Management Accounting Report for Murano Restaurant: Financial Analysis

VerifiedAdded on 2020/07/22

|17

|4865

|239

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on their application within the context of the Murano restaurant. It begins by explaining the essential requirements of management accounting systems, emphasizing their role in internal business reporting and decision-making. The report then presents various managerial reports, such as budget/performance, cost, and inventory reports, highlighting their significance in streamlining operations and aiding in financial analysis. Furthermore, it delves into different costing systems, including absorption costing and marginal costing, illustrating how they determine costs and profit margins. The report also assesses planning tools within the management accounting system and explores how these tools can be used to address financial problems. Throughout the report, the practical application of these concepts is demonstrated through examples and analysis relevant to the Murano restaurant, providing a clear understanding of how management accounting can enhance efficiency, productivity, and profitability.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

P1 Explaining MA systems along with their essential requirements.....................................1

P2 Presenting managerial reports that are related to MA......................................................4

P3 Presenting different types of costing system for determining cost and profit margin......5

P4 Assessing planning tools that are related with management accounting system..............9

P5 Explaining management accounting system that can be undertaken for responding

financial problems................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................1

P1 Explaining MA systems along with their essential requirements.....................................1

P2 Presenting managerial reports that are related to MA......................................................4

P3 Presenting different types of costing system for determining cost and profit margin......5

P4 Assessing planning tools that are related with management accounting system..............9

P5 Explaining management accounting system that can be undertaken for responding

financial problems................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................15

INTRODUCTION

Management accounting (MA) is highly associated with the preparation and analysis

of internal business reports. Tools & technique of MA assists in evaluating cost and

operations of business unit. By using MA tools manager of the business unit can assess the

area of cost control and would become able to take action for improvement. Further, field of

MA also assists business organization in developing competent framework for the upcoming

time period. For this project, Murano restaurant unit has been selected which offers dinning

services to the customers at affordable prices. In this, report will shed light on the essentials

or need of MA in the context of concerned restaurant unit. Further, it also entails the manner

in which absorption and marginal costing method helps in ascertaining cost as well as

margin. Along with this, it also develops understanding about the planning tools that helps in

developing competent financial framework. Report will also describe the way in which MA

tools help in mitigating monetary issues.

P1 Explaining MA systems along with their essential requirements

Management accounting: Filed of MA is highly concerned with the recording and

analysis of business activities related to the internal aspects or business activities. MA tools

and report helps in enhancing efficiency, productivity and profitability to a great extent.

Hence, by employing the tools and techniques of MA Murano can ensure effective

management of operations.

Significance or need of management accounting

MA provides high level of assistance to the restaurant unit in doing appropriate

forecast about future and aid in significant decision making

By undertaking MA, owner or concerned authority of Murano can make appropriate

forecast regarding cash flows (Management accounting and its importance, 2017).

It also helps in understanding variances and makes contribution in the attainment of

goals by suggesting suitable improvement measure.

Murano can analyze suitable rate of return through using the techniques of

management accounting.

Different types of management accounting system that can be undertaken by Murano

are as follows:

Management accounting (MA) is highly associated with the preparation and analysis

of internal business reports. Tools & technique of MA assists in evaluating cost and

operations of business unit. By using MA tools manager of the business unit can assess the

area of cost control and would become able to take action for improvement. Further, field of

MA also assists business organization in developing competent framework for the upcoming

time period. For this project, Murano restaurant unit has been selected which offers dinning

services to the customers at affordable prices. In this, report will shed light on the essentials

or need of MA in the context of concerned restaurant unit. Further, it also entails the manner

in which absorption and marginal costing method helps in ascertaining cost as well as

margin. Along with this, it also develops understanding about the planning tools that helps in

developing competent financial framework. Report will also describe the way in which MA

tools help in mitigating monetary issues.

P1 Explaining MA systems along with their essential requirements

Management accounting: Filed of MA is highly concerned with the recording and

analysis of business activities related to the internal aspects or business activities. MA tools

and report helps in enhancing efficiency, productivity and profitability to a great extent.

Hence, by employing the tools and techniques of MA Murano can ensure effective

management of operations.

Significance or need of management accounting

MA provides high level of assistance to the restaurant unit in doing appropriate

forecast about future and aid in significant decision making

By undertaking MA, owner or concerned authority of Murano can make appropriate

forecast regarding cash flows (Management accounting and its importance, 2017).

It also helps in understanding variances and makes contribution in the attainment of

goals by suggesting suitable improvement measure.

Murano can analyze suitable rate of return through using the techniques of

management accounting.

Different types of management accounting system that can be undertaken by Murano

are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting: Such system or technique of MA assists in making decision about

the cost pertaining to products, services, projects etc. Hence, by using such accounting

system owner of Murano can assess unit cost and thereby able to sets suitable price.

Moreover, cost accounting lays high level of emphasis on capturing or recording cost of

production, fixed expenses, depreciation on capital equipment etc (What is cost accounting?,

2017). Along with this, cost accounting also enables management team of Murano to measure

financial performance by making comparison of actual output with the standards. Hence, the

main goal of management accounting system is to enhance the level of cost efficiency and

capability by advising appropriate course of action to the management team.

