The Impact of Prospect Theory on Finance and Investment Behaviour

VerifiedAdded on 2020/12/09

|14

|3717

|62

Report

AI Summary

This report delves into the realm of investment behavior, utilizing prospect theory as its core framework to analyze how individuals make financial decisions under uncertainty. It begins with an introduction to the concept, highlighting the role of asymmetrical information and the importance of prospect theory in predicting decisions involving risk. The report's aim is to assess the predictive power of prospect theory, specifically examining the impact of loss aversion on individual behavior. The objectives include assessing individual preferences in risky monetary outcomes, evaluating the utility derived from investment strategies, and identifying areas for further research. The literature review explores individual preferences in risky monetary outcomes, the utility derived from money strategies, and areas for better research, drawing upon the works of various scholars. The methodology involves the use of questionnaires and quantitative analysis using SPSS software. The findings and conclusions of the report provide insights into how loss aversion affects investment decisions, with recommendations for improving financial choices. The report also covers concepts like expected utility, heuristics, behavioral bias, and loss aversion in detail. The conclusion summarizes the key findings and provides recommendations for enhancing investment strategies.

FINANCE AND

INVESTMENT BEHAVIOUR

INVESTMENT BEHAVIOUR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Research Aim.........................................................................................................................1

Objectives...............................................................................................................................1

Research Questions................................................................................................................1

CHAPTER 2: LITERATURE REVIEW.........................................................................................2

Q.1 What are individual preferences while assessing options with risky monetary outcomes?.2

Q.2 What is the utility derived by implementing a money strategy or position? ..................5

Q.3 What are the speculations of better research?.................................................................6

CHAPTER 3 METHODOLOGY ...................................................................................................7

CHAPTER 4 FINDINGS.................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Research Aim.........................................................................................................................1

Objectives...............................................................................................................................1

Research Questions................................................................................................................1

CHAPTER 2: LITERATURE REVIEW.........................................................................................2

Q.1 What are individual preferences while assessing options with risky monetary outcomes?.2

Q.2 What is the utility derived by implementing a money strategy or position? ..................5

Q.3 What are the speculations of better research?.................................................................6

CHAPTER 3 METHODOLOGY ...................................................................................................7

CHAPTER 4 FINDINGS.................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Investment behaviour is based on uncertainty about the future and it is thus risky for

individual. Although, presence of asymmetrical information in the investment market plays a

crucial role in decision-making for an individual (Kuhnen, 2015). Prospect theory is a

descriptive cognitive framework widely used for predicting decisions that involve uncertainty

and risk. This report aims to test the prediction power of this theory by analysing effects of loss-

aversion on the same. In addition to this, a critical review of literary works established by prior

scholars has been evidenced in relation to the theory to understand the relevancy of material in

the context of Prospect Theory. Methodology used to derive information regarding the same

includes questionnaire. Additionally, quantitative Methodology is used to analyse the response of

respondents by using SPSS Software. Conclusions and recommendations regarding improving

the investment decisions are also defined in this report.

Research Aim

This report aims to test the prediction power of prospect theory by analysing whether

loss-aversion affects behaviour of an individual or not.

Objectives

The objectives can be centralised as per following fractions:

• Assessing individual preferences in regards to risky monetary outcomes.

• To check the goodness of utility derived by implementing a money strategy or

position.

• To decide the speculations on the theme for better investigation

Research Questions

On the basis of above objectives following questions are derived:

Q.1 What are individual preferences while assessing options with risky monetary outcomes?

Q.2 What is the utility derived by implementing a money strategy or position?

Q.3 What are the speculations of better research?

1

Investment behaviour is based on uncertainty about the future and it is thus risky for

individual. Although, presence of asymmetrical information in the investment market plays a

crucial role in decision-making for an individual (Kuhnen, 2015). Prospect theory is a

descriptive cognitive framework widely used for predicting decisions that involve uncertainty

and risk. This report aims to test the prediction power of this theory by analysing effects of loss-

aversion on the same. In addition to this, a critical review of literary works established by prior

scholars has been evidenced in relation to the theory to understand the relevancy of material in

the context of Prospect Theory. Methodology used to derive information regarding the same

includes questionnaire. Additionally, quantitative Methodology is used to analyse the response of

respondents by using SPSS Software. Conclusions and recommendations regarding improving

the investment decisions are also defined in this report.

Research Aim

This report aims to test the prediction power of prospect theory by analysing whether

loss-aversion affects behaviour of an individual or not.

Objectives

The objectives can be centralised as per following fractions:

• Assessing individual preferences in regards to risky monetary outcomes.

• To check the goodness of utility derived by implementing a money strategy or

position.

• To decide the speculations on the theme for better investigation

Research Questions

On the basis of above objectives following questions are derived:

Q.1 What are individual preferences while assessing options with risky monetary outcomes?

Q.2 What is the utility derived by implementing a money strategy or position?

