Management Accounting: Functions, Systems, and Analysis

VerifiedAdded on 2020/06/04

|15

|4846

|45

Report

AI Summary

This report provides a detailed overview of management accounting, exploring its functions, types, and importance within organizations. It covers key aspects like financial and management accounting differences, various accounting systems, and their benefits, with a focus on Imda Tech's practices. The report delves into costing methods such as absorption and marginal costing, comparing their purposes and applications. It further examines budget preparation, planning, and financial problem analysis, including the use of balance scorecards. The analysis includes critical evaluations of accounting systems, financial reporting, and data analysis of financial performance, offering insights into how management accounting aids in effective decision-making and problem-solving within a business context. The report also highlights the importance of inventory management, job costing, and price optimization systems for companies like Imda Tech and how these accounting systems help in making internal departments more effective. Finally, the report evaluates the planning process and the use of accounting tools to overcome financial problems.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Preparation of report over management accounting functions.............................................1

P2: Management accounting types which are used in an organisation ......................................3

M1: Benefits of accounting system ............................................................................................4

D1: Critical analysis of accounting systems and reporting.........................................................4

TASK 2............................................................................................................................................4

P3: Various costing methods use by Imda Tech .......................................................................4

M2: Analysis of fiscal reporting.................................................................................................8

D2: Data analysis of financial performances of a company.......................................................8

TASK 3............................................................................................................................................8

P4: Preparation of budget............................................................................................................8

M3: Evaluation of planning and its application........................................................................10

D3: Analysis of financial problems...........................................................................................10

TASK 4..........................................................................................................................................11

P5: Balance score card use as an important tool to solve financial issues................................11

M4 Analysis of the problems....................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Preparation of report over management accounting functions.............................................1

P2: Management accounting types which are used in an organisation ......................................3

M1: Benefits of accounting system ............................................................................................4

D1: Critical analysis of accounting systems and reporting.........................................................4

TASK 2............................................................................................................................................4

P3: Various costing methods use by Imda Tech .......................................................................4

M2: Analysis of fiscal reporting.................................................................................................8

D2: Data analysis of financial performances of a company.......................................................8

TASK 3............................................................................................................................................8

P4: Preparation of budget............................................................................................................8

M3: Evaluation of planning and its application........................................................................10

D3: Analysis of financial problems...........................................................................................10

TASK 4..........................................................................................................................................11

P5: Balance score card use as an important tool to solve financial issues................................11

M4 Analysis of the problems....................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an utmost important aspects of any business concern those are

dealing with the large number of financial transactions. It is mostly related with collecting,

recording and summarised of the financial data those are performed during the year. In an

organisation the investors take their valuable decision after making analysis of financial

statements of the cited company (Burritt, Schaltegger and Zvezdov, 2011). Under this project

report, there are various tasks in been covered which are related with management account and

its functions. It importance in making effective decision. There are different types of accounting

systems which are used in recording of transactions are discussed under this project. Or, analysed

the net profit by using various costing methods for Imda Tech Ltd. Use of budgets and its

advantages in preparing plan are also elaborated with its process and related price strategies.

Financial problems which are arise in an organisation explain and how to overcome it by

applying various tools and techniques are mentioned in this report.

TASK 1

P1: Preparation of report over management accounting functions

In an organization, accounting is considered to be effective tool to manage and evaluate

costs and various financial and non – financial transactions. It set a base for managers to take

valuable decisions in order to achieve its aims and objectives those are targeted by the cited

company's. Generally, such accounting reports are prepared at the end of financial year. It consist

of income statements and balance sheet. Both finance and accounting are crucial aspects for a

business entity, but serves various objectives (Albu and Albu, 2012). Management accounting is

mainly concern with operational reports, those are apportioned within a cited company's. While,

financial accounting is comply with different accounting standards which are set in order to

frame a plan.

Topic Financial accounting Management accounting

Purpose The main objectives of financial

accounting is to prepare cyclic reports

to shareholder and other external

parties.

On the other hand management

accounting describe informations to

the top authority to make plan and

control various responses.

1

Management accounting is an utmost important aspects of any business concern those are

dealing with the large number of financial transactions. It is mostly related with collecting,

recording and summarised of the financial data those are performed during the year. In an

organisation the investors take their valuable decision after making analysis of financial

statements of the cited company (Burritt, Schaltegger and Zvezdov, 2011). Under this project

report, there are various tasks in been covered which are related with management account and

its functions. It importance in making effective decision. There are different types of accounting

systems which are used in recording of transactions are discussed under this project. Or, analysed

the net profit by using various costing methods for Imda Tech Ltd. Use of budgets and its

advantages in preparing plan are also elaborated with its process and related price strategies.

