Management Accounting Report: System, Costing, and Budgetary Control

VerifiedAdded on 2020/12/09

|18

|5197

|318

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing various systems, costing methods, and budgetary control techniques. It begins with an introduction to management accounting, its tools, and its differences from financial accounting. Task 1 delves into different management accounting systems, including cost accounting, inventory management, and job costing, highlighting their essential requirements and reporting methods. Task 2 focuses on calculating production costs using both marginal and absorption costing methods, accompanied by income statements and interpretations. Task 3 explores the use of planning tools in budgetary control, such as operational and cash budgets, discussing their advantages and disadvantages. The report concludes with an analysis of how management accounting can be applied to respond to various financial problems, providing valuable insights into decision-making processes. The report is designed to help students understand key concepts and practical applications within the field of finance and accounting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Demonstration of understanding of management accounting system.........................................1

TASK 2............................................................................................................................................4

TASK 3 ...........................................................................................................................................6

Explanation of use of various planning tools of budgetary control............................................6

TASK 4............................................................................................................................................9

Report showing comparison of Different ways to respond various financial problems.............9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Demonstration of understanding of management accounting system.........................................1

TASK 2............................................................................................................................................4

TASK 3 ...........................................................................................................................................6

Explanation of use of various planning tools of budgetary control............................................6

TASK 4............................................................................................................................................9

Report showing comparison of Different ways to respond various financial problems.............9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting refers to a set of tools and techniques which helps the managers

in their decision making process by providing all the relevant information of the company. The

present study includes essential requirements of various types of management accounting system

and description of methods of the management accounting reporting. It also shows the

calculation of marginal and absorption costing methods. The study also includes advantages and

disadvantages of various planning tools of budgetary control and adoption of management

accounting system to respond various financial problems.

TASK 1

Demonstration of understanding of management accounting system

Management accounting

Management accounting can be defined as a process which includes various methods,

tools and techniques, which helps the managers in detecting various important informations for

their decision making process. Reports prepared under management accounting helps the internal

users of the business to determine the position of the organisation.

Management accounting is a synonym of cost accounting. It can also be defined as a

process of determining, analysing, explaining and transferring all the informations using some

professional skills to the managers of company as to help them in performing their part of

performance i.e. decision making and development of plans and strategies for the company

(Kaplan and Atkinson, 2015). It is totally different from financial accounting, as management

accounting contains the informations which helps the managers in their decision making process.

Whereas, financial management reports helps the outsiders to know the position of the company.

Management accounting system

Management accounting system refers to a system of management which involves

professional knowledge and skills of the managerial accountant to form the managerial

accounting report in such a form so that it could transfer all the relevant and important

information to the managers in their decision making process.

Management accounting system uses all the informations included financial and non

financial informations for the purpose of preparing their reports effectively and understandable

even by a non commercial person, So that they can be easily conveyed to the managers.

Essential requirements of different types of management accounting systems

1

Management accounting refers to a set of tools and techniques which helps the managers

in their decision making process by providing all the relevant information of the company. The

present study includes essential requirements of various types of management accounting system

and description of methods of the management accounting reporting. It also shows the

calculation of marginal and absorption costing methods. The study also includes advantages and

disadvantages of various planning tools of budgetary control and adoption of management

accounting system to respond various financial problems.

TASK 1

Demonstration of understanding of management accounting system

Management accounting

Management accounting can be defined as a process which includes various methods,

tools and techniques, which helps the managers in detecting various important informations for

their decision making process. Reports prepared under management accounting helps the internal

users of the business to determine the position of the organisation.

Management accounting is a synonym of cost accounting. It can also be defined as a

process of determining, analysing, explaining and transferring all the informations using some

professional skills to the managers of company as to help them in performing their part of

performance i.e. decision making and development of plans and strategies for the company

(Kaplan and Atkinson, 2015). It is totally different from financial accounting, as management

accounting contains the informations which helps the managers in their decision making process.

Whereas, financial management reports helps the outsiders to know the position of the company.

Management accounting system

Management accounting system refers to a system of management which involves

professional knowledge and skills of the managerial accountant to form the managerial

accounting report in such a form so that it could transfer all the relevant and important

information to the managers in their decision making process.

Management accounting system uses all the informations included financial and non

financial informations for the purpose of preparing their reports effectively and understandable

even by a non commercial person, So that they can be easily conveyed to the managers.

Essential requirements of different types of management accounting systems

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are many numbers of management accounting system. Each type of accounting

systems are essentially required by the company for having better control over overall business

organisation. Essential requirements of some management accounting systems are as under:

Cost accounting system: This is the system of managerial accounting which helps the

managers in having cost control over the business. With the help of this system,

managerial accountant prepares cost reports and enables to determine cost incurred by

each department.

Requirement:

▪ This system of management accounting is required to calculate the selling price of

each product by adding set profit in the cost of the product.

▪ It helps the managers in detecting the areas containing a\wastage through which

they can develop effective strategies as to eliminate wastage from each area.

▪ It is essentially required in the fir for the purpose of having cost control in the

company.

▪ With the help of this system managers can develop plans to enhance the overall

efficiency of company.

Inventory management system: this system of management accounting provide the

company a better control over the movement of inventory of the company within or

outside the business. In includes various methods of inventory valuation like FIFO,

LIFO, weighted average method, etc.

Requirement:

▪ Its is essentially required by those businesses which need to maintain huge

number of inventory like manufacturing concerns, etc.

▪ it provides a complete detail above each movement of the inventories within the

company.

▪ Managers can detect the wastage of insufficiency of inventory easily (Otley,

2016). With the help of which they can take effective decision to eliminate such

problems.

