Management Accounting Report: Scope, Cost Analysis, and Reports

VerifiedAdded on 2023/01/19

|13

|3130

|97

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA), detailing its definition and the crucial role of the management accountant within an enterprise. It explores the scope of MA, illustrating its significance across various business functions, including planning, organizing, controlling, and decision-making. The report contrasts MA with financial accounting, highlighting key differences in their objectives, information provided, and reporting formats. It then examines different types of cost reports, such as job costing, batch costing, and inventory costing, outlining their benefits and applications. Additionally, it covers activity-based costing and its advantages. The report concludes with an analysis of break-even analysis and profit evaluation within a firm, providing a complete understanding of MA principles and practices.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Defining management accounting and discussing role of the management accountant in an

enterprise ....................................................................................................................................1

Question 2........................................................................................................................................2

Demonstrating scope of MA and its role in each function of business.......................................2

Question 3........................................................................................................................................3

Explaining the difference between MA and financial accounting..............................................3

Question 4........................................................................................................................................5

Examining different kinds of cost reports with their benefits ....................................................5

Question 5........................................................................................................................................7

Question 6........................................................................................................................................8

Question 7........................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Defining management accounting and discussing role of the management accountant in an

enterprise ....................................................................................................................................1

Question 2........................................................................................................................................2

Demonstrating scope of MA and its role in each function of business.......................................2

Question 3........................................................................................................................................3

Explaining the difference between MA and financial accounting..............................................3

Question 4........................................................................................................................................5

Examining different kinds of cost reports with their benefits ....................................................5

Question 5........................................................................................................................................7

Question 6........................................................................................................................................8

Question 7........................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting means providing statistical and the financial information timely

to the business managers in order to make the routine and the short term decisions. In other words

it means application of the professions knowledge tools in respect of preparing accounting

information in a manner that enables the management in formulating the plans and the policies,

decision making, controlling operations, optimum use of the resources etc. The present report is

based on different aspects of MA that throws a deeper insights towards the role of management

accountant and importance of MA in respect of each managerial function. Furthermore, the study

reflects contrast between MA and FA along with several cost reports with their evaluation.

Moreover, the study also highlights break even analysis and evaluation of profit within the firm.

Question 1

Defining management accounting and discussing role of the management accountant in an

enterprise

MA is the main branch of accounting that relates with presenting and facilitating an

accounting information to management in systematic manner so that they could be able to perform

their management functions that are planning, decision making and controlling in effective and

efficient manner (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015). It is the process of

determining, measuring, analysing, accumulating and communicating the financial information in

order to plan, control and evaluate business operations in an enterprise and also ensures

appropriate use for the company's resources.

Role of management accountant

Stewardship accounting- Management accountant plays a crucial role in designing a

framework of the financial accounts and the cost for making routine operational and the financial

decision making.

Long and short term planning- They plays a significant role in forecasting the future

economic and the business events for the purpose of making the future plans that includes long

range plans, market study etc.

Developing MIS- Routine reports and the reports for a long period are been forwarded to

the managerial personnel at different levels for taking appropriate actions at right time.

1

Management accounting means providing statistical and the financial information timely

to the business managers in order to make the routine and the short term decisions. In other words

it means application of the professions knowledge tools in respect of preparing accounting

information in a manner that enables the management in formulating the plans and the policies,

decision making, controlling operations, optimum use of the resources etc. The present report is

based on different aspects of MA that throws a deeper insights towards the role of management

accountant and importance of MA in respect of each managerial function. Furthermore, the study

reflects contrast between MA and FA along with several cost reports with their evaluation.

Moreover, the study also highlights break even analysis and evaluation of profit within the firm.

Question 1

Defining management accounting and discussing role of the management accountant in an

enterprise

MA is the main branch of accounting that relates with presenting and facilitating an

accounting information to management in systematic manner so that they could be able to perform

their management functions that are planning, decision making and controlling in effective and

efficient manner (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil, 2015). It is the process of

determining, measuring, analysing, accumulating and communicating the financial information in

order to plan, control and evaluate business operations in an enterprise and also ensures

appropriate use for the company's resources.

Role of management accountant

Stewardship accounting- Management accountant plays a crucial role in designing a

framework of the financial accounts and the cost for making routine operational and the financial

decision making.

Long and short term planning- They plays a significant role in forecasting the future

economic and the business events for the purpose of making the future plans that includes long

range plans, market study etc.

Developing MIS- Routine reports and the reports for a long period are been forwarded to

the managerial personnel at different levels for taking appropriate actions at right time.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Maintaining an optimum structure of capital- He plays a major role in acquiring funds for

deciding in maintaining proper mix of the debt and the equity. Fund raising is counted as the risky

task because burden of interest is associated to it irrespective of the profits gained (Coad, Jack

and Kholeif, 2015). Therefore, management accountant are accountable in maintaining the capital

structure optimally and in giving due consideration to several COC theories, leverage etc.

Control- MA analyses the accounts and frames the report like budget, standard cost, cash

flow, variance analysis, performance evaluation etc. for ensuring proper controlling.