Financial problems which are arise in an organisation explain and how to overcome it by

applying various tools and techniques are mentioned in this report.

TASK 1

P1: Preparation of report over management accounting functions

In an organization, accounting is considered to be effective tool to manage and evaluate

costs and various financial and non – financial transactions. It set a base for managers to take

valuable decisions in order to achieve its aims and objectives those are targeted by the cited

company's. Generally, such accounting reports are prepared at the end of financial year. It consist

of income statements and balance sheet. Both finance and accounting are crucial aspects for a

business entity, but serves various objectives (Albu and Albu, 2012). Management accounting is

mainly concern with operational reports, those are apportioned within a cited company's. While,

financial accounting is comply with different accounting standards which are set in order to

frame a plan.

Topic Financial accounting Management accounting

Purpose The main objectives of financial

accounting is to prepare cyclic reports

to shareholder and other external

parties.

On the other hand management

accounting describe informations to

the top authority to make plan and

control various responses.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Time aspects It is based on past activities of

financial data. Historical prospectives

are need to be considered.

The total emphasis is delivered current

year positions. But, for future target.

Subject concern It mainly targets on the whole

organisation.

It is based on a particular areas that is

needs improvement.

Auditing Under this system, it is necessary for

external parties (Hoque, 2011).

It is not compulsory to audit. As

decisions are wholly made by top

authority.

Requirement It must follow GAAP and a order

format.

There is no need to follow any

prescribed format.

Measurement In financial accounting, only cash

transactions are recorded.

It consist of non-monetary activities

such as competition and changes in the

cost of money.

Scope It has narrow. It has board scope.

Importance of management accounting: It provide quantitate message regarding economical

situations those are associated with factors which are present in an accounting system. The

importance of this is not only for the management concern but also for other external parties to

come up with various effective (Macintosh and Quattrone, 2010). Some importance are

explained as under:

Related cost analysis: It is mostly used by the company to estimated what should be sold

and how an organisation sell it. The costs analysis is used to identified total costs which are

incurred during that process.

ABC Costing: It is said to be that tools which a manager identifies various activities in

an organization and assigns the cost of every activities. It is based on that cost of production

done by the company through its available resources.

Buying techniques: Some of the decision are primary use of managerial accounting data

which is used in production process.

Utilizing the data: It provide a positive ideas to the company regarding how to increase

small scale business.

2

financial data. Historical prospectives

are need to be considered.

The total emphasis is delivered current

year positions. But, for future target.

Subject concern It mainly targets on the whole

organisation.

It is based on a particular areas that is

needs improvement.

Auditing Under this system, it is necessary for

external parties (Hoque, 2011).

It is not compulsory to audit. As

decisions are wholly made by top

authority.

Requirement It must follow GAAP and a order

format.

There is no need to follow any

prescribed format.

Measurement In financial accounting, only cash

transactions are recorded.

It consist of non-monetary activities

such as competition and changes in the

cost of money.

Scope It has narrow. It has board scope.

Importance of management accounting: It provide quantitate message regarding economical

situations those are associated with factors which are present in an accounting system. The

importance of this is not only for the management concern but also for other external parties to

come up with various effective (Macintosh and Quattrone, 2010). Some importance are

explained as under:

Related cost analysis: It is mostly used by the company to estimated what should be sold

and how an organisation sell it. The costs analysis is used to identified total costs which are

incurred during that process.

ABC Costing: It is said to be that tools which a manager identifies various activities in

an organization and assigns the cost of every activities. It is based on that cost of production

done by the company through its available resources.

Buying techniques: Some of the decision are primary use of managerial accounting data

which is used in production process.

Utilizing the data: It provide a positive ideas to the company regarding how to increase

small scale business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2: Management accounting types which are used in an organisation

With the proper utilisation of accounting in a cited company such as Imda Tech can

stabilise its financial performance. Financial position can be analysed through using such kind of

techniques which are helpful in decision making precess (Quinn, 2014). Under the IMDA Tech

they are using price optimisation, cost accounting and inventory accounting system in their

business to maintain its business activities. It will be easy for the managers to identified various

investments and cost those are used in production process during the financial year. In order to

make internal department more effective company are using various types of accounting system

which make the way to gain maximum profit in future. It will also guide the manager to use

those system in such a ways so that company would achieve its target in fixed allotted time.

