuation absorption costing is required as per

the accounting standard. In this the product will absorb all the costs whether it may be variable

cost or the fixed costs (Luft, and Shields, 2010)

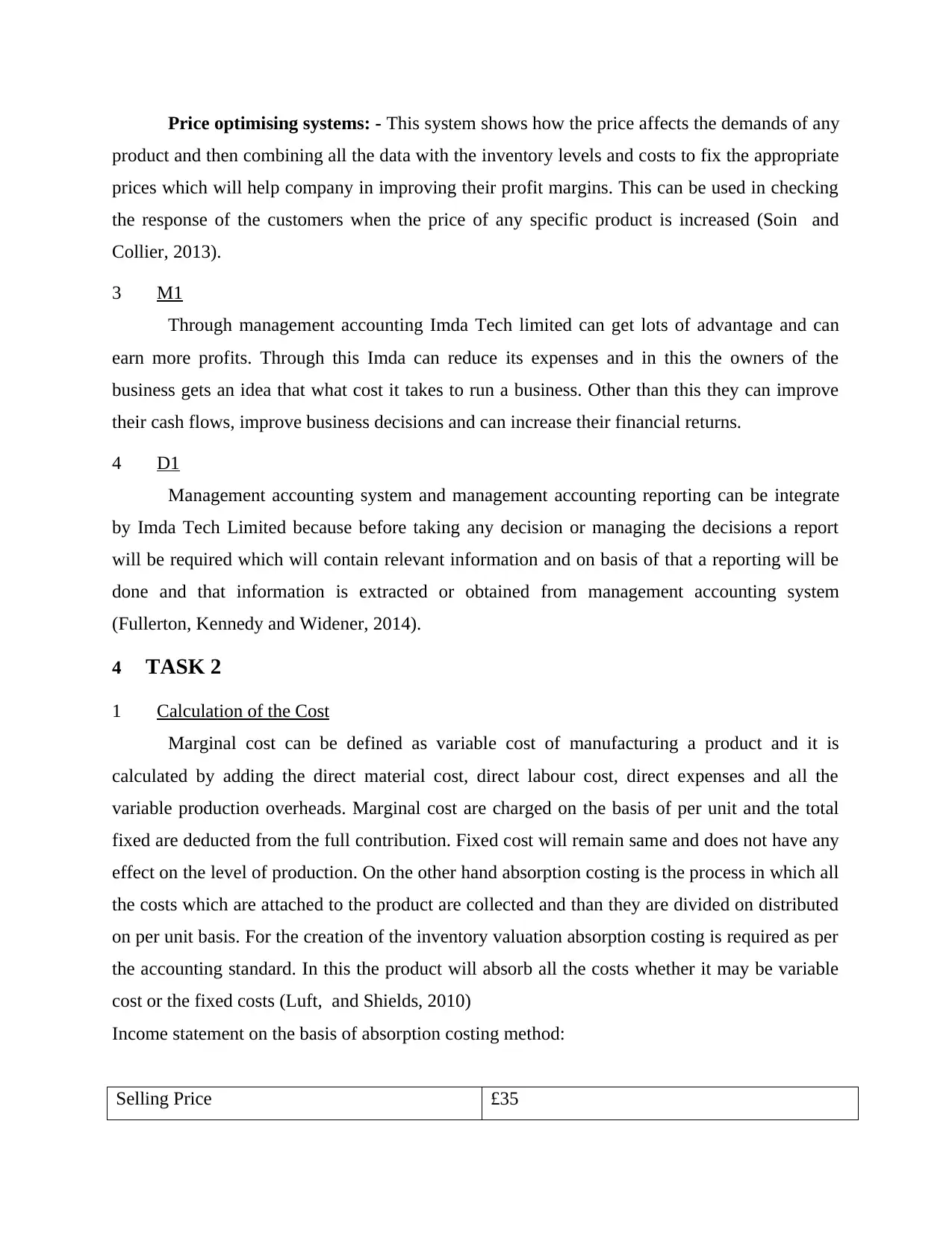

Income statement on the basis of absorption costing method:

Selling Price £35

product and then combining all the data with the inventory levels and costs to fix the appropriate

prices which will help company in improving their profit margins. This can be used in checking

the response of the customers when the price of any specific product is increased (Soin and

Collier, 2013).

