Management Accounting Report: Bittern Ltd, Costing and Budgeting

VerifiedAdded on 2019/12/04

|16

|5042

|305

Report

AI Summary

This report delves into the core principles of management accounting, utilizing Bittern Ltd, a manufacturing company, as a case study. It explores various cost types (material, labor, overheads), costing methods (job, contract, process, service), and costing techniques (marginal, standard, absorption, historical). Task 1 analyzes cost data under different scenarios (stable production/sales/inventory, fluctuating scenarios), calculating profitability using variable and absorption costing. Task 2 presents a cost report and analysis, including performance indicators (turnover, costs, customer/employee satisfaction, profitability) and strategies for cost reduction, value enhancement, and quality improvement. Task 3 examines the budgeting process, methods, and preparation. Task 4 focuses on variance calculation, identifying causes, recommending corrective actions, and preparing an operating statement to deduce budget profit, culminating in a report to management. The report provides tables to illustrate the calculations and findings.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Different types of costs..............................................................................................................3

1.2 Different types of costing methods............................................................................................3

1.3 Costing techniques.....................................................................................................................4

1.4 Analyse the cost data..................................................................................................................5

1) Stable production, sales and inventory........................................................................................5

2) Stable sales but fluctuating production, sales and inventory.......................................................5

3) Stable production but fluctuating sales and inventory................................................................6

TASK 2 ................................................................................................................................................7

2.1 Cost report and analysis.............................................................................................................7

2.2 Various performance indicators used to identify potential improvements.................................8

2.3 Ways to reduce costs, enhance value and quality......................................................................8

TASK 3 ................................................................................................................................................9

3.1 Purpose and nature of budgeting process..................................................................................9

3.2 Budgeting method and its need................................................................................................10

3.3 Budget preparation...................................................................................................................10

TASK 4...............................................................................................................................................12

1.1 Variance calculation, identify possible causes and recommend corrective actions.................12

1.2 Operating statement to deduce budget profit for May.............................................................13

1.3 Report the findings to management.........................................................................................14

REFERENCES...................................................................................................................................15

Index of Tables

Table 1: Calculation of profitability by variable costing......................................................................5

Table 2: Calculation of profitability by absorption costing..................................................................5

Table 3: Calculation of profitability by variable costing .....................................................................5

Table 4: Calculation of profitability by absorption costing.................................................................6

Table 5: Calculation of profitability by variable costing......................................................................6

Table 6: Calculation of profitability by absorption costing..................................................................7

Table 7: Material purchase budget......................................................................................................10

Table 8: Trade payable budgets..........................................................................................................11

Table 9: Cash budget of Antonio for six months ending on 31st December, 2016............................11

Table 10: Calculation of variances.....................................................................................................12

Table 11: Operating statement to deduce budget profit for May........................................................13

2

INTRODUCTION ...............................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Different types of costs..............................................................................................................3

1.2 Different types of costing methods............................................................................................3

1.3 Costing techniques.....................................................................................................................4

1.4 Analyse the cost data..................................................................................................................5

1) Stable production, sales and inventory........................................................................................5

2) Stable sales but fluctuating production, sales and inventory.......................................................5

3) Stable production but fluctuating sales and inventory................................................................6

TASK 2 ................................................................................................................................................7

2.1 Cost report and analysis.............................................................................................................7

2.2 Various performance indicators used to identify potential improvements.................................8

2.3 Ways to reduce costs, enhance value and quality......................................................................8

TASK 3 ................................................................................................................................................9

3.1 Purpose and nature of budgeting process..................................................................................9

3.2 Budgeting method and its need................................................................................................10

3.3 Budget preparation...................................................................................................................10

TASK 4...............................................................................................................................................12

1.1 Variance calculation, identify possible causes and recommend corrective actions.................12

1.2 Operating statement to deduce budget profit for May.............................................................13

1.3 Report the findings to management.........................................................................................14

REFERENCES...................................................................................................................................15

Index of Tables

Table 1: Calculation of profitability by variable costing......................................................................5

Table 2: Calculation of profitability by absorption costing..................................................................5

Table 3: Calculation of profitability by variable costing .....................................................................5

Table 4: Calculation of profitability by absorption costing.................................................................6

Table 5: Calculation of profitability by variable costing......................................................................6

Table 6: Calculation of profitability by absorption costing..................................................................7

Table 7: Material purchase budget......................................................................................................10

Table 8: Trade payable budgets..........................................................................................................11

Table 9: Cash budget of Antonio for six months ending on 31st December, 2016............................11

Table 10: Calculation of variances.....................................................................................................12

Table 11: Operating statement to deduce budget profit for May........................................................13

2

INTRODUCTION

Looking at the present competitive business world, management accounting plays an

inevitable role in the success of corporations. It is the process through which managers use

internally and external available information for the forecasting and decision-making process. It

contributes to make planning, reviewing and evaluating the success of the business. Present project

report is based on Bittern Ltd, it is a manufacturing concern who is engaged in production and

selling of the products to meet customer demand timely. The report will demonstrated different

types of costs, costing method, budgeting process and variance analysis that assist business to

achieve their target goals.

TASK 1

1.1 Different types of costs

Elements: There are three types of costs that are material, labour and overheads. Being a

manufacturing organization, expenditures that will be incurred by Bittern Ltd. to buy raw material is

called material cost (Chen and et.al., 2009). However, labour's wages is called labour costs and all

the other expenditures that are directly related to the production functions are called overheads such

as royalty and cost of moulds etc.

