Management Accounting: Financial Analysis for IMDA Tech Limited Report

VerifiedAdded on 2020/01/28

|15

|4426

|251

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of IMDA Tech Limited, a retail company. The report begins with an introduction to management accounting, differentiating it from financial accounting and emphasizing its role in providing financial data and advice for managerial decision-making. Key areas covered include cost accounting, inventory management, job costing, and price optimization systems. The report then delves into the calculation of net profit using marginal costing and absorption costing techniques. Furthermore, it examines different types of budgets, their advantages, disadvantages, and the budgeting process itself. The report also explores pricing strategies and concludes with an analysis of the balance scorecard approach, its response to financial problems, and its role in improving financial governance and development. The report includes calculations, working notes, and references to relevant literature.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A)............................................................................................................................................3

1. Meaning of management accounting and the differences between the financial accounting

and the management accounting............................................................................................3

2. Management accounting importance and the information as the decision making tool for

the managers...........................................................................................................................4

B)............................................................................................................................................5

1. Cost accounting .................................................................................................................5

2. Inventory management systems.........................................................................................6

3. Job costing systems............................................................................................................6

4. Price optimising systems....................................................................................................6

TASK 2............................................................................................................................................7

Calculation of net profit through marginal costing techniques and the absorption costing

techniques...............................................................................................................................7

TASK 3............................................................................................................................................9

a) Types of budgets and its advantages and and disadvantages ............................................9

b) Process of budget.............................................................................................................11

c) Pricing strategies..............................................................................................................12

TASK 4..........................................................................................................................................12

A)..........................................................................................................................................12

1) Balance scorecard approach and response to financial problems...................................12

2) Balance scorecards improve financial governance and the development........................13

CONCLUSION....................................................................................................................13

REFERANCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

A)............................................................................................................................................3

1. Meaning of management accounting and the differences between the financial accounting

and the management accounting............................................................................................3

2. Management accounting importance and the information as the decision making tool for

the managers...........................................................................................................................4

B)............................................................................................................................................5

1. Cost accounting .................................................................................................................5

2. Inventory management systems.........................................................................................6

3. Job costing systems............................................................................................................6

4. Price optimising systems....................................................................................................6

TASK 2............................................................................................................................................7

Calculation of net profit through marginal costing techniques and the absorption costing

techniques...............................................................................................................................7

TASK 3............................................................................................................................................9

a) Types of budgets and its advantages and and disadvantages ............................................9

b) Process of budget.............................................................................................................11

c) Pricing strategies..............................................................................................................12

TASK 4..........................................................................................................................................12

A)..........................................................................................................................................12

1) Balance scorecard approach and response to financial problems...................................12

2) Balance scorecards improve financial governance and the development........................13

CONCLUSION....................................................................................................................13

REFERANCES..............................................................................................................................13

INTRODUCTION

The IMDA Tech Limited is a retail company which produces and manufactures the

chargers for the mobiles and also produces the other gadgets on the outlets of the retail. And in

this company there is a issue that the company provide the less financial information to its

managers (Macintosh and Quattrone, 2010). The management accounting helps in to manage the

accounts and the finance from this the accounts are clarified to some managers. In the

management accounting contains the planning, directing and the decision making process and

these all are helps in formulating and preparing the financial report or the financial statement.

And the management statement prepared accurately and correct.

TASK 1

A)

1. Meaning of management accounting and the differences between the financial accounting and

the management accounting

The management accounting helps to provide the financial data and also provides the

advice related to the finance to the company. The management accounting is the process in

which there is the preparation of the financial statements and helps in providing the correct and

the exact financial data (Baldvinsdottir, Mitchell and Nørreklit, 2010). It is a process of

preparing the reports related to accounts and management that gives exact and timely statistical

and financial information which is necessary by mangers of company for making the day to day

decisions. The IMDA Tech Limited company the management accounting helps while making

the strategies. At the time of making the strategies the company have to keep these things in

mind:

determine and manage the risk of the business

examine the environment of the corporate

to review, audit and measure the risk control

to take the advice related to the acquisitions, mergers and the divestment.

Making and determine the financial strategy.

The role of the management accountants of the company are important and unmentioned. It

includes:

The IMDA Tech Limited is a retail company which produces and manufactures the

chargers for the mobiles and also produces the other gadgets on the outlets of the retail. And in

this company there is a issue that the company provide the less financial information to its

managers (Macintosh and Quattrone, 2010). The management accounting helps in to manage the

accounts and the finance from this the accounts are clarified to some managers. In the

management accounting contains the planning, directing and the decision making process and

these all are helps in formulating and preparing the financial report or the financial statement.

And the management statement prepared accurately and correct.

TASK 1

A)

1. Meaning of management accounting and the differences between the financial accounting and

the management accounting

The management accounting helps to provide the financial data and also provides the

advice related to the finance to the company. The management accounting is the process in

which there is the preparation of the financial statements and helps in providing the correct and

the exact financial data (Baldvinsdottir, Mitchell and Nørreklit, 2010). It is a process of

preparing the reports related to accounts and management that gives exact and timely statistical

and financial information which is necessary by mangers of company for making the day to day

decisions. The IMDA Tech Limited company the management accounting helps while making

the strategies. At the time of making the strategies the company have to keep these things in

mind:

determine and manage the risk of the business

examine the environment of the corporate

to review, audit and measure the risk control

to take the advice related to the acquisitions, mergers and the divestment.

