Management Economics Report: Demand Analysis for Insurance Products

VerifiedAdded on 2023/01/09

|11

|2958

|70

Report

AI Summary

This report delves into the economic analysis of the insurance and legacy solutions market, focusing on the factors that influence demand. It examines the impact of various elements, including the price of substitute goods, consumer income levels, consumer tastes and preferences, consumer expectations regarding future prices, and demographic shifts. The analysis further explores the substitution and income effects on demand, providing a comprehensive understanding of how these economic principles affect the insurance sector. The report highlights the interplay between these factors and their combined effect on the demand curve, offering insights into market dynamics and consumer behavior within the insurance industry. This study provides a detailed overview of the subject, offering a comprehensive understanding of the economics behind insurance and legacy solutions.

MANAGEMENT ECONOMICS – 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.......................................................................................................................................................3

2.......................................................................................................................................................3

3.......................................................................................................................................................5

References........................................................................................................................................6

1.......................................................................................................................................................3

2.......................................................................................................................................................3

3.......................................................................................................................................................5

References........................................................................................................................................6

1.

The selected product is Insurance and legacy solutions; in which clients provided restructuring

and operational consulting services to companies in the insurance industry with legacy business

and other corporate with long-tail or complex liabilities. The reason behind choosing this topic is

some knowledge about investment and the sources about company and the chosen product is

easily available on internet.

2.

All the factors given below affect the demand other than price; hence this will result in shift in

demand curve.

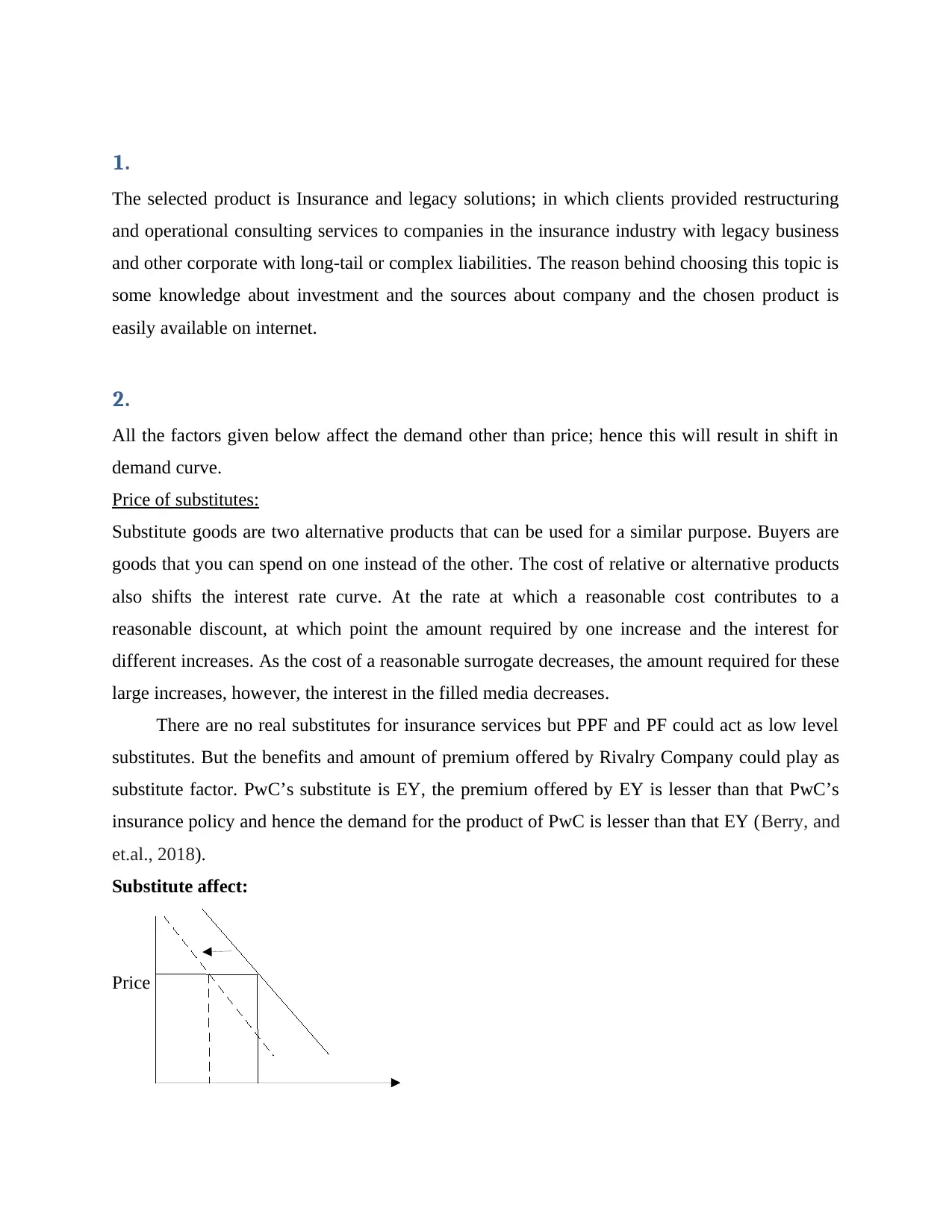

Price of substitutes:

