Management Accounting Report: Cost Analysis, and Planning Strategies

VerifiedAdded on 2020/07/23

|16

|5113

|31

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the Balti Palace restaurant. It begins by outlining the essential management accounting systems, including cost accounting, inventory management, and price optimization. The report then explores the significance of managerial reports, such as budget reports, cost reports, receivable aging reports, and inventory reports, in aiding decision-making processes. Furthermore, it delves into the evaluation of cost and profit margins using both absorption and marginal costing techniques, providing a comparative analysis of their application. The report also assesses various tools that management accountants can utilize for effective planning and addresses the role of management accounting in responding to monetary challenges faced by the business. Overall, the report offers valuable insights into the practical implementation of management accounting strategies to improve financial performance and operational efficiency.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

P1 Stating management accounting (MA) systems that firm needs to employ....................1

P2 Presenting the manner in which managerial reports aid in decision making....................3

P3 Evaluation of cost and profit margin on the basis of different techniques such as

absorption and marginal.........................................................................................................5

P4 Assessing tools that can be used by management accountant for planning......................8

P5 Stating tools of MA that helps business organization in responding monetary problems

..............................................................................................................................................11

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION......................................................................................................................1

P1 Stating management accounting (MA) systems that firm needs to employ....................1

P2 Presenting the manner in which managerial reports aid in decision making....................3

P3 Evaluation of cost and profit margin on the basis of different techniques such as

absorption and marginal.........................................................................................................5

P4 Assessing tools that can be used by management accountant for planning......................8

P5 Stating tools of MA that helps business organization in responding monetary problems

..............................................................................................................................................11

CONCLUSION........................................................................................................................14

REFERENCES.........................................................................................................................15

INTRODUCTION

In the current times, every business unit, whether small or large sized, places high

level of emphasis on undertaking management accounting tools and techniques. Tools and

techniques of management accounting assist manager in preparing financial reports. By

making evaluation of managerial accounting reports manager of the firm can take effectual

day to day and short term decisions. For this project report, Balti Palace restaurant has been

selected that offer dinning services to the customers at suitable prices. In this, current report

will provide deeper insight about management accounting system and reporting aspects.

Further, it also entails the manner in which marginal and absorption costing helps in doing

monetary evaluation. Various planning tools associated with the system of management

accounting will also be evaluated. In addition to this, manner in which managerial accounting

system helps in responding monetary issues will also be analyzed.

P1 Stating management accounting (MA) systems that firm needs to employ

To

Management Team

Balti Palace

Date: 21st January 2018

Subject : Management accounting systems

Introduction: In this, report will provide insight about the extent to which MA and its tools

as well as systems are essential for restaurant unit. Along with this, report also presents

benefits and drawbacks which are associated with different types of management accounting

systems.

Main Body:

Management accounting and its significance

MA is the process of preparing reports, related to internal operations, that provide

information about performance and helps in devising suitable plan. In the current times,

management accounting system is used by business unit’s at large level. By using the tools

and provision of management accounting restaurant unit can make appropriate forecast

regarding future aspects (Management accounting and its importance, 2018). Besides this, MA

In the current times, every business unit, whether small or large sized, places high

level of emphasis on undertaking management accounting tools and techniques. Tools and

techniques of management accounting assist manager in preparing financial reports. By

making evaluation of managerial accounting reports manager of the firm can take effectual

day to day and short term decisions. For this project report, Balti Palace restaurant has been

selected that offer dinning services to the customers at suitable prices. In this, current report

will provide deeper insight about management accounting system and reporting aspects.

Further, it also entails the manner in which marginal and absorption costing helps in doing

monetary evaluation. Various planning tools associated with the system of management

accounting will also be evaluated. In addition to this, manner in which managerial accounting

system helps in responding monetary issues will also be analyzed.

P1 Stating management accounting (MA) systems that firm needs to employ

To

Management Team

Balti Palace

Date: 21st January 2018

Subject : Management accounting systems

Introduction: In this, report will provide insight about the extent to which MA and its tools

as well as systems are essential for restaurant unit. Along with this, report also presents

benefits and drawbacks which are associated with different types of management accounting

systems.

Main Body:

Management accounting and its significance

MA is the process of preparing reports, related to internal operations, that provide

information about performance and helps in devising suitable plan. In the current times,

management accounting system is used by business unit’s at large level. By using the tools

and provision of management accounting restaurant unit can make appropriate forecast

regarding future aspects (Management accounting and its importance, 2018). Besides this, MA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also helps in analyzing the rate of return and enables to do profit planning. Further, field of

MA assists in making appropriate estimation of cash flows and understanding performance

variances. All such aspects clearly shows that management accounting tools & techniques aid

in the growth and success of firm significantly.

