Detailed Analysis of Management Accounting: ABC Costing System

VerifiedAdded on 2019/11/08

|16

|2572

|171

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of management accounting, specifically focusing on the Activity-Based Costing (ABC) system and its comparison to the conventional method. The assignment explores various aspects, including the calculation of selling prices using both methods, highlighting how ABC costing leads to different product pricing compared to the traditional approach. It delves into the allocation of overhead costs, emphasizing the use of direct labor hours in the conventional method versus cost pools and activity-based drivers in ABC. The paper further discusses the mispricing of products under traditional costing and the advantages of implementing ABC, such as accurate cost calculation, identification of inefficient activities, and improved decision-making. The assignment also outlines the disadvantages of the ABC system, including the complexity of selecting cost drivers and the high implementation costs. Finally, it underscores the importance of overcoming barriers to the adoption of ABC, such as the need for education and organizational change. The assignment references several academic sources to support its findings.

Running head: INTRODUCTION TO MANAGEMENT ACCOUNTING

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Introduction to Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTRODUCTION TO MANAGEMENT ACCOUNTING

Table of Contents

Requirement a:.................................................................................................................................2

Requirement b:.................................................................................................................................2

Requirement c:.................................................................................................................................3

Requirement d:.................................................................................................................................4

Requirement e:.................................................................................................................................4

Requirement f:.................................................................................................................................6

Requirement g:.................................................................................................................................9

Reference & Bibliography:............................................................................................................13

Table of Contents

Requirement a:.................................................................................................................................2

Requirement b:.................................................................................................................................2

Requirement c:.................................................................................................................................3

Requirement d:.................................................................................................................................4

Requirement e:.................................................................................................................................4

Requirement f:.................................................................................................................................6

Requirement g:.................................................................................................................................9

Reference & Bibliography:............................................................................................................13

2INTRODUCTION TO MANAGEMENT ACCOUNTING

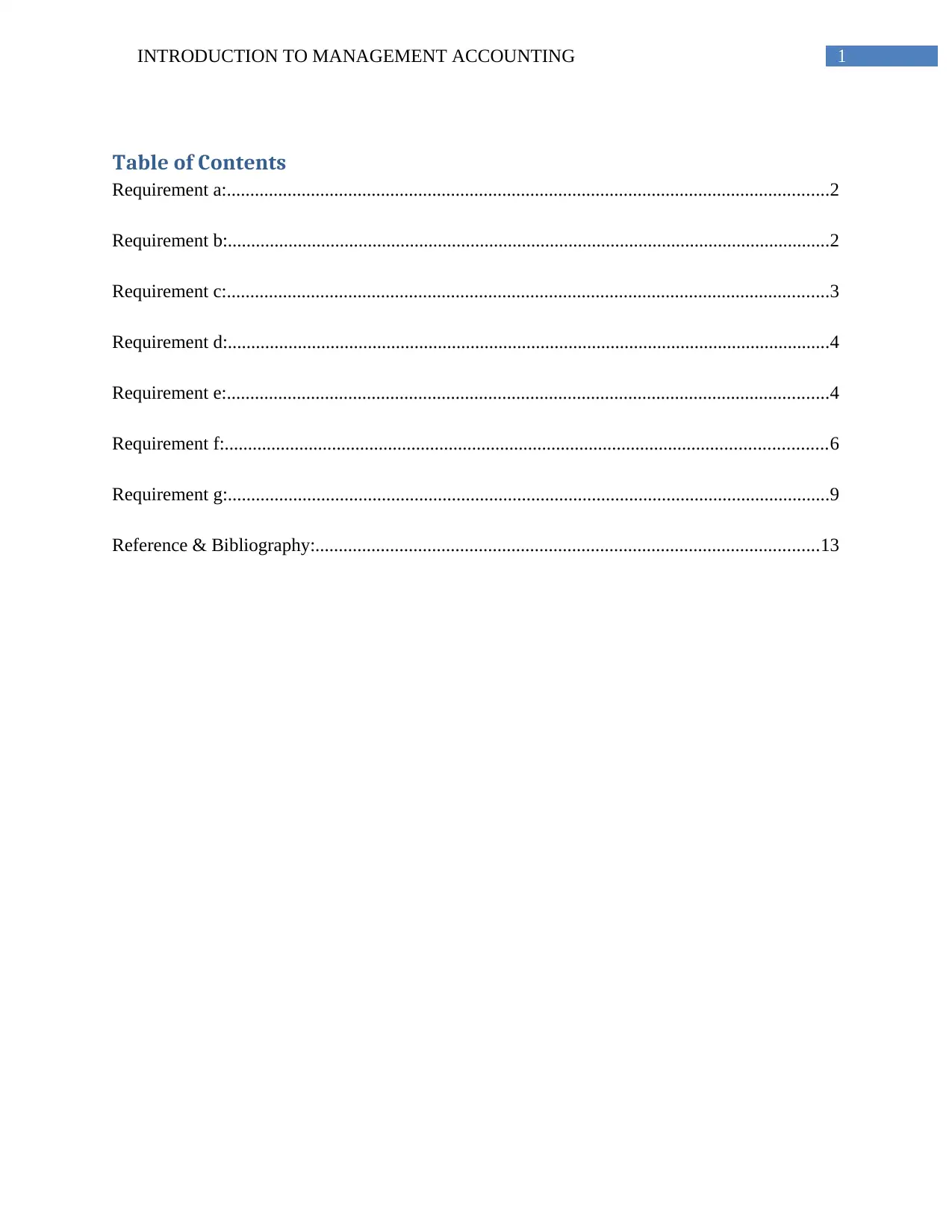

Requirement a:

Requirement b:

Requirement a:

Requirement b:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTRODUCTION TO MANAGEMENT ACCOUNTING

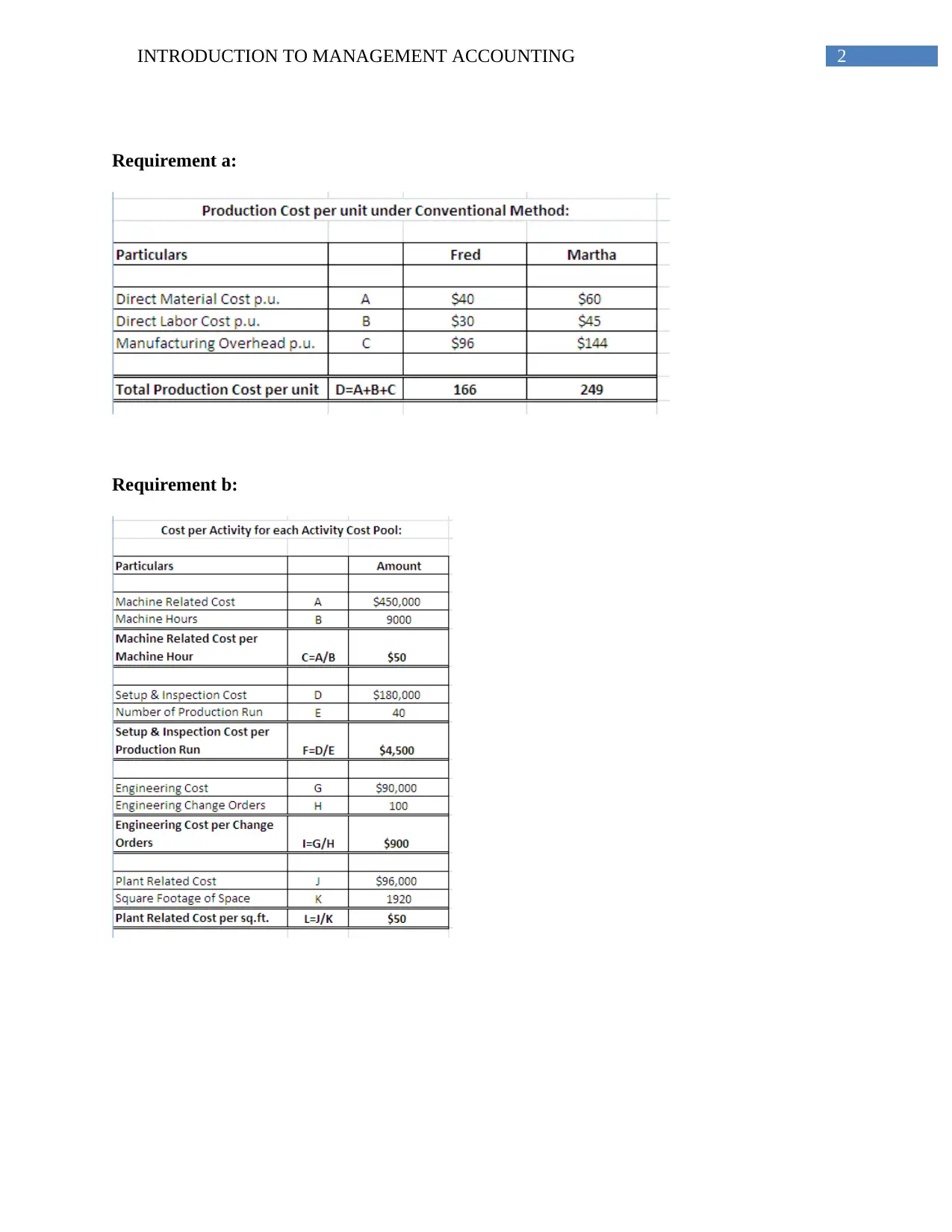

Requirement c:

Workings:

Requirement c:

Workings:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTRODUCTION TO MANAGEMENT ACCOUNTING