Substitute goods are two alternative products that can be used for a similar purpose. Buyers are

goods that you can spend on one instead of the other. The cost of relative or alternative products

also shifts the interest rate curve. At the rate at which a reasonable cost contributes to a

reasonable discount, at which point the amount required by one increase and the interest for

different increases. As the cost of a reasonable surrogate decreases, the amount required for these

large increases, however, the interest in the filled media decreases.

There are no real substitutes for insurance services but PPF and PF could act as low level

substitutes. But the benefits and amount of premium offered by Rivalry Company could play as

substitute factor. PwC’s substitute is EY, the premium offered by EY is lesser than that PwC’s

insurance policy and hence the demand for the product of PwC is lesser than that EY (Berry, and

et.al., 2018).

Substitute affect:

Price

The selected product is Insurance and legacy solutions; in which clients provided restructuring

and operational consulting services to companies in the insurance industry with legacy business

and other corporate with long-tail or complex liabilities. The reason behind choosing this topic is

some knowledge about investment and the sources about company and the chosen product is

easily available on internet.

2.

All the factors given below affect the demand other than price; hence this will result in shift in

demand curve.

Price of substitutes:

Substitute goods are two alternative products that can be used for a similar purpose. Buyers are

goods that you can spend on one instead of the other. The cost of relative or alternative products

also shifts the interest rate curve. At the rate at which a reasonable cost contributes to a

reasonable discount, at which point the amount required by one increase and the interest for

different increases. As the cost of a reasonable surrogate decreases, the amount required for these

large increases, however, the interest in the filled media decreases.

There are no real substitutes for insurance services but PPF and PF could act as low level

substitutes. But the benefits and amount of premium offered by Rivalry Company could play as

substitute factor. PwC’s substitute is EY, the premium offered by EY is lesser than that PwC’s

insurance policy and hence the demand for the product of PwC is lesser than that EY (Berry, and

et.al., 2018).

Substitute affect:

Price

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quantity

Price of complements:

Complementary goods refer to those products that are consumed together. The combination of

these products is made to meet the needs of the buyer. For instance, ink pens and Ink. If related

results appear, if a large construction cost occurs, at that point a buyer also reduces the interest in

the real bulk, for example an increase in the cost of a large one leads to a fall popularization of

the variant in this case, the curve of interest shifts in one direction.

In fact, it shows a negative cross elasticity of demand and that demand increases when

another massacre costs. In another model it can be said that; If A is an improvement on B, an

extension of cost A will cause a negative improvement on the interest curve of An and cause the

interest curve for B to move inwards; less of any kind to be necessary. In addition, a reduction in

cost A will lead to a positive development in line with the interest curve An and cause the

interest curve B to move outward; a greater amount of each kindness is required. This replaces a

proper surrogate, with demand decreasing as the place value decreases.

Investment plan is a complement for Life insurance. Complement’s price is increasing.

Due to this price of Life insurance service demand has been declined.

Price

Quantity

Consumer income:

Buyers are essential financial elements in an economy. All shoppers consume products and

campaigns directly and through increased performance and convenience. Customers are limited

in payment and must make the most of it (convenience is the need to get a final item). For the

most part, a messenger means a particular person; in any case, the buyers are made up of a

specific person, a group of people, locals and so on.

In case of normal goods, income and demand are directly related or have positive

relationships, which mean that a salary increase will increase demand and a decrease in pay will

Price of complements:

Complementary goods refer to those products that are consumed together. The combination of

these products is made to meet the needs of the buyer. For instance, ink pens and Ink. If related

results appear, if a large construction cost occurs, at that point a buyer also reduces the interest in

the real bulk, for example an increase in the cost of a large one leads to a fall popularization of

the variant in this case, the curve of interest shifts in one direction.