Thus, it can be said that cost accounting system aid in effective decision making by

recording, classifying, analyzing, summarizing and evaluating alternative ways to control

expenses. Hence, in the context of Murano, requirement of such accounting tool is highly

significant. Moreover, it considers cost plus method for the determination of pricing. Thus,

for setting price business unit is required to calculate or have information regarding per unit

cost.

Advantages Disadvantages

Helps in finding areas of wastage

losses and inefficiencies

Facilitates cost reduction and

maximizes profit margin

Advising decision in relation to make

or buy

Assists in setting prices of the

products or services offered

Under cost accounting, past

information’s are available whereas

management is concerned about

future

For the installation of cost accounting

system firm has to make several

expenses because it demands for the

high maintenance of records.

Rigid in nature so it does not meet all

the objectives

Job costing: It involves or lay emphasis on the accumulation of costs pertaining to

material, labour and overheads which are related to specific job. By using such tool of MA,

owner of Murano can trace or monitor the cost of job prominently (Job costing, 2017).

Continuous monitoring enables firm to assess whether cost can be reduced in the later jobs or

not.

the cost pertaining to products, services, projects etc. Hence, by using such accounting

system owner of Murano can assess unit cost and thereby able to sets suitable price.

Moreover, cost accounting lays high level of emphasis on capturing or recording cost of

production, fixed expenses, depreciation on capital equipment etc (What is cost accounting?,

2017). Along with this, cost accounting also enables management team of Murano to measure

financial performance by making comparison of actual output with the standards. Hence, the

main goal of management accounting system is to enhance the level of cost efficiency and

capability by advising appropriate course of action to the management team.

Thus, it can be said that cost accounting system aid in effective decision making by

recording, classifying, analyzing, summarizing and evaluating alternative ways to control

expenses. Hence, in the context of Murano, requirement of such accounting tool is highly

significant. Moreover, it considers cost plus method for the determination of pricing. Thus,

for setting price business unit is required to calculate or have information regarding per unit

cost.

Advantages Disadvantages

Helps in finding areas of wastage

losses and inefficiencies

Facilitates cost reduction and

maximizes profit margin

Advising decision in relation to make

or buy

Assists in setting prices of the

products or services offered

Under cost accounting, past

information’s are available whereas

management is concerned about

future

For the installation of cost accounting

system firm has to make several

expenses because it demands for the

high maintenance of records.

