Management Accounting Report: Analysis of Costing and Budgeting Cases

VerifiedAdded on 2020/05/28

|11

|2233

|120

Report

AI Summary

This report presents an analysis of two management accounting cases. The first case focuses on US Bright Product Company and applies activity-based costing (ABC) to determine product costs, including the allocation of indirect costs based on activity drivers. It calculates cost per unit and prepares a bill of activities for the Lamington division, highlighting the importance of including all relevant costs. The second case examines Hawthorn Leisure Works and its transition from an old membership and court fee structure to a new membership-only plan. The report compares revenue generation under both plans, assessing the impact of the new fee structure on cash receipts and overall revenue, and recommends acceptance of the new plan based on increased revenue projections. The report utilizes financial data to support its conclusions and recommendations, providing a comprehensive overview of costing and budgeting strategies.

Running Head: Management Accounting

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 2

Executive Summary:

This report consists of 2 cases on is based on activity based Costing and another on

Budgeting. The case of Activity based costing is about the US Bright Product Company

which produces cakes and pastries. This case is about the allocation of cost on the basis of

activity driver and total product cost of the company and per unit cost. The cost is calculated

by using Activity based costing. In first part per unit cost is calculated by using the activity

drivers allocated for each cot. In the second part the billing amount and the cost per unit has

been calculated of Lamington division and in the last part the additional cost required to

calculate the product cost is mentioned as without that the calculation of the total cost will be

incomplete.

The case of budgeting is about Hawthorn Leisure Works which offers tennis courts

and other physical fitness facilities to its members. They want to implement a new plan

regarding the membership fee of HLWs as under old plan the revenue is generated from

membership fee and court fee and in the new plan the revenue only comprise of membership

fee. The company wants to plan revenue according to the new plan as they think that as per

the new plan their revenues will increase. They want a complete analysis as the revenue

comparison in between the old plan and the new plan.

Executive Summary:

This report consists of 2 cases on is based on activity based Costing and another on

Budgeting. The case of Activity based costing is about the US Bright Product Company

which produces cakes and pastries. This case is about the allocation of cost on the basis of

activity driver and total product cost of the company and per unit cost. The cost is calculated

by using Activity based costing. In first part per unit cost is calculated by using the activity

drivers allocated for each cot. In the second part the billing amount and the cost per unit has

been calculated of Lamington division and in the last part the additional cost required to

calculate the product cost is mentioned as without that the calculation of the total cost will be

incomplete.

The case of budgeting is about Hawthorn Leisure Works which offers tennis courts

and other physical fitness facilities to its members. They want to implement a new plan

regarding the membership fee of HLWs as under old plan the revenue is generated from

membership fee and court fee and in the new plan the revenue only comprise of membership

fee. The company wants to plan revenue according to the new plan as they think that as per

the new plan their revenues will increase. They want a complete analysis as the revenue

comparison in between the old plan and the new plan.

Management Accounting 3

Table of Contents

Task A...................................................................................................................................................4

Introduction:......................................................................................................................................4

Part (a)...............................................................................................................................................4

Part (b)...............................................................................................................................................5

Part (c)...............................................................................................................................................5

Conclusion:........................................................................................................................................6

Task B...................................................................................................................................................7

Introduction:......................................................................................................................................7

Part (a)...............................................................................................................................................9

Part (b)...............................................................................................................................................9

Part (c)...............................................................................................................................................9

Conclusion:........................................................................................................................................9

References:..........................................................................................................................................10

Table of Contents

Task A...................................................................................................................................................4

Introduction:......................................................................................................................................4

Part (a)...............................................................................................................................................4

Part (b)...............................................................................................................................................5

Part (c)...............................................................................................................................................5

Conclusion:........................................................................................................................................6

Task B...................................................................................................................................................7

Introduction:......................................................................................................................................7

Part (a)...............................................................................................................................................9

Part (b)...............................................................................................................................................9

Part (c)...............................................................................................................................................9

Conclusion:........................................................................................................................................9