3 M1

Through management accounting Imda Tech limited can get lots of advantage and can

earn more profits. Through this Imda can reduce its expenses and in this the owners of the

business gets an idea that what cost it takes to run a business. Other than this they can improve

their cash flows, improve business decisions and can increase their financial returns.

4 D1

Management accounting system and management accounting reporting can be integrate

by Imda Tech Limited because before taking any decision or managing the decisions a report

will be required which will contain relevant information and on basis of that a reporting will be

done and that information is extracted or obtained from management accounting system

(Fullerton, Kennedy and Widener, 2014).

4 TASK 2

1 Calculation of the Cost

Marginal cost can be defined as variable cost of manufacturing a product and it is

calculated by adding the direct material cost, direct labour cost, direct expenses and all the

variable production overheads. Marginal cost are charged on the basis of per unit and the total

fixed are deducted from the full contribution. Fixed cost will remain same and does not have any

effect on the level of production. On the other hand absorption costing is the process in which all

the costs which are attached to the product are collected and than they are divided on distributed

on per unit basis. For the creation of the inventory valuation absorption costing is required as per

the accounting standard. In this the product will absorb all the costs whether it may be variable

cost or the fixed costs (Luft, and Shields, 2010)

Income statement on the basis of absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

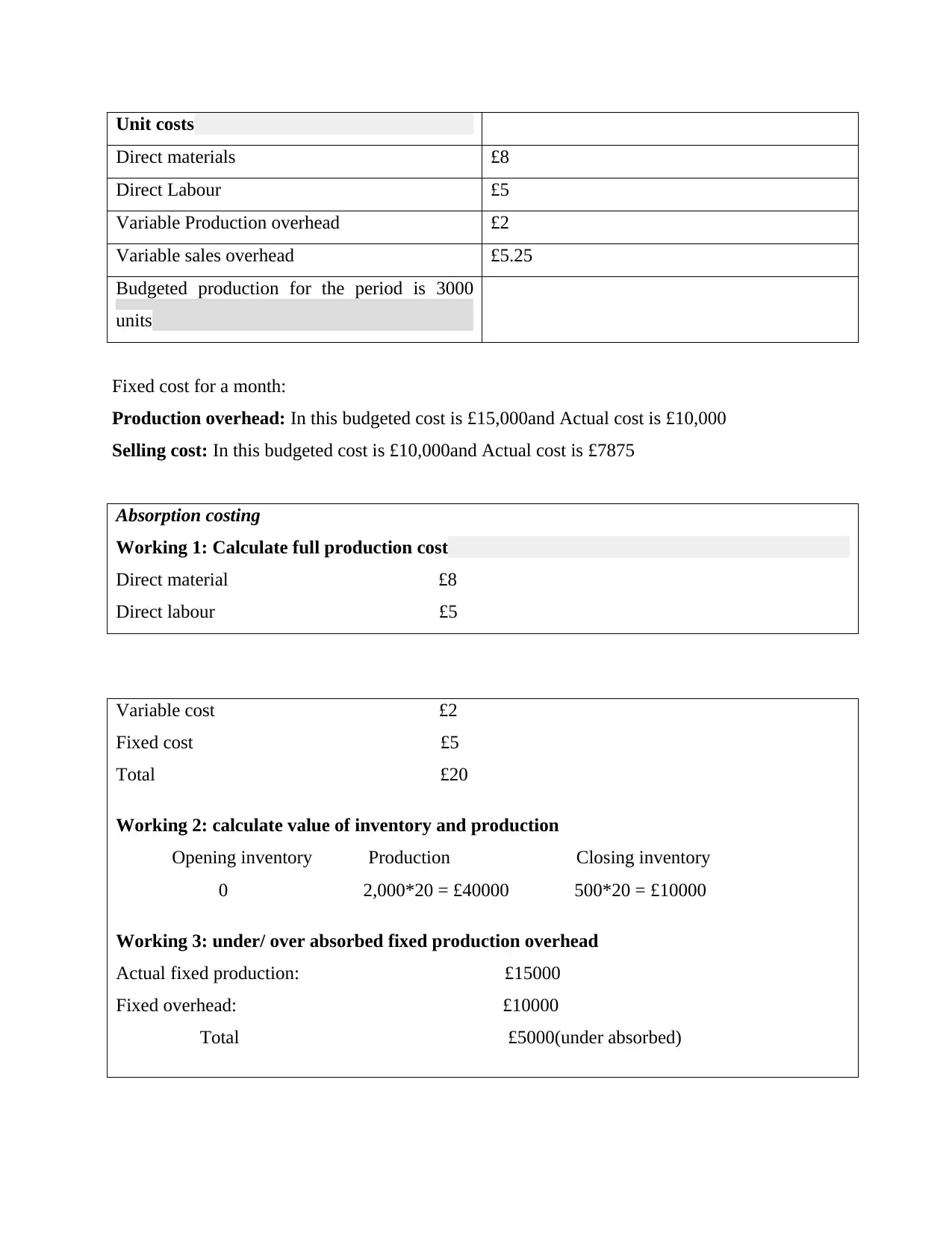

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

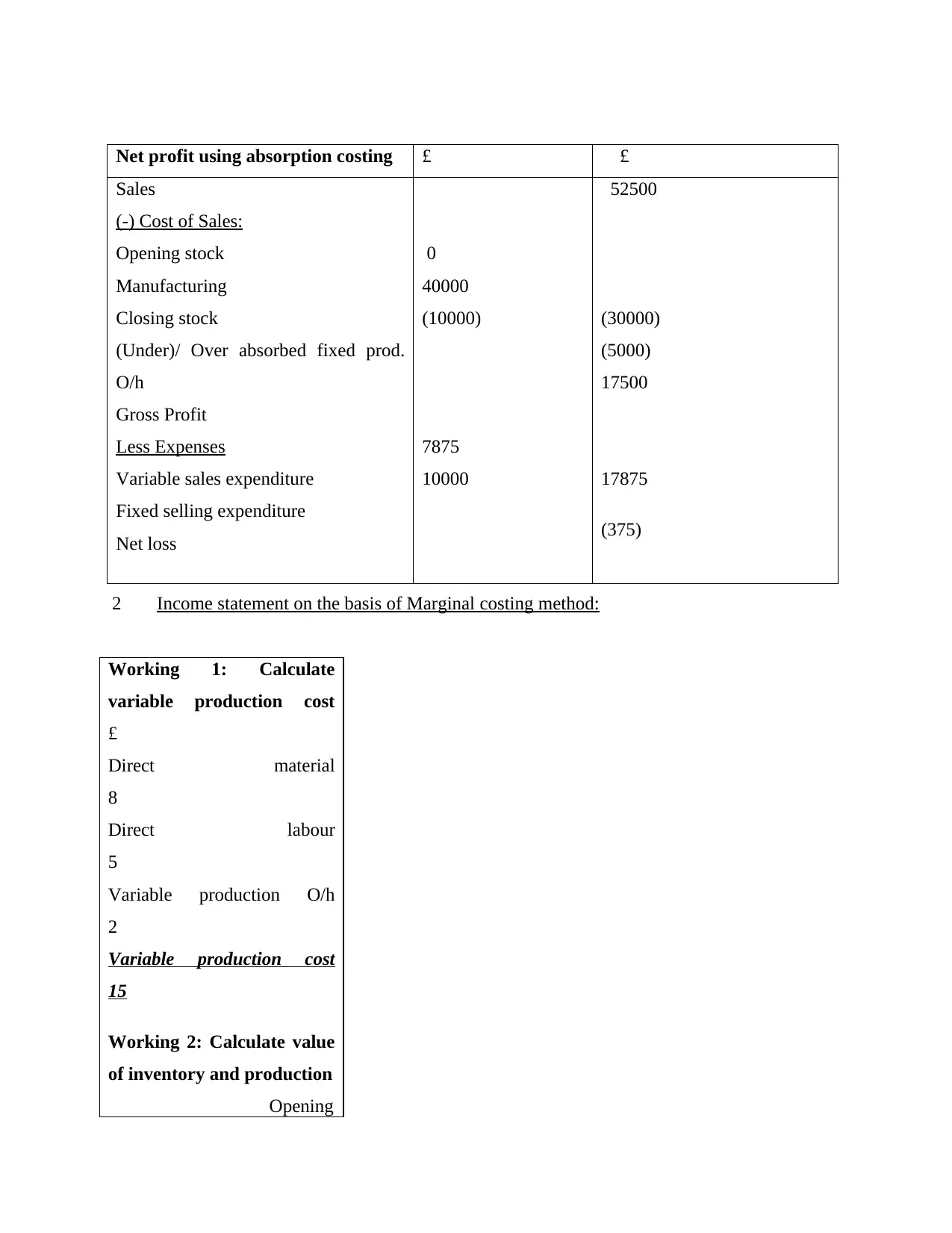