Making and determine the financial strategy.

The role of the management accountants of the company are important and unmentioned. It

includes:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps in preparation of the corporate social responsibilities report.

Forecast the budgets related to the business activities

planning, setting up and execution of the projects.

Provide advice on the pricing and the manufacturing of the products.

To analysis of the competitive environment.

The financial accounting concerned with the analyses, summary and the reporting of the

transactions of the finance in the company (Lukka and Modell, 2010). It is the process includes

the recording, measuring, summarizing and also recording the transactions. And these

transactions are help in preparation of the financial reports includes the cash flow statement,

profit & loss statement and the balance sheet of the company.

Management accounting Financial accounting

Its main objective is that to provide the

information related with the cost to the

engagement.

Its main objective is that it helps in providing

the financial condition or the financial

statement of the company.

In this, there are the internal stakeholders. In this, there are the external stakeholders.

It provides the reports on the specific problem

or the task.

It reports on the profitability and the efficiency

related to the business.

It provides the report on the level wise. It provides the results of the reports of the

whole business.

There are different types of management accounting systems:

Traditional accounting systems- This management accounting systems track the prices

by using method of process costing. It helps in evaluate the allocation costs of an organisation

which are related to direct raw materials, labour, production overhead. The process costing is

used to allocate the costs which are based on numbers and also used to manufacture the

homogeneous products.

Lean accounting- This management accounting system helps in eliminating the wastage

from minimizing cost of production.

Transfer pricing- In this method, organisations will cost products and services as they

move by various different functions or departments.

Forecast the budgets related to the business activities

planning, setting up and execution of the projects.

Provide advice on the pricing and the manufacturing of the products.

To analysis of the competitive environment.

The financial accounting concerned with the analyses, summary and the reporting of the

transactions of the finance in the company (Lukka and Modell, 2010). It is the process includes

the recording, measuring, summarizing and also recording the transactions. And these

transactions are help in preparation of the financial reports includes the cash flow statement,

profit & loss statement and the balance sheet of the company.

Management accounting Financial accounting

Its main objective is that to provide the

information related with the cost to the

engagement.

Its main objective is that it helps in providing

the financial condition or the financial

statement of the company.

In this, there are the internal stakeholders. In this, there are the external stakeholders.

It provides the reports on the specific problem

or the task.

It reports on the profitability and the efficiency

related to the business.

It provides the report on the level wise. It provides the results of the reports of the

whole business.

There are different types of management accounting systems:

Traditional accounting systems- This management accounting systems track the prices

by using method of process costing. It helps in evaluate the allocation costs of an organisation

which are related to direct raw materials, labour, production overhead. The process costing is

used to allocate the costs which are based on numbers and also used to manufacture the

homogeneous products.

Lean accounting- This management accounting system helps in eliminating the wastage

from minimizing cost of production.

Transfer pricing- In this method, organisations will cost products and services as they

move by various different functions or departments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Throughput accounting- Its main focus is on identifying the restraint with business

organisation's manufacturing systems. The restraints involves labour, manufacturing facilities,

level of raw materials etc.

2. Management accounting importance and the information as the decision making tool for the

managers

It is the importance part of the management. The management accounting helps in gives

the data and the information related to managing the accounts of the company. The management

accountant helps, guides and also gives the advice to the engagement in the problem. The

management accounting help in increasing the effectiveness and the efficiency of the business as

well as the employees (Ward, 2012). From this the company will achieve the target and enhances

the profitability. The management accounting helps to the management in the decision making.

The importance of the management accounting in the decision making are:

Utilizing the data- It provides the information and the data related to the growth of the

business. There are some examples of the management accounting like balanced scorecards,

budgeting and the financial report projections, these all are help in the provide the data or the

information and from the information guides to the management for the future of the company.

From the information and the data the management make the decisions for the improvement and

for the intelligence analysis the data of the company.

Creating or buying analysis- The management accounting helps in providing the

information which is related to the manufacturing (Renz, 2016). With the help of analysis the

owners of the small businesses take the effective factor decisions.

Analysis of relevant cost- The company used the management accounting to find out

what to be sold and how to be sell. Like for instance there is a business owner and he focuses

only on his marketing efforts. To determine the decision, the accounting manager of the

company can analyse the costs that differ between to the alternatives of the advertisement for

each the products. And to this process is called as the relevant cost analysis.

Activities based Costing techniques- Firstly the company has to examine that what

products to the sell and after that the company need to decide that to whom the products sell. By

using of this techniques, the small scale businesses can identified and to examined the activities

which are necessary to produce and provides the service in a product line.

organisation's manufacturing systems. The restraints involves labour, manufacturing facilities,

level of raw materials etc.