References:..........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 4

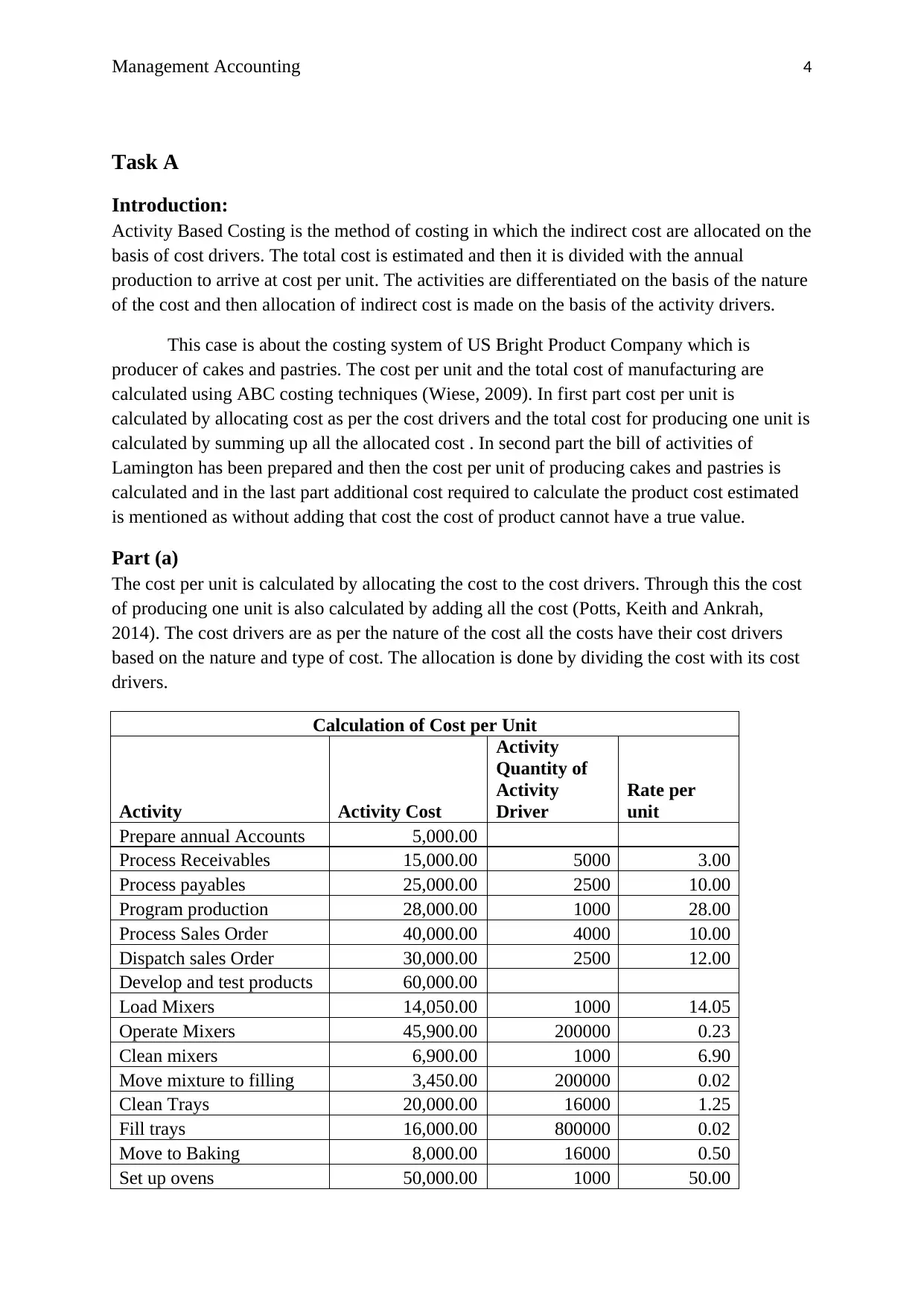

Task A

Introduction:

Activity Based Costing is the method of costing in which the indirect cost are allocated on the

basis of cost drivers. The total cost is estimated and then it is divided with the annual

production to arrive at cost per unit. The activities are differentiated on the basis of the nature

of the cost and then allocation of indirect cost is made on the basis of the activity drivers.

This case is about the costing system of US Bright Product Company which is

producer of cakes and pastries. The cost per unit and the total cost of manufacturing are

calculated using ABC costing techniques (Wiese, 2009). In first part cost per unit is

calculated by allocating cost as per the cost drivers and the total cost for producing one unit is

calculated by summing up all the allocated cost . In second part the bill of activities of

Lamington has been prepared and then the cost per unit of producing cakes and pastries is

calculated and in the last part additional cost required to calculate the product cost estimated

is mentioned as without adding that cost the cost of product cannot have a true value.

Part (a)

The cost per unit is calculated by allocating the cost to the cost drivers. Through this the cost

of producing one unit is also calculated by adding all the cost (Potts, Keith and Ankrah,

2014). The cost drivers are as per the nature of the cost all the costs have their cost drivers

based on the nature and type of cost. The allocation is done by dividing the cost with its cost

drivers.

Calculation of Cost per Unit

Activity Activity Cost

Activity

Quantity of

Activity

Driver

Rate per

unit

Prepare annual Accounts 5,000.00

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 3,450.00 200000 0.02

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Task A

Introduction:

Activity Based Costing is the method of costing in which the indirect cost are allocated on the

basis of cost drivers. The total cost is estimated and then it is divided with the annual

production to arrive at cost per unit. The activities are differentiated on the basis of the nature

of the cost and then allocation of indirect cost is made on the basis of the activity drivers.

This case is about the costing system of US Bright Product Company which is

producer of cakes and pastries. The cost per unit and the total cost of manufacturing are

calculated using ABC costing techniques (Wiese, 2009). In first part cost per unit is

calculated by allocating cost as per the cost drivers and the total cost for producing one unit is

calculated by summing up all the allocated cost . In second part the bill of activities of

Lamington has been prepared and then the cost per unit of producing cakes and pastries is

calculated and in the last part additional cost required to calculate the product cost estimated

is mentioned as without adding that cost the cost of product cannot have a true value.