Systems of management accounting and their essential requirements within the firm

Cost accounting: It is the process of recording, classifying, analyzing, summarizing

and evaluating alternative course of action. In the context of concerned restaurant

unit, requirement of cost accounting system is significant which in turn advises

appropriate course of action to management on the basis of efficiency and capability

(Edmonds and et.al., 2016). In addition to this, data regarding cost incurred pertaining

to carrying out an activity also helps firm in arriving at suitable decision regarding

price.

Advantages Disadvantages

Cost accounting system helps in

eliminating wastage, losses and

inefficiencies

Under such system, new methods

are followed which in turn leads

cost reduction.

Facilitates price fixation and helps

in doing marginal analysis of cost.

Costing records serve information

about past, whereas management

team is concerning about future.

Further, costs are usually absorbed

on the basis of pre determined rate

which in turn leads the issue of

under or over absorption of

overhead (Advantages and

Disadvantages of Cost

Accounting, 2018).

Inventory management: Such system helps firm in assessing stock level that needs to

be managed within the firm. Restaurant unit is required to consider suitable inventory

management and valuation tools such as EOQ, JIT, LIFO, FIFO etc which in turn

leads cost reduction (Kim and Schmidgall, 2017). Moreover, ordering and holding

cost enhance the level of overall expenses significantly.

Advantages Disadvantages

Reduction in cost

Maximization of profit margin

For developing skills of personnel

in relation to dealing with

inventory software firm needs to

MA assists in making appropriate estimation of cash flows and understanding performance

variances. All such aspects clearly shows that management accounting tools & techniques aid

in the growth and success of firm significantly.

Systems of management accounting and their essential requirements within the firm

Cost accounting: It is the process of recording, classifying, analyzing, summarizing

and evaluating alternative course of action. In the context of concerned restaurant

unit, requirement of cost accounting system is significant which in turn advises

appropriate course of action to management on the basis of efficiency and capability

(Edmonds and et.al., 2016). In addition to this, data regarding cost incurred pertaining

to carrying out an activity also helps firm in arriving at suitable decision regarding

price.

Advantages Disadvantages

Cost accounting system helps in

eliminating wastage, losses and

inefficiencies

Under such system, new methods

are followed which in turn leads

cost reduction.

Facilitates price fixation and helps

in doing marginal analysis of cost.

Costing records serve information

about past, whereas management

team is concerning about future.

Further, costs are usually absorbed

on the basis of pre determined rate

which in turn leads the issue of

under or over absorption of

overhead (Advantages and

Disadvantages of Cost

Accounting, 2018).

Inventory management: Such system helps firm in assessing stock level that needs to

be managed within the firm. Restaurant unit is required to consider suitable inventory

management and valuation tools such as EOQ, JIT, LIFO, FIFO etc which in turn

leads cost reduction (Kim and Schmidgall, 2017). Moreover, ordering and holding

cost enhance the level of overall expenses significantly.

Advantages Disadvantages

Reduction in cost

Maximization of profit margin

For developing skills of personnel

in relation to dealing with

inventory software firm needs to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conduct training and development

session.

Price optimization: By using such system, restaurant unit can analyze the manner in

which customers are reacting at varied price level (Olesen and Cheng, 2017). Hence,

setting suitable prices on the basis of such system restaurant unit can deal with the

competitive environment or situation prominently.

Advantages Disadvantages

Helps in enhancing customer base

Leads high productivity and

margin

Complex in nature

Conclusion: At the end of this report, it can be mentioned that management accounting

systems help in managing funds and operations in the best possible way. Along with this, it

can summarized from evaluation through undertaking cost accounting, inventory

management and price optimization firm can control operations more effectually.

Management Accountant

P2 Presenting the manner in which managerial reports aid in decision making

To

Management Team

Balti Palace

Date: 21st January 2018

Subject : Managerial reports and its significance

Introduction: This report highlights the significance of managerial reports in the context of

restaurant unit. Besides this, it also entails different types of report that restaurant can prepare

for getting monetary information.

Main Body

Managerial reports provide business unit with the performance of every department in

financial terms. By undertaking such reports manager can assess the extent to which each

department is performing well. Hence, by making evaluation of managerial reports

management team can develop competent framework for performance improvement.

From assessment, it has identified that managerial reports have high level of importance for

session.

Price optimization: By using such system, restaurant unit can analyze the manner in

which customers are reacting at varied price level (Olesen and Cheng, 2017). Hence,

setting suitable prices on the basis of such system restaurant unit can deal with the

competitive environment or situation prominently.