Nature: Direct costs are those which Bittern Ltd incurred directly for the goods

manufacturing such as material, labour and production expenses (Smith and et.al., 2009). While, all

the other expenses which are not related to the production are called indirect costs such as office

rent, stationery etc.

Function: Production costs involve indirect expenses on production like factory rent,

lighting etc. Administration costs includes expenses such as salaries, office rent, stationery, postage

etc. However, all the expenses which Bittern Ltd, incurred to sale goods in the market are called

selling and distribution costs such as delivery charges, advertisement, free delivery costs etc. (Cao

and et.al., 2009).

Behaviour: Expenses which are not impacted by different production volume of Bittern Ltd

are called fixed costs like depreciation, insurance etc. While, expenditures which increase or

decrease along with the rising and falling the production volume are called variable costs such as

material (Wait and et.al., 2013). On contrary, expenditures which is remains constant up to a fixed

production volume and thereafter get changes according to the output level are called semi-variable

costs like electricity bill.

3

Looking at the present competitive business world, management accounting plays an

inevitable role in the success of corporations. It is the process through which managers use

internally and external available information for the forecasting and decision-making process. It

contributes to make planning, reviewing and evaluating the success of the business. Present project

report is based on Bittern Ltd, it is a manufacturing concern who is engaged in production and

selling of the products to meet customer demand timely. The report will demonstrated different

types of costs, costing method, budgeting process and variance analysis that assist business to

achieve their target goals.

TASK 1

1.1 Different types of costs

Elements: There are three types of costs that are material, labour and overheads. Being a

manufacturing organization, expenditures that will be incurred by Bittern Ltd. to buy raw material is

called material cost (Chen and et.al., 2009). However, labour's wages is called labour costs and all

the other expenditures that are directly related to the production functions are called overheads such

as royalty and cost of moulds etc.

Nature: Direct costs are those which Bittern Ltd incurred directly for the goods

manufacturing such as material, labour and production expenses (Smith and et.al., 2009). While, all

the other expenses which are not related to the production are called indirect costs such as office

rent, stationery etc.

Function: Production costs involve indirect expenses on production like factory rent,

lighting etc. Administration costs includes expenses such as salaries, office rent, stationery, postage

etc. However, all the expenses which Bittern Ltd, incurred to sale goods in the market are called

selling and distribution costs such as delivery charges, advertisement, free delivery costs etc. (Cao

and et.al., 2009).

Behaviour: Expenses which are not impacted by different production volume of Bittern Ltd

are called fixed costs like depreciation, insurance etc. While, expenditures which increase or

decrease along with the rising and falling the production volume are called variable costs such as

material (Wait and et.al., 2013). On contrary, expenditures which is remains constant up to a fixed

production volume and thereafter get changes according to the output level are called semi-variable

costs like electricity bill.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Different types of costing methods

There are number of costing methods available to businesses to ascertain their product costs,

explained below:

Job costing: It is the method which accumulates all the direct as well as indirect expenditure

associated to a specific job (Garrison and et.al., 2010). This method is suitable for the organizations

who carry out their work after receiving customer order and their requests.

Contract costing: This costing method applies to contract based work such as construction

of building (Zhang and et.al., 2011). This method assist managers to ascertain costs for the work

completed till the period and after finishing the total work, it helps to determine total cost of the

contract.

Process costing: In case, when production is carried out through the different stages or

process involved is known as process costing (Darvas and et.al., 2012). This costing method helps

to ascertain costs of each process and transfer it into the next process and at the end, total

production costs will be identified.

Service costing: This method is uses by service rendering organizations such as water

supply department and electricity department to determine the costs of provided services.

1.3 Costing techniques

Costing techniques refers to the process through which organizations can allocate

expenditures effectively to determine their product costs.

Marginal costing/variable costing: According to CIMA London, marginal costing is the

method that helps to ascertain product costs and determine the impact of changes in costs, prices

and volume on the profitability (Penny and et.al., 2011). This method segregate total production

cost into fixed as well as variable costs. This method is also known as variable costing because it

exclude fixed costs in the cost ascertainment.

Standard costing: This technique evaluate actual production costs with the standard so as to

assess the effectiveness of business operations and aims at taking corrective actions to eliminate

adverse performance.

Absorption costing/Full costing technique: In this technique, all the fixed as well as

variable expenditures are taken into consideration to determine total product costs (Ogunlana and

et.al., 2010). This method is also known as full costing technique because it take into account all the

expenditures whether fixed or variable related to the production.

Historical costing: It is the technique to determine costs after incurred the expenditures so

that costs can be computed for the work done in the past. It helps to compare current costs with the

4

There are number of costing methods available to businesses to ascertain their product costs,

explained below:

Job costing: It is the method which accumulates all the direct as well as indirect expenditure

associated to a specific job (Garrison and et.al., 2010). This method is suitable for the organizations

who carry out their work after receiving customer order and their requests.

Contract costing: This costing method applies to contract based work such as construction

of building (Zhang and et.al., 2011). This method assist managers to ascertain costs for the work

completed till the period and after finishing the total work, it helps to determine total cost of the

contract.

Process costing: In case, when production is carried out through the different stages or

process involved is known as process costing (Darvas and et.al., 2012). This costing method helps

to ascertain costs of each process and transfer it into the next process and at the end, total

production costs will be identified.

Service costing: This method is uses by service rendering organizations such as water

supply department and electricity department to determine the costs of provided services.