Part (a)

The cost per unit is calculated by allocating the cost to the cost drivers. Through this the cost

of producing one unit is also calculated by adding all the cost (Potts, Keith and Ankrah,

2014). The cost drivers are as per the nature of the cost all the costs have their cost drivers

based on the nature and type of cost. The allocation is done by dividing the cost with its cost

drivers.

Calculation of Cost per Unit

Activity Activity Cost

Activity

Quantity of

Activity

Driver

Rate per

unit

Prepare annual Accounts 5,000.00

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 3,450.00 200000 0.02

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

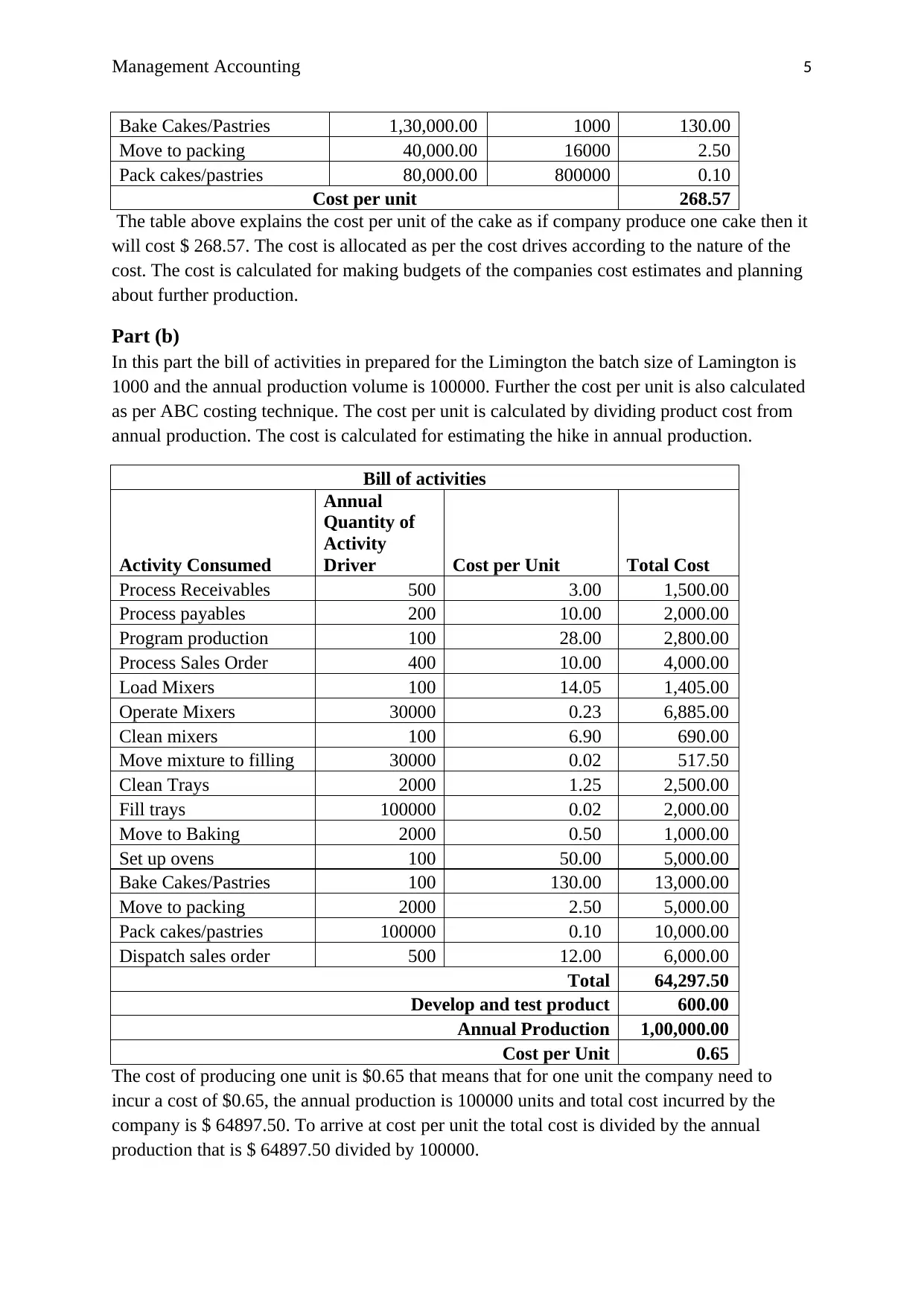

Management Accounting 5

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

The table above explains the cost per unit of the cake as if company produce one cake then it

will cost $ 268.57. The cost is allocated as per the cost drives according to the nature of the

cost. The cost is calculated for making budgets of the companies cost estimates and planning

about further production.

Part (b)

In this part the bill of activities in prepared for the Limington the batch size of Lamington is

1000 and the annual production volume is 100000. Further the cost per unit is also calculated

as per ABC costing technique. The cost per unit is calculated by dividing product cost from

annual production. The cost is calculated for estimating the hike in annual production.

