Management Accounting Report: Costing, Budgeting and Revenue Analysis

VerifiedAdded on 2020/05/16

|16

|2545

|62

Report

AI Summary

This report presents a detailed analysis of two case studies in management accounting. The first case focuses on US Bright Product Company, exploring Activity Based Costing (ABC) to determine the per-unit cost of cakes and pastries. The report calculates activity costs, cost per unit, and the bill of activities for the Lamington division, including an assessment of additional costs. The second case examines Hawthorn Leisure Works (HLW), a fitness center, and evaluates the revenue implications of a new membership plan compared to the old plan. The analysis includes revenue calculations under both plans and a comparative study to determine the financial impact of the changes. The report concludes with insights into the financial performance of both companies and the effectiveness of the costing and budgeting techniques used.

Running Head: Management Accounting

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 2

Executive Summary:

This report consist of two cases, the first case is about Activity Based Costing. Activity

Based Costing is all about allocation of cost on the basis of the cost drivers allocated for each

type of cost. The cost is divided by the particular cost driver and then the total cost per unit is

calculated by adding all the allocated costs. In this case our evaluation is regarding US bright

product company they are manufactures of cakes and pastries. The case is about they want to

know per unit cost of their product using activity based costing. Activity based costing

elaborates the relationship between activities, cost and products.

This case consists of three parts, the first part is about the calculation of the activity cost

using the activity pools and then the cost per unit is summed out from that. The second part is

about the calculation of the amount of billing and the unit cost of the cakes and pastries of

Lamington. The third case is to know about what additional costs US Bright need to add to

arrive at the product cost of Lamington.

The second case is about Budgeting Techniques, the techniques need to be implemented to

know about Hawthorn Leisure Works new plan regarding its revenues from the membership

fee of the members. Hawthorn Leisure Works is a physical fitness centre which also offers

tennis court facilities to its members. This case is about the future growth prospects of HWLs

and helps in decision making of HWLs. They want to change their membership plan and

want a brief comparison between the old and the new plan.

Executive Summary:

This report consist of two cases, the first case is about Activity Based Costing. Activity

Based Costing is all about allocation of cost on the basis of the cost drivers allocated for each

type of cost. The cost is divided by the particular cost driver and then the total cost per unit is

calculated by adding all the allocated costs. In this case our evaluation is regarding US bright

product company they are manufactures of cakes and pastries. The case is about they want to

know per unit cost of their product using activity based costing. Activity based costing

elaborates the relationship between activities, cost and products.

This case consists of three parts, the first part is about the calculation of the activity cost

using the activity pools and then the cost per unit is summed out from that. The second part is

about the calculation of the amount of billing and the unit cost of the cakes and pastries of

Lamington. The third case is to know about what additional costs US Bright need to add to

arrive at the product cost of Lamington.

The second case is about Budgeting Techniques, the techniques need to be implemented to

know about Hawthorn Leisure Works new plan regarding its revenues from the membership

fee of the members. Hawthorn Leisure Works is a physical fitness centre which also offers

tennis court facilities to its members. This case is about the future growth prospects of HWLs

and helps in decision making of HWLs. They want to change their membership plan and

want a brief comparison between the old and the new plan.

Management Accounting 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 4

Table of Contents

Assessment Task A..................................................................................................................................5

Introduction:.........................................................................................................................................5

Part (a)..................................................................................................................................................5

Part (b).................................................................................................................................................7

Part (c)..................................................................................................................................................8

Conclusion:..........................................................................................................................................9

Assessment Task B................................................................................................................................10

Introduction:.......................................................................................................................................10

Part (a)................................................................................................................................................12

Part (b)...............................................................................................................................................13

Part (c)................................................................................................................................................14

Conclusion:........................................................................................................................................15

References:.............................................................................................................................................16

Table of Contents

Assessment Task A..................................................................................................................................5

Introduction:.........................................................................................................................................5

Part (a)..................................................................................................................................................5

Part (b).................................................................................................................................................7

Part (c)..................................................................................................................................................8

Conclusion:..........................................................................................................................................9

Assessment Task B................................................................................................................................10

Introduction:.......................................................................................................................................10

Part (a)................................................................................................................................................12

Part (b)...............................................................................................................................................13

Part (c)................................................................................................................................................14

Conclusion:........................................................................................................................................15

References:.............................................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 5

Assessment Task A

Introduction:

Activity Based Costing is the method of costing that pools the activities on the basis of their

type and the quantum. The Activity Based Costing is about the allocation of cost on the basis

of the cost drivers. This costing system is used by all the manufacturing units as this is

actually the proper allocation of the cost (Edmonds, Edmonds, Tsay and Olds, 2016). With

the help of ABC Costing we can analyse the product cost and do the profitability analysis of

the company.