Q.3 What are the speculations of better research?

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 2: LITERATURE REVIEW

Q.1 What are individual preferences while assessing options with risky monetary outcomes?

As per Scott (2000), under Rational Economic Choice Theory, a rational individual tends

to make informed decisions with an assumption that individual preferences that are complete and

transitive. It is assumed that the rational agent or said individual tends to consider all the relevant

information available, probabilities of events as well as conduct a prospective cost-benefit

analysis to choose the best course of action. This is how the choices are made. Here, rationality is

a widely accepted behaviour that is exhibited by persons while making a choice.

As stated by Lewandowski (2017) in his paper, this theory takes into consideration the

motive of utility maximization as its central piece. Thus, giving rise to the concept of Expected

Utility. This concept helps in setting the standard for the rational economic choice theory in the

context of decision-making involving risk. For many years, the concept of Expected Utility has

proven to be right in its applicability. However there are some violations that people make under

this economic model by taking irrational decisions or actions. Such violations are, to some

extent, accommodated by the introduction of Prospect Theory. The Prospect Theory can be taken

as the alternative model to the Expected Utility Framework, which is not as descriptive as the

latter in terms of decision-making under risks.

As Kao and Velupillai, (2015) explains behavioural economics as an approach that

focuses on the cognitive, emotional as well as psychological patterns of individuals,

organisations and other business entities in relation to the economic decisions made by them. It

vastly contrasts with the rational decision-making behaviour observed among such variables and

their perception towards financial investments. According to Oliver (2014), financial perspective

indicates the mindset of an individual in regards to a certain of products mainly from investment

or speculation point of view. Here, the perspective mainly analyses the cognitive behaviour that

an individual projects while making or adopting investment decisions and strategies. The

arrangement likewise helps in joining the different sort of money related difficulties and

assurance of achievement of business. The aggressive investigation and varieties likewise decide

what forms the part of individual's speculation choice and what does not. An individual tends to

make financial decisions based on past experiences following a set of heuristics. These heuristics

2

Q.1 What are individual preferences while assessing options with risky monetary outcomes?

As per Scott (2000), under Rational Economic Choice Theory, a rational individual tends

to make informed decisions with an assumption that individual preferences that are complete and

transitive. It is assumed that the rational agent or said individual tends to consider all the relevant

information available, probabilities of events as well as conduct a prospective cost-benefit

analysis to choose the best course of action. This is how the choices are made. Here, rationality is

a widely accepted behaviour that is exhibited by persons while making a choice.

As stated by Lewandowski (2017) in his paper, this theory takes into consideration the

motive of utility maximization as its central piece. Thus, giving rise to the concept of Expected

Utility. This concept helps in setting the standard for the rational economic choice theory in the

context of decision-making involving risk. For many years, the concept of Expected Utility has

proven to be right in its applicability. However there are some violations that people make under

this economic model by taking irrational decisions or actions. Such violations are, to some

extent, accommodated by the introduction of Prospect Theory. The Prospect Theory can be taken

as the alternative model to the Expected Utility Framework, which is not as descriptive as the

latter in terms of decision-making under risks.

As Kao and Velupillai, (2015) explains behavioural economics as an approach that

focuses on the cognitive, emotional as well as psychological patterns of individuals,

organisations and other business entities in relation to the economic decisions made by them. It

vastly contrasts with the rational decision-making behaviour observed among such variables and

their perception towards financial investments. According to Oliver (2014), financial perspective

indicates the mindset of an individual in regards to a certain of products mainly from investment

or speculation point of view. Here, the perspective mainly analyses the cognitive behaviour that

an individual projects while making or adopting investment decisions and strategies. The

arrangement likewise helps in joining the different sort of money related difficulties and

assurance of achievement of business. The aggressive investigation and varieties likewise decide

what forms the part of individual's speculation choice and what does not. An individual tends to

make financial decisions based on past experiences following a set of heuristics. These heuristics

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are one of the main deciding factors for the selection of any investment or speculation option

undertaken by the individual.

Thaler and Ganser (2015) explain that heuristics refer to the mental shortcuts that are

adopted by rational beings to form judgements and make decisions based on them. These are

usually based on the past experience, motives and preferences of person involved in carrying out

investment related decisions. Another important factor that is usually observed among

individuals is that of behavioural bias. In the light of irrational choices, the development of

Prospect Theory has become immensely important. The concept of behavioural bias in relation to

finance is effectively explained through this theoretical frameworks which was propounded in

1979 which was further developed in 1992 by Amos Tversky and Daniel Kahneman (1981).

Behavioural bias is the cognitive patterns exhibited by an individual via taking irrational or

erratic decisions. These decisions tend to be highly risky and may cause more damage than

benefit a person. An important component of behavioural bias is loss-aversion. This component

was first discovered by Tversky and Kahneman (1981). As information published in article

Prospect Theory and Loss Aversion (2016), this theory is based on the assumption that losses and

gains have different values and are evaluated differently so that individual makes decisions on

the basis of estimated profits instead of estimated losses. It is also known as “loss-aversion”

theory.