1.3 Costing techniques

Costing techniques refers to the process through which organizations can allocate

expenditures effectively to determine their product costs.

Marginal costing/variable costing: According to CIMA London, marginal costing is the

method that helps to ascertain product costs and determine the impact of changes in costs, prices

and volume on the profitability (Penny and et.al., 2011). This method segregate total production

cost into fixed as well as variable costs. This method is also known as variable costing because it

exclude fixed costs in the cost ascertainment.

Standard costing: This technique evaluate actual production costs with the standard so as to

assess the effectiveness of business operations and aims at taking corrective actions to eliminate

adverse performance.

Absorption costing/Full costing technique: In this technique, all the fixed as well as

variable expenditures are taken into consideration to determine total product costs (Ogunlana and

et.al., 2010). This method is also known as full costing technique because it take into account all the

expenditures whether fixed or variable related to the production.

Historical costing: It is the technique to determine costs after incurred the expenditures so

that costs can be computed for the work done in the past. It helps to compare current costs with the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

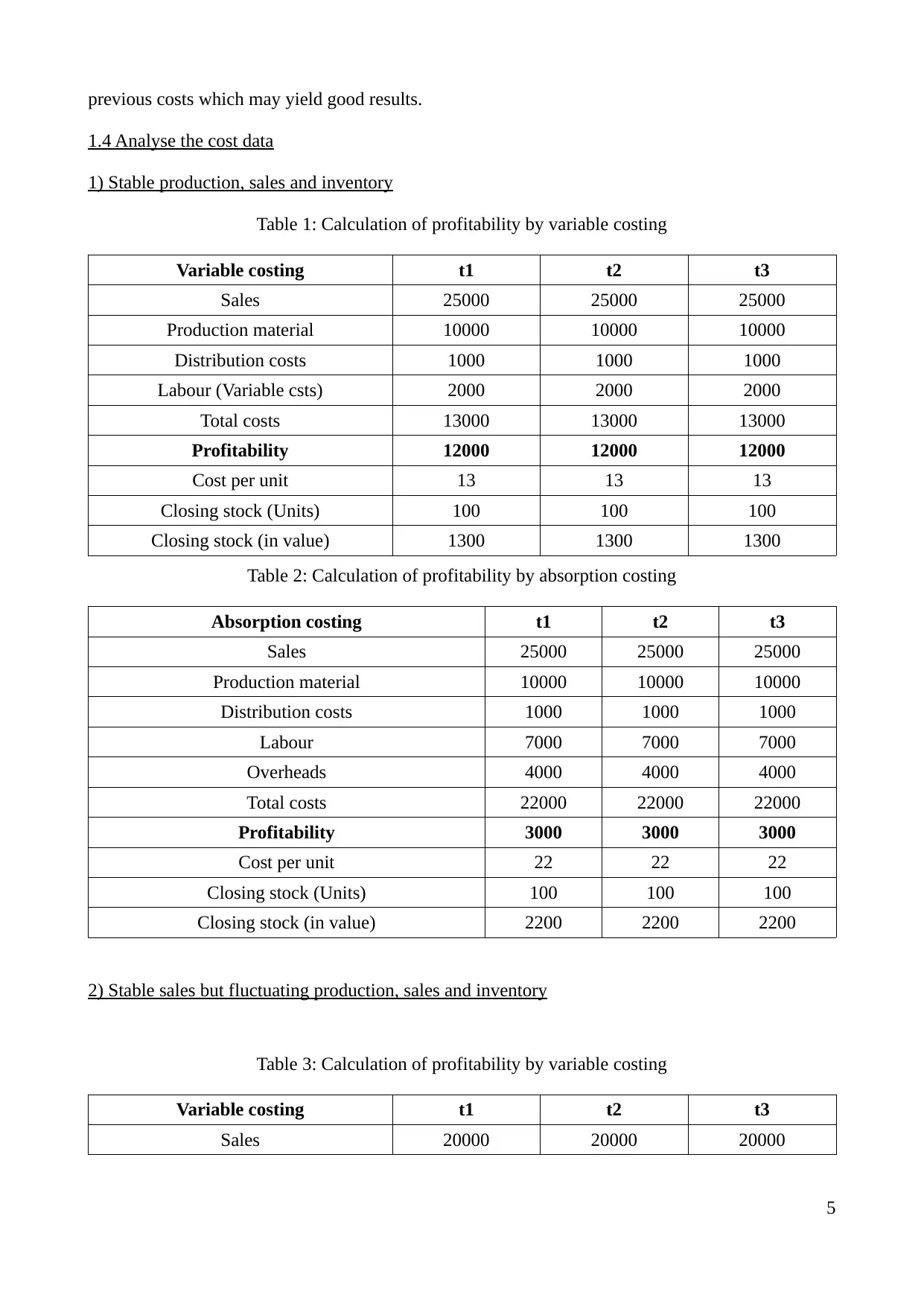

previous costs which may yield good results.

1.4 Analyse the cost data

1) Stable production, sales and inventory

Table 1: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable csts) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

2) Stable sales but fluctuating production, sales and inventory

Table 3: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 20000 20000 20000

5

1.4 Analyse the cost data

1) Stable production, sales and inventory

Table 1: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable csts) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

2) Stable sales but fluctuating production, sales and inventory

Table 3: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 20000 20000 20000

5

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Oveheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit

18.666666666

7 24.5

26.285714285

7

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.5714285

714

3) Stable production but fluctuating sales and inventory

Table 5: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

6

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Oveheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit

18.666666666

7 24.5

26.285714285

7

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.5714285

714

3) Stable production but fluctuating sales and inventory

Table 5: Calculation of profitability by variable costing

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Closing stock (in value) 7560 4960 1210

Table 6: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Oveheads 4000 4000 4000

Total costs 21600 21400 21100

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Enclosed in power point presentation.

