British Tobacco Company: Application of Management Accounting

VerifiedAdded on 2023/04/20

|13

|2016

|323

Report

AI Summary

This report provides a comprehensive analysis of management accounting techniques and their application to British Tobacco Company. It begins by defining management accounting and its importance in strategic decision-making, highlighting techniques such as marginal costing, ratio analysis, standard costing, activity-based costing (ABC), and cash flow statements. The report then demonstrates the application of ABC costing and ratio analysis, interpreting the results with a focus on debt-equity and profitability ratios. The analysis suggests that while British Tobacco's debt-equity ratio has improved, it remains high, indicating a reliance on debt financing. Profitability has increased, providing better returns to shareholders. The report concludes that proper implementation of management accounting techniques can enhance resource utilization, reduce costs, and improve overall company performance. Desklib offers a range of solved assignments and study resources to aid students in understanding these concepts further.

Running Head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author Note

Management Accounting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Executive Summary:

The purpose of this assignment is to provide clear understanding about the management

accounting through explanation of different management techniques and their impact on the

decision making process of management. This assignment also evaluates the performance of the

company from the data obtained from recent financial statement of British Tobacco Company.

MANAGEMENT ACCOUNTING

Executive Summary:

The purpose of this assignment is to provide clear understanding about the management

accounting through explanation of different management techniques and their impact on the

decision making process of management. This assignment also evaluates the performance of the

company from the data obtained from recent financial statement of British Tobacco Company.

2

MANAGEMENT ACCOUNTING

Table of Contents

1. Introduction:................................................................................................................................4

2. Management Accounting and its importance:.............................................................................4

2.1 Management Accounting:......................................................................................................4

2.2 Importance of Management Accounting...............................................................................5

3. Management accounting techniques available to BAT group:....................................................7

3.1 Marginal costing:...................................................................................................................7

3.2 Ratio analysis:........................................................................................................................7

3.3 Standard costing:...................................................................................................................7

3.4 Activity Based Costing (ABC):.............................................................................................8

3.5 Cash flow statement:..............................................................................................................8

4. Application of Different Management Techniques:....................................................................8

4.1 Application of ABC Costing:................................................................................................8

4.2 Application of Ratios:............................................................................................................9

5. Interpretation of Results and Recommendations:......................................................................10

5.2 Interpretation of financial ratios:.........................................................................................10

5.2.1 Debt-Equity Ratio:........................................................................................................10

5.2.2 Profitability Ratio:........................................................................................................10

5.2 Interpretation of Product Profitability:................................................................................10

6. Conclusion:................................................................................................................................10

7. References:................................................................................................................................12

MANAGEMENT ACCOUNTING

Table of Contents

1. Introduction:................................................................................................................................4

2. Management Accounting and its importance:.............................................................................4

2.1 Management Accounting:......................................................................................................4

2.2 Importance of Management Accounting...............................................................................5

3. Management accounting techniques available to BAT group:....................................................7

3.1 Marginal costing:...................................................................................................................7

3.2 Ratio analysis:........................................................................................................................7

3.3 Standard costing:...................................................................................................................7

3.4 Activity Based Costing (ABC):.............................................................................................8

3.5 Cash flow statement:..............................................................................................................8

4. Application of Different Management Techniques:....................................................................8

4.1 Application of ABC Costing:................................................................................................8

4.2 Application of Ratios:............................................................................................................9

5. Interpretation of Results and Recommendations:......................................................................10

5.2 Interpretation of financial ratios:.........................................................................................10

5.2.1 Debt-Equity Ratio:........................................................................................................10

5.2.2 Profitability Ratio:........................................................................................................10

5.2 Interpretation of Product Profitability:................................................................................10

6. Conclusion:................................................................................................................................10

7. References:................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

1. Introduction:

British American Tobacco Company is one of the leading tobacco and cigarette

manufacturing company in the world. It has its headquarter in London and primarily listed in

London stock exchange. The company has also secondary listing in Johannesburg stock

exchange, Nairobi Securities Exchange and New York stock exchange. It is also known for its

top most selling brands such as Dunhill, Lucky strike, Kent and Pall Mall which is popular

worldwide.