In fact, it shows a negative cross elasticity of demand and that demand increases when

another massacre costs. In another model it can be said that; If A is an improvement on B, an

extension of cost A will cause a negative improvement on the interest curve of An and cause the

interest curve for B to move inwards; less of any kind to be necessary. In addition, a reduction in

cost A will lead to a positive development in line with the interest curve An and cause the

interest curve B to move outward; a greater amount of each kindness is required. This replaces a

proper surrogate, with demand decreasing as the place value decreases.

Investment plan is a complement for Life insurance. Complement’s price is increasing.

Due to this price of Life insurance service demand has been declined.

Price

Quantity

Consumer income:

Buyers are essential financial elements in an economy. All shoppers consume products and

campaigns directly and through increased performance and convenience. Customers are limited

in payment and must make the most of it (convenience is the need to get a final item). For the

most part, a messenger means a particular person; in any case, the buyers are made up of a

specific person, a group of people, locals and so on.

In case of normal goods, income and demand are directly related or have positive

relationships, which mean that a salary increase will increase demand and a decrease in pay will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

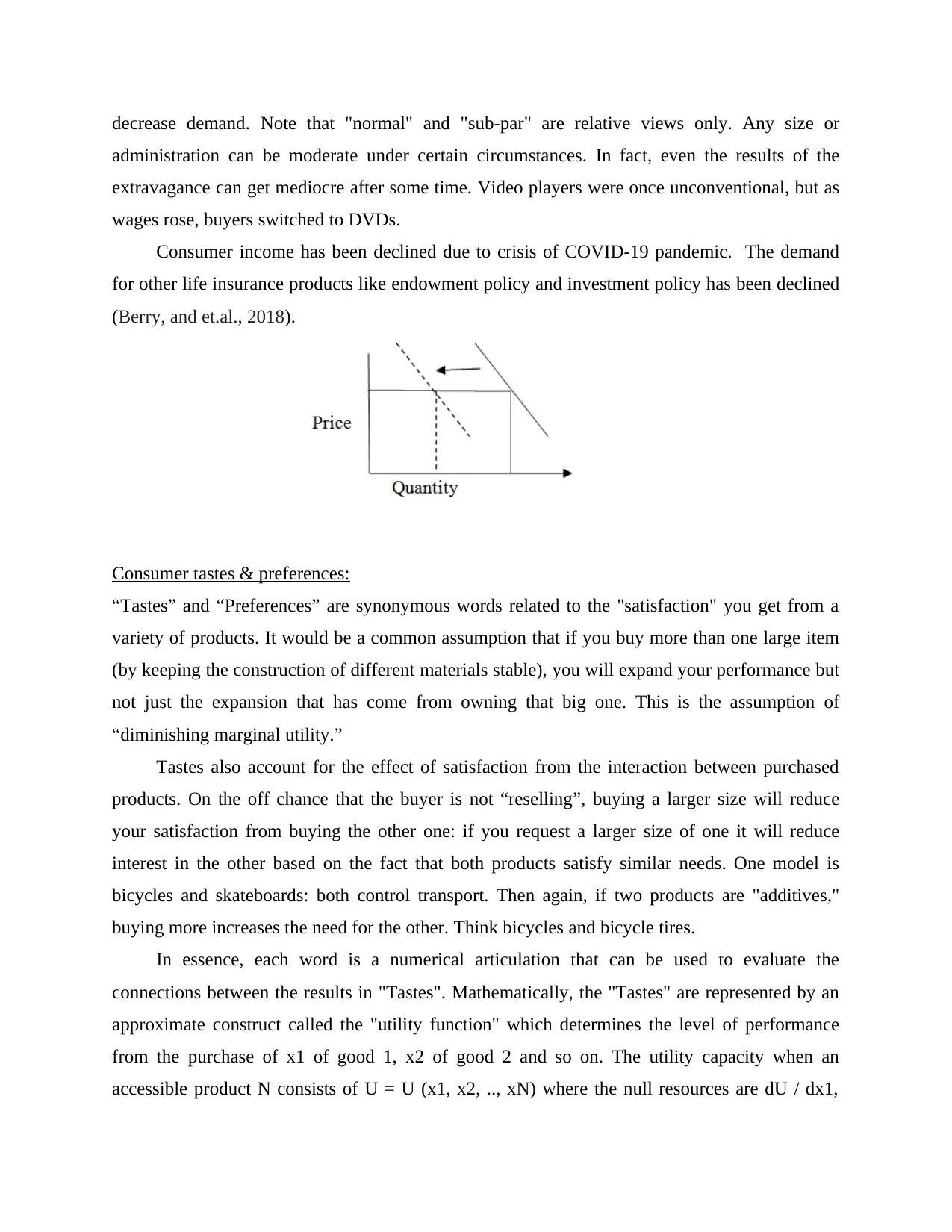

decrease demand. Note that "normal" and "sub-par" are relative views only. Any size or

administration can be moderate under certain circumstances. In fact, even the results of the

extravagance can get mediocre after some time. Video players were once unconventional, but as

wages rose, buyers switched to DVDs.

