Management Accounting Model Assignment, UGB253, Sunderland Uni, Sem 1

VerifiedAdded on 2022/08/12

|19

|4038

|473

Homework Assignment

AI Summary

This assignment delves into the core concepts of management accounting, focusing on marginal and absorption costing methods. It begins by defining and differentiating between these two costing approaches, highlighting their distinct features and applications in inventory valuation and decision-making. The discussion extends to the theoretical criticisms of both marginal and absorption costing, examining their limitations and potential drawbacks. Furthermore, the assignment explores practical problems associated with each costing method and proposes solutions to overcome these challenges. The assignment also covers strategic management accounting, including strategy formulation, vision, mission, objectives, and SWOT analysis. It emphasizes the importance of aligning organizational strengths and weaknesses with opportunities and threats to achieve strategic goals. Overall, the assignment provides a comprehensive overview of management accounting principles and their practical implications in business strategy and operations.

Running head: MANAGEMENT ACCOUNTING MODEL

MANAGEMENT ACCOUNTING MODEL

Name of the Student

Name of the University

Author Note:

MANAGEMENT ACCOUNTING MODEL

Name of the Student

Name of the University

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING MODEL

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Answer to Question 1(a)..................................................................................................................3

Marginal Costing.........................................................................................................................3

Absorption Costing......................................................................................................................4

Underlying difference between marginal and absorption costing approach (Hall, 2018)...........4

Answer to Question 1(b)..................................................................................................................5

Theoretical Criticism of Marginal Costing (Pearce, 2016):........................................................5

Theoretical Criticism of Absorption Costing (Mikaeeli et al., 2015)..........................................6

Answer to Question 1 (C)................................................................................................................8

Practical Problems and ways to overcome problems in Marginal Costing.................................8

Practical Problems and ways to overcome problems in Absorption costing...............................9

Answer to Question 2 (a).................................................................................................................9

Answer to Question 2(b)................................................................................................................11

Answer to Question 2(c)................................................................................................................13

Answer to Question 2(d)................................................................................................................13

Answer to Question 2(e)................................................................................................................15

Answer to Question 3(a)................................................................................................................15

Answer to Question 3(b)................................................................................................................16

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Answer to Question 1(a)..................................................................................................................3

Marginal Costing.........................................................................................................................3

Absorption Costing......................................................................................................................4

Underlying difference between marginal and absorption costing approach (Hall, 2018)...........4

Answer to Question 1(b)..................................................................................................................5

Theoretical Criticism of Marginal Costing (Pearce, 2016):........................................................5

Theoretical Criticism of Absorption Costing (Mikaeeli et al., 2015)..........................................6

Answer to Question 1 (C)................................................................................................................8

Practical Problems and ways to overcome problems in Marginal Costing.................................8

Practical Problems and ways to overcome problems in Absorption costing...............................9

Answer to Question 2 (a).................................................................................................................9

Answer to Question 2(b)................................................................................................................11

Answer to Question 2(c)................................................................................................................13

Answer to Question 2(d)................................................................................................................13

Answer to Question 2(e)................................................................................................................15

Answer to Question 3(a)................................................................................................................15

Answer to Question 3(b)................................................................................................................16

2MANAGEMENT ACCOUNTING MODEL

Conclusion.....................................................................................................................................16

Reference.......................................................................................................................................18

Conclusion.....................................................................................................................................16

Reference.......................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING MODEL

Introduction

Marginal costing and Absorption costing are two diverse types of approaches that are

used in inventory valuation by the company. The variable cost that is incurred by the company is

applied to the inventory under marginal costing whereas in absorption costing fixed as well as

variable costing sustained by the company are applied to the inventory. Therefore, the cost that

varies with a decision must only be involved in the decision-making analysis (Kaplan and

Atkinson, 2015).

Discussion

Answer to Question 1(a)

Marginal Costing

In marginal costing, only variable cost is gauged as the product cost, while the fixed cost

is regarded as the cost for the given period. Marginal costing might be demarcated as the practice

of presenting the cost data where the fixed costs and variable costs are shown distinctly for

managerial decision-making. This process of costing is different from job costing and batch

costing and is rather merely a process of analyzing cost information for the supervision of

management who stabs to figure out the result of profit owing to the change in the volume of

output (Aleem, Khan and Hamad, 2016).