2. Management accounting importance and the information as the decision making tool for the

managers

It is the importance part of the management. The management accounting helps in gives

the data and the information related to managing the accounts of the company. The management

accountant helps, guides and also gives the advice to the engagement in the problem. The

management accounting help in increasing the effectiveness and the efficiency of the business as

well as the employees (Ward, 2012). From this the company will achieve the target and enhances

the profitability. The management accounting helps to the management in the decision making.

The importance of the management accounting in the decision making are:

Utilizing the data- It provides the information and the data related to the growth of the

business. There are some examples of the management accounting like balanced scorecards,

budgeting and the financial report projections, these all are help in the provide the data or the

information and from the information guides to the management for the future of the company.

From the information and the data the management make the decisions for the improvement and

for the intelligence analysis the data of the company.

Creating or buying analysis- The management accounting helps in providing the

information which is related to the manufacturing (Renz, 2016). With the help of analysis the

owners of the small businesses take the effective factor decisions.

Analysis of relevant cost- The company used the management accounting to find out

what to be sold and how to be sell. Like for instance there is a business owner and he focuses

only on his marketing efforts. To determine the decision, the accounting manager of the

company can analyse the costs that differ between to the alternatives of the advertisement for

each the products. And to this process is called as the relevant cost analysis.

Activities based Costing techniques- Firstly the company has to examine that what

products to the sell and after that the company need to decide that to whom the products sell. By

using of this techniques, the small scale businesses can identified and to examined the activities

which are necessary to produce and provides the service in a product line.

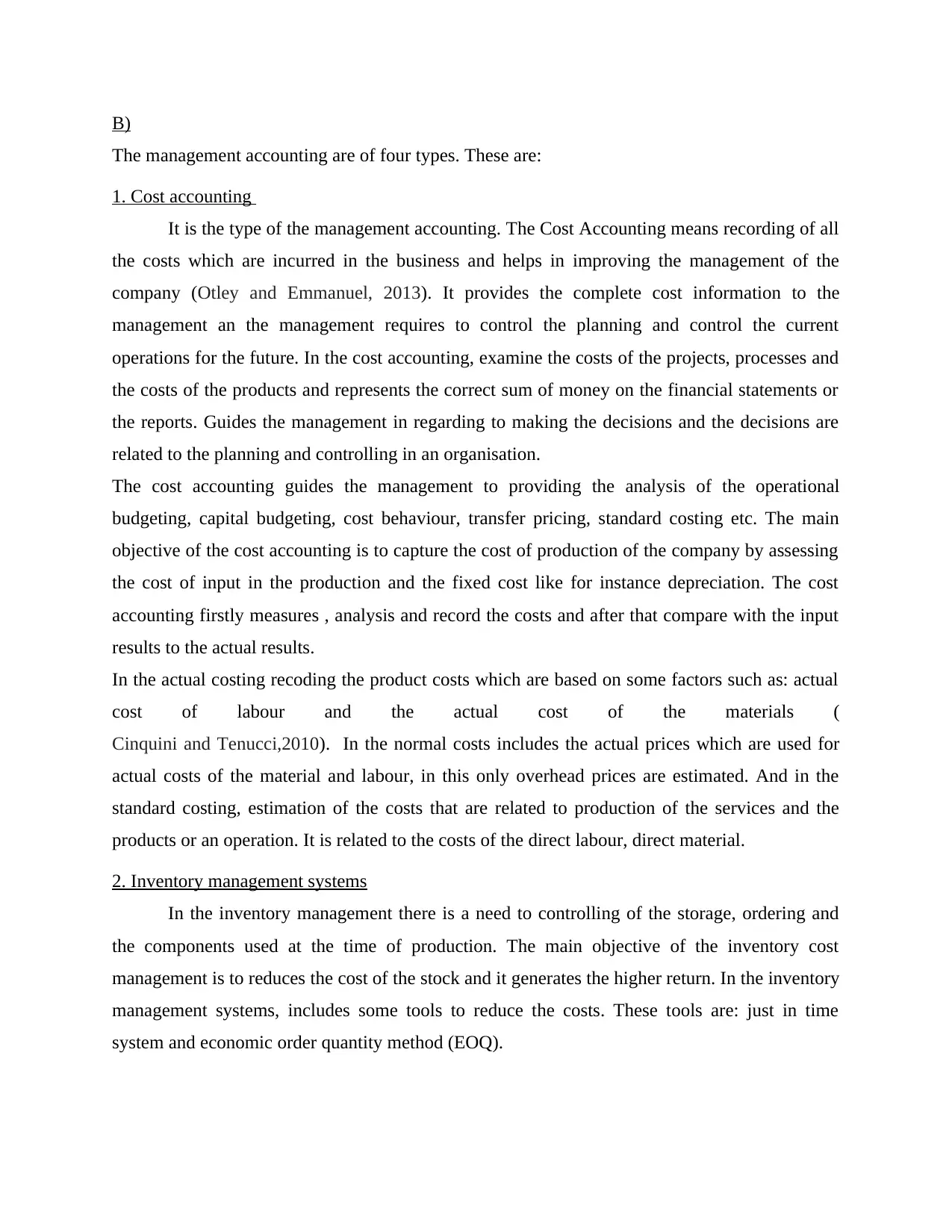

B)