Consumer income has been declined due to crisis of COVID-19 pandemic. The demand

for other life insurance products like endowment policy and investment policy has been declined

(Berry, and et.al., 2018).

Consumer tastes & preferences:

“Tastes” and “Preferences” are synonymous words related to the "satisfaction" you get from a

variety of products. It would be a common assumption that if you buy more than one large item

(by keeping the construction of different materials stable), you will expand your performance but

not just the expansion that has come from owning that big one. This is the assumption of

“diminishing marginal utility.”

Tastes also account for the effect of satisfaction from the interaction between purchased

products. On the off chance that the buyer is not “reselling”, buying a larger size will reduce

your satisfaction from buying the other one: if you request a larger size of one it will reduce

interest in the other based on the fact that both products satisfy similar needs. One model is

bicycles and skateboards: both control transport. Then again, if two products are "additives,"

buying more increases the need for the other. Think bicycles and bicycle tires.

In essence, each word is a numerical articulation that can be used to evaluate the

connections between the results in "Tastes". Mathematically, the "Tastes" are represented by an

approximate construct called the "utility function" which determines the level of performance

from the purchase of x1 of good 1, x2 of good 2 and so on. The utility capacity when an

accessible product N consists of U = U (x1, x2, .., xN) where the null resources are dU / dx1,

administration can be moderate under certain circumstances. In fact, even the results of the

extravagance can get mediocre after some time. Video players were once unconventional, but as

wages rose, buyers switched to DVDs.

Consumer income has been declined due to crisis of COVID-19 pandemic. The demand

for other life insurance products like endowment policy and investment policy has been declined

(Berry, and et.al., 2018).

Consumer tastes & preferences:

“Tastes” and “Preferences” are synonymous words related to the "satisfaction" you get from a

variety of products. It would be a common assumption that if you buy more than one large item

(by keeping the construction of different materials stable), you will expand your performance but

not just the expansion that has come from owning that big one. This is the assumption of

“diminishing marginal utility.”

Tastes also account for the effect of satisfaction from the interaction between purchased

products. On the off chance that the buyer is not “reselling”, buying a larger size will reduce

your satisfaction from buying the other one: if you request a larger size of one it will reduce

interest in the other based on the fact that both products satisfy similar needs. One model is

bicycles and skateboards: both control transport. Then again, if two products are "additives,"

buying more increases the need for the other. Think bicycles and bicycle tires.

In essence, each word is a numerical articulation that can be used to evaluate the

connections between the results in "Tastes". Mathematically, the "Tastes" are represented by an

approximate construct called the "utility function" which determines the level of performance

from the purchase of x1 of good 1, x2 of good 2 and so on. The utility capacity when an

accessible product N consists of U = U (x1, x2, .., xN) where the null resources are dU / dx1,

dU / dx2,. . ., dU / dxN is generally certain (best of all output), the minimum resource of

reasonable deductions as more is spent (reducing the convenience of margins), and branches are

negative if products I and J are surrogates and positive that they are not additives.