Particulars Fred Martha Total

Production Quantity (in units) A 1000 5000 6000

A1 A2 A3=A1+A2

Machine Hours B 4 1 5

B1 B2 B3=B1+B2

Total Machine Hours C 4000 5000 9000

C1=A1xB1 C2=A2xB2 C3=C1+C2

Machine related Cost per

Machine Hours D $50 $50 $50

Total Machine Related Cost E $200,000 $250,000 $450,000

E1=C1xD E2=C2xD E3=C3xD

Units per Production Run F 50 250

F1 F2

Total Production Run G 20 20 40

G1=A1/F1 G2=A2/F2 G3=G1+G2

Setup & Inspection Cost per

Production Run H $4,500 $4,500 $4,500

Total Setup & Inspection Cost I $90,000 $90,000 $180,000

I1=G1xH I2=G2xH I3=G3xH

Engineering Change Orders J 75 25 100

J1=J3x(3/4) J2=J3-J1 J3

Engineering Cost per Change

Orders K $900 $900 $900

Total Engineering Cost L $67,500 $22,500 $90,000

L1=J1xK L2=J2xK L3=J3xK

Total Square Foot of Space M 1536 384 1920

M1=M3x80% M2=M3-M1 M3

Plant Related Cost per sq.ft. N $50 $50 $50

Total Plant Related Cost O $76,800 $19,200 $96,000

O1=M1xN O2=M2xN O3=O1+O2

Total Manufacturing Overhead P $434,300 $381,700 $816,000

P1=E1+G1+L1+O1 P2=E2+G2+L2+O2 P3=E3+G3+L3+O3

Manufacturing Overhead p.u. Q $434 $76

Q1=P1/A1 Q2=P2/A2

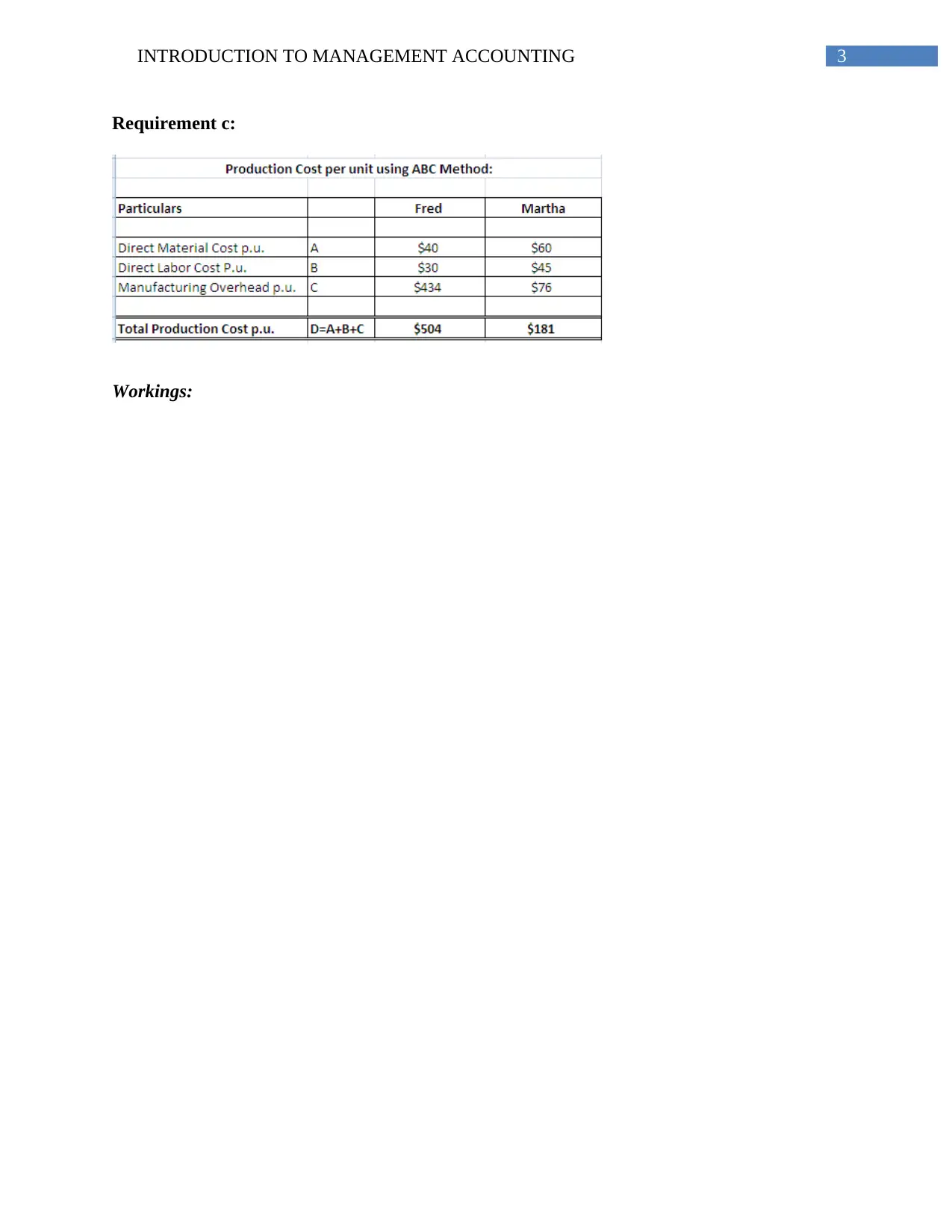

Calculation of Manufacturing Overhead per unit under ABC Method:

Particulars Fred Martha Total

Production Quantity (in units) A 1000 5000 6000

A1 A2 A3=A1+A2

Machine Hours B 4 1 5

B1 B2 B3=B1+B2

Total Machine Hours C 4000 5000 9000

C1=A1xB1 C2=A2xB2 C3=C1+C2

Machine related Cost per

Machine Hours D $50 $50 $50

Total Machine Related Cost E $200,000 $250,000 $450,000

E1=C1xD E2=C2xD E3=C3xD

Units per Production Run F 50 250

F1 F2

Total Production Run G 20 20 40

G1=A1/F1 G2=A2/F2 G3=G1+G2

Setup & Inspection Cost per

Production Run H $4,500 $4,500 $4,500

Total Setup & Inspection Cost I $90,000 $90,000 $180,000

I1=G1xH I2=G2xH I3=G3xH

Engineering Change Orders J 75 25 100

J1=J3x(3/4) J2=J3-J1 J3

Engineering Cost per Change

Orders K $900 $900 $900

Total Engineering Cost L $67,500 $22,500 $90,000

L1=J1xK L2=J2xK L3=J3xK

Total Square Foot of Space M 1536 384 1920

M1=M3x80% M2=M3-M1 M3

Plant Related Cost per sq.ft. N $50 $50 $50

Total Plant Related Cost O $76,800 $19,200 $96,000

O1=M1xN O2=M2xN O3=O1+O2

Total Manufacturing Overhead P $434,300 $381,700 $816,000

P1=E1+G1+L1+O1 P2=E2+G2+L2+O2 P3=E3+G3+L3+O3

Manufacturing Overhead p.u. Q $434 $76

Q1=P1/A1 Q2=P2/A2

Calculation of Manufacturing Overhead per unit under ABC Method:

5INTRODUCTION TO MANAGEMENT ACCOUNTING

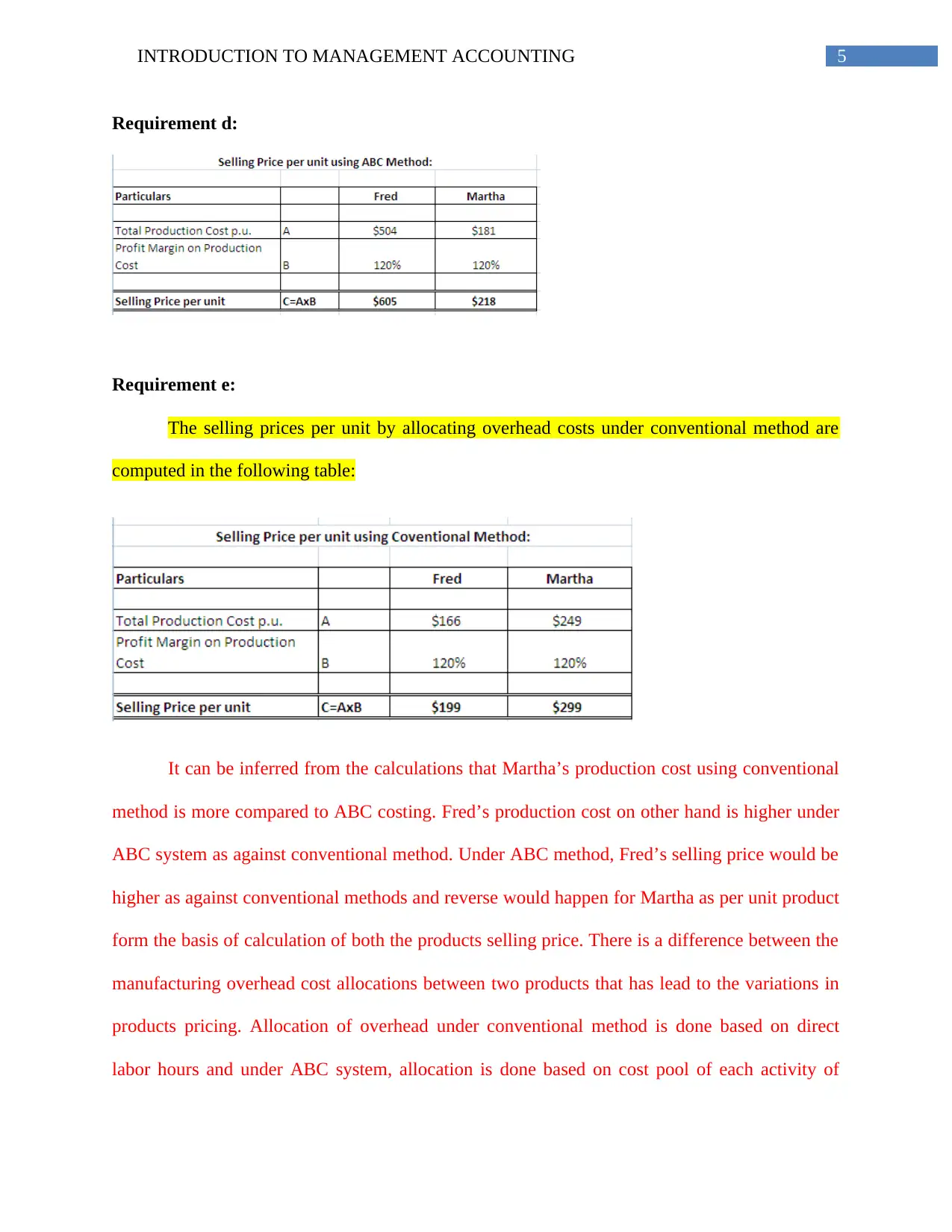

Requirement d:

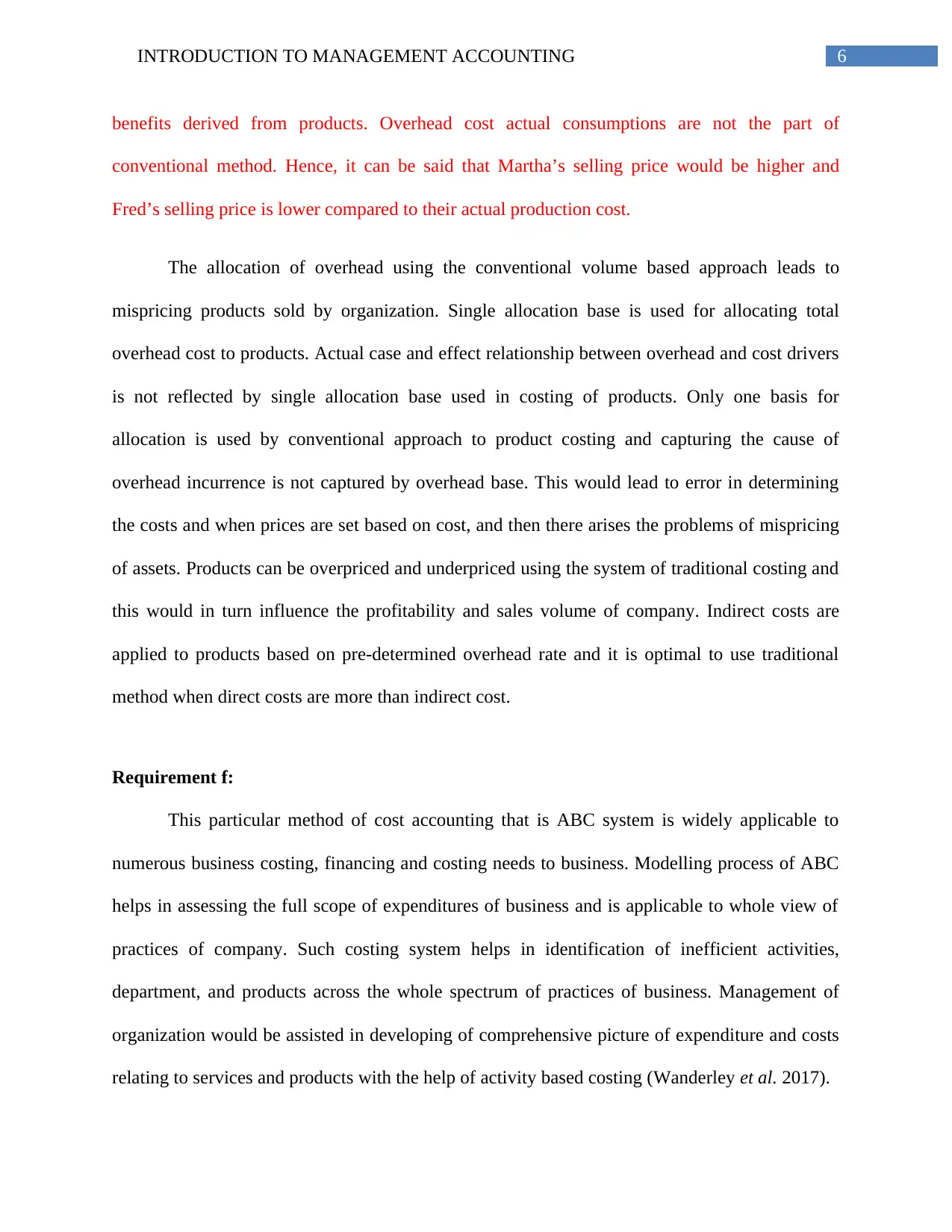

Requirement e:

The selling prices per unit by allocating overhead costs under conventional method are

computed in the following table:

It can be inferred from the calculations that Martha’s production cost using conventional

method is more compared to ABC costing. Fred’s production cost on other hand is higher under

ABC system as against conventional method. Under ABC method, Fred’s selling price would be

higher as against conventional methods and reverse would happen for Martha as per unit product

form the basis of calculation of both the products selling price. There is a difference between the

manufacturing overhead cost allocations between two products that has lead to the variations in

products pricing. Allocation of overhead under conventional method is done based on direct

labor hours and under ABC system, allocation is done based on cost pool of each activity of

Requirement d:

Requirement e:

The selling prices per unit by allocating overhead costs under conventional method are

computed in the following table:

It can be inferred from the calculations that Martha’s production cost using conventional

method is more compared to ABC costing. Fred’s production cost on other hand is higher under

ABC system as against conventional method. Under ABC method, Fred’s selling price would be

higher as against conventional methods and reverse would happen for Martha as per unit product

form the basis of calculation of both the products selling price. There is a difference between the

manufacturing overhead cost allocations between two products that has lead to the variations in

products pricing. Allocation of overhead under conventional method is done based on direct

labor hours and under ABC system, allocation is done based on cost pool of each activity of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTRODUCTION TO MANAGEMENT ACCOUNTING

benefits derived from products. Overhead cost actual consumptions are not the part of

conventional method. Hence, it can be said that Martha’s selling price would be higher and

Fred’s selling price is lower compared to their actual production cost.

