Comprehensive Management Accounting Report for Imda Tech Ltd

VerifiedAdded on 2020/01/07

|18

|5040

|376

Report

AI Summary

This report provides a comprehensive overview of management accounting, using Imda Tech Ltd as a case study. It begins by defining management accounting and distinguishing it from financial accounting, emphasizing its role in decision-making. The report explores different types of management accounting systems, including costing, inventory management, job costing, and price optimization systems. It then delves into absorption and marginal costing methods, presenting income statements for Imda Tech Ltd based on each method. Furthermore, the report examines various budgeting types, their advantages, disadvantages, and the budgeting process. Pricing strategies are also discussed. Finally, the report describes the Balance Score Card (BSC) and its implementation, including its use in identifying and responding to financial problems and improving financial governance and strategy development. The analysis covers key aspects of management accounting, offering valuable insights for business development and financial management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

introduction......................................................................................................................................4

TASK 1............................................................................................................................................4

a) Preparing a well-researcheched written report on the functions of management accounting. 4

i) Defining management accounting and distinguish management accounting from financial

accounting....................................................................................................................................4

ii) Importance of management accounting information as decision making tool........................5

b) Different types of management accounting system ................................................................6

TASK 2............................................................................................................................................7

Absorption costing.......................................................................................................................7

Marginal costing methods............................................................................................................9

TASK 3..........................................................................................................................................11

a) Different types of budgets and their advantages and disadvantages.....................................11

b) Process of preparing the budgets...........................................................................................12

c) Pricing strategies....................................................................................................................13

TASK 4..........................................................................................................................................13

a) Describing the Balance Score Card and its implementation..................................................14

i) Using Balance Score Card (BSC) to identify and respond financial problem.......................14

ii) Use of Balance Score Card to improve the financial governance and development of

effective strategies.....................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

Illustration Index

Illustration 1: Financial perspective of BSC..................................................................................15

Illustration 2: Balance Score Card.................................................................................................16

introduction......................................................................................................................................4

TASK 1............................................................................................................................................4

a) Preparing a well-researcheched written report on the functions of management accounting. 4

i) Defining management accounting and distinguish management accounting from financial

accounting....................................................................................................................................4

ii) Importance of management accounting information as decision making tool........................5

b) Different types of management accounting system ................................................................6

TASK 2............................................................................................................................................7

Absorption costing.......................................................................................................................7

Marginal costing methods............................................................................................................9

TASK 3..........................................................................................................................................11

a) Different types of budgets and their advantages and disadvantages.....................................11

b) Process of preparing the budgets...........................................................................................12

c) Pricing strategies....................................................................................................................13

TASK 4..........................................................................................................................................13

a) Describing the Balance Score Card and its implementation..................................................14

i) Using Balance Score Card (BSC) to identify and respond financial problem.......................14

ii) Use of Balance Score Card to improve the financial governance and development of

effective strategies.....................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

Illustration Index

Illustration 1: Financial perspective of BSC..................................................................................15

Illustration 2: Balance Score Card.................................................................................................16

INTRODUCTION

Management accounting is the important field or section of the finance which helps to

prepare the effective report and meet the expectations of all related parties. It covers activities

related to presenting the financial information with the accumulation of reliable information or

valid data. The current report is based on Imda Tech Ltd; dealing with special charger for mobile

telephone and other carry on gadgets in UK. Further, report covers the difference between

management and financial accounting. In addition to this, Balance Score card has also been

applied for measuring the performance of the business and meeting the expected objectives or

outcome. Moreover, different types of management accounting system are also explained.

TASK 1

a) Preparing a well-researcheched written report on the functions of management accounting

The functions of management accounting are explained as follows which consists of

different aspects related to costing. This enables corporation to integrate all related activities and

accomplish long as well as short term objectives of the business in an effectual manner. It covers

below mentioned aspects-

i) Defining management accounting and distinguish management accounting from financial

accounting

The management accounting consists of several activities such as preparing and

providing timely statistical and financial information to business management so as to take daily

decision along with other related short term decision. For this purpose, it becomes easy to state

the difference between management and financial accounting (Kaplan and Atkinson, 2015).

Furthermore management accounting helps corporation Imda Tech Ltd, in the following manner-

The decision making and planning are based on the data collected or presented through

management accounting

The employees or managers are motivated for achieving the organizational objectives

Use of management accounting facilitates to create the competitive position of the

business in the marketplace.

The performance of the corporation is measures in accordance with activities, sub-units

and managers as well as employees.

Management accounting is the important field or section of the finance which helps to

prepare the effective report and meet the expectations of all related parties. It covers activities

related to presenting the financial information with the accumulation of reliable information or

valid data. The current report is based on Imda Tech Ltd; dealing with special charger for mobile

telephone and other carry on gadgets in UK. Further, report covers the difference between

management and financial accounting. In addition to this, Balance Score card has also been

applied for measuring the performance of the business and meeting the expected objectives or

outcome. Moreover, different types of management accounting system are also explained.

TASK 1

a) Preparing a well-researcheched written report on the functions of management accounting

The functions of management accounting are explained as follows which consists of

different aspects related to costing. This enables corporation to integrate all related activities and

accomplish long as well as short term objectives of the business in an effectual manner. It covers

below mentioned aspects-

i) Defining management accounting and distinguish management accounting from financial

accounting

The management accounting consists of several activities such as preparing and

providing timely statistical and financial information to business management so as to take daily

decision along with other related short term decision. For this purpose, it becomes easy to state

the difference between management and financial accounting (Kaplan and Atkinson, 2015).