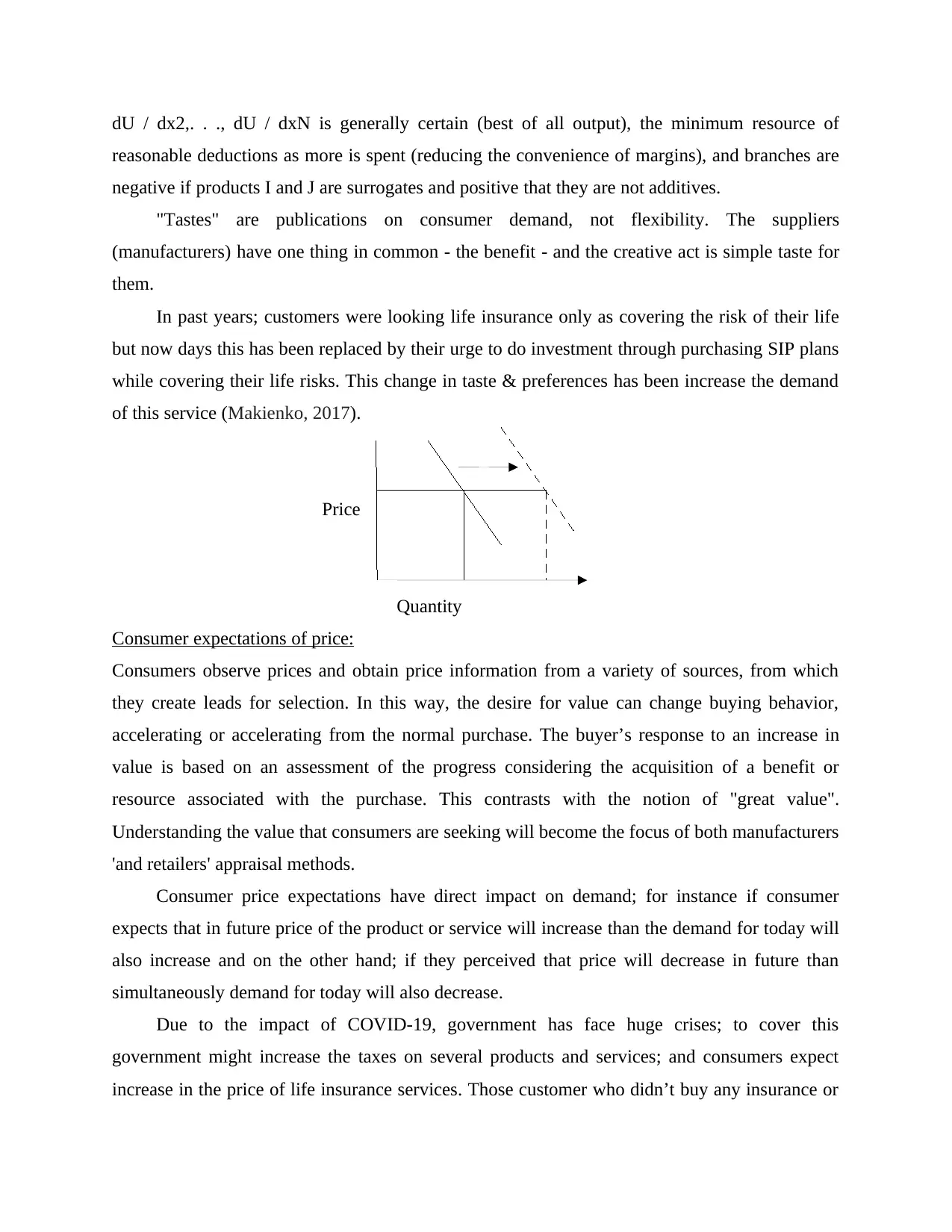

"Tastes" are publications on consumer demand, not flexibility. The suppliers

(manufacturers) have one thing in common - the benefit - and the creative act is simple taste for

them.

In past years; customers were looking life insurance only as covering the risk of their life

but now days this has been replaced by their urge to do investment through purchasing SIP plans

while covering their life risks. This change in taste & preferences has been increase the demand

of this service (Makienko, 2017).

Price

Quantity

Consumer expectations of price:

Consumers observe prices and obtain price information from a variety of sources, from which

they create leads for selection. In this way, the desire for value can change buying behavior,

accelerating or accelerating from the normal purchase. The buyer’s response to an increase in

value is based on an assessment of the progress considering the acquisition of a benefit or

resource associated with the purchase. This contrasts with the notion of "great value".

Understanding the value that consumers are seeking will become the focus of both manufacturers

'and retailers' appraisal methods.

Consumer price expectations have direct impact on demand; for instance if consumer

expects that in future price of the product or service will increase than the demand for today will

also increase and on the other hand; if they perceived that price will decrease in future than

simultaneously demand for today will also decrease.

Due to the impact of COVID-19, government has face huge crises; to cover this

government might increase the taxes on several products and services; and consumers expect

increase in the price of life insurance services. Those customer who didn’t buy any insurance or

reasonable deductions as more is spent (reducing the convenience of margins), and branches are

negative if products I and J are surrogates and positive that they are not additives.

"Tastes" are publications on consumer demand, not flexibility. The suppliers

(manufacturers) have one thing in common - the benefit - and the creative act is simple taste for

them.

In past years; customers were looking life insurance only as covering the risk of their life

but now days this has been replaced by their urge to do investment through purchasing SIP plans

while covering their life risks. This change in taste & preferences has been increase the demand

of this service (Makienko, 2017).

Price

Quantity

Consumer expectations of price:

Consumers observe prices and obtain price information from a variety of sources, from which

they create leads for selection. In this way, the desire for value can change buying behavior,

accelerating or accelerating from the normal purchase. The buyer’s response to an increase in

value is based on an assessment of the progress considering the acquisition of a benefit or

resource associated with the purchase. This contrasts with the notion of "great value".

