Comparative Cost Analysis of Jackson Ltd. Products: Fred & Martha

VerifiedAdded on 2020/06/06

|9

|2435

|90

Report

AI Summary

This report examines the cost accounting practices of Jackson Ltd., focusing on the production of two products, Fred and Martha. It compares and contrasts conventional costing methods with activity-based costing (ABC) techniques to determine product costs and pricing strategies. The report includes detailed calculations of per-unit costs using both approaches, highlighting the differences in overhead allocation and the potential for mispricing under conventional methods. It also details the cost per activity for each activity cost pool in ABC, and calculates the selling price using the ABC method. Further, the report outlines the benefits and disadvantages of using ABC, emphasizing its ability to provide more accurate cost information for decision-making. The conclusion suggests that Jackson Ltd. can optimize its business operations by adopting ABC for improved profitability and competitive advantage.

Information to

management Accounting

management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

a). Per unit cost by using conventional approach:.......................................................................1

b). Cost per activity for each activity cost pool:.........................................................................1

c).Product cost per unit as per Activity-based-costing technique: .............................................2

d). Calculate the price:................................................................................................................3

e). How conventional value approach leads to misprice the product:.........................................3

f). Benefits of activity based Costing..........................................................................................4

g). Disadvantages of using ABC costing...................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

a). Per unit cost by using conventional approach:.......................................................................1

b). Cost per activity for each activity cost pool:.........................................................................1

c).Product cost per unit as per Activity-based-costing technique: .............................................2

d). Calculate the price:................................................................................................................3

e). How conventional value approach leads to misprice the product:.........................................3

f). Benefits of activity based Costing..........................................................................................4

g). Disadvantages of using ABC costing...................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Management accounting helps the managers and other key members to take an

independent decisions so that they could able to frame decisions in terms of analysing the cost. If

there is any wastage of cost, then with the help of this, the cost can be eliminate. Normally, this

is occurred under the manufacturing entities (Islam, and Hu, 2012). Under this project, the

Jackson limited produces two product Fred and Martha and the cost accountant emphasis to

calculate the cost by using conventional approach and activity based costing methods. In this

project, the company opt activity based accounting approach so that the price of the product can

be reduced by way of eliminating the extra cost. Under this project, the cited company needs to

make their business operations effectively so that the business can get their objectives.

a). Per unit cost by using conventional approach:

Particular

Martha cost per

unit

Fred cost per

unit

Direct Material 60 40

Direct Labour 45 30

Manufacturing overheads 816000/6000 136 136

Total per unit cost 241 206

Under this calculation, the costs as per the conventional costing, are calculated and this is

the method which was used earlier while calculating cost. All direct costs are the same as earlier

but the manufacturing overheads cost changed under this method. However, there are so many

advance techniques emerged in the market under which the costs are optimum used. Under this

technique, the manufacturing overheads are calculated by sum up of all entire manufacturing cost

and then divide it by total number of units.

b). Cost per activity for each activity cost pool:

An activity cost pool is a pre-set costs group which arises at the time of specified

operations are performed in a firm (Activity based costing, 2017). By accounting for entire costs

are incurred under a particular activity with a pool, this is an easy process to allot those costs to

products and covered an accurate forecasting of production costs. Activity cost pool is the entire

cost required to execute production.

1

Management accounting helps the managers and other key members to take an

independent decisions so that they could able to frame decisions in terms of analysing the cost. If

there is any wastage of cost, then with the help of this, the cost can be eliminate. Normally, this

is occurred under the manufacturing entities (Islam, and Hu, 2012). Under this project, the

Jackson limited produces two product Fred and Martha and the cost accountant emphasis to

calculate the cost by using conventional approach and activity based costing methods. In this

project, the company opt activity based accounting approach so that the price of the product can

be reduced by way of eliminating the extra cost. Under this project, the cited company needs to

make their business operations effectively so that the business can get their objectives.

a). Per unit cost by using conventional approach:

Particular

Martha cost per

unit

Fred cost per

unit

Direct Material 60 40

Direct Labour 45 30

Manufacturing overheads 816000/6000 136 136

Total per unit cost 241 206

Under this calculation, the costs as per the conventional costing, are calculated and this is

the method which was used earlier while calculating cost. All direct costs are the same as earlier

but the manufacturing overheads cost changed under this method. However, there are so many

advance techniques emerged in the market under which the costs are optimum used. Under this

technique, the manufacturing overheads are calculated by sum up of all entire manufacturing cost

and then divide it by total number of units.