The management accounting are of four types. These are:

1. Cost accounting

It is the type of the management accounting. The Cost Accounting means recording of all

the costs which are incurred in the business and helps in improving the management of the

company (Otley and Emmanuel, 2013). It provides the complete cost information to the

management an the management requires to control the planning and control the current

operations for the future. In the cost accounting, examine the costs of the projects, processes and

the costs of the products and represents the correct sum of money on the financial statements or

the reports. Guides the management in regarding to making the decisions and the decisions are

related to the planning and controlling in an organisation.

The cost accounting guides the management to providing the analysis of the operational

budgeting, capital budgeting, cost behaviour, transfer pricing, standard costing etc. The main

objective of the cost accounting is to capture the cost of production of the company by assessing

the cost of input in the production and the fixed cost like for instance depreciation. The cost

accounting firstly measures , analysis and record the costs and after that compare with the input

results to the actual results.

In the actual costing recoding the product costs which are based on some factors such as: actual

cost of labour and the actual cost of the materials (

Cinquini and Tenucci,2010). In the normal costs includes the actual prices which are used for

actual costs of the material and labour, in this only overhead prices are estimated. And in the

standard costing, estimation of the costs that are related to production of the services and the

products or an operation. It is related to the costs of the direct labour, direct material.

2. Inventory management systems

In the inventory management there is a need to controlling of the storage, ordering and

the components used at the time of production. The main objective of the inventory cost

management is to reduces the cost of the stock and it generates the higher return. In the inventory

management systems, includes some tools to reduce the costs. These tools are: just in time

system and economic order quantity method (EOQ).

The management accounting are of four types. These are:

1. Cost accounting

It is the type of the management accounting. The Cost Accounting means recording of all

the costs which are incurred in the business and helps in improving the management of the

company (Otley and Emmanuel, 2013). It provides the complete cost information to the

management an the management requires to control the planning and control the current

operations for the future. In the cost accounting, examine the costs of the projects, processes and

the costs of the products and represents the correct sum of money on the financial statements or

the reports. Guides the management in regarding to making the decisions and the decisions are

related to the planning and controlling in an organisation.

The cost accounting guides the management to providing the analysis of the operational

budgeting, capital budgeting, cost behaviour, transfer pricing, standard costing etc. The main

objective of the cost accounting is to capture the cost of production of the company by assessing

the cost of input in the production and the fixed cost like for instance depreciation. The cost

accounting firstly measures , analysis and record the costs and after that compare with the input

results to the actual results.

In the actual costing recoding the product costs which are based on some factors such as: actual

cost of labour and the actual cost of the materials (

Cinquini and Tenucci,2010). In the normal costs includes the actual prices which are used for

actual costs of the material and labour, in this only overhead prices are estimated. And in the

standard costing, estimation of the costs that are related to production of the services and the

products or an operation. It is related to the costs of the direct labour, direct material.

2. Inventory management systems

In the inventory management there is a need to controlling of the storage, ordering and

the components used at the time of production. The main objective of the inventory cost

management is to reduces the cost of the stock and it generates the higher return. In the inventory

management systems, includes some tools to reduce the costs. These tools are: just in time

system and economic order quantity method (EOQ).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Job costing systems

In the job costing includes the accumulated costs of the labour, material and the overhead

for the particular job. Mainly it is the structure in which the business finds the way of collecting

the cost which is related to the particular production of work (Qian, Burritt and Monroe 2011). It

used in those situations where the jobs are different. The job costing system includes the data of

the direct costs and the indirect costs. The data defines to deciding the efficiency in the

organisation's structure.

4. Price optimising systems

The price optimising systems of a company used to examine that hoe the customers will

give the response towards the different prices for the services and the products by the different

medium of channels of the company. It is used to examine the costs that the company evaluate

will meet the aims like to maximising the operating profit. The price optimization system has

been applied in some industries. These industries are banking, retail, hotels, airlines and the

insurance industries.

TASK 2

Calculation of net profit through marginal costing techniques and the absorption costing

techniques

In the net profit, the actual profit after the expanses is not included under the calculation

of the gross profit (Vaivio and Sirén, 2010). In the management accounting, the net profit can be

determined through different methods. In the IMDA Tech Limited, the net profit is calculated by

using the marginal cost and the absorption cost method.

Absorption cost- It is the cost method in which the cost of all the expenses are associated

with the manufacturing of the specific product and it is necessary for the generally accepted

accounting principles (GAAP). Mainly the absorption costs involves the direct cost in producing

of the goods. The direct cost related with the manufacturing of the products like for instance

overall costs, raw materials which are used in the production of the products.