Understanding the value that consumers are seeking will become the focus of both manufacturers

'and retailers' appraisal methods.

Consumer price expectations have direct impact on demand; for instance if consumer

expects that in future price of the product or service will increase than the demand for today will

also increase and on the other hand; if they perceived that price will decrease in future than

simultaneously demand for today will also decrease.

Due to the impact of COVID-19, government has face huge crises; to cover this

government might increase the taxes on several products and services; and consumers expect

increase in the price of life insurance services. Those customer who didn’t buy any insurance or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

waiting for good policy has start investing in PwC as they expect hike in price of service in

future. Hence, the demand of the product may rise (Makienko, 2017).

Demographics:

It is argued that a small elasticity of a product is characterized by a greater impact of the size of

population on the consumption of such a product. More specific elasticity reduces the impact of

population. The population effect is similarly limited by the standard pay and pay structure. The

remuneration structure influences costs and costs influence flexibility and demand, which affects

utilization. In a market-driven financial framework, the influence of population size on market

demand has a flexible effect, demand and cost. The current market demand reflects the flexible

influence and demand of the past. Normal population size influences future market demand

through flexible costs and flexibility. Population changes are moderate and usage changes are

moderate. The gradual process of progress means that there is a unique opportunity for the

creation and distribution of change to gracefully achieve market strength. Controlling rising costs

and expansion will drive financial development and social sustainability.

Number of buyers for life insurance has been declined; this has negatively affect demand

of insurance services (Makienko, 2017).

future. Hence, the demand of the product may rise (Makienko, 2017).

Demographics:

It is argued that a small elasticity of a product is characterized by a greater impact of the size of

population on the consumption of such a product. More specific elasticity reduces the impact of

population. The population effect is similarly limited by the standard pay and pay structure. The

remuneration structure influences costs and costs influence flexibility and demand, which affects

utilization. In a market-driven financial framework, the influence of population size on market

demand has a flexible effect, demand and cost. The current market demand reflects the flexible

influence and demand of the past. Normal population size influences future market demand

through flexible costs and flexibility. Population changes are moderate and usage changes are

moderate. The gradual process of progress means that there is a unique opportunity for the

creation and distribution of change to gracefully achieve market strength. Controlling rising costs

and expansion will drive financial development and social sustainability.

Number of buyers for life insurance has been declined; this has negatively affect demand

of insurance services (Makienko, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.

Substitution effect:

Substitution effect is the effect of changing the relative value only, by controlling the change in

effective pay. To understand this, we ask which group would make the customer just as happy as

they would have been before the value changed, however with the chance that they would not

have to settle on their own decision towards the new costs. Currently, two slightly different ideas

about the impact of a center have been formed; one with Hicks and Allen and the other with

Slutsky. Both of these resettlement impact ideas are named after their creators. In this way, the

Hicksian substitution effect is called the Hicksian substitution effect and the one created by E.

Slutsky is called the Slutsky Financial Effect.

Both views contradict the rate of magnitude of the change in money income which should

be affected so as to neutralize the change in real income of the consumer resulting from a cost

change. In Hicksian, the change in the value of the renewal effect is exacerbated by such a huge

improvement in cash payments that the buyer is no happier or more apprehensive than before.

Therefore, the buyer’s cash salary is adjusted by an amount that keeps the customer on a similar

postage curve before the cost change. In this way, the effect of Hicksian substitution occurs on a

similar indifference curve.

Life insurance product is necessity for people; as it is compulsory and abounded by the law

to have vehicle insurance compulsory for all citizens. Yes, this indicates that demand is more

inelastic as there is no impact on demand either increasing or decreasing in the price of the

service. People have to insurance policy for their vehicle at any cost (Gimenez-Nadal, 2018).

Price

Quantity

Substitution effect:

Substitution effect is the effect of changing the relative value only, by controlling the change in

effective pay. To understand this, we ask which group would make the customer just as happy as

they would have been before the value changed, however with the chance that they would not

have to settle on their own decision towards the new costs. Currently, two slightly different ideas

about the impact of a center have been formed; one with Hicks and Allen and the other with

Slutsky. Both of these resettlement impact ideas are named after their creators. In this way, the

Hicksian substitution effect is called the Hicksian substitution effect and the one created by E.

Slutsky is called the Slutsky Financial Effect.

Both views contradict the rate of magnitude of the change in money income which should

be affected so as to neutralize the change in real income of the consumer resulting from a cost

change. In Hicksian, the change in the value of the renewal effect is exacerbated by such a huge

improvement in cash payments that the buyer is no happier or more apprehensive than before.