It was formed in late of 1902 due to joint venture agreement between Imperial Tobacco

Company of UK and American Tobacco Company of US to share mutual understanding and to

divide market share among them.

2. Management Accounting and its importance:

2.1 Management Accounting:

Management accounting is the systematic evaluation, analysis and interpretation of

financial information in such a way that the findings of such evaluation, analysis and

interpretation helps the management in formulating policies regarding future course of action and

making strategic decisions. Management accountant generally uses financial as well as

accounting information to predict upcoming threats and opportunities for the company. So it can

be used as an early signs of threats to protect from the adverse effects of such threats before that

threat results into a substantial or material loss to the company. Thus, Management accounting

means the use of financial and accounting data to evaluate, measure and prepare the report on

company’s performance in order to develop an insight about the strategies adopted by the

management and its implications on the current performance.

MANAGEMENT ACCOUNTING

1. Introduction:

British American Tobacco Company is one of the leading tobacco and cigarette

manufacturing company in the world. It has its headquarter in London and primarily listed in

London stock exchange. The company has also secondary listing in Johannesburg stock

exchange, Nairobi Securities Exchange and New York stock exchange. It is also known for its

top most selling brands such as Dunhill, Lucky strike, Kent and Pall Mall which is popular

worldwide.

It was formed in late of 1902 due to joint venture agreement between Imperial Tobacco

Company of UK and American Tobacco Company of US to share mutual understanding and to

divide market share among them.

2. Management Accounting and its importance:

2.1 Management Accounting:

Management accounting is the systematic evaluation, analysis and interpretation of

financial information in such a way that the findings of such evaluation, analysis and

interpretation helps the management in formulating policies regarding future course of action and

making strategic decisions. Management accountant generally uses financial as well as

accounting information to predict upcoming threats and opportunities for the company. So it can

be used as an early signs of threats to protect from the adverse effects of such threats before that

threat results into a substantial or material loss to the company. Thus, Management accounting

means the use of financial and accounting data to evaluate, measure and prepare the report on

company’s performance in order to develop an insight about the strategies adopted by the

management and its implications on the current performance.

5

MANAGEMENT ACCOUNTING

The management accounting gives the idea about the health of the company financial

performance through different management techniques such as marginal costing, standard

costing, fund flow analysis and cash flow analysis to the different stakeholders of the company.

Proper use of management accounting techniques gives the management of the company, the

ability to enhance their performance and to formulate strategic road map to tackle upcoming

sudden changes in the process or In the market segment.

2.2 Importance of Management Accounting.

Management accounting has several important features that can be achieved through proper

utilization of management accounting techniques and proper formulation and implementation of

strategic managerial policies. Followings are the importance of management accounting

technique, explained below:

Calculation and interpretation of variances: variances are the result of the improper policy

adopted by the management. variances is of two type , first one is favorable variances

which is the result of proper planning and the second one is the adverse variances which

is the result of inappropriate implementation of management plan. Variances give the

management the insight about area of improvement in the existing process. For example,

variances like raw material price variances could be the result of improper purchase

procedure adopted and emergency requirement of raw materials.

As British American Tobacco Company is engaged in the acquiring raw tobacco

from different sources, it is exposed towards to the fluctuation in the price of raw

tobacco, which may or may not be favorable for the company. Therefore, proper purchase

mechanism can reduce the adverse price variances due to such fluctuation in prices.

MANAGEMENT ACCOUNTING

The management accounting gives the idea about the health of the company financial

performance through different management techniques such as marginal costing, standard

costing, fund flow analysis and cash flow analysis to the different stakeholders of the company.

Proper use of management accounting techniques gives the management of the company, the

ability to enhance their performance and to formulate strategic road map to tackle upcoming

sudden changes in the process or In the market segment.

2.2 Importance of Management Accounting.

Management accounting has several important features that can be achieved through proper

utilization of management accounting techniques and proper formulation and implementation of

strategic managerial policies. Followings are the importance of management accounting

technique, explained below:

Calculation and interpretation of variances: variances are the result of the improper policy

adopted by the management. variances is of two type , first one is favorable variances

which is the result of proper planning and the second one is the adverse variances which

is the result of inappropriate implementation of management plan. Variances give the

management the insight about area of improvement in the existing process. For example,

variances like raw material price variances could be the result of improper purchase

procedure adopted and emergency requirement of raw materials.