2.1 Cost report and analysis

Hennes and Mauritz is UK based organization who sells variety of fashionable cloth

products to different age of people at cost effective prices. Steps to prepare cost report are

mentioned below:

At the initial stage, H&M business has to collect information about different types of costs

whether direct or indirect.

There after, H&M has to segregate costs into direct and indirect costs. Material, labour and

other production overhead are considered which helps to ascertain production costs. direct

while other will be called indirect.

After that, management has to decide profit margin to generate profitability through sales

operations.

H&M's managers has to construct costs report by accumulating all the costs such as

production, office and selling and distribution costs. It helps to determine total cost of

production and goods sold by the company.

After that, senior management need to analyse actual results with the standard costs. Less

actual costs indicates that H&M is administrating operations effectively which helps to

enlarge profitability. Further, high actual revenue than budgeted is also considered good and

indicates high productivity and contribute to increase profitability as well.

7

Table 6: Calculation of profitability by absorption costing

Absorption costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Oveheads 4000 4000 4000

Total costs 21600 21400 21100

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Enclosed in power point presentation.

2.1 Cost report and analysis

Hennes and Mauritz is UK based organization who sells variety of fashionable cloth

products to different age of people at cost effective prices. Steps to prepare cost report are

mentioned below:

At the initial stage, H&M business has to collect information about different types of costs

whether direct or indirect.

There after, H&M has to segregate costs into direct and indirect costs. Material, labour and

other production overhead are considered which helps to ascertain production costs. direct

while other will be called indirect.

After that, management has to decide profit margin to generate profitability through sales

operations.

H&M's managers has to construct costs report by accumulating all the costs such as

production, office and selling and distribution costs. It helps to determine total cost of

production and goods sold by the company.

After that, senior management need to analyse actual results with the standard costs. Less

actual costs indicates that H&M is administrating operations effectively which helps to

enlarge profitability. Further, high actual revenue than budgeted is also considered good and

indicates high productivity and contribute to increase profitability as well.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2 Various performance indicators used to identify potential improvements

There are various performance indicators that Hennes and Maurtiz can use to identify areas

for potential improvement, described below:

Turnover: Regular supply of fashionable and designer cloth products at affordable prices

helps to enlarge turnover, While, if H&M face declining in their turnover than it has to take

decisions to improve sales in the future.

Costs: H&M has to make effective control over the direct as well as indirect costs.

However, if costs is not effectively controlled by the H&M's management than they should

take decisions to reduce costs other wise, performance will be adversely affected.

Customer satisfaction: Supplying clothing products according to the customer demand is

necessary to satisfy them. Otherwise, H&M will lose their customers because consumers

will start to use other competitor's products. Hence, customer satisfaction is also a indicators

which helps to measure performance.

Employee satisfaction: Employees are the most crucial and integral part of H&M.

Therefore, company needs to satisfy their employees through providing good salary,

working culture and environment so that they will work hard and contributes to business

success.

Profitability: It is a sign of operational performance which can be computed through

subtracting total incurred expenses out of generated revenues. Rising trend of profit is

always considered good otherwise, H&M's management need to work on it.

2.3 Ways to reduce costs, enhance value and quality

Costs can be reduce through following ways:

Systematic cost control through consistently monitoring of the H&M's daily functions.

Comparison of actual costs with the prepared budgets so that corrective actions can be taken

to reduce costs for the future period.

Delegate authority and responsibility to the H&M's personnel at an incentive, specially

employees to control specific kind of costs by suggesting ideas to them.

Saving through reduction in unnecessary expenditures such as bargain with suppliers for

discounts, eliminate wastage by recycle and reuse etc.

Tighter control on financing, curtailment of short-term financing like training, advertisement

etc., reduce pay roll costs and use advanced technological which helps to automation

process.

8

There are various performance indicators that Hennes and Maurtiz can use to identify areas

for potential improvement, described below:

Turnover: Regular supply of fashionable and designer cloth products at affordable prices

helps to enlarge turnover, While, if H&M face declining in their turnover than it has to take

decisions to improve sales in the future.

Costs: H&M has to make effective control over the direct as well as indirect costs.

However, if costs is not effectively controlled by the H&M's management than they should

take decisions to reduce costs other wise, performance will be adversely affected.

Customer satisfaction: Supplying clothing products according to the customer demand is

necessary to satisfy them. Otherwise, H&M will lose their customers because consumers

will start to use other competitor's products. Hence, customer satisfaction is also a indicators

which helps to measure performance.

Employee satisfaction: Employees are the most crucial and integral part of H&M.

Therefore, company needs to satisfy their employees through providing good salary,

working culture and environment so that they will work hard and contributes to business

success.

Profitability: It is a sign of operational performance which can be computed through

subtracting total incurred expenses out of generated revenues. Rising trend of profit is

always considered good otherwise, H&M's management need to work on it.

2.3 Ways to reduce costs, enhance value and quality

Costs can be reduce through following ways:

Systematic cost control through consistently monitoring of the H&M's daily functions.

Comparison of actual costs with the prepared budgets so that corrective actions can be taken

to reduce costs for the future period.