These theories state that while assessing any investment opportunity, an individual tends

to look at their savings, their motive to invest in a certain option, the risk attached to it as well as

the level of risk they are ready to take. An individual knows that investment markets are a risky

business, hence, showing rational behaviour is what is to be expected from them. However, as

Samson (2014) says, past experience or situation of a person may lead to irrational behaviour on

individual's part. The time spent in gathering information and merging factual investigation

according to the proficiency and assessment also plays an important role to determine loss-

aversion.

As pointed out by Kothiyal, Spinu and Wakker (2014), another important concept given

by this theory is that the individuals are risk averse in terms of gains whereas they are seeking in

terms of losses. This statement is also evident in the case presented by Wang, Rieger and Hens

(2017) that assert psychology influences an agent to magnify losses and reduce gains.

3

undertaken by the individual.

Thaler and Ganser (2015) explain that heuristics refer to the mental shortcuts that are

adopted by rational beings to form judgements and make decisions based on them. These are

usually based on the past experience, motives and preferences of person involved in carrying out

investment related decisions. Another important factor that is usually observed among

individuals is that of behavioural bias. In the light of irrational choices, the development of

Prospect Theory has become immensely important. The concept of behavioural bias in relation to

finance is effectively explained through this theoretical frameworks which was propounded in

1979 which was further developed in 1992 by Amos Tversky and Daniel Kahneman (1981).

Behavioural bias is the cognitive patterns exhibited by an individual via taking irrational or

erratic decisions. These decisions tend to be highly risky and may cause more damage than

benefit a person. An important component of behavioural bias is loss-aversion. This component

was first discovered by Tversky and Kahneman (1981). As information published in article

Prospect Theory and Loss Aversion (2016), this theory is based on the assumption that losses and

gains have different values and are evaluated differently so that individual makes decisions on

the basis of estimated profits instead of estimated losses. It is also known as “loss-aversion”

theory.

These theories state that while assessing any investment opportunity, an individual tends

to look at their savings, their motive to invest in a certain option, the risk attached to it as well as

the level of risk they are ready to take. An individual knows that investment markets are a risky

business, hence, showing rational behaviour is what is to be expected from them. However, as

Samson (2014) says, past experience or situation of a person may lead to irrational behaviour on

individual's part. The time spent in gathering information and merging factual investigation

according to the proficiency and assessment also plays an important role to determine loss-

aversion.

As pointed out by Kothiyal, Spinu and Wakker (2014), another important concept given

by this theory is that the individuals are risk averse in terms of gains whereas they are seeking in

terms of losses. This statement is also evident in the case presented by Wang, Rieger and Hens

(2017) that assert psychology influences an agent to magnify losses and reduce gains.