As British American Tobacco Company is engaged in the acquiring raw tobacco

from different sources, it is exposed towards to the fluctuation in the price of raw

tobacco, which may or may not be favorable for the company. Therefore, proper purchase

mechanism can reduce the adverse price variances due to such fluctuation in prices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

Helps in choosing best course of action between Make or Buy: The appropriate strategy

or course of action between Make or buy, can be analyzed through the cost benefit

analysis technique of management accounting. In this technique cost of manufacturing

and cost of purchasing are compared together to understand best suitable alternative to

adopt with analysis of opportunity cost to be achieved or to be lost.

The British American Tobacco company uses different types of raw materials to

be used in the production process. Therefore, it can use the above said technique to

evaluate whether In house production or outsourcing of such material is favorable or not.

Profitability analysis of the product: the profitability analysis of the upcoming project or

product can be analyzed through use of marginal costing technique. In this management

technique, management accountant uses some historical data to forecast estimated cost

and the amount of contribution that can be achieved through this product to recover

unavoidable fixed overhead related to the product. It gives the clear idea about the break-

even sales and margin of safety that the company will have to maintain for avoiding the

losses, which mostly will consist of, allocated unavoidable fixed overhead. The British

American Tobacco company is on the way of lunch of two products namely B&H

Strawberry and B&H cherry. It can use marginal costing technique to evaluate

profitability of the product.

Prediction of future cash flows: the management accountant can forecast estimated future

cash flows of a project or product through budgetary control technique and trend analysis

of past cash flows. In budgetary control technique, budgets are prepared based on the past

performance of the company and to compare the actual result of the company with the

MANAGEMENT ACCOUNTING

Helps in choosing best course of action between Make or Buy: The appropriate strategy

or course of action between Make or buy, can be analyzed through the cost benefit

analysis technique of management accounting. In this technique cost of manufacturing

and cost of purchasing are compared together to understand best suitable alternative to

adopt with analysis of opportunity cost to be achieved or to be lost.

The British American Tobacco company uses different types of raw materials to

be used in the production process. Therefore, it can use the above said technique to

evaluate whether In house production or outsourcing of such material is favorable or not.

Profitability analysis of the product: the profitability analysis of the upcoming project or

product can be analyzed through use of marginal costing technique. In this management

technique, management accountant uses some historical data to forecast estimated cost

and the amount of contribution that can be achieved through this product to recover

unavoidable fixed overhead related to the product. It gives the clear idea about the break-

even sales and margin of safety that the company will have to maintain for avoiding the

losses, which mostly will consist of, allocated unavoidable fixed overhead. The British

American Tobacco company is on the way of lunch of two products namely B&H

Strawberry and B&H cherry. It can use marginal costing technique to evaluate

profitability of the product.

Prediction of future cash flows: the management accountant can forecast estimated future

cash flows of a project or product through budgetary control technique and trend analysis

of past cash flows. In budgetary control technique, budgets are prepared based on the past

performance of the company and to compare the actual result of the company with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

parameters set out in budget which will help the management to take remedial steps to

overcome with the variances occurred in between budgeted and actual result.

3. Management accounting techniques available to BAT group:

List of management accounting that can be used in the BAT group:

Marginal costing.

Ratio analysis.

Standard costing.

Activity Based Costing (ABC).

Cash flow statement.

3.1 Marginal costing:

In this, the product pricing depends upon the variable cost and unavoidable fixed cost

associated with the product to determine the target sale by which optimal return on capital

employed can be achieved.

3.2 Ratio analysis:

Ratio is computed based on the financial information to interpret the health of the

business. In ratio analysis, the computed ratios are compared with the industry averages to

understand the level of effectiveness being offered by the company through its work. Investors to

evaluate the return potential of the company mostly use ratio.

3.3 Standard costing:

In this management technique, the management fixes standards by considering past

performances and such other factor, which is directly attributable to the fixing of standard.

MANAGEMENT ACCOUNTING

parameters set out in budget which will help the management to take remedial steps to

overcome with the variances occurred in between budgeted and actual result.

3. Management accounting techniques available to BAT group:

List of management accounting that can be used in the BAT group:

Marginal costing.

