Evaluating Management Accounting Tools at Barry House Hotel

VerifiedAdded on 2020/06/04

|15

|4412

|51

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices relevant to the Barry House Hotel. It begins by introducing management accounting and its importance, followed by an examination of specific tools such as cost accounting, price optimization, and inventory management, highlighting their pros and cons. The report then delves into managerial reporting, detailing various types of reports including cost reports, budget/performance reports, debtors reports, and inventory reports, emphasizing their significance in decision-making. Finally, the report explores costing systems, comparing and contrasting absorption and marginal costing methods, and includes income statements calculated using both methods to illustrate their practical application. The report concludes with a summary of the findings, emphasizing the importance of management accounting for effective financial management and decision-making within the hotel context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Managerial accounting is highly concerned with the collection of data related to the

internal operations and functions. In this, management accountant plays a vital role in

analyzing and evaluating data set. Thus, by making internal evaluation manager develops

suitable framework for the maximization of both productivity and profitability. In the present

times, use of management accounting tools and techniques are increased significantly for the

preparation of budget, cost as well as profit analysis. For the concerned project Barry House

hotel has been selected that offers accommodation facility to the customers. Now, company is

interested in using management accounting tools with the objective to control cost and

enhance margin. Moreover, such hotel unit can offer suitable and high quality services to the

customers at affordable prices only when it has good control over cost. Thus, report will

entail the tools and techniques that hotel unit needs to undertake for ensuring effective

management of funds. Besides this, it will also shed light on the costing systems and planning

tools that prove to be more beneficial for hotel.

P1 Presenting management accounting tools and their requirements in the context of Barry

House

To

Management Team

Barry House Hotel

Date: 3rd December 2017

Subject: Management Accounting Systems

Introduction: The present report highlights the system of MA that aid in organizational decision

making, growth as well as success.

Task

Management accounting is the process of collecting, analyzing, interpreting and communicating

results that are associated with the internal business operations. In the context of business unit system

of MA is essentially required for the purpose of effective decision making. Hence, by using the tools

of management accounting business organization can evaluate performance and take cost effective

measures that maximizes both sales as well as profit margin.

Cost accounting: It may be served a process that assists in controlling cost through the means of

Managerial accounting is highly concerned with the collection of data related to the

internal operations and functions. In this, management accountant plays a vital role in

analyzing and evaluating data set. Thus, by making internal evaluation manager develops

suitable framework for the maximization of both productivity and profitability. In the present

times, use of management accounting tools and techniques are increased significantly for the

preparation of budget, cost as well as profit analysis. For the concerned project Barry House

hotel has been selected that offers accommodation facility to the customers. Now, company is

interested in using management accounting tools with the objective to control cost and

enhance margin. Moreover, such hotel unit can offer suitable and high quality services to the

customers at affordable prices only when it has good control over cost. Thus, report will

entail the tools and techniques that hotel unit needs to undertake for ensuring effective

management of funds. Besides this, it will also shed light on the costing systems and planning

tools that prove to be more beneficial for hotel.

P1 Presenting management accounting tools and their requirements in the context of Barry

House

To

Management Team

Barry House Hotel

Date: 3rd December 2017

Subject: Management Accounting Systems

Introduction: The present report highlights the system of MA that aid in organizational decision

making, growth as well as success.

Task

Management accounting is the process of collecting, analyzing, interpreting and communicating

results that are associated with the internal business operations. In the context of business unit system

of MA is essentially required for the purpose of effective decision making. Hence, by using the tools

of management accounting business organization can evaluate performance and take cost effective

measures that maximizes both sales as well as profit margin.

Cost accounting: It may be served a process that assists in controlling cost through the means of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recording, categorizing, summarizing and evaluating differences. In other words, it can be depicted

that cost account is used by the business unit for the ascertainment, allocation and distribution of cost.

By undertaking such formal mechanism, firm can take decision about decision and become able to

make use of financial resources optimally (Saladrigues and Tena, 2017).

Pros: It provides necessary or relevant cost information and helps in exert control on

wastage to a great extent. In addition to this, through using the data set of cost

accounting comparison can be done in relation to periods, volume of output,

determent and process. Further, cost accounting tool of MA also disclose information

about both profitable and non- profitable areas (Ward, 2012). Hence, by getting

information about profitable areas firm can take decision regarding expansion.

Cons: For the installation and maintenance of cost accounting system within the firm,

hotel unit requires more money and manpower. Moreover, cost accounting can be

done or performed by the personnel who have exceptional knowledge pertaining to

such field (Cost Accounting, 2017). Along with this, complexity of system and

pointless application is also recognized as a limitation of cost accounting system.

Price optimization system: Such system of MA assists firm in understanding the views, expectation

and willingness in relation to making payment. In the competitive environment firm can attain success

only when its prices and offerings are in line with the customer’s expectation. Thus, by setting

optimal prices hotel can attract more customers and thereby enhance sales revenue. Once loyalty has

built among the customers regarding the services of hotel unit then it can generate or earn high profit

by charging high prices.

Pros:

Enhancement of customer base

Improvement or enhancement in financial performance

Cons:

High knowledge and evaluation is required (Suomala, Lyly-Yrjänäinen and Lukka,

2014)

Need competent for dealing with the complex model of price optimization.

Inventory management: In the context of hotel unit, satisfaction level of customers is highly

influenced from the quality of services offered to them. Along with this, ineffective stock

management also may cause of high cost and less margin (Simons, 2013). Thus, by taking into

account the systems such as economic order quantity, just in time (JIT) etc firm can maintain enough

stock.

Pros:

that cost account is used by the business unit for the ascertainment, allocation and distribution of cost.

By undertaking such formal mechanism, firm can take decision about decision and become able to

make use of financial resources optimally (Saladrigues and Tena, 2017).

Pros: It provides necessary or relevant cost information and helps in exert control on

wastage to a great extent. In addition to this, through using the data set of cost

accounting comparison can be done in relation to periods, volume of output,

determent and process. Further, cost accounting tool of MA also disclose information

about both profitable and non- profitable areas (Ward, 2012). Hence, by getting

information about profitable areas firm can take decision regarding expansion.

Cons: For the installation and maintenance of cost accounting system within the firm,

hotel unit requires more money and manpower. Moreover, cost accounting can be

done or performed by the personnel who have exceptional knowledge pertaining to

such field (Cost Accounting, 2017). Along with this, complexity of system and

pointless application is also recognized as a limitation of cost accounting system.