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

2 Income statement on the basis of Marginal costing method:

Working 1: Calculate

variable production cost

£

Direct material

8

Direct labour

5

Variable production O/h

2

Variable production cost

15

Working 2: Calculate value

of inventory and production

Opening

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

2 Income statement on the basis of Marginal costing method:

Working 1: Calculate

variable production cost

£

Direct material

8

Direct labour

5

Variable production O/h

2

Variable production cost

15

Working 2: Calculate value

of inventory and production

Opening

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory

Production

Closing inventory

0

2000*15 = 30000

500*15 = 7500

Net profit using marginal

costing

£ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

3 M2

Absorption costing and marginal costing can be used to calculate the net profits of the

firm and it is seen that both are equally important at their places and are different form each

other. In marginal costing only variable costs are considered and in absorption costing fixed cost

is taken. To reconcile both the fixed overheads will be considered and by doing that profits will

be reconciled and thus bring the appropriate financial reporting document (Qian, Burritt and

Monroe, 2011).

4 D2

If a company wants to achieve its goals and targets than they need to make sure that the

data which is available to them are correct and are prepared through conducting proper research.

A irrelevant data can bring loss to the company because the decision made by the managers are

Production

Closing inventory

0

2000*15 = 30000

500*15 = 7500

Net profit using marginal

costing

£ £

Sales

Less Variable costs

Opening stock

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

3 M2