Ratio analysis.

Standard costing.

Activity Based Costing (ABC).

Cash flow statement.

3.1 Marginal costing:

In this, the product pricing depends upon the variable cost and unavoidable fixed cost

associated with the product to determine the target sale by which optimal return on capital

employed can be achieved.

3.2 Ratio analysis:

Ratio is computed based on the financial information to interpret the health of the

business. In ratio analysis, the computed ratios are compared with the industry averages to

understand the level of effectiveness being offered by the company through its work. Investors to

evaluate the return potential of the company mostly use ratio.

3.3 Standard costing:

In this management technique, the management fixes standards by considering past

performances and such other factor, which is directly attributable to the fixing of standard.

8

MANAGEMENT ACCOUNTING

Standard results are compared with the actual result to calculate variances. Variances of adverse

nature are to be reported to the management and necessary steps can be taken to reduce such

adverse variances.

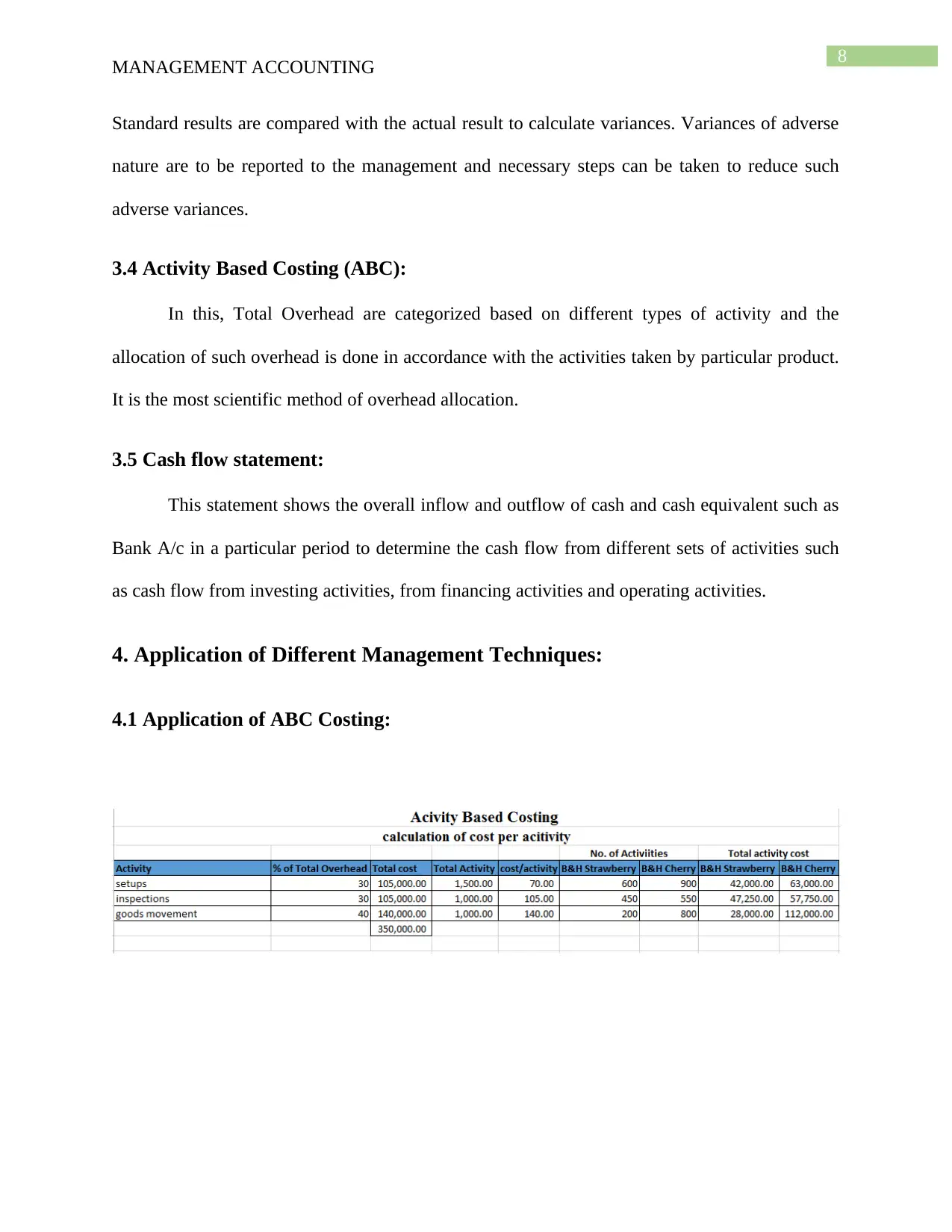

3.4 Activity Based Costing (ABC):

In this, Total Overhead are categorized based on different types of activity and the

allocation of such overhead is done in accordance with the activities taken by particular product.