Our case is about US Bright Product Company they are manufactures of cakes and pastries,

they use Activity Based Costing Technique for allocating their indirect cost to the product.

Our analysis is also based on the allocation of indirect cost with the help of Activity Based

Costing Techniques. The companies Indirect costs are given, what we need to do is to

allocate these costs on the basis of cost drivers available to us. The first part is all about

allocation of indirect cost on the basis of cost drivers. The second case is about one of the

division of US Bright that is Lamington; we need to draw a Statement of Bill of Activities of

Lamington and then we need to calculate its product cost. Lastly we need to tell them about

the additional costs that need to be added in the Lamington cost to arrive at the Lamington

product cost.

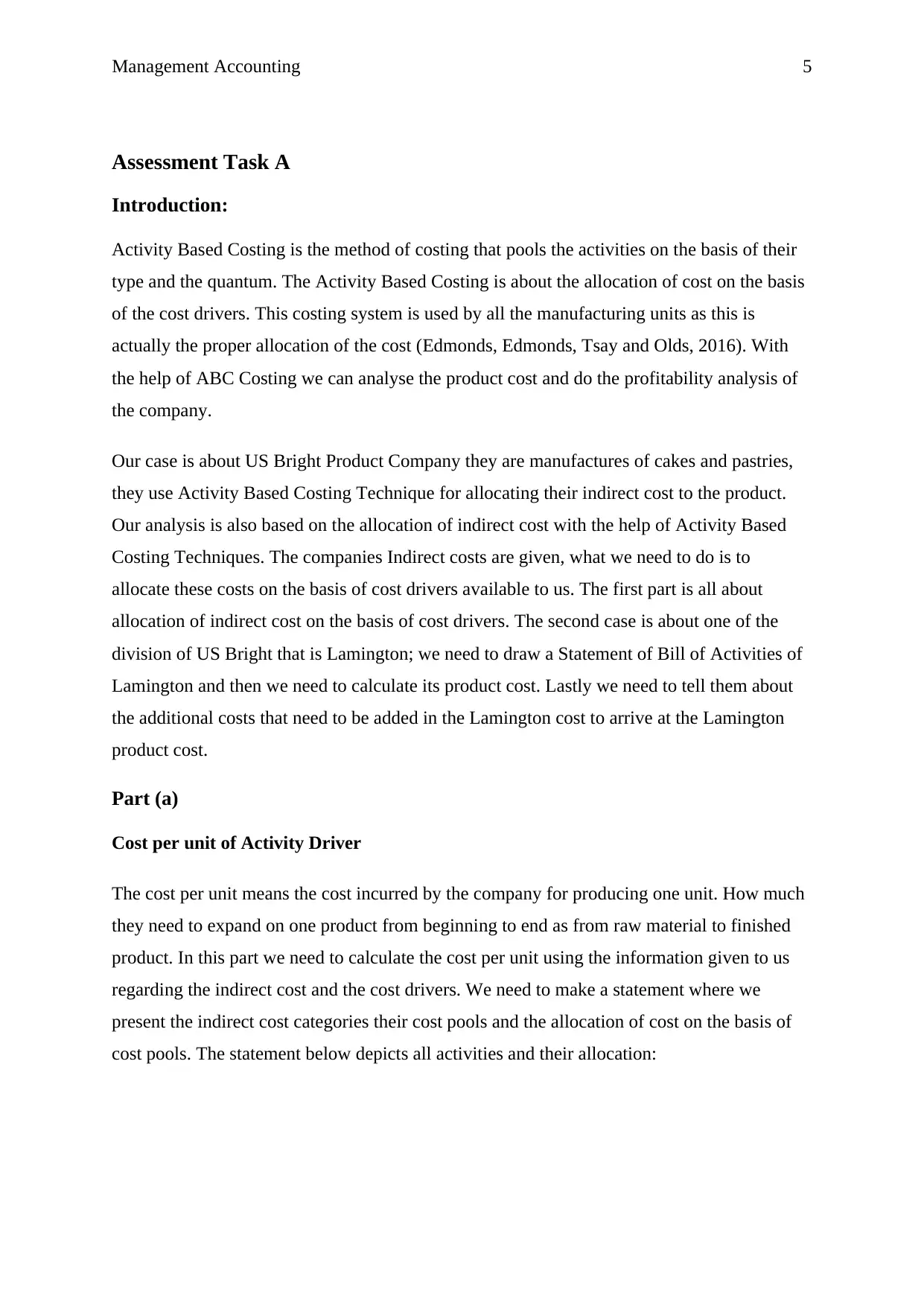

Part (a)

Cost per unit of Activity Driver

The cost per unit means the cost incurred by the company for producing one unit. How much

they need to expand on one product from beginning to end as from raw material to finished

product. In this part we need to calculate the cost per unit using the information given to us

regarding the indirect cost and the cost drivers. We need to make a statement where we

present the indirect cost categories their cost pools and the allocation of cost on the basis of

cost pools. The statement below depicts all activities and their allocation:

Assessment Task A

Introduction:

Activity Based Costing is the method of costing that pools the activities on the basis of their

type and the quantum. The Activity Based Costing is about the allocation of cost on the basis

of the cost drivers. This costing system is used by all the manufacturing units as this is

actually the proper allocation of the cost (Edmonds, Edmonds, Tsay and Olds, 2016). With

the help of ABC Costing we can analyse the product cost and do the profitability analysis of

the company.