b). Cost per activity for each activity cost pool:

An activity cost pool is a pre-set costs group which arises at the time of specified

operations are performed in a firm (Activity based costing, 2017). By accounting for entire costs

are incurred under a particular activity with a pool, this is an easy process to allot those costs to

products and covered an accurate forecasting of production costs. Activity cost pool is the entire

cost required to execute production.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

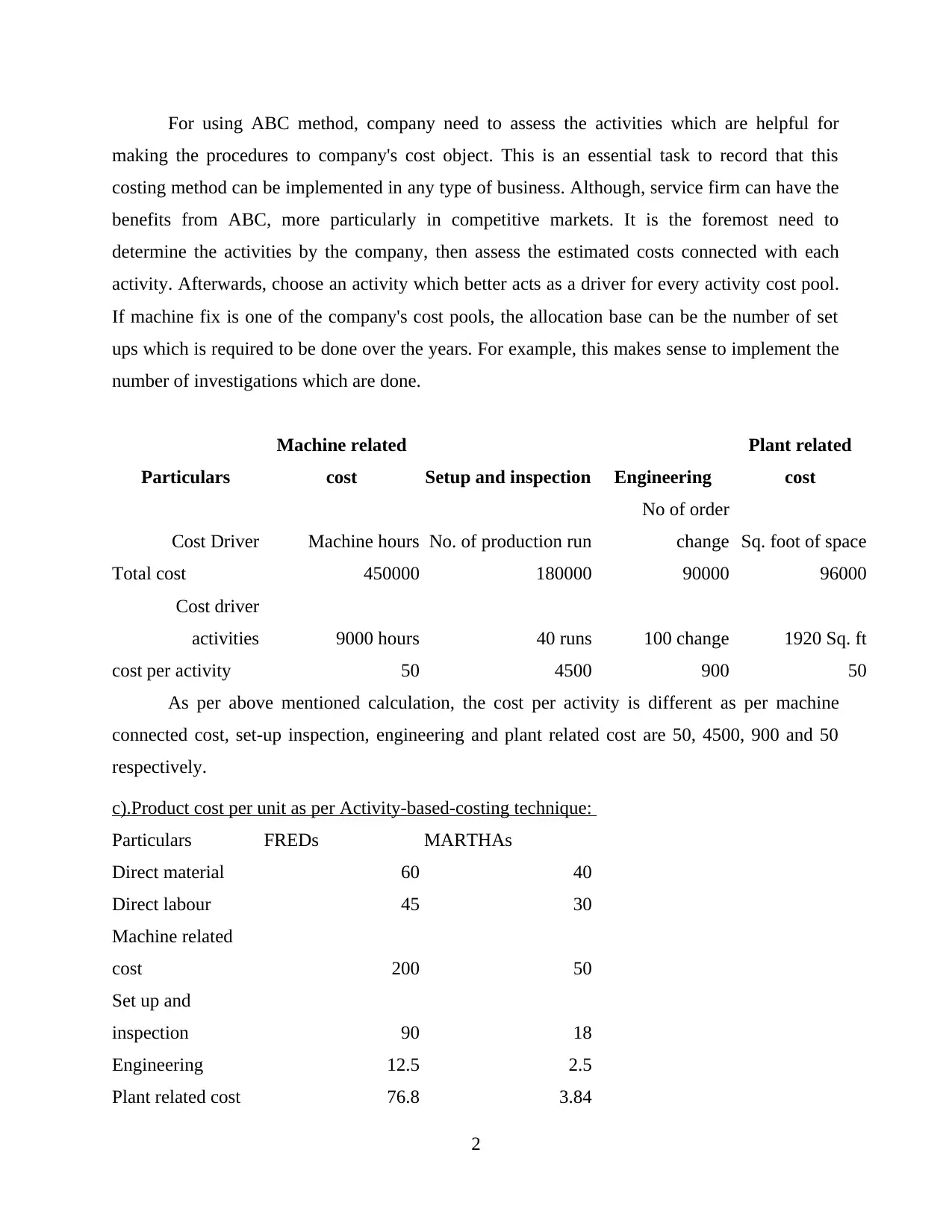

For using ABC method, company need to assess the activities which are helpful for

making the procedures to company's cost object. This is an essential task to record that this

costing method can be implemented in any type of business. Although, service firm can have the

benefits from ABC, more particularly in competitive markets. It is the foremost need to

determine the activities by the company, then assess the estimated costs connected with each

activity. Afterwards, choose an activity which better acts as a driver for every activity cost pool.