Absorption costing and marginal costing can be used to calculate the net profits of the

firm and it is seen that both are equally important at their places and are different form each

other. In marginal costing only variable costs are considered and in absorption costing fixed cost

is taken. To reconcile both the fixed overheads will be considered and by doing that profits will

be reconciled and thus bring the appropriate financial reporting document (Qian, Burritt and

Monroe, 2011).

4 D2

If a company wants to achieve its goals and targets than they need to make sure that the

data which is available to them are correct and are prepared through conducting proper research.

A irrelevant data can bring loss to the company because the decision made by the managers are

based on those wrong assumptions. So they should check and conduct the business activities by

keeping a notion in their mind.

5 TASK 3

1 (a) Different types of Budget.

Budgeting is the financial planning by a company in which they decide or comes out with

a plan in which they describe where they will be investing the money or funds. There can be

various types of budget which are as follows: -

Financial Budgets: - Such kind of budget are responsible for managing the income,

expenses, assets and cash flows. Strategies are made to allocate funds for these things and it

shows a company spending in relation to its income from the core operations of the company.

Cash Flow Budget: - This kind of budget shows the projected inflow and outflow of the

cash in the business for a specified period of time is known as cash flow budget. Advantage of

this budget is that the company can know that their funds are utilized in proper manner or not.

They could have an idea of the fact that whether they have sufficient money for the task

(Fullerton, Kennedy and Widener, 2013). Through this they can manage the resources of the

company.