Decision making- It is main role that is played by management accountant where he

facilitates essential information to the management in making short run decisions. For instance-

product pricing, buying, discontinuing the process etc. and also decisions for long term such as

project financing, capital budgeting etc.

Question 2

Demonstrating scope of MA and its role in each function of business

The scope relating to the role of MA is much wider as in includes all the information that

is provided to management for making the suitable financial analysis and interpreting the business

transactions (Englund and Gerdin, 2018). It makes use of the financial data in finding out the cost

of several jobs, processes and the product. MA plays a critical role in every managerial functions

within the organization that are as follows-

Planning- MA is been closely interwoven in the planning for long as well as short term

goals as it facilitates information for making decision and accounting reports prepared under it act

as base for the entire process of budgeting (Joshi and Li, 2016). MA helps the managers making a

plan by providing the reports that states the effect of the estimate for alternative actions on ability

of the enterprise in achieving the desired goals.

Organising- It is the process of developing a framework and in assigning responsibility to

the people function in an enterprise for attaining the goals. MA enables the managers in

2

deciding in maintaining proper mix of the debt and the equity. Fund raising is counted as the risky

task because burden of interest is associated to it irrespective of the profits gained (Coad, Jack

and Kholeif, 2015). Therefore, management accountant are accountable in maintaining the capital

structure optimally and in giving due consideration to several COC theories, leverage etc.

Control- MA analyses the accounts and frames the report like budget, standard cost, cash

flow, variance analysis, performance evaluation etc. for ensuring proper controlling.

Decision making- It is main role that is played by management accountant where he

facilitates essential information to the management in making short run decisions. For instance-

product pricing, buying, discontinuing the process etc. and also decisions for long term such as

project financing, capital budgeting etc.

Question 2

Demonstrating scope of MA and its role in each function of business

The scope relating to the role of MA is much wider as in includes all the information that

is provided to management for making the suitable financial analysis and interpreting the business

transactions (Englund and Gerdin, 2018). It makes use of the financial data in finding out the cost

of several jobs, processes and the product. MA plays a critical role in every managerial functions

within the organization that are as follows-

Planning- MA is been closely interwoven in the planning for long as well as short term

goals as it facilitates information for making decision and accounting reports prepared under it act

as base for the entire process of budgeting (Joshi and Li, 2016). MA helps the managers making a

plan by providing the reports that states the effect of the estimate for alternative actions on ability

of the enterprise in achieving the desired goals.

Organising- It is the process of developing a framework and in assigning responsibility to

the people function in an enterprise for attaining the goals. MA enables the managers in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organising the business activities by providing the necessary information and in providing the

reports for regulating the activities and the operations in context of the changing circumstances.

Controlling- It the practice of measuring, monitoring, correcting the actual results in

ensuring that the goals of the business enterprise are been achieved. MA plays a crucial role in

controlling function by producing the performance and the control reports that highlights the

variances present in between the actual and the expected performances (Alsharari, Dixon and

Youssef, 2015). Such kind of the reports acts a base in taking the corrective action for controlling

the operations. Usage of control and the performance reports follows principle of the management

by exception. At times of the significant differences in between the actual and the budgeted

results, managers usually investigate in determining wrong and right where the subordinates or the

units may require help.

Decision making- It means a process of selecting among the competing alternatives. It is

considered as inherent within each of the 3 management functions named as planning, controlling,

organising etc. Manager could not plan without making appropriate decisions and needs to choose

among the competing techniques and the methods in carrying out the chosen goals. Similar to it,

managers requires to decide for a structure of an organization and on the particular actions that are

to be taken on routine operations (Carlsson-Wall, Kraus and Lind, 2015). In controlling,

managers has to decide that whether the variances are counted as worth investigating.