Furthermore management accounting helps corporation Imda Tech Ltd, in the following manner-

The decision making and planning are based on the data collected or presented through

management accounting

The employees or managers are motivated for achieving the organizational objectives

Use of management accounting facilitates to create the competitive position of the

business in the marketplace.

The performance of the corporation is measures in accordance with activities, sub-units

and managers as well as employees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

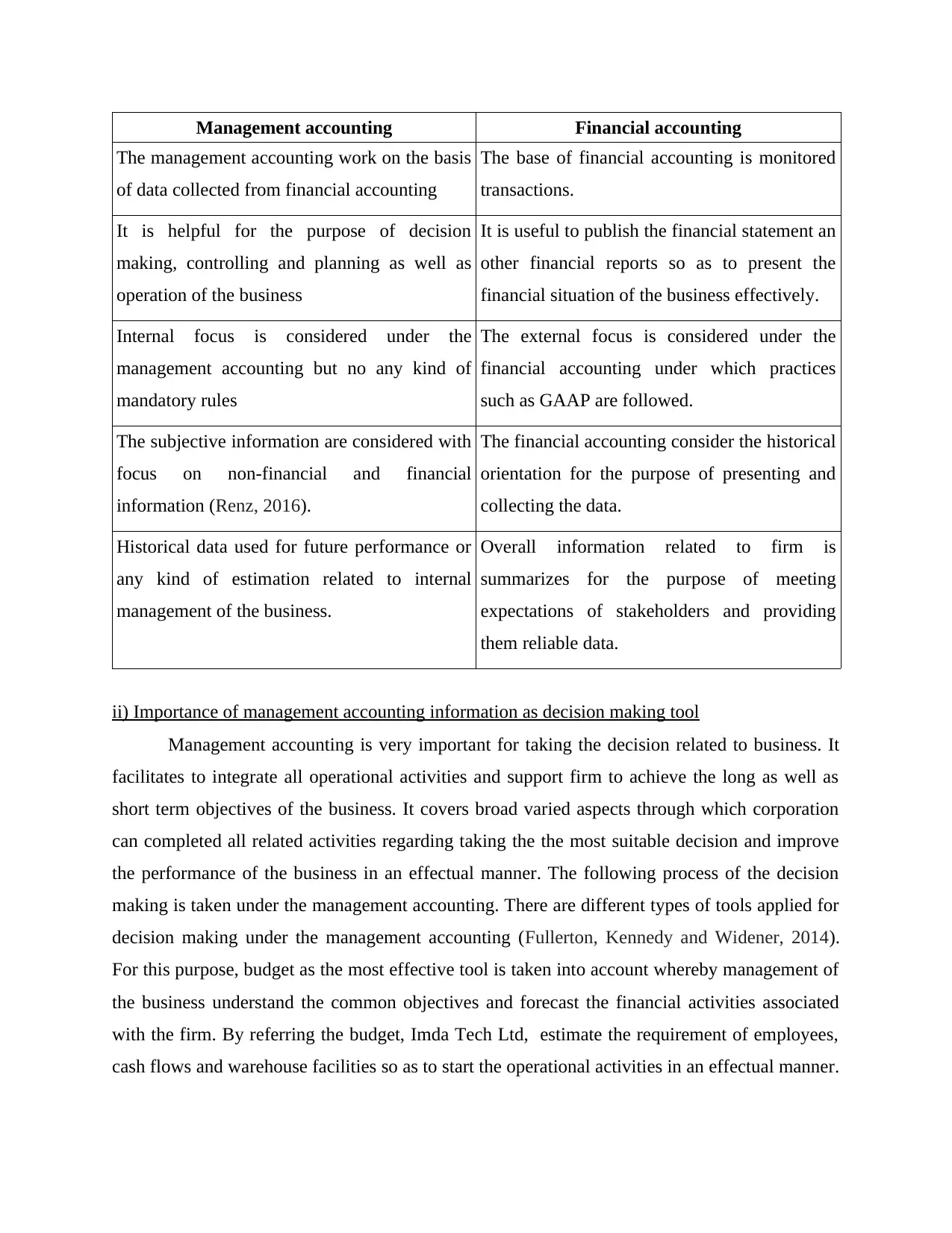

Management accounting Financial accounting

The management accounting work on the basis

of data collected from financial accounting

The base of financial accounting is monitored

transactions.

It is helpful for the purpose of decision

making, controlling and planning as well as

operation of the business

It is useful to publish the financial statement an

other financial reports so as to present the

financial situation of the business effectively.

Internal focus is considered under the

management accounting but no any kind of

mandatory rules

The external focus is considered under the

financial accounting under which practices

such as GAAP are followed.

The subjective information are considered with

focus on non-financial and financial

information (Renz, 2016).

The financial accounting consider the historical

orientation for the purpose of presenting and

collecting the data.

Historical data used for future performance or

any kind of estimation related to internal

management of the business.