Price optimization system: Such system of MA assists firm in understanding the views, expectation

and willingness in relation to making payment. In the competitive environment firm can attain success

only when its prices and offerings are in line with the customer’s expectation. Thus, by setting

optimal prices hotel can attract more customers and thereby enhance sales revenue. Once loyalty has

built among the customers regarding the services of hotel unit then it can generate or earn high profit

by charging high prices.

Pros:

Enhancement of customer base

Improvement or enhancement in financial performance

Cons:

High knowledge and evaluation is required (Suomala, Lyly-Yrjänäinen and Lukka,

2014)

Need competent for dealing with the complex model of price optimization.

Inventory management: In the context of hotel unit, satisfaction level of customers is highly

influenced from the quality of services offered to them. Along with this, ineffective stock

management also may cause of high cost and less margin (Simons, 2013). Thus, by taking into

account the systems such as economic order quantity, just in time (JIT) etc firm can maintain enough

stock.

Pros:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reduction in holding and ordering cost

Helps in enhancing profit through controlling wastage

Cons:

Need to maintain extensive record

Time consuming activity and stock management software is expensive

Conclusion: From overall report it can be stated that systems of MA ensures effective management of

funds. Thus, by using such tools manager can control cost and improves profit margin to a great

extent.

Sincerely

Management Accountant

P2 Methods used for managerial reporting

To

Management Team

Barry House Hotel

Date: 3rd December 2017

Subject: Management Accounting reporting

Introduction: This report is based on need and types of managerial accounting reports. It entails the

reasons due to which firms are encouraged to prepare managerial reports.

Task

Managerial reports and its need: It implies for the reports that contain information about cost, profit,

sales, expenses and stock etc. In other words, managerial reports are linked with the financial

performance of different departments. Hence, the main motive of firm behind the preparation of

managerial report is to identify the extent to which business is running smoothly. Thus, by

undertaking managerial report and developing strategies hotel unit can enhance the efficiency of

business operations and functions to the significant level.

Types

Cost report: Profit maximization and recovery of expenses or cost incurred is one of the motives of

Barry House. Thus, using cost report hotel unit can do profit planning in the best possible way.

Moreover, it provides management team and precise and detailed information about the total cost

expenses incurred as well as unit cost. On the basis of cost level, management team can decide profit

margin they need to earn from each customer (Zimmerman and Yahya-Zadeh, 2011).

Besides this, cost report also offers opportunity to the firm in relation to assessing or comparing cost

with the previous period or years. Thus, it gives indication to the organization in relation to

undertaking cost effective ways for cost control and profit maximization.

Helps in enhancing profit through controlling wastage

Cons:

Need to maintain extensive record

Time consuming activity and stock management software is expensive

Conclusion: From overall report it can be stated that systems of MA ensures effective management of

funds. Thus, by using such tools manager can control cost and improves profit margin to a great

extent.

Sincerely

Management Accountant

P2 Methods used for managerial reporting

To

Management Team

Barry House Hotel

Date: 3rd December 2017

Subject: Management Accounting reporting

Introduction: This report is based on need and types of managerial accounting reports. It entails the

reasons due to which firms are encouraged to prepare managerial reports.

Task

Managerial reports and its need: It implies for the reports that contain information about cost, profit,

sales, expenses and stock etc. In other words, managerial reports are linked with the financial

performance of different departments. Hence, the main motive of firm behind the preparation of

managerial report is to identify the extent to which business is running smoothly. Thus, by

undertaking managerial report and developing strategies hotel unit can enhance the efficiency of

business operations and functions to the significant level.

Types

Cost report: Profit maximization and recovery of expenses or cost incurred is one of the motives of

Barry House. Thus, using cost report hotel unit can do profit planning in the best possible way.

Moreover, it provides management team and precise and detailed information about the total cost

expenses incurred as well as unit cost. On the basis of cost level, management team can decide profit

margin they need to earn from each customer (Zimmerman and Yahya-Zadeh, 2011).

Besides this, cost report also offers opportunity to the firm in relation to assessing or comparing cost

with the previous period or years. Thus, it gives indication to the organization in relation to

undertaking cost effective ways for cost control and profit maximization.