Our case is about US Bright Product Company they are manufactures of cakes and pastries,

they use Activity Based Costing Technique for allocating their indirect cost to the product.

Our analysis is also based on the allocation of indirect cost with the help of Activity Based

Costing Techniques. The companies Indirect costs are given, what we need to do is to

allocate these costs on the basis of cost drivers available to us. The first part is all about

allocation of indirect cost on the basis of cost drivers. The second case is about one of the

division of US Bright that is Lamington; we need to draw a Statement of Bill of Activities of

Lamington and then we need to calculate its product cost. Lastly we need to tell them about

the additional costs that need to be added in the Lamington cost to arrive at the Lamington

product cost.

Part (a)

Cost per unit of Activity Driver

The cost per unit means the cost incurred by the company for producing one unit. How much

they need to expand on one product from beginning to end as from raw material to finished

product. In this part we need to calculate the cost per unit using the information given to us

regarding the indirect cost and the cost drivers. We need to make a statement where we

present the indirect cost categories their cost pools and the allocation of cost on the basis of

cost pools. The statement below depicts all activities and their allocation:

Management Accounting 6

Statement of Cost per unit (of activities listed)

Activity Activity Cost ($)

Annual Quantity of

activity Driver Rate per unit ($)

Prepare annual Accounts 5,000.00 None -

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00 None -

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 200000 0.02

Statement of Cost per unit (of activities listed)

Activity Activity Cost ($)

Annual Quantity of

activity Driver Rate per unit ($)