Following types of systems are used by the cited company:

Inventory management system: In an organization stock management department are

responsible for controlling and maintains of their inventory. These are done so because it can be

use during production. There are so techniques which can be used by the managers to maintain

their stock level. Such as: ABC techniques which is used by the company according to the

durability and quality of the stock present. Other methods are related with shipping, tracking and

recording of stock eateries.

Cost accounting system: It is said to be that techniques which are used by the managers

in order to overcome the cost which are incurred during the production process. It will help to

determine total cost of goods for analysis of gains, inventory evaluation and to manager the extra

unit costs of production (Pitkänen and Lukka, 2011). As it has been observed that costs are one

of the most important aspect for the company which they can use it in future expansion of their

business. It consist of various other costing such as standard costing, normal and actual costing

which are incurred in direct cost of productions.

Job costing system: Under this system of accounting, manufacturing cost to an

individual goods or products batches. It is used as when the goods those are manufactured are

related with different from each other. In Imda Tech the products are arranged in a sequences as

a unit of chain so the they can easily calculated. These are said to be combines costs which are

which incurred on the individual units of products or each unit of production.

Price optimisation system: Under this system company which need to determine the

perception of the customers. That is they are able to buy products according to the range set by

3

With the proper utilisation of accounting in a cited company such as Imda Tech can

stabilise its financial performance. Financial position can be analysed through using such kind of

techniques which are helpful in decision making precess (Quinn, 2014). Under the IMDA Tech

they are using price optimisation, cost accounting and inventory accounting system in their

business to maintain its business activities. It will be easy for the managers to identified various

investments and cost those are used in production process during the financial year. In order to

make internal department more effective company are using various types of accounting system

which make the way to gain maximum profit in future. It will also guide the manager to use

those system in such a ways so that company would achieve its target in fixed allotted time.

Following types of systems are used by the cited company:

Inventory management system: In an organization stock management department are

responsible for controlling and maintains of their inventory. These are done so because it can be

use during production. There are so techniques which can be used by the managers to maintain

their stock level. Such as: ABC techniques which is used by the company according to the

durability and quality of the stock present. Other methods are related with shipping, tracking and

recording of stock eateries.

Cost accounting system: It is said to be that techniques which are used by the managers

in order to overcome the cost which are incurred during the production process. It will help to

determine total cost of goods for analysis of gains, inventory evaluation and to manager the extra

unit costs of production (Pitkänen and Lukka, 2011). As it has been observed that costs are one

of the most important aspect for the company which they can use it in future expansion of their

business. It consist of various other costing such as standard costing, normal and actual costing

which are incurred in direct cost of productions.

Job costing system: Under this system of accounting, manufacturing cost to an

individual goods or products batches. It is used as when the goods those are manufactured are

related with different from each other. In Imda Tech the products are arranged in a sequences as

a unit of chain so the they can easily calculated. These are said to be combines costs which are

which incurred on the individual units of products or each unit of production.

Price optimisation system: Under this system company which need to determine the

perception of the customers. That is they are able to buy products according to the range set by

3

the company for there products. prior setting of the price company need to set an objectives after

making proper analysis of the customer attention towards their brand.

From all these methods job costing and inventory is more reliable and accurate for Imda

Tech to manage their electronic gadgets (Hiebl, 2014). The company would be able to plan and

earn extra profit if they are using above mentioned accounting in their business operations.

M1: Benefits of accounting system

From the above analyses of all the management accounting system for the IMDA Tech

Pvt Ltd. Out of them inventory system and job costing system is more reliable and valuable for

generating positive results for the cited company. The basic advantages for using these system is

to maximise the productivity and growth of the company. The efficiency in work among various

departments will increase through using the these systems in more perfect manner. The future

planning and forecasting is also based on the manager decision which they are made with using

those systems. The financial statement can be analysed before making any investment under the

company.

D1: Critical analysis of accounting systems and reporting

According to the Jansen, 2011 reporting of financial transactions can make the company

more effective to take valuable decision regarding the future growth and planning. The main part

of this system is associated with the social and operations need which are arise among

stakeholders of the company. In the above mentioned plan and accounting system a cited

company has budget reporting, inventory reporting and operational expenses reporting system.

These all can be use by the managers in order to prepare a perfect plan and report for future

period. The resources should be utilised in proper manner so that more positive results can be

achieved in order to get its objectives.