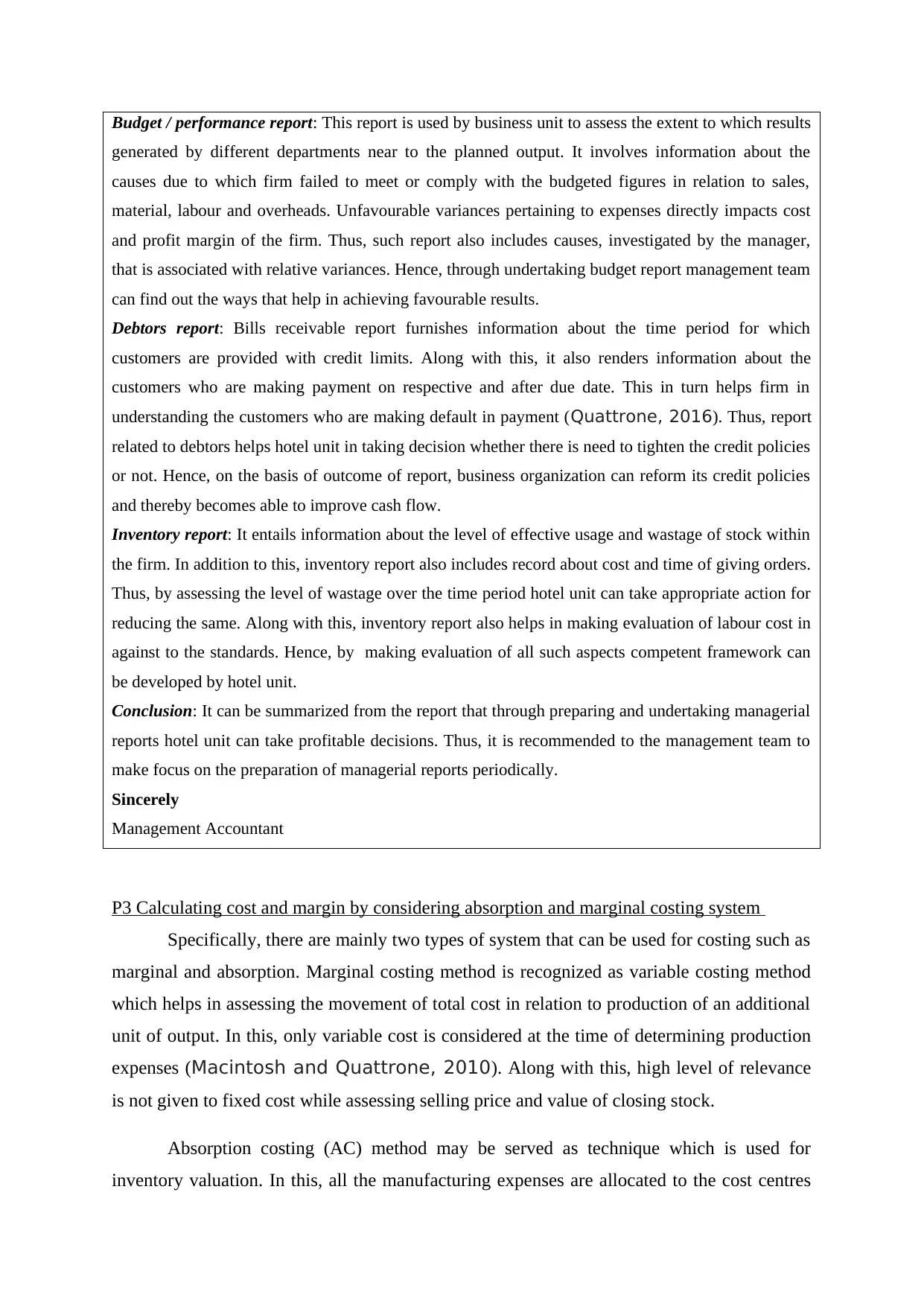

Budget / performance report: This report is used by business unit to assess the extent to which results

generated by different departments near to the planned output. It involves information about the

causes due to which firm failed to meet or comply with the budgeted figures in relation to sales,

material, labour and overheads. Unfavourable variances pertaining to expenses directly impacts cost

and profit margin of the firm. Thus, such report also includes causes, investigated by the manager,

that is associated with relative variances. Hence, through undertaking budget report management team

can find out the ways that help in achieving favourable results.

Debtors report: Bills receivable report furnishes information about the time period for which

customers are provided with credit limits. Along with this, it also renders information about the

customers who are making payment on respective and after due date. This in turn helps firm in

understanding the customers who are making default in payment (Quattrone, 2016). Thus, report

related to debtors helps hotel unit in taking decision whether there is need to tighten the credit policies

or not. Hence, on the basis of outcome of report, business organization can reform its credit policies

and thereby becomes able to improve cash flow.

Inventory report: It entails information about the level of effective usage and wastage of stock within

the firm. In addition to this, inventory report also includes record about cost and time of giving orders.

Thus, by assessing the level of wastage over the time period hotel unit can take appropriate action for

reducing the same. Along with this, inventory report also helps in making evaluation of labour cost in

against to the standards. Hence, by making evaluation of all such aspects competent framework can

be developed by hotel unit.

Conclusion: It can be summarized from the report that through preparing and undertaking managerial

reports hotel unit can take profitable decisions. Thus, it is recommended to the management team to

make focus on the preparation of managerial reports periodically.

Sincerely

Management Accountant

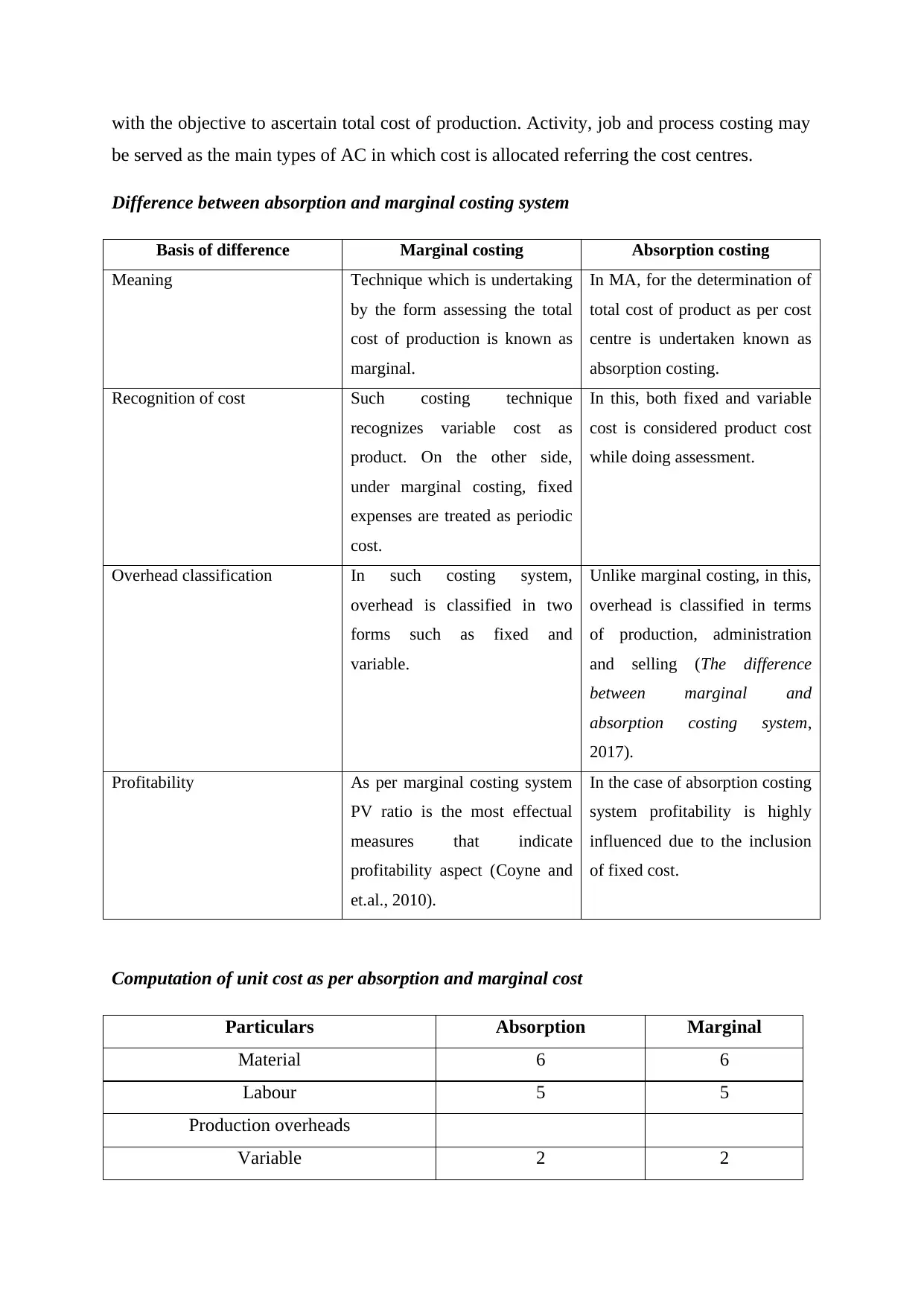

P3 Calculating cost and margin by considering absorption and marginal costing system

Specifically, there are mainly two types of system that can be used for costing such as

marginal and absorption. Marginal costing method is recognized as variable costing method

which helps in assessing the movement of total cost in relation to production of an additional

unit of output. In this, only variable cost is considered at the time of determining production

expenses (Macintosh and Quattrone, 2010). Along with this, high level of relevance

is not given to fixed cost while assessing selling price and value of closing stock.