3

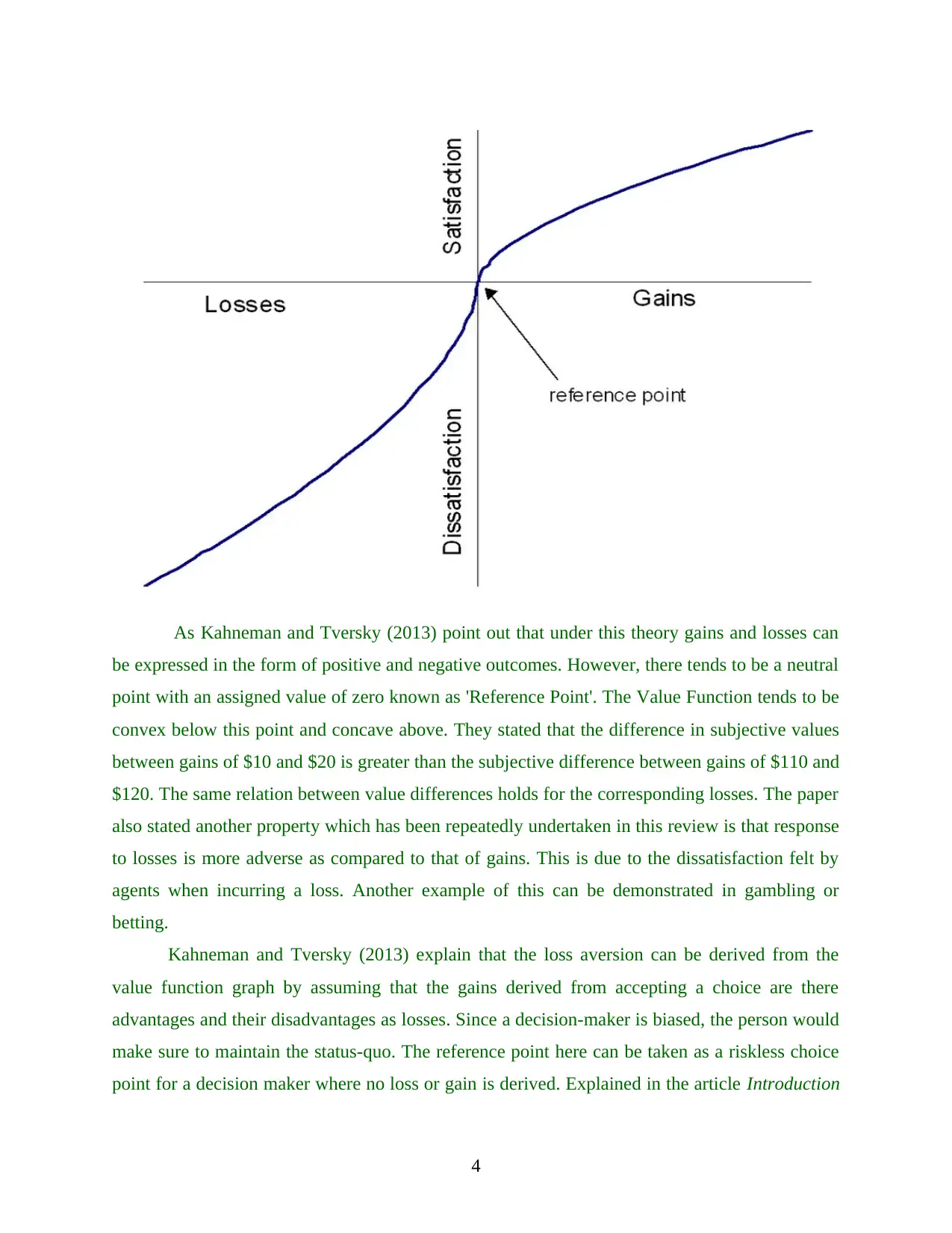

As Kahneman and Tversky (2013) point out that under this theory gains and losses can

be expressed in the form of positive and negative outcomes. However, there tends to be a neutral

point with an assigned value of zero known as 'Reference Point'. The Value Function tends to be

convex below this point and concave above. They stated that the difference in subjective values

between gains of $10 and $20 is greater than the subjective difference between gains of $110 and

$120. The same relation between value differences holds for the corresponding losses. The paper

also stated another property which has been repeatedly undertaken in this review is that response

to losses is more adverse as compared to that of gains. This is due to the dissatisfaction felt by

agents when incurring a loss. Another example of this can be demonstrated in gambling or

betting.

Kahneman and Tversky (2013) explain that the loss aversion can be derived from the

value function graph by assuming that the gains derived from accepting a choice are there

advantages and their disadvantages as losses. Since a decision-maker is biased, the person would

make sure to maintain the status-quo. The reference point here can be taken as a riskless choice

point for a decision maker where no loss or gain is derived. Explained in the article Introduction

4

be expressed in the form of positive and negative outcomes. However, there tends to be a neutral

point with an assigned value of zero known as 'Reference Point'. The Value Function tends to be

convex below this point and concave above. They stated that the difference in subjective values

between gains of $10 and $20 is greater than the subjective difference between gains of $110 and

$120. The same relation between value differences holds for the corresponding losses. The paper

also stated another property which has been repeatedly undertaken in this review is that response

to losses is more adverse as compared to that of gains. This is due to the dissatisfaction felt by

agents when incurring a loss. Another example of this can be demonstrated in gambling or

betting.

Kahneman and Tversky (2013) explain that the loss aversion can be derived from the

value function graph by assuming that the gains derived from accepting a choice are there

advantages and their disadvantages as losses. Since a decision-maker is biased, the person would

make sure to maintain the status-quo. The reference point here can be taken as a riskless choice

point for a decision maker where no loss or gain is derived. Explained in the article Introduction

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to Prospect Theory by John Miyamoto (2017), it is noteworthy that the risk aversion and risk

seeking frames apply to gains and losses but not the states of wealth. Hence, when the utility

function is highly concave it indicates the risk averse tendency of the decision-maker while c

This is a repetitive and repetitive process that is executed until the threat of loss equals any

incurred gains. Instances of such patterns can be found through endowment effect and sunk cost

fallacy.

Chang (2019) states that endowment effect is a bias which asserts that individuals tend to

prioritise those goods or financial products that owned by them rather than ones that are identical

or not owned by them altogether .According to Frame and White (2014), Sunk Cost Fallacy bias

is a result of an ongoing commitment which is difficult to be abandoned. This factor examines

the imbalances made in minds of individual about losses and gains. Hammond, Keeney and

Raiffa (2015) assert that the more urgent a person is to avoid threats in regards to an investment

decision, the more likely they are to be motivated to make cautious decisions ensuring gains.