▪ Methods of inventory management system also helps managers in detecting

minimum requirement of the inventory in the business. It helps them in

maintaining the sufficient amount of inventory within the business.

2

systems are essentially required by the company for having better control over overall business

organisation. Essential requirements of some management accounting systems are as under:

Cost accounting system: This is the system of managerial accounting which helps the

managers in having cost control over the business. With the help of this system,

managerial accountant prepares cost reports and enables to determine cost incurred by

each department.

Requirement:

▪ This system of management accounting is required to calculate the selling price of

each product by adding set profit in the cost of the product.

▪ It helps the managers in detecting the areas containing a\wastage through which

they can develop effective strategies as to eliminate wastage from each area.

▪ It is essentially required in the fir for the purpose of having cost control in the

company.

▪ With the help of this system managers can develop plans to enhance the overall

efficiency of company.

Inventory management system: this system of management accounting provide the

company a better control over the movement of inventory of the company within or

outside the business. In includes various methods of inventory valuation like FIFO,

LIFO, weighted average method, etc.

Requirement:

▪ Its is essentially required by those businesses which need to maintain huge

number of inventory like manufacturing concerns, etc.

▪ it provides a complete detail above each movement of the inventories within the

company.

▪ Managers can detect the wastage of insufficiency of inventory easily (Otley,

2016). With the help of which they can take effective decision to eliminate such

problems.

▪ Methods of inventory management system also helps managers in detecting

minimum requirement of the inventory in the business. It helps them in

maintaining the sufficient amount of inventory within the business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: It is another type of management accounting system which helps the

in determining the price of product when they are manufactured as per the requirement of

the customers.

Requirement

▪ It is required by the business to calculate total amount of cost incurred on each job

of the business.

▪ It is essentially required by the managers when products or services are being

manufactured in customized form.

▪ This method helps the managers in determining the cost incurred by the business

on each product or services.

In this way, it can be analysed that management accounting systems are the essential

requirements of the company.

Management accounting reporting

Management accounting reporting refers to the process of preparing financial reports in

such a way so that it could provide all the relevant information to the managers and could tranfer

all the relevant information in the actual sense.

In management accounting reporting, includes all the functional and financial

informations which are usable of internal management of the organisation for developing their

strategies and plans fir the company.

Methods of management accounting reporting:

There are various methods of preparation of management accounting reporting. Some of

them are as under:

Budgetary reports: These reports are prepared by the managerial accountant to forecast

the future flow of funds within the organisation. These reports contain all the estimated

incomes and expenses which would be beard by the business within the specific time.

Managers prepares these reports after analysing past performance of the company and its

efficiency.

Cost reports: These reports contains the total amount of cost incurred by the business in

manufacturing a product. Managers prepares this reports after disadvantagesidering each

cost including variable and fixed cost incurred by the company.

3

in determining the price of product when they are manufactured as per the requirement of

the customers.

Requirement

▪ It is required by the business to calculate total amount of cost incurred on each job

of the business.

▪ It is essentially required by the managers when products or services are being

manufactured in customized form.

▪ This method helps the managers in determining the cost incurred by the business

on each product or services.

In this way, it can be analysed that management accounting systems are the essential

requirements of the company.

Management accounting reporting

Management accounting reporting refers to the process of preparing financial reports in

such a way so that it could provide all the relevant information to the managers and could tranfer

all the relevant information in the actual sense.

In management accounting reporting, includes all the functional and financial

informations which are usable of internal management of the organisation for developing their

strategies and plans fir the company.

Methods of management accounting reporting:

There are various methods of preparation of management accounting reporting. Some of

them are as under:

Budgetary reports: These reports are prepared by the managerial accountant to forecast

the future flow of funds within the organisation. These reports contain all the estimated

incomes and expenses which would be beard by the business within the specific time.

Managers prepares these reports after analysing past performance of the company and its

efficiency.

Cost reports: These reports contains the total amount of cost incurred by the business in

manufacturing a product. Managers prepares this reports after disadvantagesidering each

cost including variable and fixed cost incurred by the company.

3

Variance analysis reports: Variance report involves information about the differences

between actual and budgeted reports. These are used for the purpose of maintaining

control over various activities of the business.

Performance reports: This report is prepared by the managers as to evaluate

performance of the employees and overall business as well (Lin, 2017). These reports are

used by the managers for the purpose of rewarding any employee or providing appraisals

or incentives to each employees as per their performance in the company.

Accounting reports: These reports provides all the relevant informations of the financial

statements of the company. These reports help the managers in their planning, decision

making, controlling and regulating process.

In this regard, it can be evaluate that that various managerial accounting systems helps

the managers in getting all relevant informations of the business so that they can have better

control over each activity of the company by developing different plans and strategies as per the

actual performance of the business.

On the other hand maintenance of all the management accounting reporting helps in

gaining all the relevant information of the company in easy form (Maas, K., Schaltegger, S. and

Crutzen, 2016). So that managers can get the exact sense behind the reports of the company and

take their decisions accordingly.

TASK 2

Calculation of Production cost for marginal costing

Particular

Amount

(budgeted)

Amount

(actual)

Direct material 10

Direct labour 20

Prime cost 30

Variable production overheads 5.55

Fixed production overheads 40.55

Cost of production

Calculation of Production cost for absorption costing

Particular Amount Amount

4

between actual and budgeted reports. These are used for the purpose of maintaining

control over various activities of the business.

Performance reports: This report is prepared by the managers as to evaluate

performance of the employees and overall business as well (Lin, 2017). These reports are

used by the managers for the purpose of rewarding any employee or providing appraisals

or incentives to each employees as per their performance in the company.