Absorption costing (AC) method may be served as technique which is used for

inventory valuation. In this, all the manufacturing expenses are allocated to the cost centres

generated by different departments near to the planned output. It involves information about the

causes due to which firm failed to meet or comply with the budgeted figures in relation to sales,

material, labour and overheads. Unfavourable variances pertaining to expenses directly impacts cost

and profit margin of the firm. Thus, such report also includes causes, investigated by the manager,

that is associated with relative variances. Hence, through undertaking budget report management team

can find out the ways that help in achieving favourable results.

Debtors report: Bills receivable report furnishes information about the time period for which

customers are provided with credit limits. Along with this, it also renders information about the

customers who are making payment on respective and after due date. This in turn helps firm in

understanding the customers who are making default in payment (Quattrone, 2016). Thus, report

related to debtors helps hotel unit in taking decision whether there is need to tighten the credit policies

or not. Hence, on the basis of outcome of report, business organization can reform its credit policies

and thereby becomes able to improve cash flow.

Inventory report: It entails information about the level of effective usage and wastage of stock within

the firm. In addition to this, inventory report also includes record about cost and time of giving orders.

Thus, by assessing the level of wastage over the time period hotel unit can take appropriate action for

reducing the same. Along with this, inventory report also helps in making evaluation of labour cost in

against to the standards. Hence, by making evaluation of all such aspects competent framework can

be developed by hotel unit.

Conclusion: It can be summarized from the report that through preparing and undertaking managerial

reports hotel unit can take profitable decisions. Thus, it is recommended to the management team to

make focus on the preparation of managerial reports periodically.

Sincerely

Management Accountant

P3 Calculating cost and margin by considering absorption and marginal costing system

Specifically, there are mainly two types of system that can be used for costing such as

marginal and absorption. Marginal costing method is recognized as variable costing method

which helps in assessing the movement of total cost in relation to production of an additional

unit of output. In this, only variable cost is considered at the time of determining production

expenses (Macintosh and Quattrone, 2010). Along with this, high level of relevance

is not given to fixed cost while assessing selling price and value of closing stock.

Absorption costing (AC) method may be served as technique which is used for

inventory valuation. In this, all the manufacturing expenses are allocated to the cost centres

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with the objective to ascertain total cost of production. Activity, job and process costing may

be served as the main types of AC in which cost is allocated referring the cost centres.

Difference between absorption and marginal costing system

Basis of difference Marginal costing Absorption costing

Meaning Technique which is undertaking

by the form assessing the total

cost of production is known as

marginal.

In MA, for the determination of

total cost of product as per cost

centre is undertaken known as

absorption costing.

Recognition of cost Such costing technique

recognizes variable cost as

product. On the other side,

under marginal costing, fixed

expenses are treated as periodic

cost.

In this, both fixed and variable

cost is considered product cost

while doing assessment.

Overhead classification In such costing system,

overhead is classified in two

forms such as fixed and

variable.

Unlike marginal costing, in this,

overhead is classified in terms

of production, administration

and selling (The difference

between marginal and

absorption costing system,

2017).

Profitability As per marginal costing system

PV ratio is the most effectual

measures that indicate

profitability aspect (Coyne and

et.al., 2010).

In the case of absorption costing

system profitability is highly

influenced due to the inclusion

of fixed cost.

Computation of unit cost as per absorption and marginal cost

Particulars Absorption Marginal

Material 6 6

Labour 5 5

Production overheads

Variable 2 2

be served as the main types of AC in which cost is allocated referring the cost centres.

Difference between absorption and marginal costing system

Basis of difference Marginal costing Absorption costing

Meaning Technique which is undertaking

by the form assessing the total

cost of production is known as

marginal.

In MA, for the determination of

total cost of product as per cost

centre is undertaken known as

absorption costing.

Recognition of cost Such costing technique

recognizes variable cost as

product. On the other side,

under marginal costing, fixed

expenses are treated as periodic

cost.

In this, both fixed and variable

cost is considered product cost

while doing assessment.

Overhead classification In such costing system,

overhead is classified in two

forms such as fixed and

variable.

Unlike marginal costing, in this,

overhead is classified in terms

of production, administration

and selling (The difference

between marginal and

absorption costing system,

2017).

Profitability As per marginal costing system

PV ratio is the most effectual

measures that indicate

profitability aspect (Coyne and

et.al., 2010).

In the case of absorption costing

system profitability is highly

influenced due to the inclusion

of fixed cost.