Delegate authority and responsibility to the H&M's personnel at an incentive, specially

employees to control specific kind of costs by suggesting ideas to them.

Saving through reduction in unnecessary expenditures such as bargain with suppliers for

discounts, eliminate wastage by recycle and reuse etc.

Tighter control on financing, curtailment of short-term financing like training, advertisement

etc., reduce pay roll costs and use advanced technological which helps to automation

process.

8

Enhance value and quality:

In order to encourage H&M's workforce, managers need to satisfy them by job specification,

standardization and treat them in well manner. Health environment can be developed

through monitoring and motivating them continuously with the helps to monetary as well as

non-monetary rewards.

Advanced technology and highly talented employees will help to produce qualitative

products and lead to high customer satisfaction. Further, quality control mechanism also can

be use to quality control.

High profitability will increase shareholder's worth and business value as well. Further,

H&M's business expansion, high competitive strength and strategic capabilities also

contribute to increase corporation value.

TASK 3

3.1 Purpose and nature of budgeting process

Budget is the monetary plan of the organizations that forecast probable revenues and

expenditures for a specified period. The main purpose of budgets for Antonio Ltd, are given below:

Forecasting: It aims at estimating probable incomes, expenditure and profitability for the

budgeted period.

Financial planning: it is a tool that works as financial framework and provide huge

assistance to Antonio Ltd, managers for their decision-making process (VanDerbeck, 2012).

Comparison: It aims at making comparative study of actual performance with the set

targets and thereby take effective decisions to remove adverse variances and achieve desired

goals.

Nature of budgeting process:

Forecasting through the use of financial performance of the last period or budgets.

Determining the inflow that can be generated from sales and other business functions (Libby

and et.al., 2010).

Ascertain required amount that will be needed to spent on future course of actions and

activities. For instance, expenses on raw material purchase, wages payment, production as

well as non-production overheads.

Estimate deficit or surplus by subtracting total estimated expenditures from the revenues

generated.

Review the prepared budget for the final submission which will be communicated to

Antonio Ltd's all departments and will be expected to achieve these set targets by operating

9

In order to encourage H&M's workforce, managers need to satisfy them by job specification,

standardization and treat them in well manner. Health environment can be developed

through monitoring and motivating them continuously with the helps to monetary as well as

non-monetary rewards.

Advanced technology and highly talented employees will help to produce qualitative

products and lead to high customer satisfaction. Further, quality control mechanism also can

be use to quality control.

High profitability will increase shareholder's worth and business value as well. Further,

H&M's business expansion, high competitive strength and strategic capabilities also

contribute to increase corporation value.

TASK 3

3.1 Purpose and nature of budgeting process

Budget is the monetary plan of the organizations that forecast probable revenues and

expenditures for a specified period. The main purpose of budgets for Antonio Ltd, are given below:

Forecasting: It aims at estimating probable incomes, expenditure and profitability for the

budgeted period.

Financial planning: it is a tool that works as financial framework and provide huge

assistance to Antonio Ltd, managers for their decision-making process (VanDerbeck, 2012).

Comparison: It aims at making comparative study of actual performance with the set

targets and thereby take effective decisions to remove adverse variances and achieve desired

goals.

Nature of budgeting process:

Forecasting through the use of financial performance of the last period or budgets.

Determining the inflow that can be generated from sales and other business functions (Libby

and et.al., 2010).

Ascertain required amount that will be needed to spent on future course of actions and

activities. For instance, expenses on raw material purchase, wages payment, production as

well as non-production overheads.

Estimate deficit or surplus by subtracting total estimated expenditures from the revenues

generated.

Review the prepared budget for the final submission which will be communicated to

Antonio Ltd's all departments and will be expected to achieve these set targets by operating

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accordingly.

3.2 Budgeting method and its need

Antonio Ltd, can prepare budget by using any of the below explained methods.

Incremental budgeting: In this method, historical budget of the Antonio Ltd will be carried

forward for the budget preparation of next year. Incremental budgeting method make necessary

adjustment in the previous budget for the known factors like new legislations, additional sources,

price and wages rate increase due to inflation etc. This method is called incremental because only

the marginal adjustment will be require for budget formulation for each period (The Role of

Managerial Accounting in the Management Process, n.d.). The good aspect of this budget is it is

very simple to prepare budget and easily understandable by all the affected parties. While, its

limitation is it rely on the assumption that all the historical operations will be carry out in future

hence, it will enhance unnecessary expenditures and lead to reduce profitability of Antonio Ltd.

Zero-based budgeting (ZBB): This budgeting method assumes that Antonio Ltd is

starting their operations afresh in the new planning period. This method involves an in-depth

process in which management identify their future operations and estimate revenues and

expenditures from such activities. Every period budget is prepared with the focus on how Antonio

Ltd can achieve their targets hence, it aims at effective allocation of resources so that resources can

be optimized used which lead to enhance profitability (Rigby and et.al., 2015). It assist Antonio Ltd

to maximize their turnover, control costs and increase their potential profitability. Its drawback is it

takes very much time and consume high monetary sources. In order to obtain external information

about the market, Antonio Ltd need to conduct an market research so that it can identify that what

necessary functions will be carry out in future. Hence, it is an expensive approach.

