Investment Opportunity Evaluation: A Report for Pinto Limited

VerifiedAdded on 2023/06/12

|6

|1345

|370

Report

AI Summary

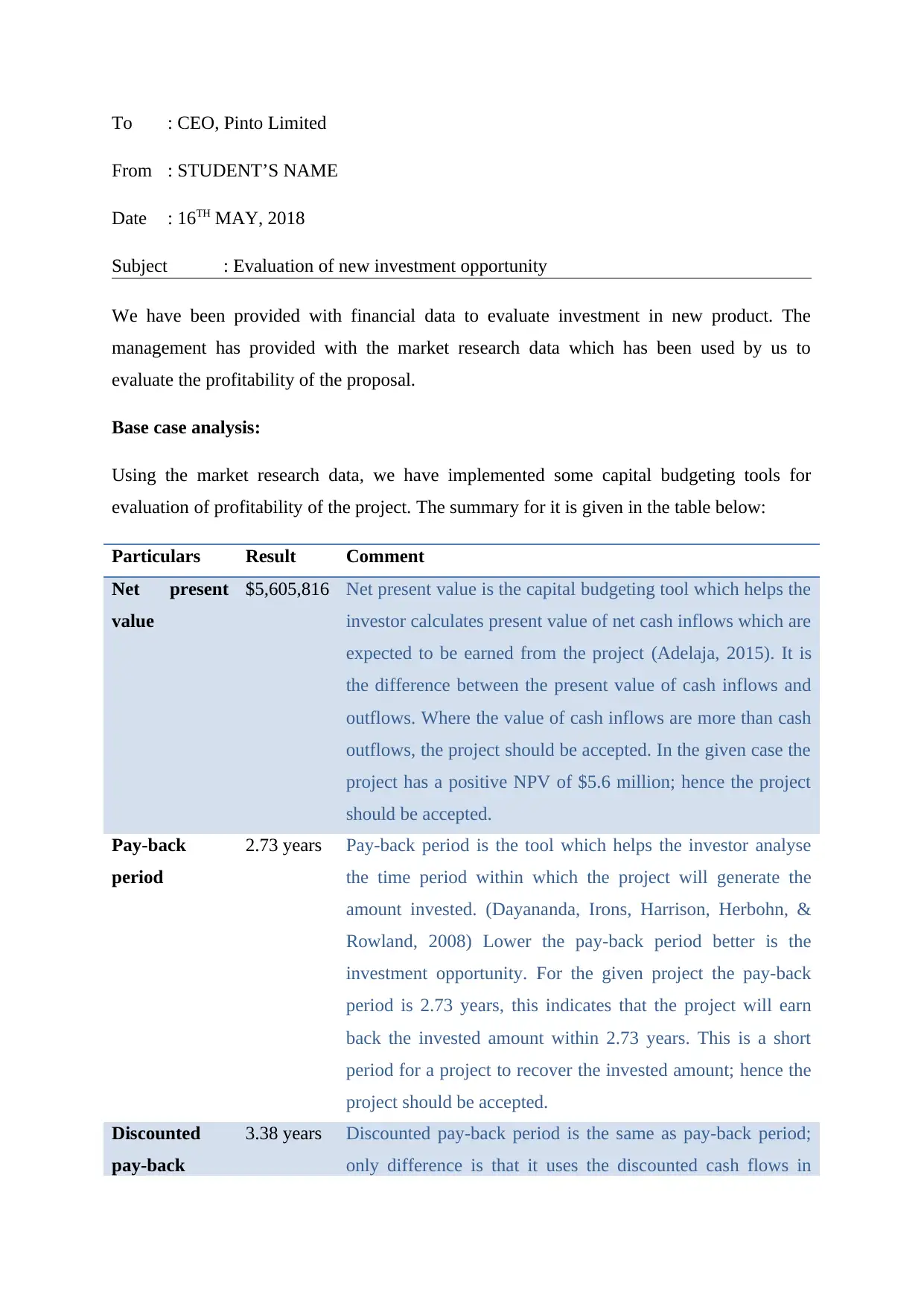

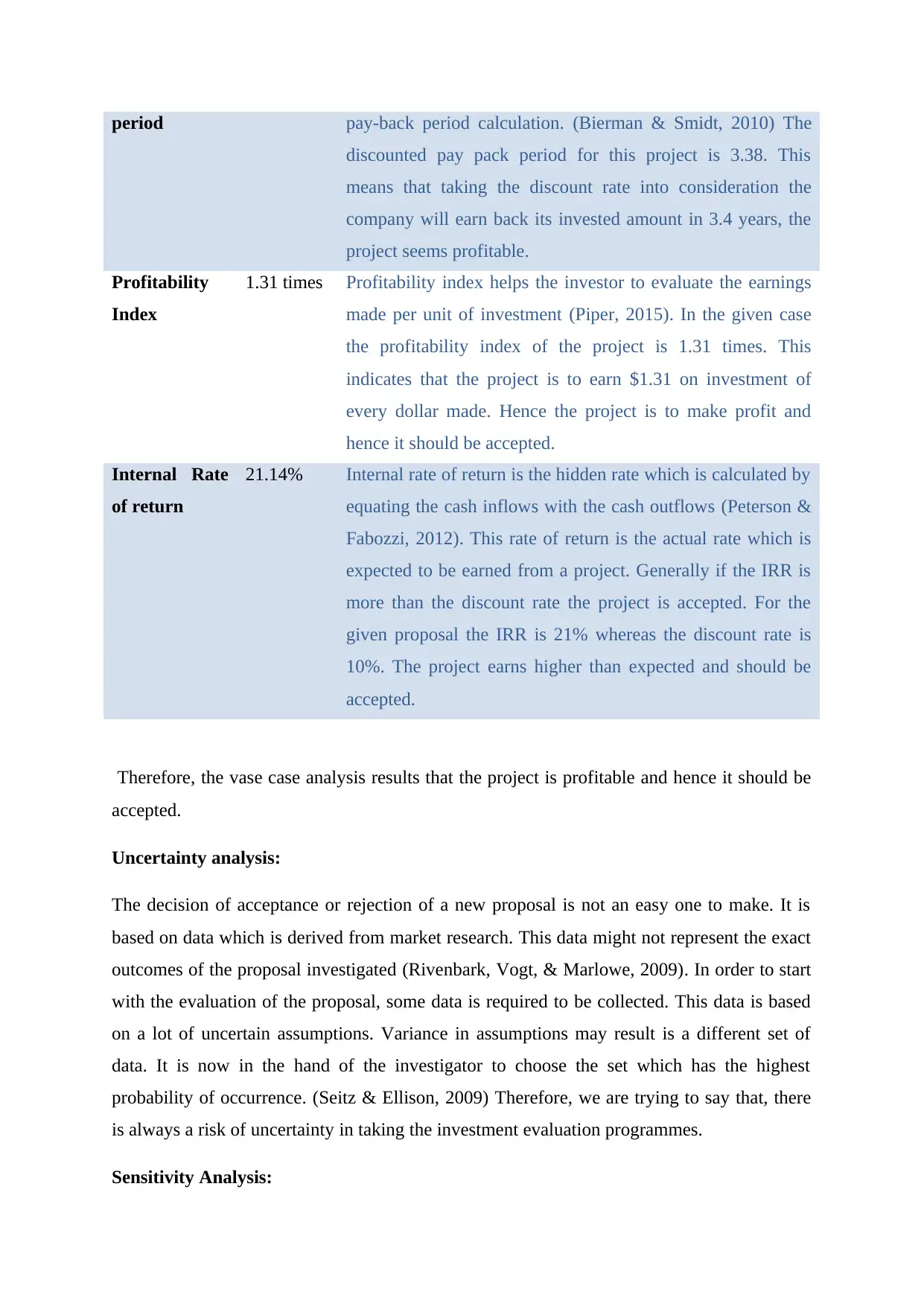

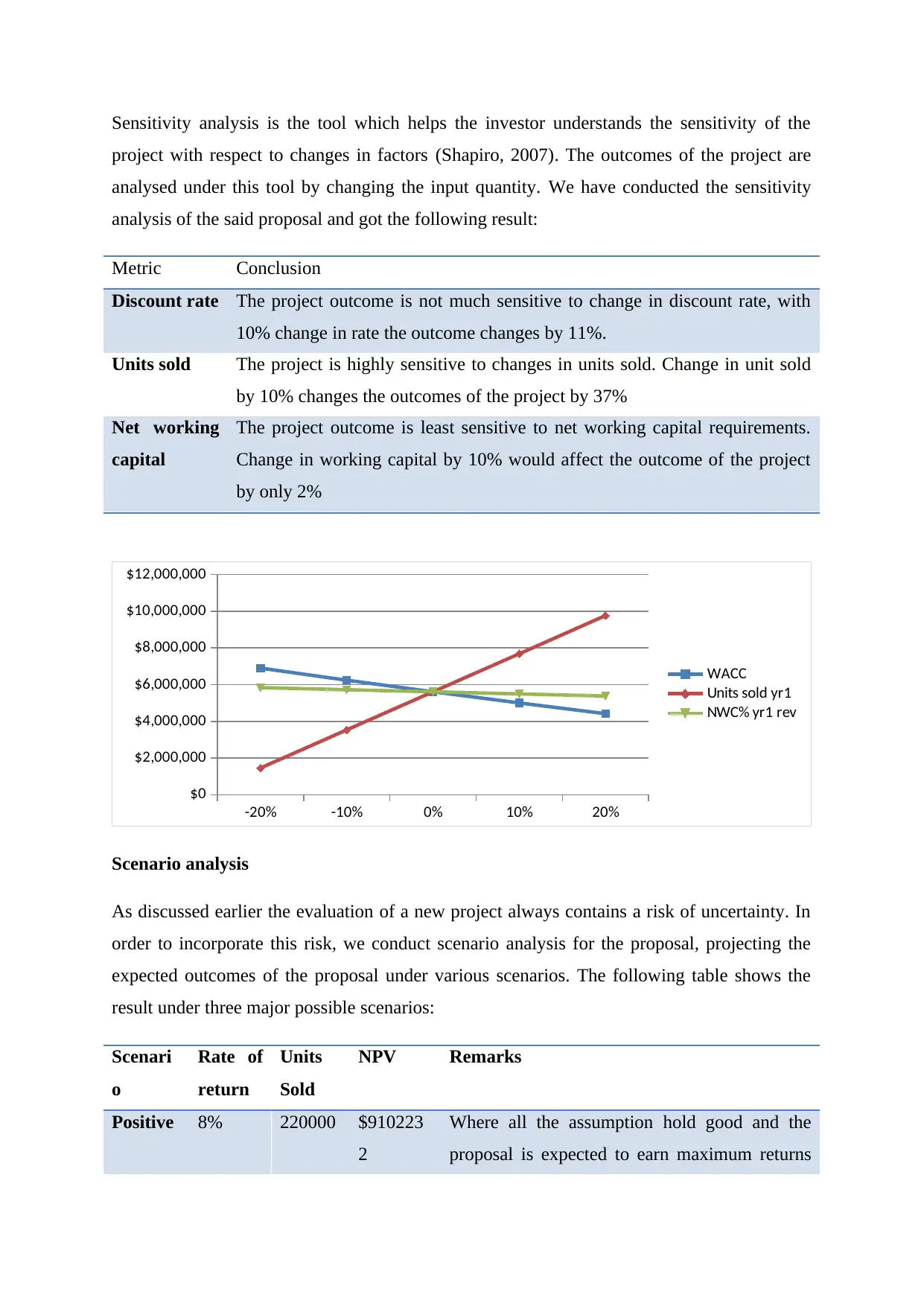

This report presents a comprehensive financial evaluation of a new investment opportunity for Pinto Limited. It employs various capital budgeting tools, including Net Present Value (NPV), Payback Period, Discounted Payback Period, Profitability Index, and Internal Rate of Return (IRR), to assess the project's profitability. The base case analysis indicates a positive NPV of $5.6 million and a payback period of 2.73 years, suggesting the project is financially viable. Uncertainty analysis, including sensitivity and scenario analysis, is conducted to address potential risks. Sensitivity analysis reveals the project's high sensitivity to changes in units sold. Scenario analysis projects outcomes under positive, neutral, and negative scenarios. The report concludes that the project is expected to generate a positive NPV and recommends that Pinto Limited accept the proposal, as it is likely to be profitable.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.