Rigid in nature so it does not meet all

the objectives

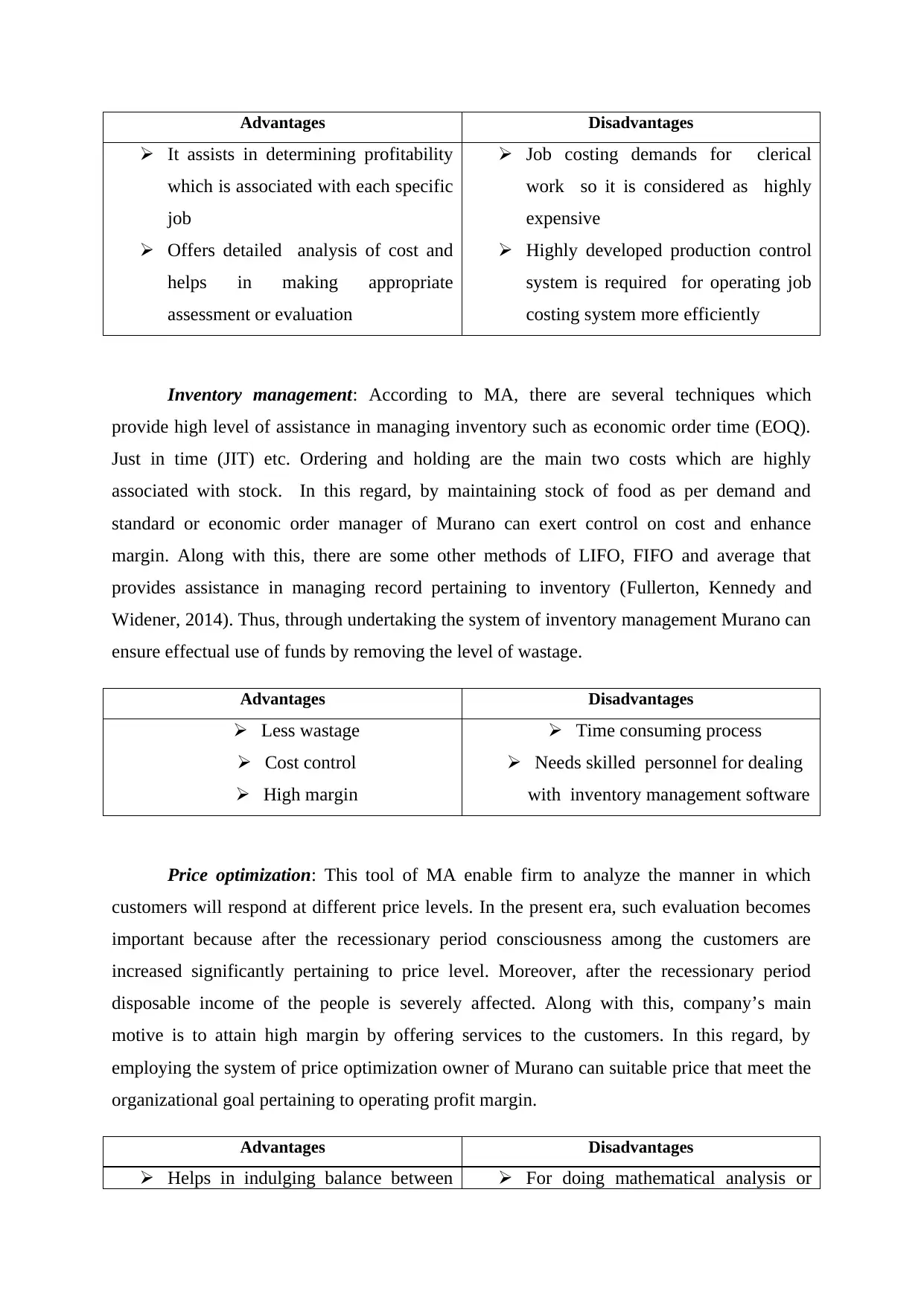

Job costing: It involves or lay emphasis on the accumulation of costs pertaining to

material, labour and overheads which are related to specific job. By using such tool of MA,

owner of Murano can trace or monitor the cost of job prominently (Job costing, 2017).

Continuous monitoring enables firm to assess whether cost can be reduced in the later jobs or

not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages Disadvantages

It assists in determining profitability

which is associated with each specific

job

Offers detailed analysis of cost and

helps in making appropriate

assessment or evaluation

Job costing demands for clerical

work so it is considered as highly

expensive

Highly developed production control

system is required for operating job

costing system more efficiently

Inventory management: According to MA, there are several techniques which

provide high level of assistance in managing inventory such as economic order time (EOQ).

Just in time (JIT) etc. Ordering and holding are the main two costs which are highly

associated with stock. In this regard, by maintaining stock of food as per demand and

standard or economic order manager of Murano can exert control on cost and enhance

margin. Along with this, there are some other methods of LIFO, FIFO and average that

provides assistance in managing record pertaining to inventory (Fullerton, Kennedy and

Widener, 2014). Thus, through undertaking the system of inventory management Murano can

ensure effectual use of funds by removing the level of wastage.

Advantages Disadvantages

Less wastage

Cost control

High margin

Time consuming process

Needs skilled personnel for dealing

with inventory management software

Price optimization: This tool of MA enable firm to analyze the manner in which

customers will respond at different price levels. In the present era, such evaluation becomes

important because after the recessionary period consciousness among the customers are

increased significantly pertaining to price level. Moreover, after the recessionary period

disposable income of the people is severely affected. Along with this, company’s main

motive is to attain high margin by offering services to the customers. In this regard, by

employing the system of price optimization owner of Murano can suitable price that meet the

organizational goal pertaining to operating profit margin.

Advantages Disadvantages

Helps in indulging balance between For doing mathematical analysis or

It assists in determining profitability

which is associated with each specific

job

Offers detailed analysis of cost and

helps in making appropriate

assessment or evaluation

Job costing demands for clerical

work so it is considered as highly

expensive

Highly developed production control

system is required for operating job

costing system more efficiently

Inventory management: According to MA, there are several techniques which

provide high level of assistance in managing inventory such as economic order time (EOQ).

Just in time (JIT) etc. Ordering and holding are the main two costs which are highly

associated with stock. In this regard, by maintaining stock of food as per demand and

standard or economic order manager of Murano can exert control on cost and enhance

margin. Along with this, there are some other methods of LIFO, FIFO and average that

provides assistance in managing record pertaining to inventory (Fullerton, Kennedy and

Widener, 2014). Thus, through undertaking the system of inventory management Murano can

ensure effectual use of funds by removing the level of wastage.

Advantages Disadvantages

Less wastage

Cost control

High margin

Time consuming process

Needs skilled personnel for dealing

with inventory management software

Price optimization: This tool of MA enable firm to analyze the manner in which

customers will respond at different price levels. In the present era, such evaluation becomes

important because after the recessionary period consciousness among the customers are

increased significantly pertaining to price level. Moreover, after the recessionary period

disposable income of the people is severely affected. Along with this, company’s main

motive is to attain high margin by offering services to the customers. In this regard, by

employing the system of price optimization owner of Murano can suitable price that meet the

organizational goal pertaining to operating profit margin.

Advantages Disadvantages

Helps in indulging balance between For doing mathematical analysis or

customer’s expectation and

organizational goal

Assists in enhancing customer base

evaluation firm needs talented

personnel. In the absence of having

same restaurant unit will not become

able to take benefit from such model.

P2 Presenting managerial reports that are related to MA

Managerial reports imply for the framework which gives information about day to day

functioning of restaurant unit. It provides manager with timely and accurate information

about the internal operations. MA reports are highly significant which in turn helps in

streamlining operations by indicating the need for better decision making. Benefits which are

associated with managerial reporting are as follows:

Helps in evaluating performance of each department

Gives input for setting appropriate bonus and incentive plans for the employees

Assists in identifying the efficiency level of personnel and helps in conducting

training session on time.