Marginal costing technique has invented new concept of contribution. Contribution can

be derived by reducing the variable cost from the sales revenue is shown as the profit left before

the retrieval of the fixed cost. In case the firm does not make a profit nor suffers a loss, then the

Introduction

Marginal costing and Absorption costing are two diverse types of approaches that are

used in inventory valuation by the company. The variable cost that is incurred by the company is

applied to the inventory under marginal costing whereas in absorption costing fixed as well as

variable costing sustained by the company are applied to the inventory. Therefore, the cost that

varies with a decision must only be involved in the decision-making analysis (Kaplan and

Atkinson, 2015).

Discussion

Answer to Question 1(a)

Marginal Costing

In marginal costing, only variable cost is gauged as the product cost, while the fixed cost

is regarded as the cost for the given period. Marginal costing might be demarcated as the practice

of presenting the cost data where the fixed costs and variable costs are shown distinctly for

managerial decision-making. This process of costing is different from job costing and batch

costing and is rather merely a process of analyzing cost information for the supervision of

management who stabs to figure out the result of profit owing to the change in the volume of

output (Aleem, Khan and Hamad, 2016).

Marginal costing technique has invented new concept of contribution. Contribution can

be derived by reducing the variable cost from the sales revenue is shown as the profit left before

the retrieval of the fixed cost. In case the firm does not make a profit nor suffers a loss, then the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING MODEL

contribution will be equivalent to the fixed cost, which is also recognized as the break-even

point.

Principal of Marginal Costing

By selling an additional item of product or services the revenue will rise by the sales

value per unit, and the cost will upsurge by the variable cost per unit.

If the sales volume reduces, the profit will also decrease by the amount of contribution

from that item.

Fixed cost remains unaffected with an increase or decrease in the production of the item,

as they are bound to incur without any fluctuation.

Absorption Costing

On the other hand, the absorption costing is a method that contemplates both fixed costs

and variable costs as cost of the product. Absorption cost recaptures all the cost associated with

the manufacturing process and includes all the direct and indirect cost incurred, such as rent,

labour insurance and direct material. This method of costing is essential for the reporting

purpose. Two distinctive features of the absorption costing is that fixed factory expenses are

counted in both unit and inventory value (Gersil and Kayal, 2016).

Underlying difference between marginal and absorption costing approach (Hall,

2018).

In marginal costing, the cost of semi-finished and finished product are esteemed at

marginal cost, while in absorption costing, they are valued at the total cost of production.

Henceforth the profit differs under these two methods.

contribution will be equivalent to the fixed cost, which is also recognized as the break-even

point.

Principal of Marginal Costing

By selling an additional item of product or services the revenue will rise by the sales

value per unit, and the cost will upsurge by the variable cost per unit.

If the sales volume reduces, the profit will also decrease by the amount of contribution

from that item.

Fixed cost remains unaffected with an increase or decrease in the production of the item,

as they are bound to incur without any fluctuation.

Absorption Costing

On the other hand, the absorption costing is a method that contemplates both fixed costs

and variable costs as cost of the product. Absorption cost recaptures all the cost associated with

the manufacturing process and includes all the direct and indirect cost incurred, such as rent,

labour insurance and direct material. This method of costing is essential for the reporting

purpose. Two distinctive features of the absorption costing is that fixed factory expenses are

counted in both unit and inventory value (Gersil and Kayal, 2016).

Underlying difference between marginal and absorption costing approach (Hall,

2018).

In marginal costing, the cost of semi-finished and finished product are esteemed at

marginal cost, while in absorption costing, they are valued at the total cost of production.

Henceforth the profit differs under these two methods.

5MANAGEMENT ACCOUNTING MODEL

Marginal costing helps the management to identify variable cost and contribution, and

such cost information helps the management to take an effective decision and also helps

in the budget decision making process.

Under absorption costing, actual cost or fully absorbed unit cost are reduced if the

production quantity increases, whereas in marginal costing, unit variable costing is not

effected by the increase or decrease in the volume of production.

When the closing stock is greater than the opening stock, the profit will be higher in

absorption costing as compared to marginal costing because a higher portion of the fixed

cost is involved in the closing stock which is conceded over to the next year. On the

contrary, the profit will be lower in absorption costing if the opening stock is more than

the closing stock.