Prepare annual Accounts 5,000.00 None -

Process Receivables 15,000.00 5000 3.00

Process payables 25,000.00 2500 10.00

Program production 28,000.00 1000 28.00

Process Sales Order 40,000.00 4000 10.00

Dispatch sales Order 30,000.00 2500 12.00

Develop and test products 60,000.00 None -

Load Mixers 14,050.00 1000 14.05

Operate Mixers 45,900.00 200000 0.23

Clean mixers 6,900.00 1000 6.90

Move mixture to filling 200000 0.02

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

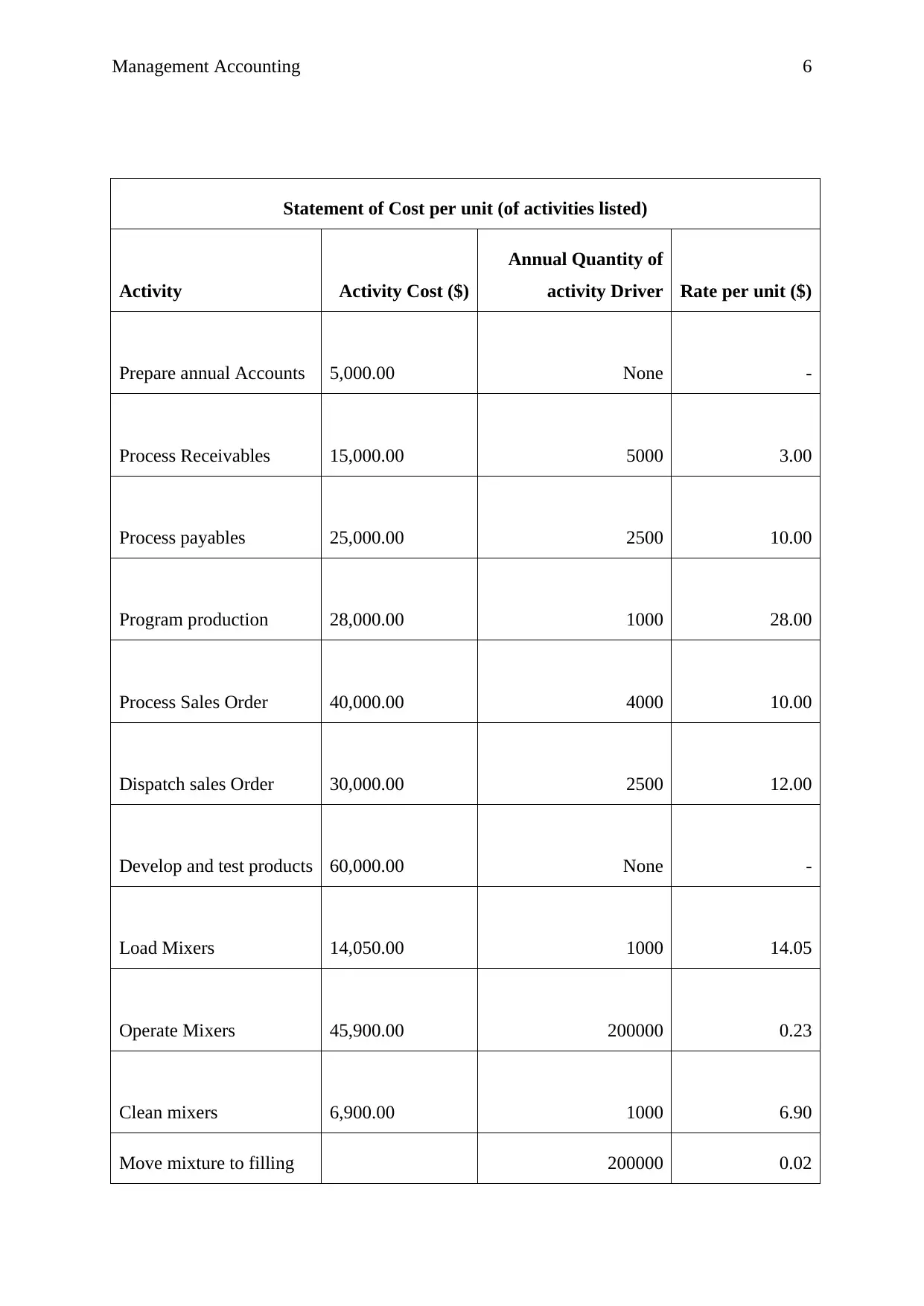

Management Accounting 7

3,450.00

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

This table is about the indirect costs their activity pools and the cost per unit of the product.

The cost per unit is $ 268.57 which we got by adding all the costs which we allocated on the

basis of cost pools.

Part (b)

Bill of Activities:

In this part we need to prepare a statement for the bill of activities of the Lamington. The

annual production volume of Lamington is 100000 and the batch size is 1000 batches. We

also need to calculate here the cost per unit which we calculate by dividing the total cost from

annual production volume.

3,450.00

Clean Trays 20,000.00 16000 1.25

Fill trays 16,000.00 800000 0.02

Move to Baking 8,000.00 16000 0.50

Set up ovens 50,000.00 1000 50.00

Bake Cakes/Pastries 1,30,000.00 1000 130.00

Move to packing 40,000.00 16000 2.50

Pack cakes/pastries 80,000.00 800000 0.10

Cost per unit 268.57

This table is about the indirect costs their activity pools and the cost per unit of the product.

The cost per unit is $ 268.57 which we got by adding all the costs which we allocated on the

basis of cost pools.

Part (b)

Bill of Activities:

In this part we need to prepare a statement for the bill of activities of the Lamington. The

annual production volume of Lamington is 100000 and the batch size is 1000 batches. We

also need to calculate here the cost per unit which we calculate by dividing the total cost from

annual production volume.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 8

Bill of Activities (Lamington)

Activity Consumed

Annual Quantity of

Activity Driver Cost per Unit ($) Total Cost ($)

Process Receivables 500 3.00 1,500.00

Process payables 200 10.00 2,000.00

Program production 100 28.00 2,800.00

Process Sales Order 400 10.00 4,000.00

Load Mixers 100 14.05 1,405.00

Operate Mixers 30000 0.23 6,885.00

Clean mixers 100 6.90 690.00

Move mixture to

filling 30000 0.02 517.50

Clean Trays 2000 1.25 2,500.00

Fill trays 100000 0.02 2,000.00

Move to Baking 2000 0.50 1,000.00

Set up ovens 100 5,000.00

Bill of Activities (Lamington)

Activity Consumed

Annual Quantity of

Activity Driver Cost per Unit ($) Total Cost ($)