Overall information related to firm is

summarizes for the purpose of meeting

expectations of stakeholders and providing

them reliable data.

ii) Importance of management accounting information as decision making tool

Management accounting is very important for taking the decision related to business. It

facilitates to integrate all operational activities and support firm to achieve the long as well as

short term objectives of the business. It covers broad varied aspects through which corporation

can completed all related activities regarding taking the the most suitable decision and improve

the performance of the business in an effectual manner. The following process of the decision

making is taken under the management accounting. There are different types of tools applied for

decision making under the management accounting (Fullerton, Kennedy and Widener, 2014).

For this purpose, budget as the most effective tool is taken into account whereby management of

the business understand the common objectives and forecast the financial activities associated

with the firm. By referring the budget, Imda Tech Ltd, estimate the requirement of employees,

cash flows and warehouse facilities so as to start the operational activities in an effectual manner.

The management accounting work on the basis

of data collected from financial accounting

The base of financial accounting is monitored

transactions.

It is helpful for the purpose of decision

making, controlling and planning as well as

operation of the business

It is useful to publish the financial statement an

other financial reports so as to present the

financial situation of the business effectively.

Internal focus is considered under the

management accounting but no any kind of

mandatory rules

The external focus is considered under the

financial accounting under which practices

such as GAAP are followed.

The subjective information are considered with

focus on non-financial and financial

information (Renz, 2016).

The financial accounting consider the historical

orientation for the purpose of presenting and

collecting the data.

Historical data used for future performance or

any kind of estimation related to internal

management of the business.

Overall information related to firm is

summarizes for the purpose of meeting

expectations of stakeholders and providing

them reliable data.

ii) Importance of management accounting information as decision making tool

Management accounting is very important for taking the decision related to business. It

facilitates to integrate all operational activities and support firm to achieve the long as well as

short term objectives of the business. It covers broad varied aspects through which corporation

can completed all related activities regarding taking the the most suitable decision and improve

the performance of the business in an effectual manner. The following process of the decision

making is taken under the management accounting. There are different types of tools applied for

decision making under the management accounting (Fullerton, Kennedy and Widener, 2014).

For this purpose, budget as the most effective tool is taken into account whereby management of

the business understand the common objectives and forecast the financial activities associated

with the firm. By referring the budget, Imda Tech Ltd, estimate the requirement of employees,

cash flows and warehouse facilities so as to start the operational activities in an effectual manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this manner, budget is applied for the purpose of bring certainty with the business and

managing the cash flow in an effectual manner. Furthermore, make or buy decision is taken

under the management accounting which is derived with the help of comparing the relevant cost.

The decision making tool as the cost volume-profit analysis is applied so that decision

related to approximate sales turnover can be taken. Here, management shed light on graphical

form of the collected data and accordingly gather the information that what proportion of sales

will be needed to meet the objectives (Otley and Emmanuel, 2013). At the same time, estimated

price is also determined through which company can reduce the certain and ensure competitive

edge of the business. In addition to this, product costing is helpful to find the cost of product by

using marginal accounting.

b) Different types of management accounting system

There are different types of management accounting system applied by the corporation.

This in turn each job is completed in a cost effective manner. These different types of

management accounting system are explained as follows-

i) Costing accounting system

This method is applied to find the cost of each products and service produced under Imda

Tech Ltd. It involves the job order costing and process costing. At this juncture, different

methods are included under the cost accounting system such as input measurement basis,

inventory valuation methods as well as cost-flow assumption and recording interval capacity. It

is helpful for business to derive valid outcome and reach the end results effectively. Here, the

real time component reflects the most valuable feature associated with cost accounting. In this

manner, it consists of both job and process costing so as to represent the benefits from the cost

accounting (Suomala, Lyly-Yrjänäinen and Lukka, 2014). This leads to keep record related to

performance of the business in an effectual manner. Many corporations like Imda Tech Ltd

follows the computerized system so as that keep track over progress of each operational

department. This is effective to control the inventory system and determine the long run success

of the business by controlling overall expenses associated with the production procedure of the

Imda Tech Ltd.

ii) Inventory management systems

managing the cash flow in an effectual manner. Furthermore, make or buy decision is taken

under the management accounting which is derived with the help of comparing the relevant cost.

The decision making tool as the cost volume-profit analysis is applied so that decision

related to approximate sales turnover can be taken. Here, management shed light on graphical

form of the collected data and accordingly gather the information that what proportion of sales

will be needed to meet the objectives (Otley and Emmanuel, 2013). At the same time, estimated

price is also determined through which company can reduce the certain and ensure competitive

edge of the business. In addition to this, product costing is helpful to find the cost of product by

using marginal accounting.

b) Different types of management accounting system

There are different types of management accounting system applied by the corporation.

This in turn each job is completed in a cost effective manner. These different types of

management accounting system are explained as follows-

i) Costing accounting system

This method is applied to find the cost of each products and service produced under Imda

Tech Ltd. It involves the job order costing and process costing. At this juncture, different

methods are included under the cost accounting system such as input measurement basis,

inventory valuation methods as well as cost-flow assumption and recording interval capacity. It

is helpful for business to derive valid outcome and reach the end results effectively. Here, the

real time component reflects the most valuable feature associated with cost accounting. In this

manner, it consists of both job and process costing so as to represent the benefits from the cost

accounting (Suomala, Lyly-Yrjänäinen and Lukka, 2014). This leads to keep record related to

performance of the business in an effectual manner. Many corporations like Imda Tech Ltd

follows the computerized system so as that keep track over progress of each operational

department. This is effective to control the inventory system and determine the long run success

of the business by controlling overall expenses associated with the production procedure of the