Therefore, the buyer’s cash salary is adjusted by an amount that keeps the customer on a similar

postage curve before the cost change. In this way, the effect of Hicksian substitution occurs on a

similar indifference curve.

Life insurance product is necessity for people; as it is compulsory and abounded by the law

to have vehicle insurance compulsory for all citizens. Yes, this indicates that demand is more

inelastic as there is no impact on demand either increasing or decreasing in the price of the

service. People have to insurance policy for their vehicle at any cost (Gimenez-Nadal, 2018).

Price

Quantity

Income effect:

The income effect is due to changes in real wages. For example, when the cost increases, the

buyer cannot accept the same number of sets that they could have bought before. Unlike the

substitution effect, the effect on revenues can be either positive or negative depending on

whether the object is normal or moderate. With the way we built them, the substitution effect and

the effect on revenues outweigh the overall effect of the change in value, impact of wage

changes on the purchase or exercise of the right. An important feature that is responsible for

changes in deterministic use is the repositioning effect. While the salary effect reflects the

change in the amount purchased by a customer as a result of changes in his payment, the costs

remain stable, the effect of the replacement means a change by receiving an allowance only

following a change in related expenses, and the actual payment remains constant Gimenez-

Nadal, 2018).

At the rate at which a reasonable cost changes, a buyer's actual payment or purchase

intensity changes further. To keep the acquirer's actual salary stable so that the effect is known

only due to a relevant change in value, a change in value is offset by a synchronous change in

payment. For example, when a reasonable cost decreases, tell X, the customer's actual salary

would increase.

To determine the effect of a place, i.e. a change in the amount of X purchased due to the

direct change in the color value, the customer's cash payment must be is indicated by an amount

that balances the addition in the resulting actual payment by cost reduction.

Buying insurance policy gives multiple options to the consumers which are annually, half-

yearly, quarterly and monthly. This premium only costs small amount from consumer’s income.

So, not much effect can be seen on demand and it his more inelastic (Gimenez-Nadal, 2018).

One can also analyze the income and substitution effects by first considering the change in

compensation that is important to move the buyer to the new level of convenience at the basic

costs. This includes the effect of salary. The movement along the new indifference curve from

the intermediate point to the new equilibrium as the slope of the price line changes is then the

substitution effect.

The income effect is due to changes in real wages. For example, when the cost increases, the

buyer cannot accept the same number of sets that they could have bought before. Unlike the

substitution effect, the effect on revenues can be either positive or negative depending on

whether the object is normal or moderate. With the way we built them, the substitution effect and

the effect on revenues outweigh the overall effect of the change in value, impact of wage

changes on the purchase or exercise of the right. An important feature that is responsible for

changes in deterministic use is the repositioning effect. While the salary effect reflects the

change in the amount purchased by a customer as a result of changes in his payment, the costs

remain stable, the effect of the replacement means a change by receiving an allowance only

following a change in related expenses, and the actual payment remains constant Gimenez-

Nadal, 2018).

At the rate at which a reasonable cost changes, a buyer's actual payment or purchase

intensity changes further. To keep the acquirer's actual salary stable so that the effect is known

only due to a relevant change in value, a change in value is offset by a synchronous change in

payment. For example, when a reasonable cost decreases, tell X, the customer's actual salary

would increase.

To determine the effect of a place, i.e. a change in the amount of X purchased due to the

direct change in the color value, the customer's cash payment must be is indicated by an amount

that balances the addition in the resulting actual payment by cost reduction.

Buying insurance policy gives multiple options to the consumers which are annually, half-

yearly, quarterly and monthly. This premium only costs small amount from consumer’s income.

So, not much effect can be seen on demand and it his more inelastic (Gimenez-Nadal, 2018).

One can also analyze the income and substitution effects by first considering the change in

compensation that is important to move the buyer to the new level of convenience at the basic

costs. This includes the effect of salary. The movement along the new indifference curve from

the intermediate point to the new equilibrium as the slope of the price line changes is then the

substitution effect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pricing policy:

Generally, pricing policy refers to how an organization sets the costs of its items and

administrations based on cost, value, demand, and conflict. A valuation approach, therefore,

refers to how an organization uses estimates to achieve its key objectives, for example, offering

lower costs to determine the size of contracts or more significant costs expand to reduce

overload. Despite a certain degree of variation, the evaluation strategy and system are generally

comprehensive and the various arrangements and procedures are largely independent (Baffes,

Kabundi and Nagle, 2020).