TASK 2

P3: Various costing methods use by Imda Tech

In an organisation, there are various costing methods which are used in order to get more

effective outcome in the benefit of a company. It help to determine total cost which are incurred

in manufacturing of products and services during the year. So in the ways to find out after

incurring total cost how much net profit a company able to generated during the year. So in that

process they are using following of the two methods:

4

making proper analysis of the customer attention towards their brand.

From all these methods job costing and inventory is more reliable and accurate for Imda

Tech to manage their electronic gadgets (Hiebl, 2014). The company would be able to plan and

earn extra profit if they are using above mentioned accounting in their business operations.

M1: Benefits of accounting system

From the above analyses of all the management accounting system for the IMDA Tech

Pvt Ltd. Out of them inventory system and job costing system is more reliable and valuable for

generating positive results for the cited company. The basic advantages for using these system is

to maximise the productivity and growth of the company. The efficiency in work among various

departments will increase through using the these systems in more perfect manner. The future

planning and forecasting is also based on the manager decision which they are made with using

those systems. The financial statement can be analysed before making any investment under the

company.

D1: Critical analysis of accounting systems and reporting

According to the Jansen, 2011 reporting of financial transactions can make the company

more effective to take valuable decision regarding the future growth and planning. The main part

of this system is associated with the social and operations need which are arise among

stakeholders of the company. In the above mentioned plan and accounting system a cited

company has budget reporting, inventory reporting and operational expenses reporting system.

These all can be use by the managers in order to prepare a perfect plan and report for future

period. The resources should be utilised in proper manner so that more positive results can be

achieved in order to get its objectives.

TASK 2

P3: Various costing methods use by Imda Tech

In an organisation, there are various costing methods which are used in order to get more

effective outcome in the benefit of a company. It help to determine total cost which are incurred

in manufacturing of products and services during the year. So in the ways to find out after

incurring total cost how much net profit a company able to generated during the year. So in that

process they are using following of the two methods:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing method: It is considered to be that costs which are incurred on direct

cost of production (Hopwood, Unerman and Fries, 2010). It mainly included direct labour,

material and overhead costs. Under this costing fixed costs are not considered except all others.

The main objective of using this method is to find out over and under absorption in that process.

The standard and actual costing which are use to analysed the total outcome from the cited

process.

Marginal costing method: It is associated with that costs which is related with both

fixed and variable costs. Under this process contribution per unit is calculated by the company

in-spite of gross profit. In the calculation of net profit fixed costs are considered with all those

variable costs. In other words, it can be said that costs which are current for the production of

one extra units of products and services.

Comparison among above two costing methods

BASIS ABSORPTION COSTING MARGINAL COSTING

Purpose It is based on external purpose. It is generally, prepared for the internal

reporting.

Profits If the company is having higher

ending stock, the profit will be

higher (Cooper, Ezzamel and Qu,

2017).

If it goes lower of ending stocks, the

profit will get low.

Fixed overhead

treatment

Fixed costs are considered as

product costs.

Under this period cost are considered.

High spot Only Net profit is calculated. Contribution per units are calculated.

Cost per units In this costing, opening and

closing inventory get affected as

the cost per units.

Under this beginning and closing

inventory are not influence as the cost

per unit of total outcome.

Computation of Net profit through using absorption costing

PARTICULAR £Amount £Amount

5

cost of production (Hopwood, Unerman and Fries, 2010). It mainly included direct labour,

material and overhead costs. Under this costing fixed costs are not considered except all others.

The main objective of using this method is to find out over and under absorption in that process.

The standard and actual costing which are use to analysed the total outcome from the cited

process.

Marginal costing method: It is associated with that costs which is related with both

fixed and variable costs. Under this process contribution per unit is calculated by the company

in-spite of gross profit. In the calculation of net profit fixed costs are considered with all those

variable costs. In other words, it can be said that costs which are current for the production of

one extra units of products and services.

Comparison among above two costing methods

BASIS ABSORPTION COSTING MARGINAL COSTING

Purpose It is based on external purpose. It is generally, prepared for the internal

reporting.

Profits If the company is having higher

ending stock, the profit will be

higher (Cooper, Ezzamel and Qu,

2017).

If it goes lower of ending stocks, the

profit will get low.

Fixed overhead

treatment

Fixed costs are considered as

product costs.

Under this period cost are considered.

High spot Only Net profit is calculated. Contribution per units are calculated.

Cost per units In this costing, opening and

closing inventory get affected as

the cost per units.