Imda Tech Ltd.

ii) Inventory management systems

The inventory management system is the most important part of the business through

which all input used under the production of products and services. For this purpose, appropriate

techniques such as Just in time and last in first out and first in first out are used. This is helpful to

manage the inventory effectively and reduce the extra cost incurred in the storage etc. This is

done under the management accounting system and accordingly most effective tool is applied for

better performance of the business.

iii) Job costing systems

The job costing system is a system under which manufacturing cost of each individual

unit produced under the particular batch is recorded. This is helpful for management to

determine the price of products and services. For this purpose, different aspects are considered

under the job costing such as allocation of overheads, labour and material etc. In addition to this,

job costing accumulate the cost related to overheads, material and labor effective trough which

price of product and services is considered (Job Costing, 2017). In this manner, costing for each

element is determined through which it becomes easy to increase overall rate of return.

iv) Price optimizing systems

Price optimization system is another aspect under which cost or price of the product is

determined with the help of different price levels. For this purpose, cost related to cost and

inventory level are applied for the recommending the appropriate price decision for the purpose

of deriving higher level of profitability.

TASK 2

According to the give, scenario, income statement of the Imda Tech Ltd has been

prepared which is presenting the information related to sales turnover and other related expenses

regarding different activities. It has been presented as follows. In this context, absorption and

marginal costing are considered for preparing the income statement. However, major difference

of the both costing method can be seen under income statement of the business. This proves to be

effective to derive valid outcome and ensure the best utilization of limited resources and meet the

long as well as short term objectives of the same (Dung and Aoki, 2014).

Absorption costing

The absorption costing is calculated on the basis of total cost for each cost center for the

purpose finding the total cost. Here, variable and fixed cost both are considered along with

which all input used under the production of products and services. For this purpose, appropriate

techniques such as Just in time and last in first out and first in first out are used. This is helpful to

manage the inventory effectively and reduce the extra cost incurred in the storage etc. This is

done under the management accounting system and accordingly most effective tool is applied for

better performance of the business.

iii) Job costing systems

The job costing system is a system under which manufacturing cost of each individual

unit produced under the particular batch is recorded. This is helpful for management to

determine the price of products and services. For this purpose, different aspects are considered

under the job costing such as allocation of overheads, labour and material etc. In addition to this,

job costing accumulate the cost related to overheads, material and labor effective trough which

price of product and services is considered (Job Costing, 2017). In this manner, costing for each

element is determined through which it becomes easy to increase overall rate of return.

iv) Price optimizing systems

Price optimization system is another aspect under which cost or price of the product is

determined with the help of different price levels. For this purpose, cost related to cost and

inventory level are applied for the recommending the appropriate price decision for the purpose

of deriving higher level of profitability.

TASK 2

According to the give, scenario, income statement of the Imda Tech Ltd has been

prepared which is presenting the information related to sales turnover and other related expenses

regarding different activities. It has been presented as follows. In this context, absorption and

marginal costing are considered for preparing the income statement. However, major difference

of the both costing method can be seen under income statement of the business. This proves to be

effective to derive valid outcome and ensure the best utilization of limited resources and meet the

long as well as short term objectives of the same (Dung and Aoki, 2014).

Absorption costing

The absorption costing is calculated on the basis of total cost for each cost center for the

purpose finding the total cost. Here, variable and fixed cost both are considered along with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