3.3 Budget preparation

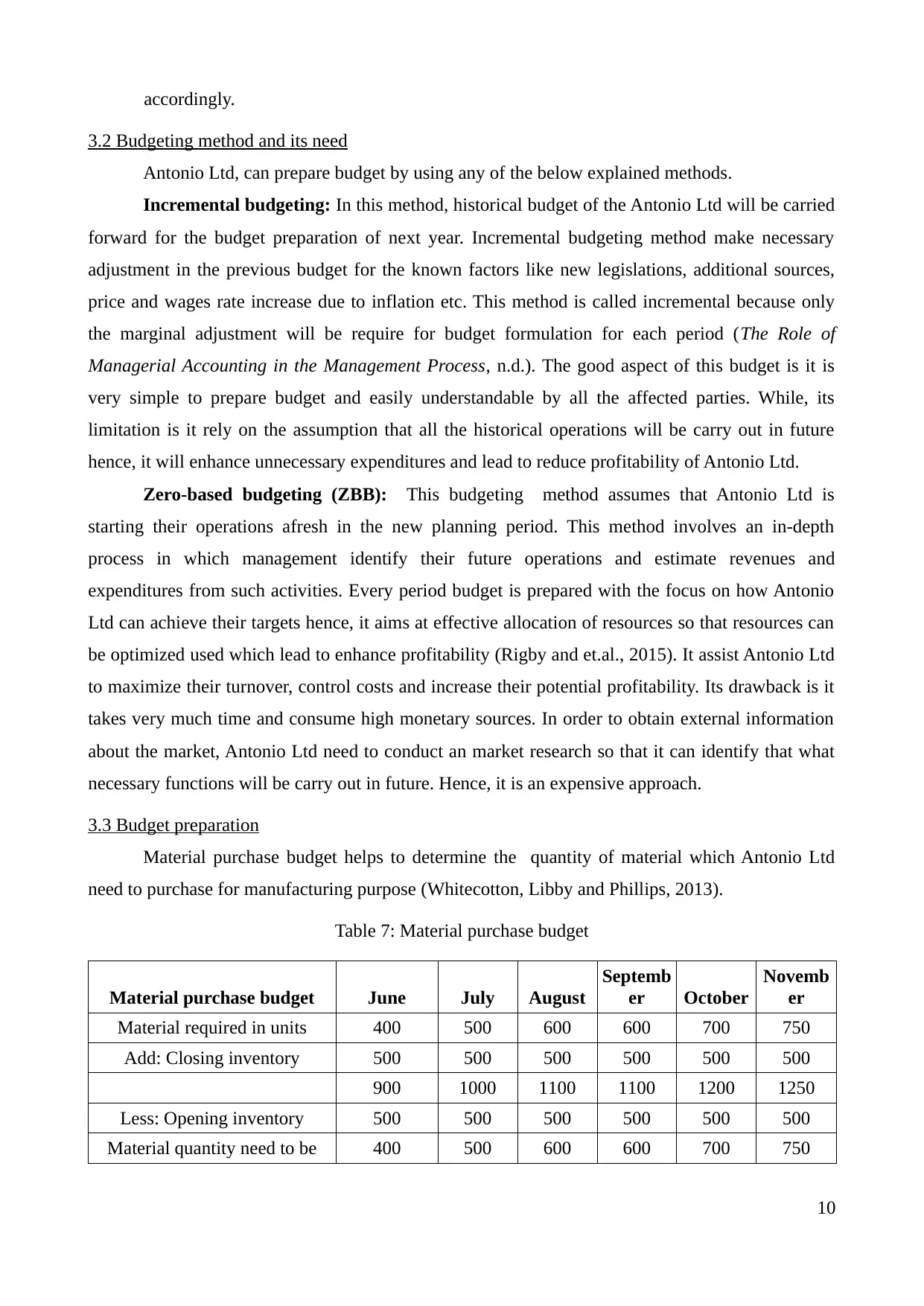

Material purchase budget helps to determine the quantity of material which Antonio Ltd

need to purchase for manufacturing purpose (Whitecotton, Libby and Phillips, 2013).

Table 7: Material purchase budget

Material purchase budget June July August

Septemb

er October

Novemb

er

Material required in units 400 500 600 600 700 750

Add: Closing inventory 500 500 500 500 500 500

900 1000 1100 1100 1200 1250

Less: Opening inventory 500 500 500 500 500 500

Material quantity need to be 400 500 600 600 700 750

10

3.2 Budgeting method and its need

Antonio Ltd, can prepare budget by using any of the below explained methods.

Incremental budgeting: In this method, historical budget of the Antonio Ltd will be carried

forward for the budget preparation of next year. Incremental budgeting method make necessary

adjustment in the previous budget for the known factors like new legislations, additional sources,

price and wages rate increase due to inflation etc. This method is called incremental because only

the marginal adjustment will be require for budget formulation for each period (The Role of

Managerial Accounting in the Management Process, n.d.). The good aspect of this budget is it is

very simple to prepare budget and easily understandable by all the affected parties. While, its

limitation is it rely on the assumption that all the historical operations will be carry out in future

hence, it will enhance unnecessary expenditures and lead to reduce profitability of Antonio Ltd.

Zero-based budgeting (ZBB): This budgeting method assumes that Antonio Ltd is

starting their operations afresh in the new planning period. This method involves an in-depth

process in which management identify their future operations and estimate revenues and

expenditures from such activities. Every period budget is prepared with the focus on how Antonio

Ltd can achieve their targets hence, it aims at effective allocation of resources so that resources can

be optimized used which lead to enhance profitability (Rigby and et.al., 2015). It assist Antonio Ltd

to maximize their turnover, control costs and increase their potential profitability. Its drawback is it

takes very much time and consume high monetary sources. In order to obtain external information

about the market, Antonio Ltd need to conduct an market research so that it can identify that what

necessary functions will be carry out in future. Hence, it is an expensive approach.