Advantages Disadvantages

Helps in enhancing customer base

Leads high productivity and

margin

Complex in nature

Conclusion: At the end of this report, it can be mentioned that management accounting

systems help in managing funds and operations in the best possible way. Along with this, it

can summarized from evaluation through undertaking cost accounting, inventory

management and price optimization firm can control operations more effectually.

Management Accountant

P2 Presenting the manner in which managerial reports aid in decision making

To

Management Team

Balti Palace

Date: 21st January 2018

Subject : Managerial reports and its significance

Introduction: This report highlights the significance of managerial reports in the context of

restaurant unit. Besides this, it also entails different types of report that restaurant can prepare

for getting monetary information.

Main Body

Managerial reports provide business unit with the performance of every department in

financial terms. By undertaking such reports manager can assess the extent to which each

department is performing well. Hence, by making evaluation of managerial reports

management team can develop competent framework for performance improvement.

From assessment, it has identified that managerial reports have high level of importance for

the firm as it provides information about sales etc on day to day basis. In addition to this,

through making evaluation of managerial reports manager can identify training and

development need for personnel. Further, different types of report and their evaluation gives

clear indication in relation to taking suitable measure for the maximization of both

productivity and profitability.

Budget or performance report: This report contains information regarding deviations

occurred in the performance of department during the specified time frame. For

making effective usage of funds company focuses on setting standards that employees

need to follow while performing activities. In this, budget report entails the level to

which expenses incurred by the department are in accordance with the budgeting

framework (Appelbaum and et.al., 2017). Further, performance report also entails the

causes of deficiencies found. Thus, considering such report manager of Balti Palace

can formulate sound strategic and policy framework. Further, through such report

manager also would become able to set appropriate budget and standards for the

upcoming time period.

Cost report: For effective decision making, manager of the firm also needs to prepare

costing report. Costing report contains information about the expenses incurred for

producing or offering products and services. By undertaking such report manager can

track cost information over the time frame. This in turn helps business unit in

determining whether there is a need to take strategic measure for controlling cost or

not. In addition to this, cost report also assists firm in setting pricing strategies and

doing profit planning. By accumulating overall expenses and dividing the same from

offering firm can assess per unit cost. Hence, by adding desired level of margin in unit

cost restaurant unit can set prices of offerings.

Receivable ageing report: Such report helps in ascertaining period within which

debtors are making payment. Usually, in restaurant unit, customers use services on

cash basis or term but for the generation of high sales and margin it also makes deal

with tourist firms. In this, by making assessment of ageing report firm can assess the

customers having potential to default in the upcoming time frame (Lachmann, Trapp

and Trapp, 2017). It also clearly exhibits debtors who are making payment within the

assigned credit duration. Thus, such report gives indication whether there is a need to

update existing credit terms or not.

Inventory report: Stock report gives information about ordering and holding cost as

well as level of wastage. Through making evaluation of such report, manager can

through making evaluation of managerial reports manager can identify training and

development need for personnel. Further, different types of report and their evaluation gives

clear indication in relation to taking suitable measure for the maximization of both

productivity and profitability.

Budget or performance report: This report contains information regarding deviations

occurred in the performance of department during the specified time frame. For

making effective usage of funds company focuses on setting standards that employees

need to follow while performing activities. In this, budget report entails the level to

which expenses incurred by the department are in accordance with the budgeting

framework (Appelbaum and et.al., 2017). Further, performance report also entails the

causes of deficiencies found. Thus, considering such report manager of Balti Palace

can formulate sound strategic and policy framework. Further, through such report

manager also would become able to set appropriate budget and standards for the

upcoming time period.

Cost report: For effective decision making, manager of the firm also needs to prepare

costing report. Costing report contains information about the expenses incurred for

producing or offering products and services. By undertaking such report manager can

track cost information over the time frame. This in turn helps business unit in

determining whether there is a need to take strategic measure for controlling cost or

not. In addition to this, cost report also assists firm in setting pricing strategies and

doing profit planning. By accumulating overall expenses and dividing the same from

offering firm can assess per unit cost. Hence, by adding desired level of margin in unit

cost restaurant unit can set prices of offerings.

Receivable ageing report: Such report helps in ascertaining period within which

debtors are making payment. Usually, in restaurant unit, customers use services on

cash basis or term but for the generation of high sales and margin it also makes deal

with tourist firms. In this, by making assessment of ageing report firm can assess the

customers having potential to default in the upcoming time frame (Lachmann, Trapp

and Trapp, 2017). It also clearly exhibits debtors who are making payment within the

assigned credit duration. Thus, such report gives indication whether there is a need to

update existing credit terms or not.

