UGB223 Business Finance: Financial Viability & Investment Appraisal

VerifiedAdded on 2023/06/18

|18

|3908

|473

Report

AI Summary

This report provides a comprehensive analysis of investment appraisal techniques and cash cycle management within the context of business finance. It includes calculations of Net Present Value (NPV) and Internal Rate of Return (IRR) for a proposed project, assessing its financial viability for Braithwaite plc. The report also compares different investment appraisal methods, highlighting their strengths and weaknesses. Furthermore, it examines Ramsworth Ltd.'s liquidity position through the calculation of the average operating cash cycle, current ratio, and acid-test ratio, and discusses the potential cost and risk reductions associated with inventory reduction strategies. The report also evaluates the options available to an investor holding shares in Mainsbury PLC, considering the implications of a rights issue.

UGB223 Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 1....................................................................................................................................3

a) Identification of annual relevant cash flows and Calculation of Net Present value................3

b) Estimation and Calculation of Internal Rate of Return...........................................................4

c) Financial viability of investing in the project..........................................................................5

d) Comparison between different methods of investment appraisal and capital budgeting........5

Question 2....................................................................................................................................7

a) Calculation of average operating cash cycle in days...............................................................7

b) Calculation of current and acid-test ratio................................................................................7

c) Types of risk and cost reduced by the proposal of inventory reduction..................................8

Question 3....................................................................................................................................9

Question 4..................................................................................................................................10

CONCLUDION.............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

Question 1....................................................................................................................................3

a) Identification of annual relevant cash flows and Calculation of Net Present value................3

b) Estimation and Calculation of Internal Rate of Return...........................................................4

c) Financial viability of investing in the project..........................................................................5

d) Comparison between different methods of investment appraisal and capital budgeting........5

Question 2....................................................................................................................................7

a) Calculation of average operating cash cycle in days...............................................................7

b) Calculation of current and acid-test ratio................................................................................7

c) Types of risk and cost reduced by the proposal of inventory reduction..................................8

Question 3....................................................................................................................................9

Question 4..................................................................................................................................10

CONCLUDION.............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION

Business finance means the funds which every company need to acquire from the market

to either use it for expansion or for further investment. This report will discuss the use of cash

operating cycle and also analyse the liquidity position of the Ramsworth Ltd. Further, the report

will also compare and contrast the different methods of investment appraisal. The report will also

calculate the NPV and IRR of the project plan and also the cash operating cycle and various

ratios of the company to make decision.

Question 1

a) Identification of annual relevant cash flows and Calculation of Net Present value

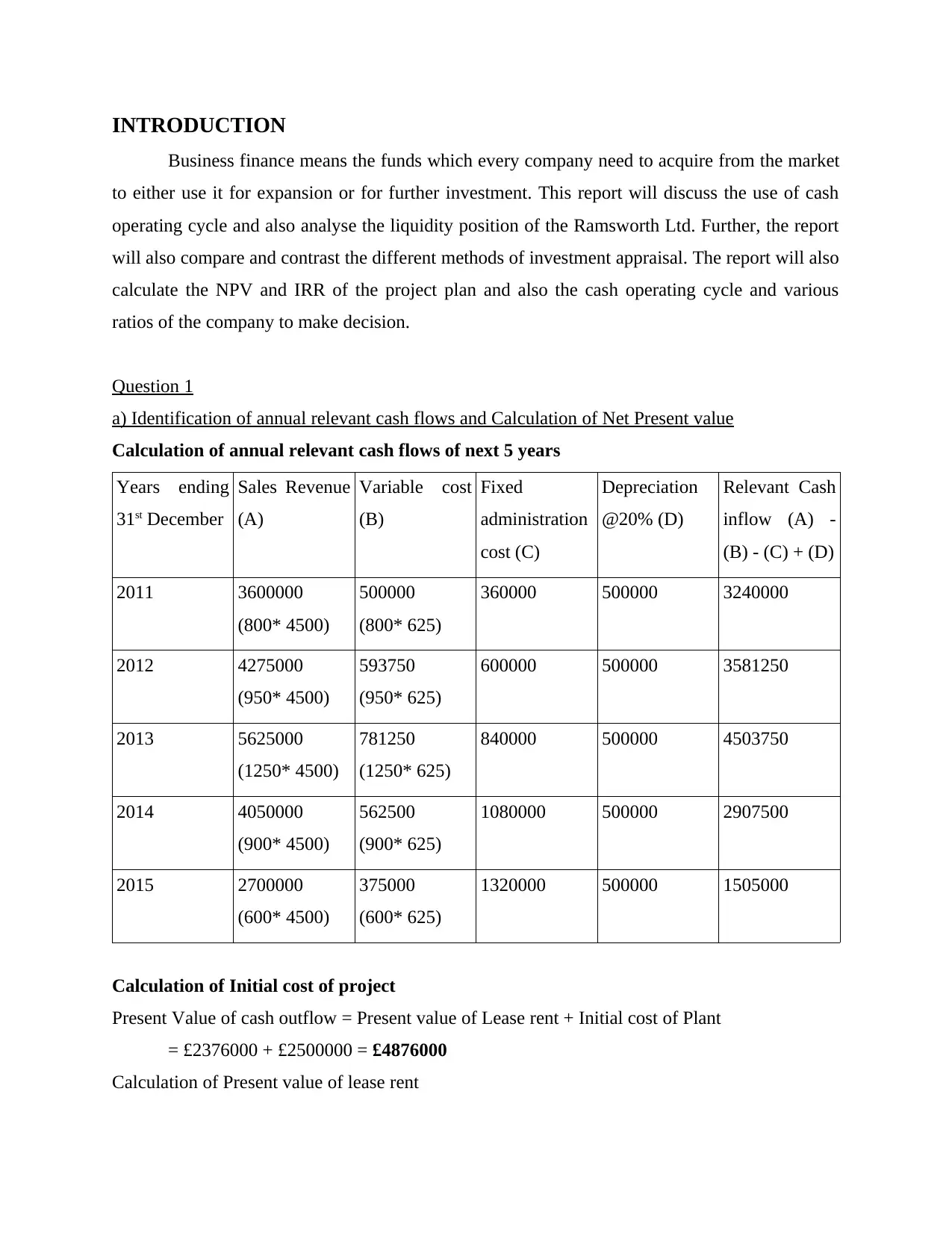

Calculation of annual relevant cash flows of next 5 years

Years ending

31st December

Sales Revenue

(A)