If machine fix is one of the company's cost pools, the allocation base can be the number of set

ups which is required to be done over the years. For example, this makes sense to implement the

number of investigations which are done.

Particulars

Machine related

cost Setup and inspection Engineering

Plant related

cost

Cost Driver Machine hours No. of production run

No of order

change Sq. foot of space

Total cost 450000 180000 90000 96000

Cost driver

activities 9000 hours 40 runs 100 change 1920 Sq. ft

cost per activity 50 4500 900 50

As per above mentioned calculation, the cost per activity is different as per machine

connected cost, set-up inspection, engineering and plant related cost are 50, 4500, 900 and 50

respectively.

c).Product cost per unit as per Activity-based-costing technique:

Particulars FREDs MARTHAs

Direct material 60 40

Direct labour 45 30

Machine related

cost 200 50

Set up and

inspection 90 18

Engineering 12.5 2.5

Plant related cost 76.8 3.84

2

making the procedures to company's cost object. This is an essential task to record that this

costing method can be implemented in any type of business. Although, service firm can have the

benefits from ABC, more particularly in competitive markets. It is the foremost need to

determine the activities by the company, then assess the estimated costs connected with each

activity. Afterwards, choose an activity which better acts as a driver for every activity cost pool.

If machine fix is one of the company's cost pools, the allocation base can be the number of set

ups which is required to be done over the years. For example, this makes sense to implement the

number of investigations which are done.

Particulars

Machine related

cost Setup and inspection Engineering

Plant related

cost

Cost Driver Machine hours No. of production run

No of order

change Sq. foot of space

Total cost 450000 180000 90000 96000

Cost driver

activities 9000 hours 40 runs 100 change 1920 Sq. ft

cost per activity 50 4500 900 50

As per above mentioned calculation, the cost per activity is different as per machine

connected cost, set-up inspection, engineering and plant related cost are 50, 4500, 900 and 50

respectively.

c).Product cost per unit as per Activity-based-costing technique:

Particulars FREDs MARTHAs

Direct material 60 40

Direct labour 45 30

Machine related

cost 200 50

Set up and

inspection 90 18

Engineering 12.5 2.5

Plant related cost 76.8 3.84

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total cost (per

unit) 484.3 144.34

By using activity based costing, Fred and Martha's cost per unit is calculated as 484.3 and 144.34

respectively (Nielsen, Mitchell and Nørreklit, 2015). This costing technique is used in order to

make the price of the company effective so that the company can able to have the competitive

advantage in a better manner. This will also help out to make their business sustainable and

prosperous. After considering these prices, the company is able to grow their sale in an effective

manner.

d). Calculate the price:

Particulars FREDs MARTHAs

Direct material 60 40

Direct labour 45 30

Machine related

cost 200 50

Set up and

inspection 90 18

Engineering 12.5 2.5

Plant related cost 76.8 3.84

Total cost 484.3 144.34

selling price (per

unit) 581.16 173.208

The selling price of the product under the activity based costing of the are 581.16 and

173.21. which is better than the conventional methods of costing.

e). How conventional value approach leads to misprice the product:

Under the conventional approach, a common pre- decided overheads rate is implemented.

Entire manufacturing overhead costs are merged into single cost pool, and they are used to goods

on the basis of single cost driver which is connected to production volume. Direct labour hour,

machine-hours and total units of production are the main drivers under conventional costing

which are more frequently implemented. While, on the other hand, ABC categorises costs into

two main stages. Under one stage, the establishment of the activity cost pools are done. In other

stage, for each activity cost pool, cost driver is determined. Henceforth, the costs under each pool

3

unit) 484.3 144.34

By using activity based costing, Fred and Martha's cost per unit is calculated as 484.3 and 144.34

respectively (Nielsen, Mitchell and Nørreklit, 2015). This costing technique is used in order to

make the price of the company effective so that the company can able to have the competitive

advantage in a better manner. This will also help out to make their business sustainable and

prosperous. After considering these prices, the company is able to grow their sale in an effective

manner.

d). Calculate the price:

Particulars FREDs MARTHAs

Direct material 60 40

Direct labour 45 30

Machine related

cost 200 50

Set up and

inspection 90 18

Engineering 12.5 2.5

Plant related cost 76.8 3.84

Total cost 484.3 144.34

selling price (per

unit) 581.16 173.208

The selling price of the product under the activity based costing of the are 581.16 and

173.21. which is better than the conventional methods of costing.

e). How conventional value approach leads to misprice the product:

Under the conventional approach, a common pre- decided overheads rate is implemented.