Bill of activities

Activity Consumed

Annual

Quantity of

Activity

Driver Cost per Unit Total Cost

Process Receivables 500 3.00 1,500.00

Process payables 200 10.00 2,000.00

Program production 100 28.00 2,800.00

Process Sales Order 400 10.00 4,000.00

Load Mixers 100 14.05 1,405.00

Operate Mixers 30000 0.23 6,885.00

Clean mixers 100 6.90 690.00

Move mixture to filling 30000 0.02 517.50

Clean Trays 2000 1.25 2,500.00

Fill trays 100000 0.02 2,000.00

Move to Baking 2000 0.50 1,000.00

Set up ovens 100 50.00 5,000.00

Bake Cakes/Pastries 100 130.00 13,000.00

Move to packing 2000 2.50 5,000.00

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Total 64,297.50

Develop and test product 600.00

Annual Production 1,00,000.00

Cost per Unit 0.65

The cost of producing one unit is $0.65 that means that for one unit the company need to

incur a cost of $0.65, the annual production is 100000 units and total cost incurred by the

company is $ 64897.50. To arrive at cost per unit the total cost is divided by the annual

production that is $ 64897.50 divided by 100000.

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

The table above explains the cost per unit of the cake as if company produce one cake then it

will cost $ 268.57. The cost is allocated as per the cost drives according to the nature of the

cost. The cost is calculated for making budgets of the companies cost estimates and planning

about further production.

Part (b)

In this part the bill of activities in prepared for the Limington the batch size of Lamington is

1000 and the annual production volume is 100000. Further the cost per unit is also calculated

as per ABC costing technique. The cost per unit is calculated by dividing product cost from

annual production. The cost is calculated for estimating the hike in annual production.

Bill of activities

Activity Consumed

Annual

Quantity of

Activity

Driver Cost per Unit Total Cost

Process Receivables 500 3.00 1,500.00

Process payables 200 10.00 2,000.00

Program production 100 28.00 2,800.00

Process Sales Order 400 10.00 4,000.00

Load Mixers 100 14.05 1,405.00

Operate Mixers 30000 0.23 6,885.00

Clean mixers 100 6.90 690.00

Move mixture to filling 30000 0.02 517.50

Clean Trays 2000 1.25 2,500.00

Fill trays 100000 0.02 2,000.00

Move to Baking 2000 0.50 1,000.00

Set up ovens 100 50.00 5,000.00

Bake Cakes/Pastries 100 130.00 13,000.00

Move to packing 2000 2.50 5,000.00

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Total 64,297.50

Develop and test product 600.00

Annual Production 1,00,000.00

Cost per Unit 0.65

The cost of producing one unit is $0.65 that means that for one unit the company need to

incur a cost of $0.65, the annual production is 100000 units and total cost incurred by the

company is $ 64897.50. To arrive at cost per unit the total cost is divided by the annual

production that is $ 64897.50 divided by 100000.

Management Accounting 6

Part (c)

The company prepared the schedule for calculating the total billing amount as well as the cost

of producing per unit but the total cost cannot be calculated without adding the cost of

preparing annual accounts in the cost schedule. Hence, the cost of preparing annual accounts

must be added to arrive at the product cost of Lamington. This is not product attributable cost

that is why we need to add it into the product cost to arrive at total cost.

Conclusion:

The above study illustrates the cost structure of US Bright and its Division Lamington. We

did also estimated the cost of producing one unit as well the billing amount of Lamington and

per unit cost of cakes and pastries. The cost of producing one unit based on the allocation of

cost on their cost drivers is $268.6. The per unit cost of lamington is $0.65 and the billing

amount calculated is $ 64897.50. Further we came to know that they also need to add the cost

of preparing annual accounts to arrive at the total cost of the Lamington. Through this

analysis the company can make its budget cost estimate as well as estimate the production

quantity and prepare the budgets accordingly(Goektuerk, 2007)..

Part (c)

The company prepared the schedule for calculating the total billing amount as well as the cost

of producing per unit but the total cost cannot be calculated without adding the cost of

preparing annual accounts in the cost schedule. Hence, the cost of preparing annual accounts

must be added to arrive at the product cost of Lamington. This is not product attributable cost

that is why we need to add it into the product cost to arrive at total cost.

Conclusion:

The above study illustrates the cost structure of US Bright and its Division Lamington. We

did also estimated the cost of producing one unit as well the billing amount of Lamington and

per unit cost of cakes and pastries. The cost of producing one unit based on the allocation of

cost on their cost drivers is $268.6. The per unit cost of lamington is $0.65 and the billing

amount calculated is $ 64897.50. Further we came to know that they also need to add the cost

of preparing annual accounts to arrive at the total cost of the Lamington. Through this

analysis the company can make its budget cost estimate as well as estimate the production

quantity and prepare the budgets accordingly(Goektuerk, 2007)..