Enables manager to make optimum use of funds by taking corrective measure on time

when deviations are identified

Types of managerial report

Budget or performance report: Preparation of such report is highly significant in the

context of Murano. Moreover, this managerial report contains information about the

deviations take places in actual and standard aspect. Along with this, such report also

presents the reasons due to which specific target in relation to sales and expenses are

not met (Chenhall and Moers, 2015). Thus, by taking into account performance report

owner of Murano can take timely action for improvement. Further, considering the

level of deviation business organization can allocate suitable monetary fund to each

business activity.

Cost report: This report furnishes information about the cost incurred while

performing different activities and functions. By using this report, owner of the

restaurant unit can assess the expenses related to offering services to each customer. It

helps company in taking suitable pricing decision and generating enough margins.

Further, cost report also helps in assessing redundant activities and reduces the level

of expenses to a great extent. By using such report, manager of Murano can compare

organizational goal

Assists in enhancing customer base

evaluation firm needs talented

personnel. In the absence of having

same restaurant unit will not become

able to take benefit from such model.

P2 Presenting managerial reports that are related to MA

Managerial reports imply for the framework which gives information about day to day

functioning of restaurant unit. It provides manager with timely and accurate information

about the internal operations. MA reports are highly significant which in turn helps in

streamlining operations by indicating the need for better decision making. Benefits which are

associated with managerial reporting are as follows:

Helps in evaluating performance of each department

Gives input for setting appropriate bonus and incentive plans for the employees

Assists in identifying the efficiency level of personnel and helps in conducting

training session on time.

Enables manager to make optimum use of funds by taking corrective measure on time

when deviations are identified

Types of managerial report

Budget or performance report: Preparation of such report is highly significant in the

context of Murano. Moreover, this managerial report contains information about the

deviations take places in actual and standard aspect. Along with this, such report also

presents the reasons due to which specific target in relation to sales and expenses are

not met (Chenhall and Moers, 2015). Thus, by taking into account performance report

owner of Murano can take timely action for improvement. Further, considering the

level of deviation business organization can allocate suitable monetary fund to each

business activity.

Cost report: This report furnishes information about the cost incurred while

performing different activities and functions. By using this report, owner of the

restaurant unit can assess the expenses related to offering services to each customer. It

helps company in taking suitable pricing decision and generating enough margins.

Further, cost report also helps in assessing redundant activities and reduces the level

of expenses to a great extent. By using such report, manager of Murano can compare

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost and becomes able to take strategic measure or action for improvement.

Considering all such aspects it can be stated that cost report assists in comparing

expenses and helps in offering products or services at less price. Thus, input which are

offered by such report helps in formulating suitable policies and gaining comparative

edge over others.

Inventory report: Stock management report is highly significant in the context of

Murano restaurant unit. Such unit contains information about the cost level and

wastage. Thus, from such report manager of the firm can identify the level to which

inventory is used, sold and replaced more frequently. In addition to this, such report

also helps in making comparison between wastage level and gives indication

regarding the need of taking action. Moreover, high level of wastage places direct

impact on cost level and affects organizational profit margin.

Accounts receivable or ageing report: Debtors report can be prepared by Murano for

assessing the time period within which they are making payment. From assessment, it

has identified that debtors time period has significant influence on the level of

working capital. Thus, by using such report business unit can assess whether they

need to make modifications in the existing policies or framework or not (Otley and

Emmanuel, 2013). Thus, by taking suitable measure on time restaurant can improve

its working capital position and becomes able to carry out day to day activities in the

best possible way.

Hence, by taking into account all the above depicted aspects it can be presented that

managerial reports accelerate decision making aspect. It offers opportunity to the restaurant

unit to achieve success or meet goals by taking appropriate action on time.

P3 Presenting different types of costing system for determining cost and profit margin

Absorption costing: It implies for the too which lays emphasis on treating all the costs

as product irrespective of the aspect that they are variable or fixed. Under this, cost of

production includes material, labour, fixed and variable overheads. Moreover, such costing

method assumes that all the incurred cost can be recovered through the means of selling

price. Hence, such full costing method provides high level of assistance in ascertaining

appropriate cost and margin. It is highly aligned with the matching and accrual concept of

accounting (Absorption Costing: Definition, Formula & Example, 2017). Moreover, such

accounting concepts demand for matching cost with the revenue pertaining to particular

period. Further, it presents the better view of cost and margin by avoiding the separation of

Considering all such aspects it can be stated that cost report assists in comparing

expenses and helps in offering products or services at less price. Thus, input which are

offered by such report helps in formulating suitable policies and gaining comparative

edge over others.

Inventory report: Stock management report is highly significant in the context of

Murano restaurant unit. Such unit contains information about the cost level and

wastage. Thus, from such report manager of the firm can identify the level to which

inventory is used, sold and replaced more frequently. In addition to this, such report

also helps in making comparison between wastage level and gives indication

regarding the need of taking action. Moreover, high level of wastage places direct

impact on cost level and affects organizational profit margin.