3.3 Budget preparation

Material purchase budget helps to determine the quantity of material which Antonio Ltd

need to purchase for manufacturing purpose (Whitecotton, Libby and Phillips, 2013).

Table 7: Material purchase budget

Material purchase budget June July August

Septemb

er October

Novemb

er

Material required in units 400 500 600 600 700 750

Add: Closing inventory 500 500 500 500 500 500

900 1000 1100 1100 1200 1250

Less: Opening inventory 500 500 500 500 500 500

Material quantity need to be 400 500 600 600 700 750

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purchased

Material price 8 8 8 8 8 8

Total material value 3200 4000 4800 4800 5600 6000

Trade payable budget helps to determine closing payable balance.

Table 8: Trade payable budgets

Particulars June July August September October

Novemb

er

Trade payable for material 3200 4000 4800 4800 5600 6000

Trade payable for production

overheads 280 320 320 320 320 400

Total trade payables 3480 4320 5120 5120 5920 6400

3.4 Preparation of cash budget for Antonio Ltd

It is a budget which take into consideration all the cash inflow and outflow aims at

determining net cash flow and closing cash balance (Cash Budget, 2016).

Table 9: Cash budget of Antonio for six months ending on 31st December, 2016

Particulars July August September October Nov. Dec.

Opening cash at bank 7500 13840 27680 53560 104620 208220

Cash inflow

Cash sales 4800 6000 7200 7800 8400 9600

Credit sales for two

months 2800 3200 3200 4000 4800 5200

Total cash inflow 7600 9200 10400 11800 13200 14800

Total cash available

for use 15100 23040 38080 65360 117820 223020

Cash outflow

Raw material purchase

at one month credit 3200 4000 4800 4800 5600 6000

Direct production

expenses including

labour 3000 3600 3600 4200 4500 4500

Production overheads

excluded depreciation 1560 1600 1600 1600 1920 1920

New item of plant 2200 2200 2200

Advertisement costs 1000 1500

Total cash outflow 8760 9200 12200 14300 14220 12420

11

Material price 8 8 8 8 8 8

Total material value 3200 4000 4800 4800 5600 6000

Trade payable budget helps to determine closing payable balance.

Table 8: Trade payable budgets

Particulars June July August September October

Novemb

er

Trade payable for material 3200 4000 4800 4800 5600 6000

Trade payable for production

overheads 280 320 320 320 320 400

Total trade payables 3480 4320 5120 5120 5920 6400

3.4 Preparation of cash budget for Antonio Ltd

It is a budget which take into consideration all the cash inflow and outflow aims at

determining net cash flow and closing cash balance (Cash Budget, 2016).

Table 9: Cash budget of Antonio for six months ending on 31st December, 2016

Particulars July August September October Nov. Dec.

Opening cash at bank 7500 13840 27680 53560 104620 208220

Cash inflow

Cash sales 4800 6000 7200 7800 8400 9600

Credit sales for two

months 2800 3200 3200 4000 4800 5200

Total cash inflow 7600 9200 10400 11800 13200 14800

Total cash available

for use 15100 23040 38080 65360 117820 223020

Cash outflow

Raw material purchase

at one month credit 3200 4000 4800 4800 5600 6000

Direct production

expenses including

labour 3000 3600 3600 4200 4500 4500

Production overheads

excluded depreciation 1560 1600 1600 1600 1920 1920

New item of plant 2200 2200 2200

Advertisement costs 1000 1500

Total cash outflow 8760 9200 12200 14300 14220 12420

11

Net cash flow 6340 13840 25880 51060 103600 210600

Closing cash balance 13840 27680 53560 104620 208220 418820

How to remove deficit net cash flow:

Control the spendings is one of the significant way to control cash outflow and enlarge net

cash flow. It helps to manage material cost, labour costs, direct and indirect production

overhead as well.

Increasing the turnover is also beneficial to remove deficit balance of cash and thereby

increasing closing cash balance.