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 7

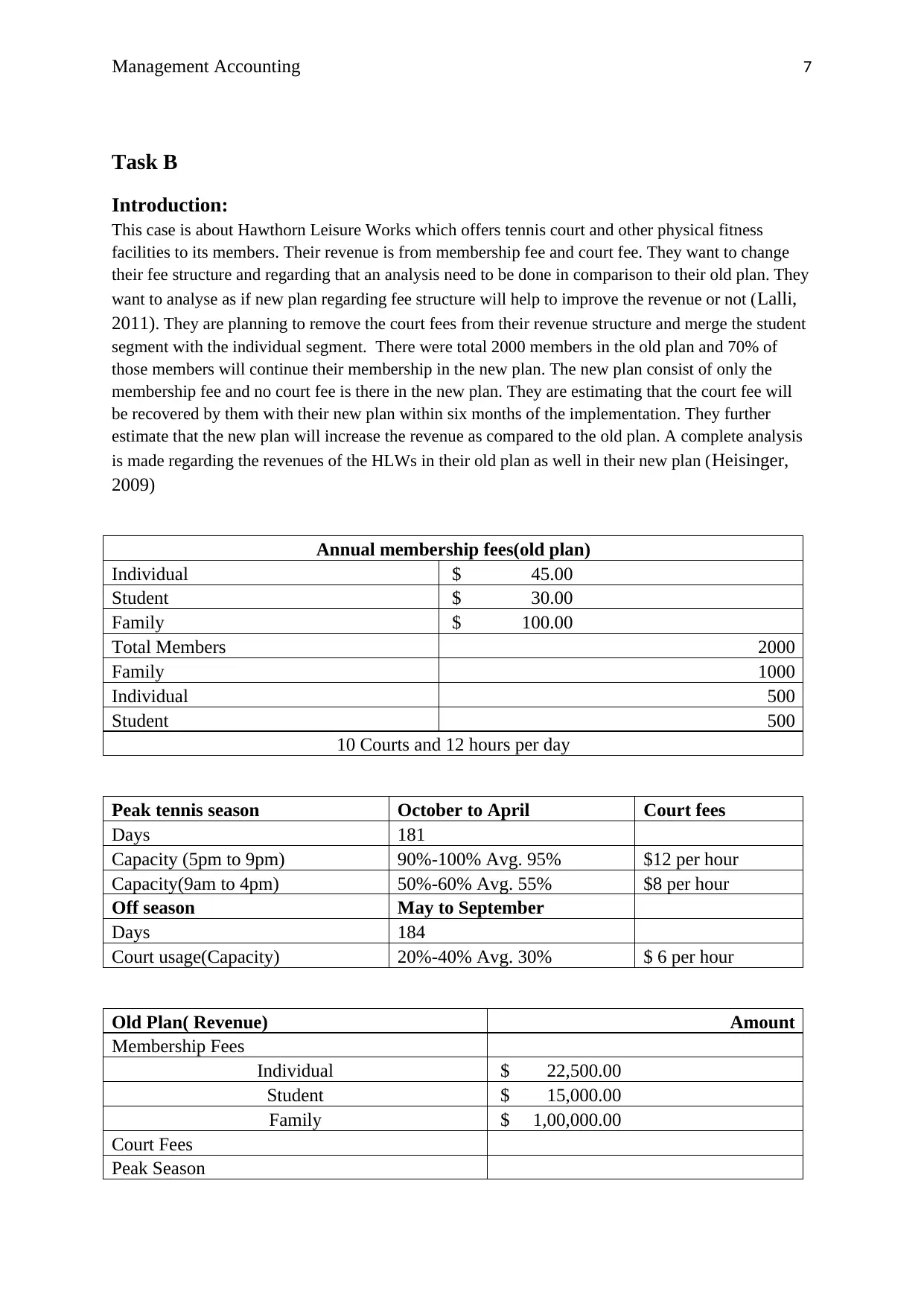

Task B

Introduction:

This case is about Hawthorn Leisure Works which offers tennis court and other physical fitness

facilities to its members. Their revenue is from membership fee and court fee. They want to change

their fee structure and regarding that an analysis need to be done in comparison to their old plan. They

want to analyse as if new plan regarding fee structure will help to improve the revenue or not (Lalli,

2011). They are planning to remove the court fees from their revenue structure and merge the student

segment with the individual segment. There were total 2000 members in the old plan and 70% of

those members will continue their membership in the new plan. The new plan consist of only the

membership fee and no court fee is there in the new plan. They are estimating that the court fee will

be recovered by them with their new plan within six months of the implementation. They further

estimate that the new plan will increase the revenue as compared to the old plan. A complete analysis

is made regarding the revenues of the HLWs in their old plan as well in their new plan (Heisinger,

2009)

Annual membership fees(old plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

10 Courts and 12 hours per day

Peak tennis season October to April Court fees

Days 181

Capacity (5pm to 9pm) 90%-100% Avg. 95% $12 per hour

Capacity(9am to 4pm) 50%-60% Avg. 55% $8 per hour

Off season May to September

Days 184

Court usage(Capacity) 20%-40% Avg. 30% $ 6 per hour

Old Plan( Revenue) Amount

Membership Fees

Individual $ 22,500.00

Student $ 15,000.00

Family $ 1,00,000.00

Court Fees

Peak Season

Task B

Introduction:

This case is about Hawthorn Leisure Works which offers tennis court and other physical fitness

facilities to its members. Their revenue is from membership fee and court fee. They want to change

their fee structure and regarding that an analysis need to be done in comparison to their old plan. They

want to analyse as if new plan regarding fee structure will help to improve the revenue or not (Lalli,

2011). They are planning to remove the court fees from their revenue structure and merge the student

segment with the individual segment. There were total 2000 members in the old plan and 70% of

those members will continue their membership in the new plan. The new plan consist of only the

membership fee and no court fee is there in the new plan. They are estimating that the court fee will

be recovered by them with their new plan within six months of the implementation. They further

estimate that the new plan will increase the revenue as compared to the old plan. A complete analysis

is made regarding the revenues of the HLWs in their old plan as well in their new plan (Heisinger,

2009)

Annual membership fees(old plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

10 Courts and 12 hours per day

Peak tennis season October to April Court fees

Days 181

Capacity (5pm to 9pm) 90%-100% Avg. 95% $12 per hour

Capacity(9am to 4pm) 50%-60% Avg. 55% $8 per hour

Off season May to September

Days 184

Court usage(Capacity) 20%-40% Avg. 30% $ 6 per hour

Old Plan( Revenue) Amount

Membership Fees

Individual $ 22,500.00

Student $ 15,000.00

Family $ 1,00,000.00

Court Fees

Peak Season

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 8

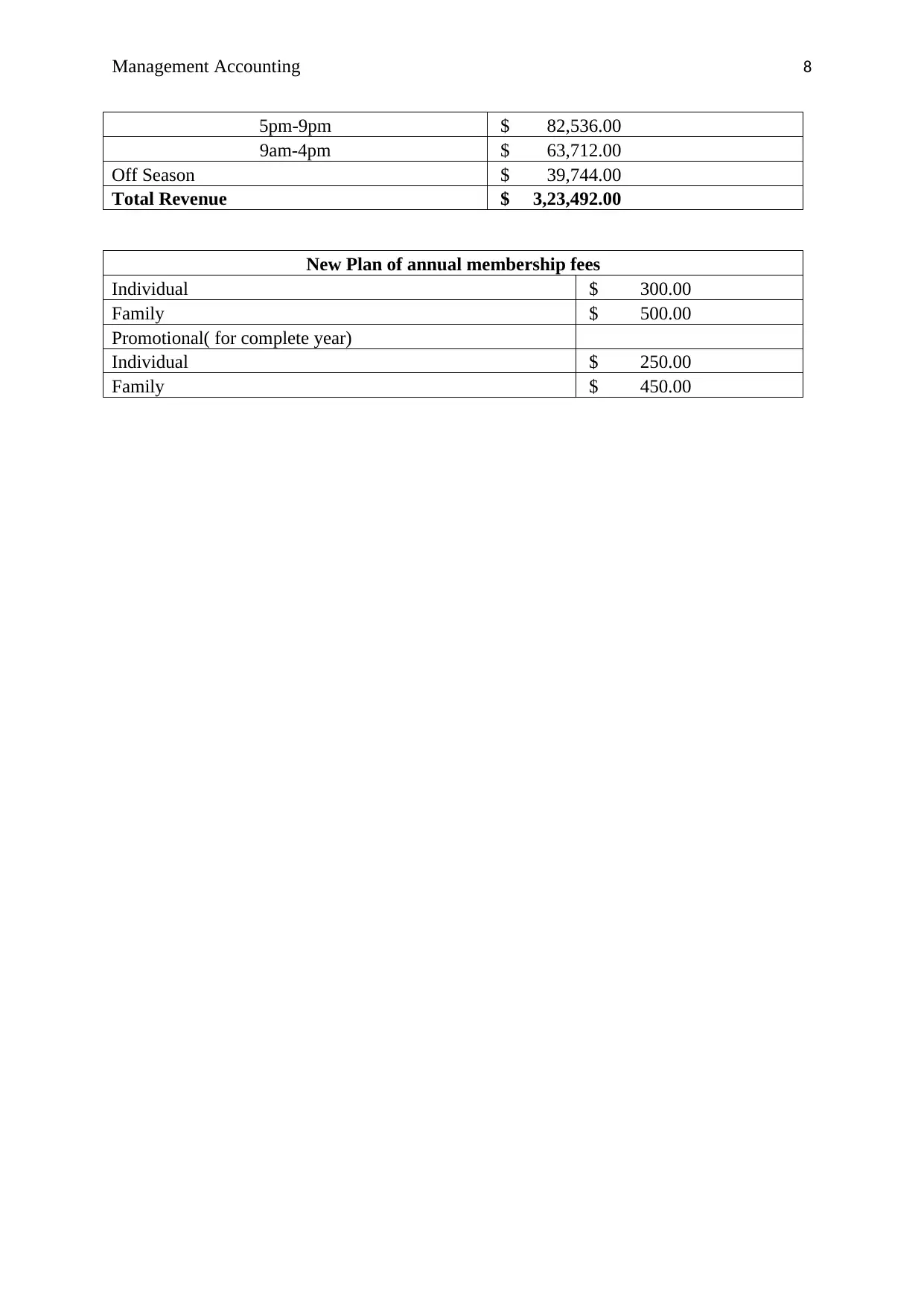

5pm-9pm $ 82,536.00

9am-4pm $ 63,712.00

Off Season $ 39,744.00

Total Revenue $ 3,23,492.00

New Plan of annual membership fees

Individual $ 300.00

Family $ 500.00

Promotional( for complete year)