Process Receivables 500 3.00 1,500.00

Process payables 200 10.00 2,000.00

Program production 100 28.00 2,800.00

Process Sales Order 400 10.00 4,000.00

Load Mixers 100 14.05 1,405.00

Operate Mixers 30000 0.23 6,885.00

Clean mixers 100 6.90 690.00

Move mixture to

filling 30000 0.02 517.50

Clean Trays 2000 1.25 2,500.00

Fill trays 100000 0.02 2,000.00

Move to Baking 2000 0.50 1,000.00

Set up ovens 100 5,000.00

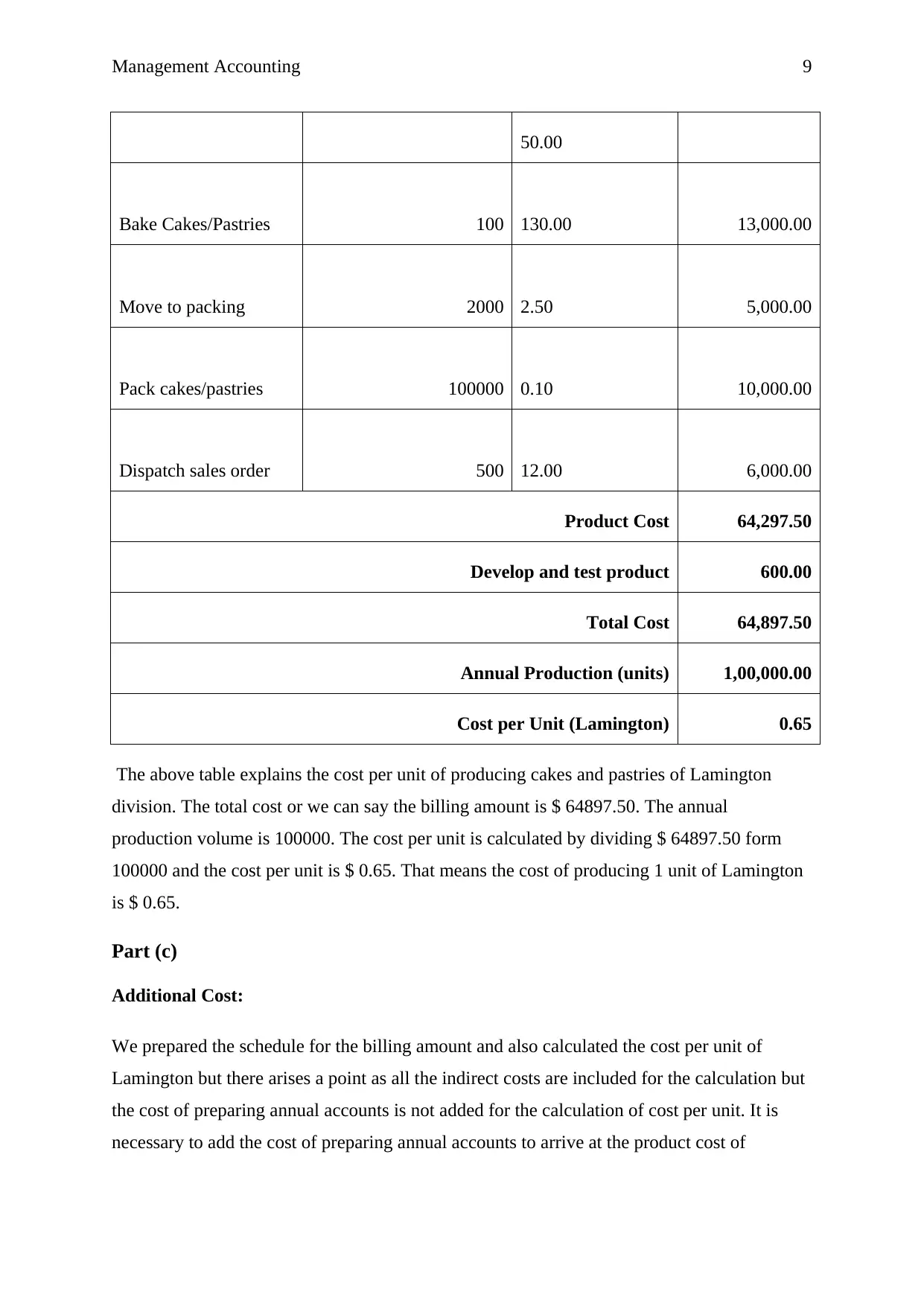

Management Accounting 9

50.00

Bake Cakes/Pastries 100 130.00 13,000.00

Move to packing 2000 2.50 5,000.00

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Product Cost 64,297.50

Develop and test product 600.00

Total Cost 64,897.50

Annual Production (units) 1,00,000.00

Cost per Unit (Lamington) 0.65

The above table explains the cost per unit of producing cakes and pastries of Lamington

division. The total cost or we can say the billing amount is $ 64897.50. The annual

production volume is 100000. The cost per unit is calculated by dividing $ 64897.50 form

100000 and the cost per unit is $ 0.65. That means the cost of producing 1 unit of Lamington

is $ 0.65.

Part (c)

Additional Cost:

We prepared the schedule for the billing amount and also calculated the cost per unit of

Lamington but there arises a point as all the indirect costs are included for the calculation but

the cost of preparing annual accounts is not added for the calculation of cost per unit. It is

necessary to add the cost of preparing annual accounts to arrive at the product cost of

50.00

Bake Cakes/Pastries 100 130.00 13,000.00

Move to packing 2000 2.50 5,000.00

Pack cakes/pastries 100000 0.10 10,000.00

Dispatch sales order 500 12.00 6,000.00

Product Cost 64,297.50

Develop and test product 600.00

Total Cost 64,897.50

Annual Production (units) 1,00,000.00

Cost per Unit (Lamington) 0.65

The above table explains the cost per unit of producing cakes and pastries of Lamington

division. The total cost or we can say the billing amount is $ 64897.50. The annual

production volume is 100000. The cost per unit is calculated by dividing $ 64897.50 form

100000 and the cost per unit is $ 0.65. That means the cost of producing 1 unit of Lamington

is $ 0.65.