Question 3

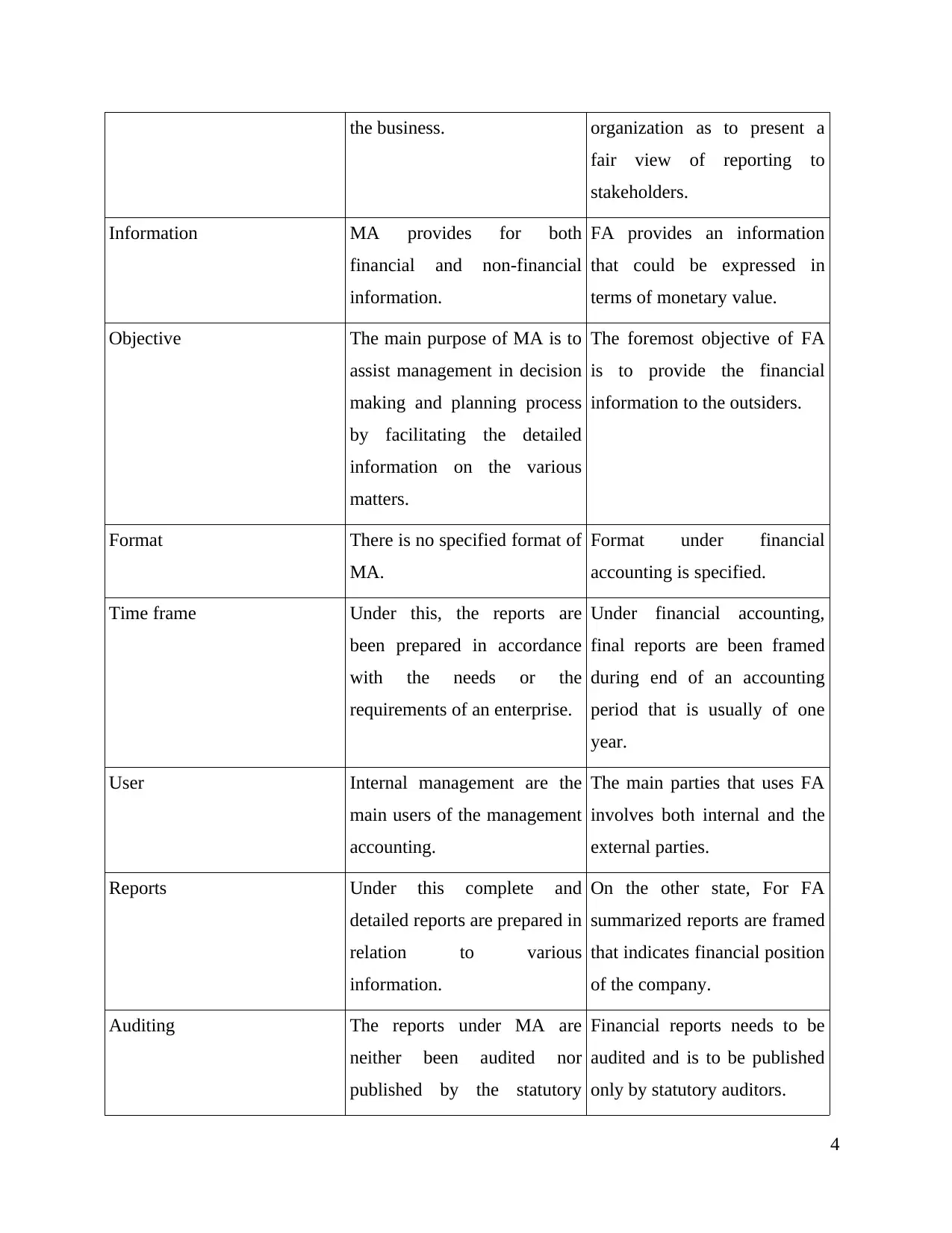

Explaining the difference between MA and financial accounting

Basis Management accounting Financial accounting

Meaning It is the system that provides

for relevant information to the

managers in making policies,

strategies, plans for the

purpose of running a business

efficiently and effectively.

It refers to accounting system

that emphasize on preparation

of the final reports of an

enterprise in providing the

financial information to the

interested users.

Compulsion It is not necessary for every

company to follow MA within

Financial accounting is

compulsory for each and every

3

reports for regulating the activities and the operations in context of the changing circumstances.

Controlling- It the practice of measuring, monitoring, correcting the actual results in

ensuring that the goals of the business enterprise are been achieved. MA plays a crucial role in

controlling function by producing the performance and the control reports that highlights the

variances present in between the actual and the expected performances (Alsharari, Dixon and

Youssef, 2015). Such kind of the reports acts a base in taking the corrective action for controlling

the operations. Usage of control and the performance reports follows principle of the management

by exception. At times of the significant differences in between the actual and the budgeted

results, managers usually investigate in determining wrong and right where the subordinates or the

units may require help.

Decision making- It means a process of selecting among the competing alternatives. It is

considered as inherent within each of the 3 management functions named as planning, controlling,

organising etc. Manager could not plan without making appropriate decisions and needs to choose

among the competing techniques and the methods in carrying out the chosen goals. Similar to it,

managers requires to decide for a structure of an organization and on the particular actions that are

to be taken on routine operations (Carlsson-Wall, Kraus and Lind, 2015). In controlling,

managers has to decide that whether the variances are counted as worth investigating.

Question 3

Explaining the difference between MA and financial accounting

Basis Management accounting Financial accounting

Meaning It is the system that provides

for relevant information to the

managers in making policies,

strategies, plans for the

purpose of running a business

efficiently and effectively.

It refers to accounting system

that emphasize on preparation

of the final reports of an

enterprise in providing the

financial information to the

interested users.

Compulsion It is not necessary for every

company to follow MA within

Financial accounting is

compulsory for each and every

3

the business. organization as to present a

fair view of reporting to

stakeholders.

Information MA provides for both

financial and non-financial

information.

FA provides an information

that could be expressed in

terms of monetary value.

Objective The main purpose of MA is to

assist management in decision

making and planning process

by facilitating the detailed

information on the various

matters.

The foremost objective of FA

is to provide the financial

information to the outsiders.

Format There is no specified format of

MA.

Format under financial

accounting is specified.