Variable cost

(B)

Fixed

administration

cost (C)

Depreciation

@20% (D)

Relevant Cash

inflow (A) -

(B) - (C) + (D)

2011 3600000

(800* 4500)

500000

(800* 625)

360000 500000 3240000

2012 4275000

(950* 4500)

593750

(950* 625)

600000 500000 3581250

2013 5625000

(1250* 4500)

781250

(1250* 625)

840000 500000 4503750

2014 4050000

(900* 4500)

562500

(900* 625)

1080000 500000 2907500

2015 2700000

(600* 4500)

375000

(600* 625)

1320000 500000 1505000

Calculation of Initial cost of project

Present Value of cash outflow = Present value of Lease rent + Initial cost of Plant

= £2376000 + £2500000 = £4876000

Calculation of Present value of lease rent

Business finance means the funds which every company need to acquire from the market

to either use it for expansion or for further investment. This report will discuss the use of cash

operating cycle and also analyse the liquidity position of the Ramsworth Ltd. Further, the report

will also compare and contrast the different methods of investment appraisal. The report will also

calculate the NPV and IRR of the project plan and also the cash operating cycle and various

ratios of the company to make decision.

Question 1

a) Identification of annual relevant cash flows and Calculation of Net Present value

Calculation of annual relevant cash flows of next 5 years

Years ending

31st December

Sales Revenue

(A)

Variable cost

(B)

Fixed

administration

cost (C)

Depreciation

@20% (D)

Relevant Cash

inflow (A) -

(B) - (C) + (D)

2011 3600000

(800* 4500)

500000

(800* 625)

360000 500000 3240000

2012 4275000

(950* 4500)

593750

(950* 625)

600000 500000 3581250

2013 5625000

(1250* 4500)

781250

(1250* 625)

840000 500000 4503750

2014 4050000

(900* 4500)

562500

(900* 625)

1080000 500000 2907500

2015 2700000

(600* 4500)

375000

(600* 625)

1320000 500000 1505000

Calculation of Initial cost of project

Present Value of cash outflow = Present value of Lease rent + Initial cost of Plant

= £2376000 + £2500000 = £4876000

Calculation of Present value of lease rent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