According to the Absorption costing:

Selling price £35

Unit costs

Direct materials £8

In the job costing includes the accumulated costs of the labour, material and the overhead

for the particular job. Mainly it is the structure in which the business finds the way of collecting

the cost which is related to the particular production of work (Qian, Burritt and Monroe 2011). It

used in those situations where the jobs are different. The job costing system includes the data of

the direct costs and the indirect costs. The data defines to deciding the efficiency in the

organisation's structure.

4. Price optimising systems

The price optimising systems of a company used to examine that hoe the customers will

give the response towards the different prices for the services and the products by the different

medium of channels of the company. It is used to examine the costs that the company evaluate

will meet the aims like to maximising the operating profit. The price optimization system has

been applied in some industries. These industries are banking, retail, hotels, airlines and the

insurance industries.

TASK 2

Calculation of net profit through marginal costing techniques and the absorption costing

techniques

In the net profit, the actual profit after the expanses is not included under the calculation

of the gross profit (Vaivio and Sirén, 2010). In the management accounting, the net profit can be

determined through different methods. In the IMDA Tech Limited, the net profit is calculated by

using the marginal cost and the absorption cost method.

Absorption cost- It is the cost method in which the cost of all the expenses are associated

with the manufacturing of the specific product and it is necessary for the generally accepted

accounting principles (GAAP). Mainly the absorption costs involves the direct cost in producing

of the goods. The direct cost related with the manufacturing of the products like for instance

overall costs, raw materials which are used in the production of the products.

According to the Absorption costing:

Selling price £35

Unit costs

Direct materials £8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

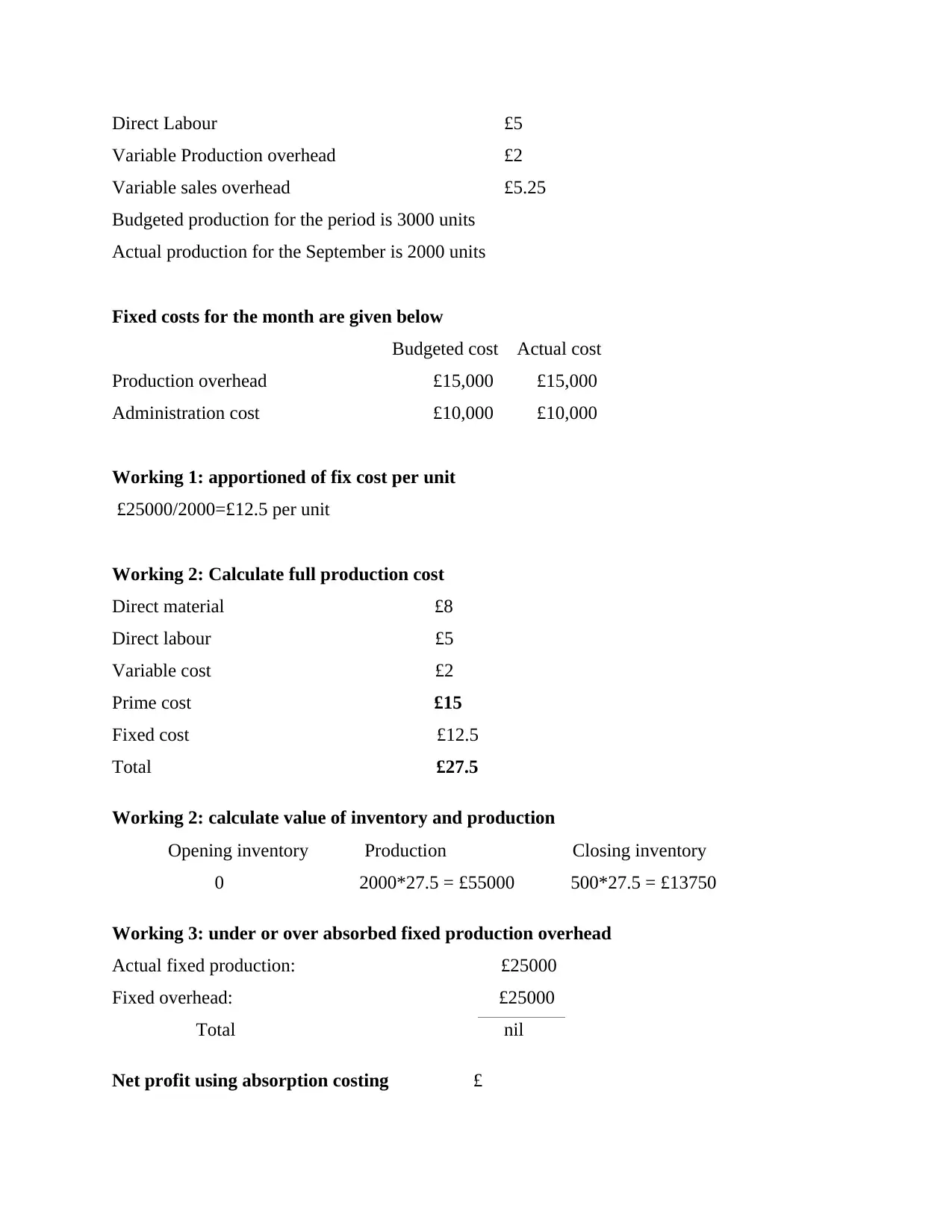

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000 units

Actual production for the September is 2000 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £15,000 £15,000