Time frame Under this, the reports are

been prepared in accordance

with the needs or the

requirements of an enterprise.

Under financial accounting,

final reports are been framed

during end of an accounting

period that is usually of one

year.

User Internal management are the

main users of the management

accounting.

The main parties that uses FA

involves both internal and the

external parties.

Reports Under this complete and

detailed reports are prepared in

relation to various

information.

On the other state, For FA

summarized reports are framed

that indicates financial position

of the company.

Auditing The reports under MA are

neither been audited nor

published by the statutory

Financial reports needs to be

audited and is to be published

only by statutory auditors.

4

fair view of reporting to

stakeholders.

Information MA provides for both

financial and non-financial

information.

FA provides an information

that could be expressed in

terms of monetary value.

Objective The main purpose of MA is to

assist management in decision

making and planning process

by facilitating the detailed

information on the various

matters.

The foremost objective of FA

is to provide the financial

information to the outsiders.

Format There is no specified format of

MA.

Format under financial

accounting is specified.

Time frame Under this, the reports are

been prepared in accordance

with the needs or the

requirements of an enterprise.

Under financial accounting,

final reports are been framed

during end of an accounting

period that is usually of one

year.

User Internal management are the

main users of the management

accounting.

The main parties that uses FA

involves both internal and the

external parties.

Reports Under this complete and

detailed reports are prepared in

relation to various

information.

On the other state, For FA

summarized reports are framed

that indicates financial position

of the company.

Auditing The reports under MA are

neither been audited nor

published by the statutory

Financial reports needs to be

audited and is to be published

only by statutory auditors.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

auditors.

Question 4

Examining different kinds of cost reports with their benefits

Job costing- This system means practice of accumulating an information about a cost

attached with a particular service job or the production. This information might be needed for

submitting cost information to the customer under the contract where the costs are been

reimbursed (Makrygiannakis and Jack, 2016). The information gathered under this system is more

and more useful in determining accuracy in an estimating system of an enterprise which needs to

be quote prices that allows for the reasonable profit. This information could also be used in

assigning the inventoriable cost in manufacturing the goods.

Benefits of job costing are as follows-

This system helps in tracking material cost that are been used during a course of job. The

system could compile this direct material cost through manual tracing of the materials on

the costing sheets or information that could be charged by making use of the online

terminals within a warehouse and the area of production.

Job costing helps in tracking the labor cost relating to the services that compromise all the

job cost. It is been typically assigned towards a particular job with timecard on the

computer.

It is the system that assigns the cost of overhead towards one or more than one cost pools.

At end of every accounting period, total amount in every cost pool is been assigned

towards several jobs on the basis of some allocation that is been applied constantly.

Batch costing- It is considered as another type of the job costing as under this technique,

homogenous products are been taken as the unit cost. A particular batch is comprised of the

specific number of the products or the articles. This number changes from the one batch to another

(Andersén and Samuelsson, 2016). This report is been used for identifying per unit article.

Benefits of batch costing-

Under this costing, reduced accounting work is been seen as the costing is made in context

of the batch of a homogenous jobs.

5

Question 4

Examining different kinds of cost reports with their benefits

Job costing- This system means practice of accumulating an information about a cost

attached with a particular service job or the production. This information might be needed for

submitting cost information to the customer under the contract where the costs are been

reimbursed (Makrygiannakis and Jack, 2016). The information gathered under this system is more

and more useful in determining accuracy in an estimating system of an enterprise which needs to

be quote prices that allows for the reasonable profit. This information could also be used in

assigning the inventoriable cost in manufacturing the goods.

Benefits of job costing are as follows-

This system helps in tracking material cost that are been used during a course of job. The

system could compile this direct material cost through manual tracing of the materials on

the costing sheets or information that could be charged by making use of the online

terminals within a warehouse and the area of production.

Job costing helps in tracking the labor cost relating to the services that compromise all the

job cost. It is been typically assigned towards a particular job with timecard on the

computer.

It is the system that assigns the cost of overhead towards one or more than one cost pools.

At end of every accounting period, total amount in every cost pool is been assigned

towards several jobs on the basis of some allocation that is been applied constantly.

Batch costing- It is considered as another type of the job costing as under this technique,

homogenous products are been taken as the unit cost. A particular batch is comprised of the

specific number of the products or the articles. This number changes from the one batch to another

(Andersén and Samuelsson, 2016). This report is been used for identifying per unit article.