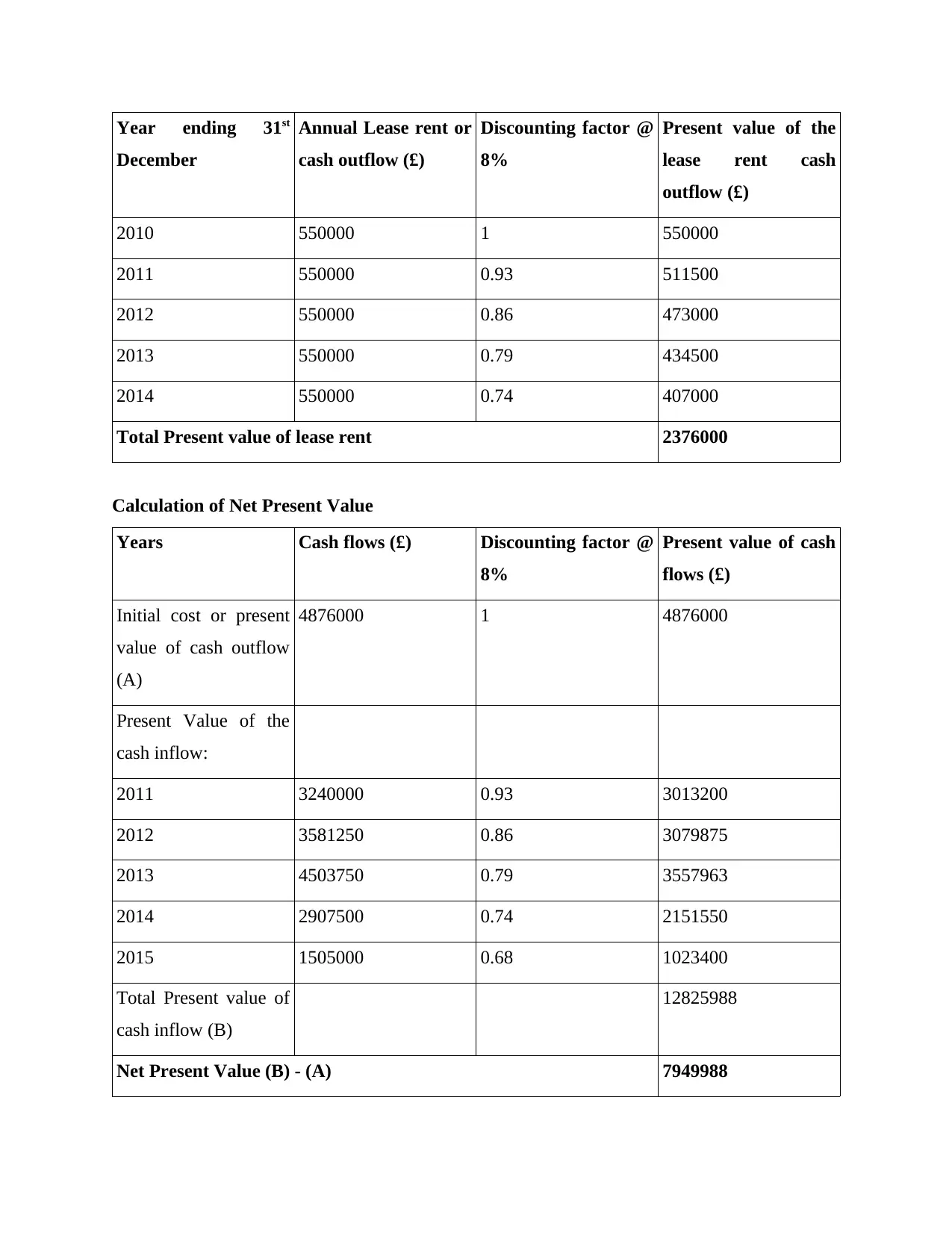

Year ending 31st

December

Annual Lease rent or

cash outflow (£)

Discounting factor @

8%

Present value of the

lease rent cash

outflow (£)

2010 550000 1 550000

2011 550000 0.93 511500

2012 550000 0.86 473000

2013 550000 0.79 434500

2014 550000 0.74 407000

Total Present value of lease rent 2376000

Calculation of Net Present Value

Years Cash flows (£) Discounting factor @

8%

Present value of cash

flows (£)

Initial cost or present

value of cash outflow

(A)

4876000 1 4876000

Present Value of the

cash inflow:

2011 3240000 0.93 3013200

2012 3581250 0.86 3079875

2013 4503750 0.79 3557963

2014 2907500 0.74 2151550

2015 1505000 0.68 1023400

Total Present value of

cash inflow (B)

12825988

Net Present Value (B) - (A) 7949988

December

Annual Lease rent or

cash outflow (£)

Discounting factor @

8%

Present value of the

lease rent cash

outflow (£)

2010 550000 1 550000

2011 550000 0.93 511500

2012 550000 0.86 473000

2013 550000 0.79 434500

2014 550000 0.74 407000

Total Present value of lease rent 2376000

Calculation of Net Present Value

Years Cash flows (£) Discounting factor @

8%

Present value of cash

flows (£)

Initial cost or present

value of cash outflow

(A)

4876000 1 4876000

Present Value of the

cash inflow:

2011 3240000 0.93 3013200

2012 3581250 0.86 3079875

2013 4503750 0.79 3557963

2014 2907500 0.74 2151550

2015 1505000 0.68 1023400

Total Present value of

cash inflow (B)