Computation of unit cost as per absorption and marginal cost

Particulars Absorption Marginal

Material 6 6

Labour 5 5

Production overheads

Variable 2 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

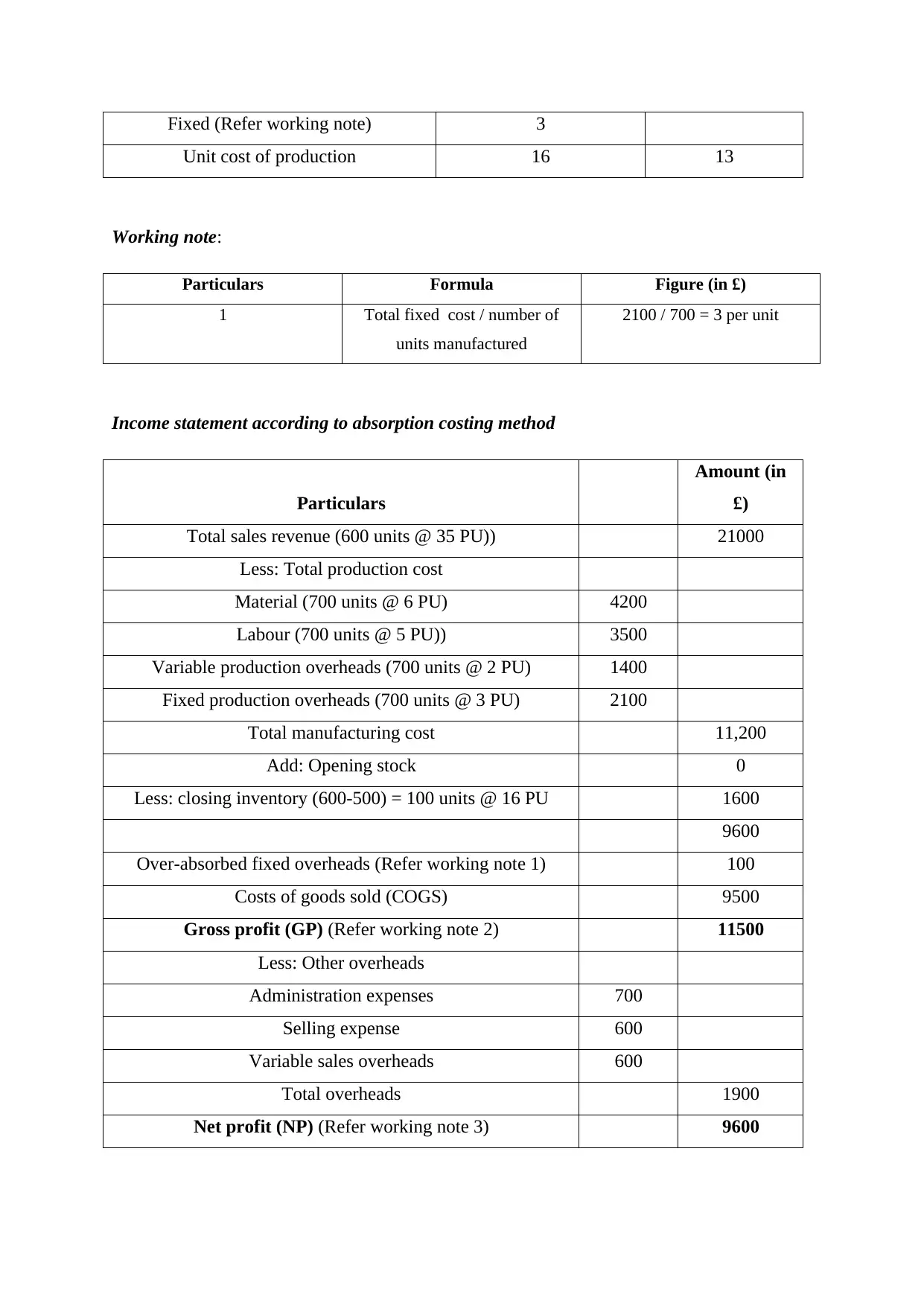

Fixed (Refer working note) 3

Unit cost of production 16 13

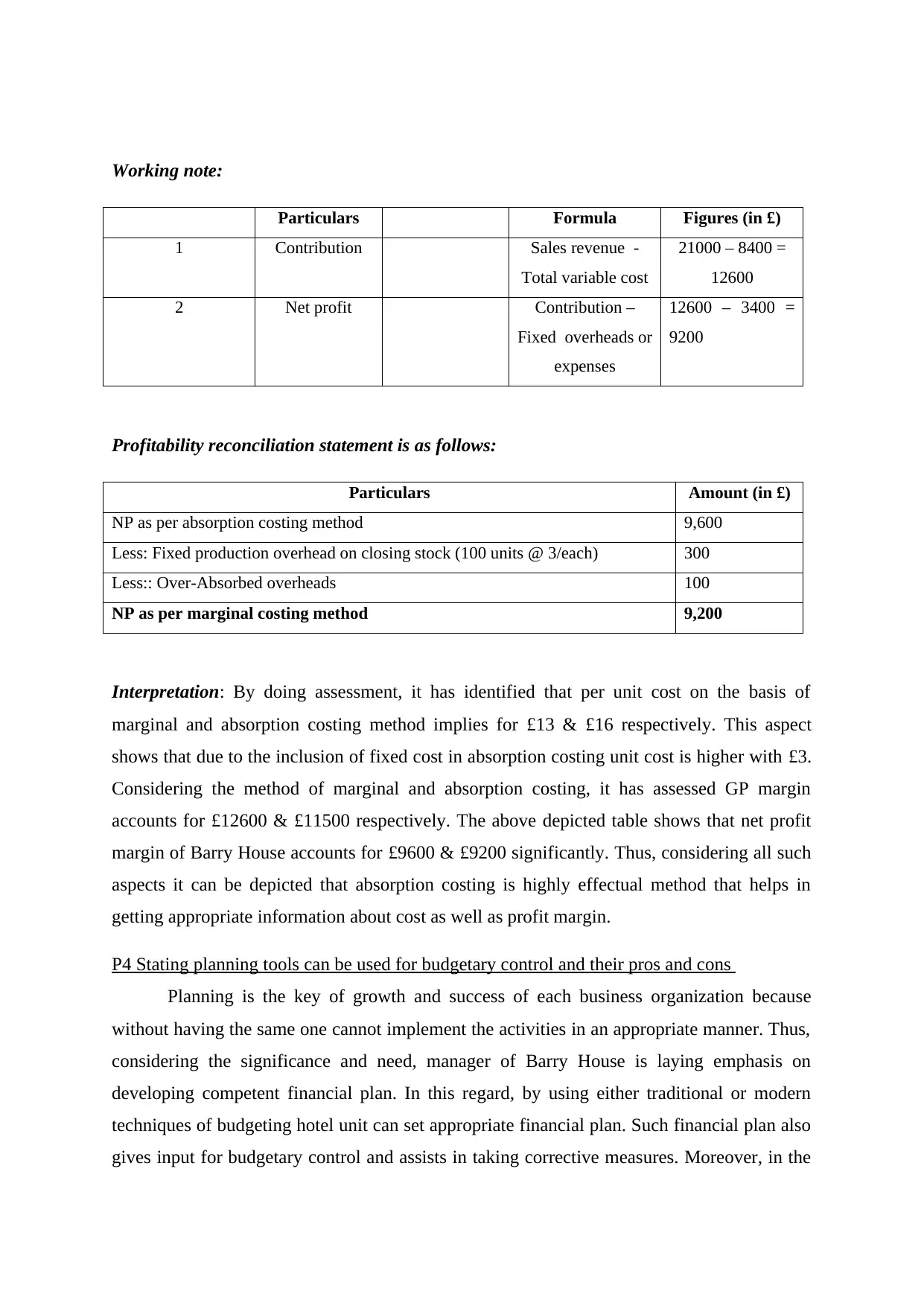

Working note:

Particulars Formula Figure (in £)

1 Total fixed cost / number of

units manufactured

2100 / 700 = 3 per unit

Income statement according to absorption costing method

Particulars

Amount (in

£)