Accounts receivable or ageing report: Debtors report can be prepared by Murano for

assessing the time period within which they are making payment. From assessment, it

has identified that debtors time period has significant influence on the level of

working capital. Thus, by using such report business unit can assess whether they

need to make modifications in the existing policies or framework or not (Otley and

Emmanuel, 2013). Thus, by taking suitable measure on time restaurant can improve

its working capital position and becomes able to carry out day to day activities in the

best possible way.

Hence, by taking into account all the above depicted aspects it can be presented that

managerial reports accelerate decision making aspect. It offers opportunity to the restaurant

unit to achieve success or meet goals by taking appropriate action on time.

P3 Presenting different types of costing system for determining cost and profit margin

Absorption costing: It implies for the too which lays emphasis on treating all the costs

as product irrespective of the aspect that they are variable or fixed. Under this, cost of

production includes material, labour, fixed and variable overheads. Moreover, such costing

method assumes that all the incurred cost can be recovered through the means of selling

price. Hence, such full costing method provides high level of assistance in ascertaining

appropriate cost and margin. It is highly aligned with the matching and accrual concept of

accounting (Absorption Costing: Definition, Formula & Example, 2017). Moreover, such

accounting concepts demand for matching cost with the revenue pertaining to particular

period. Further, it presents the better view of cost and margin by avoiding the separation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost in terms of fixed and variable. However, on the critical note, it can be stated that

absorption costing method creates difficulty in making comparison and control of cost.

Marginal costing: It helps in ascertaining the increase or decrease which takes place

in total cost of production when one additional unit is produced. It classifies cost in terms of

fixed and variable. Under marginal costing method, profitability is measured through the

means of PV ratio. Further, in this, variances which take place in the opening and closing

stock does not place high level of impact on per unit cost of output (Marginal Cost:

Definition, Equation & Formula, 2017). MC method highlights per unit contribution and

presents the extent to which it is related to each product.

Particulars

Cost per unit according to

absorption costing method (in £)

Cost per unit according to

Marginal costing (per unit (in £)

Material cost 6 6

Labour cost 5 5

Production overheads

Non-fixed

expenses 2 2

Fixed (2100 /

700) 3

Cost per unit

(production) 16 13

Assessment of GP and NP (absorption costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Total manufacturing cost (refer working note 1) 11,200

Add: stock in the starting of period 0

Less: Ending inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

absorption costing method creates difficulty in making comparison and control of cost.

Marginal costing: It helps in ascertaining the increase or decrease which takes place

in total cost of production when one additional unit is produced. It classifies cost in terms of

fixed and variable. Under marginal costing method, profitability is measured through the

means of PV ratio. Further, in this, variances which take place in the opening and closing

stock does not place high level of impact on per unit cost of output (Marginal Cost:

Definition, Equation & Formula, 2017). MC method highlights per unit contribution and

presents the extent to which it is related to each product.

Particulars

Cost per unit according to

absorption costing method (in £)

Cost per unit according to

Marginal costing (per unit (in £)

Material cost 6 6

Labour cost 5 5

Production overheads

Non-fixed

expenses 2 2

Fixed (2100 /

700) 3

Cost per unit

(production) 16 13

Assessment of GP and NP (absorption costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Total manufacturing cost (refer working note 1) 11,200