Accounting reports: These reports provides all the relevant informations of the financial

statements of the company. These reports help the managers in their planning, decision

making, controlling and regulating process.

In this regard, it can be evaluate that that various managerial accounting systems helps

the managers in getting all relevant informations of the business so that they can have better

control over each activity of the company by developing different plans and strategies as per the

actual performance of the business.

On the other hand maintenance of all the management accounting reporting helps in

gaining all the relevant information of the company in easy form (Maas, K., Schaltegger, S. and

Crutzen, 2016). So that managers can get the exact sense behind the reports of the company and

take their decisions accordingly.

TASK 2

Calculation of Production cost for marginal costing

Particular

Amount

(budgeted)

Amount

(actual)

Direct material 10

Direct labour 20

Prime cost 30

Variable production overheads 5.55

Fixed production overheads 40.55

Cost of production

Calculation of Production cost for absorption costing

Particular Amount Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

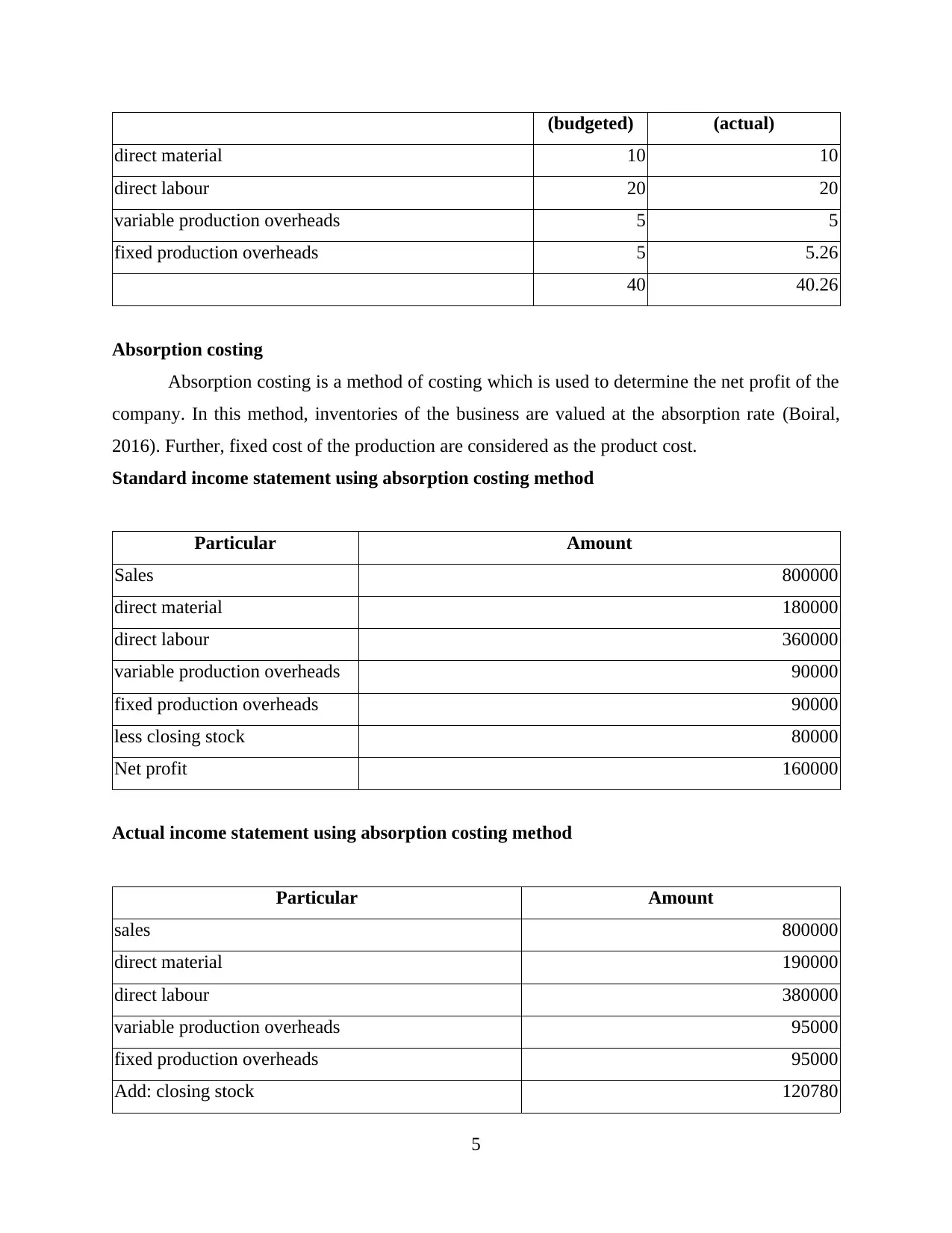

(budgeted) (actual)

direct material 10 10

direct labour 20 20

variable production overheads 5 5

fixed production overheads 5 5.26

40 40.26

Absorption costing

Absorption costing is a method of costing which is used to determine the net profit of the

company. In this method, inventories of the business are valued at the absorption rate (Boiral,

2016). Further, fixed cost of the production are considered as the product cost.

Standard income statement using absorption costing method

Particular Amount

Sales 800000

direct material 180000

direct labour 360000

variable production overheads 90000

fixed production overheads 90000

less closing stock 80000

Net profit 160000

Actual income statement using absorption costing method

Particular Amount

sales 800000

direct material 190000

direct labour 380000

variable production overheads 95000

fixed production overheads 95000

Add: closing stock 120780

5

direct material 10 10

direct labour 20 20

variable production overheads 5 5

fixed production overheads 5 5.26

40 40.26

Absorption costing

Absorption costing is a method of costing which is used to determine the net profit of the

company. In this method, inventories of the business are valued at the absorption rate (Boiral,

2016). Further, fixed cost of the production are considered as the product cost.