Administration cost £10,000 £10,000

Working 1: apportioned of fix cost per unit

£25000/2000=£12.5 per unit

Working 2: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Fixed cost £12.5

Total £27.5

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*27.5 = £55000 500*27.5 = £13750

Working 3: under or over absorbed fixed production overhead

Actual fixed production: £25000

Fixed overhead: £25000

Total nil

Net profit using absorption costing £

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000 units

Actual production for the September is 2000 units

Fixed costs for the month are given below

Budgeted cost Actual cost

Production overhead £15,000 £15,000

Administration cost £10,000 £10,000

Working 1: apportioned of fix cost per unit

£25000/2000=£12.5 per unit

Working 2: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Fixed cost £12.5

Total £27.5

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*27.5 = £55000 500*27.5 = £13750

Working 3: under or over absorbed fixed production overhead

Actual fixed production: £25000

Fixed overhead: £25000

Total nil

Net profit using absorption costing £

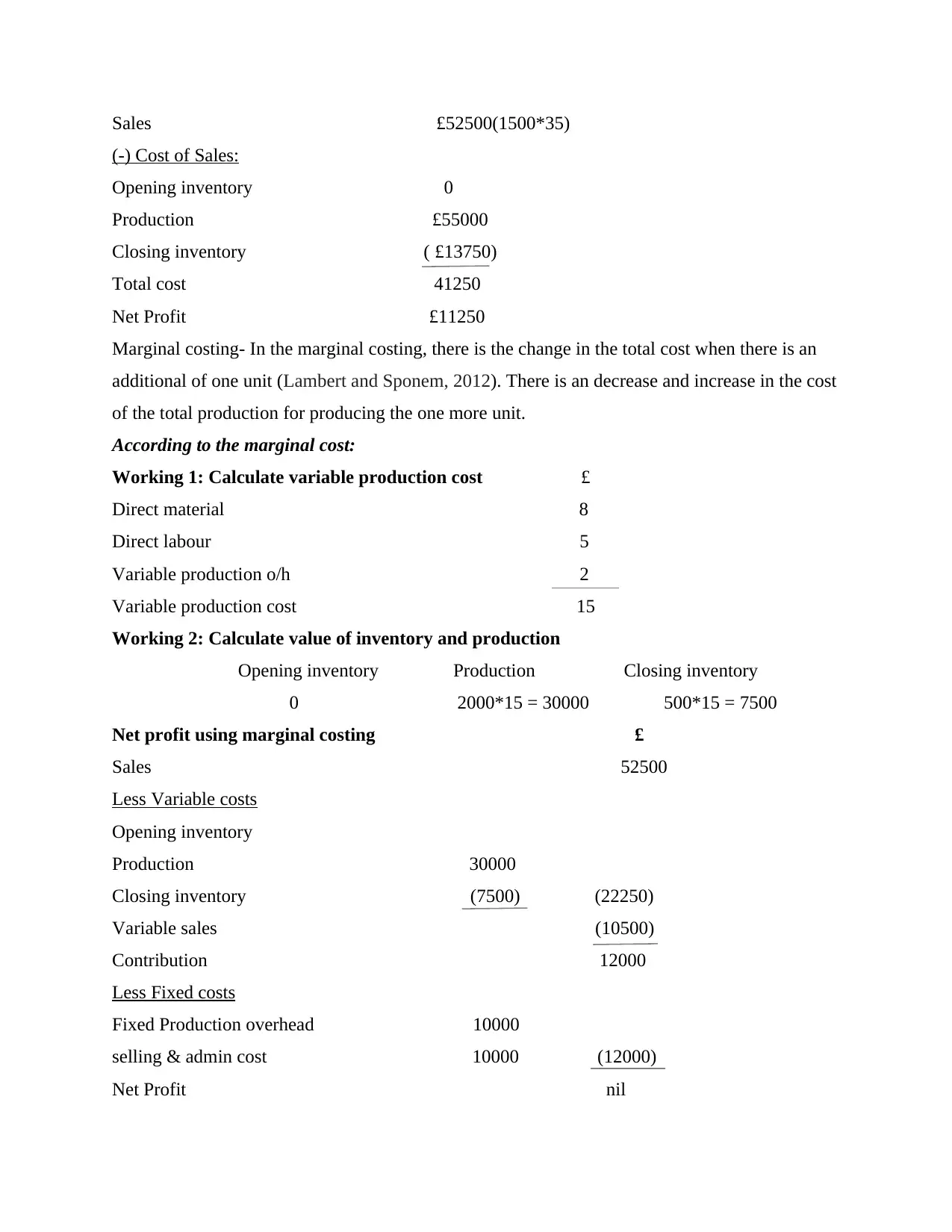

Sales £52500(1500*35)

(-) Cost of Sales:

Opening inventory 0

Production £55000

Closing inventory ( £13750)

Total cost 41250

Net Profit £11250

Marginal costing- In the marginal costing, there is the change in the total cost when there is an

additional of one unit (Lambert and Sponem, 2012). There is an decrease and increase in the cost

of the total production for producing the one more unit.

