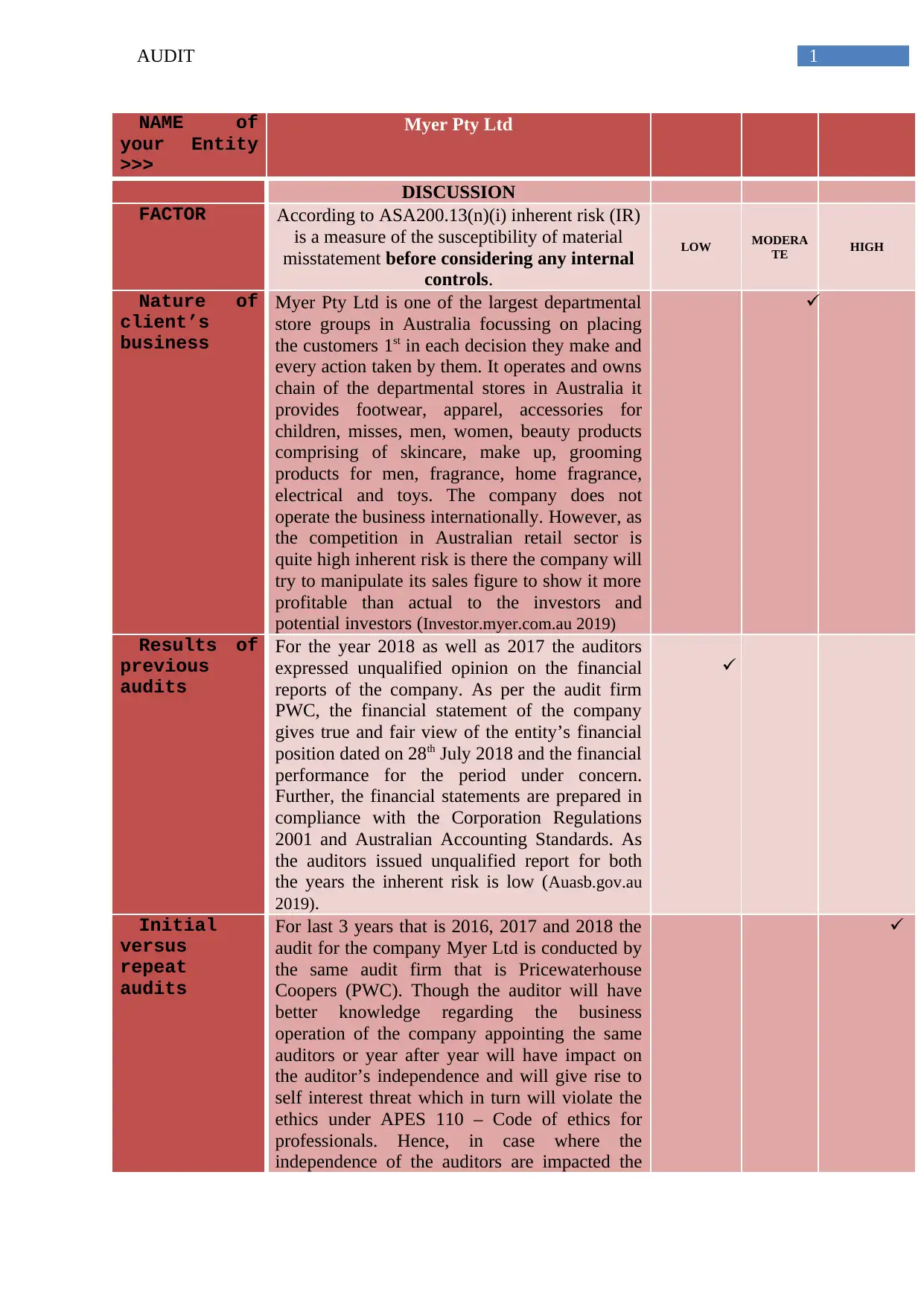

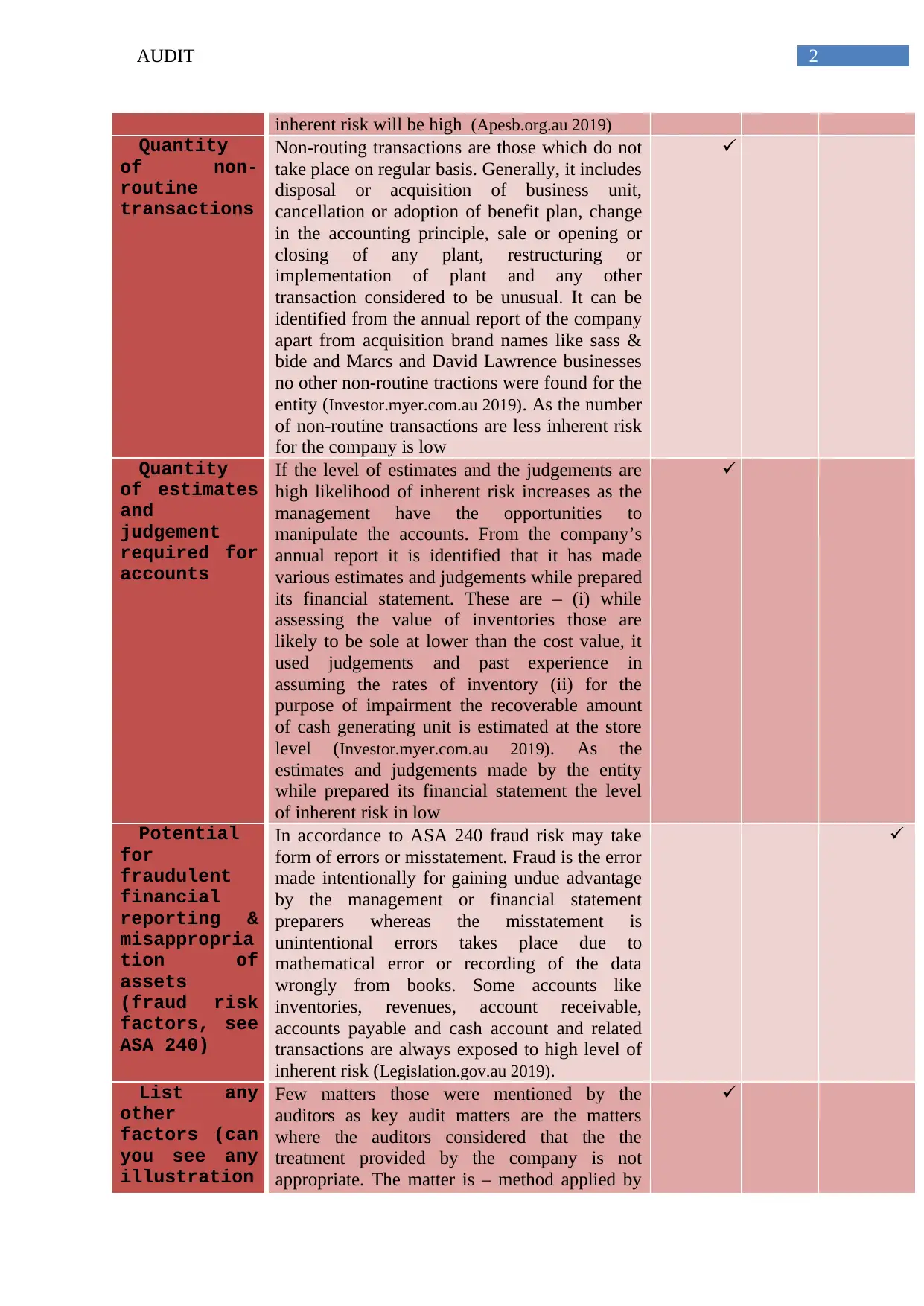

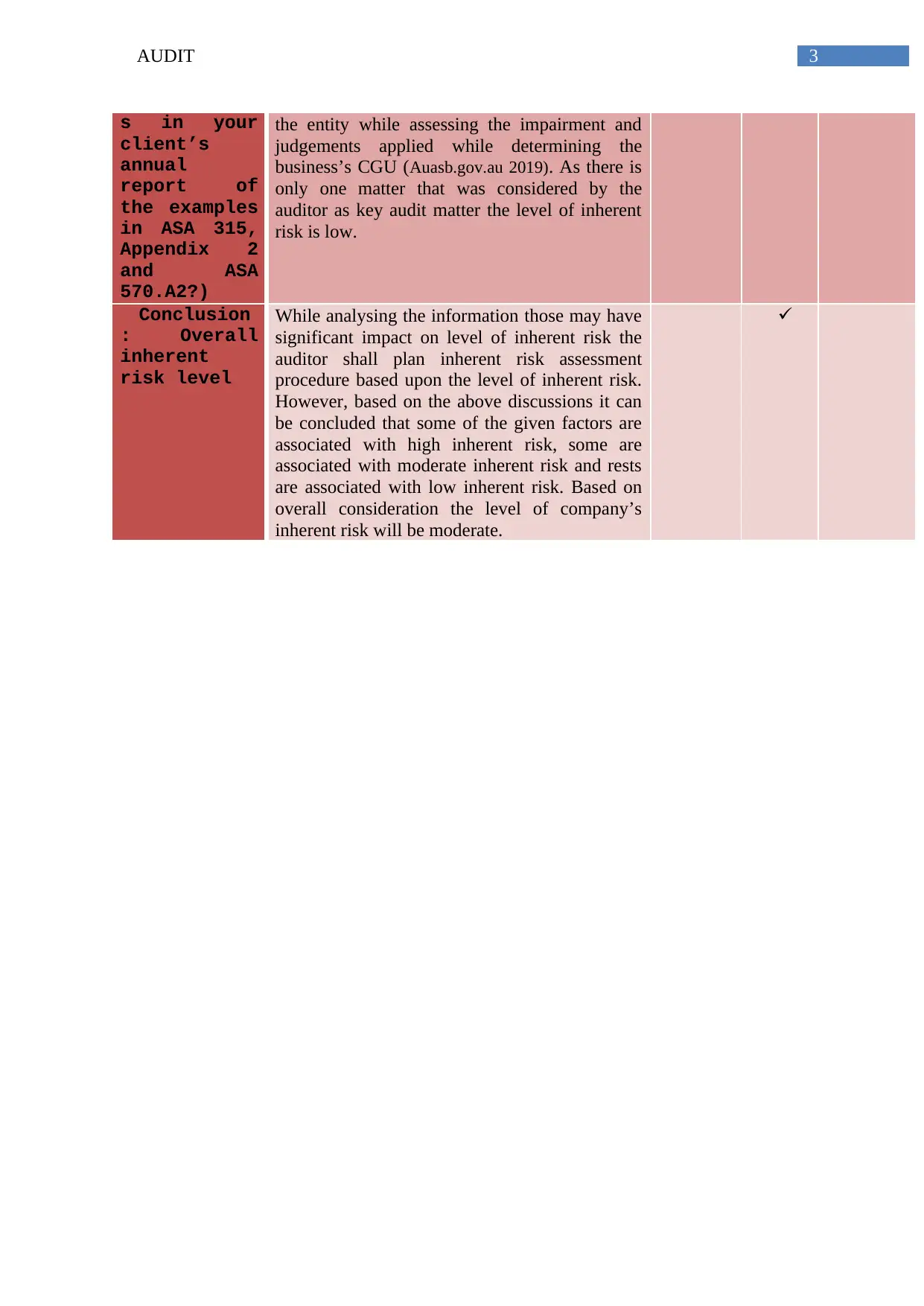

Inherent Risk Assessment of Myer Pty Ltd - Audit Report

VerifiedAdded on 2023/04/22

|5

|1137

|187

Report

AI Summary

This audit report provides an assessment of the inherent risk level for Myer Pty Ltd, a major Australian departmental store group. It considers factors such as the nature of the client's business, results of previous audits, and the distinction between initial and repeat audits. The report discusses the inherent risk associated with the competitive retail sector and potential manipulation of sales figures. It references unqualified opinions from previous audits by PWC and examines non-routine transactions, estimates, judgments, and potential for fraudulent financial reporting. Key audit matters, such as impairment assessments, are also analyzed. The report concludes that the overall inherent risk level for Myer Pty Ltd is moderate, based on a combination of high, moderate, and low-risk factors. The document is contributed by a student and available on Desklib, a platform providing study tools for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.