12825988

Net Present Value (B) - (A) 7949988

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

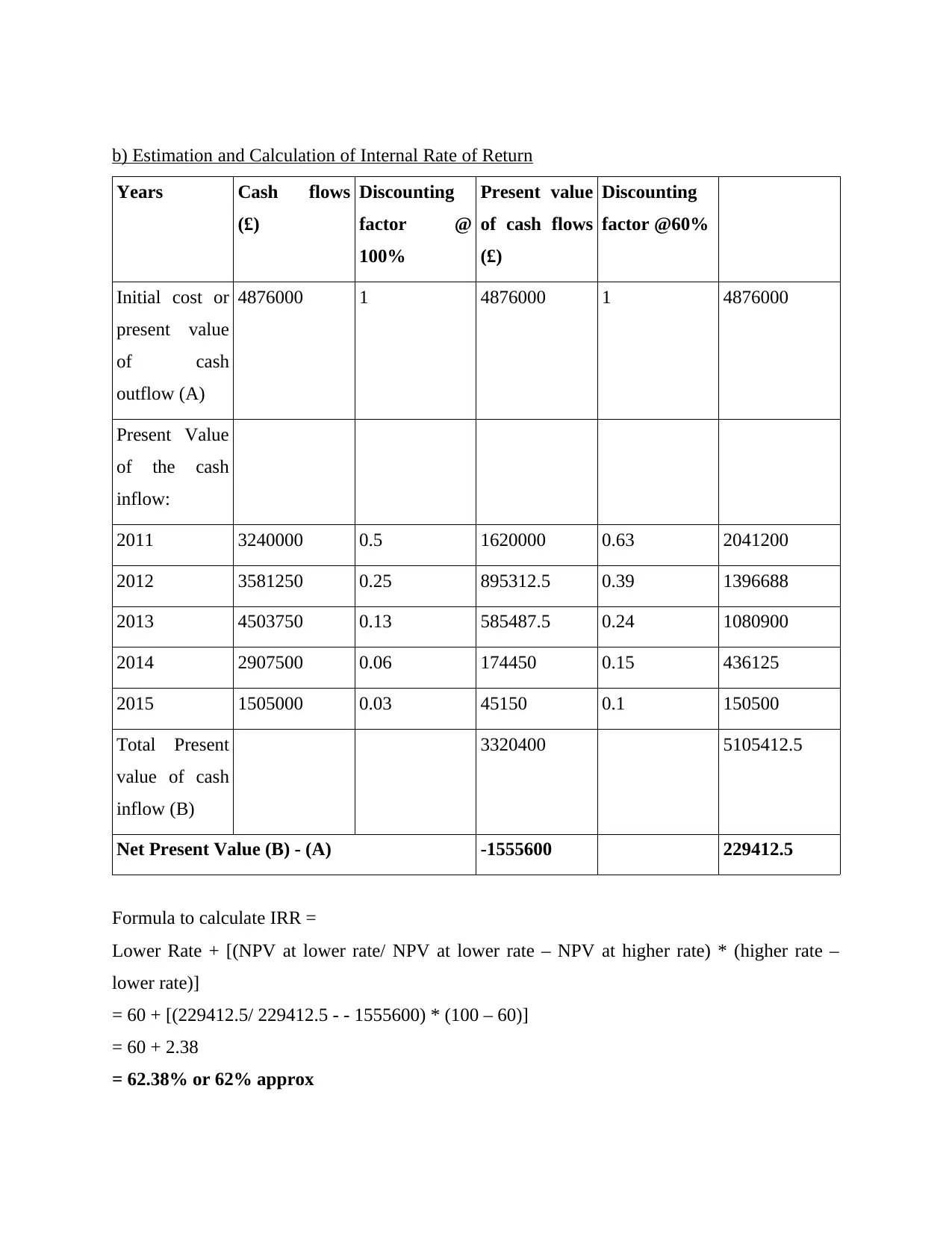

b) Estimation and Calculation of Internal Rate of Return

Years Cash flows

(£)

Discounting

factor @

100%

Present value

of cash flows

(£)

Discounting

factor @60%

Initial cost or

present value

of cash

outflow (A)

4876000 1 4876000 1 4876000

Present Value

of the cash

inflow:

2011 3240000 0.5 1620000 0.63 2041200

2012 3581250 0.25 895312.5 0.39 1396688

2013 4503750 0.13 585487.5 0.24 1080900

2014 2907500 0.06 174450 0.15 436125

2015 1505000 0.03 45150 0.1 150500

Total Present

value of cash

inflow (B)

3320400 5105412.5

Net Present Value (B) - (A) -1555600 229412.5

Formula to calculate IRR =

Lower Rate + [(NPV at lower rate/ NPV at lower rate – NPV at higher rate) * (higher rate –

lower rate)]

= 60 + [(229412.5/ 229412.5 - - 1555600) * (100 – 60)]

= 60 + 2.38

= 62.38% or 62% approx

Years Cash flows

(£)

Discounting

factor @

100%

Present value

of cash flows

(£)

Discounting

factor @60%

Initial cost or

present value

of cash

outflow (A)

4876000 1 4876000 1 4876000

Present Value

of the cash

inflow:

2011 3240000 0.5 1620000 0.63 2041200

2012 3581250 0.25 895312.5 0.39 1396688

2013 4503750 0.13 585487.5 0.24 1080900

2014 2907500 0.06 174450 0.15 436125

2015 1505000 0.03 45150 0.1 150500

Total Present

value of cash

inflow (B)

3320400 5105412.5

Net Present Value (B) - (A) -1555600 229412.5

Formula to calculate IRR =

Lower Rate + [(NPV at lower rate/ NPV at lower rate – NPV at higher rate) * (higher rate –

lower rate)]

= 60 + [(229412.5/ 229412.5 - - 1555600) * (100 – 60)]

= 60 + 2.38

= 62.38% or 62% approx

c) Financial viability of investing in the project

On the basis of above calculation and the result of NPV and IRR, it is clearly

interpretable that the company will get higher return than its cost of capital if they will invest in

the particular project. The 62% of return and positive net present value indicate that this project

is perfectly suitable and profitable for Braithwaite plc. That's why it is advisable to the company

to invest in the particular project.