According to the marginal cost:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production o/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £

Sales 52500

Less Variable costs

Opening inventory

Production 30000

Closing inventory (7500) (22250)

Variable sales (10500)

Contribution 12000

Less Fixed costs

Fixed Production overhead 10000

selling & admin cost 10000 (12000)

Net Profit nil

(-) Cost of Sales:

Opening inventory 0

Production £55000

Closing inventory ( £13750)

Total cost 41250

Net Profit £11250

Marginal costing- In the marginal costing, there is the change in the total cost when there is an

additional of one unit (Lambert and Sponem, 2012). There is an decrease and increase in the cost

of the total production for producing the one more unit.

According to the marginal cost:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production o/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £

Sales 52500

Less Variable costs

Opening inventory

Production 30000

Closing inventory (7500) (22250)

Variable sales (10500)

Contribution 12000

Less Fixed costs

Fixed Production overhead 10000

selling & admin cost 10000 (12000)

Net Profit nil

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

a) Types of budgets and its advantages and and disadvantages

Budget is for the future estimation of the expenses and the revenues. The deficit budget

means the the expenses will exceed from the revenues and the surplus budget means the profits.

The businesses use the different types of the budgets (Van Helden and Northcott 2010). Every

department of the company makes their own budgets fro this the department estimates their

expenses and the revenues. There are five different types of budgets:

A) Master budget

B) Operational budget

C)Financial budget

D)Cash flow budget

E) Static budget

A) Master budget- The master budget is an estimation of the company budget which is

designed to show complete image of the financial activities of the business. In the master budget

includes the factors such as operating expenses, sales, assets and the income streams which

permit to the companies to set up the goals and to determine the overall performance. Generally

the master budgets are used in the large companies to keep the managers on aligned. There are

some advantages and some disadvantages of the master budget (Herbert and Seal,2012). The

advantages are:

All the budgets are available in the one report.

The master budget provides the overall estimation of the profit of the company.

It helps in evaluating the completely budget in the capsule form.

Disadvantages are:

In this budget there is less specification.

It determines the whole budget so there is a difficulty in creating and reading and

understanding the budgets.

B) Operational budget- In these types of the budgets includes the expenses and the

revenues which are around to the day to day operations of the company. The expenses presents

the overhead, cost of goods sold which are directly related with the production of the services

and the goods and the revenues are generally related with the sales of the services and the goods.

In the operational budgets includes some factors like administrative expenses, overhead costs,

a) Types of budgets and its advantages and and disadvantages

Budget is for the future estimation of the expenses and the revenues. The deficit budget

means the the expenses will exceed from the revenues and the surplus budget means the profits.

The businesses use the different types of the budgets (Van Helden and Northcott 2010). Every

department of the company makes their own budgets fro this the department estimates their

expenses and the revenues. There are five different types of budgets:

A) Master budget

B) Operational budget

C)Financial budget

D)Cash flow budget

E) Static budget

A) Master budget- The master budget is an estimation of the company budget which is

designed to show complete image of the financial activities of the business. In the master budget

includes the factors such as operating expenses, sales, assets and the income streams which

permit to the companies to set up the goals and to determine the overall performance. Generally

the master budgets are used in the large companies to keep the managers on aligned. There are

some advantages and some disadvantages of the master budget (Herbert and Seal,2012). The

advantages are:

All the budgets are available in the one report.

The master budget provides the overall estimation of the profit of the company.

It helps in evaluating the completely budget in the capsule form.

Disadvantages are:

In this budget there is less specification.

It determines the whole budget so there is a difficulty in creating and reading and

understanding the budgets.

B) Operational budget- In these types of the budgets includes the expenses and the

revenues which are around to the day to day operations of the company. The expenses presents

the overhead, cost of goods sold which are directly related with the production of the services

and the goods and the revenues are generally related with the sales of the services and the goods.

In the operational budgets includes some factors like administrative expenses, overhead costs,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

material costs, manufacturing and the labour costs (Dillard and Roslender, 2011). The

operational budgets are prepared generally on the monthly basis, weekly basis or on the yearly

basis. In the operational budget there are some advantages and some disadvantages. The

advantages are:

It helps in evaluate the projection of future expenses

The operational expenses are helps in managing the current expenses.

Some disadvantages are:

It is costly because the cost is spend on managing the activities.

C)Financial budgets- In the financial budgets shows the strategy of the company for managing

the expenses, income and the cash flow. The financial budget represents the financial health of

the company and also represents the overview which is related to the revenues from the

operations. The financial budgets have some advantages and some disadvantages. The

advantages are:

Financial budgets are helpful in creating the budgets effectively and easy to

understandable.

This budget gives the controls over the finance.

There are also some disadvantage:

The financial budget id lengthy in the nature so it is difficult to understand.