Benefits of batch costing-

Under this costing, reduced accounting work is been seen as the costing is made in context

of the batch of a homogenous jobs.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

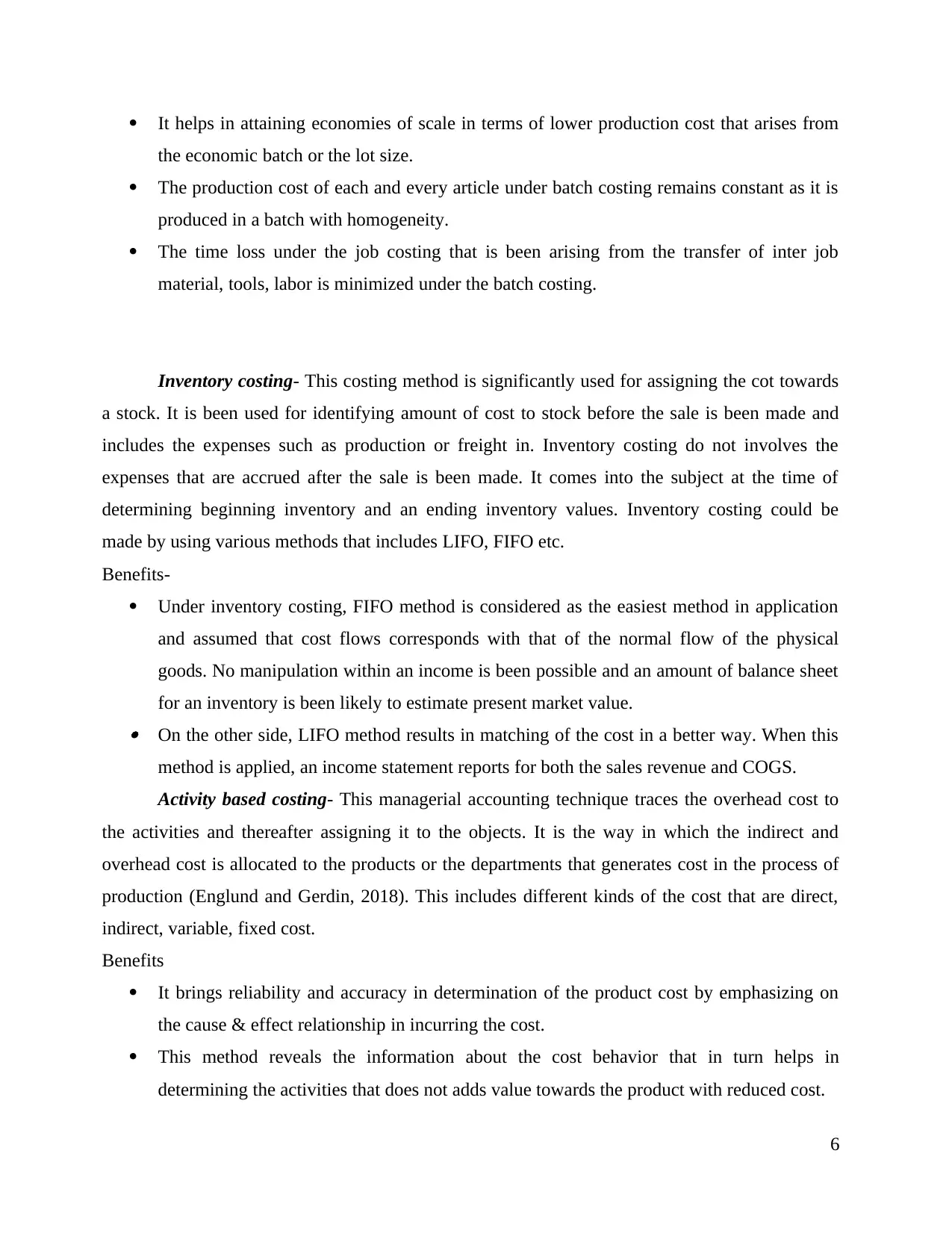

It helps in attaining economies of scale in terms of lower production cost that arises from

the economic batch or the lot size.

The production cost of each and every article under batch costing remains constant as it is

produced in a batch with homogeneity.

The time loss under the job costing that is been arising from the transfer of inter job

material, tools, labor is minimized under the batch costing.

Inventory costing- This costing method is significantly used for assigning the cot towards

a stock. It is been used for identifying amount of cost to stock before the sale is been made and

includes the expenses such as production or freight in. Inventory costing do not involves the

expenses that are accrued after the sale is been made. It comes into the subject at the time of

determining beginning inventory and an ending inventory values. Inventory costing could be

made by using various methods that includes LIFO, FIFO etc.

Benefits-

Under inventory costing, FIFO method is considered as the easiest method in application

and assumed that cost flows corresponds with that of the normal flow of the physical

goods. No manipulation within an income is been possible and an amount of balance sheet

for an inventory is been likely to estimate present market value. On the other side, LIFO method results in matching of the cost in a better way. When this

method is applied, an income statement reports for both the sales revenue and COGS.

Activity based costing- This managerial accounting technique traces the overhead cost to

the activities and thereafter assigning it to the objects. It is the way in which the indirect and

overhead cost is allocated to the products or the departments that generates cost in the process of

production (Englund and Gerdin, 2018). This includes different kinds of the cost that are direct,

indirect, variable, fixed cost.

Benefits

It brings reliability and accuracy in determination of the product cost by emphasizing on

the cause & effect relationship in incurring the cost.

This method reveals the information about the cost behavior that in turn helps in

determining the activities that does not adds value towards the product with reduced cost.

6

the economic batch or the lot size.

The production cost of each and every article under batch costing remains constant as it is

produced in a batch with homogeneity.