Standard income statement using absorption costing method

Particular Amount

Sales 800000

direct material 180000

direct labour 360000

variable production overheads 90000

fixed production overheads 90000

less closing stock 80000

Net profit 160000

Actual income statement using absorption costing method

Particular Amount

sales 800000

direct material 190000

direct labour 380000

variable production overheads 95000

fixed production overheads 95000

Add: closing stock 120780

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

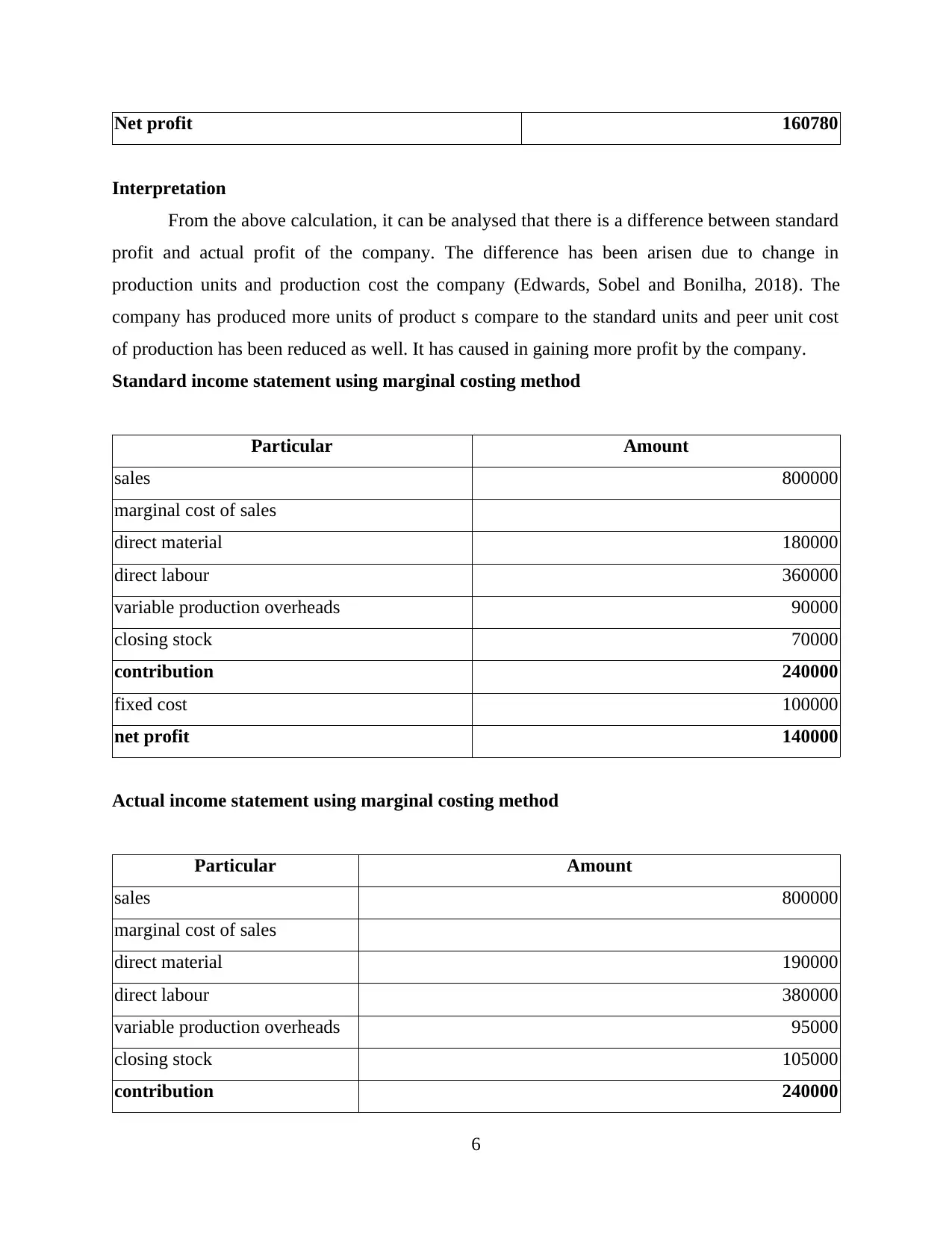

Net profit 160780

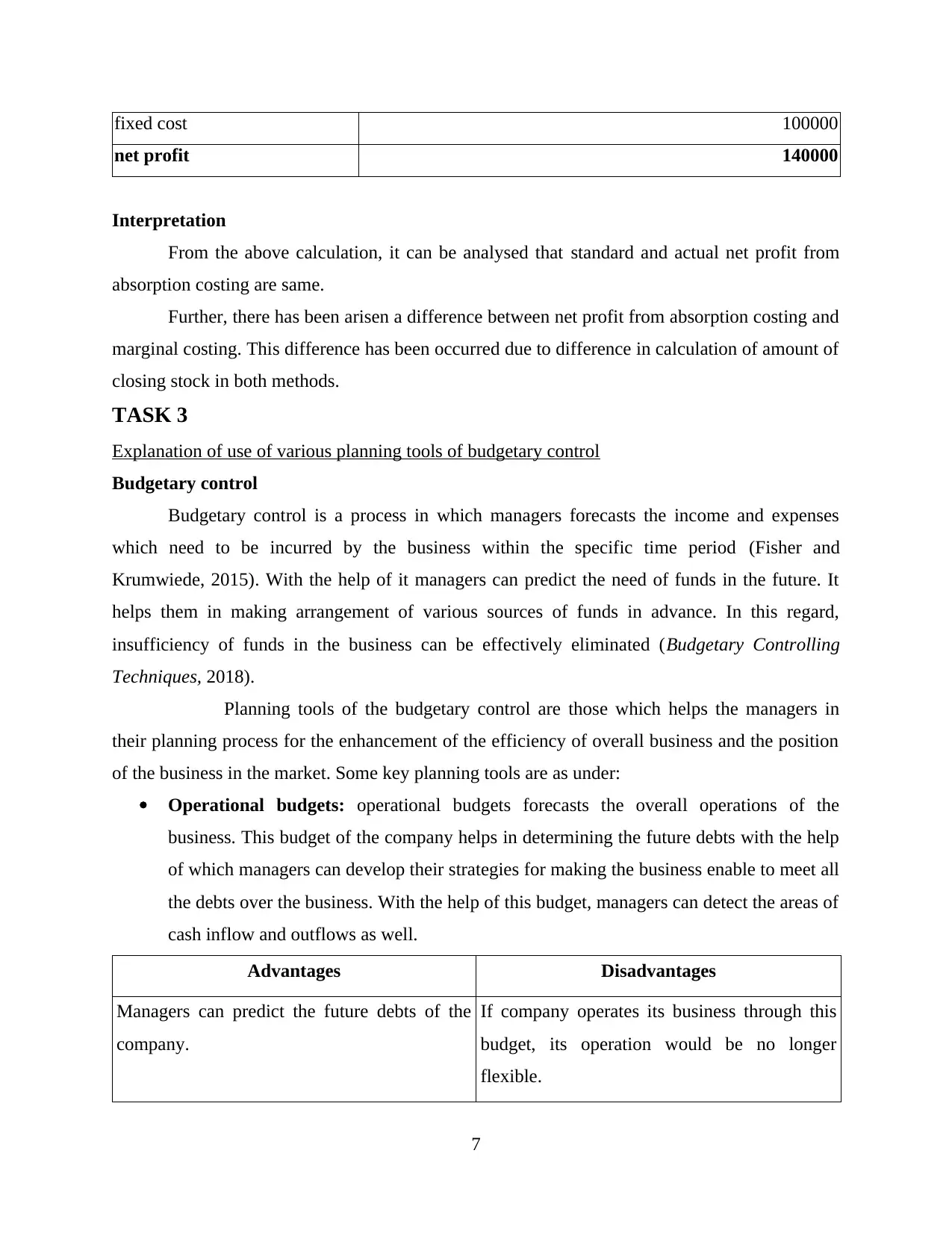

Interpretation

From the above calculation, it can be analysed that there is a difference between standard

profit and actual profit of the company. The difference has been arisen due to change in

production units and production cost the company (Edwards, Sobel and Bonilha, 2018). The

company has produced more units of product s compare to the standard units and peer unit cost

of production has been reduced as well. It has caused in gaining more profit by the company.

Standard income statement using marginal costing method

Particular Amount

sales 800000

marginal cost of sales

direct material 180000

direct labour 360000

variable production overheads 90000

closing stock 70000

contribution 240000

fixed cost 100000

net profit 140000

Actual income statement using marginal costing method

Particular Amount

sales 800000

marginal cost of sales

direct material 190000

direct labour 380000

variable production overheads 95000

closing stock 105000

contribution 240000

6

Interpretation

From the above calculation, it can be analysed that there is a difference between standard

profit and actual profit of the company. The difference has been arisen due to change in

production units and production cost the company (Edwards, Sobel and Bonilha, 2018). The

company has produced more units of product s compare to the standard units and peer unit cost

of production has been reduced as well. It has caused in gaining more profit by the company.

Standard income statement using marginal costing method

Particular Amount

sales 800000

marginal cost of sales

direct material 180000

direct labour 360000

variable production overheads 90000

closing stock 70000

contribution 240000

fixed cost 100000

net profit 140000

Actual income statement using marginal costing method

Particular Amount

sales 800000

marginal cost of sales

direct material 190000

direct labour 380000

variable production overheads 95000

closing stock 105000

contribution 240000

6

fixed cost 100000

net profit 140000

Interpretation

From the above calculation, it can be analysed that standard and actual net profit from

absorption costing are same.

Further, there has been arisen a difference between net profit from absorption costing and

marginal costing. This difference has been occurred due to difference in calculation of amount of

closing stock in both methods.