Hence, loss-aversion is an important factor that analyses pay-off between potential gains and

losses.

Q.2 What is the utility derived by implementing a money strategy or position?

An investment strategy adopted by the individual is of no use if they are not able to

derive gains more than the risk undertaken by them. In general, the models mainly helps in

creating the effective analysis and control with managing the proper information of cash flow

information. Loss aversion also analyses the theoretical and political evaluation and control with

different different opportunities for various labels. It also helps in determination of the flexibility

in overcomes by looking at considerable changes. The utility here is measured in the terms of

gains incurred and losses avoided or averted by making a financial decision.

Here, Prospect theory will apply, when an individual has two alternatives, one which are

equal, and other one being presented in terms of prospective gains and possible losses. As

explained by John Miyamoto (2017) in the previous research question, value function can help

determine the situation of loss aversion when the gains are treated as advantages. Here, the

reflection effect is treated as the concluding inference or result under which circumstance, there

is high preference given to to switching from risk averse to risk seeking, especially when the

losses and gains are deemed to be dynamic or easily changeable. Then it is obvious that first

option will be chosen. The main intention behind formation of this theory is that, the above-

5

seeking frames apply to gains and losses but not the states of wealth. Hence, when the utility

function is highly concave it indicates the risk averse tendency of the decision-maker while c

This is a repetitive and repetitive process that is executed until the threat of loss equals any

incurred gains. Instances of such patterns can be found through endowment effect and sunk cost

fallacy.

Chang (2019) states that endowment effect is a bias which asserts that individuals tend to

prioritise those goods or financial products that owned by them rather than ones that are identical

or not owned by them altogether .According to Frame and White (2014), Sunk Cost Fallacy bias

is a result of an ongoing commitment which is difficult to be abandoned. This factor examines

the imbalances made in minds of individual about losses and gains. Hammond, Keeney and

Raiffa (2015) assert that the more urgent a person is to avoid threats in regards to an investment

decision, the more likely they are to be motivated to make cautious decisions ensuring gains.

Hence, loss-aversion is an important factor that analyses pay-off between potential gains and

losses.

Q.2 What is the utility derived by implementing a money strategy or position?

An investment strategy adopted by the individual is of no use if they are not able to

derive gains more than the risk undertaken by them. In general, the models mainly helps in

creating the effective analysis and control with managing the proper information of cash flow

information. Loss aversion also analyses the theoretical and political evaluation and control with

different different opportunities for various labels. It also helps in determination of the flexibility

in overcomes by looking at considerable changes. The utility here is measured in the terms of

gains incurred and losses avoided or averted by making a financial decision.

Here, Prospect theory will apply, when an individual has two alternatives, one which are

equal, and other one being presented in terms of prospective gains and possible losses. As

explained by John Miyamoto (2017) in the previous research question, value function can help

determine the situation of loss aversion when the gains are treated as advantages. Here, the

reflection effect is treated as the concluding inference or result under which circumstance, there

is high preference given to to switching from risk averse to risk seeking, especially when the

losses and gains are deemed to be dynamic or easily changeable. Then it is obvious that first

option will be chosen. The main intention behind formation of this theory is that, the above-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

mentioned economists wanted how a person can take accurate decisions by comparing it with the

expected return. Furthermore, they tried to explain that, individual choices are independent and

the decision are made on the fact that a gain is generally assumed to be higher. The another

motive behind this theory is that an individual feel emotionally impacted when he suffers loss

instead of gains, therefore he should choose the one giving more return.

Q.3 What are the speculations of better research?

Prospect theory hails from behavioural economic subgroup, that describes how an investor

make his choice between the alternatives with possible risks and there is probability of different

outcomes that are completely unknown to the investor. According to Shiller, (2012), Loss

aversion is imagined that the torment of losing is mentally about twi9.7ce as incredible as the joy

of picking up. As individuals are all the more ready to dodge a misfortune, repugnance from such

situations can clarify contrasts in hazard looking for versus revolution. The concept behind this is

mainly associated with analysing the amount to be paid and expected to attain by people that

wants to attain behaviour of change. Clemen and Reilly (2013) cited that Loss aversion is an

imperative idea related with prospect hypothesis and is embodied in the articulation "Loss

aversion increasingly pose a threat than additions". Loss aversion is one of the main reason that

defies economic rational behavioural model exhibited by the individual. In order to safeguard

their finance, an investor may speculate or participate in short-term investment decision-making

resulting in adoption of more risky investments.

6

expected return. Furthermore, they tried to explain that, individual choices are independent and

the decision are made on the fact that a gain is generally assumed to be higher. The another

motive behind this theory is that an individual feel emotionally impacted when he suffers loss

instead of gains, therefore he should choose the one giving more return.

Q.3 What are the speculations of better research?