The time loss under the job costing that is been arising from the transfer of inter job

material, tools, labor is minimized under the batch costing.

Inventory costing- This costing method is significantly used for assigning the cot towards

a stock. It is been used for identifying amount of cost to stock before the sale is been made and

includes the expenses such as production or freight in. Inventory costing do not involves the

expenses that are accrued after the sale is been made. It comes into the subject at the time of

determining beginning inventory and an ending inventory values. Inventory costing could be

made by using various methods that includes LIFO, FIFO etc.

Benefits-

Under inventory costing, FIFO method is considered as the easiest method in application

and assumed that cost flows corresponds with that of the normal flow of the physical

goods. No manipulation within an income is been possible and an amount of balance sheet

for an inventory is been likely to estimate present market value. On the other side, LIFO method results in matching of the cost in a better way. When this

method is applied, an income statement reports for both the sales revenue and COGS.

Activity based costing- This managerial accounting technique traces the overhead cost to

the activities and thereafter assigning it to the objects. It is the way in which the indirect and

overhead cost is allocated to the products or the departments that generates cost in the process of

production (Englund and Gerdin, 2018). This includes different kinds of the cost that are direct,

indirect, variable, fixed cost.

Benefits

It brings reliability and accuracy in determination of the product cost by emphasizing on

the cause & effect relationship in incurring the cost.

This method reveals the information about the cost behavior that in turn helps in

determining the activities that does not adds value towards the product with reduced cost.

6

Under this, multiple cost drivers are used in which many of the drivers are transaction

based instead of the product volume. This helps in tracing more and more overhead cost

towards the product within and beyond a factory.

Question 5

Income statement as per absorption costing

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Cost of goods sold 80000

Gross or Net profit (120000-80000) 40000

Calculation of the cost per unit

Particulars Amount

Prime cost 4

Variable cost of production 2

Foxed cost of production 4

Total cost of production 10

Evaluation of COGS-

Particulars Amount Cost per unit Total Net amount

Opening stock 500 10 5000

Production 10000 10 100000

Closing stock 2500 10 25000

Cost of goods

sold= opening

stock +

purchases-

closing stock

80000

Income statement as per Marginal costing-

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Variable cost 48000

Contribution

(Operating revenue-

variable cost)

72000

Less: Fixed overhead

production cost

40000

Net profit 32000

7

based instead of the product volume. This helps in tracing more and more overhead cost

towards the product within and beyond a factory.

Question 5

Income statement as per absorption costing

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Cost of goods sold 80000

Gross or Net profit (120000-80000) 40000

Calculation of the cost per unit

Particulars Amount

Prime cost 4

Variable cost of production 2

Foxed cost of production 4

Total cost of production 10

Evaluation of COGS-

Particulars Amount Cost per unit Total Net amount

Opening stock 500 10 5000

Production 10000 10 100000

Closing stock 2500 10 25000

Cost of goods

sold= opening

stock +

purchases-

closing stock

80000

Income statement as per Marginal costing-

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Variable cost 48000

Contribution

(Operating revenue-

variable cost)