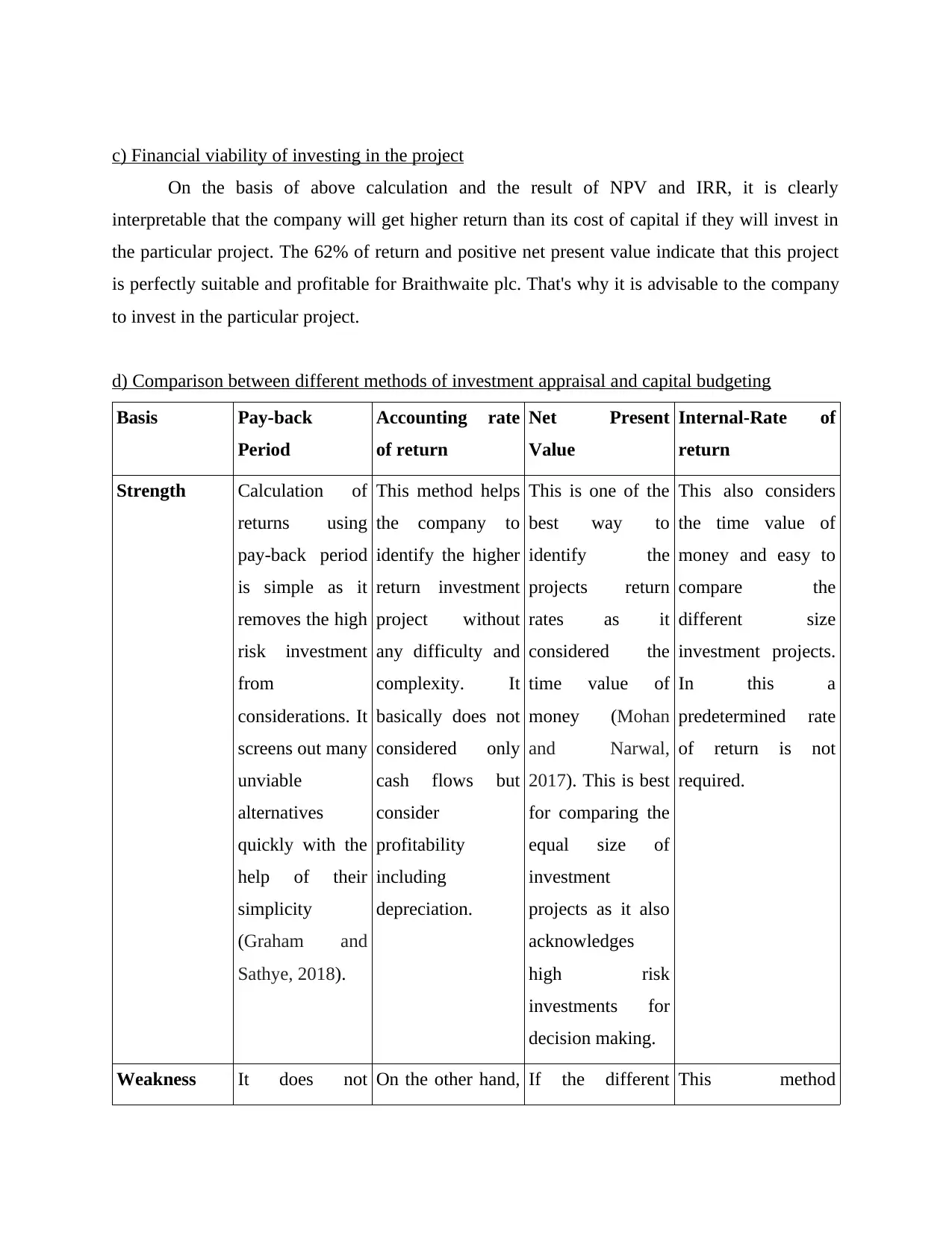

d) Comparison between different methods of investment appraisal and capital budgeting

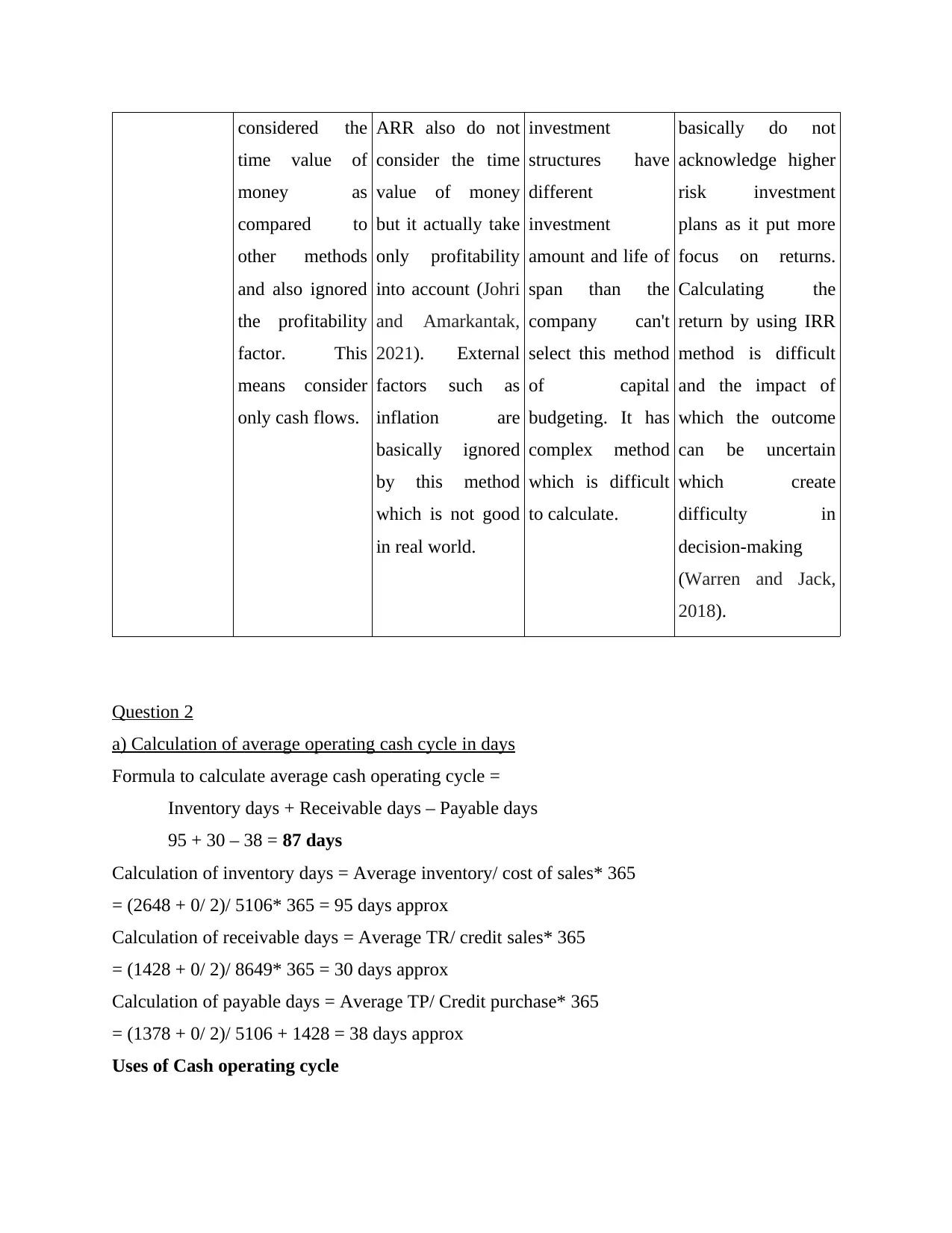

Basis Pay-back

Period

Accounting rate

of return

Net Present

Value

Internal-Rate of

return

Strength Calculation of

returns using

pay-back period

is simple as it

removes the high

risk investment

from

considerations. It

screens out many

unviable

alternatives

quickly with the

help of their

simplicity

(Graham and

Sathye, 2018).

This method helps

the company to

identify the higher

return investment

project without

any difficulty and

complexity. It

basically does not

considered only

cash flows but

consider

profitability

including

depreciation.