Total sales revenue (600 units @ 35 PU)) 21000

Less: Total production cost

Material (700 units @ 6 PU) 4200

Labour (700 units @ 5 PU)) 3500

Variable production overheads (700 units @ 2 PU) 1400

Fixed production overheads (700 units @ 3 PU) 2100

Total manufacturing cost 11,200

Add: Opening stock 0

Less: closing inventory (600-500) = 100 units @ 16 PU 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

Gross profit (GP) (Refer working note 2) 11500

Less: Other overheads

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (Refer working note 3) 9600

Unit cost of production 16 13

Working note:

Particulars Formula Figure (in £)

1 Total fixed cost / number of

units manufactured

2100 / 700 = 3 per unit

Income statement according to absorption costing method

Particulars

Amount (in

£)

Total sales revenue (600 units @ 35 PU)) 21000

Less: Total production cost

Material (700 units @ 6 PU) 4200

Labour (700 units @ 5 PU)) 3500

Variable production overheads (700 units @ 2 PU) 1400

Fixed production overheads (700 units @ 3 PU) 2100

Total manufacturing cost 11,200

Add: Opening stock 0

Less: closing inventory (600-500) = 100 units @ 16 PU 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

Gross profit (GP) (Refer working note 2) 11500

Less: Other overheads

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (Refer working note 3) 9600

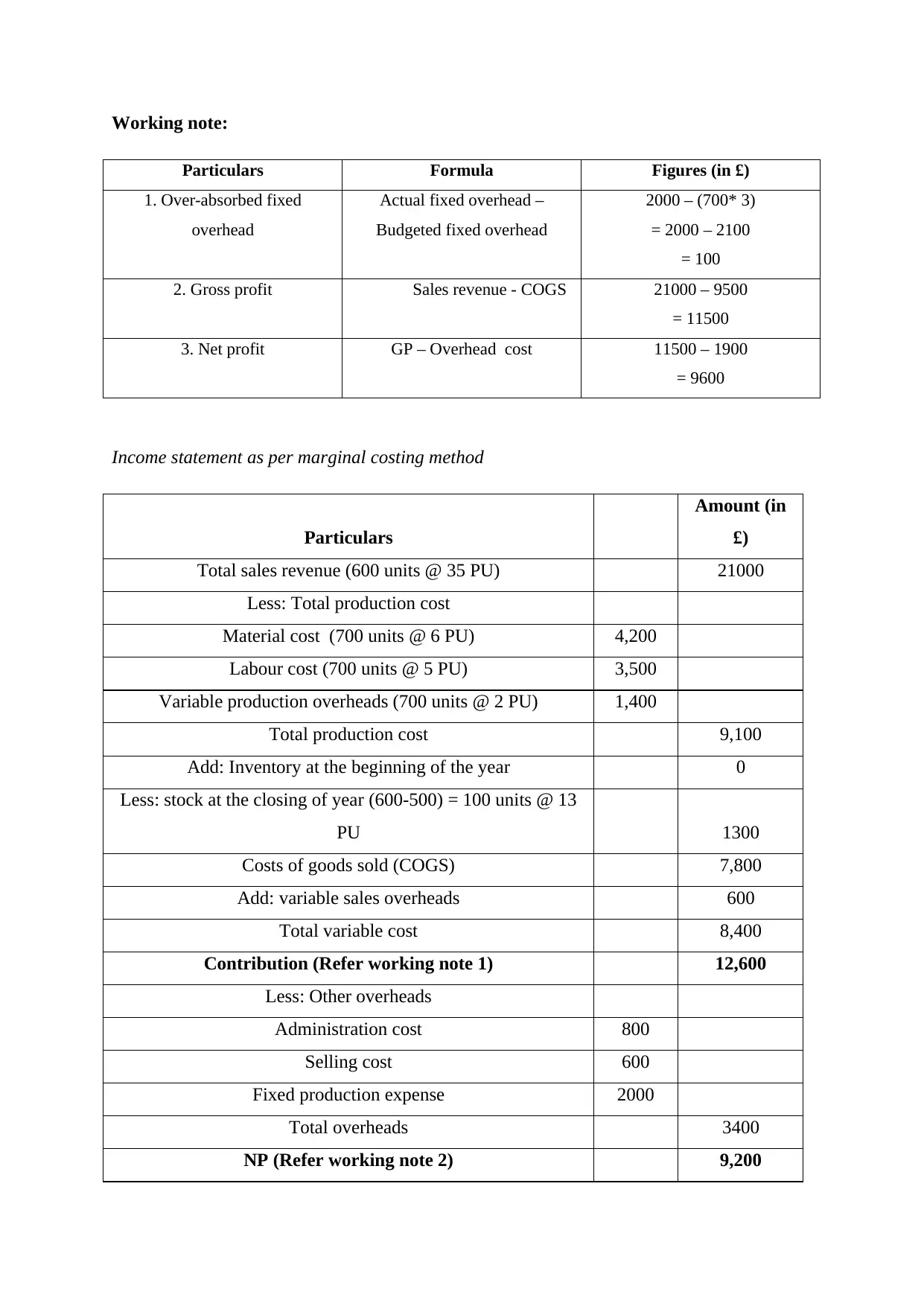

Working note:

Particulars Formula Figures (in £)

1. Over-absorbed fixed

overhead

Actual fixed overhead –

Budgeted fixed overhead

2000 – (700* 3)

= 2000 – 2100

= 100

2. Gross profit Sales revenue - COGS 21000 – 9500

= 11500

3. Net profit GP – Overhead cost 11500 – 1900

= 9600

Income statement as per marginal costing method

Particulars

Amount (in

£)

Total sales revenue (600 units @ 35 PU) 21000

Less: Total production cost

Material cost (700 units @ 6 PU) 4,200

Labour cost (700 units @ 5 PU) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost 9,100

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 13

PU 1300

Costs of goods sold (COGS) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution (Refer working note 1) 12,600

Less: Other overheads

Administration cost 800

Selling cost 600

Fixed production expense 2000

Total overheads 3400

NP (Refer working note 2) 9,200

Particulars Formula Figures (in £)

1. Over-absorbed fixed

overhead

Actual fixed overhead –

Budgeted fixed overhead

2000 – (700* 3)

= 2000 – 2100

= 100

2. Gross profit Sales revenue - COGS 21000 – 9500

= 11500

3. Net profit GP – Overhead cost 11500 – 1900

= 9600

Income statement as per marginal costing method

Particulars

Amount (in

£)

Total sales revenue (600 units @ 35 PU) 21000

Less: Total production cost

Material cost (700 units @ 6 PU) 4,200

Labour cost (700 units @ 5 PU) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost 9,100