It is the most scientific method of overhead allocation.

3.5 Cash flow statement:

This statement shows the overall inflow and outflow of cash and cash equivalent such as

Bank A/c in a particular period to determine the cash flow from different sets of activities such

as cash flow from investing activities, from financing activities and operating activities.

4. Application of Different Management Techniques:

4.1 Application of ABC Costing:

MANAGEMENT ACCOUNTING

Standard results are compared with the actual result to calculate variances. Variances of adverse

nature are to be reported to the management and necessary steps can be taken to reduce such

adverse variances.

3.4 Activity Based Costing (ABC):

In this, Total Overhead are categorized based on different types of activity and the

allocation of such overhead is done in accordance with the activities taken by particular product.

It is the most scientific method of overhead allocation.

3.5 Cash flow statement:

This statement shows the overall inflow and outflow of cash and cash equivalent such as

Bank A/c in a particular period to determine the cash flow from different sets of activities such

as cash flow from investing activities, from financing activities and operating activities.

4. Application of Different Management Techniques:

4.1 Application of ABC Costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

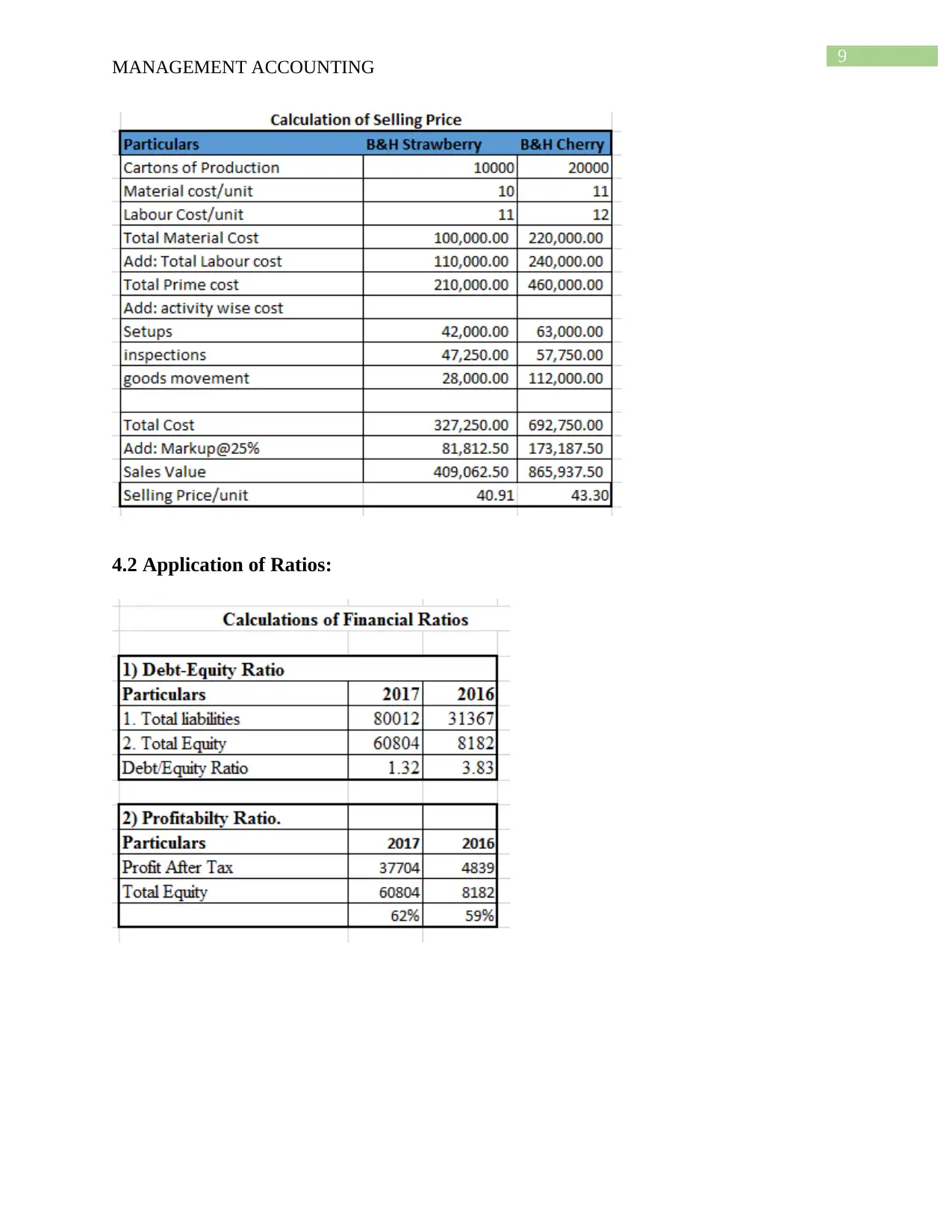

4.2 Application of Ratios:

MANAGEMENT ACCOUNTING

4.2 Application of Ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

5. Interpretation of Results and Recommendations:

5.2 Interpretation of financial ratios:

5.2.1 Debt-Equity Ratio:

As seen from the above calculations, the ratio of 2016 is 3.83 and of 2017 is 1.32. it

means overall Debt allocation to the financial statement as compared to the equity has been

improved but the company still has ratio greater than 1. This means the company is more of debt

funded which is not a good sign for the potential investors and Debt Holders of the company

because they prefer a ratio lower than one. Higher the ratio, the company is more exposed

towards higher borrowing cost.

5.2.2 Profitability Ratio:

The overall profitability of the company has been increased from 59% to 62% resulting in

the more return to the shareholders. The ratio shows that how much return has been provided to

potential investors of the company in terms of Profit after tax. The company has provided more

return as compared to previous financial year.

5.2 Interpretation of Product Profitability:

Using ABC costing for calculating the price of the product is appropriate method of price