Add: stock in the starting of period 0

Less: Ending inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

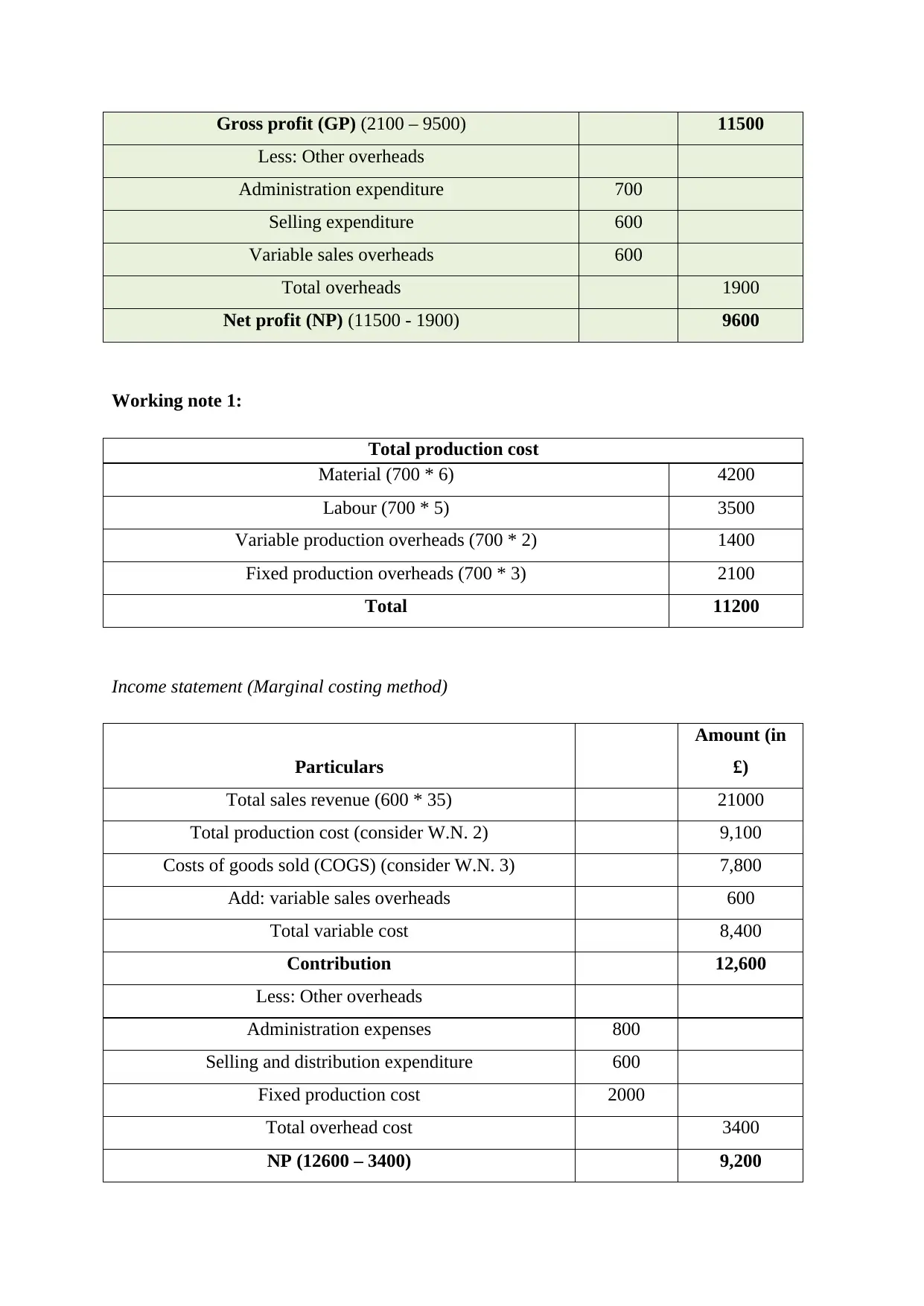

Gross profit (GP) (2100 – 9500) 11500

Less: Other overheads

Administration expenditure 700

Selling expenditure 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (11500 - 1900) 9600

Working note 1:

Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total 11200

Income statement (Marginal costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Total production cost (consider W.N. 2) 9,100

Costs of goods sold (COGS) (consider W.N. 3) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration expenses 800

Selling and distribution expenditure 600

Fixed production cost 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

Less: Other overheads

Administration expenditure 700

Selling expenditure 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (11500 - 1900) 9600

Working note 1:

Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total 11200

Income statement (Marginal costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Total production cost (consider W.N. 2) 9,100

Costs of goods sold (COGS) (consider W.N. 3) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration expenses 800