TASK 4

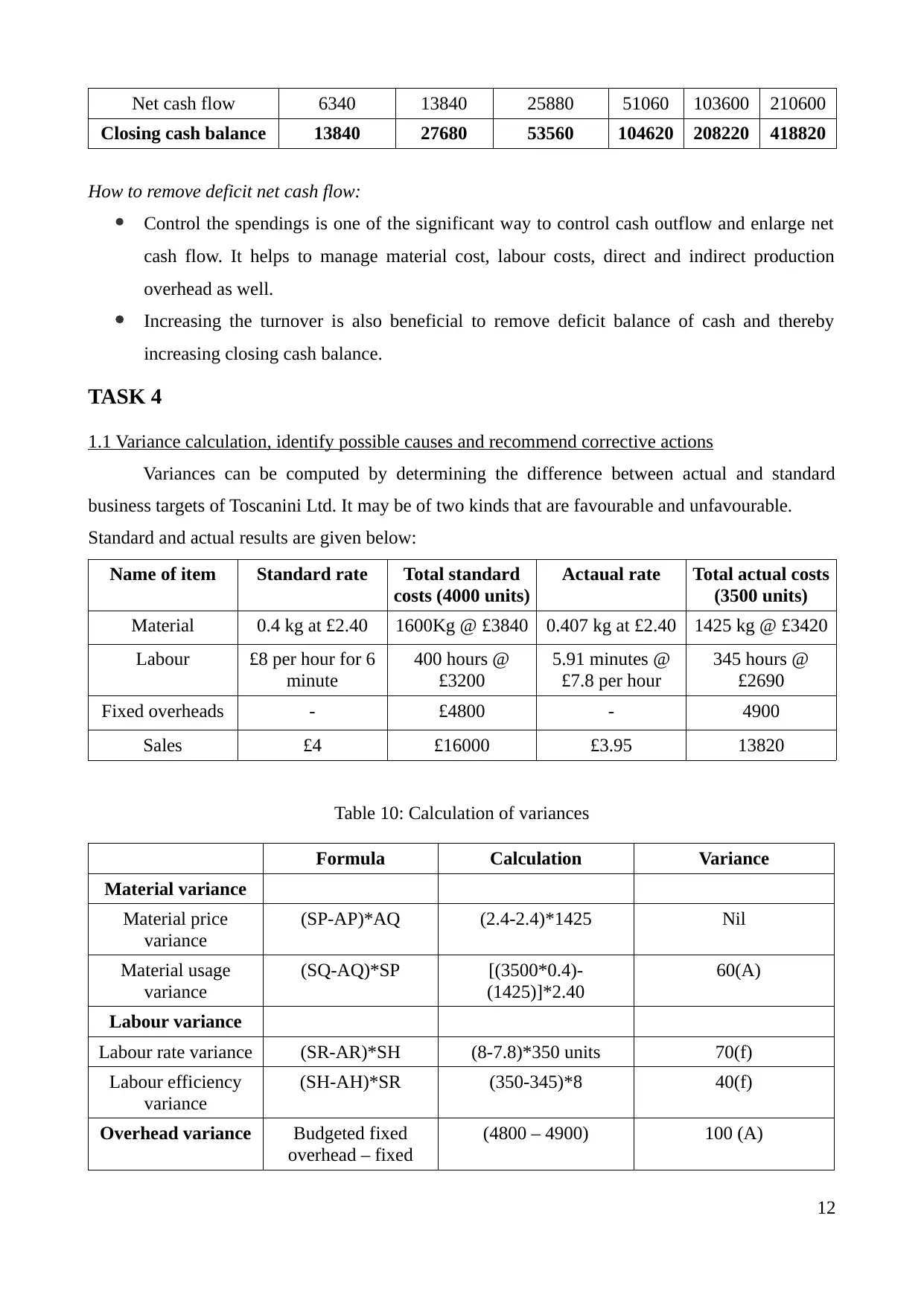

1.1 Variance calculation, identify possible causes and recommend corrective actions

Variances can be computed by determining the difference between actual and standard

business targets of Toscanini Ltd. It may be of two kinds that are favourable and unfavourable.

Standard and actual results are given below:

Name of item Standard rate Total standard

costs (4000 units)

Actaual rate Total actual costs

(3500 units)

Material 0.4 kg at £2.40 1600Kg @ £3840 0.407 kg at £2.40 1425 kg @ £3420

Labour £8 per hour for 6

minute

400 hours @

£3200

5.91 minutes @

£7.8 per hour

345 hours @

£2690

Fixed overheads - £4800 - 4900

Sales £4 £16000 £3.95 13820

Table 10: Calculation of variances

Formula Calculation Variance

Material variance

Material price

variance

(SP-AP)*AQ (2.4-2.4)*1425 Nil

Material usage

variance

(SQ-AQ)*SP [(3500*0.4)-

(1425)]*2.40

60(A)

Labour variance

Labour rate variance (SR-AR)*SH (8-7.8)*350 units 70(f)

Labour efficiency

variance

(SH-AH)*SR (350-345)*8 40(f)

Overhead variance Budgeted fixed

overhead – fixed

(4800 – 4900) 100 (A)

12

Closing cash balance 13840 27680 53560 104620 208220 418820

How to remove deficit net cash flow:

Control the spendings is one of the significant way to control cash outflow and enlarge net

cash flow. It helps to manage material cost, labour costs, direct and indirect production

overhead as well.

Increasing the turnover is also beneficial to remove deficit balance of cash and thereby

increasing closing cash balance.

TASK 4

1.1 Variance calculation, identify possible causes and recommend corrective actions

Variances can be computed by determining the difference between actual and standard

business targets of Toscanini Ltd. It may be of two kinds that are favourable and unfavourable.

Standard and actual results are given below:

Name of item Standard rate Total standard

costs (4000 units)

Actaual rate Total actual costs

(3500 units)

Material 0.4 kg at £2.40 1600Kg @ £3840 0.407 kg at £2.40 1425 kg @ £3420

Labour £8 per hour for 6

minute

400 hours @

£3200

5.91 minutes @

£7.8 per hour

345 hours @

£2690

Fixed overheads - £4800 - 4900

Sales £4 £16000 £3.95 13820

Table 10: Calculation of variances

Formula Calculation Variance

Material variance

Material price

variance

(SP-AP)*AQ (2.4-2.4)*1425 Nil

Material usage

variance

(SQ-AQ)*SP [(3500*0.4)-

(1425)]*2.40

60(A)

Labour variance

Labour rate variance (SR-AR)*SH (8-7.8)*350 units 70(f)

Labour efficiency

variance

(SH-AH)*SR (350-345)*8 40(f)

Overhead variance Budgeted fixed

overhead – fixed

(4800 – 4900) 100 (A)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.