TASK 3

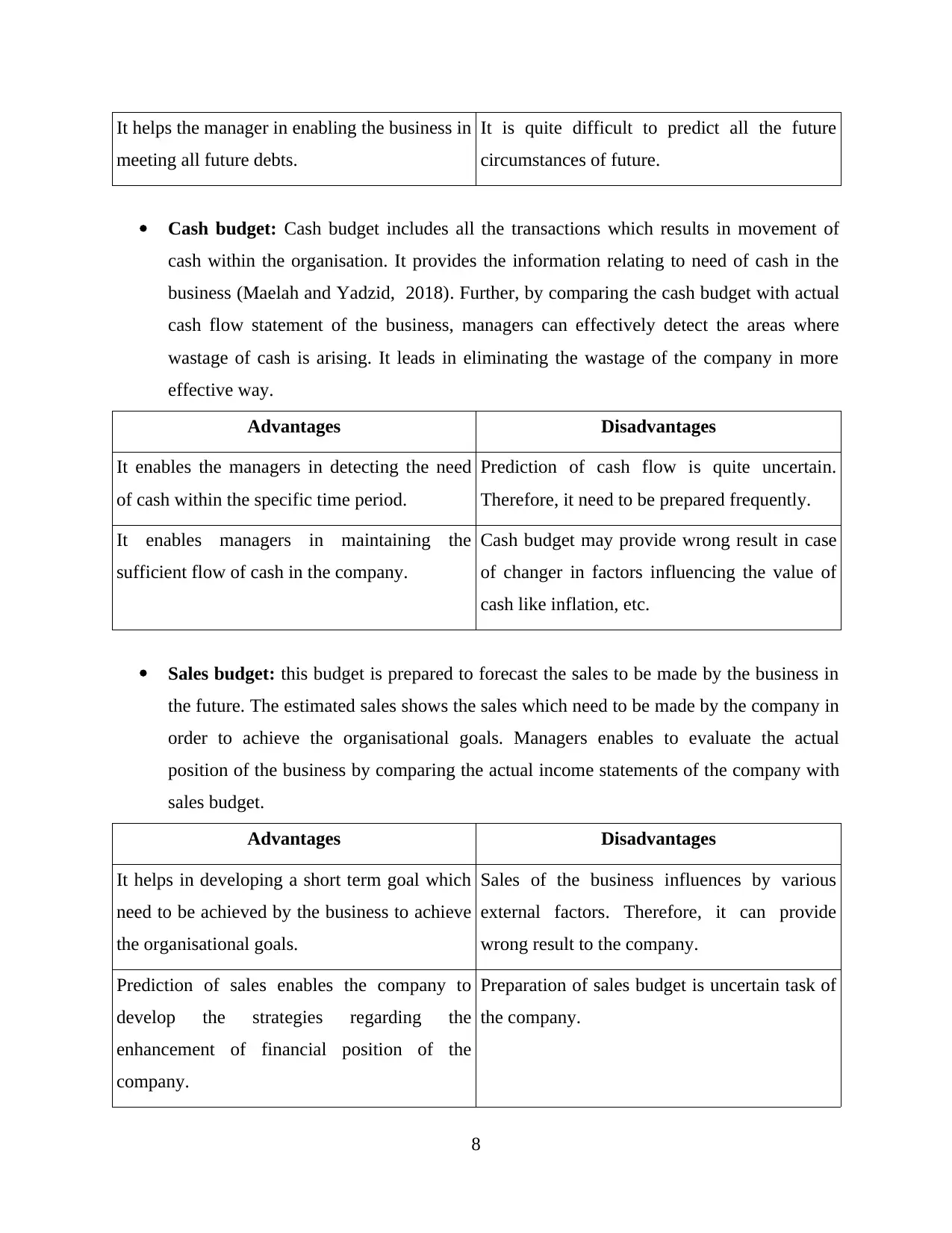

Explanation of use of various planning tools of budgetary control

Budgetary control

Budgetary control is a process in which managers forecasts the income and expenses

which need to be incurred by the business within the specific time period (Fisher and

Krumwiede, 2015). With the help of it managers can predict the need of funds in the future. It

helps them in making arrangement of various sources of funds in advance. In this regard,

insufficiency of funds in the business can be effectively eliminated (Budgetary Controlling

Techniques, 2018).

Planning tools of the budgetary control are those which helps the managers in

their planning process for the enhancement of the efficiency of overall business and the position

of the business in the market. Some key planning tools are as under:

Operational budgets: operational budgets forecasts the overall operations of the

business. This budget of the company helps in determining the future debts with the help

of which managers can develop their strategies for making the business enable to meet all

the debts over the business. With the help of this budget, managers can detect the areas of

cash inflow and outflows as well.

Advantages Disadvantages

Managers can predict the future debts of the

company.

If company operates its business through this

budget, its operation would be no longer

flexible.

7

net profit 140000

Interpretation

From the above calculation, it can be analysed that standard and actual net profit from

absorption costing are same.

Further, there has been arisen a difference between net profit from absorption costing and

marginal costing. This difference has been occurred due to difference in calculation of amount of

closing stock in both methods.

TASK 3

Explanation of use of various planning tools of budgetary control

Budgetary control

Budgetary control is a process in which managers forecasts the income and expenses

which need to be incurred by the business within the specific time period (Fisher and

Krumwiede, 2015). With the help of it managers can predict the need of funds in the future. It

helps them in making arrangement of various sources of funds in advance. In this regard,

insufficiency of funds in the business can be effectively eliminated (Budgetary Controlling

Techniques, 2018).

Planning tools of the budgetary control are those which helps the managers in

their planning process for the enhancement of the efficiency of overall business and the position

of the business in the market. Some key planning tools are as under:

Operational budgets: operational budgets forecasts the overall operations of the

business. This budget of the company helps in determining the future debts with the help

of which managers can develop their strategies for making the business enable to meet all

the debts over the business. With the help of this budget, managers can detect the areas of

cash inflow and outflows as well.

Advantages Disadvantages

Managers can predict the future debts of the

company.

If company operates its business through this

budget, its operation would be no longer

flexible.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the manager in enabling the business in

meeting all future debts.

It is quite difficult to predict all the future

circumstances of future.

Cash budget: Cash budget includes all the transactions which results in movement of

cash within the organisation. It provides the information relating to need of cash in the

business (Maelah and Yadzid, 2018). Further, by comparing the cash budget with actual

cash flow statement of the business, managers can effectively detect the areas where

wastage of cash is arising. It leads in eliminating the wastage of the company in more

effective way.