Inventory report: Stock report gives information about ordering and holding cost as

well as level of wastage. Through making evaluation of such report, manager can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assess whether inventory cost is inclined or decreased over the time. By evaluating

this, manager can determine suitable inventory level that needs to be maintained

within the firm for ensuring smooth functioning and reducing cost. Further, cost of the

stock that restaurant unit requires for offering services to the customers are perishable

in nature. Thus, it is advised to restaurant unit to use either EOQ or just in time

method for assessing stock level. This in turn helps in managing cost and enhances

profit margin significantly.

Conclusion: It has been concluded that managerial reports give specific information to the

management about internal performance. Besides this, reports based on managerial reporting

system also helps in taking decision about future aspect. Thus, it is recommended to the

owner of Balti Palace to prepare inventory, debtors, cost and performance report for

measuring or evaluating performance over the time period.

Management Accountant

P3 Evaluation of cost and profit margin on the basis of different techniques such as

absorption and marginal

Specifically, there are mainly two types of costing system that can be undertaken by

the owner of Balti Palace namely marginal and absorption. Both such costing systems help in

determining unit cost and profit margin.

Marginal costing: Decision making technique that is considered for ascertaining total

cost of production recognized as marginal costing. Under marginal costing, variable cost is

treated as product, whereas fixed expenses considered as periodical. In this, cost is classified

in terms of fixed as well as variable and profit is measured in terms of PV ratio (Difference

between Marginal Costing and Absorption Costing, 2018). It highlights contribution that is

associated with each product.

Absorption costing: In accordance with such costing technique, apportionment of cost

is based on its respective centre. Under absorption costing method, business unit considers

both fixed and variable expenses for the determination of total production cost. In this,

overheads are classified in terms of production, administration, selling & distribution

(Soderstrom, Soderstrom and Stewart, 2017). Absorption costing system also known as full

costing in which variances take place in opening and closing stock does not affect per unit

this, manager can determine suitable inventory level that needs to be maintained

within the firm for ensuring smooth functioning and reducing cost. Further, cost of the

stock that restaurant unit requires for offering services to the customers are perishable

in nature. Thus, it is advised to restaurant unit to use either EOQ or just in time

method for assessing stock level. This in turn helps in managing cost and enhances

profit margin significantly.

Conclusion: It has been concluded that managerial reports give specific information to the

management about internal performance. Besides this, reports based on managerial reporting

system also helps in taking decision about future aspect. Thus, it is recommended to the

owner of Balti Palace to prepare inventory, debtors, cost and performance report for

measuring or evaluating performance over the time period.

Management Accountant

P3 Evaluation of cost and profit margin on the basis of different techniques such as

absorption and marginal

Specifically, there are mainly two types of costing system that can be undertaken by

the owner of Balti Palace namely marginal and absorption. Both such costing systems help in

determining unit cost and profit margin.

Marginal costing: Decision making technique that is considered for ascertaining total

cost of production recognized as marginal costing. Under marginal costing, variable cost is

treated as product, whereas fixed expenses considered as periodical. In this, cost is classified

in terms of fixed as well as variable and profit is measured in terms of PV ratio (Difference

between Marginal Costing and Absorption Costing, 2018). It highlights contribution that is

associated with each product.

Absorption costing: In accordance with such costing technique, apportionment of cost

is based on its respective centre. Under absorption costing method, business unit considers

both fixed and variable expenses for the determination of total production cost. In this,

overheads are classified in terms of production, administration, selling & distribution

(Soderstrom, Soderstrom and Stewart, 2017). Absorption costing system also known as full

costing in which variances take place in opening and closing stock does not affect per unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost. In this, cost data is presented in conventional way which in turn helps in determining net

margin. Such costing method entails that due to the inclusion of fixed cost profitability is

highly influenced.

Computation of Unit cost

Absorption costing ( per unit)

in £

Marginal costing (per unit in

£)

Material 6 6

Labour 5 5

Production

overheads

Variable 2 2

Fixed (2100 / 700) 3 Nil

Unit cost of

production 16 13

Gross and net profit evaluation as per absorption costing method

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total manufacturing cost 11,200

Add: Opening inventory 0

Less: closing inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads 100

Costs of goods sold (COGS) 9500

Gross profit (2100 – 9500) 11500

margin. Such costing method entails that due to the inclusion of fixed cost profitability is

highly influenced.