Operating Budget: - An operating budget is a forecast and analysis of projected income

and expenses over the course of a specified time period. To create an accurate picture, operating

budgets must account for factors such as sales, production, labour cost, materials costs, overhead,

manufacturing costs and the administrative costs. They are prepared in a week, month or on

yearly basis. The manager could compare these reports and can see where the company is

trending. The main advantage of this is that it assists in managing the current expenses and also

helps in projecting the future expenses that are required to be done by the company.

Master Budget: - It is a aggregate of a company's individual budget designed to present

a complete picture of its financial activity. It contains factors like sales, operating expenses,

assets, and income streams to allow companies to establish goals and can analyse overall

performance. They are used in the large capital companies so that all the individual managers are

aligned. Its advantage is that it gives complete overview of the company and there is no

specificity in it which can be its disadvantage (Cinquini and Tenucci, 2010).

keeping a notion in their mind.

5 TASK 3

1 (a) Different types of Budget.

Budgeting is the financial planning by a company in which they decide or comes out with

a plan in which they describe where they will be investing the money or funds. There can be

various types of budget which are as follows: -

Financial Budgets: - Such kind of budget are responsible for managing the income,

expenses, assets and cash flows. Strategies are made to allocate funds for these things and it

shows a company spending in relation to its income from the core operations of the company.

Cash Flow Budget: - This kind of budget shows the projected inflow and outflow of the

cash in the business for a specified period of time is known as cash flow budget. Advantage of

this budget is that the company can know that their funds are utilized in proper manner or not.

They could have an idea of the fact that whether they have sufficient money for the task

(Fullerton, Kennedy and Widener, 2013). Through this they can manage the resources of the

company.

Operating Budget: - An operating budget is a forecast and analysis of projected income

and expenses over the course of a specified time period. To create an accurate picture, operating

budgets must account for factors such as sales, production, labour cost, materials costs, overhead,

manufacturing costs and the administrative costs. They are prepared in a week, month or on

yearly basis. The manager could compare these reports and can see where the company is

trending. The main advantage of this is that it assists in managing the current expenses and also

helps in projecting the future expenses that are required to be done by the company.

Master Budget: - It is a aggregate of a company's individual budget designed to present

a complete picture of its financial activity. It contains factors like sales, operating expenses,

assets, and income streams to allow companies to establish goals and can analyse overall

performance. They are used in the large capital companies so that all the individual managers are

aligned. Its advantage is that it gives complete overview of the company and there is no

specificity in it which can be its disadvantage (Cinquini and Tenucci, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Static Budget: - It is a fixed budget that remains constant regardless of the changes in

factors such as sales volume or revenue. Imda Tech limited might allocate budget for some

products and the budget for them is same every year whenever budget is allotted. These kinds of

budget are easy to follow and implement and it is basic advantage but these budget lack the

flexibility which prove to be its major disadvantage.

2 (b) Process of preparing a Budget.

There are steps which are followed while preparing a budget, at the initial step it should

be ensured that all the estimates which are required for making budget should be taken into the

account than all those should be distributed or allocated according to the need. In the third step

the concerned departments should be communicated and informed about the budget of their

department. All the authorities should be well aware about the budget and in the fourth step it

should be ensured that budget allocated should be properly implemented and should not go in

waste of effort (Lukka and Modell, 2010). A proper inspection makes sure that all the decided

things are under control and in the final stage a feedback is necessary which gives the company

the detail about the what are the profits and losses. Through this they will get to know what went

wrong and what are the areas where they are lagging behind.

3 (c) Pricing Strategies

It is a way through which the prices of the products are decided and price or cost is the

factor on which the profits of the company depends. While making a pricing strategy a lot of

things are kept in mind like what kind of product it is, what are initial costs like the

manufacturing cost, labour cost, transportation cost are included. Other than this the market of

that product is also considered which helps them to know the market value of that product or

service. Prices should be relevant enough not too high and not too low because a too high price

will dis-attract customers and they will switch on to the different brand and a low price may

attract customers but will give losses to the company. So a medium range price will be best and

will give competitive advantage to the company. Following are some of the pricing strategies

which can be followed:-

Pricing at a Premium: In this the prices are set higher than the competitors and this is

adopted when there is something unique about the products or if something new is introduced in

the market. This is the best strategy for the companies who are entering into the new market and

wants to increase their revenues.

factors such as sales volume or revenue. Imda Tech limited might allocate budget for some

products and the budget for them is same every year whenever budget is allotted. These kinds of

budget are easy to follow and implement and it is basic advantage but these budget lack the

flexibility which prove to be its major disadvantage.