D) Cash flow budget- In this budget there is an assumption of all the expenditures and all the

cash receipts that are expects to happen in a specific period of time. The estimation can be

prepared on the quarterly, monthly and the bimonthly basis (Chenhall and Smith, 2011). The

cash flow budgets have some advantages and disadvantages. The advantages are:

The main advantage are it is easy to maintain the exact cast reserves.

The audit is more easily in this budget than the matching concepts.

E) Static budget- It is the fixed budget that remains with the unaltered changes under the

factors like revenue and the sales volume. In the static budgets, includes the elements in which

the expenditures are to be unchanged . The advantages of the Static budgeting are:

The static budget is easy to implement and easy to follow

This budget offer strong insights in the cost of the company and the profits.

Disadvantages are:

There is the lack of flexibility.

operational budgets are prepared generally on the monthly basis, weekly basis or on the yearly

basis. In the operational budget there are some advantages and some disadvantages. The

advantages are:

It helps in evaluate the projection of future expenses

The operational expenses are helps in managing the current expenses.

Some disadvantages are:

It is costly because the cost is spend on managing the activities.

C)Financial budgets- In the financial budgets shows the strategy of the company for managing

the expenses, income and the cash flow. The financial budget represents the financial health of

the company and also represents the overview which is related to the revenues from the

operations. The financial budgets have some advantages and some disadvantages. The

advantages are:

Financial budgets are helpful in creating the budgets effectively and easy to

understandable.

This budget gives the controls over the finance.

There are also some disadvantage:

The financial budget id lengthy in the nature so it is difficult to understand.

D) Cash flow budget- In this budget there is an assumption of all the expenditures and all the

cash receipts that are expects to happen in a specific period of time. The estimation can be

prepared on the quarterly, monthly and the bimonthly basis (Chenhall and Smith, 2011). The

cash flow budgets have some advantages and disadvantages. The advantages are:

The main advantage are it is easy to maintain the exact cast reserves.

The audit is more easily in this budget than the matching concepts.

E) Static budget- It is the fixed budget that remains with the unaltered changes under the

factors like revenue and the sales volume. In the static budgets, includes the elements in which

the expenditures are to be unchanged . The advantages of the Static budgeting are:

The static budget is easy to implement and easy to follow

This budget offer strong insights in the cost of the company and the profits.

Disadvantages are:

There is the lack of flexibility.

It is based on the previous data so there is a difficulty to the new businesses to

implementation.

b) Process of budget

To preparing the budgets the company have to follow some points. These points are :

1. Firstly collect the information regarding the expenses and income from the different

sources.

2. After that there is a need to allocate the required factors which are helpful in making the

budgets.

3. After allocation of the factors there is a need to make the list of the monthly expenses.

On this list mentioned all types of the expenses.

4. In this step there is a need to split the expenses in to the variable expenses and in the

fixed expenses. In the variable expenses includes daily things like coffee, eating or food

items, groceries items (Natasha Gilani.,2017).In the fixed expenses includes the bills like

for instance rent, Internet expenses, cable bills etc.

5. After that total of the monthly expenses and the incomes. This helps in calculation of the

profit and loss inside the business.

6. Then there is a need to cut the irrelevant expenses or which are not necessary, if the

expenses are higher than the income.

7. Then it is necessary to take the monthly review of the budget and check that the activities

are managed properly.

8. After that if there is any kind of need arise related to extra expenses then plan for the

extra expenses

9. Money saving in budget. If there is some money left in the budget then add the money in

to the savings.

10. After all these steps, the company need to balance the budget.

c) Pricing strategies

The pricing strategies generally used in the different types of the purposes like for

instance expansion of the profit margin and increment in the market share (Contrafatto and

Burns, 2013). The company uses the different types of the pricing strategies. The types of this

strategies are:

implementation.

b) Process of budget

To preparing the budgets the company have to follow some points. These points are :

1. Firstly collect the information regarding the expenses and income from the different

sources.

2. After that there is a need to allocate the required factors which are helpful in making the

budgets.

3. After allocation of the factors there is a need to make the list of the monthly expenses.

On this list mentioned all types of the expenses.

4. In this step there is a need to split the expenses in to the variable expenses and in the

fixed expenses. In the variable expenses includes daily things like coffee, eating or food

items, groceries items (Natasha Gilani.,2017).In the fixed expenses includes the bills like

for instance rent, Internet expenses, cable bills etc.

5. After that total of the monthly expenses and the incomes. This helps in calculation of the

profit and loss inside the business.

6. Then there is a need to cut the irrelevant expenses or which are not necessary, if the

expenses are higher than the income.

7. Then it is necessary to take the monthly review of the budget and check that the activities

are managed properly.

8. After that if there is any kind of need arise related to extra expenses then plan for the

extra expenses

9. Money saving in budget. If there is some money left in the budget then add the money in

to the savings.

10. After all these steps, the company need to balance the budget.

c) Pricing strategies

The pricing strategies generally used in the different types of the purposes like for

instance expansion of the profit margin and increment in the market share (Contrafatto and

Burns, 2013). The company uses the different types of the pricing strategies. The types of this

strategies are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.