72000

Less: Fixed overhead

production cost

40000

Net profit 32000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

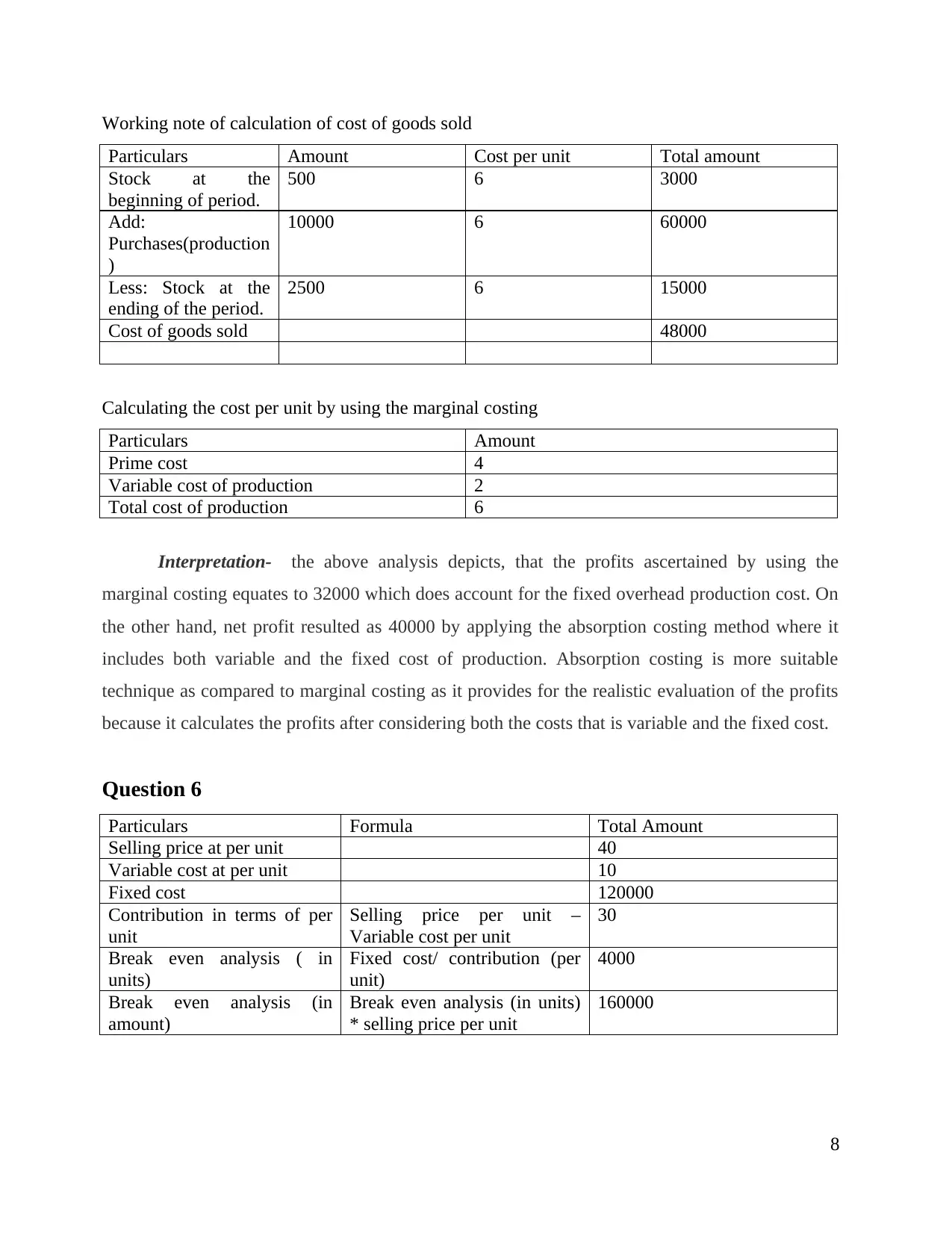

Working note of calculation of cost of goods sold

Particulars Amount Cost per unit Total amount

Stock at the

beginning of period.

500 6 3000

Add:

Purchases(production

)

10000 6 60000

Less: Stock at the

ending of the period.

2500 6 15000

Cost of goods sold 48000

Calculating the cost per unit by using the marginal costing

Particulars Amount

Prime cost 4

Variable cost of production 2

Total cost of production 6

Interpretation- the above analysis depicts, that the profits ascertained by using the

marginal costing equates to 32000 which does account for the fixed overhead production cost. On

the other hand, net profit resulted as 40000 by applying the absorption costing method where it

includes both variable and the fixed cost of production. Absorption costing is more suitable

technique as compared to marginal costing as it provides for the realistic evaluation of the profits

because it calculates the profits after considering both the costs that is variable and the fixed cost.

Question 6

Particulars Formula Total Amount

Selling price at per unit 40

Variable cost at per unit 10

Fixed cost 120000

Contribution in terms of per

unit

Selling price per unit –

Variable cost per unit

30

Break even analysis ( in

units)

Fixed cost/ contribution (per

unit)

4000

Break even analysis (in

amount)

Break even analysis (in units)

* selling price per unit

160000

8

Particulars Amount Cost per unit Total amount

Stock at the

beginning of period.

500 6 3000

Add:

Purchases(production

)

10000 6 60000

Less: Stock at the

ending of the period.

2500 6 15000

Cost of goods sold 48000

Calculating the cost per unit by using the marginal costing

Particulars Amount

Prime cost 4

Variable cost of production 2

Total cost of production 6

Interpretation- the above analysis depicts, that the profits ascertained by using the

marginal costing equates to 32000 which does account for the fixed overhead production cost. On

the other hand, net profit resulted as 40000 by applying the absorption costing method where it

includes both variable and the fixed cost of production. Absorption costing is more suitable

technique as compared to marginal costing as it provides for the realistic evaluation of the profits

because it calculates the profits after considering both the costs that is variable and the fixed cost.

Question 6

Particulars Formula Total Amount

Selling price at per unit 40

Variable cost at per unit 10

Fixed cost 120000

Contribution in terms of per

unit

Selling price per unit –

Variable cost per unit

30

Break even analysis ( in

units)

Fixed cost/ contribution (per

unit)

4000

Break even analysis (in

amount)

Break even analysis (in units)

* selling price per unit

160000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break even analysis is counted as the significant aspect of the effective business plan as it

helps in determining cost structures, no. of units that required to sold for covering the profit.