Under this beginning and closing

inventory are not influence as the cost

per unit of total outcome.

Computation of Net profit through using absorption costing

PARTICULAR £Amount £Amount

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

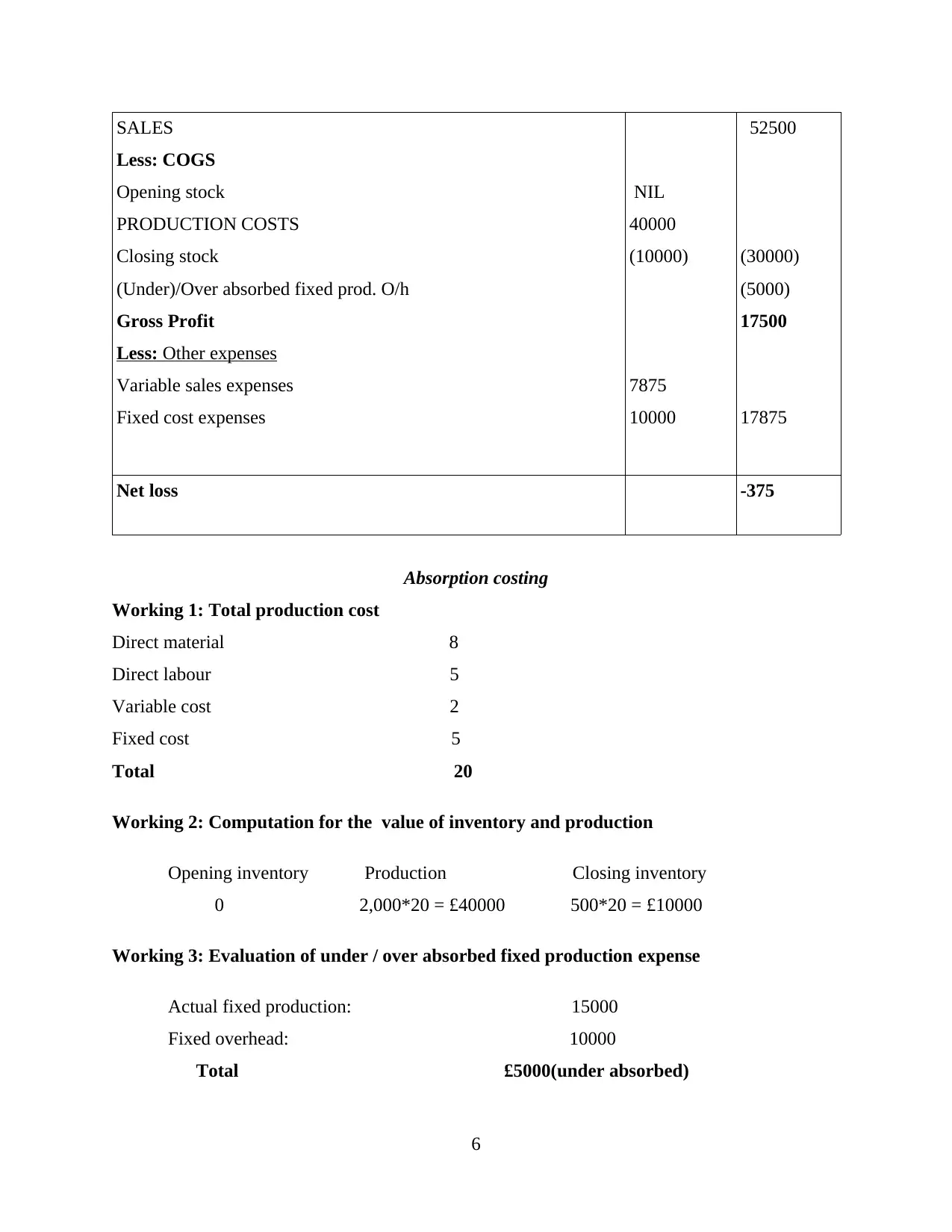

SALES

Less: COGS

Opening stock

PRODUCTION COSTS

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Other expenses

Variable sales expenses

Fixed cost expenses

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

Absorption costing

Working 1: Total production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: Computation for the value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: Evaluation of under / over absorbed fixed production expense

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

6

Less: COGS

Opening stock

PRODUCTION COSTS

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Other expenses

Variable sales expenses

Fixed cost expenses

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

Absorption costing

Working 1: Total production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: Computation for the value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: Evaluation of under / over absorbed fixed production expense