Answer to Question 1(b)

Theoretical Criticism of Marginal Costing (Pearce, 2016):

While determining and valuing product cost and inventory, this method neglects the

presence of fixed costs which does not provide an exact decision for the decision-making

process.

Recovery of the asset is important in the long-term of the business. However, the use of

recovering the fixed overhead over the product pricing is overlooked in marginal costing.

While valuing inventory, Income tax authorities does not consider the inventory under

marginal cost. In a real-life scenario, the variability of cost establishment is not an easy

task because the fixed cost is not completely fixed and not completely variable.

Though marginal costing is important in short-term profit planning and decision-making

but for the long term effect, one will be focused on purpose cost.

Marginal costing helps the management to identify variable cost and contribution, and

such cost information helps the management to take an effective decision and also helps

in the budget decision making process.

Under absorption costing, actual cost or fully absorbed unit cost are reduced if the

production quantity increases, whereas in marginal costing, unit variable costing is not

effected by the increase or decrease in the volume of production.

When the closing stock is greater than the opening stock, the profit will be higher in

absorption costing as compared to marginal costing because a higher portion of the fixed

cost is involved in the closing stock which is conceded over to the next year. On the

contrary, the profit will be lower in absorption costing if the opening stock is more than

the closing stock.

Answer to Question 1(b)

Theoretical Criticism of Marginal Costing (Pearce, 2016):

While determining and valuing product cost and inventory, this method neglects the

presence of fixed costs which does not provide an exact decision for the decision-making

process.

Recovery of the asset is important in the long-term of the business. However, the use of

recovering the fixed overhead over the product pricing is overlooked in marginal costing.

While valuing inventory, Income tax authorities does not consider the inventory under

marginal cost. In a real-life scenario, the variability of cost establishment is not an easy

task because the fixed cost is not completely fixed and not completely variable.

Though marginal costing is important in short-term profit planning and decision-making

but for the long term effect, one will be focused on purpose cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING MODEL

Moreover, there is no established accepted accounting practice that allows eliminating

fixed cost from the inventory valuation

Theoretical Criticism of Absorption Costing (Mikaeeli et al., 2015)

The problem with the absorption costing is that the behavioural pattern of cost is not

highlighted and thereby, many situations go unnoticed, which can be utilized under

marginal costing.

Absorption costing buries the relationship of cost volume profit as a large share of fixed

overhead is assigned to the product cost under absorption costing for the decision-

making process.

The fixed overhead lying in the closing stock is charged in the next year’s opening stock

which is an unsound practice.

The absorption costing method uses random method of cost distribution for controlling

purpose that the practical utility of the cost data is reduced.