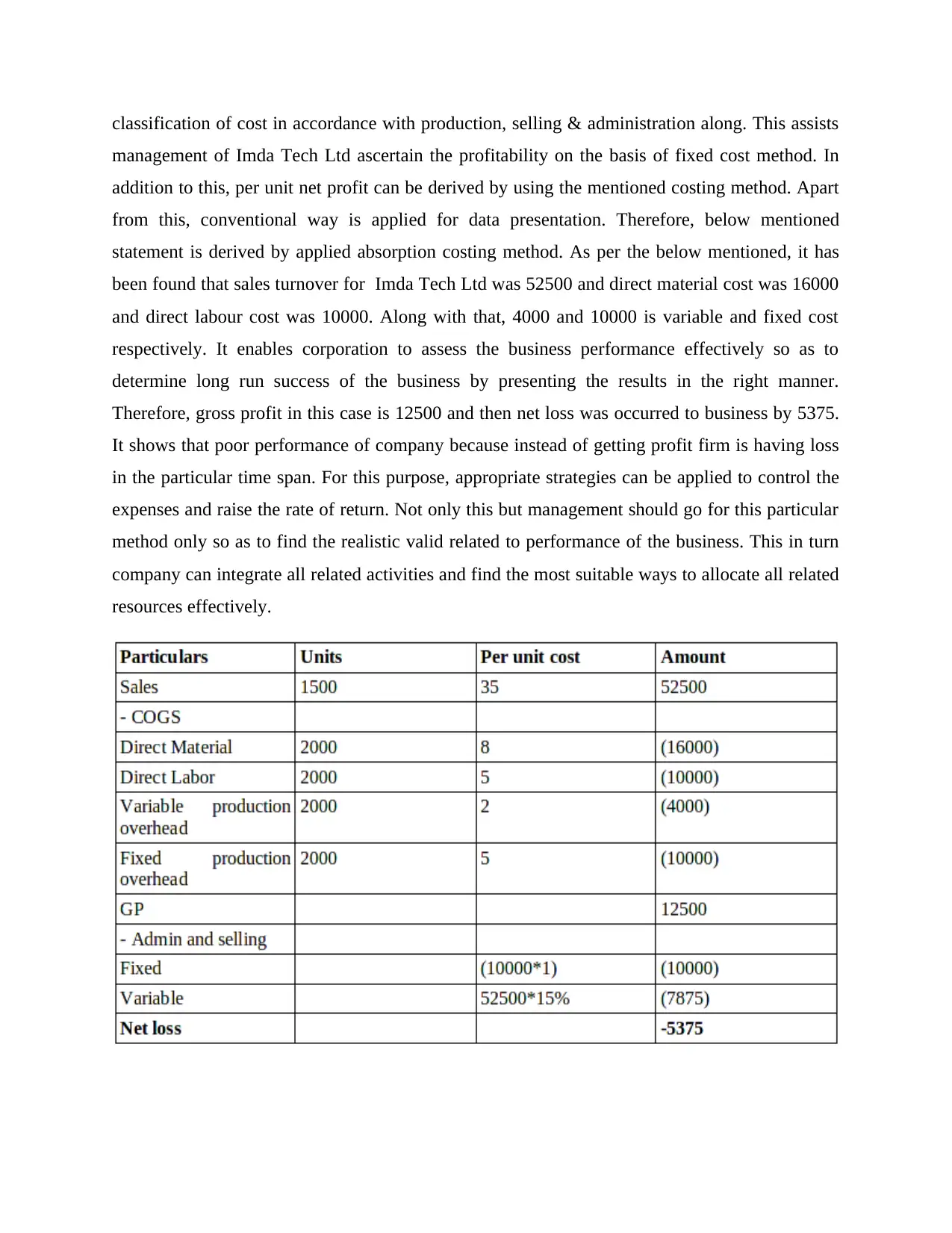

classification of cost in accordance with production, selling & administration along. This assists

management of Imda Tech Ltd ascertain the profitability on the basis of fixed cost method. In

addition to this, per unit net profit can be derived by using the mentioned costing method. Apart

from this, conventional way is applied for data presentation. Therefore, below mentioned

statement is derived by applied absorption costing method. As per the below mentioned, it has

been found that sales turnover for Imda Tech Ltd was 52500 and direct material cost was 16000

and direct labour cost was 10000. Along with that, 4000 and 10000 is variable and fixed cost

respectively. It enables corporation to assess the business performance effectively so as to

determine long run success of the business by presenting the results in the right manner.

Therefore, gross profit in this case is 12500 and then net loss was occurred to business by 5375.

It shows that poor performance of company because instead of getting profit firm is having loss

in the particular time span. For this purpose, appropriate strategies can be applied to control the

expenses and raise the rate of return. Not only this but management should go for this particular

method only so as to find the realistic valid related to performance of the business. This in turn

company can integrate all related activities and find the most suitable ways to allocate all related

resources effectively.

management of Imda Tech Ltd ascertain the profitability on the basis of fixed cost method. In

addition to this, per unit net profit can be derived by using the mentioned costing method. Apart

from this, conventional way is applied for data presentation. Therefore, below mentioned

statement is derived by applied absorption costing method. As per the below mentioned, it has

been found that sales turnover for Imda Tech Ltd was 52500 and direct material cost was 16000

and direct labour cost was 10000. Along with that, 4000 and 10000 is variable and fixed cost

respectively. It enables corporation to assess the business performance effectively so as to

determine long run success of the business by presenting the results in the right manner.

Therefore, gross profit in this case is 12500 and then net loss was occurred to business by 5375.

It shows that poor performance of company because instead of getting profit firm is having loss

in the particular time span. For this purpose, appropriate strategies can be applied to control the

expenses and raise the rate of return. Not only this but management should go for this particular

method only so as to find the realistic valid related to performance of the business. This in turn

company can integrate all related activities and find the most suitable ways to allocate all related