The allocation of overhead using the conventional volume based approach leads to

mispricing products sold by organization. Single allocation base is used for allocating total

overhead cost to products. Actual case and effect relationship between overhead and cost drivers

is not reflected by single allocation base used in costing of products. Only one basis for

allocation is used by conventional approach to product costing and capturing the cause of

overhead incurrence is not captured by overhead base. This would lead to error in determining

the costs and when prices are set based on cost, and then there arises the problems of mispricing

of assets. Products can be overpriced and underpriced using the system of traditional costing and

this would in turn influence the profitability and sales volume of company. Indirect costs are

applied to products based on pre-determined overhead rate and it is optimal to use traditional

method when direct costs are more than indirect cost.

Requirement f:

This particular method of cost accounting that is ABC system is widely applicable to

numerous business costing, financing and costing needs to business. Modelling process of ABC

helps in assessing the full scope of expenditures of business and is applicable to whole view of

practices of company. Such costing system helps in identification of inefficient activities,

department, and products across the whole spectrum of practices of business. Management of

organization would be assisted in developing of comprehensive picture of expenditure and costs

relating to services and products with the help of activity based costing (Wanderley et al. 2017).

benefits derived from products. Overhead cost actual consumptions are not the part of

conventional method. Hence, it can be said that Martha’s selling price would be higher and

Fred’s selling price is lower compared to their actual production cost.

The allocation of overhead using the conventional volume based approach leads to

mispricing products sold by organization. Single allocation base is used for allocating total

overhead cost to products. Actual case and effect relationship between overhead and cost drivers

is not reflected by single allocation base used in costing of products. Only one basis for

allocation is used by conventional approach to product costing and capturing the cause of

overhead incurrence is not captured by overhead base. This would lead to error in determining

the costs and when prices are set based on cost, and then there arises the problems of mispricing

of assets. Products can be overpriced and underpriced using the system of traditional costing and

this would in turn influence the profitability and sales volume of company. Indirect costs are

applied to products based on pre-determined overhead rate and it is optimal to use traditional

method when direct costs are more than indirect cost.

Requirement f:

This particular method of cost accounting that is ABC system is widely applicable to

numerous business costing, financing and costing needs to business. Modelling process of ABC

helps in assessing the full scope of expenditures of business and is applicable to whole view of

practices of company. Such costing system helps in identification of inefficient activities,

department, and products across the whole spectrum of practices of business. Management of

organization would be assisted in developing of comprehensive picture of expenditure and costs

relating to services and products with the help of activity based costing (Wanderley et al. 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTRODUCTION TO MANAGEMENT ACCOUNTING

Implementation of ABC system would provide an organization with the listed advantages

and they are as follows:

- ABC system provided company with the facility of accurately calculating cost of

production by establishing cause and effect relationship with each activity.

- Ascertaining and elimination of extraneous cost through the employment of ABC system

would help in increasing efficiency of business. It also helps in controlling the

distribution of resources at any product level and identifying places that would support

unprofitable areas of business.

- Such cost that does not contribute to adding value to business can be understood by ABC

system as it helps in understating different business behavior costs.

- Performance appraisal process and cost management department receives assistance from

the ABC system as it helps in recognition of cost drivers.

- It deals with the identification of reason for incurring of costs and the cost pool activities

have proper control through the implementation of such system and thereby reducing cost

and providing assistance to management.

- The cost of products will be accurately determined by employing the system of activity

based costing that helps in bringing reliability and accuracy and emphasizing on cause

and effect relationship in incurrence of cost. It helps in recognition of the fact that

activities consume products and activities that are responsible for incurring of costs.

- The real nature of cost behavior is identified by implementing ABC system along with

activities that does not help in adding value to products and cost reduction. An

organization experience increase in fixed overhead cost due to many activities and

Implementation of ABC system would provide an organization with the listed advantages

and they are as follows:

- ABC system provided company with the facility of accurately calculating cost of

production by establishing cause and effect relationship with each activity.

- Ascertaining and elimination of extraneous cost through the employment of ABC system

would help in increasing efficiency of business. It also helps in controlling the

distribution of resources at any product level and identifying places that would support

unprofitable areas of business.

- Such cost that does not contribute to adding value to business can be understood by ABC

system as it helps in understating different business behavior costs.

- Performance appraisal process and cost management department receives assistance from

the ABC system as it helps in recognition of cost drivers.

- It deals with the identification of reason for incurring of costs and the cost pool activities

have proper control through the implementation of such system and thereby reducing cost

and providing assistance to management.