Prospect theory hails from behavioural economic subgroup, that describes how an investor

make his choice between the alternatives with possible risks and there is probability of different

outcomes that are completely unknown to the investor. According to Shiller, (2012), Loss

aversion is imagined that the torment of losing is mentally about twi9.7ce as incredible as the joy

of picking up. As individuals are all the more ready to dodge a misfortune, repugnance from such

situations can clarify contrasts in hazard looking for versus revolution. The concept behind this is

mainly associated with analysing the amount to be paid and expected to attain by people that

wants to attain behaviour of change. Clemen and Reilly (2013) cited that Loss aversion is an

imperative idea related with prospect hypothesis and is embodied in the articulation "Loss

aversion increasingly pose a threat than additions". Loss aversion is one of the main reason that

defies economic rational behavioural model exhibited by the individual. In order to safeguard

their finance, an investor may speculate or participate in short-term investment decision-making

resulting in adoption of more risky investments.

6

CHAPTER 3 METHODOLOGY

Research methodology are the specific methods and tools employed to identify, select and

analyse authenticity of research within a proper time limit. The use of quantitative methodology

is mainly used to analyse the data and responses received form respondents. For the purpose of

successfully answering research questions formed above, questionnaire has been developed to

collect relevant data and necessary analysis has been undertaken through SPSS. The

questionnaire is as follows:

7

Research methodology are the specific methods and tools employed to identify, select and

analyse authenticity of research within a proper time limit. The use of quantitative methodology

is mainly used to analyse the data and responses received form respondents. For the purpose of

successfully answering research questions formed above, questionnaire has been developed to

collect relevant data and necessary analysis has been undertaken through SPSS. The

questionnaire is as follows:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CHAPTER 4 FINDINGS

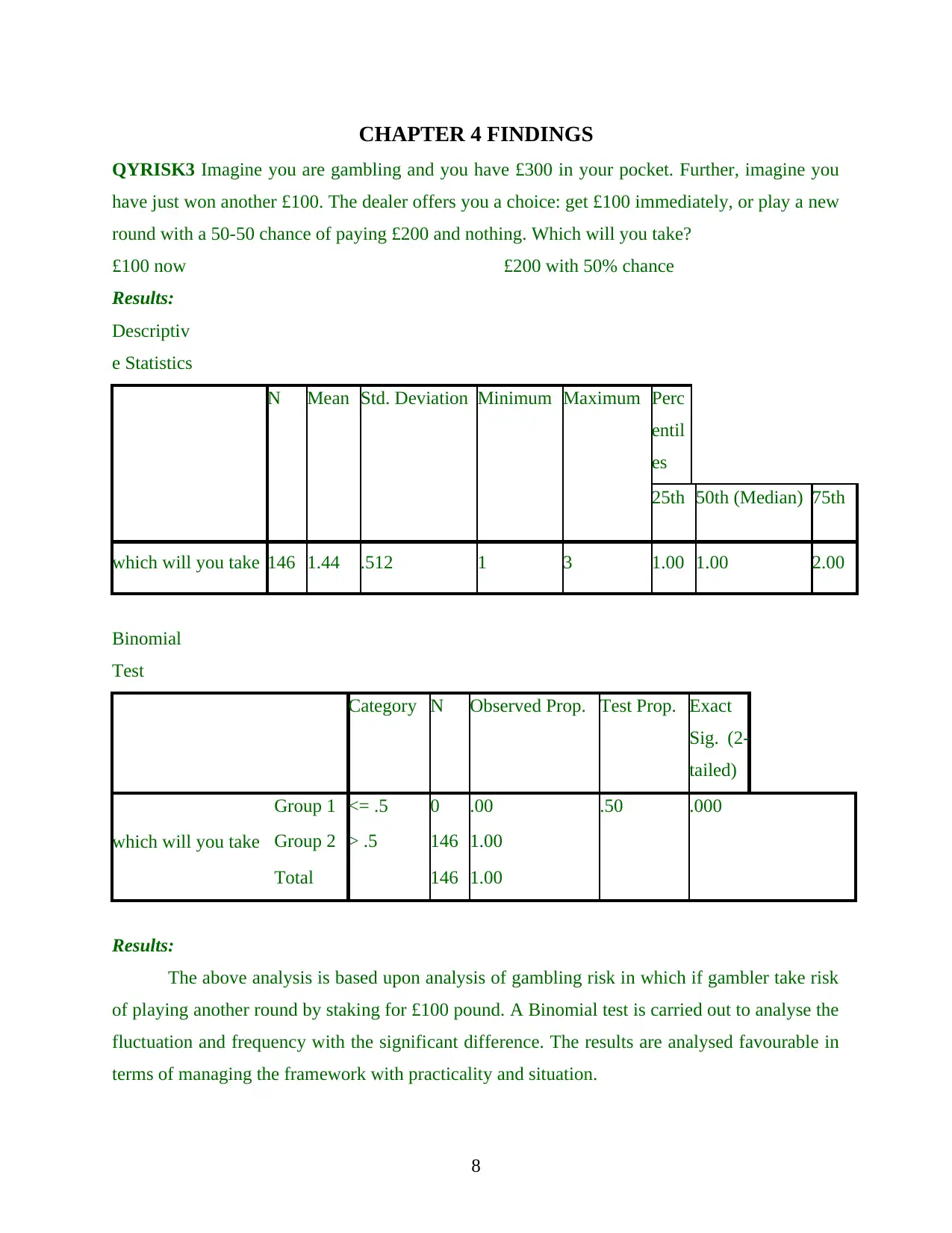

QYRISK3 Imagine you are gambling and you have £300 in your pocket. Further, imagine you