2 (b) Process of preparing a Budget.

There are steps which are followed while preparing a budget, at the initial step it should

be ensured that all the estimates which are required for making budget should be taken into the

account than all those should be distributed or allocated according to the need. In the third step

the concerned departments should be communicated and informed about the budget of their

department. All the authorities should be well aware about the budget and in the fourth step it

should be ensured that budget allocated should be properly implemented and should not go in

waste of effort (Lukka and Modell, 2010). A proper inspection makes sure that all the decided

things are under control and in the final stage a feedback is necessary which gives the company

the detail about the what are the profits and losses. Through this they will get to know what went

wrong and what are the areas where they are lagging behind.

3 (c) Pricing Strategies

It is a way through which the prices of the products are decided and price or cost is the

factor on which the profits of the company depends. While making a pricing strategy a lot of

things are kept in mind like what kind of product it is, what are initial costs like the

manufacturing cost, labour cost, transportation cost are included. Other than this the market of

that product is also considered which helps them to know the market value of that product or

service. Prices should be relevant enough not too high and not too low because a too high price

will dis-attract customers and they will switch on to the different brand and a low price may

attract customers but will give losses to the company. So a medium range price will be best and

will give competitive advantage to the company. Following are some of the pricing strategies

which can be followed:-

Pricing at a Premium: In this the prices are set higher than the competitors and this is

adopted when there is something unique about the products or if something new is introduced in

the market. This is the best strategy for the companies who are entering into the new market and

wants to increase their revenues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pricing for the Market Penetration: With such strategies the new companies will enter

into the market in order to convince people to try their products. Generally, the prices of the

products will be low in comparison to the other brands. Although this will bring losses at the

initial but will give long term profits.

Economy Pricing: In this companies take low cost approach to the marketing and they

does not do anything fancy. This way they are able to keep prices low and attract a certain

specific area of the market.

Price Skimming: Those firms which has competitive advantage can consider this

strategy and can maximize sales on the new products and services. This way they set high rates

during the introductory phase. But after some time they lower the prices sightly as they feel that

competitors goods appear on the market.

Psychology Pricing: This is a unique strategy or technique in which marketers use to

encourage consumers to respond on emotional levels rather than logical ones. For example; the

price of the watch is set £150 so it will attract more customer than setting it at £200 although the

difference is quite low.

4 M3.

Before implementing any work a planning is made which tells a organisation how they

will work in that situation. For preparation of budget forecasting techniques should be used and

on the basis of that estimates are made that they want to achieve that goal in specific period of

time and will require that specific amount for that activity (Ward, 2012).

5 D3.

For solving any financial problems almost every organisation uses different planning tool

and by using those tools they get a sustainable success. Budget is a planning tools which gives a

idea to the organisation that for such type of activity how much money or fund will be required.

Budgets are based on the estimates so any financial can occur and to overcome that situation they

need to be very conscious in budget planning.

into the market in order to convince people to try their products. Generally, the prices of the

products will be low in comparison to the other brands. Although this will bring losses at the

initial but will give long term profits.

Economy Pricing: In this companies take low cost approach to the marketing and they

does not do anything fancy. This way they are able to keep prices low and attract a certain

specific area of the market.

Price Skimming: Those firms which has competitive advantage can consider this

strategy and can maximize sales on the new products and services. This way they set high rates

during the introductory phase. But after some time they lower the prices sightly as they feel that

competitors goods appear on the market.

Psychology Pricing: This is a unique strategy or technique in which marketers use to

encourage consumers to respond on emotional levels rather than logical ones. For example; the

price of the watch is set £150 so it will attract more customer than setting it at £200 although the

difference is quite low.