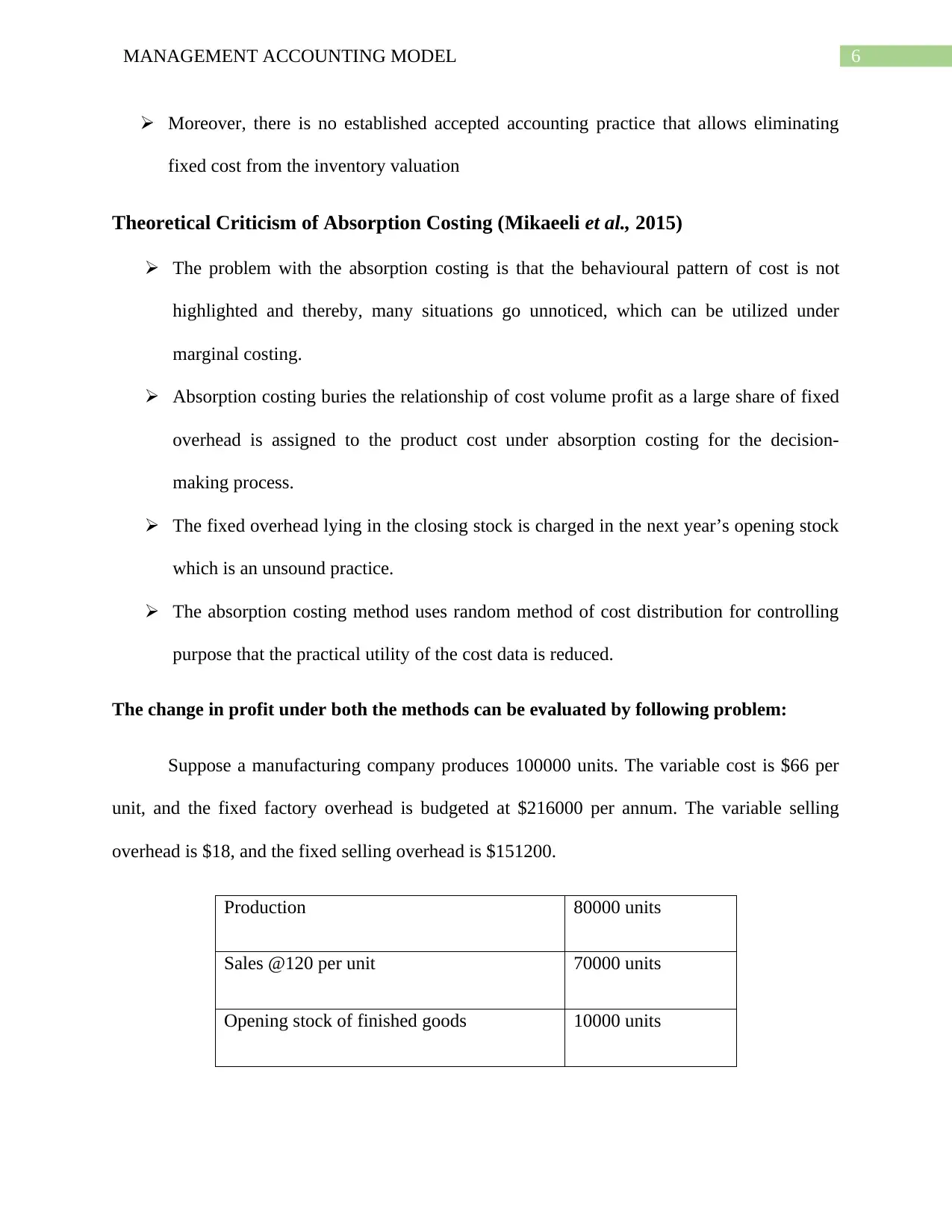

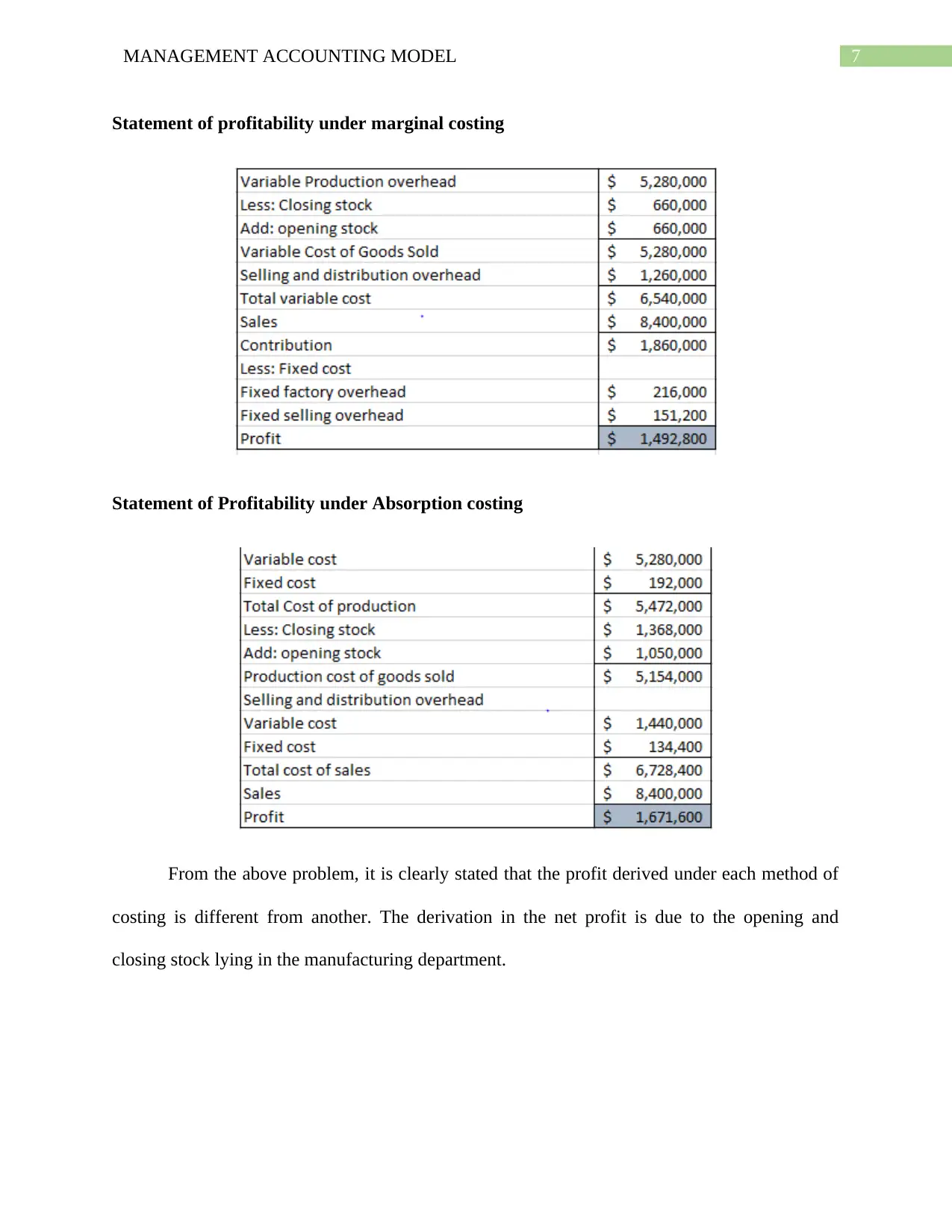

The change in profit under both the methods can be evaluated by following problem:

Suppose a manufacturing company produces 100000 units. The variable cost is $66 per

unit, and the fixed factory overhead is budgeted at $216000 per annum. The variable selling

overhead is $18, and the fixed selling overhead is $151200.

Production 80000 units

Sales @120 per unit 70000 units

Opening stock of finished goods 10000 units

Moreover, there is no established accepted accounting practice that allows eliminating

fixed cost from the inventory valuation

Theoretical Criticism of Absorption Costing (Mikaeeli et al., 2015)

The problem with the absorption costing is that the behavioural pattern of cost is not

highlighted and thereby, many situations go unnoticed, which can be utilized under

marginal costing.

Absorption costing buries the relationship of cost volume profit as a large share of fixed

overhead is assigned to the product cost under absorption costing for the decision-

making process.

The fixed overhead lying in the closing stock is charged in the next year’s opening stock

which is an unsound practice.

The absorption costing method uses random method of cost distribution for controlling

purpose that the practical utility of the cost data is reduced.

The change in profit under both the methods can be evaluated by following problem:

Suppose a manufacturing company produces 100000 units. The variable cost is $66 per

unit, and the fixed factory overhead is budgeted at $216000 per annum. The variable selling

overhead is $18, and the fixed selling overhead is $151200.

Production 80000 units

Sales @120 per unit 70000 units

Opening stock of finished goods 10000 units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING MODEL

Statement of profitability under marginal costing

Statement of Profitability under Absorption costing

From the above problem, it is clearly stated that the profit derived under each method of

costing is different from another. The derivation in the net profit is due to the opening and

closing stock lying in the manufacturing department.

Statement of profitability under marginal costing

Statement of Profitability under Absorption costing

From the above problem, it is clearly stated that the profit derived under each method of

costing is different from another. The derivation in the net profit is due to the opening and

closing stock lying in the manufacturing department.

8MANAGEMENT ACCOUNTING MODEL

Answer to Question 1 (C)

Practical Problems and ways to overcome problems in Marginal Costing

1) Fixation of the selling price: The marginal cost represents the minimum price for the

product. It may sometimes happen that the management may set any price that is below

the cost price and may suffer losses (Flannery, 2017). Therefore, fixation of such price of

the product is necessary so that variable cost is covered and contribution towards fixed

overhead is also done. This could be done by marginal costing if the cost and the desired

profit the manufacturing company wants to achieve is known.