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

6

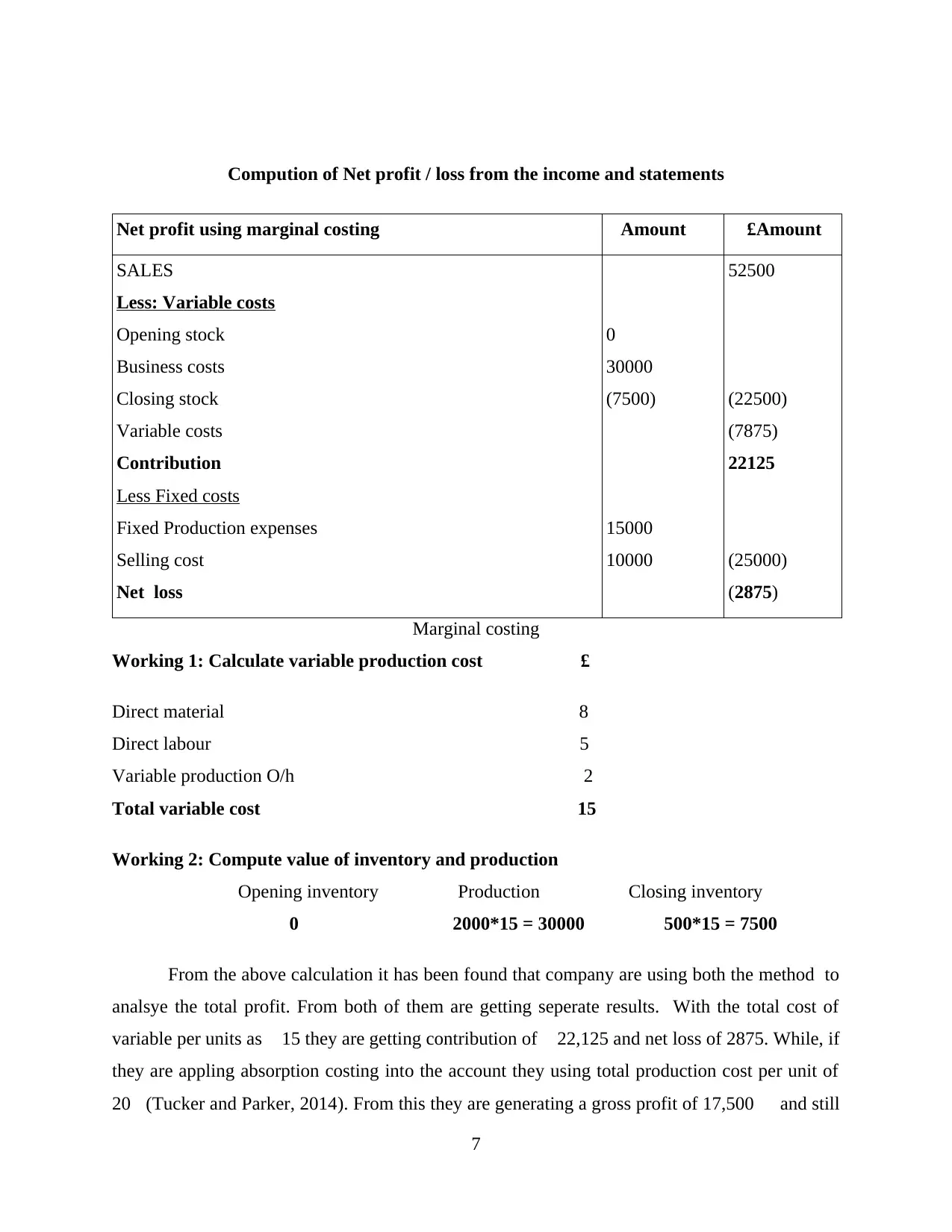

Compution of Net profit / loss from the income and statements

Net profit using marginal costing £Amount £Amount

SALES

Less: Variable costs

Opening stock

Business costs

Closing stock

Variable costs

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal costing

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Total variable cost 15

Working 2: Compute value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

From the above calculation it has been found that company are using both the method to

analsye the total profit. From both of them are getting seperate results. With the total cost of

variable per units as £15 they are getting contribution of£ 22,125 and net loss of 2875. While, if

they are appling absorption costing into the account they using total production cost per unit of

20£(Tucker and Parker, 2014). From this they are generating a gross profit of 17,500 £ and still