resources effectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

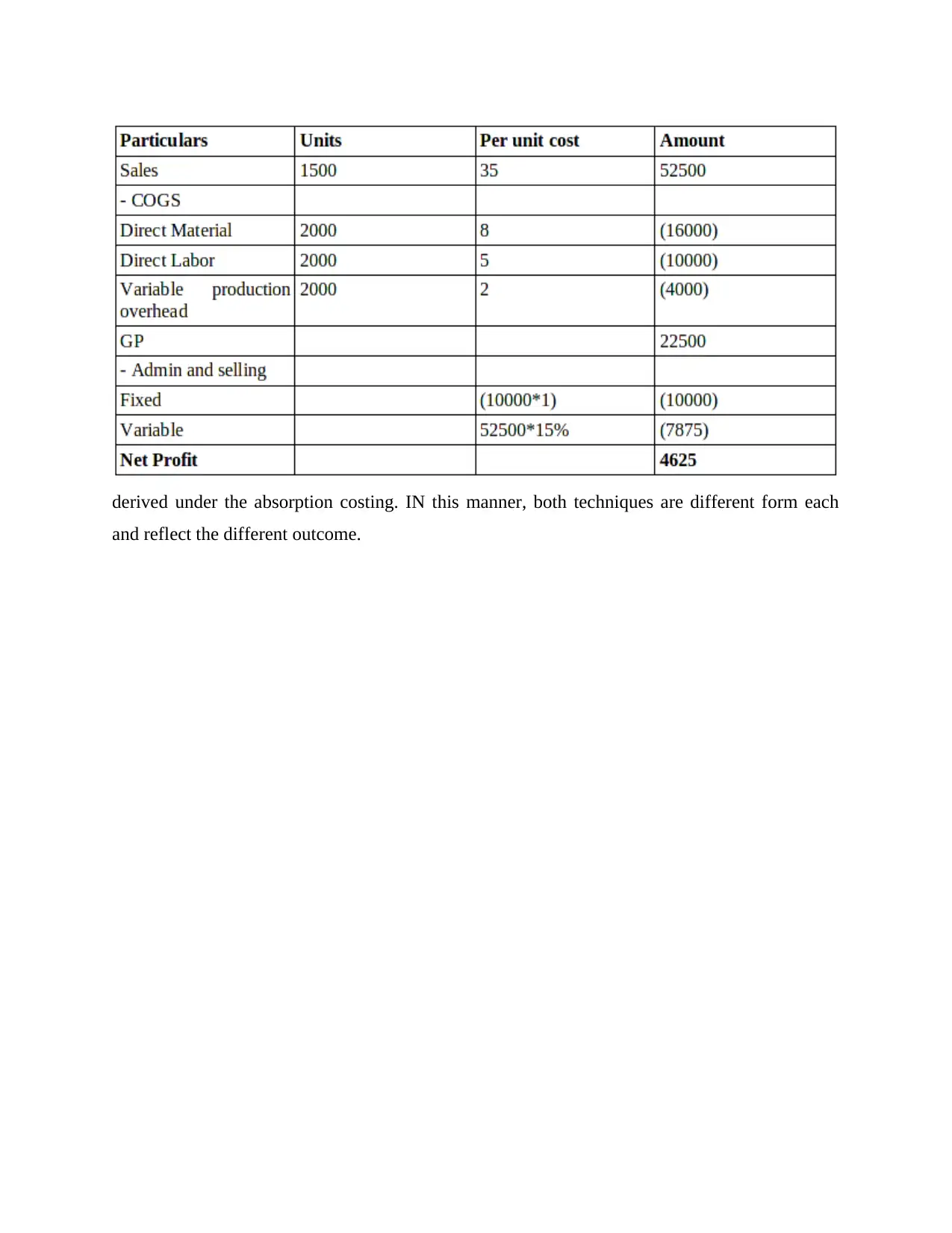

Marginal costing methods

The marginal costing method is considered as the another important one under which

data are collected and presented in the tabular form. Here, total cost of production is known as

the marginal costing wherein both fixed and variable cost are considered in context of

classification. Furthermore, the ratio used to measure the profitability is by profit volume ratio. It

contributes towards the determining the success of the business over a certain time span (Kaplan

and Atkinson, 2015). Moreover, the cost per unit does not have any impact of the variance

between closing and opening stock. Moreover, contribution per unit is considered by Imda Tech

Ltd for keeping record related to financial performance of the business. The below mentioned

table is showing that net profit derive from the Imda Tech Ltd for particular time span. It has

been found that sales turnover will be 52500 and cost occurred in direct material was 16000. On

the other hand, direct lobour has cost of 10000 whereas variable production overhead was 4000.

In this manner, gross profit derived for the business was 22500. Furthermore, administration and

selling cost has been deductive through which net profit has 4625 was derived by the business.

This is showing that profitability under marginal cost can be derived ion comparison to other

selected method of cost. The main reason behind the same is that fixed cost is not deducted from

the gross profit and accordingly corporation easily cover its cost of production and derive the

higher rate of return.

The report mentioned from each as marginal and absorption costing has found and

accordingly, it has been suggested to management of Imda Tech Ltd to go for first method only.

The main reason behind applying that particular method to find the clear information related to

financial performance of the business and control over the related activities to deliver good

quality of services among all related parties. In this manner, it can be effectively said or stated

that firm can use the suitable method to keep record related to direct or indirect expenses and

direct effect of the same can be seen on profitability of the same. In addition to this, difference

between the marginal and absorption costing can be taken into account which reflects that cost

application is different and measurement as well as profitability arrived from both kind of

method is also different (Taipaleenmäki and Ikäheimo, 2013). It enables corporation to integrate

all related activities and determine the higher rate of return from the business. In addition to this,

marginal costing reflects the profit measurement with the help of contribution whereas gross is

The marginal costing method is considered as the another important one under which

data are collected and presented in the tabular form. Here, total cost of production is known as

the marginal costing wherein both fixed and variable cost are considered in context of

classification. Furthermore, the ratio used to measure the profitability is by profit volume ratio. It

contributes towards the determining the success of the business over a certain time span (Kaplan

and Atkinson, 2015). Moreover, the cost per unit does not have any impact of the variance

between closing and opening stock. Moreover, contribution per unit is considered by Imda Tech

Ltd for keeping record related to financial performance of the business. The below mentioned

table is showing that net profit derive from the Imda Tech Ltd for particular time span. It has

been found that sales turnover will be 52500 and cost occurred in direct material was 16000. On

the other hand, direct lobour has cost of 10000 whereas variable production overhead was 4000.

In this manner, gross profit derived for the business was 22500. Furthermore, administration and

selling cost has been deductive through which net profit has 4625 was derived by the business.