2) Problems related to sustaining a desired level of profit: The contribution per unit reduces

when the industry has to cut its price from time to time due to various government

regulation or on account of competition or some other reasons. Therefore, the

manufacturing company may fail to maintain the desired level of profit (Storey et al.,

2016). The desired level of profit can be achieved through marginal costing if the demand

for the product is elastic. Similarly, the profit can be increased by increasing the volume

of sales, and the volume of sales can be derived from the marginal costing method.

Practical Problems and ways to overcome problems in Absorption costing

1) Difficult to compare product lines: It is difficult to compare the profits of different

product lines in the practical life since this costing technique takes into account indirect

cost which is not related to the production (Dees and Anderson, 2017). To overcome such

problem management must ensure that expenses related to or which is incurred

exclusively other than manufacturing the product are excluded.

2) Skewing of profit: This is a major flaw of absorption costing and can potentially mislead

the investors. Unless the product is sold, related fixed expenses are not deducted from the

Answer to Question 1 (C)

Practical Problems and ways to overcome problems in Marginal Costing

1) Fixation of the selling price: The marginal cost represents the minimum price for the

product. It may sometimes happen that the management may set any price that is below

the cost price and may suffer losses (Flannery, 2017). Therefore, fixation of such price of

the product is necessary so that variable cost is covered and contribution towards fixed

overhead is also done. This could be done by marginal costing if the cost and the desired

profit the manufacturing company wants to achieve is known.

2) Problems related to sustaining a desired level of profit: The contribution per unit reduces

when the industry has to cut its price from time to time due to various government

regulation or on account of competition or some other reasons. Therefore, the

manufacturing company may fail to maintain the desired level of profit (Storey et al.,

2016). The desired level of profit can be achieved through marginal costing if the demand

for the product is elastic. Similarly, the profit can be increased by increasing the volume

of sales, and the volume of sales can be derived from the marginal costing method.

Practical Problems and ways to overcome problems in Absorption costing

1) Difficult to compare product lines: It is difficult to compare the profits of different

product lines in the practical life since this costing technique takes into account indirect

cost which is not related to the production (Dees and Anderson, 2017). To overcome such

problem management must ensure that expenses related to or which is incurred

exclusively other than manufacturing the product are excluded.

2) Skewing of profit: This is a major flaw of absorption costing and can potentially mislead

the investors. Unless the product is sold, related fixed expenses are not deducted from the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING MODEL

revenues, which mislead the profit of the company. To overcome such default

management must charge fixed expenses in the year of occurrence irrespective of

whether the product is sold or not.

Answer to Question 2 (a)

The necessary elements and concepts required to develop a strategy for an organization to

achieve its objective is identified in the strategic management model. The strategic management

accounting, on the other hand, is the provision and examination of the management accounting

data which is used in the monitoring and implementing changes in the strategy of the business

(Oboh and Ajibolade, 2017).

Strategy formulation is the most important step of the strategic management model. Such

strategy formulation includes developing mission, vision, objectives and goals of the company

and this step is considered as a path forming step as it provides a route to the organisation for

future movements (Rothaermel, 2016).

Vision is a future statement that enunciates the basic characteristics that figures the

organisation strategy. It indicates where the organisation is headed and what it intends to be. It

provides a roadmap to the company regarding the future and suggests the kind of company

management is trying to create for the future.

The purpose and mission of the strategic management of an organisation is an enduring

general statement that infers the image which the organisation seeks to project, and it also

includes the decision-making philosophy of the business (Bryce, 2017). The guidelines for the

formulation of the mission statement may include that the profit-making will not be the sole

mission, and it must include the interest of customer and society. The mission and purpose

revenues, which mislead the profit of the company. To overcome such default

management must charge fixed expenses in the year of occurrence irrespective of

whether the product is sold or not.

Answer to Question 2 (a)

The necessary elements and concepts required to develop a strategy for an organization to

achieve its objective is identified in the strategic management model. The strategic management

accounting, on the other hand, is the provision and examination of the management accounting

data which is used in the monitoring and implementing changes in the strategy of the business

(Oboh and Ajibolade, 2017).

Strategy formulation is the most important step of the strategic management model. Such

strategy formulation includes developing mission, vision, objectives and goals of the company

and this step is considered as a path forming step as it provides a route to the organisation for

future movements (Rothaermel, 2016).