7

Net profit using marginal costing £Amount £Amount

SALES

Less: Variable costs

Opening stock

Business costs

Closing stock

Variable costs

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Marginal costing

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Total variable cost 15

Working 2: Compute value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

From the above calculation it has been found that company are using both the method to

analsye the total profit. From both of them are getting seperate results. With the total cost of

variable per units as £15 they are getting contribution of£ 22,125 and net loss of 2875. While, if

they are appling absorption costing into the account they using total production cost per unit of

20£(Tucker and Parker, 2014). From this they are generating a gross profit of 17,500 £ and still

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they are getting a net loss of -375. So the company need to select absorption costing as they

value of loss is much less than the marginal costing. The basic possiblitiy from using the

absorption costing is to identifiy over and under absorption from the total fixed cost. In the above

situation it incurs a under absorption of £5000. so overall results says that company would select

absorption costing as they are more accurate and positive.

M2: Analysis of fiscal reporting

From the above evaluation of accounting system, it has been found that Imda Tech have

various financial techniques which they can make use in their business operations. Some of them

are comparative income statements, working capital and common size balance sheet (Tayles,

2011). From using these techniques a cited company can evaluate their performance and make

changes accordingly. The investors are firstly look over all these statements before making any

investment decision. The more useful statements are profit and loss statements which carries all

the relevant details about company present and previous year performances.

D2: Data analysis of financial performances of a company

According to the above information collected regarding Imda Tech Pvt Ltd financial

analysis. The company is using both marginal and absorption costing methods to analyse the net

profit for the company during the year. It has been found that from absorption costing a total of

5,000 is categories as under absorption. As in either of costing methods, which are used by

IMDA Tech is getting a negative losses. But, from the one which is incurring less loss for the

company would taken into consideration. The final outcome are not enough to analyse the

organization accounting position. The financial reporting can be more useful sometime when

decision are affecting the profitability of the business entity.

TASK 3

P4: Preparation of budget

Budget: It refers as the company's total estimation of costs, sales and other resource

which a company is going to be use in coming time. The budget reflects the financial position

and future growth potential of a particular company (Quinn, 2011). In that phase, an organisation

8

value of loss is much less than the marginal costing. The basic possiblitiy from using the

absorption costing is to identifiy over and under absorption from the total fixed cost. In the above

situation it incurs a under absorption of £5000. so overall results says that company would select

absorption costing as they are more accurate and positive.

M2: Analysis of fiscal reporting

From the above evaluation of accounting system, it has been found that Imda Tech have

various financial techniques which they can make use in their business operations. Some of them

are comparative income statements, working capital and common size balance sheet (Tayles,

2011). From using these techniques a cited company can evaluate their performance and make

changes accordingly. The investors are firstly look over all these statements before making any

investment decision. The more useful statements are profit and loss statements which carries all

the relevant details about company present and previous year performances.

D2: Data analysis of financial performances of a company

According to the above information collected regarding Imda Tech Pvt Ltd financial

analysis. The company is using both marginal and absorption costing methods to analyse the net

profit for the company during the year. It has been found that from absorption costing a total of

5,000 is categories as under absorption. As in either of costing methods, which are used by

IMDA Tech is getting a negative losses. But, from the one which is incurring less loss for the

company would taken into consideration. The final outcome are not enough to analyse the

organization accounting position. The financial reporting can be more useful sometime when

decision are affecting the profitability of the business entity.

TASK 3

P4: Preparation of budget

Budget: It refers as the company's total estimation of costs, sales and other resource

which a company is going to be use in coming time. The budget reflects the financial position

and future growth potential of a particular company (Quinn, 2011). In that phase, an organisation

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have so many types of budgets which can be prepared from taken guidance from the other

departments.

Importance of budgets:

It is helpful for the development of company performance in future in order to increase

the goodwill in the market.

Productivity of the company is the main aspect which need to be increase through using

various budgets.

Total costs which are incurred during production process can be analysed through

operating budgets.

Budgets are important tool for making appropriate decision for the company.

Types of Budgets:

Operating budgets: This is related with the expenses which a cited company uses during the

production of goods and services. It indicate a future forecasting of total income required in

order to produce products for the selected time period (Setthasakko, 2010). All those direct costs

which are impact the profitably of the company are need to be analysed through this budgets.

Advantages

Total expenses are identified during the year are identified from this budgets.

The alarming losses should be controlled by the company.

Disadvantage:

Misuse and cost can be control by the single person during the year.

The regular monetary of production expense can not be done properly.