have just won another £100. The dealer offers you a choice: get £100 immediately, or play a new

round with a 50-50 chance of paying £200 and nothing. Which will you take?

£100 now £200 with 50% chance

Results:

Descriptiv

e Statistics

N Mean Std. Deviation Minimum Maximum Perc

entil

es

25th 50th (Median) 75th

which will you take 146 1.44 .512 1 3 1.00 1.00 2.00

Binomial

Test

Category N Observed Prop. Test Prop. Exact

Sig. (2-

tailed)

which will you take

Group 1 <= .5 0 .00 .50 .000

Group 2 > .5 146 1.00

Total 146 1.00

Results:

The above analysis is based upon analysis of gambling risk in which if gambler take risk

of playing another round by staking for £100 pound. A Binomial test is carried out to analyse the

fluctuation and frequency with the significant difference. The results are analysed favourable in

terms of managing the framework with practicality and situation.

8

QYRISK3 Imagine you are gambling and you have £300 in your pocket. Further, imagine you

have just won another £100. The dealer offers you a choice: get £100 immediately, or play a new

round with a 50-50 chance of paying £200 and nothing. Which will you take?

£100 now £200 with 50% chance

Results:

Descriptiv

e Statistics

N Mean Std. Deviation Minimum Maximum Perc

entil

es

25th 50th (Median) 75th

which will you take 146 1.44 .512 1 3 1.00 1.00 2.00

Binomial

Test

Category N Observed Prop. Test Prop. Exact

Sig. (2-

tailed)

which will you take

Group 1 <= .5 0 .00 .50 .000

Group 2 > .5 146 1.00

Total 146 1.00

Results:

The above analysis is based upon analysis of gambling risk in which if gambler take risk

of playing another round by staking for £100 pound. A Binomial test is carried out to analyse the

fluctuation and frequency with the significant difference. The results are analysed favourable in

terms of managing the framework with practicality and situation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