Vision is a future statement that enunciates the basic characteristics that figures the

organisation strategy. It indicates where the organisation is headed and what it intends to be. It

provides a roadmap to the company regarding the future and suggests the kind of company

management is trying to create for the future.

The purpose and mission of the strategic management of an organisation is an enduring

general statement that infers the image which the organisation seeks to project, and it also

includes the decision-making philosophy of the business (Bryce, 2017). The guidelines for the

formulation of the mission statement may include that the profit-making will not be the sole

mission, and it must include the interest of customer and society. The mission and purpose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING MODEL

usually consist of a long-term vision that the organization wants to achieve and which is within

the logical extension of the business capabilities.

Strategic planning includes objectives and achieving, which fulfils the existence of the

organisation. The objective must be time-framed, focused, specific and measurable. The

objectives are the performance target which the organization wants to achieve within a specified

period, and it can be long-term as well as short-term. A formal strategy comprises three

elements:

Desired goals to be achieved.

The policies that guide and limits the action.

Action structure required to achieve the goals.

Answer to Question 2(b)

The corporate mission and vision and objectives examine both weakness and strength of

the corporate. To formulate a good plan, a balance and mix of both organisational strength and

weakness are analysed to achieve the entity’s objective during a period (Jenkins and Williamson,

2015). Opportunities and threats are external factors that may impact the company’s

performance. The SWOT analysis seeks to isolate the major issues faced by an organization

through careful analysis which a manager can use to formulate strategy:

With a high professional-managerial group including directors and chief executive and an

environment existing that provides job commitment improves the corporate teamwork and

provides the following strengths:

Good Infrastructure;

Technologically rich along with expertise;

usually consist of a long-term vision that the organization wants to achieve and which is within

the logical extension of the business capabilities.

Strategic planning includes objectives and achieving, which fulfils the existence of the

organisation. The objective must be time-framed, focused, specific and measurable. The

objectives are the performance target which the organization wants to achieve within a specified

period, and it can be long-term as well as short-term. A formal strategy comprises three

elements:

Desired goals to be achieved.

The policies that guide and limits the action.

Action structure required to achieve the goals.

Answer to Question 2(b)

The corporate mission and vision and objectives examine both weakness and strength of

the corporate. To formulate a good plan, a balance and mix of both organisational strength and

weakness are analysed to achieve the entity’s objective during a period (Jenkins and Williamson,

2015). Opportunities and threats are external factors that may impact the company’s

performance. The SWOT analysis seeks to isolate the major issues faced by an organization

through careful analysis which a manager can use to formulate strategy:

With a high professional-managerial group including directors and chief executive and an

environment existing that provides job commitment improves the corporate teamwork and

provides the following strengths:

Good Infrastructure;

Technologically rich along with expertise;

11MANAGEMENT ACCOUNTING MODEL

Good relation with the departments of the government;

No political interference;

Financially very sound;

Full capacity utilisation

Strengths and weakness goes hand in hand, therefore corporate strength is always accompanied

by weakness:

Under-utilisation of the resources due to economic slump;

Poor product-mix;

Technology gap;

Lack of managerial strengths;

When an opportunity is timely used and availed then the organization gains. Such opportunities

can be as follows:

Seasonal or climatical demand for the product;

Exploring and penetrating rural markets;

Opportunities for merger and acquisition;

Exploring under-developed and developing markets;

The liberalized policy of the government.

Examination of prevailing threats is necessary and necessary action needs to be taken in order to

solve these threats prudently. These threats can be:

Competition;

Globalisation;

Political instability;

Good relation with the departments of the government;

No political interference;

Financially very sound;

Full capacity utilisation

Strengths and weakness goes hand in hand, therefore corporate strength is always accompanied

by weakness:

Under-utilisation of the resources due to economic slump;

Poor product-mix;

Technology gap;

Lack of managerial strengths;

When an opportunity is timely used and availed then the organization gains. Such opportunities

can be as follows:

Seasonal or climatical demand for the product;

Exploring and penetrating rural markets;

Opportunities for merger and acquisition;

Exploring under-developed and developing markets;

The liberalized policy of the government.

Examination of prevailing threats is necessary and necessary action needs to be taken in order to

solve these threats prudently. These threats can be:

Competition;

Globalisation;

Political instability;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.