Master budget: It is the combination of all the financial budget which are made by

manager to bring all the activities into common point. The most of the investors are use to take

decision according this budgets.

Advantages:

It explains all the main problems of the company that they are facing during the year.

The overall growth and performance are identified from this single budgets.

Disadvantage:

Lack of control of department.

Taken more time to prepared a accurate budgets.

9

departments.

Importance of budgets:

It is helpful for the development of company performance in future in order to increase

the goodwill in the market.

Productivity of the company is the main aspect which need to be increase through using

various budgets.

Total costs which are incurred during production process can be analysed through

operating budgets.

Budgets are important tool for making appropriate decision for the company.

Types of Budgets:

Operating budgets: This is related with the expenses which a cited company uses during the

production of goods and services. It indicate a future forecasting of total income required in

order to produce products for the selected time period (Setthasakko, 2010). All those direct costs

which are impact the profitably of the company are need to be analysed through this budgets.

Advantages

Total expenses are identified during the year are identified from this budgets.

The alarming losses should be controlled by the company.

Disadvantage:

Misuse and cost can be control by the single person during the year.

The regular monetary of production expense can not be done properly.

Master budget: It is the combination of all the financial budget which are made by

manager to bring all the activities into common point. The most of the investors are use to take

decision according this budgets.

Advantages:

It explains all the main problems of the company that they are facing during the year.

The overall growth and performance are identified from this single budgets.

Disadvantage:

Lack of control of department.

Taken more time to prepared a accurate budgets.

9

Cash budget: It is the document that shows the total of estimated inflow or outflow of funds in a

particular time frame. It is an important tool as this way an organisation can plan its cash

requirements and also decision regarding maintaining liquidity can also be taken.

Advantages

Helps in avoiding the situation of shortage in finance

Disadvantages

It is difficult to formulate

require experts for correct preparations

Process of budgeting

It is a difficult process that starts with defining the need of it. Than the past actual data

regarding the subject matter is analysed from which a base for budget is prepared. Than the

available information us access and final plan is made (TalhaRaj aand Seetharaman, 2010).

Thereafter, the process of reviewing the prepared budget starts which continues to reporting and

posting of the prepared program. Lastly when the whole process is completed and execution

starts monitoring is done on its progress so as to see weather it is effective or not.

Pricing strategies: It refers to that plan which are set by the company for there products

and services according to get competitive advantages from other company's. Some of them are:

Price penetration which is based on low price in order to maximise the market share and

competition.

No- frill pricing is a type of pricing which a company used to set for those customers who

are more sensitive in paying high prices.

M3: Evaluation of planning and its application

From the above analyse it has been found that company can increase its performance and

stability through using various budgets. As because, future forecasting can only be done after

proper estimation is generated by the company. Cost benefit and operating expenses analyse can

be the major application which can be analysed properly.

D3: Analysis of financial problems

In the process of resolving financial issues of a company. There are various techniques

which can be used by the company to manage and control the operations. In that process Key

performance indicator, benchmarking are the common tools can be more effective.

10

particular time frame. It is an important tool as this way an organisation can plan its cash

requirements and also decision regarding maintaining liquidity can also be taken.

Advantages

Helps in avoiding the situation of shortage in finance

Disadvantages

It is difficult to formulate

require experts for correct preparations

Process of budgeting

It is a difficult process that starts with defining the need of it. Than the past actual data

regarding the subject matter is analysed from which a base for budget is prepared. Than the

available information us access and final plan is made (TalhaRaj aand Seetharaman, 2010).

Thereafter, the process of reviewing the prepared budget starts which continues to reporting and

posting of the prepared program. Lastly when the whole process is completed and execution

starts monitoring is done on its progress so as to see weather it is effective or not.

Pricing strategies: It refers to that plan which are set by the company for there products

and services according to get competitive advantages from other company's. Some of them are:

Price penetration which is based on low price in order to maximise the market share and

competition.

No- frill pricing is a type of pricing which a company used to set for those customers who

are more sensitive in paying high prices.

M3: Evaluation of planning and its application

From the above analyse it has been found that company can increase its performance and

stability through using various budgets. As because, future forecasting can only be done after

proper estimation is generated by the company. Cost benefit and operating expenses analyse can

be the major application which can be analysed properly.

D3: Analysis of financial problems

In the process of resolving financial issues of a company. There are various techniques

which can be used by the company to manage and control the operations. In that process Key

performance indicator, benchmarking are the common tools can be more effective.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.