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 13

PU 1300

Costs of goods sold (COGS) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution (Refer working note 1) 12,600

Less: Other overheads

Administration cost 800

Selling cost 600

Fixed production expense 2000

Total overheads 3400

NP (Refer working note 2) 9,200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working note:

Particulars Formula Figures (in £)

1 Contribution Sales revenue -

Total variable cost

21000 – 8400 =

12600

2 Net profit Contribution –

Fixed overheads or

expenses

12600 – 3400 =

9200

Profitability reconciliation statement is as follows:

Particulars Amount (in £)

NP as per absorption costing method 9,600

Less: Fixed production overhead on closing stock (100 units @ 3/each) 300

Less:: Over-Absorbed overheads 100

NP as per marginal costing method 9,200

Interpretation: By doing assessment, it has identified that per unit cost on the basis of

marginal and absorption costing method implies for £13 & £16 respectively. This aspect

shows that due to the inclusion of fixed cost in absorption costing unit cost is higher with £3.

Considering the method of marginal and absorption costing, it has assessed GP margin

accounts for £12600 & £11500 respectively. The above depicted table shows that net profit

margin of Barry House accounts for £9600 & £9200 significantly. Thus, considering all such

aspects it can be depicted that absorption costing is highly effectual method that helps in

getting appropriate information about cost as well as profit margin.

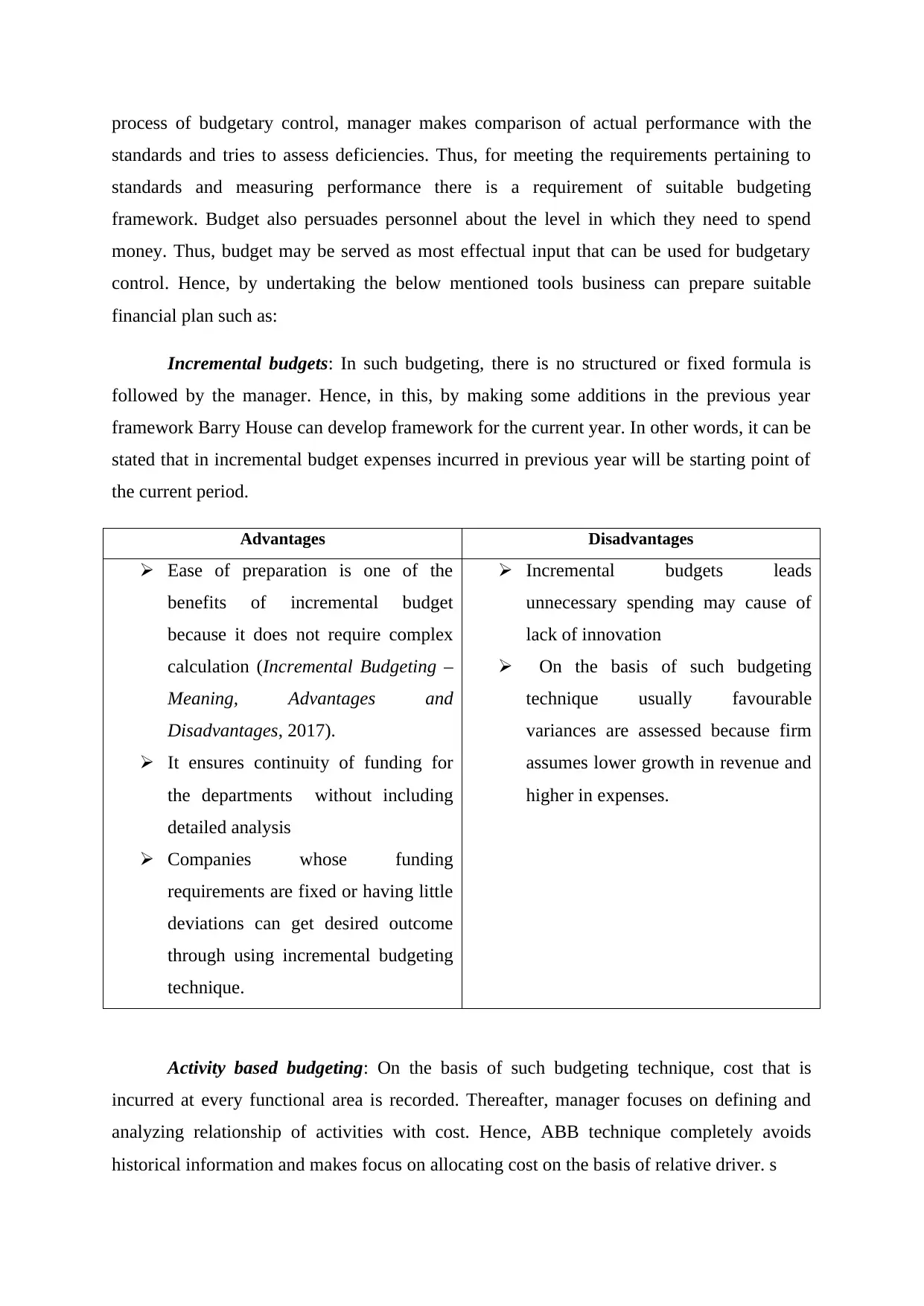

P4 Stating planning tools can be used for budgetary control and their pros and cons

Planning is the key of growth and success of each business organization because

without having the same one cannot implement the activities in an appropriate manner. Thus,

considering the significance and need, manager of Barry House is laying emphasis on

developing competent financial plan. In this regard, by using either traditional or modern

techniques of budgeting hotel unit can set appropriate financial plan. Such financial plan also

gives input for budgetary control and assists in taking corrective measures. Moreover, in the

Particulars Formula Figures (in £)

1 Contribution Sales revenue -

Total variable cost

21000 – 8400 =

12600

2 Net profit Contribution –

Fixed overheads or

expenses

12600 – 3400 =

9200

Profitability reconciliation statement is as follows:

Particulars Amount (in £)

NP as per absorption costing method 9,600

Less: Fixed production overhead on closing stock (100 units @ 3/each) 300

Less:: Over-Absorbed overheads 100

NP as per marginal costing method 9,200

Interpretation: By doing assessment, it has identified that per unit cost on the basis of

marginal and absorption costing method implies for £13 & £16 respectively. This aspect

shows that due to the inclusion of fixed cost in absorption costing unit cost is higher with £3.