This is one of the

best way to

identify the

projects return

rates as it

considered the

time value of

money (Mohan

and Narwal,

2017). This is best

for comparing the

equal size of

investment

projects as it also

acknowledges

high risk

investments for

decision making.

This also considers

the time value of

money and easy to

compare the

different size

investment projects.

In this a

predetermined rate

of return is not

required.

Weakness It does not On the other hand, If the different This method

On the basis of above calculation and the result of NPV and IRR, it is clearly

interpretable that the company will get higher return than its cost of capital if they will invest in

the particular project. The 62% of return and positive net present value indicate that this project

is perfectly suitable and profitable for Braithwaite plc. That's why it is advisable to the company

to invest in the particular project.

d) Comparison between different methods of investment appraisal and capital budgeting

Basis Pay-back

Period

Accounting rate

of return

Net Present

Value

Internal-Rate of

return

Strength Calculation of

returns using

pay-back period

is simple as it

removes the high

risk investment

from

considerations. It

screens out many

unviable

alternatives

quickly with the

help of their

simplicity

(Graham and

Sathye, 2018).

This method helps

the company to

identify the higher

return investment

project without

any difficulty and

complexity. It

basically does not

considered only

cash flows but

consider

profitability

including

depreciation.

This is one of the

best way to

identify the

projects return

rates as it

considered the

time value of

money (Mohan

and Narwal,

2017). This is best

for comparing the

equal size of

investment

projects as it also

acknowledges

high risk

investments for

decision making.

This also considers

the time value of

money and easy to

compare the

different size

investment projects.

In this a

predetermined rate

of return is not

required.

Weakness It does not On the other hand, If the different This method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered the

time value of

money as

compared to

other methods

and also ignored

the profitability

factor. This

means consider

only cash flows.

ARR also do not

consider the time

value of money

but it actually take

only profitability

into account (Johri

and Amarkantak,

2021). External

factors such as

inflation are

basically ignored

by this method

which is not good

in real world.

investment

structures have

different

investment

amount and life of

span than the

company can't

select this method

of capital

budgeting. It has

complex method

which is difficult

to calculate.

basically do not

acknowledge higher

risk investment

plans as it put more

focus on returns.

Calculating the

return by using IRR

method is difficult

and the impact of

which the outcome

can be uncertain

which create

difficulty in

decision-making

(Warren and Jack,

2018).

Question 2

a) Calculation of average operating cash cycle in days

Formula to calculate average cash operating cycle =

Inventory days + Receivable days – Payable days

95 + 30 – 38 = 87 days

Calculation of inventory days = Average inventory/ cost of sales* 365

= (2648 + 0/ 2)/ 5106* 365 = 95 days approx

Calculation of receivable days = Average TR/ credit sales* 365

= (1428 + 0/ 2)/ 8649* 365 = 30 days approx

Calculation of payable days = Average TP/ Credit purchase* 365

= (1378 + 0/ 2)/ 5106 + 1428 = 38 days approx

Uses of Cash operating cycle

time value of

money as

compared to

other methods

and also ignored

the profitability

factor. This

means consider

only cash flows.

ARR also do not

consider the time

value of money

but it actually take

only profitability

into account (Johri

and Amarkantak,

2021). External

factors such as

inflation are

basically ignored

by this method

which is not good

in real world.

investment

structures have

different

investment

amount and life of

span than the

company can't

select this method

of capital

budgeting. It has

complex method

which is difficult

to calculate.

basically do not

acknowledge higher

risk investment

plans as it put more

focus on returns.

Calculating the

return by using IRR

method is difficult

and the impact of

which the outcome

can be uncertain

which create

difficulty in

decision-making

(Warren and Jack,

2018).

Question 2

a) Calculation of average operating cash cycle in days

Formula to calculate average cash operating cycle =

Inventory days + Receivable days – Payable days

95 + 30 – 38 = 87 days

Calculation of inventory days = Average inventory/ cost of sales* 365

= (2648 + 0/ 2)/ 5106* 365 = 95 days approx

Calculation of receivable days = Average TR/ credit sales* 365

= (1428 + 0/ 2)/ 8649* 365 = 30 days approx

Calculation of payable days = Average TP/ Credit purchase* 365

= (1378 + 0/ 2)/ 5106 + 1428 = 38 days approx

Uses of Cash operating cycle

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company could use the cash operating cycle for the management of the business

operations and inventory. This is used by the business for identifying whether the company is

able to generate cash from its inventory or not. That's why Ramsworth Ltd. can use this

techniques to manage its inventory but is not advisable to the company which do not carry stock

in their warehouse.

b) Calculation of current and acid-test ratio

Current ratio = Current assets/ current liabilities

= 4076/ 2933 = 1.39

Acid-test ratio = Current assets – inventory/ current liabilities

= 1428/ 2933 = 0.49

Liquidity position of the company

On the basis of calculation of current and acid-test ratio, it is interpretable that the

liquidity position of the Ramsworth ltd. was poor. It is because the ideal ratio of current and

acid-test ratio define by industry average is 2 and 1 respectively. As the ratio of the company is

below the ideal ratio so it is worked as an evidence that company is not able to pay its short-term

obligations on time.

c) Types of risk and cost reduced by the proposal of inventory reduction

Reducing the level of inventory helps the managers of the Ramsworth Ltd. in further reducing

the various cost and risk attached with the company and that include: Holding cost: The company able to reduce the holding cost of the inventory at the

warehouse which further reduces the overall cost and risk of stock obsolescence of the

company (Nontapot, 2020). Low inventory required less space which further reduce the

rent of the warehouse building. Losses of stock due to spoilage and out-dated is also one

of the most crucial risk that company faces which get eliminated by adopting the proposal

of inventory reduction. Ordering cost: The ordering cost of the stock is determined by the level of inventory

ordered by the company in the whole year. The lower level of inventory reduced the

ordering cost of company and further help them in attaining the economic order quantity

operations and inventory. This is used by the business for identifying whether the company is

able to generate cash from its inventory or not. That's why Ramsworth Ltd. can use this

techniques to manage its inventory but is not advisable to the company which do not carry stock

in their warehouse.