This is showing that profitability under marginal cost can be derived ion comparison to other

selected method of cost. The main reason behind the same is that fixed cost is not deducted from

the gross profit and accordingly corporation easily cover its cost of production and derive the

higher rate of return.

The report mentioned from each as marginal and absorption costing has found and

accordingly, it has been suggested to management of Imda Tech Ltd to go for first method only.

The main reason behind applying that particular method to find the clear information related to

financial performance of the business and control over the related activities to deliver good

quality of services among all related parties. In this manner, it can be effectively said or stated

that firm can use the suitable method to keep record related to direct or indirect expenses and

direct effect of the same can be seen on profitability of the same. In addition to this, difference

between the marginal and absorption costing can be taken into account which reflects that cost

application is different and measurement as well as profitability arrived from both kind of

method is also different (Taipaleenmäki and Ikäheimo, 2013). It enables corporation to integrate

all related activities and determine the higher rate of return from the business. In addition to this,

marginal costing reflects the profit measurement with the help of contribution whereas gross is

derived under the absorption costing. IN this manner, both techniques are different form each

and reflect the different outcome.

and reflect the different outcome.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

a) Different types of budgets and their advantages and disadvantages

There are different types of budget which can be used by corporation to manage all

operational activities effectively so as to meet the objectives of Imda Tech Limited. Following

types of budgets are prepared by the business- Master budget-It is considered as the final budget under which all functions are added

and approved by the top management for its implementation. The advantages of master

budget is that it represents all functions budget and provide the estimation of profit.

Furthermore, forecasting can be done by the budget effectively. The disadvantages of

master budget is that issue in one budget leads to wrong foresting. Operational budget-This budget deals with daily operational activities of corporation.

Here, revenue shows that activities which derive the profit for the business where as cost

or expenses head indicates that how firm increases the cost of production. The major

advantages of operational budget is appropriate management of current expenses and

protecting the future one (Blackstone, 2017). This in turn revenue can be built for future.

In addition to this, disadvantages of operational budget indicates inaccuracy and rigid

decision making. Cash flow budget-It is the most common budget prepared in each organization like Imda

Tech Limited so as to manage the present or future cash as well as expenses. The major

advantage of cash budget is control over expenses and disadvantages can be related to

wrong estimation and ignorance to external factors affecting the performance of the

business.

Sales budget-It is considered as the planning instrument and control mechanism under

which all related activities of the business is associated in order to manage the

performance of the business effectively and control the entire performance of the

corporation to a great extent (Beatty and Liao, 2014).

b) Process of preparing the budgets

The budget is considered as the important aspect for estimation of future profitability and

expenses regarding the company under consideration. For this purpose, management of Imda

Tech Ltd can prepare the budget in the following manner-

a) Different types of budgets and their advantages and disadvantages

There are different types of budget which can be used by corporation to manage all

operational activities effectively so as to meet the objectives of Imda Tech Limited. Following

types of budgets are prepared by the business- Master budget-It is considered as the final budget under which all functions are added

and approved by the top management for its implementation. The advantages of master

budget is that it represents all functions budget and provide the estimation of profit.

Furthermore, forecasting can be done by the budget effectively. The disadvantages of

master budget is that issue in one budget leads to wrong foresting. Operational budget-This budget deals with daily operational activities of corporation.

Here, revenue shows that activities which derive the profit for the business where as cost

or expenses head indicates that how firm increases the cost of production. The major

advantages of operational budget is appropriate management of current expenses and

protecting the future one (Blackstone, 2017). This in turn revenue can be built for future.

In addition to this, disadvantages of operational budget indicates inaccuracy and rigid

decision making. Cash flow budget-It is the most common budget prepared in each organization like Imda

Tech Limited so as to manage the present or future cash as well as expenses. The major

advantage of cash budget is control over expenses and disadvantages can be related to

wrong estimation and ignorance to external factors affecting the performance of the

business.

Sales budget-It is considered as the planning instrument and control mechanism under

which all related activities of the business is associated in order to manage the

performance of the business effectively and control the entire performance of the

corporation to a great extent (Beatty and Liao, 2014).

b) Process of preparing the budgets

The budget is considered as the important aspect for estimation of future profitability and

expenses regarding the company under consideration. For this purpose, management of Imda

Tech Ltd can prepare the budget in the following manner-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Obtaining the estimation-It is the first and foremost step under which estimation is done

for the production and sales level. This in turn it becomes easy for the management to

forecast the cost in term of available resources. However, Imda Tech Ltd will consider

the cost of each department with regard, production, marketing and sales etc. Coordinating the estimates-Under this stage, team of budget consult regarding the

different plans related to availability of resources so as to implement the plan on right in

an effectual manner. Here, resources are allocated for each activities involved under the

development of budget (Tan, Libby and Hunton, 2015). Communicating budget-After completion of planning activities and allocation of

resources, management of finance department handle the task related to communicating

regarding the purpose or aim of the plans among the responsible parties. However,

necessary changes and modification are incorporated under budget if any department

provides the valuable suggestion. Implementing the budget plan- Just after the communication regarding the budget for

each department and Imda Tech Ltd, management implement the budget by taking into

account certain budget period (Kaplan and Atkinson, 2015). For this purpose, required

material such as labour, facilities and other related aspects for carrying out production

activities are provided.