Part (c)

Additional Cost:

We prepared the schedule for the billing amount and also calculated the cost per unit of

Lamington but there arises a point as all the indirect costs are included for the calculation but

the cost of preparing annual accounts is not added for the calculation of cost per unit. It is

necessary to add the cost of preparing annual accounts to arrive at the product cost of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management Accounting 10

Lamington. The cost of preparing annual accounts is not a product attributable cost so that is

why we need to add this cost to the total of indirect cost.

Conclusion:

The above analysis is all about the costing techniques used by US Bright for producing cakes

and pastries we did used activity based costing to perform a detailed analysis for the

allocation of the indirect cost of US Bright Product Company. The cost per unit of

manufacturing cakes and pastries is $ 268.6 we calculated this cost by adding all the cost. The

indirect costs are allocated on the basis of cost per unit and then they all are added together to

arrive at the unit cost of producing. Lamington is a division of US Bright and we did prepared

a bill of activities of US Bright and the total billing amount is $ 64897.50. We did also

calculated per unit cost for Lamington and the unit cost is $ 0.65. The additional cost which

can be added in the company’s cost to arrive at the total cost by the company is the cost of

preparing annual accounts although this cost is not product attributable but still we cannot

consider it as irrelevant cost. We cannot avoid the cost of preparing annual accounts it is

relevant for decision making. The complete analysis is all about the cost structure of US

Bright and Lamington and about per unit cost of producing cakes and pastries.

Lamington. The cost of preparing annual accounts is not a product attributable cost so that is

why we need to add this cost to the total of indirect cost.

Conclusion:

The above analysis is all about the costing techniques used by US Bright for producing cakes

and pastries we did used activity based costing to perform a detailed analysis for the

allocation of the indirect cost of US Bright Product Company. The cost per unit of

manufacturing cakes and pastries is $ 268.6 we calculated this cost by adding all the cost. The

indirect costs are allocated on the basis of cost per unit and then they all are added together to

arrive at the unit cost of producing. Lamington is a division of US Bright and we did prepared

a bill of activities of US Bright and the total billing amount is $ 64897.50. We did also

calculated per unit cost for Lamington and the unit cost is $ 0.65. The additional cost which

can be added in the company’s cost to arrive at the total cost by the company is the cost of

preparing annual accounts although this cost is not product attributable but still we cannot

consider it as irrelevant cost. We cannot avoid the cost of preparing annual accounts it is

relevant for decision making. The complete analysis is all about the cost structure of US

Bright and Lamington and about per unit cost of producing cakes and pastries.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting 11