b) Calculation of current and acid-test ratio

Current ratio = Current assets/ current liabilities

= 4076/ 2933 = 1.39

Acid-test ratio = Current assets – inventory/ current liabilities

= 1428/ 2933 = 0.49

Liquidity position of the company

On the basis of calculation of current and acid-test ratio, it is interpretable that the

liquidity position of the Ramsworth ltd. was poor. It is because the ideal ratio of current and

acid-test ratio define by industry average is 2 and 1 respectively. As the ratio of the company is

below the ideal ratio so it is worked as an evidence that company is not able to pay its short-term

obligations on time.

c) Types of risk and cost reduced by the proposal of inventory reduction

Reducing the level of inventory helps the managers of the Ramsworth Ltd. in further reducing

the various cost and risk attached with the company and that include: Holding cost: The company able to reduce the holding cost of the inventory at the

warehouse which further reduces the overall cost and risk of stock obsolescence of the

company (Nontapot, 2020). Low inventory required less space which further reduce the

rent of the warehouse building. Losses of stock due to spoilage and out-dated is also one

of the most crucial risk that company faces which get eliminated by adopting the proposal

of inventory reduction. Ordering cost: The ordering cost of the stock is determined by the level of inventory

ordered by the company in the whole year. The lower level of inventory reduced the

ordering cost of company and further help them in attaining the economic order quantity

level. As it is also helpful for reducing the risk of loss of stock which further reduce the

insurance cost of the company. Labour cost: The lower level of inventory could also help the company's manager in

reducing labour cost which get involve in tracking and verifying inventory. It is because

less labour is required to maintain the warehouse as smaller warehouses are easier to

manage which reduces the safety and security of employees risk of the company. If the

company do not keep large quantity of inventory at their workplace the risk of having the

defect products in closing stock get solved (Shah and Chen, 2021).

Improved Quality: Besides reducing the cost and risk of the company, the inventory

reduction also help the businesses in improving the quality of their products. The risk of

out-dated product is get reduced by this policy and the impact of which company need

not to invest the fund into marketing for selling-off such large quantity of older and

absolute product (Kaushik and et.al., 2019.). The low level of stock helps the company to

remove the risk of poor product quality.

Question 3

A) Theoretical ex right price:

New share issues * market value + Existing share * market value

= 120 (720 / 6) * .2 + 720

= 744

B) Value of a right associated with holding shares

= 720 / .2 * 6 * .13 (.2 * .65)

= 78

c) Evaluation of each of the option with investor

Investor owning a share holding of 10000 number of shares in the company. Currently

the management of the Mainsbury PLC has planned to issue a right share to the shareholders in

the company. In case the investor own the shares it will have to further invest in the company as

the right share will cost a certain value that will be lower than the market value of the shares.

Current the market price is 0.2 whereas, in case of investor looking after to invest further in the

company it would have to put out further capital in the company stock. The advantage investor

would get against investing the capital in the company business is that the share it will own

insurance cost of the company. Labour cost: The lower level of inventory could also help the company's manager in

reducing labour cost which get involve in tracking and verifying inventory. It is because

less labour is required to maintain the warehouse as smaller warehouses are easier to

manage which reduces the safety and security of employees risk of the company. If the

company do not keep large quantity of inventory at their workplace the risk of having the

defect products in closing stock get solved (Shah and Chen, 2021).

Improved Quality: Besides reducing the cost and risk of the company, the inventory

reduction also help the businesses in improving the quality of their products. The risk of

out-dated product is get reduced by this policy and the impact of which company need

not to invest the fund into marketing for selling-off such large quantity of older and

absolute product (Kaushik and et.al., 2019.). The low level of stock helps the company to

remove the risk of poor product quality.

Question 3

A) Theoretical ex right price:

New share issues * market value + Existing share * market value

= 120 (720 / 6) * .2 + 720

= 744

B) Value of a right associated with holding shares

= 720 / .2 * 6 * .13 (.2 * .65)

= 78

c) Evaluation of each of the option with investor

Investor owning a share holding of 10000 number of shares in the company. Currently

the management of the Mainsbury PLC has planned to issue a right share to the shareholders in

the company. In case the investor own the shares it will have to further invest in the company as

the right share will cost a certain value that will be lower than the market value of the shares.

Current the market price is 0.2 whereas, in case of investor looking after to invest further in the

company it would have to put out further capital in the company stock. The advantage investor

would get against investing the capital in the company business is that the share it will own

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

would be allotted less than the market value of the ordinary shares (Octavia, Hakim and Randini,

2021). Right share are like a privilege to the ordinary shareholder of company to own more

number of shares as a result of existing investment company has made in business operations of

organisation. The key advantage investor would hold against investing in the business to own a

share less than the current market value of the shares. The company is performing well as the

company is performing well that could further allow the organisation to maximises the value of

shares. In case the investment is made in the company this would allow the investor to gain

return against the investment made in the organisation. Every year the investor would hold a

return in the form of dividend. This is a safe way to keep holding the respective investment of

the organisation.

On the order hand in case the investor do not look forward to invest in the company

business this would allow the investor to explore other investment choices. This would certainly

empower the investor to have diversification in investment portfolio of business. This is an

important part of the investment decision-making to keep on diversification in the investment.