Considering the method of marginal and absorption costing, it has assessed GP margin

accounts for £12600 & £11500 respectively. The above depicted table shows that net profit

margin of Barry House accounts for £9600 & £9200 significantly. Thus, considering all such

aspects it can be depicted that absorption costing is highly effectual method that helps in

getting appropriate information about cost as well as profit margin.

P4 Stating planning tools can be used for budgetary control and their pros and cons

Planning is the key of growth and success of each business organization because

without having the same one cannot implement the activities in an appropriate manner. Thus,

considering the significance and need, manager of Barry House is laying emphasis on

developing competent financial plan. In this regard, by using either traditional or modern

techniques of budgeting hotel unit can set appropriate financial plan. Such financial plan also

gives input for budgetary control and assists in taking corrective measures. Moreover, in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

process of budgetary control, manager makes comparison of actual performance with the

standards and tries to assess deficiencies. Thus, for meeting the requirements pertaining to

standards and measuring performance there is a requirement of suitable budgeting

framework. Budget also persuades personnel about the level in which they need to spend

money. Thus, budget may be served as most effectual input that can be used for budgetary

control. Hence, by undertaking the below mentioned tools business can prepare suitable

financial plan such as:

Incremental budgets: In such budgeting, there is no structured or fixed formula is

followed by the manager. Hence, in this, by making some additions in the previous year

framework Barry House can develop framework for the current year. In other words, it can be

stated that in incremental budget expenses incurred in previous year will be starting point of

the current period.

Advantages Disadvantages

Ease of preparation is one of the

benefits of incremental budget

because it does not require complex

calculation (Incremental Budgeting –

Meaning, Advantages and

Disadvantages, 2017).

It ensures continuity of funding for

the departments without including

detailed analysis

Companies whose funding

requirements are fixed or having little

deviations can get desired outcome

through using incremental budgeting

technique.

Incremental budgets leads

unnecessary spending may cause of

lack of innovation

On the basis of such budgeting

technique usually favourable

variances are assessed because firm

assumes lower growth in revenue and

higher in expenses.

Activity based budgeting: On the basis of such budgeting technique, cost that is

incurred at every functional area is recorded. Thereafter, manager focuses on defining and

analyzing relationship of activities with cost. Hence, ABB technique completely avoids

historical information and makes focus on allocating cost on the basis of relative driver. s

standards and tries to assess deficiencies. Thus, for meeting the requirements pertaining to

standards and measuring performance there is a requirement of suitable budgeting

framework. Budget also persuades personnel about the level in which they need to spend

money. Thus, budget may be served as most effectual input that can be used for budgetary

control. Hence, by undertaking the below mentioned tools business can prepare suitable

financial plan such as:

Incremental budgets: In such budgeting, there is no structured or fixed formula is

followed by the manager. Hence, in this, by making some additions in the previous year

framework Barry House can develop framework for the current year. In other words, it can be

stated that in incremental budget expenses incurred in previous year will be starting point of

the current period.

Advantages Disadvantages

Ease of preparation is one of the

benefits of incremental budget

because it does not require complex

calculation (Incremental Budgeting –

Meaning, Advantages and

Disadvantages, 2017).

It ensures continuity of funding for

the departments without including

detailed analysis

Companies whose funding

requirements are fixed or having little

deviations can get desired outcome

through using incremental budgeting

technique.

Incremental budgets leads

unnecessary spending may cause of

lack of innovation

On the basis of such budgeting

technique usually favourable

variances are assessed because firm

assumes lower growth in revenue and

higher in expenses.

Activity based budgeting: On the basis of such budgeting technique, cost that is

incurred at every functional area is recorded. Thereafter, manager focuses on defining and

analyzing relationship of activities with cost. Hence, ABB technique completely avoids

historical information and makes focus on allocating cost on the basis of relative driver. s

Advantages Disadvantages

ABB is highly effectual and

integrated with six sigma as well as

other continuous programs.

It facilitates benchmarking and

supports performance as well as

scorecard (Advantages &

Disadvantages of Activity-Based

Costing, 2017).

Provides accurate view of product

cost and thereby aid in business

decision making.

Such budgeting technique is highly

expensive to implement.

Further, ABB is considered as time

consuming activity.

For developing understanding among

the concerned managers firm has to

conduct training session. This in turn

imposes cost in front of firm and

affects profit margin.

Zero based budgeting: In this, all the budgetary or financial allocations of each

department are setting down by considering the monetary base as zero. Hence, under ZBB by

doing assessment of each alternative and cost effective ways of performing activities budget

is prepared. In addition to this, manager who sets budget as per ZBB is accountable to justify

the level of expenses for the current year. Thus, by using such technique Barry House cn

channelize fund in the prioritized areas.

Advantages Disadvantages

ZBB assures efficient allocation of

funds by avoiding the level of

unnecessary expense.

Enhances services by utilizing or

using the cost effective ways (Pros

and Cons of Zero-Based Budgeting,

2017)

Increases staff motivation and

performance through involving them

in the decision making process.

Provides high level of assistance in

relating cost with the mission and

As compared to traditional tools, ZBB

is time consuming and expensive

process.

For preparing budget according to

ZBB, business unit require highly

skilled and educated staffs.

Further, for better and appropriate

execution, high commitment as well

as professional attitude is required.

ABB is highly effectual and

integrated with six sigma as well as

other continuous programs.

It facilitates benchmarking and

supports performance as well as

scorecard (Advantages &

Disadvantages of Activity-Based

Costing, 2017).

Provides accurate view of product

cost and thereby aid in business

decision making.

Such budgeting technique is highly

expensive to implement.

Further, ABB is considered as time

consuming activity.

For developing understanding among

the concerned managers firm has to

conduct training session. This in turn

imposes cost in front of firm and

affects profit margin.

Zero based budgeting: In this, all the budgetary or financial allocations of each

department are setting down by considering the monetary base as zero. Hence, under ZBB by

doing assessment of each alternative and cost effective ways of performing activities budget

is prepared. In addition to this, manager who sets budget as per ZBB is accountable to justify

the level of expenses for the current year. Thus, by using such technique Barry House cn

channelize fund in the prioritized areas.

Advantages Disadvantages

ZBB assures efficient allocation of

funds by avoiding the level of

unnecessary expense.

Enhances services by utilizing or

using the cost effective ways (Pros

and Cons of Zero-Based Budgeting,

2017)

Increases staff motivation and

performance through involving them

in the decision making process.

Provides high level of assistance in

relating cost with the mission and

As compared to traditional tools, ZBB

is time consuming and expensive

process.

For preparing budget according to

ZBB, business unit require highly

skilled and educated staffs.

Further, for better and appropriate

execution, high commitment as well

as professional attitude is required.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.