Computation of Unit cost

Absorption costing ( per unit)

in £

Marginal costing (per unit in

£)

Material 6 6

Labour 5 5

Production

overheads

Variable 2 2

Fixed (2100 / 700) 3 Nil

Unit cost of

production 16 13

Gross and net profit evaluation as per absorption costing method

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total manufacturing cost 11,200

Add: Opening inventory 0

Less: closing inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads 100

Costs of goods sold (COGS) 9500

Gross profit (2100 – 9500) 11500

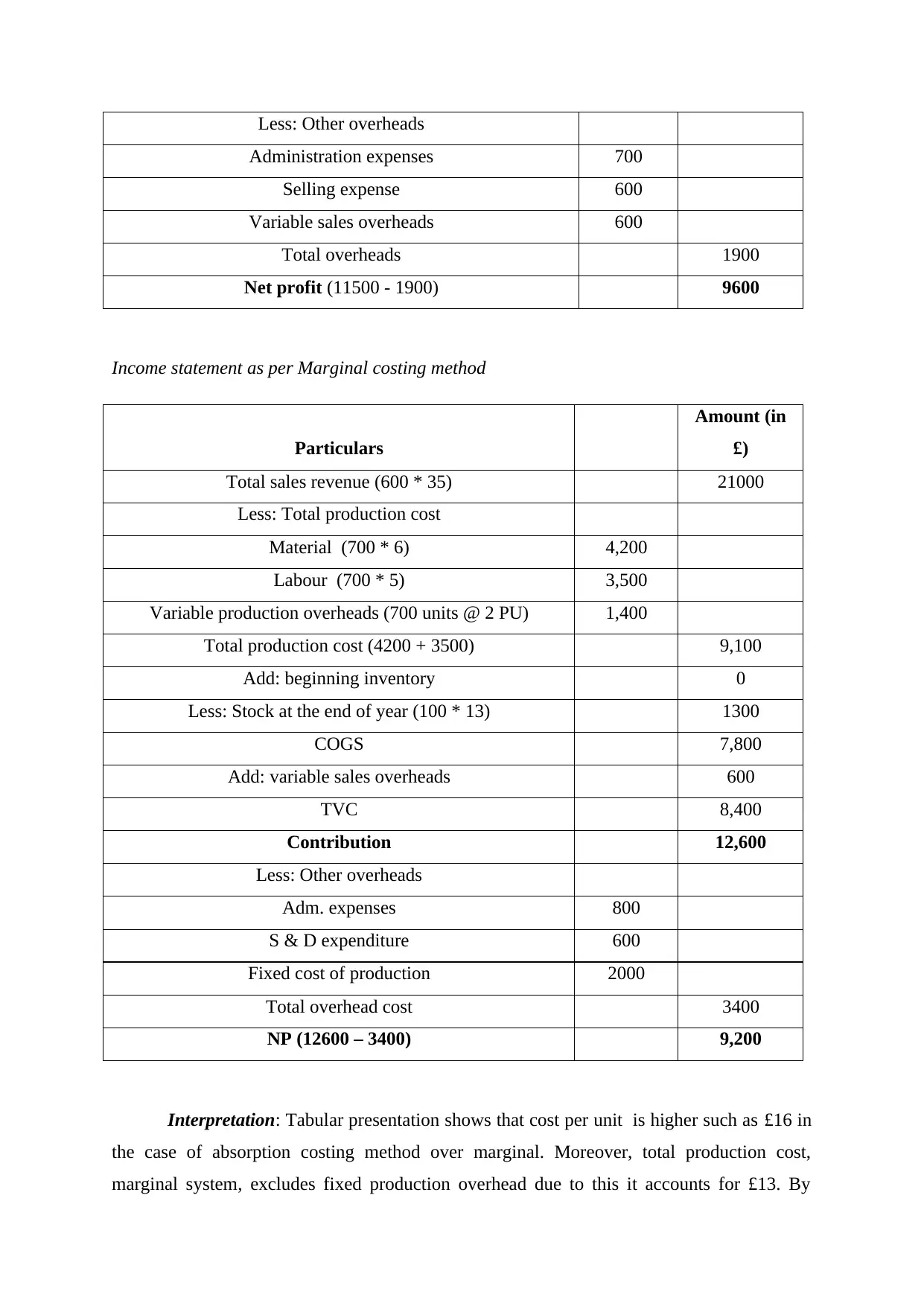

Less: Other overheads

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (11500 - 1900) 9600

Income statement as per Marginal costing method

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4,200

Labour (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500) 9,100

Add: beginning inventory 0

Less: Stock at the end of year (100 * 13) 1300

COGS 7,800

Add: variable sales overheads 600

TVC 8,400

Contribution 12,600

Less: Other overheads

Adm. expenses 800

S & D expenditure 600

Fixed cost of production 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

Interpretation: Tabular presentation shows that cost per unit is higher such as £16 in

the case of absorption costing method over marginal. Moreover, total production cost,

marginal system, excludes fixed production overhead due to this it accounts for £13. By