This is very risky in investment term to keep all investment at one channel. There must be

multiple investment option available with the company that can allow the investor to earn as

many return as possible. This certainly extend the diversity in the investment portfolio of

company. This decision-making would also support the organisation to minimise risk of holding

capital in only one stock (Myšková and Hájek, 2017). There are many instances have been

noticed where the organisation and company go into default due to the failure of business. IN

such a situation investor would lose all its money or capital. IN case the other investment choices

are approached this would allow the investor to safe its capital or finances by keeping funds at

other potential investment choices. On the basis of the entire information it can be evaluated that

investor should look forward to other investing option.

d) Option to raise debt capital

In order to raise the debt capital company can give for public funding option. This choice

would allow the organisation to generate potential financial resources at a very cheapest price

possible. This is an option that involve approaching to the general people to invest in the

business operations of organisation (Sari, Saputra and Siahaan, 2018). This choice is very

affordable in nature as it would allow the organisation to not to have a constant interest burden

over the investment made. Other option like preference shares could al;so been issued. This is an

2021). Right share are like a privilege to the ordinary shareholder of company to own more

number of shares as a result of existing investment company has made in business operations of

organisation. The key advantage investor would hold against investing in the business to own a

share less than the current market value of the shares. The company is performing well as the

company is performing well that could further allow the organisation to maximises the value of

shares. In case the investment is made in the company this would allow the investor to gain

return against the investment made in the organisation. Every year the investor would hold a

return in the form of dividend. This is a safe way to keep holding the respective investment of

the organisation.

On the order hand in case the investor do not look forward to invest in the company

business this would allow the investor to explore other investment choices. This would certainly

empower the investor to have diversification in investment portfolio of business. This is an

important part of the investment decision-making to keep on diversification in the investment.

This is very risky in investment term to keep all investment at one channel. There must be

multiple investment option available with the company that can allow the investor to earn as

many return as possible. This certainly extend the diversity in the investment portfolio of

company. This decision-making would also support the organisation to minimise risk of holding

capital in only one stock (Myšková and Hájek, 2017). There are many instances have been

noticed where the organisation and company go into default due to the failure of business. IN

such a situation investor would lose all its money or capital. IN case the other investment choices

are approached this would allow the investor to safe its capital or finances by keeping funds at

other potential investment choices. On the basis of the entire information it can be evaluated that

investor should look forward to other investing option.

d) Option to raise debt capital

In order to raise the debt capital company can give for public funding option. This choice

would allow the organisation to generate potential financial resources at a very cheapest price

possible. This is an option that involve approaching to the general people to invest in the

business operations of organisation (Sari, Saputra and Siahaan, 2018). This choice is very

affordable in nature as it would allow the organisation to not to have a constant interest burden

over the investment made. Other option like preference shares could al;so been issued. This is an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

affordable way as interest rate that is paid to the shareholder is less than the debt loan. Multiple

debt options can also been approached by the company in order to mitigate the funding

requirements of company.

Question 4

A

1. Return on capital employed

EBIT (Earning before interest and tax) / Capital employed

2019:

3751 / 10062 (14393 – 4331) * 100

= 37.28%

2020:

3453 / 14269 (23115 – 8846) * 100

= 24.19%

2. Return on ordinary shareholder fund

Earning after tax / Shareholder's equity

2019:

2809 / 10062

= .28

2020:

2332 / 11494

= .203

3. Gross profit margin

Gross profit / Sales * 100

2019:

7540 / 17640 * 100

= 43%

2020:

8710 / 25690 * 100

= 34%

4. Operating profit margin

Operating profit / Sales * 100

debt options can also been approached by the company in order to mitigate the funding

requirements of company.

Question 4

A

1. Return on capital employed

EBIT (Earning before interest and tax) / Capital employed

2019:

3751 / 10062 (14393 – 4331) * 100

= 37.28%

2020:

3453 / 14269 (23115 – 8846) * 100

= 24.19%

2. Return on ordinary shareholder fund

Earning after tax / Shareholder's equity

2019:

2809 / 10062

= .28

2020:

2332 / 11494

= .203

3. Gross profit margin

Gross profit / Sales * 100

2019:

7540 / 17640 * 100

= 43%

2020:

8710 / 25690 * 100

= 34%

4. Operating profit margin

Operating profit / Sales * 100

2019:

3751 / 17640 * 100

= 21.26%

2020:

3453 / 25690 * 100

= 13.44%

5. Inventory turnover period

Cost of good sold / Average inventory

2019:

10100 / 1820 (1800 + 1840 / 2)

= 5.6 Times

2020:

16980 /2887 (1840 + 3934 / 2)

= 5.9 Times

6. Trade receivable period

Total net credit sale / Average trade receivable

2019:

17640 / 1008 (1005 + 1011 / 2)

= 17.5

2020:

25690 / 1600.5 (1011 + 2190 / 2)

= 16.05 Times

7. Trade payable period

Account payable / Cost of good sold * 365

2019:

1605 / 10100 * 365

= 58 Days

2020:

3598 / 16980 * 365

= 77 Days

8. Current ratio

3751 / 17640 * 100

= 21.26%

2020:

3453 / 25690 * 100

= 13.44%

5. Inventory turnover period

Cost of good sold / Average inventory

2019:

10100 / 1820 (1800 + 1840 / 2)

= 5.6 Times

2020:

16980 /2887 (1840 + 3934 / 2)

= 5.9 Times

6. Trade receivable period

Total net credit sale / Average trade receivable

2019:

17640 / 1008 (1005 + 1011 / 2)

= 17.5

2020:

25690 / 1600.5 (1011 + 2190 / 2)

= 16.05 Times

7. Trade payable period

Account payable / Cost of good sold * 365

2019:

1605 / 10100 * 365

= 58 Days

2020:

3598 / 16980 * 365

= 77 Days

8. Current ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.