Reporting interim progress towards the budgeted objectives-This report is prepared by

each department of Imda Tech Ltd and provided to the management of the corporation. It

aids to assess the performance of the business in accordance with set standards. However,

top management also organize the investigation to assess the gap between actual and

expected results. It leads to bring the perfection in the budget process and meet the

objectives of the corporation effectively.

c) Pricing strategies

The pricing strategies plays important role in recovering the cost of production and

determining the long run success of the business in the marketplace. The pricing strategies

explained as follows- Competitive pricing-Under this price of products and services are set in accordance with

competitors. It is most effective only in case when firm is targeting for its survival only.

for the production and sales level. This in turn it becomes easy for the management to

forecast the cost in term of available resources. However, Imda Tech Ltd will consider

the cost of each department with regard, production, marketing and sales etc. Coordinating the estimates-Under this stage, team of budget consult regarding the

different plans related to availability of resources so as to implement the plan on right in

an effectual manner. Here, resources are allocated for each activities involved under the

development of budget (Tan, Libby and Hunton, 2015). Communicating budget-After completion of planning activities and allocation of

resources, management of finance department handle the task related to communicating

regarding the purpose or aim of the plans among the responsible parties. However,

necessary changes and modification are incorporated under budget if any department

provides the valuable suggestion. Implementing the budget plan- Just after the communication regarding the budget for

each department and Imda Tech Ltd, management implement the budget by taking into

account certain budget period (Kaplan and Atkinson, 2015). For this purpose, required

material such as labour, facilities and other related aspects for carrying out production

activities are provided.

Reporting interim progress towards the budgeted objectives-This report is prepared by

each department of Imda Tech Ltd and provided to the management of the corporation. It

aids to assess the performance of the business in accordance with set standards. However,

top management also organize the investigation to assess the gap between actual and

expected results. It leads to bring the perfection in the budget process and meet the

objectives of the corporation effectively.

c) Pricing strategies

The pricing strategies plays important role in recovering the cost of production and

determining the long run success of the business in the marketplace. The pricing strategies

explained as follows- Competitive pricing-Under this price of products and services are set in accordance with

competitors. It is most effective only in case when firm is targeting for its survival only.

It aids to avoid price war and allow business to maintain its competitive edge in the

marketplace. It facilitates to increase the profitability and meet the expectations of all

related parties. Multiple pricing-This strategy is applied by the business to attract more customers. For

example, Imda Tech Ltd can charge 5GBP for one charger and 7GBP for charger plus

earphone. It proves to be effective to increase sales turnover and raise the profitability of

business too. This in turn resources can be used in an appropriate manner whereby

company can effectively integrate its resources so as to determine competitive edge in the

marketplace (Fullerton, Kennedy and Widener, 2014). Penetration pricing-Such kind of pricing strategy is very effective for new market under

which Imda Tech Ltd at first set very low price to gain the attraction of the customers.

Once the specific objectives of the business met then prices are increased to raise the rate

of return. However, it is applicable in case firm want to maximize the quality and or

revenue. It is also helpful to retain customers and enhance their level of satisfaction in an

effectual manner.

Skim pricing- This pricing strategy is applied for the unique product which are few in the

market and competitors are not higher for the same. This assists business to control the

expenses and increase overall rate of return. However, when the competition in the

market increases then business start lowering down the price. This in turn it becomes

easy to create the competitive edge of the business in the marketplace (Otley and

Emmanuel, 2013).

TASK 4

According to the given scenario, Imda Tech Ltd suffer from loss of £1.5 million and now

management has desire to implement effective ways through which performance can be

improved. At this juncture, role of management accounting in responding the financial problems

have been explained. This in turn auditors will go for the Balance Score Card approach to

improve the current performance effectively.

a) Describing the Balance Score Card and its implementation

Balance Score Card refers to the management tool which helps to maintain the short term

performance of business by measuring the financial aspects. By using this approach it becomes

marketplace. It facilitates to increase the profitability and meet the expectations of all

related parties. Multiple pricing-This strategy is applied by the business to attract more customers. For

example, Imda Tech Ltd can charge 5GBP for one charger and 7GBP for charger plus

earphone. It proves to be effective to increase sales turnover and raise the profitability of

business too. This in turn resources can be used in an appropriate manner whereby

company can effectively integrate its resources so as to determine competitive edge in the

marketplace (Fullerton, Kennedy and Widener, 2014). Penetration pricing-Such kind of pricing strategy is very effective for new market under

which Imda Tech Ltd at first set very low price to gain the attraction of the customers.

Once the specific objectives of the business met then prices are increased to raise the rate

of return. However, it is applicable in case firm want to maximize the quality and or

revenue. It is also helpful to retain customers and enhance their level of satisfaction in an

effectual manner.

Skim pricing- This pricing strategy is applied for the unique product which are few in the

market and competitors are not higher for the same. This assists business to control the

expenses and increase overall rate of return. However, when the competition in the

market increases then business start lowering down the price. This in turn it becomes

easy to create the competitive edge of the business in the marketplace (Otley and

Emmanuel, 2013).

TASK 4

According to the given scenario, Imda Tech Ltd suffer from loss of £1.5 million and now

management has desire to implement effective ways through which performance can be

improved. At this juncture, role of management accounting in responding the financial problems

have been explained. This in turn auditors will go for the Balance Score Card approach to

improve the current performance effectively.

a) Describing the Balance Score Card and its implementation

Balance Score Card refers to the management tool which helps to maintain the short term

performance of business by measuring the financial aspects. By using this approach it becomes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.