- The cost of products will be accurately determined by employing the system of activity

based costing that helps in bringing reliability and accuracy and emphasizing on cause

and effect relationship in incurrence of cost. It helps in recognition of the fact that

activities consume products and activities that are responsible for incurring of costs.

- The real nature of cost behavior is identified by implementing ABC system along with

activities that does not help in adding value to products and cost reduction. An

organization experience increase in fixed overhead cost due to many activities and

8INTRODUCTION TO MANAGEMENT ACCOUNTING

managers are able to exercise control over such activities and thereby reducing fixed

overhead costs. Reason is attributable to the fact that it become possible for management

to identify the behaviors and activities that results in rising overhead costs becomes clear

and visible (Groot and Selto 2013).

- There exists greater diversity among the products that are manufactured such as high

volume products, low volume products. In such event, correct and reliable product cost

data produces by implementing the system of ABC costing. On other hand using

traditional method of costing, make use of arbitrary absorption and apportionment

methods that is likely to bring approximation and errors in determining cost of products

(Quinn 2014).

- Relevant and useful information are provided to the management of organization with the

help of ABC system and performance appraisal of responsibility centers. Information on

transaction volume and rate of cost drivers are provided by such system. Rate of cost

drivers can be advantageously used for designing existing and new products as costing of

products include the overhead costs (Anderson et al. 2015).

- Multiple cost drivers are used by ABC costing and rather than product based they are

based on transaction. Overhead cost to products are traced as the system is concerned

beyond and within the activities.

- The cost of products and data becomes readily available as ABC system usefully helps in

fixation of products selling prices.

- Decision making by managers is improved as the system of ABC helps in employing

reliable cost product data.

managers are able to exercise control over such activities and thereby reducing fixed

overhead costs. Reason is attributable to the fact that it become possible for management

to identify the behaviors and activities that results in rising overhead costs becomes clear

and visible (Groot and Selto 2013).

- There exists greater diversity among the products that are manufactured such as high

volume products, low volume products. In such event, correct and reliable product cost

data produces by implementing the system of ABC costing. On other hand using

traditional method of costing, make use of arbitrary absorption and apportionment

methods that is likely to bring approximation and errors in determining cost of products

(Quinn 2014).

- Relevant and useful information are provided to the management of organization with the

help of ABC system and performance appraisal of responsibility centers. Information on

transaction volume and rate of cost drivers are provided by such system. Rate of cost

drivers can be advantageously used for designing existing and new products as costing of

products include the overhead costs (Anderson et al. 2015).

- Multiple cost drivers are used by ABC costing and rather than product based they are

based on transaction. Overhead cost to products are traced as the system is concerned

beyond and within the activities.

- The cost of products and data becomes readily available as ABC system usefully helps in

fixation of products selling prices.

- Decision making by managers is improved as the system of ABC helps in employing

reliable cost product data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTRODUCTION TO MANAGEMENT ACCOUNTING

- Costs of products are managed by the mechanisms provided by ABC system along with

providing the base for calculating the cost of products more accurately.

- Besides tracing the cost of products, employment of ABC system helps in tracing cost in

other areas of organization such as process, areas of managers’ responsibility,

departments and customers.

- Management can be convinced to take steps for sustaining in competitive environment

with the help of an assessment provided by ABC system. This would enable them reduce

the cost of products while focusing on improving the quality of products. Such system

would help in analyzing the process of manufacturing, the cost associated with it,and this

helps in stimulating the organizing process activities, reducing costs (Soin and Collier

2013).

- Transparent system of ABC would help in determining which costs are relevant and areas

of irrelevant cost can be identified and eliminated (Bromwich and Scapens 2016).

- There can be accurate analysis of volume of production by management with an

improved cost analysis that is needed to achieve break even on products of low volume.

Analysis of activity would help in continuously improving the support by providing

corrective actions against less efficient and non-value added activities. This is closely

related to the productivity problems of organization.

- Growth of non-product factory activity is growing in the manufacturing sector and

overhead factory cost can be traced using the system of ABC. Since there can be tracking

of activity leading non-factor cost, analysis of system of SBC cost pays attention to all

such aspects.

- Costs of products are managed by the mechanisms provided by ABC system along with

providing the base for calculating the cost of products more accurately.

- Besides tracing the cost of products, employment of ABC system helps in tracing cost in

other areas of organization such as process, areas of managers’ responsibility,

departments and customers.

- Management can be convinced to take steps for sustaining in competitive environment

with the help of an assessment provided by ABC system. This would enable them reduce

the cost of products while focusing on improving the quality of products. Such system

would help in analyzing the process of manufacturing, the cost associated with it,and this

helps in stimulating the organizing process activities, reducing costs (Soin and Collier

2013).

- Transparent system of ABC would help in determining which costs are relevant and areas

of irrelevant cost can be identified and eliminated (Bromwich and Scapens 2016).

- There can be accurate analysis of volume of production by management with an

improved cost analysis that is needed to achieve break even on products of low volume.

Analysis of activity would help in continuously improving the support by providing

corrective actions against less efficient and non-value added activities. This is closely

related to the productivity problems of organization.