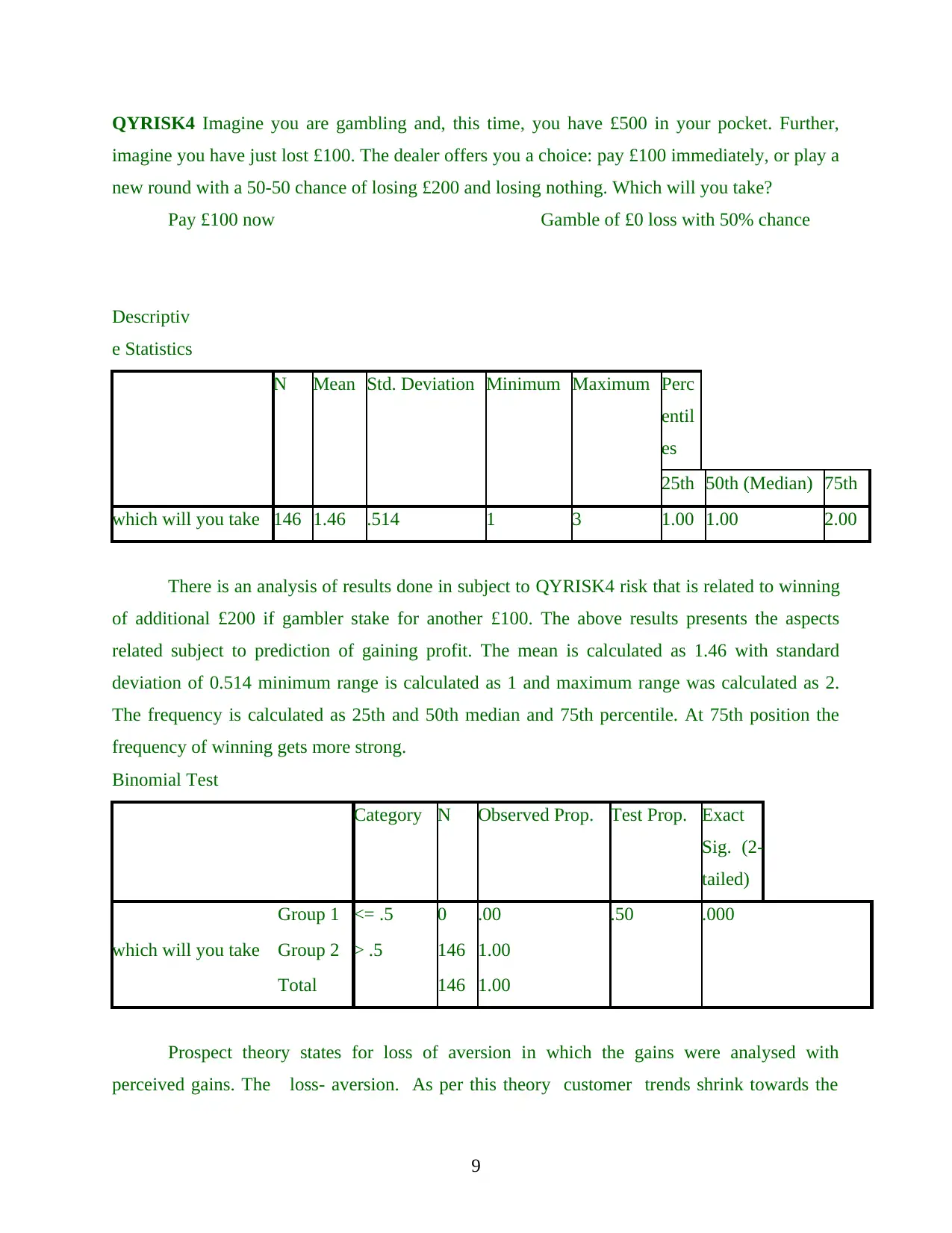

QYRISK4 Imagine you are gambling and, this time, you have £500 in your pocket. Further,

imagine you have just lost £100. The dealer offers you a choice: pay £100 immediately, or play a

new round with a 50-50 chance of losing £200 and losing nothing. Which will you take?

Pay £100 now Gamble of £0 loss with 50% chance

Descriptiv

e Statistics

N Mean Std. Deviation Minimum Maximum Perc

entil

es

25th 50th (Median) 75th

which will you take 146 1.46 .514 1 3 1.00 1.00 2.00

There is an analysis of results done in subject to QYRISK4 risk that is related to winning

of additional £200 if gambler stake for another £100. The above results presents the aspects

related subject to prediction of gaining profit. The mean is calculated as 1.46 with standard

deviation of 0.514 minimum range is calculated as 1 and maximum range was calculated as 2.

The frequency is calculated as 25th and 50th median and 75th percentile. At 75th position the

frequency of winning gets more strong.

Binomial Test

Category N Observed Prop. Test Prop. Exact

Sig. (2-

tailed)

which will you take

Group 1 <= .5 0 .00 .50 .000

Group 2 > .5 146 1.00

Total 146 1.00

Prospect theory states for loss of aversion in which the gains were analysed with

perceived gains. The loss- aversion. As per this theory customer trends shrink towards the

9

imagine you have just lost £100. The dealer offers you a choice: pay £100 immediately, or play a

new round with a 50-50 chance of losing £200 and losing nothing. Which will you take?

Pay £100 now Gamble of £0 loss with 50% chance

Descriptiv

e Statistics

N Mean Std. Deviation Minimum Maximum Perc

entil

es

25th 50th (Median) 75th

which will you take 146 1.46 .514 1 3 1.00 1.00 2.00

There is an analysis of results done in subject to QYRISK4 risk that is related to winning

of additional £200 if gambler stake for another £100. The above results presents the aspects

related subject to prediction of gaining profit. The mean is calculated as 1.46 with standard

deviation of 0.514 minimum range is calculated as 1 and maximum range was calculated as 2.

The frequency is calculated as 25th and 50th median and 75th percentile. At 75th position the

frequency of winning gets more strong.

Binomial Test

Category N Observed Prop. Test Prop. Exact

Sig. (2-

tailed)

which will you take

Group 1 <= .5 0 .00 .50 .000

Group 2 > .5 146 1.00

Total 146 1.00

Prospect theory states for loss of aversion in which the gains were analysed with

perceived gains. The loss- aversion. As per this theory customer trends shrink towards the

9

profitability. In the case where two alternatives are available with same results then it is

evaluated that organisation should compress the changes accordingly. The formation of

viability also remain same and stable.

In the above analysis results are same but with different results. However, there is very

significant difference found in the above analysis as QYRISK3 with significant difference of

0.512 and QYRISK4 with significant difference of 0.514. Gambler should go with the

QYRISK3 because it contains less difference.

10

evaluated that organisation should compress the changes accordingly. The formation of

viability also remain same and stable.

In the above analysis results are same but with different results. However, there is very

significant difference found in the above analysis as QYRISK3 with significant difference of

0.512 and QYRISK4 with significant difference of 0.514. Gambler should go with the

QYRISK3 because it contains less difference.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.