A detailed approach to option estimation requires a situation assessor to summarize and

categorize it into a strategic coverage of all key assessment issues. Strategies can and should be

adapted to suit different situations. A conventional approach to contract exercises is equally

unconventional in evaluation.

Most manufacturing companies have an advertising strategy, a consumption strategy, and a

channel strategy. However, the estimation of choice remains a tangle of non-trivial choices. For

many, in any position far above the company, the value strategy has been urgently managed.

This kind of value undermined by disaster managers is the kind of systematic analysis needed for

transparent evaluation methods (Baffes, Kabundi and Nagle, 2020).

Pricing policy must be tailored to the adverse market conditions. We need to know if the

company is going through a flawless or flawed conflict. In an impeccable conflict, the producers

have no influence on the cost. An evaluation strategy has a special meaning just under

incomplete conflict. For the most part, financial managers are reluctant to pay a hefty fee

because this could involve a number of manufacturers in the industry. Overall, companies need

to anticipate the opponent's sector. The estimate should address government support from the

long-regulated body.

As there’s no direct impact on consumer’s demand due to substitution and income effect.

But on the other hand; price offered by Competitor Company named EY affects the demand for

the product or service provided by PwC (Baffes, Kabundi and Nagle, 2020). Hence, our

company has two options follow with; which is either to reduce the price of the service

equivalent to EY’s or providing any add on service with the existing product like customer can

Generally, pricing policy refers to how an organization sets the costs of its items and

administrations based on cost, value, demand, and conflict. A valuation approach, therefore,

refers to how an organization uses estimates to achieve its key objectives, for example, offering

lower costs to determine the size of contracts or more significant costs expand to reduce

overload. Despite a certain degree of variation, the evaluation strategy and system are generally

comprehensive and the various arrangements and procedures are largely independent (Baffes,

Kabundi and Nagle, 2020).

A detailed approach to option estimation requires a situation assessor to summarize and

categorize it into a strategic coverage of all key assessment issues. Strategies can and should be

adapted to suit different situations. A conventional approach to contract exercises is equally

unconventional in evaluation.

Most manufacturing companies have an advertising strategy, a consumption strategy, and a

channel strategy. However, the estimation of choice remains a tangle of non-trivial choices. For

many, in any position far above the company, the value strategy has been urgently managed.

This kind of value undermined by disaster managers is the kind of systematic analysis needed for

transparent evaluation methods (Baffes, Kabundi and Nagle, 2020).

Pricing policy must be tailored to the adverse market conditions. We need to know if the

company is going through a flawless or flawed conflict. In an impeccable conflict, the producers

have no influence on the cost. An evaluation strategy has a special meaning just under

incomplete conflict. For the most part, financial managers are reluctant to pay a hefty fee

because this could involve a number of manufacturers in the industry. Overall, companies need

to anticipate the opponent's sector. The estimate should address government support from the

long-regulated body.

As there’s no direct impact on consumer’s demand due to substitution and income effect.

But on the other hand; price offered by Competitor Company named EY affects the demand for

the product or service provided by PwC (Baffes, Kabundi and Nagle, 2020). Hence, our

company has two options follow with; which is either to reduce the price of the service

equivalent to EY’s or providing any add on service with the existing product like customer can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

claim higher amount compare to EY and get cheaper roaster plan on policy taken for whole

family.

References

Berry, K., Bayham, J., Meyer, S.R. and Fenichel, E.P., 2018. The allocation of time and risk of

Lyme: a case of ecosystem service income and substitution effects. Environmental and

Resource Economics, 70(3), pp.631-650.

Gimenez-Nadal, J.I., 2018. The Substitution Effect from the Profit Function in Consumption.

Baffes, J., Kabundi, A. and Nagle, P., 2020. The role of income and substitution in commodity

demand.

Makienko, I., 2017. Price Elasticity Concept in Pricing and Non-Pricing Contexts: Learning

Activity. Journal for Advancement of Marketing Education, 25.

family.

References

Berry, K., Bayham, J., Meyer, S.R. and Fenichel, E.P., 2018. The allocation of time and risk of

Lyme: a case of ecosystem service income and substitution effects. Environmental and

Resource Economics, 70(3), pp.631-650.

Gimenez-Nadal, J.I., 2018. The Substitution Effect from the Profit Function in Consumption.

Baffes, J., Kabundi, A. and Nagle, P., 2020. The role of income and substitution in commodity

demand.

Makienko, I., 2017. Price Elasticity Concept in Pricing and Non-Pricing Contexts: Learning

Activity. Journal for Advancement of Marketing Education, 25.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.