Individual $ 250.00

Family $ 450.00

5pm-9pm $ 82,536.00

9am-4pm $ 63,712.00

Off Season $ 39,744.00

Total Revenue $ 3,23,492.00

New Plan of annual membership fees

Individual $ 300.00

Family $ 500.00

Promotional( for complete year)

Individual $ 250.00

Family $ 450.00

Management Accounting 9

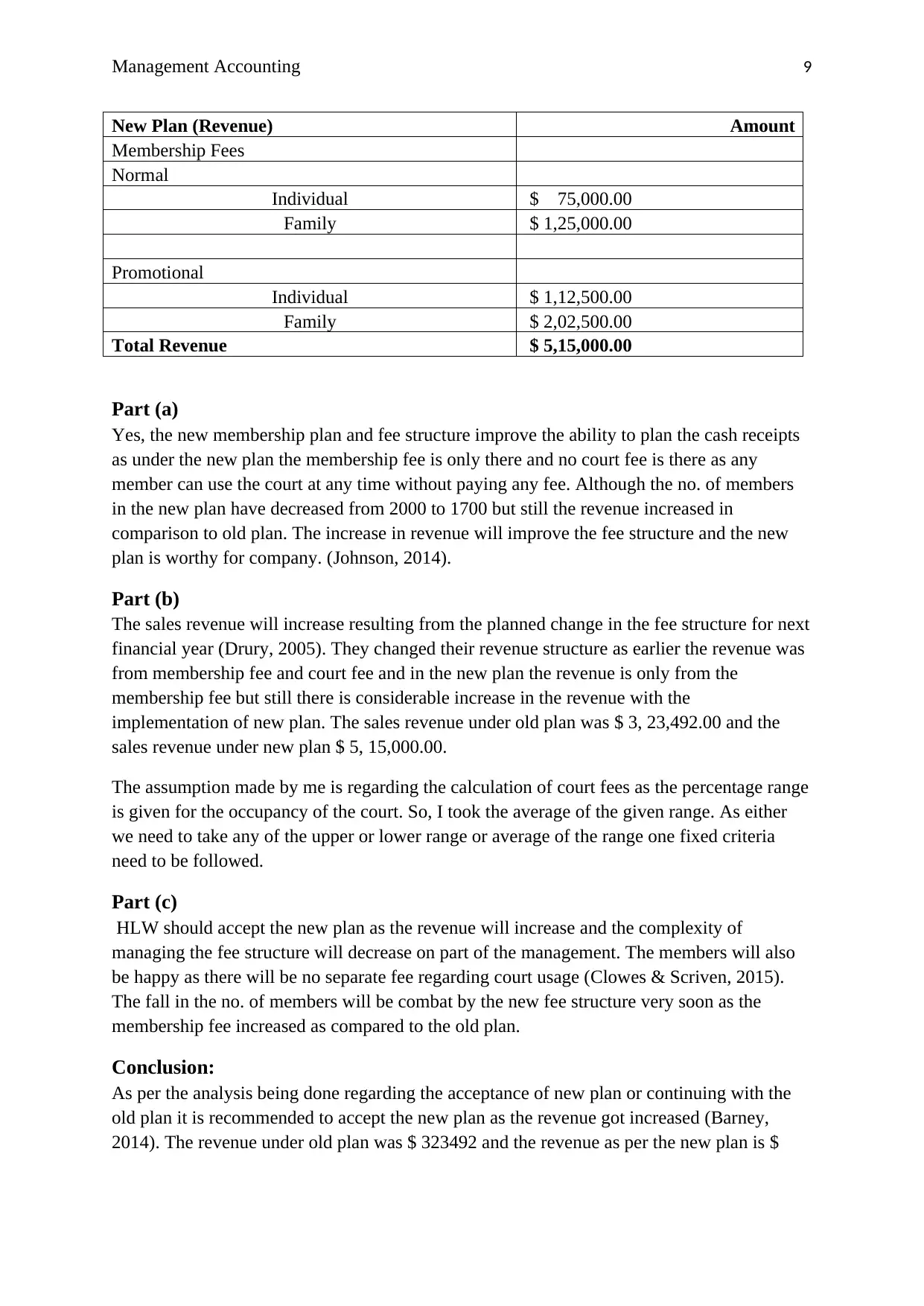

New Plan (Revenue) Amount

Membership Fees

Normal

Individual $ 75,000.00

Family $ 1,25,000.00

Promotional

Individual $ 1,12,500.00

Family $ 2,02,500.00

Total Revenue $ 5,15,000.00

Part (a)

Yes, the new membership plan and fee structure improve the ability to plan the cash receipts

as under the new plan the membership fee is only there and no court fee is there as any

member can use the court at any time without paying any fee. Although the no. of members

in the new plan have decreased from 2000 to 1700 but still the revenue increased in

comparison to old plan. The increase in revenue will improve the fee structure and the new

plan is worthy for company. (Johnson, 2014).