Advantages Disadvantages

It enables the managers in detecting the need

of cash within the specific time period.

Prediction of cash flow is quite uncertain.

Therefore, it need to be prepared frequently.

It enables managers in maintaining the

sufficient flow of cash in the company.

Cash budget may provide wrong result in case

of changer in factors influencing the value of

cash like inflation, etc.

Sales budget: this budget is prepared to forecast the sales to be made by the business in

the future. The estimated sales shows the sales which need to be made by the company in

order to achieve the organisational goals. Managers enables to evaluate the actual

position of the business by comparing the actual income statements of the company with

sales budget.

Advantages Disadvantages

It helps in developing a short term goal which

need to be achieved by the business to achieve

the organisational goals.

Sales of the business influences by various

external factors. Therefore, it can provide

wrong result to the company.

Prediction of sales enables the company to

develop the strategies regarding the

enhancement of financial position of the

company.

Preparation of sales budget is uncertain task of

the company.

8

meeting all future debts.

It is quite difficult to predict all the future

circumstances of future.

Cash budget: Cash budget includes all the transactions which results in movement of

cash within the organisation. It provides the information relating to need of cash in the

business (Maelah and Yadzid, 2018). Further, by comparing the cash budget with actual

cash flow statement of the business, managers can effectively detect the areas where

wastage of cash is arising. It leads in eliminating the wastage of the company in more

effective way.

Advantages Disadvantages

It enables the managers in detecting the need

of cash within the specific time period.

Prediction of cash flow is quite uncertain.

Therefore, it need to be prepared frequently.

It enables managers in maintaining the

sufficient flow of cash in the company.

Cash budget may provide wrong result in case

of changer in factors influencing the value of

cash like inflation, etc.

Sales budget: this budget is prepared to forecast the sales to be made by the business in

the future. The estimated sales shows the sales which need to be made by the company in

order to achieve the organisational goals. Managers enables to evaluate the actual

position of the business by comparing the actual income statements of the company with

sales budget.

Advantages Disadvantages

It helps in developing a short term goal which

need to be achieved by the business to achieve

the organisational goals.

Sales of the business influences by various

external factors. Therefore, it can provide

wrong result to the company.

Prediction of sales enables the company to

develop the strategies regarding the

enhancement of financial position of the

company.

Preparation of sales budget is uncertain task of

the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based budgeting: This type of planning tools help managers in identification

and analysis of various activities of the business (Otley, 2015). With the help of this

system, managers also enables to determine various activities with all the sources if

business. They also enable in analysing the efficiency of various activities of the

company.

Advantages Disadvantages

Activity based budgeting helps in analysing

actual cost of production.

It is a costly planning tool of budgetary

control.

It enables the managers in analysing the

relationship between various activities of the

business with its existing sources.

Data evaluated through this tool may not be

useful for the businesses amount of overheads

spent by the business is low.

Static budget: Static budgets are those that are required to track all the finance in the

business including incomes and expenses.

Advantages Disadvantages

Easy to be implemented in business Lack of flexibility

Can help in determination of overestimation of

underestimation of costs

Additional resources for keeping the business

up can't be allotted in this budget.

Flexible budget: Flexible budgets are those that are prepared different for different level

of production the business.

Advantages Disadvantages

It provides better control over business. It assumes linearity in the costs.

It leads in frequently adjusting the revenues

and expenses for various level of the business.

It is highly dependent upon various

assumptions.

Rolling budget: in this budget, budgets are continuously being updates as the passage of

time.

9

and analysis of various activities of the business (Otley, 2015). With the help of this

system, managers also enables to determine various activities with all the sources if

business. They also enable in analysing the efficiency of various activities of the

company.

Advantages Disadvantages

Activity based budgeting helps in analysing

actual cost of production.

It is a costly planning tool of budgetary

control.

It enables the managers in analysing the

relationship between various activities of the

business with its existing sources.

Data evaluated through this tool may not be

useful for the businesses amount of overheads

spent by the business is low.

Static budget: Static budgets are those that are required to track all the finance in the

business including incomes and expenses.

Advantages Disadvantages

Easy to be implemented in business Lack of flexibility

Can help in determination of overestimation of

underestimation of costs

Additional resources for keeping the business

up can't be allotted in this budget.

Flexible budget: Flexible budgets are those that are prepared different for different level

of production the business.

Advantages Disadvantages

It provides better control over business. It assumes linearity in the costs.

It leads in frequently adjusting the revenues

and expenses for various level of the business.

It is highly dependent upon various

assumptions.

Rolling budget: in this budget, budgets are continuously being updates as the passage of

time.