Selling and distribution expenditure 600

Fixed production cost 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

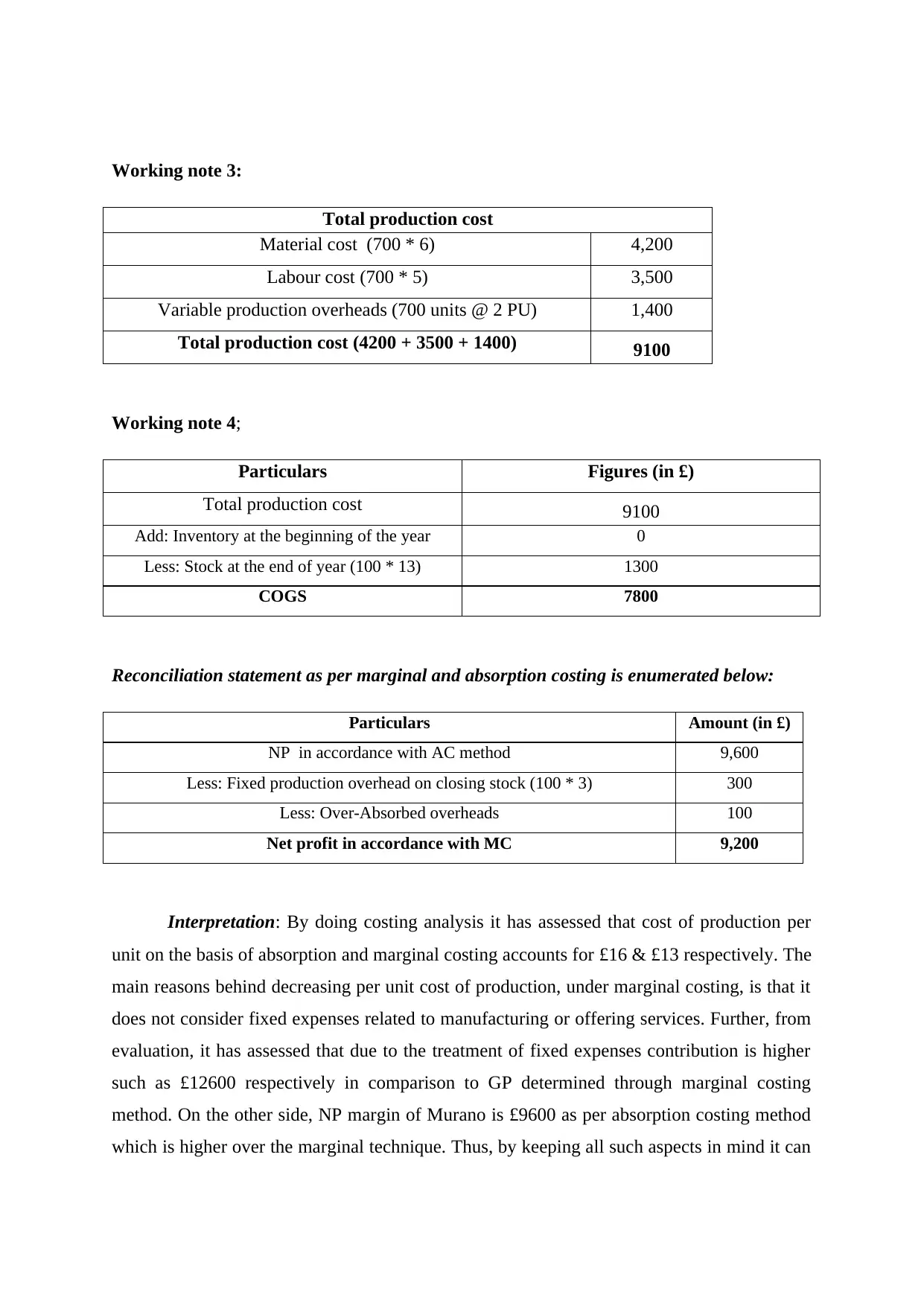

Working note 3:

Total production cost

Material cost (700 * 6) 4,200

Labour cost (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500 + 1400) 9100

Working note 4;

Particulars Figures (in £)

Total production cost 9100

Add: Inventory at the beginning of the year 0

Less: Stock at the end of year (100 * 13) 1300

COGS 7800

Reconciliation statement as per marginal and absorption costing is enumerated below:

Particulars Amount (in £)

NP in accordance with AC method 9,600

Less: Fixed production overhead on closing stock (100 * 3) 300

Less: Over-Absorbed overheads 100

Net profit in accordance with MC 9,200

Interpretation: By doing costing analysis it has assessed that cost of production per

unit on the basis of absorption and marginal costing accounts for £16 & £13 respectively. The

main reasons behind decreasing per unit cost of production, under marginal costing, is that it

does not consider fixed expenses related to manufacturing or offering services. Further, from

evaluation, it has assessed that due to the treatment of fixed expenses contribution is higher

such as £12600 respectively in comparison to GP determined through marginal costing

method. On the other side, NP margin of Murano is £9600 as per absorption costing method

which is higher over the marginal technique. Thus, by keeping all such aspects in mind it can

Total production cost

Material cost (700 * 6) 4,200

Labour cost (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500 + 1400) 9100

Working note 4;

Particulars Figures (in £)

Total production cost 9100

Add: Inventory at the beginning of the year 0

Less: Stock at the end of year (100 * 13) 1300

COGS 7800

Reconciliation statement as per marginal and absorption costing is enumerated below:

Particulars Amount (in £)

NP in accordance with AC method 9,600

Less: Fixed production overhead on closing stock (100 * 3) 300

Less: Over-Absorbed overheads 100

Net profit in accordance with MC 9,200

Interpretation: By doing costing analysis it has assessed that cost of production per

unit on the basis of absorption and marginal costing accounts for £16 & £13 respectively. The

main reasons behind decreasing per unit cost of production, under marginal costing, is that it

does not consider fixed expenses related to manufacturing or offering services. Further, from

evaluation, it has assessed that due to the treatment of fixed expenses contribution is higher

such as £12600 respectively in comparison to GP determined through marginal costing

method. On the other side, NP margin of Murano is £9600 as per absorption costing method

which is higher over the marginal technique. Thus, by keeping all such aspects in mind it can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be depicted that Murano should determine cost and margin by referring the technique of

absorption over others.

P4 Assessing planning tools that are related with management accounting system

Effective planning is the key of organizational growth and has high level of impact on

profitability aspect. On the basis of such aspect, in the absence of having suitable and

competent financial plan Murano might face difficulty in making optimum use of financial

resources. In this regard, there are several methods that Murano restaurant can employ for the

purpose of planning are as follows:

Zero base budgeting: It is recognized as a modern tool of budgeting which helps in

developing realistic monetary framework. Under ZBB, manager starts with zero base which

shows that it completely ignores the past year frameworks. Budget based on this method is

highly realistic in nature because in this every expense in clearly justified. As per this

technique, manager of restaurant unit needs to make focus on assessing each alternative way

of performing activities and thereby includes the cost of same in the plan (Fullerton, Kennedy

and Widener, 2013). Thus, while preparing budget as per ZBB restaurant unit needs to keep

in mind following benefits and drawbacks:

Advantages:

ZBB assists in removing all the redundant activities by presenting the cost effectual

ways of doing activities.