Part (b)

The sales revenue will increase resulting from the planned change in the fee structure for next

financial year (Drury, 2005). They changed their revenue structure as earlier the revenue was

from membership fee and court fee and in the new plan the revenue is only from the

membership fee but still there is considerable increase in the revenue with the

implementation of new plan. The sales revenue under old plan was $ 3, 23,492.00 and the

sales revenue under new plan $ 5, 15,000.00.

The assumption made by me is regarding the calculation of court fees as the percentage range

is given for the occupancy of the court. So, I took the average of the given range. As either

we need to take any of the upper or lower range or average of the range one fixed criteria

need to be followed.

Part (c)

HLW should accept the new plan as the revenue will increase and the complexity of

managing the fee structure will decrease on part of the management. The members will also

be happy as there will be no separate fee regarding court usage (Clowes & Scriven, 2015).

The fall in the no. of members will be combat by the new fee structure very soon as the

membership fee increased as compared to the old plan.

Conclusion:

As per the analysis being done regarding the acceptance of new plan or continuing with the

old plan it is recommended to accept the new plan as the revenue got increased (Barney,

2014). The revenue under old plan was $ 323492 and the revenue as per the new plan is $

New Plan (Revenue) Amount

Membership Fees

Normal

Individual $ 75,000.00

Family $ 1,25,000.00

Promotional

Individual $ 1,12,500.00

Family $ 2,02,500.00

Total Revenue $ 5,15,000.00

Part (a)

Yes, the new membership plan and fee structure improve the ability to plan the cash receipts

as under the new plan the membership fee is only there and no court fee is there as any

member can use the court at any time without paying any fee. Although the no. of members

in the new plan have decreased from 2000 to 1700 but still the revenue increased in

comparison to old plan. The increase in revenue will improve the fee structure and the new

plan is worthy for company. (Johnson, 2014).

Part (b)

The sales revenue will increase resulting from the planned change in the fee structure for next

financial year (Drury, 2005). They changed their revenue structure as earlier the revenue was

from membership fee and court fee and in the new plan the revenue is only from the

membership fee but still there is considerable increase in the revenue with the

implementation of new plan. The sales revenue under old plan was $ 3, 23,492.00 and the

sales revenue under new plan $ 5, 15,000.00.

The assumption made by me is regarding the calculation of court fees as the percentage range

is given for the occupancy of the court. So, I took the average of the given range. As either

we need to take any of the upper or lower range or average of the range one fixed criteria

need to be followed.

Part (c)

HLW should accept the new plan as the revenue will increase and the complexity of

managing the fee structure will decrease on part of the management. The members will also

be happy as there will be no separate fee regarding court usage (Clowes & Scriven, 2015).

The fall in the no. of members will be combat by the new fee structure very soon as the

membership fee increased as compared to the old plan.

Conclusion:

As per the analysis being done regarding the acceptance of new plan or continuing with the

old plan it is recommended to accept the new plan as the revenue got increased (Barney,

2014). The revenue under old plan was $ 323492 and the revenue as per the new plan is $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 10

515000. The benefit is clearly there and no other contention is required to support the new

plan.

515000. The benefit is clearly there and no other contention is required to support the new

plan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 11

References:

Barney, J. B. 2014, Gaining and Sustaining Competitive Advantage, Pearson Higher Ed.

Clowes, R & Scriven, V 2015, Budgeting: A Practical Approach, Pearson Higher Education

AU.

Drury, C 2005, Management Accounting for Business, Cengage Learning EMEA.

Goektuerk, H 2007, Activity Based Costing (ABC) - Advantages and Disadvantages, GRIN

Verlag.

Heisinger, K 2009, Essentials to Managerial Accounting, Cengage Learning.

Johnson, P. F. 2014, Purchasing and Supply Management, McGraw-Hill Higher Education.

Lalli, W. R. 2011, Handbook of Budgeting, John Wiley & Sons.

Potts, Keith, and Ankrah, N 2014, Construction Cost Management: learning from case

studies, Routledge.

Wiese, N 2009, Activity Based Costing, GRIN Verlag.

References:

Barney, J. B. 2014, Gaining and Sustaining Competitive Advantage, Pearson Higher Ed.

Clowes, R & Scriven, V 2015, Budgeting: A Practical Approach, Pearson Higher Education

AU.

Drury, C 2005, Management Accounting for Business, Cengage Learning EMEA.

Goektuerk, H 2007, Activity Based Costing (ABC) - Advantages and Disadvantages, GRIN

Verlag.

Heisinger, K 2009, Essentials to Managerial Accounting, Cengage Learning.

Johnson, P. F. 2014, Purchasing and Supply Management, McGraw-Hill Higher Education.

Lalli, W. R. 2011, Handbook of Budgeting, John Wiley & Sons.

Potts, Keith, and Ankrah, N 2014, Construction Cost Management: learning from case

studies, Routledge.

Wiese, N 2009, Activity Based Costing, GRIN Verlag.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.