9

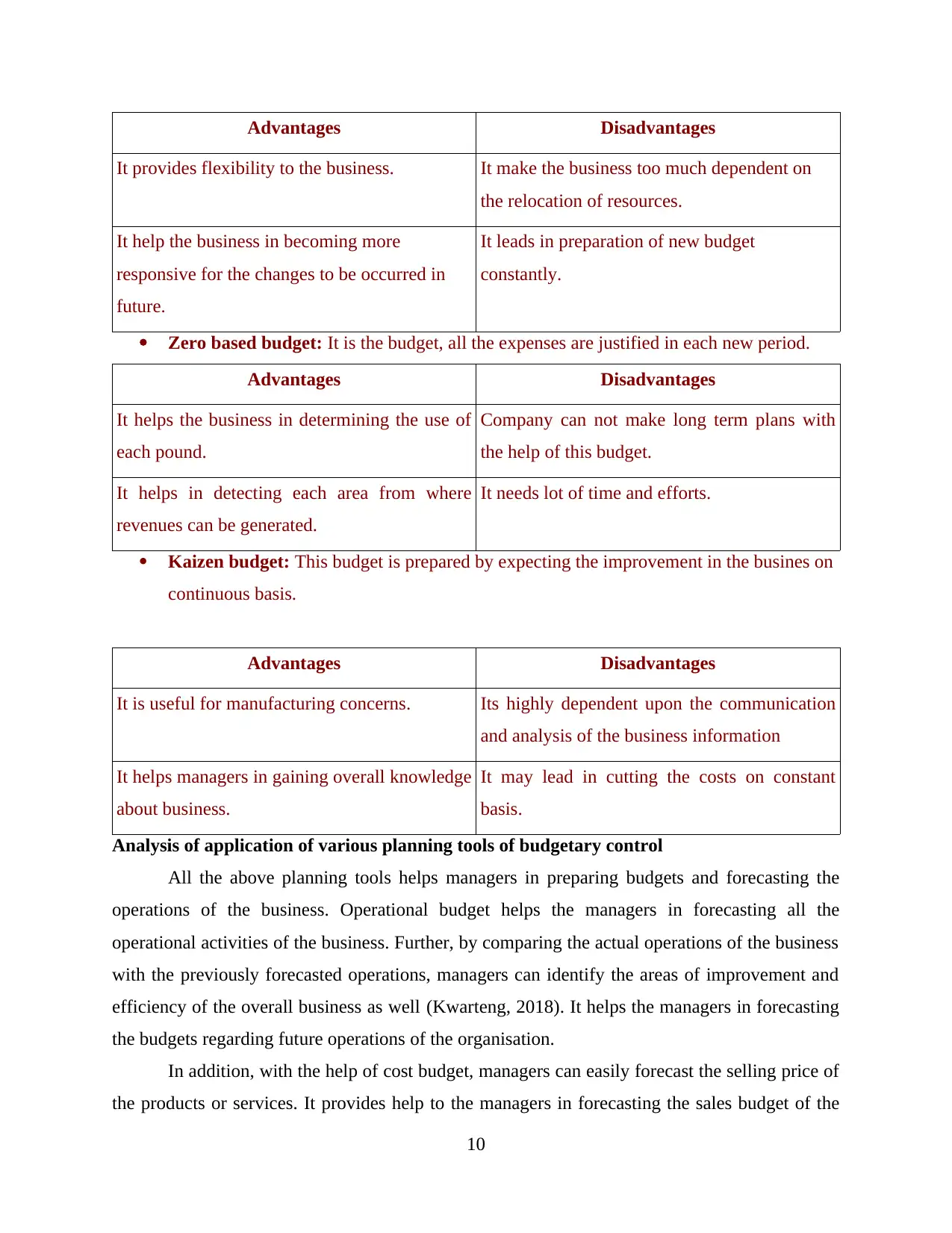

Advantages Disadvantages

It provides flexibility to the business. It make the business too much dependent on

the relocation of resources.

It help the business in becoming more

responsive for the changes to be occurred in

future.

It leads in preparation of new budget

constantly.

Zero based budget: It is the budget, all the expenses are justified in each new period.

Advantages Disadvantages

It helps the business in determining the use of

each pound.

Company can not make long term plans with

the help of this budget.

It helps in detecting each area from where

revenues can be generated.

It needs lot of time and efforts.

Kaizen budget: This budget is prepared by expecting the improvement in the busines on

continuous basis.

Advantages Disadvantages

It is useful for manufacturing concerns. Its highly dependent upon the communication

and analysis of the business information

It helps managers in gaining overall knowledge

about business.

It may lead in cutting the costs on constant

basis.

Analysis of application of various planning tools of budgetary control

All the above planning tools helps managers in preparing budgets and forecasting the

operations of the business. Operational budget helps the managers in forecasting all the

operational activities of the business. Further, by comparing the actual operations of the business

with the previously forecasted operations, managers can identify the areas of improvement and

efficiency of the overall business as well (Kwarteng, 2018). It helps the managers in forecasting

the budgets regarding future operations of the organisation.

In addition, with the help of cost budget, managers can easily forecast the selling price of

the products or services. It provides help to the managers in forecasting the sales budget of the

10

It provides flexibility to the business. It make the business too much dependent on

the relocation of resources.

It help the business in becoming more

responsive for the changes to be occurred in

future.

It leads in preparation of new budget

constantly.

Zero based budget: It is the budget, all the expenses are justified in each new period.

Advantages Disadvantages

It helps the business in determining the use of

each pound.

Company can not make long term plans with

the help of this budget.

It helps in detecting each area from where

revenues can be generated.

It needs lot of time and efforts.

Kaizen budget: This budget is prepared by expecting the improvement in the busines on

continuous basis.

Advantages Disadvantages

It is useful for manufacturing concerns. Its highly dependent upon the communication

and analysis of the business information

It helps managers in gaining overall knowledge

about business.

It may lead in cutting the costs on constant

basis.

Analysis of application of various planning tools of budgetary control

All the above planning tools helps managers in preparing budgets and forecasting the

operations of the business. Operational budget helps the managers in forecasting all the

operational activities of the business. Further, by comparing the actual operations of the business

with the previously forecasted operations, managers can identify the areas of improvement and

efficiency of the overall business as well (Kwarteng, 2018). It helps the managers in forecasting

the budgets regarding future operations of the organisation.

In addition, with the help of cost budget, managers can easily forecast the selling price of

the products or services. It provides help to the managers in forecasting the sales budget of the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.