4 M3.

Before implementing any work a planning is made which tells a organisation how they

will work in that situation. For preparation of budget forecasting techniques should be used and

on the basis of that estimates are made that they want to achieve that goal in specific period of

time and will require that specific amount for that activity (Ward, 2012).

5 D3.

For solving any financial problems almost every organisation uses different planning tool

and by using those tools they get a sustainable success. Budget is a planning tools which gives a

idea to the organisation that for such type of activity how much money or fund will be required.

Budgets are based on the estimates so any financial can occur and to overcome that situation they

need to be very conscious in budget planning.

6 TASK 4

1 (a) Balance scorecard approach.

Balance scorecard is a strategy performance management tool they are used by the

companies to track of the execution of activities by the staff within their control and to monitor

the consequences arising from the actions. Organisations uses it communicate what they are

trying to accomplish, use to measure the performance through monitoring progress towards set

targets and align the day to day work that everyone is doing with strategy. It connects the dots

between big pictures strategy elements like mission or the purpose, what we aspire for, core

values in which we believe in, strategic focus areas like themes, results or goals and the more

other operational elements such as objectives, key performance indicators which track

performance and the initiatives. Balanced scorecards are used by the companies and is widely

used management tool around the world (Otley and Emmanuel, 2013). According to the BSC

Imda Tech (UK) limited can be viewed through four different perspectives and if they want to

achieve, measure, develops objectives they can work on these areas. Following are the factors

through which a organisation can be viewed: -

● Financial:- This perspective sees the Imda Tech (UK) limited through on behalf of their

financial performance and how they use the financial resources. Normally whenever

someone wants to see the performance of any organisation he will simply go through the

profits and losses of the company, what is their sales, how much revenues they are

generating, how much marketing they holds and what is the value of their shares in the

stock market. All the data which falls in financial record are the summary of the company

and gives a brief idea about the companies performance in the specific time period. Every

year it comes out with a financial report which states all the things related to sales,

profits, revenues and this report describe the company in a financial year which has gone.

● Customers/ Stakeholders:- This perspective reviews organisational performance from

the customer or its stakeholders point of view. Customer are the assets of an organisation

and if the customers of the company is happy and satisfied than automatically the

company will be in profit. Imda Tech (UK) limited should take the feedback from the

customers about their charges and which will help them in knowing that does really their

customers are happy from the products they are delivering (Renz, 2016). If customers are

1 (a) Balance scorecard approach.

Balance scorecard is a strategy performance management tool they are used by the

companies to track of the execution of activities by the staff within their control and to monitor

the consequences arising from the actions. Organisations uses it communicate what they are

trying to accomplish, use to measure the performance through monitoring progress towards set

targets and align the day to day work that everyone is doing with strategy. It connects the dots

between big pictures strategy elements like mission or the purpose, what we aspire for, core

values in which we believe in, strategic focus areas like themes, results or goals and the more

other operational elements such as objectives, key performance indicators which track

performance and the initiatives. Balanced scorecards are used by the companies and is widely

used management tool around the world (Otley and Emmanuel, 2013). According to the BSC

Imda Tech (UK) limited can be viewed through four different perspectives and if they want to

achieve, measure, develops objectives they can work on these areas. Following are the factors

through which a organisation can be viewed: -

● Financial:- This perspective sees the Imda Tech (UK) limited through on behalf of their

financial performance and how they use the financial resources. Normally whenever

someone wants to see the performance of any organisation he will simply go through the

profits and losses of the company, what is their sales, how much revenues they are

generating, how much marketing they holds and what is the value of their shares in the

stock market. All the data which falls in financial record are the summary of the company

and gives a brief idea about the companies performance in the specific time period. Every

year it comes out with a financial report which states all the things related to sales,

profits, revenues and this report describe the company in a financial year which has gone.

● Customers/ Stakeholders:- This perspective reviews organisational performance from

the customer or its stakeholders point of view. Customer are the assets of an organisation

and if the customers of the company is happy and satisfied than automatically the

company will be in profit. Imda Tech (UK) limited should take the feedback from the

customers about their charges and which will help them in knowing that does really their

customers are happy from the products they are delivering (Renz, 2016). If customers are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.