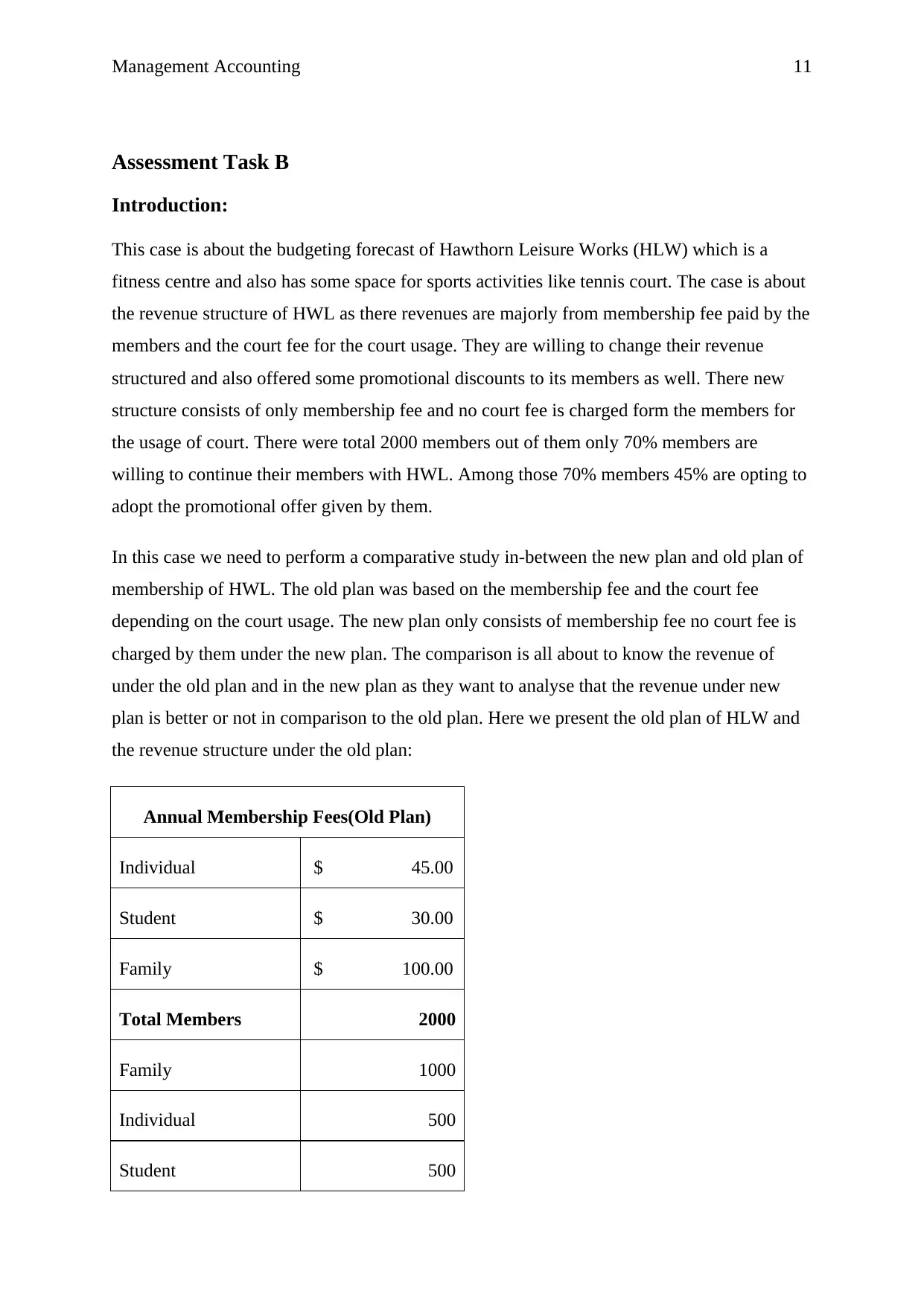

Assessment Task B

Introduction:

This case is about the budgeting forecast of Hawthorn Leisure Works (HLW) which is a

fitness centre and also has some space for sports activities like tennis court. The case is about

the revenue structure of HWL as there revenues are majorly from membership fee paid by the

members and the court fee for the court usage. They are willing to change their revenue

structured and also offered some promotional discounts to its members as well. There new

structure consists of only membership fee and no court fee is charged form the members for

the usage of court. There were total 2000 members out of them only 70% members are

willing to continue their members with HWL. Among those 70% members 45% are opting to

adopt the promotional offer given by them.

In this case we need to perform a comparative study in-between the new plan and old plan of

membership of HWL. The old plan was based on the membership fee and the court fee

depending on the court usage. The new plan only consists of membership fee no court fee is

charged by them under the new plan. The comparison is all about to know the revenue of

under the old plan and in the new plan as they want to analyse that the revenue under new

plan is better or not in comparison to the old plan. Here we present the old plan of HLW and

the revenue structure under the old plan:

Annual Membership Fees(Old Plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

Assessment Task B

Introduction:

This case is about the budgeting forecast of Hawthorn Leisure Works (HLW) which is a

fitness centre and also has some space for sports activities like tennis court. The case is about

the revenue structure of HWL as there revenues are majorly from membership fee paid by the

members and the court fee for the court usage. They are willing to change their revenue

structured and also offered some promotional discounts to its members as well. There new

structure consists of only membership fee and no court fee is charged form the members for

the usage of court. There were total 2000 members out of them only 70% members are

willing to continue their members with HWL. Among those 70% members 45% are opting to

adopt the promotional offer given by them.

In this case we need to perform a comparative study in-between the new plan and old plan of

membership of HWL. The old plan was based on the membership fee and the court fee

depending on the court usage. The new plan only consists of membership fee no court fee is

charged by them under the new plan. The comparison is all about to know the revenue of

under the old plan and in the new plan as they want to analyse that the revenue under new

plan is better or not in comparison to the old plan. Here we present the old plan of HLW and

the revenue structure under the old plan:

Annual Membership Fees(Old Plan)