Entire manufacturing overhead costs are merged into single cost pool, and they are used to goods

on the basis of single cost driver which is connected to production volume. Direct labour hour,

machine-hours and total units of production are the main drivers under conventional costing

which are more frequently implemented. While, on the other hand, ABC categorises costs into

two main stages. Under one stage, the establishment of the activity cost pools are done. In other

stage, for each activity cost pool, cost driver is determined. Henceforth, the costs under each pool

3

are allotted to each product line under proportion to the amount of the cost driver used by the

each product line.

Under the activity based costing technique, Fred and Martha product cost per unit is

calculated as 581.16 and, martha's per unit price is calculated 173.21. On the other hand, as per

the conventional approach, the per unit cost of product fred and martha are 206 and 241

respectively. Henceforth, product Martha cost is optimum by using conventional value approach

(Harris and Durden, 2012). But product fred cost is at an optimum level when the cited company

use the activity based costing method. Henceforth, the cited company can make their product

accordingly.

Illustration 1: ABC vs. Treditional Methods, 2017

f). Benefits of activity based Costing

Activity based costing are defined as managerial accounts process that are useful in analysing

the final cost of the goods and services offered by delivering the overhead cost to the direct

costing process (Activity based costing, 2017.). This is useful in assigning cost factors to the

4

each product line.

Under the activity based costing technique, Fred and Martha product cost per unit is

calculated as 581.16 and, martha's per unit price is calculated 173.21. On the other hand, as per

the conventional approach, the per unit cost of product fred and martha are 206 and 241

respectively. Henceforth, product Martha cost is optimum by using conventional value approach

(Harris and Durden, 2012). But product fred cost is at an optimum level when the cited company

use the activity based costing method. Henceforth, the cited company can make their product

accordingly.

Illustration 1: ABC vs. Treditional Methods, 2017

f). Benefits of activity based Costing

Activity based costing are defined as managerial accounts process that are useful in analysing

the final cost of the goods and services offered by delivering the overhead cost to the direct

costing process (Activity based costing, 2017.). This is useful in assigning cost factors to the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activity which are operating at business organisations according to the actual process in which

the resources are to be consumed. This is useful in sharing their overheads cost in order to know

the actual prices of the products.

Advantages

The major benefits of ABC activities are related with finding out individual cost of the

products and the services which have been offered to there potential customers. If the overhead

cost are being transferred in finding out single cost of goods. This in turn is beneficial for

business in order to evaluate the non profitability factors that are entering into effective product

lines.

The major benefits are described as:

There should be scientific and equitable prices adopted by making reduction in the prices

of products that are utilising less resources and the prices of those products should be

increased which are mostly demanded by the customers (Bobryshev and et. al., 2014).

It is useful in giving services with added values or making innovations in the existing

goods on the basis of the cost which have been incorporated actually.

All those should be removed from the product lines which are non profitable. The

outcome of this will be that profitability will be increase without making changes in the

pricing policy.

The cost which have been made on the maintenance and running of the non remunerative

acts which helps in increasing the overall profitability factors of firms.

The resources should be implemented effectively in profitable ways so that they can

easily recover all the cost factors (Islam and Hu, 2012).

The tools which are used for performance management systems should be compatible.

This can be achieved by analysing the contribution factors of each persons in determining

the cost and thereby profit ratios.

The waste should be exposed and the inefficient factors that are valuable in boosting

productivity ratios.

Identification of all those activities which are not adding any values or the task which are

not having any contribution towards the final values of the process involved in

manufacturing products (Yigitbasioglu and Velcu, 2012). Example: The activities which

5

the resources are to be consumed. This is useful in sharing their overheads cost in order to know

the actual prices of the products.

Advantages

The major benefits of ABC activities are related with finding out individual cost of the

products and the services which have been offered to there potential customers. If the overhead

cost are being transferred in finding out single cost of goods. This in turn is beneficial for

business in order to evaluate the non profitability factors that are entering into effective product

lines.

The major benefits are described as:

There should be scientific and equitable prices adopted by making reduction in the prices

of products that are utilising less resources and the prices of those products should be

increased which are mostly demanded by the customers (Bobryshev and et. al., 2014).