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (11500 - 1900) 9600

Income statement as per Marginal costing method

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4,200

Labour (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500) 9,100

Add: beginning inventory 0

Less: Stock at the end of year (100 * 13) 1300

COGS 7,800

Add: variable sales overheads 600

TVC 8,400

Contribution 12,600

Less: Other overheads

Adm. expenses 800

S & D expenditure 600

Fixed cost of production 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

Interpretation: Tabular presentation shows that cost per unit is higher such as £16 in

the case of absorption costing method over marginal. Moreover, total production cost,

marginal system, excludes fixed production overhead due to this it accounts for £13. By

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

doing evaluation, it has assessed that GP and net margin according to absorption costing

system accounts for £11500 & £9600 respectively. On the other side, marginal costing

system entails £12600 (contribution) and £9200 (net margin) respectively. By taking into

account overall evaluation it can be mentioned that owner of Balti Palace should undertake

absorption costing system for the assessment of both cost and margin because it is highly

realistic in nature.

Reconciliation statement

Particulars Amount (in £)

NP (according to absorption costing method) 9,600

Less: Fixed production overhead with respect to ending stock (100 * 3) 300

Less: Over-Absorbed overhead 100

Net profit (marginal costing method) 9,200

P4 Assessing tools that can be used by management accountant for planning

In the competitive business arena, for gaining competitive edge over others and

attaining success firm needs to develop an effectual financial plan. There are several

traditional and modern techniques that manager can undertake for developing suitable budget.

Now, every firm creates spending plan with an objective to make effective use of financial

resources. Along with this, budget also helps company in making appropriate estimation

regarding revenue and developing future plan. Hence, by using below mentioned technique

Balti Palace can make effective plan.

Zero base budgeting: This technique of budgeting lays focus on justifying every line

of item or expense before including the same in budget. In accordance with ZBB, managers

start with zero bases and make efforts in relation to assessing cost effective ways of

performing activities (Nuhu, Baird and Bala Appuhamilage, 2017). Hence, manager of Balti

Palace should employ such technique for preparing budget or financial planning. At the time

of considering such technique business entity should keep in mind benefits and drawbacks

associated with ZBB such as:

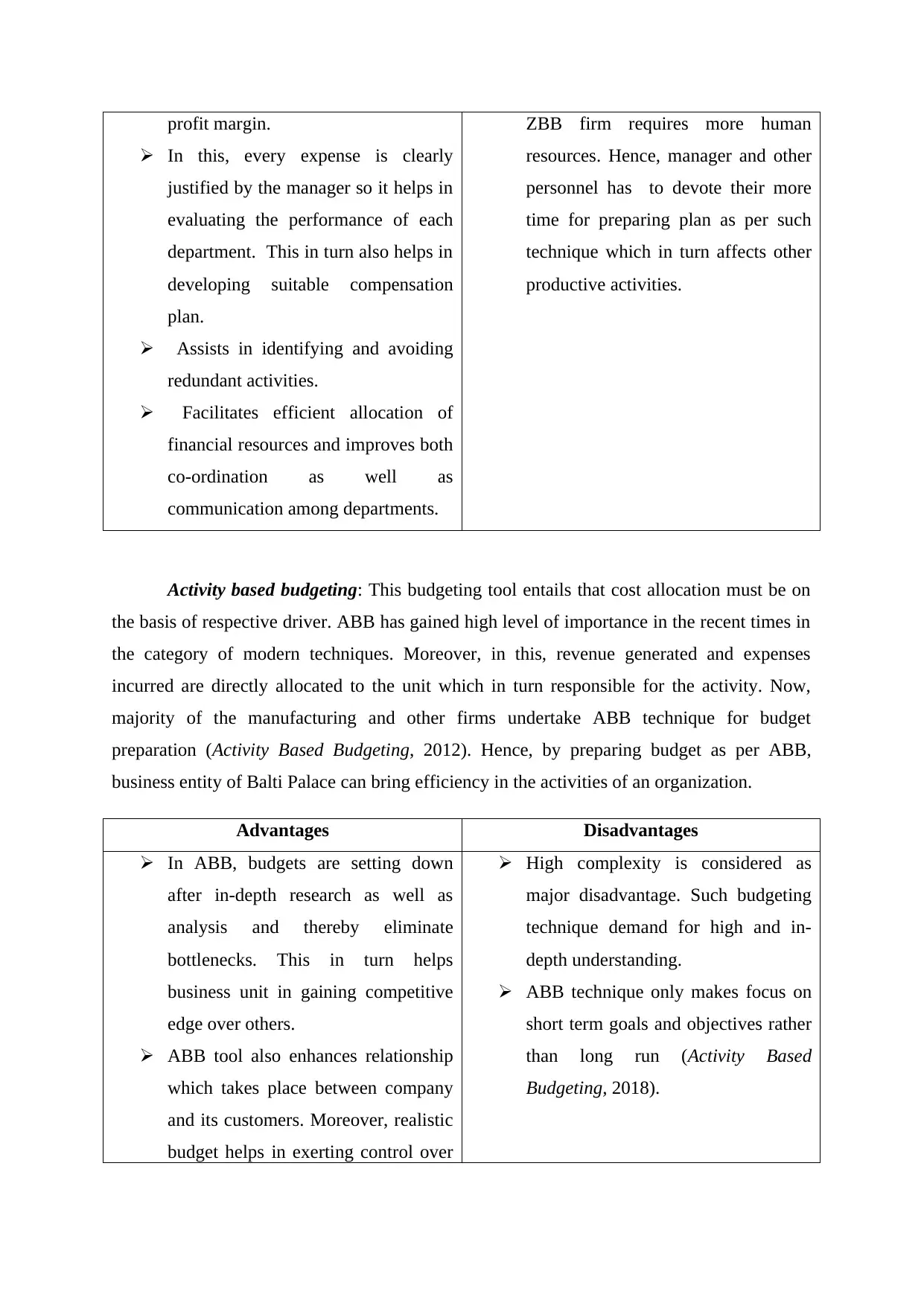

Advantages Disadvantages

Cost effective alternative ensures

enough usage of funds and enhances

Time intensive exercise

For preparing budget according to

system accounts for £11500 & £9600 respectively. On the other side, marginal costing

system entails £12600 (contribution) and £9200 (net margin) respectively. By taking into

account overall evaluation it can be mentioned that owner of Balti Palace should undertake

absorption costing system for the assessment of both cost and margin because it is highly

realistic in nature.

Reconciliation statement

Particulars Amount (in £)

NP (according to absorption costing method) 9,600

Less: Fixed production overhead with respect to ending stock (100 * 3) 300

Less: Over-Absorbed overhead 100

Net profit (marginal costing method) 9,200

P4 Assessing tools that can be used by management accountant for planning

In the competitive business arena, for gaining competitive edge over others and

attaining success firm needs to develop an effectual financial plan. There are several

traditional and modern techniques that manager can undertake for developing suitable budget.

Now, every firm creates spending plan with an objective to make effective use of financial

resources. Along with this, budget also helps company in making appropriate estimation

regarding revenue and developing future plan. Hence, by using below mentioned technique

Balti Palace can make effective plan.

Zero base budgeting: This technique of budgeting lays focus on justifying every line

of item or expense before including the same in budget. In accordance with ZBB, managers

start with zero bases and make efforts in relation to assessing cost effective ways of

performing activities (Nuhu, Baird and Bala Appuhamilage, 2017). Hence, manager of Balti

Palace should employ such technique for preparing budget or financial planning. At the time

of considering such technique business entity should keep in mind benefits and drawbacks

associated with ZBB such as:

Advantages Disadvantages

Cost effective alternative ensures

enough usage of funds and enhances

Time intensive exercise

For preparing budget according to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit margin.

In this, every expense is clearly

justified by the manager so it helps in

evaluating the performance of each

department. This in turn also helps in

developing suitable compensation

plan.

Assists in identifying and avoiding

redundant activities.

Facilitates efficient allocation of

financial resources and improves both

co-ordination as well as

communication among departments.

ZBB firm requires more human

resources. Hence, manager and other

personnel has to devote their more

time for preparing plan as per such

technique which in turn affects other

productive activities.

Activity based budgeting: This budgeting tool entails that cost allocation must be on

the basis of respective driver. ABB has gained high level of importance in the recent times in

the category of modern techniques. Moreover, in this, revenue generated and expenses

incurred are directly allocated to the unit which in turn responsible for the activity. Now,

majority of the manufacturing and other firms undertake ABB technique for budget

preparation (Activity Based Budgeting, 2012). Hence, by preparing budget as per ABB,

business entity of Balti Palace can bring efficiency in the activities of an organization.

Advantages Disadvantages

In ABB, budgets are setting down

after in-depth research as well as

analysis and thereby eliminate

bottlenecks. This in turn helps

business unit in gaining competitive

edge over others.

ABB tool also enhances relationship

which takes place between company

and its customers. Moreover, realistic

budget helps in exerting control over

High complexity is considered as

major disadvantage. Such budgeting

technique demand for high and in-

depth understanding.