Individual $ 45.00

Student $ 30.00

Family $ 100.00

Total Members 2000

Family 1000

Individual 500

Student 500

Management Accounting 12

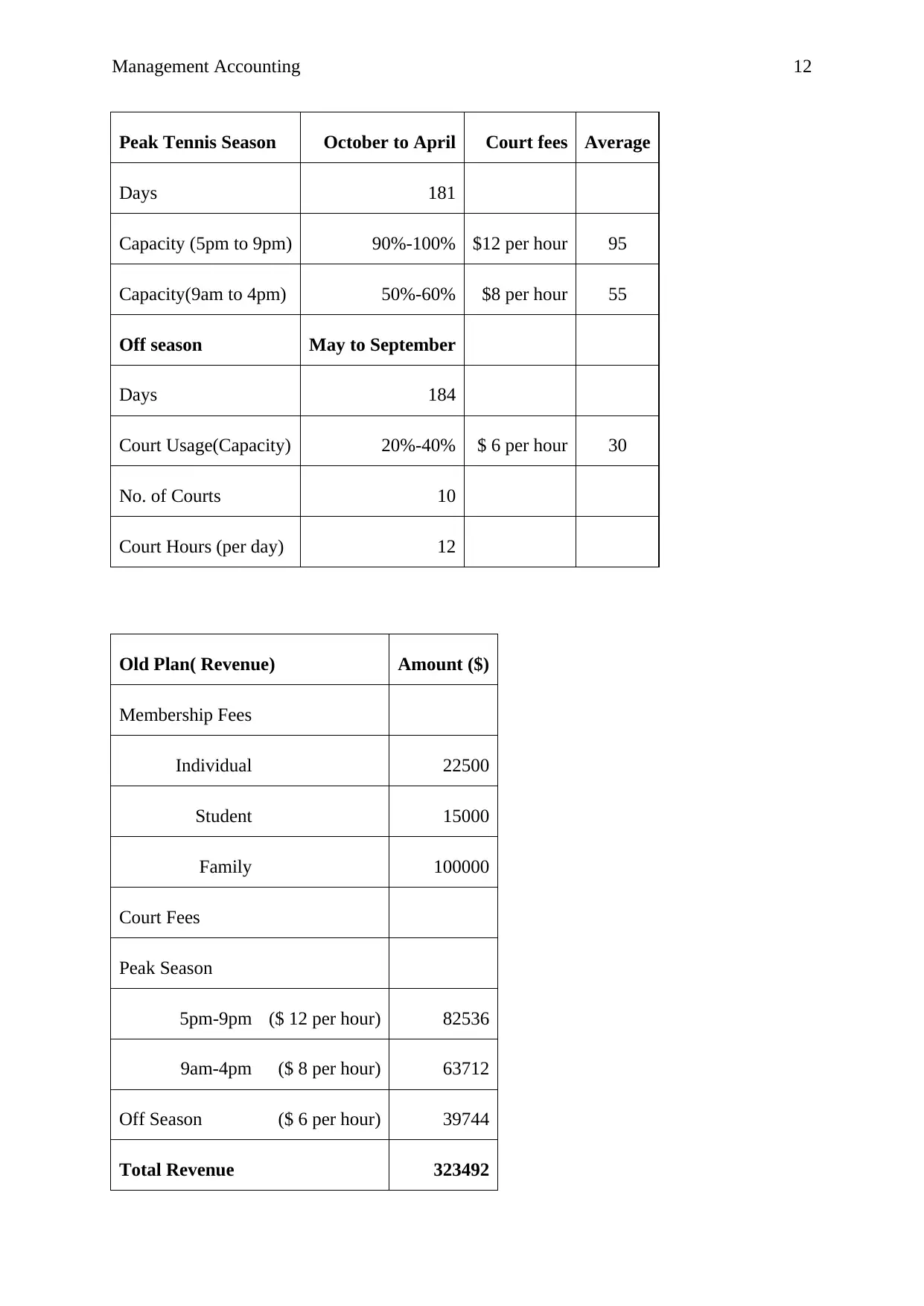

Peak Tennis Season October to April Court fees Average

Days 181

Capacity (5pm to 9pm) 90%-100% $12 per hour 95

Capacity(9am to 4pm) 50%-60% $8 per hour 55

Off season May to September

Days 184

Court Usage(Capacity) 20%-40% $ 6 per hour 30

No. of Courts 10

Court Hours (per day) 12

Old Plan( Revenue) Amount ($)

Membership Fees

Individual 22500

Student 15000

Family 100000

Court Fees

Peak Season

5pm-9pm ($ 12 per hour) 82536

9am-4pm ($ 8 per hour) 63712

Off Season ($ 6 per hour) 39744

Total Revenue 323492

Peak Tennis Season October to April Court fees Average

Days 181

Capacity (5pm to 9pm) 90%-100% $12 per hour 95

Capacity(9am to 4pm) 50%-60% $8 per hour 55

Off season May to September

Days 184

Court Usage(Capacity) 20%-40% $ 6 per hour 30

No. of Courts 10

Court Hours (per day) 12

Old Plan( Revenue) Amount ($)

Membership Fees

Individual 22500

Student 15000

Family 100000

Court Fees

Peak Season

5pm-9pm ($ 12 per hour) 82536

9am-4pm ($ 8 per hour) 63712

Off Season ($ 6 per hour) 39744

Total Revenue 323492

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.