It is useful in giving services with added values or making innovations in the existing

goods on the basis of the cost which have been incorporated actually.

All those should be removed from the product lines which are non profitable. The

outcome of this will be that profitability will be increase without making changes in the

pricing policy.

The cost which have been made on the maintenance and running of the non remunerative

acts which helps in increasing the overall profitability factors of firms.

The resources should be implemented effectively in profitable ways so that they can

easily recover all the cost factors (Islam and Hu, 2012).

The tools which are used for performance management systems should be compatible.

This can be achieved by analysing the contribution factors of each persons in determining

the cost and thereby profit ratios.

The waste should be exposed and the inefficient factors that are valuable in boosting

productivity ratios.

Identification of all those activities which are not adding any values or the task which are

not having any contribution towards the final values of the process involved in

manufacturing products (Yigitbasioglu and Velcu, 2012). Example: The activities which

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are not adding any values to products include duplication process and inspections which

are not needed.

For effective planning of all the strategies there should be appropriate figures provided in

order to find out there values.

However, there are certain questions which are need to consider while implementing the ABC

technique in their operations. These are:

Do the cost accountant entirely know the resource implications of using, running and

managing ABC technique (Lambert and Sponem, 2012).

Do the company have resources to use ABC.

Will the costs outweigh the profit.

Do the company have enough stakeholder buy-in.

g). Disadvantages of using ABC costing

There are various disadvantage which are analysed in using ABC costing methods which

are described as:

These activities cannot be implemented those companies which are having there business

operations at very small small scales as they are not able to find out the single cost of each

product.

If the overheads cost are very less or are at smaller scales than there is no use of

implementing activity based Costing techniques.

Many of the companies are not focusing on expanding there product lines and they are

only dealing in producing single products. Thus in this situations activity costing cannot be

applied at the work place (DRURY, 2013).

The ABC methods are not useful in preparing the statements which reflect the monthly

profit ratios which have been achieved by firms.

There is difficulty faced in identification of the total activities or task which influences

the costing factors.

By this methods we cannot select the best and the most appropriate cost driving factors.

The activities which have been conducted at business organisations are not helpful in

analysing the cost factors which have been used in manufacturing them.

6

are not needed.

For effective planning of all the strategies there should be appropriate figures provided in

order to find out there values.

However, there are certain questions which are need to consider while implementing the ABC

technique in their operations. These are:

Do the cost accountant entirely know the resource implications of using, running and

managing ABC technique (Lambert and Sponem, 2012).

Do the company have resources to use ABC.

Will the costs outweigh the profit.

Do the company have enough stakeholder buy-in.

g). Disadvantages of using ABC costing

There are various disadvantage which are analysed in using ABC costing methods which

are described as:

These activities cannot be implemented those companies which are having there business

operations at very small small scales as they are not able to find out the single cost of each

product.

If the overheads cost are very less or are at smaller scales than there is no use of

implementing activity based Costing techniques.

Many of the companies are not focusing on expanding there product lines and they are

only dealing in producing single products. Thus in this situations activity costing cannot be

applied at the work place (DRURY, 2013).

The ABC methods are not useful in preparing the statements which reflect the monthly

profit ratios which have been achieved by firms.

There is difficulty faced in identification of the total activities or task which influences

the costing factors.

By this methods we cannot select the best and the most appropriate cost driving factors.

The activities which have been conducted at business organisations are not helpful in

analysing the cost factors which have been used in manufacturing them.

6

CONCLUSION

From the above report, this is analysed that the Jackson company can make their business

operations in a optimum manner by using the advanced costing technique. Under this report, this

is observed that the company uses conventional approach and activity based costing approach for

ascertaining the price in an effective manner. The activity based costing approach used to assess

the cost of the product Martha and Fred, and then the pricing strategy is made in order to have

the maximum sales. So that the management of the company is able to make their business

effective and this will also make the business operations in a more smooth way so that the firm

can earn profits in an effective manner.

7

From the above report, this is analysed that the Jackson company can make their business

operations in a optimum manner by using the advanced costing technique. Under this report, this

is observed that the company uses conventional approach and activity based costing approach for

ascertaining the price in an effective manner. The activity based costing approach used to assess

the cost of the product Martha and Fred, and then the pricing strategy is made in order to have

the maximum sales. So that the management of the company is able to make their business

effective and this will also make the business operations in a more smooth way so that the firm

can earn profits in an effective manner.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.