ABB technique only makes focus on

short term goals and objectives rather

than long run (Activity Based

Budgeting, 2018).

In this, every expense is clearly

justified by the manager so it helps in

evaluating the performance of each

department. This in turn also helps in

developing suitable compensation

plan.

Assists in identifying and avoiding

redundant activities.

Facilitates efficient allocation of

financial resources and improves both

co-ordination as well as

communication among departments.

ZBB firm requires more human

resources. Hence, manager and other

personnel has to devote their more

time for preparing plan as per such

technique which in turn affects other

productive activities.

Activity based budgeting: This budgeting tool entails that cost allocation must be on

the basis of respective driver. ABB has gained high level of importance in the recent times in

the category of modern techniques. Moreover, in this, revenue generated and expenses

incurred are directly allocated to the unit which in turn responsible for the activity. Now,

majority of the manufacturing and other firms undertake ABB technique for budget

preparation (Activity Based Budgeting, 2012). Hence, by preparing budget as per ABB,

business entity of Balti Palace can bring efficiency in the activities of an organization.

Advantages Disadvantages

In ABB, budgets are setting down

after in-depth research as well as

analysis and thereby eliminate

bottlenecks. This in turn helps

business unit in gaining competitive

edge over others.

ABB tool also enhances relationship

which takes place between company

and its customers. Moreover, realistic

budget helps in exerting control over

High complexity is considered as

major disadvantage. Such budgeting

technique demand for high and in-

depth understanding.

ABB technique only makes focus on

short term goals and objectives rather

than long run (Activity Based

Budgeting, 2018).

cost and thereby provides customers

with services at suitable price.

It facilitates realistic evaluation

because in this every cost driver is

assessed.

Incremental budgeting: Under this, by making some additions in the budget of

previous year, current financial plan is developed by the manager. Hence, in this, previous

year budget is considered as base for arriving at new one. Incremental budgets are prepared

on the basis of assumption that department will continue at their current expense level.

Hence, in this, according to requirement more expenses are included in budget to arrive at

next year budget estimation. Thus, through undertaking incremental budgeting technique

owner of Balti Palace can do financial planning with ease.

Advantages Disadvantages

Incremental budget does not include

complex calculations so it is

considered as time saving exercise

Conflicts among the departments can

be avoided

By using such technique co-

ordination between budgets can easily

be achieved (Incremental Budgeting –

Meaning, Advantages and

Disadvantages, 2018).

Under incremental budgeting

technique, there is the absence of

incentives for cost reduction and

development of new ideas.

Assumption in relation to the

adoption of same activities and

working methods is unrealistic.

Responsibility budgeting: Now, for achieving gaols firm makes focus on creating

several responsibility centre’s regarding revenue, expense, profit etc. On the basis of such

budgeting, all the centre’s are controlled by specific manager and emphasis is placed on the

delegation of basis roles as well as responsibilities. Further, responsibility budgeting tends to

make focus on taking input from the managers of each department. Along with this, on the

identification of deviation owner also asks question regarding the same. Referring all such

aspects, it can be presented that responsibility budgeting helps in planning to a great extent.

with services at suitable price.

It facilitates realistic evaluation

because in this every cost driver is

assessed.

Incremental budgeting: Under this, by making some additions in the budget of

previous year, current financial plan is developed by the manager. Hence, in this, previous

year budget is considered as base for arriving at new one. Incremental budgets are prepared

on the basis of assumption that department will continue at their current expense level.

Hence, in this, according to requirement more expenses are included in budget to arrive at

next year budget estimation. Thus, through undertaking incremental budgeting technique

owner of Balti Palace can do financial planning with ease.

Advantages Disadvantages

Incremental budget does not include

complex calculations so it is

considered as time saving exercise

Conflicts among the departments can

be avoided

By using such technique co-

ordination between budgets can easily

be achieved (Incremental Budgeting –

Meaning, Advantages and

Disadvantages, 2018).

Under incremental budgeting

technique, there is the absence of

incentives for cost reduction and

development of new ideas.

Assumption in relation to the

adoption of same activities and

working methods is unrealistic.

Responsibility budgeting: Now, for achieving gaols firm makes focus on creating

several responsibility centre’s regarding revenue, expense, profit etc. On the basis of such

budgeting, all the centre’s are controlled by specific manager and emphasis is placed on the

delegation of basis roles as well as responsibilities. Further, responsibility budgeting tends to

make focus on taking input from the managers of each department. Along with this, on the

identification of deviation owner also asks question regarding the same. Referring all such

aspects, it can be presented that responsibility budgeting helps in planning to a great extent.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.