- Growth of non-product factory activity is growing in the manufacturing sector and

overhead factory cost can be traced using the system of ABC. Since there can be tracking

of activity leading non-factor cost, analysis of system of SBC cost pays attention to all

such aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTRODUCTION TO MANAGEMENT ACCOUNTING

Requirement g:

ABC system comes with some disadvantages that are listed below:

- One of the complications of ABC system is related to appropriate cost driver selection for

each cost of overhead.

- Employment of ABC system is not suitable for small manufacturing organizations and

evaluating costs based on activities is difficult. An activity that influences the overall

costs is also difficult to identify.

- An organization manufacturing few products are not capable of deriving benefits from

ABC system as it is beneficial to organization that producing multiple products.

- ABC system is not affordable to small enterprises as it involves huge expenses.

- System of ABC is more complex compared to traditional product costing system as the

former employs multiple cost drivers and several cost pool.

- Some of aspects of activity based costing that can act as road blocking for firms involves

subsequent running cost and capital expenditure involved in running the system.

- Reports prepared by organization for internal and external purposes require using

traditional as well as system of activity based costing. This is so because system of

activity based costing do not comply with General accepted accounting principles.

- Allocation of cost under the system of activity based costing is done based on cost drivers

and there is an accurate cost allocation for products manufactured. There exists a danger

of over running and under running the products costs in event when irrelevant activities

and irrelevant cost drivers are assigned to products.

Requirement g:

ABC system comes with some disadvantages that are listed below:

- One of the complications of ABC system is related to appropriate cost driver selection for

each cost of overhead.

- Employment of ABC system is not suitable for small manufacturing organizations and

evaluating costs based on activities is difficult. An activity that influences the overall

costs is also difficult to identify.

- An organization manufacturing few products are not capable of deriving benefits from

ABC system as it is beneficial to organization that producing multiple products.

- ABC system is not affordable to small enterprises as it involves huge expenses.

- System of ABC is more complex compared to traditional product costing system as the

former employs multiple cost drivers and several cost pool.

- Some of aspects of activity based costing that can act as road blocking for firms involves

subsequent running cost and capital expenditure involved in running the system.

- Reports prepared by organization for internal and external purposes require using

traditional as well as system of activity based costing. This is so because system of

activity based costing do not comply with General accepted accounting principles.

- Allocation of cost under the system of activity based costing is done based on cost drivers

and there is an accurate cost allocation for products manufactured. There exists a danger

of over running and under running the products costs in event when irrelevant activities

and irrelevant cost drivers are assigned to products.

11INTRODUCTION TO MANAGEMENT ACCOUNTING

- System of activity based costing is not suitable to all organizations and it is certainly

possible that small organizations does not have resources for adapting such systems.

They might have complex activities and transactions might be too low.

- Implementation of ABC system would led to emergence of difficulties such as assigning

common cost, selecting the cost drivers and varying rates of cost drivers.

- System of ABC can be used more efficiently by larger manufacturing organizations as

compared to smaller organizations as it has different level of utility for different types of

organizations. An accurate cost of products is given by employing ABC system and this

feature of costing system provides advantage to firm depending upon cost plus pricing

(Bhimani et al. 2013). However, ABC system is not favored by organization making use

of market based prices. Application of ABC system is also affected by manufacturing

environment and technology level prevailing in different firms.

- The determination of cost drivers, analysis of activities occurring in activity centers and

tracing of cost of such activities requires additional costs. Significant amount of cost and

time is required for implementation of activity based costing system.

- Implementation of ABC system requires creation of environment of change (Ax and

Greve 2017). Several barriers faced by organization environment, individual should be

overcome for the application of such system. Some of the barriers that needs to be

overcome involves loss of potential status, shift in status quo and shift to unknown and a

need to learn new skills.

- It is essential on part of management of organization to investigate the existence of

barriers and the cause of barriers should be investigated. How, what and why of ABC

- System of activity based costing is not suitable to all organizations and it is certainly

possible that small organizations does not have resources for adapting such systems.

They might have complex activities and transactions might be too low.

- Implementation of ABC system would led to emergence of difficulties such as assigning

common cost, selecting the cost drivers and varying rates of cost drivers.

- System of ABC can be used more efficiently by larger manufacturing organizations as

compared to smaller organizations as it has different level of utility for different types of

organizations. An accurate cost of products is given by employing ABC system and this

feature of costing system provides advantage to firm depending upon cost plus pricing

(Bhimani et al. 2013). However, ABC system is not favored by organization making use

of market based prices. Application of ABC system is also affected by manufacturing

environment and technology level prevailing in different firms.

- The determination of cost drivers, analysis of activities occurring in activity centers and

tracing of cost of such activities requires additional costs. Significant amount of cost and

time is required for implementation of activity based costing system.

- Implementation of ABC system requires creation of environment of change (Ax and

Greve 2017). Several barriers faced by organization environment, individual should be

overcome for the application of such system. Some of the barriers that needs to be

overcome involves loss of potential status, shift in status quo and shift to unknown and a

need to learn new skills.

- It is essential on part of management of organization to investigate the existence of

barriers and the cause of barriers should be investigated. How, what and why of ABC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.