It facilitates efficient allocation of financial resources by laying emphasis on avoiding

historical numbers.

Zero base budgets leads or enhances employee motivation by involving them in the

decision making aspect.

By relooking every item of cash flow manager prepares budget under ZBB and

thereby helps in presenting accurate view of financial aspects.

Disadvantages:

For preparing budget as per ZBB, manager of restaurant unit has to organize training

because without the same it is difficult to explain or justify every line of item.

ZBB is recognized as time consuming process because it demands for in-depth

evaluation.

absorption over others.

P4 Assessing planning tools that are related with management accounting system

Effective planning is the key of organizational growth and has high level of impact on

profitability aspect. On the basis of such aspect, in the absence of having suitable and

competent financial plan Murano might face difficulty in making optimum use of financial

resources. In this regard, there are several methods that Murano restaurant can employ for the

purpose of planning are as follows:

Zero base budgeting: It is recognized as a modern tool of budgeting which helps in

developing realistic monetary framework. Under ZBB, manager starts with zero base which

shows that it completely ignores the past year frameworks. Budget based on this method is

highly realistic in nature because in this every expense in clearly justified. As per this

technique, manager of restaurant unit needs to make focus on assessing each alternative way

of performing activities and thereby includes the cost of same in the plan (Fullerton, Kennedy

and Widener, 2013). Thus, while preparing budget as per ZBB restaurant unit needs to keep

in mind following benefits and drawbacks:

Advantages:

ZBB assists in removing all the redundant activities by presenting the cost effectual

ways of doing activities.

It facilitates efficient allocation of financial resources by laying emphasis on avoiding

historical numbers.

Zero base budgets leads or enhances employee motivation by involving them in the

decision making aspect.

By relooking every item of cash flow manager prepares budget under ZBB and

thereby helps in presenting accurate view of financial aspects.

Disadvantages:

For preparing budget as per ZBB, manager of restaurant unit has to organize training

because without the same it is difficult to explain or justify every line of item.

ZBB is recognized as time consuming process because it demands for in-depth

evaluation.

Further, for preparing budget according to ZBB, involvement of large number of

employees is required. Thus, if a different department of business unit does not have

enough personnel then it might difficulty to prepare budget according to ZBB.

Activity based budgeting: By undertaking ABB technique owner of Murano can ensure

greater transparency in the budget process. On the basis of such modern tool, cost incurred

pertaining to each functional area is recorded. Hence, considering the respective cost driver

emphasis is laid on determining relationship between cost and activity (Messner, 2016).

Thus, by employing such tool business entity of Murano can formulate suitable budget.

Advantages:

ABB facilitates cost reduction by offering meaningful information

It leads proper pricing policy by ensuring optimal allocation of cost to various

products

Gives indication in relation to eliminating unproductive activities and thereby ensures

better performance

Further, ABB provides accurate cost information and helps management team in

employing suitable productivity improvement approaches like TQM, business process

re-engineering etc.

Disadvantages:

Highly time intensive process

Such technique is not suitable for the small sized business units

Along with this, such tool is not suitable for the companies which offer one or few

products

Investment appraisal tools: It includes wide range of tools such as net present value,

payback period, average and internal rate of return that business unit can be undertaken for

evaluating the viability of capital project. Attainment of high profit margin over the

investment is one of the main objectives of business organization. In this regard, by

evaluating cost and benefit of proposal over the foreseeable life manager of the restaurant

unit can assess the level of return (Ax and Greve, 2017). Tool of investment appraisal such as

payback method assists firm in identifying time period within which it will recover initial

investment. Further, ARR method helps in identifying mean return that is associated with the

employees is required. Thus, if a different department of business unit does not have

enough personnel then it might difficulty to prepare budget according to ZBB.

Activity based budgeting: By undertaking ABB technique owner of Murano can ensure

greater transparency in the budget process. On the basis of such modern tool, cost incurred

pertaining to each functional area is recorded. Hence, considering the respective cost driver

emphasis is laid on determining relationship between cost and activity (Messner, 2016).

Thus, by employing such tool business entity of Murano can formulate suitable budget.

Advantages:

ABB facilitates cost reduction by offering meaningful information

It leads proper pricing policy by ensuring optimal allocation of cost to various

products

Gives indication in relation to eliminating unproductive activities and thereby ensures

better performance

Further, ABB provides accurate cost information and helps management team in

employing suitable productivity improvement approaches like TQM, business process

re-engineering etc.

Disadvantages:

Highly time intensive process

Such technique is not suitable for the small sized business units

Along with this, such tool is not suitable for the companies which offer one or few

products

Investment appraisal tools: It includes wide range of tools such as net present value,

payback period, average and internal rate of return that business unit can be undertaken for

evaluating the viability of capital project. Attainment of high profit margin over the

investment is one of the main objectives of business organization. In this regard, by

evaluating cost and benefit of proposal over the foreseeable life manager of the restaurant

unit can assess the level of return (Ax and Greve, 2017). Tool of investment appraisal such as

payback method assists firm in identifying time period within which it will recover initial

investment. Further, ARR method helps in identifying mean return that is associated with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.