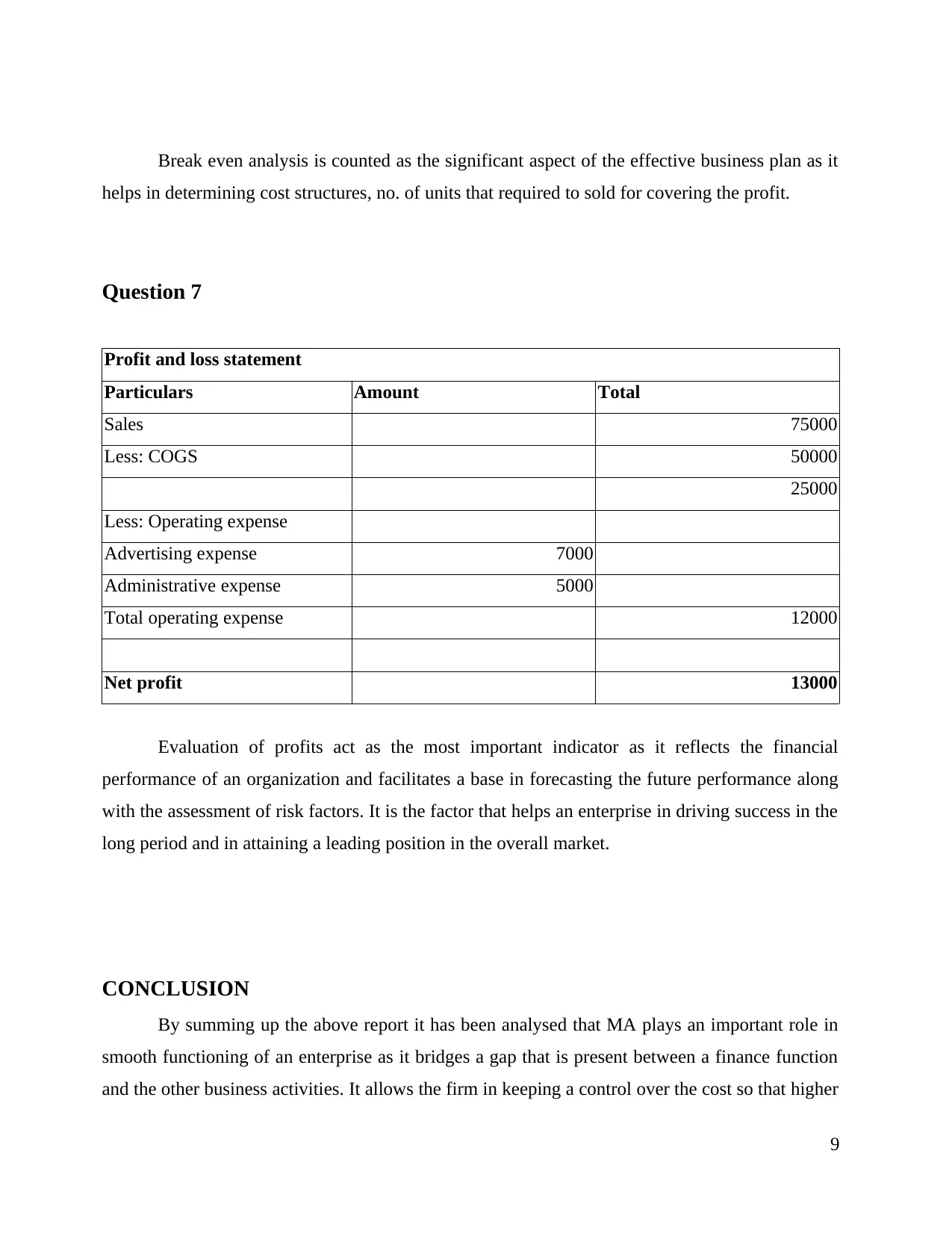

Question 7

Profit and loss statement

Particulars Amount Total

Sales 75000

Less: COGS 50000

25000

Less: Operating expense

Advertising expense 7000

Administrative expense 5000

Total operating expense 12000

Net profit 13000

Evaluation of profits act as the most important indicator as it reflects the financial

performance of an organization and facilitates a base in forecasting the future performance along

with the assessment of risk factors. It is the factor that helps an enterprise in driving success in the

long period and in attaining a leading position in the overall market.

CONCLUSION

By summing up the above report it has been analysed that MA plays an important role in

smooth functioning of an enterprise as it bridges a gap that is present between a finance function

and the other business activities. It allows the firm in keeping a control over the cost so that higher

9

helps in determining cost structures, no. of units that required to sold for covering the profit.

Question 7

Profit and loss statement

Particulars Amount Total

Sales 75000

Less: COGS 50000

25000

Less: Operating expense

Advertising expense 7000

Administrative expense 5000

Total operating expense 12000

Net profit 13000

Evaluation of profits act as the most important indicator as it reflects the financial

performance of an organization and facilitates a base in forecasting the future performance along

with the assessment of risk factors. It is the factor that helps an enterprise in driving success in the

long period and in attaining a leading position in the overall market.

CONCLUSION

By summing up the above report it has been analysed that MA plays an important role in

smooth functioning of an enterprise as it bridges a gap that is present between a finance function

and the other business activities. It allows the firm in keeping a control over the cost so that higher

9

profits could be gained which in turn leads to growing success of an enterprise in the long run.

Moreover, it has also been assessed that management accountant plays a significant role in

performing the major business activities in efficient manner.

10

Moreover, it has also been assessed that management accountant plays a significant role in

performing the major business activities in efficient manner.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.