fixation but it has some limitations i.e. sometimes the price of the product is market driven. The

estimated return on the product shows the return on capital employed on the product.

6. Conclusion:

It can be concluded that the proper implementation techniques will result in an increase in

the overall performance of the company. The company can achieve proper utilization of the

MANAGEMENT ACCOUNTING

5. Interpretation of Results and Recommendations:

5.2 Interpretation of financial ratios:

5.2.1 Debt-Equity Ratio:

As seen from the above calculations, the ratio of 2016 is 3.83 and of 2017 is 1.32. it

means overall Debt allocation to the financial statement as compared to the equity has been

improved but the company still has ratio greater than 1. This means the company is more of debt

funded which is not a good sign for the potential investors and Debt Holders of the company

because they prefer a ratio lower than one. Higher the ratio, the company is more exposed

towards higher borrowing cost.

5.2.2 Profitability Ratio:

The overall profitability of the company has been increased from 59% to 62% resulting in

the more return to the shareholders. The ratio shows that how much return has been provided to

potential investors of the company in terms of Profit after tax. The company has provided more

return as compared to previous financial year.

5.2 Interpretation of Product Profitability:

Using ABC costing for calculating the price of the product is appropriate method of price

fixation but it has some limitations i.e. sometimes the price of the product is market driven. The

estimated return on the product shows the return on capital employed on the product.

6. Conclusion:

It can be concluded that the proper implementation techniques will result in an increase in

the overall performance of the company. The company can achieve proper utilization of the

11

MANAGEMENT ACCOUNTING

resources employed with a significant reduction in the cost through proper utilization of

management techniques and proper allocation of available resources. The management

accounting techniques plays key role in structuring of managerial decisions through deep

analysis of financial results with the application of different management techniques.

MANAGEMENT ACCOUNTING

resources employed with a significant reduction in the cost through proper utilization of

management techniques and proper allocation of available resources. The management

accounting techniques plays key role in structuring of managerial decisions through deep

analysis of financial results with the application of different management techniques.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.